Languages

Pages

Legal

#CBALIVE | 1 1

Integrating Digital Experiences for Collections

Default Forum

#CBALIVE | 1

#CBALIVE | 2

Dave LaRoche

Bridgeforce

Brian Moore

Nuance

Default Forum

Presented by:

#CBALIVE | 3

Dave LaRoche

Bridgeforce

Dave is the Default Management and Auto Finance practice leader for

Bridgeforce. He has held senior executive positions focused on managing

collections operations, risk management strategies, technology platforms

including telephony and web buildouts, loss forecasting, and MIS reporting

for a wide range of consumer loan products including auto, credit cards,

and consumer finance. Prior to Bridgeforce, David worked with MBNA,

Wells Fargo, and American Express.

#CBALIVE | 4#CBALIVE | 4

Objectives

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

1

2

3

4

Understand the Consumer Landscape and Digital Space

Identify Where You Stand and What Others are Doing

Demonstrate How You Can Get Started

Nuance: Ready, Set, Collect (Digitally)

#CBALIVE | 5#CBALIVE | 5

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

Expectations Increase with Changing Consumer Climate

Face ID

SPEED CONVENIENCE SIMPLICITY

Companies are Striving to Deliver a Clear Value Proposition to their Customers

#CBALIVE | 6#CBALIVE | 6

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

The Consumer Lifecycle is Online More than Ever

Source: eMarketer 9/14 (2008-2010); eMarketer 4/15 (2011-2013); eMarketer 4/17 (2014-20176). Note: Other connected devices include OTT, and

game consoles. Mobile includes smartphone and tablet. Usage includes both home and work. Ages 18+; time spent with each medium includes

all time spent with that medium, regardless of multitasking.

