Languages

Pages

Legal

International Tax Concepts for Cross-border

Employees

Cross-border Tax Issues Seminar

2

AGENDA

Basic Tax Concepts for Cross-border Employees

Tax Residency – U.S. vs. Canada

U.S. - Canada Tax Treaty considerations

Income Tax – reporting/withholding for employers

Social Security Tax

Retirement Plans

Common Cross-border Issues

4

Trowbridge Professional Corporation is a specialty tax firm, providing tax services for Canadians that live and work around the world

Offices in Toronto, Montreal, Vancouver and London,

Through our affiliation with the Global Tax Network we are able to provide global solutions to our clients.

Who We Are

5

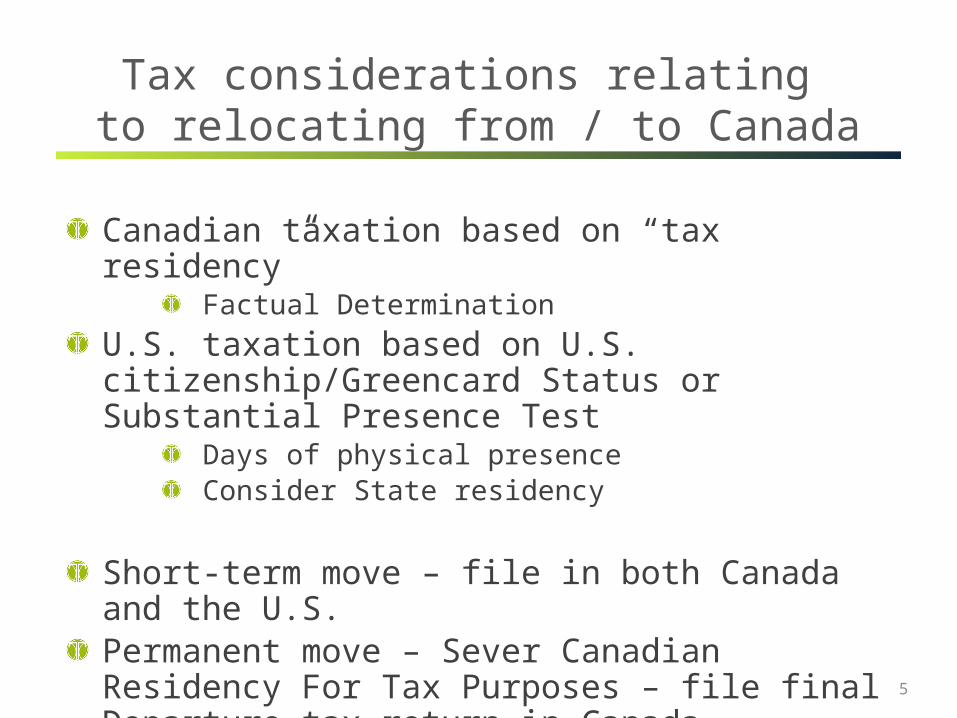

Tax considerations relating to relocating from / to Canada

Canadian taxation based on “tax residency” Factual Determination

U.S. taxation based on U.S. citizenship/Greencard Status or Substantial Presence Test

Days of physical presence Consider State residency

Short-term move – file in both Canada and the U.S. Permanent move – Sever Canadian Residency For Tax Purposes – file final Departure tax return in Canada

6

Canada Tax Residency - Common Primary and Secondary Ties

Primary: Vacant Home, leaving dependent spouse in Canada.

Secondary: personal property left behind in Canada, maintaining Canadian bank accounts, Canadian credit cards, professional and/or club memberships in Canadian organizations, maintaining provincial health coverage, Canadian drivers license.

7

U.S. Tax Residency

“Substantial Presence” test:

Were you present in the U.S. 31 days during the current year, and

183 days during the 3-year period that includes the current year and

the 2 years immediately before that, counting: All the days you were present in the current year, and 1/3 of the days you were present in the first year before the

current year, and 1/6 of the days you were present in the second year before

the current year.

8

U.S. – Canada Tax Treaty Issues

Purpose to avoid double taxation

Employment Income – exemption under Treaty– Less than $10,000– Spend less than 184 days in any 12 month period and your

remuneration is not paid by, or on behalf of, a person who is resident in the United States and is not borne by a permanent establishment in the United States

Residency “Tie-breaker” rules– permanent home – center of vital interests – personal and economic ties– habitual abode

9

Employer Reporting / Withholding

Employer Reporting / Withholding requirement even if exemption under Tax Treaty

Income Tax Withholding Waiver

Frequent Business Travelers

10

Social Security Taxes

US FICA and Medicare taxes vs. Canadian social security taxes (Canada Pension Plan and Employment Insurance)

U.S. Canada Totalization Agreement

11

RRSP’s/401(k)/IRA

RRSP’s Tax protected while in the US – you can also contribute in year of departure and any other year (may not be beneficial to do so) – file Form 8891

IRA’s/401(k) tax protected in Canada until disposition

May be best to leave IRA/401(K) as is until you need income in the future – not taxed in Canada or U.S. until disposed

12

Common Cross-border Issues

Sale of home – U.S. treatment vs. Canadian treatment

– Clearance Certificate / Withholding Taxes

Executive compensation / stock option plans

Foreign Disclosure Requirements

– Form T1135 / FBAR

Impact on Investments Tax treatment for dividends / capital gains

Foreign Disclosure Requirements

Estate planning / update will

13

Vancouver Office, Trowbridge 604.288.7700

Questions?

14

Legal

This presentation is for information purposes only and does not provide tax or

legal advice. Due to the complex tax rules for U.S. and Canada, it is imperative

that you obtain professional advice from a qualified tax or legal advisor

specializing in cross-border tax planning before you act on any of the

information provided.

Top Related