![Green bonds - OECD bonds PP [f3] [lr].pdf · Debt currently finances the majority of LCR Annual issuance of labelled green bonds tripled in 2014 to reach USD 36.6 billion, and issuance](https://static.fdocuments.in/doc/165x107/5f072f9e7e708231d41bbc02/green-bonds-oecd-bonds-pp-f3-lrpdf-debt-currently-finances-the-majority.jpg)

Languages

Pages

Legal

Macroeconomic and F inan cial Managemen t In stitu te of Eastern and Sou thern Afr ica

Inflation-Linked Bonds Issuance: A potential tool in

Debt Management Strategy for MEFMI Countries

By

Cappitus J.O. Chironga (MEFMI Fellow)

Central Bank of Kenya

A Technical Paper Submitted in partial fulfillment of the MEFMI Fellows Accreditation, April 2015

i

Table of Contents LIST OF TABLES AND FIGURES ................................................................................................................... ii

LIST OF ACRONYMS ........................................................................................................................................iii

Abstract ............................................................................................................................................................... iv

1. INTRODUCTION ....................................................................................................................................... 1

1.1 Global Experience in ILBs Issuance .................................................................................................... 3

1.2 Problem Statement ................................................................................................................................ 5

1.3 Objectives of the Study .......................................................................................................................... 6

2 RESEARCH METHODOLOGY ................................................................................................................ 7

2.1 Review of the MEFMI Region Conditions .......................................................................................... 7

2.2 Pricing Methodology of Inflation Linked Bonds.............................................................................. 10

2.3 Inflation-Linked Bonds and Public Policy ........................................................................................ 14

3 INFLATION – LINKED BONDS AS A DEBT MANAGEMENT STRATEGY................................... 18

3.1 Cost-Risk Management Objective of the Issuer (and Investor)..................................................... 19

3.2 Cash Management Objective of the Issuer (Government) ............................................................. 22

3.3 Inflation-Linked Bonds and Monetary Policy Implementation .................................................... 28

3.4 Inflation-Linked Bonds and Capital Markets Development .......................................................... 30

4 CONCLUSIONS ........................................................................................................................................ 33

Annex 1: South African Outstanding Bonds Portfolio as at March 2014 ................................................. 35

Annex 2: Top Global ILBs Issuances and Reasons ...................................................................................... 35

ii

LIST OF TABLES AND FIGURES Tables

Table 1: Consumer Price Index ...................................................................................................................... 12

Table 2: Unit Root Tests based on Seasonally Undjusted Data .......................................................................... 26

Table 3: Summary Results (with a Constant) .................................................................................. 26

Table 4: Summary Results (no Constant) ............................................................................................................ 27

Figures

Figure 1: Real GDP, Tax Collections and CPI (Logs) .................................................................................. 24

Figure 2: Real GDP and Tax Collections ....................................................................................................... 25

Figure 3: Seasonally Adjusted Real GDP and Tax Collections Data ......................................................... 25

iii

LIST OF ACRONYMS BEIR Breakeven inflation rate CPI Consumer Price Index CPI-U Consumer Price Index for Urban Consumers DMS Debt Management Strategy GDP Gross Domestic Product LN Natural Logarithm Logs Logarithm MEFMI Macroeconomic and Financial Management Institute of Eastern

and Southern Africa NFRB Nominal Fixed Rate Bonds OLS Inflation Linked Bonds RGDP Real Gross Domestic Product WPI Whole Sale Price Index TIPS Treasury Inflation Protected Securities UK United Kingdom US United States of America

iv

Abstract

Debt management strategy remains one of the key policy instruments Governments all over the

world use to ensure that public and publicly guaranteed debt remain sustainable in the medium

term. Among the objectives, both primary and secondary, embedded in a typical DMS are; Cost –

Risks management goals, Cash Management, Policy implementation and domestic financial

development. Various tools used in attainment of these objectives have proven effective to a large

extend in many countries. However, the use Inflation Linked Bonds (ILBs) as a direct public dent

management strategy tool remain less exploited more so in Africa and the MEFMI region in

particular. The instrument has grown in usage in developed and emerging markets economies across

the globe. Sadly, Africa continues to lag behind in tapping this tool in its debt management

frameworks. To the best of the knowledge of the author, only South Africa has actively used this