Mobile

Desktop/Laptop

Other

Connected

Devices

Ho

urs

pe

r D

ay

Time Spent with Digital Media per Adult User/Day, US2008 - 2016

16 million

text messages

What Happens in an Internet Minute

@LoriLewis; @OfficiallyChadd

3.5million

search queries

$751,522spent online

342,000apps

downloaded

156 million

emails

sent

#CBALIVE | 7#CBALIVE | 7

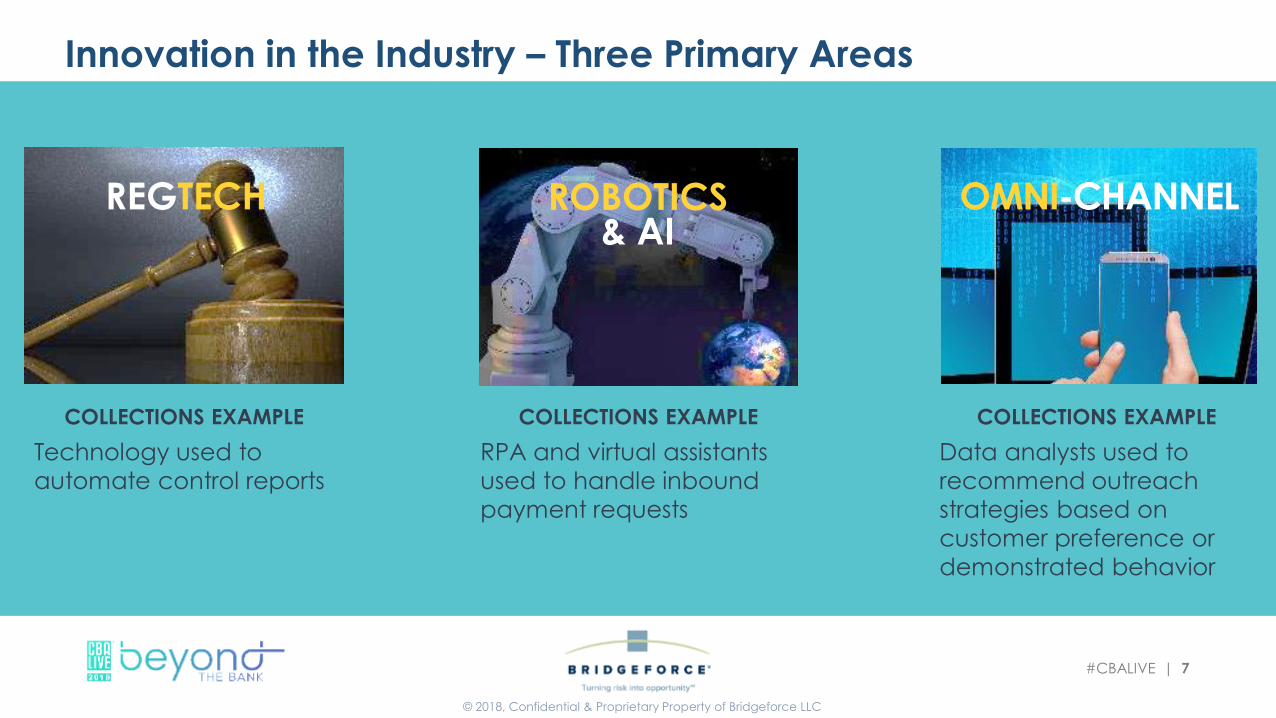

Innovation in the Industry – Three Primary Areas

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

COLLECTIONS EXAMPLE

Data analysts used to

recommend outreach

strategies based on

customer preference or

demonstrated behavior

COLLECTIONS EXAMPLE

RPA and virtual assistants

used to handle inbound

payment requests

COLLECTIONS EXAMPLE

Technology used to

automate control reports

OMNI-CHANNELROBOTICS& AI

REGTECH

#CBALIVE | 8#CBALIVE | 8

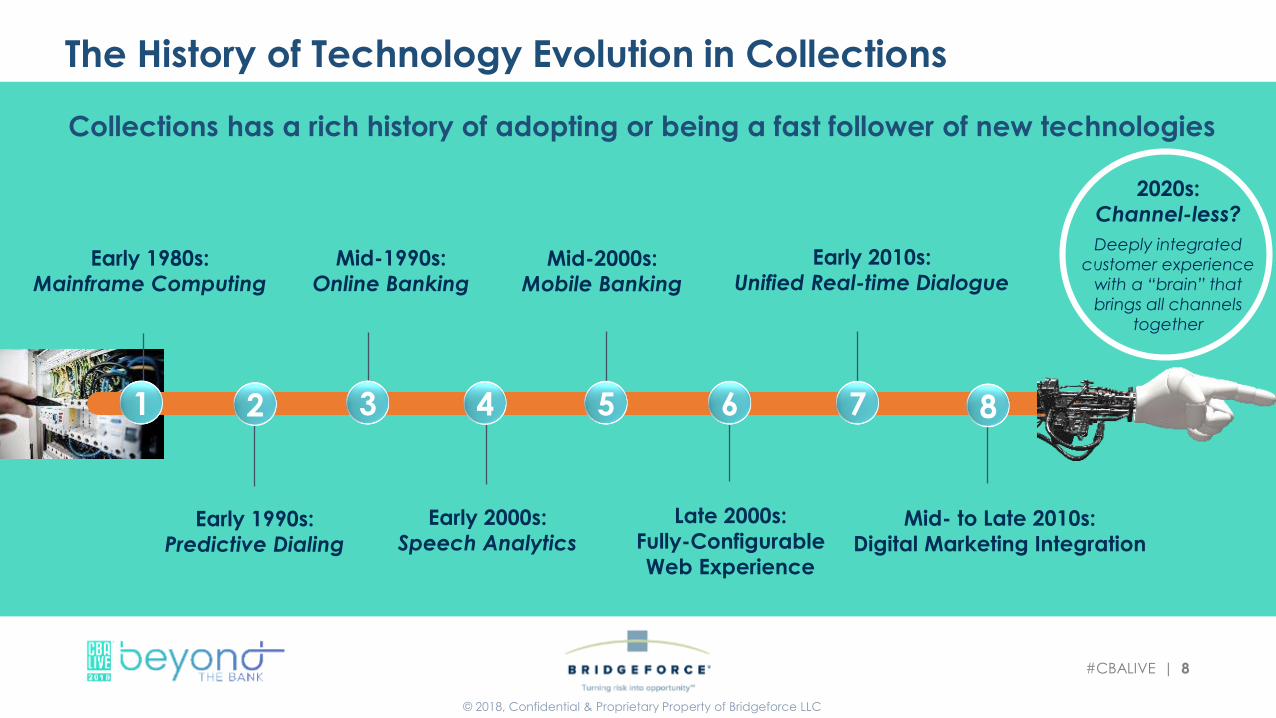

The History of Technology Evolution in Collections

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

Early 1980s:

Mainframe Computing

1

Early 1990s:

Predictive Dialing

2

Mid-1990s:

Online Banking

3

Early 2000s:

Speech Analytics

4

Mid-2000s:

Mobile Banking

5

Late 2000s:

Fully-Configurable

Web Experience

6

Early 2010s:

Unified Real-time Dialogue

7

2020s:

Channel-less?

Deeply integrated customer experience

with a “brain” that brings all channels

together

Collections has a rich history of adopting or being a fast follower of new technologies

Mid- to Late 2010s:

Digital Marketing Integration

8

#CBALIVE | 9#CBALIVE | 9

Why It’s Time to Get in The Game

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

America's debt is surging, and riskiest borrowers are struggling to pay it back.

Business Insider, November 2017

Cumulative Loan Originations by Key US Digital Lenders ($B)

Includes cumulative loan originations since inception for 13 digital lenders tracked by S&P Global Market Intelligence

Based on company-provided information, rating agency reports and S&P Global Market Intelligence estimates. For

details, see methodology section at the end of the report.

SME = Small and Medium enterprise © 2017. S&P Global Market Intelligence. All rights reserved.

$2.64 Tn

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

3,800

3,600

3,400

3,200

3,000

2,800

2,600

2,400

2,200

Total Consumer Credit

+45%

Billions $Q4 2017

$3.84 Tn

Source: Fed Board of Governors, St. Louis Fed WOLFSTREET.com

#CBALIVE | 10#CBALIVE | 10

How to Get Started: Identify Where You Are Today

• Omni-channel contact capability

• Integrated web presence

• Robust analytics driving strategy

• Core learning systems leveraging AI

• Mobile app with push notifications and

self-service capabilities

LEADERS

#CBALIVE | 10

#CBALIVE | 11#CBALIVE | 11

How to Get Started: Identify Where You Are Today

#CBALIVE | 11

• SORs with standard routing and queuing

• Basic VRU with prompts

• Some email and text capability

• Reliance on dialers, letters and roll rates

• Limited or no web presence

MAJORITY

#CBALIVE | 12#CBALIVE | 12

How to Get Started: Identify Where You Are Today

#CBALIVE | 12

• Innovative analytics & segmentation (data, scoring and journeys).

• Integrated customer journey creating a superior value proposition.

• Drive an experience that separates you from others.