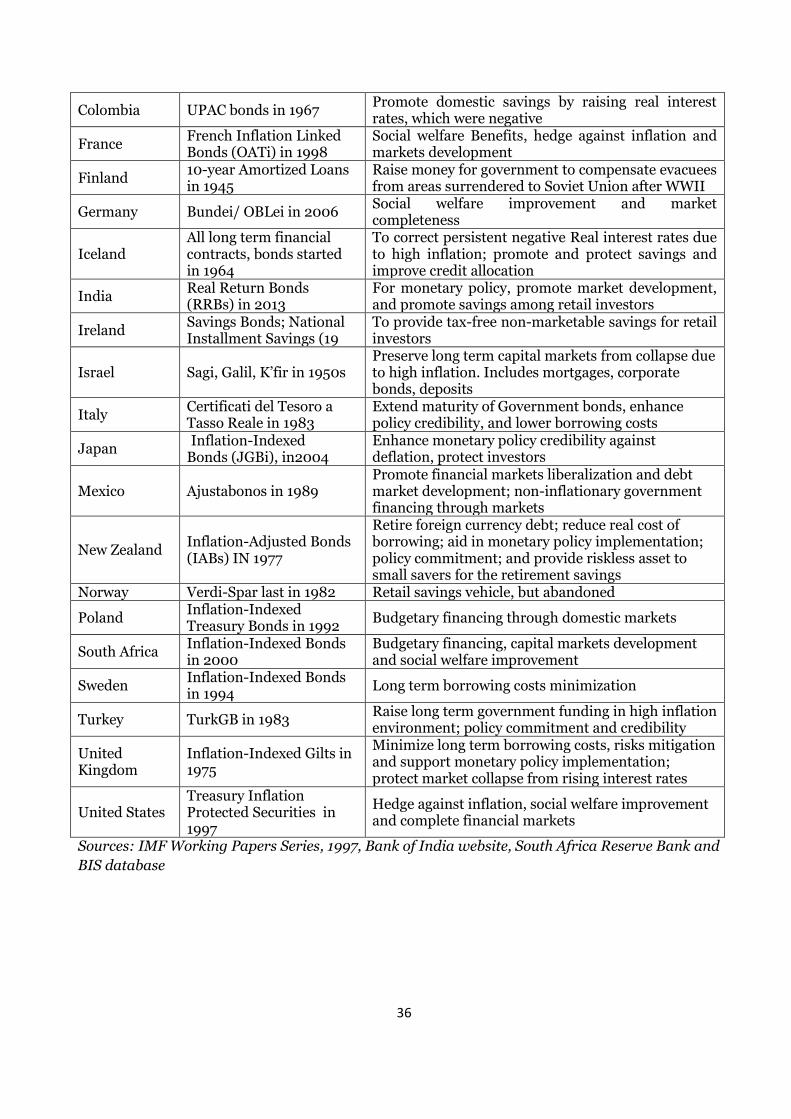

instrument (annex I and II) among the African countries as part of its debt management strategy.

This paper has tried to show the many benefits that accrue to use of ILBs from three perspectives

derived from public DMS objectives; Public Debt Management Operations, Monetary Policy

implementation, and Financial Markets Development. From the empirical literature, global

experiences and econometric analysis results, we deduce that ILBs contribute immensely to cost

savings to the extent of inflation expectations and inflation risk premium. In addition, the fact that

the Cash flows (interest and principal payouts) of ILBs are indexed on realized inflation and so are

the Government tax collections since both are nominal variables, ILBs therefore minimizes the

mismatch between the two cash flows that be caused by sudden inflation dynamics, thus

contributing to the stability of Government debt cost structure. The OLS estimation using Kenya‟s

quarterly data shows significant impact of inflation on tax collections, and intuitively on debt service

costs. From monetary policy perspective, if ILBs portfolio accounts for a critical proportion of overall

Government Debt Portfolio, then monetary authorities will experience enhance policy credibility

towards price stability. The breakeven inflation (yield spread between ILB and nominal bond of

similar maturity) provide information signaling mechanism to the monetary policy authorities about

average inflation expectations build-up. In terms of financial markets development, ILBs provide

alternative asset for inflation hedging, and therefore become a preferred instrument by long term

investors like pension and insurance firms. In effect, inflation protection element of ILBs dissuades

potential investors from divesting from fixed income into commodities, real estate and even imports,

thereby contributing to a more developed and vibrant long term capital markets. Care should

however be taken so that ILBs do not lead to over-indexation of other sectors of the economy,

including wages, loans, and other contracts.