HOW LEADERS ARE MOVING FORWARD

#CBALIVE | 13#CBALIVE | 13

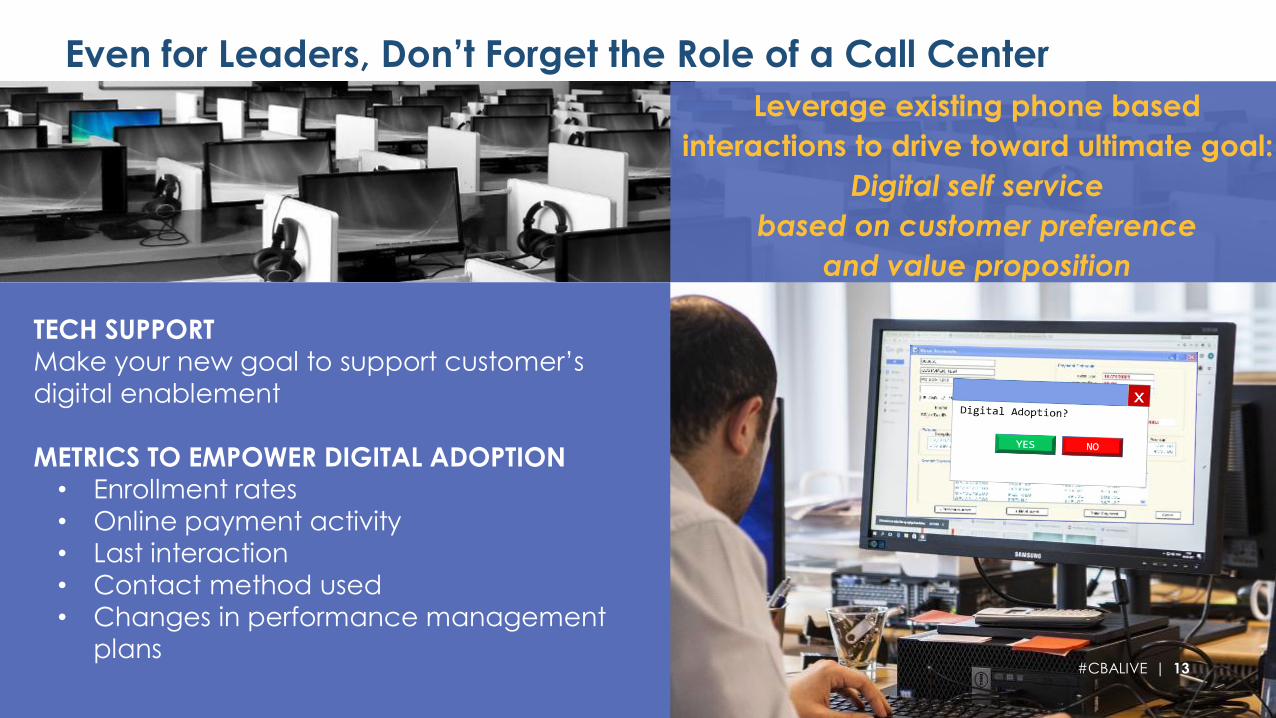

TECH SUPPORT

Make your new goal to support customer’s

digital enablement

METRICS TO EMPOWER DIGITAL ADOPTION

• Enrollment rates

• Online payment activity

• Last interaction

• Contact method used

• Changes in performance management

plans

Leverage existing phone based

interactions to drive toward ultimate goal:

Digital self service

based on customer preference

and value proposition

#CBALIVE | 13

Even for Leaders, Don’t Forget the Role of a Call Center

#CBALIVE | 14#CBALIVE | 14

Building Momentum: Two Approaches

TRADITIONAL APPROACH

“JUST DO IT” APPROACH

If it is not a strategic priority

then there are two approaches

Build your internal business case, obtain funding,

and prioritization. Looking at 18-24 months

before you make some progress.

Just get started. Getting online and/or in the

mobile app is critical. Identify what you have

and expand on it, show value and impact

and use that to make your case to fund a

larger investment.

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

#CBALIVE | 15#CBALIVE | 15

Show why technology is needed to achieve organizational goals:

▪ Declining contact rates over time

▪ Declining customer satisfaction rates

▪ Collections complaint drivers/trends:

– focus on complaints from too many calls or inconvenience (time / channel)

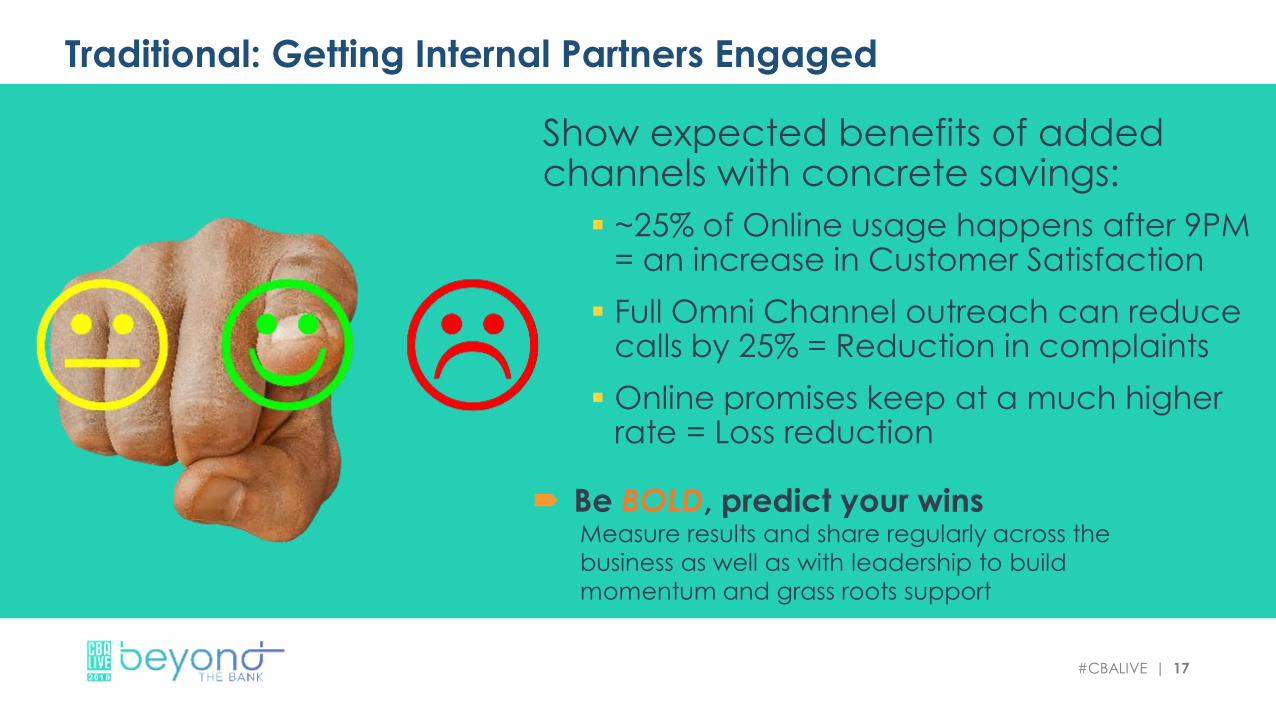

Traditional: Getting Internal Partners Engaged

#CBALIVE | 16#CBALIVE | 16

If internal barriers persist, create or buy a phone/written customer survey.

▪ Ask customers how they prefer to interact and give options:

– Phone, letters, mobile app, text,

email, online, chat as options

– Aggregate phone/letters against all

others to show what customers want

▪ Challenge partners to provide alternatives if there are objections in the face of hard data

Traditional: Getting Internal Partners Engaged

#CBALIVE | 17#CBALIVE | 17

Show expected benefits of added channels with concrete savings:

▪ ~25% of Online usage happens after 9PM = an increase in Customer Satisfaction

▪ Full Omni Channel outreach can reduce calls by 25% = Reduction in complaints

▪ Online promises keep at a much higher rate = Loss reduction

Be BOLD, predict your winsMeasure results and share regularly across the

business as well as with leadership to build

momentum and grass roots support

Traditional: Getting Internal Partners Engaged

#CBALIVE | 18#CBALIVE | 18

© 2018, Confidential & Proprietary Property of Bridgeforce LLC

OPTION #1

Leverage existing footprint for basic collections functionality 1. Payment Reminders and Education

2. Treatment Offers and Enrollment

3. Setting Contact Information / Preferences / Consent

OPTION #2

If you can’t obtain funding approval and/or IT

resources, use an existing vendor to build URL or

mobile app functionality

JUST DO IT

If you are operating in a dialer and letter

environment, start developing an online

and/or mobile presence for collections.

Get Started with What You Have or Can Access Quickly

#CBALIVE | 19#CBALIVE | 19

Brian Moore, senior principal, industry solutions of Nuance’s Enterprise division, brings more than 30 years of

experience in financial services, mortgage and collections operations and technology to the company. He

is also our resident compliance expert, advising companies on the TCPA, FDCPA, TSR and other regulations

impacting customer engagement.

© 2018 Nuance Communications, Inc. All rights reserved. 20

Ready, set, collect (digitally)!