Key Words: Indexation, Inflation Linked Bonds, Public Debt Management Strategy, Inflation Risk

Premium

1

1. INTRODUCTION

Sovereign debt management is a process of formulating and executing a strategy for

managing government debt in order to raise the required funding levels, achieves its risk

and cost objectives and meet any other goals the government may have set, including

development and maintenance of efficient domestic financial markets1. As a prudent public

policy, governments normally seek to ensure that both the level and rate of growth in their

public debt is largely sustainable, and can be serviced under a wide range of circumstances

while meeting cost and risk objectives. This means that the choice of debt instruments to

issue should be tailor-made to achieving these strategic objectives.

Sovereign debt managers share fiscal and monetary policy advisors‟ concerns that public

sector indebtedness remains on a sustainable path and that a credible strategy is in place to

reduce excessive levels of debt. Debt managers should therefore ensure that the fiscal

authorities are aware of the impact of government financing requirements and debt levels on

borrowing costs. By reducing the risk that the government‟s own debt portfolio management

will become a source of instability for the private sector, prudent government debt

management, along with sound policies for managing contingent liabilities, can make

countries less susceptible to contagion and financial risk.

Sound debt management policies thus play a catalytic role for broader financial market

development and financial deepening. Inadequate debt management policies together with

inappropriate fiscal, monetary, or exchange rate policies generate uncertainty in financial

markets regarding the future returns, thereby inducing investors to demand higher risk

premiums. In developing and emerging markets, borrowers and lenders alike may refrain

from entering into longer-term commitments, which in turn stifles the development of

domestic financial markets, and severely hinder debt managers‟ efforts to protect the

government from excessive rollover risks.

A government‟s debt portfolio is usually the largest financial portfolio in a country and

contains complex and risky financial structures, which can generate substantial risk to the

government‟s balance sheet with spillovers to the country‟s financial stability. Consequently,

1 Definition by the World Bank/IMF Guidelines for Public Debt Management, 2001

2

strategies such as establishing portfolio benchmarks targeting desired currency composition,

duration, and maturity structure of the debt have been adopted to enable governments

reduce their exposure to potential risks. The less used instrument that is now emerging as a

very important debt management tool in achieving strategic objectives of debt managers is

the issuance of inflation-linked bonds. An inflation linked bond (ILB) is a debt security

issued by governments (or government agencies) and private sector firms in order to provide

a hedge against inflation to both issuers and investors. The instrument is aimed at protecting

the bond holder‟s purchasing power by tying interest and principal payments (cash flows) to

an index of price changes (Price, 1997). The security thus consists of two components; a real

return and a compensation for the erosion of purchasing power of the investor.

To the private sector issuers, these securities provide a better hedge between assets and

revenues on one hand, and liabilities and debt on the other for activities that are highly

correlated with inflation developments, such as infrastructure projects, retail business,

rental property, and municipality taxes. Majority of issuers of ILBs are governments given

their role in creating inflation through fiscal and monetary operations. Substantial benefits

have been reported by countries that have used inflation-indexed bonds in terms of cost-risk

management and domestic financial markets development, which are primary and

secondary objectives of debt management strategy. The beauty about this instrument is that

it is beneficial to both the issuers and the investors in terms of hedging against future

uncertainties. It is on this basis that this paper seeks to explore the potential use of ILBs in

the MEFMI region.

The rest of this paper is structured as follows. Chapter two of this paper discusses the

methodology used in this study while Chapter provides extensive analysis on the use of

Inflation Linked Bonds as a Debt Management Strategy. Chapter four of the study draws

conclusions based on the empirical evidence and reviews, providing recommendations on

the road map for MEFMI countries concerning this new instrument. The last part of the

study covers annexes.

3

1.1 Global Experience in ILBs Issuance2

The ILBs have a long history, dating back to the 18th century when the first known indexed

financial instrument was issued by the Commonwealth of Massachusetts in 1742. The bills of

public debt issued were linked to the cost of silver on the London Stock Exchange. The State

of Massachusetts then followed by linking its debt to broader set of commodities following

steep appreciation of silver prices than the general prices. In 1780, Massachusetts Bay

Company linked its issued bond principal and interest payments to the price of a basket of

goods including wheat. Since then, these instruments have grown in importance and usage

globally, especially in more developed bond markets and in countries with ageing population

that care about pension payments in real terms.