#CBALIVE | 21

#CBALIVE | 22

Omni-Channel Engagement Platform

Professional & Hosting Services

Digital Voice Outbound Security

Customer Acquisition Customer Care

OMNI-CHANNEL ENGAGEMENT PLATFORM

Data Security Business Intelligence Tooling APIs & SDKs

AI for Prediction AI for Conversation AI for Analytics

• Intent prediction

• Targeting & Routing

• Fraud Management

• Intent Discovery

• Knowledge

• Identification & Verification

• Speech recognition

• Dialog

• Transcription

Learning Loop

Web Mobile Phone

#CBALIVE | 23#CBALIVE | 23

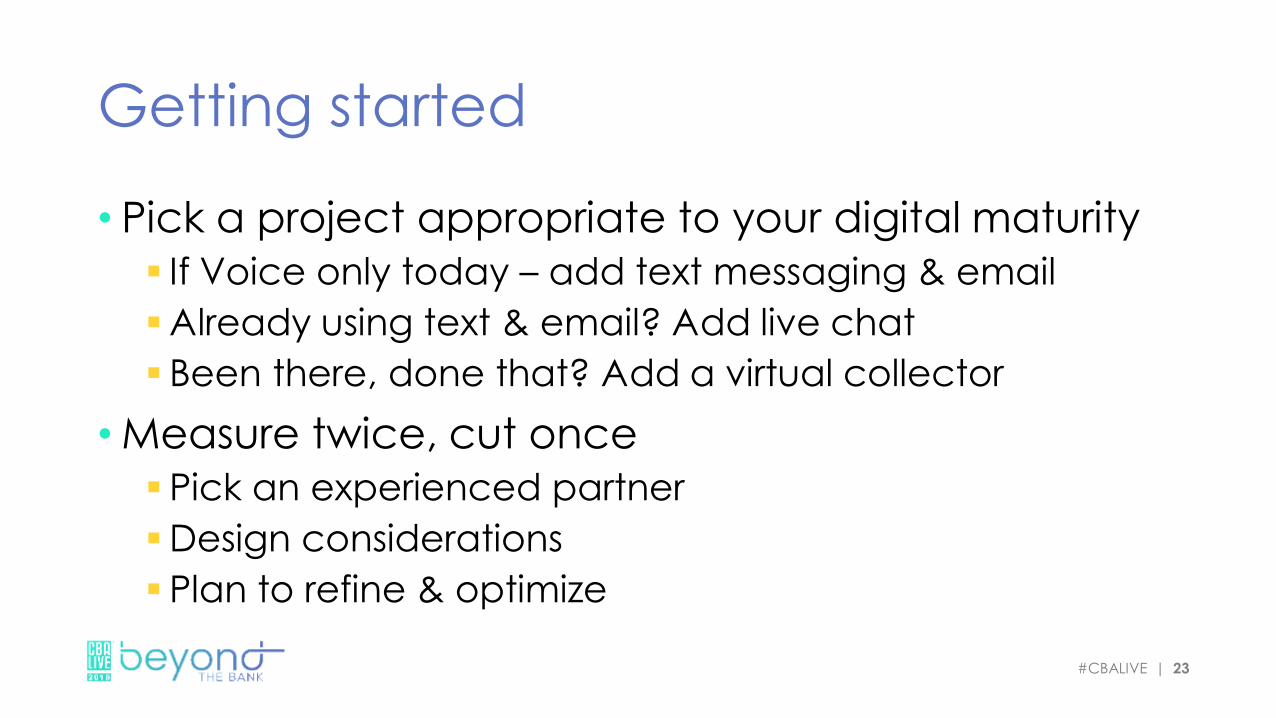

Getting started

• Pick a project appropriate to your digital maturity

▪ If Voice only today – add text messaging & email

▪Already using text & email? Add live chat

▪ Been there, done that? Add a virtual collector

•Measure twice, cut once

▪ Pick an experienced partner

▪Design considerations