Inflation-linked bonds have been issued for different reasons and in different circumstances,

but all culminate into attaining the set debt management objectives. Reasons advanced by

various countries can be broadly categorized into three3:

(1) Countries experiencing high and volatile inflation used ILBs as the best option in raising

long term capital in the bond market, which could not be achieved using plain vanilla bonds.

They include, Chile (1956), Brazil (1964), Argentina (1973), Turkey, and Italy (1983);

(2) Countries that issued inflation-linked bonds to reinforce credibility of their

disinflationary policies, which demonstrates government commitment to these policies and

reduce cost of borrowing, by exploiting excessive inflation expectations. In this group are;

the United Kingdom (1981), Australia (1985), Sweden (1994) and New Zealand (1995); and

(3) Countries that issued these securities for social welfare benefits and to complete financial

markets by providing effective hedge against inflation, especially to the pension sector

include; Canada (1991), U.S (1997), France (1998), Greece (2003), Japan (2004) and

Germany (2006).

2 Refer to annex II for detailed review

3 Garcia and Rixtel, 2007

4

The largest market for inflation-linkers is the United States, where the US government

issues Treasury Inflation Protected Securities (TIPS). In 2013, TIPS accounted for 10 percent

of total marketable debt in the U.S and more than 3.5 percent of GDP. Both institutional and

retail investors hold them in their portfolio. TIPS feature protection of principal and interest

payments from inflation. The principal is linked to changes in the non-seasonally adjusted

Consumer Price Index for Urban Consumers (CPI-U). The semi-annual coupons on the bond

are also inflation-adjusted since they are based on the underlying inflation-adjusted

principal amount. TIPS also incorporate a „deflation floor,‟ so that all cash flows (principal

and coupons) on the securities do not fall below the original face value of the bonds, thus

protecting investors against prolonged periods of deflation.

According the BIS database, as of April 2012, global government ILBs market approximated

U.S$2 trillion4 where the United States accounted for $ 866 billion, United Kingdom at $

549 billion, France with $ 235 billion and Italy with $ 132 billion. Indeed in 2013, ILBs/ILGs

accounted for more than 30 percent of the U.K public debt, equivalent to 10 percent of UK

GDP5. The U.K Government has now proposed to issue super-long maturities6 or even

perpetual inflation-linked Guilts to meet the strong market demand both at home and in the

Euro Area. This may also contribute to the Forward Guidance monetary policy adopted by

the Bank of England. Japan also revived its ILBs market after a long period of deflationary

environment. Other countries both developed and emerging Markets and developing

economies have built sizeable portfolio of these bonds. These include; Canada, Australia,

Brazil, India, Turkey, Israel and South Africa being among the leading issuers (Barclays

Capital World Government Inflation Linked Bonds markets).

In Africa, and the MEFMI region in particular, these instruments have not been issued

extensively despite their rapid growth in other parts of the world. Outside the MEFMI

region, South Africa was the first country to issue this type of bonds in 2000 and remains

the largest and most active market. In the MEFMI region, only Angola has issued these

instruments, but remains largely inactive. There is an opportunity for Africa and the MEFMI

region in particular to develop this segment of the market in order to benefit from dividends

accruing from ILBs.

4 Bridgewater Hedge Fund reported that in 2013, global government ILBs market was estimated at $ 2.5 trillion,

surpassing the high-yield corporate bond market and double the dollar denominated emerging markets bond market. 5 National Bureau of Economic Research (NBER) Report 2013 No. 3

6 Maturities beyond the current longest tenor of 50 years

5

1.2 Problem Statement

Bonds markets development in the MEFMI region is moving at a snail pace. Investor base

remains narrow and products/instruments range is limited to the conventional Treasury

bonds, Treasury bills, central bank papers and equities. With growing population, emerging

middle class and continued liberalization of the financial markets, including reforms in the

pensions and insurance sectors, policy makers in the region must quickly provide ample

opportunities to meet the needs of this evolving market. This would among other incentives,

include asset class that would minimize risks and guarantee investors‟ expected rate of

return. Issuance of Inflation-Linked Bonds (ILBs) as additional instruments to supplement

conventional bonds perfectly fit here.