▪ Plan to refine & optimize

#CBALIVE | 24

What can you expect?Adding one-way text messaging to a voice-only strategy

• Increase self-service cures 3-7%

• Reduce operational costs• Save 10 – 15 FTE per 100K

accounts

• Building block for automated conversations

Customer Action Average

Web Visit 6.2%

Web Pay 1.8%

IVR Call 7.0%

IVR Pay 3.4%

Overall Response 13.2%

Overall Pay 5.1%

Response to early stage collections texts

4-7%

1-3%

3-7%

% of Delivered Texts

Range

6-8%

2-4%

10-15%

#CBALIVE | 25#CBALIVE | 25

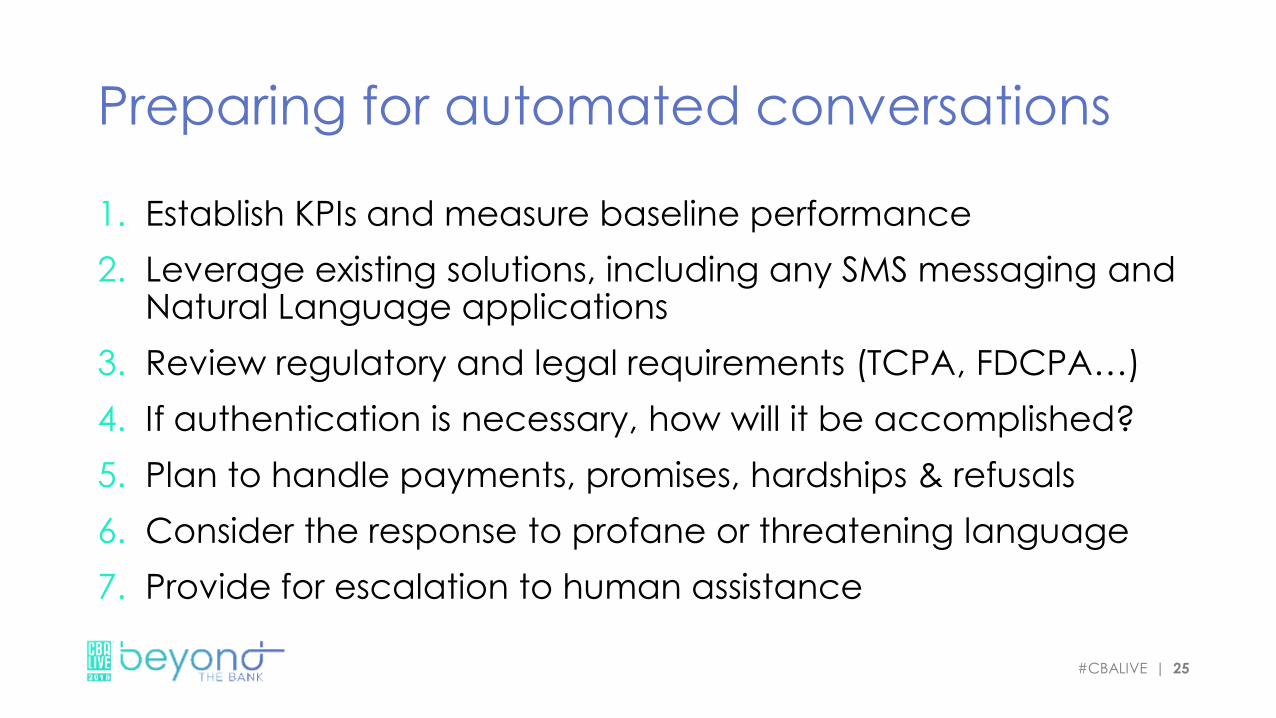

Preparing for automated conversations

1. Establish KPIs and measure baseline performance

2. Leverage existing solutions, including any SMS messaging and Natural Language applications

3. Review regulatory and legal requirements (TCPA, FDCPA…)

4. If authentication is necessary, how will it be accomplished?

5. Plan to handle payments, promises, hardships & refusals