The MEFMI Government Securities Issuance Guidelines (2013) shows that the region

requires accelerated development of the financial markets, especially domestic debt markets.

Financial markets development is one of the secondary objectives many countries‟ debt

management strategies actually are set to achieve as discussed in the World Bank Public

Debt Management Strategy (2001). In the MEFMI region, countries like Kenya have fairly

well-developed financial markets while the rest of MEFMI region lag behind. Absence of

pricing benchmarks such as benchmark yield curve makes it difficult to issue new bonds that

are correctly priced, further compounding the underdeveloped market problem. Issuance of

ILBs, which mainly rely on CPI as a pricing benchmark is one way of resolving this problem.

Macroeconomic conditions are fairly stable in the MEFMI countries, thus providing ample

conditions for ILBs, yet none has explored development of this market. Even the countries

neighbouring South Africa, which is biggest market for ILBs in Africa, have not exploited

window by has issuing the ILBs despite huge potential and benefits that exist. Issuers of

these instruments stand to gain in terms of; Social welfare improvement, efficient debt

management, enhancement of monetary policy and credibility and development of capital

markets, Price (1997) and Garcia and Rixtel, (2007). This is what this paper aims at creating

awareness to MEFMI member countries.

6

1.3 Objectives of the Study

The General Objective of the study is to demonstrate that Inflation Linked Bonds issuance in

the MEFMI region, is adopted and implemented properly would contribute significantly to

achievement of Public Debt Management Strategic objectives in the region that include Cost-

Risk Management, Funding needs, Cash Management and Financial Markets Development.

Specific Objectives of the study are;

1. To review global market for Inflation Linked Bonds to obtain lessons for the MEFMI

region

2. Using 10-year quarterly data on CPI, Tax Collections and Real Gross Domestic

Product from Kenya, to demonstrate how ILBs can effectively be used in Public Debt

Management Strategy for MEFMI countries

3. Based study findings, recommend on the Wayforward for the MEFMI region in the

use of ILBs.

7

2 RESEARCH METHODOLOGY

The study covers the review of MEFMI countries to explore the potential candidates for

Inflation-Linked Bonds issuance as a debt management strategy. It explains pricing

methodology for the ILBs with illustrations so that potential issuers can easily use the

method in pricing their securities at primary market.

This being a desk research, it that uses available literature and Kenya‟s data on CPI, real

GDP and Tax Collections to explain how ILBs are important in fulfilling debt management

objectives. It is expected that the MEFMI Region can use the results to identify opportunities

for issuance and investing in Inflation-Linked Bonds. Simple small-scale econometric

models are run to provide empirical evidence on the relationship between inflation

developments and select macroeconomic variables, which is crucial to debt management

objectives such as cash management, cost-risk management and financial markets

development. Descriptive statistics and diagnostics tests are discussed to examine the

characteristics of the data used in the analysis.

2.1 Review of the MEFMI Region Conditions

MEFMI region comprises of thirteen countries located in Eastern and Southern Africa. The

member countries are heterogeneous in terms of language, level of financial markets

development and government policies geared towards economic management. MEFMI

continues to create a significant level of homogeneity through its capacity building

programmes across the region.

An important prerequisite for building investor confidence is a credible, stable and sound

macroeconomic environment, which needs to be in place before starting a journey to

develop stable financial markets. Conditions such as implementing appropriate, credible and

well-coordinated fiscal and monetary policies; transparent national budgets; robust

legislative & regulatory framework; and market friendly tax regime that does not hinder the

development & liquidity of the financial markets and distort the behavior of market

participants to the detriment of markets are essential. It is against this background that the

study undertakes indepth review of the MEMFI region to establish their potential for ILBs

issuance.

8

All MEFMI member countries have issued government securities in one form or another.