6. Consider the response to profane or threatening language

7. Provide for escalation to human assistance

#CBALIVE | 26#CBALIVE | 26

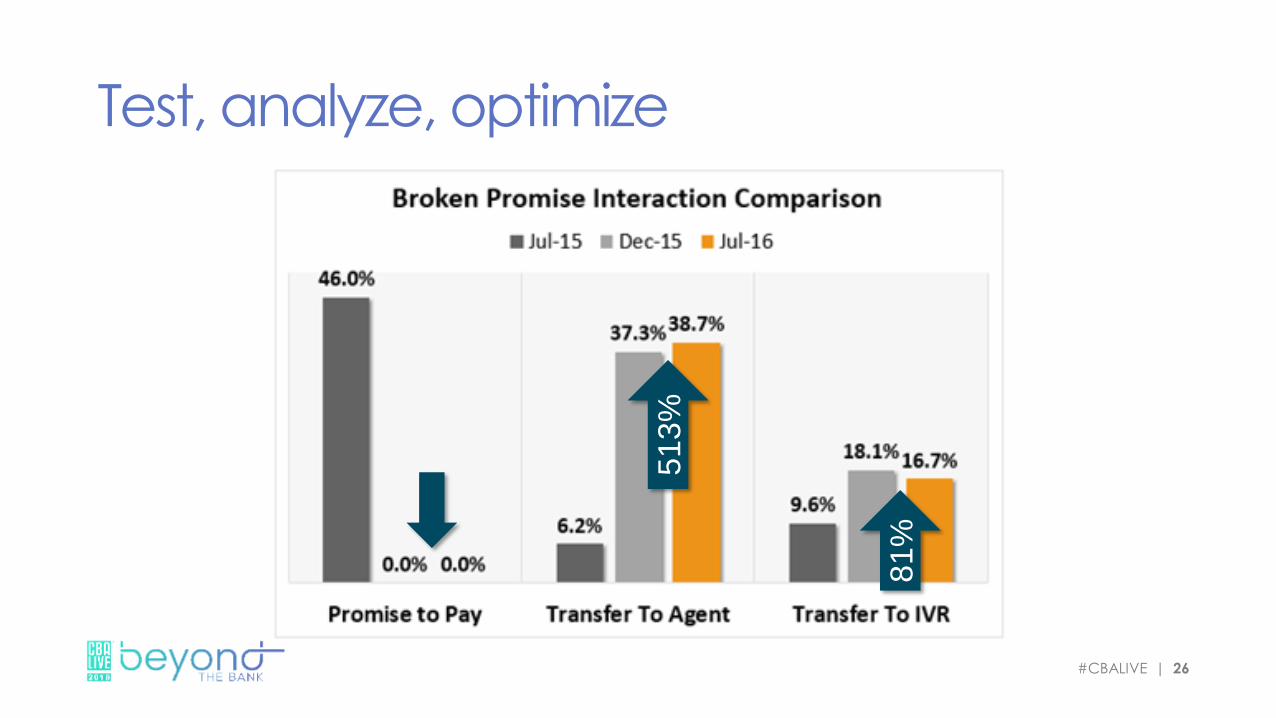

Test, analyze, optimize

51

3%

81

%

#CBALIVE | 27

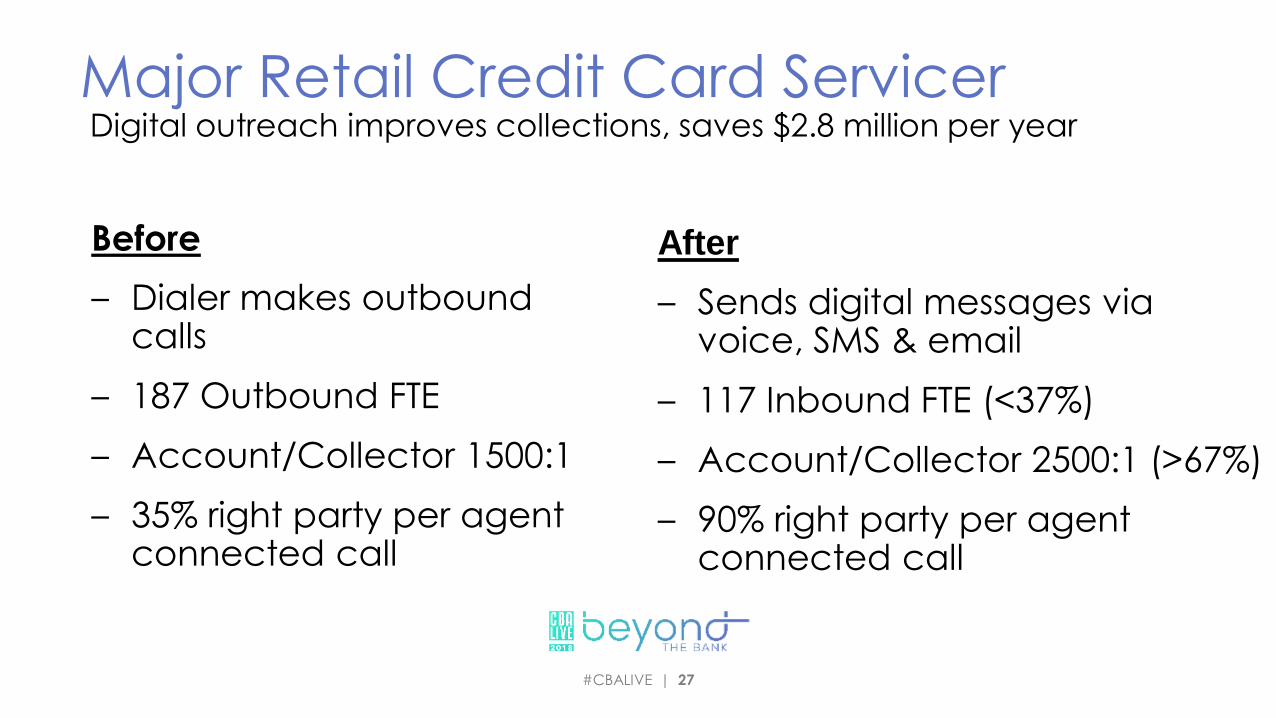

Major Retail Credit Card Servicer

Before

– Dialer makes outbound calls

– 187 Outbound FTE

– Account/Collector 1500:1

– 35% right party per agent connected call

Digital outreach improves collections, saves $2.8 million per year

After

– Sends digital messages via voice, SMS & email

– 117 Inbound FTE (<37%)

– Account/Collector 2500:1 (>67%)

– 90% right party per agent connected call

© 2018 Nuance Communications, Inc. All rights reserved. 28

Questions?

#CBALIVE | 29#CBALIVE | 29

David Laroche, Default Management

and Auto Finance Practice Leader

+1 302.465.3247

CONTACTInformation

Top Related