Long dated securities and corporate sector debt remain nascent, with few countries having

yet issued any municipal debt instruments. Mozambique issues Treasury bonds for deficit

financing and Treasury bills for monetary policy. Treasury bills are issued in maturities of

91, 182 and 364 days on weekly auctions. Treasury bonds are issued through the stock

exchange while central bank issues treasury bills. Although bonds are by law tradable at the

stock exchange, no actual trading that takes place due to buy-and-hold strategy. Treasury

bond auctions are volume-based, hence no price discovery or yield curve. Zambia issues

treasury bonds and bills primarily for fiscal purposes, open to both local and foreign

investors. Treasury bills are in maturities of 91, 182, 273 and 364 days. Treasury bonds are

in tenors of 2, 3, 5, 7, 10 and 15 years, all with fixed coupons. Corporate bonds issued by

banks and other firms generally mature in the range of 3 – 5 years, and all trade at the

Lusaka Stock Exchange (LUSE). Pricing of both bonds and bills is yield-based, uniform-

price auction. The investor base includes banks, insurance companies, pension schemes, and

custodians.

Uganda issues Treasury bills and bonds for domestic financing, with the former issued

fortnightly in maturities of 91, 182 and 364 days. Both securities are liquid instruments and

tradable in the secondary market. Treasury bonds are issued monthly in maturities of 2, 3, 5

and 10 years, tradable at the Uganda Securities Exchange and the OTC platform run by

Primary Dealers. The corporate bond market is relatively thin. The investor base is narrow

but growing, with banks and the national pension fund dominating all securities markets. It

has stable macroeconomic environment, with single digit inflation.

Tanzania issues treasury securities for fiscal and monetary purposes. Treasury bills are

issued fortnightly in maturities of 35, 91, 182 and 364 days. Treasury bonds are also issued

fortnightly for fiscal requirements and market development. Bonds are in maturities of 2, 5,

7 and 10 years, all with fixed coupons. Macroeconomic environment remains stable and

capital controls continue to ease, therefore allowing foreign investors to participate in the

market. Investor base is widening, especially with liberalization of pension sector.

Rwanda issues Treasury bill and bonds for fiscal purposes, with the former being issued in

maturities of 28, 91, 182 and 364 days while the later are issued for market development,

with the longest maturity being 5 years. Auctions are open to all investor categories, with no

restrictions on foreigners. Commercial banks dominate the primary and secondary markets,

9

which are largely inactive. There is no reliable benchmark yield curve and mark-to-market

prices are not published. Namibia issues Treasury bills and bonds for government budget

financing, with Treasury bills are issued on weekly while treasury bonds are issued monthly.

Market participants include commercial banks, brokers, Collective Investment Schemes,

Insurance Companies and Pension Funds. The secondary market is illiquid. Namibian

financial market is highly integrated with South Africa‟s market, especially being a member

of Common Monetary Area.

Malawi issues both Treasury bills and bonds for fiscal purposes, market development and

monetary policy implementation. Treasury bills are issued in maturities of 91, 182 and 364

days while Treasury bonds are in maturities of 2, 3, and 5 years. The country experienced

macroeconomic shocks leading to high inflation and weakening currency, which has

negatively affected the securities market. The secondary market is inactive as banks

dominate and securities are mainly short term. Lesotho issues both Treasury bills and

Treasury bonds for deficit financing of the government. Treasury bills are issued in

maturities of 91, 182, 273 and 364 days on monthly and bimonthly basis. Treasury bonds are

issued in maturities of 3, 5 and 10 years. Secondary market is non-existent as a result of the

buy-and-hold strategy, no yield curve or mark-to-market prices. Most investors are South

African. Botswana issues Treasury bills, Bonds and Bank of Botswana Certificates. The

BoBCs are issued weekly for monetary policy purpose in maturities of 14 and 91 days, and

only banks are allowed to participate. Treasury bills and bonds are issued to finance

government budget and market development. Secondary market is almost non-existent due

to shortage of securities and buy-and-hold strategy of banks. Angola‟s securities market is

still at infancy stage, with very few government securities and no stock market. There are

treasury bills, central bank bills and treasury bonds, with commercial banks being the only

active participants. The central bank issues securities on behalf of government. The liquidity

absorption instruments issued weekly are in maturities of 14, 28 and 63 days at fixed or

floating rate. There are bonds with maturities of 1 year to 20 years issued for budget support

in local currency. The central bank can rediscount treasury securities and also buy back from

the secondary market.

Kenya issues both treasury bills and bonds for budgetary support, infrastructure

development and market development. All tradable government securities are liquid

instruments and therefore are part of statutory liquidity requirements for commercial banks.

10

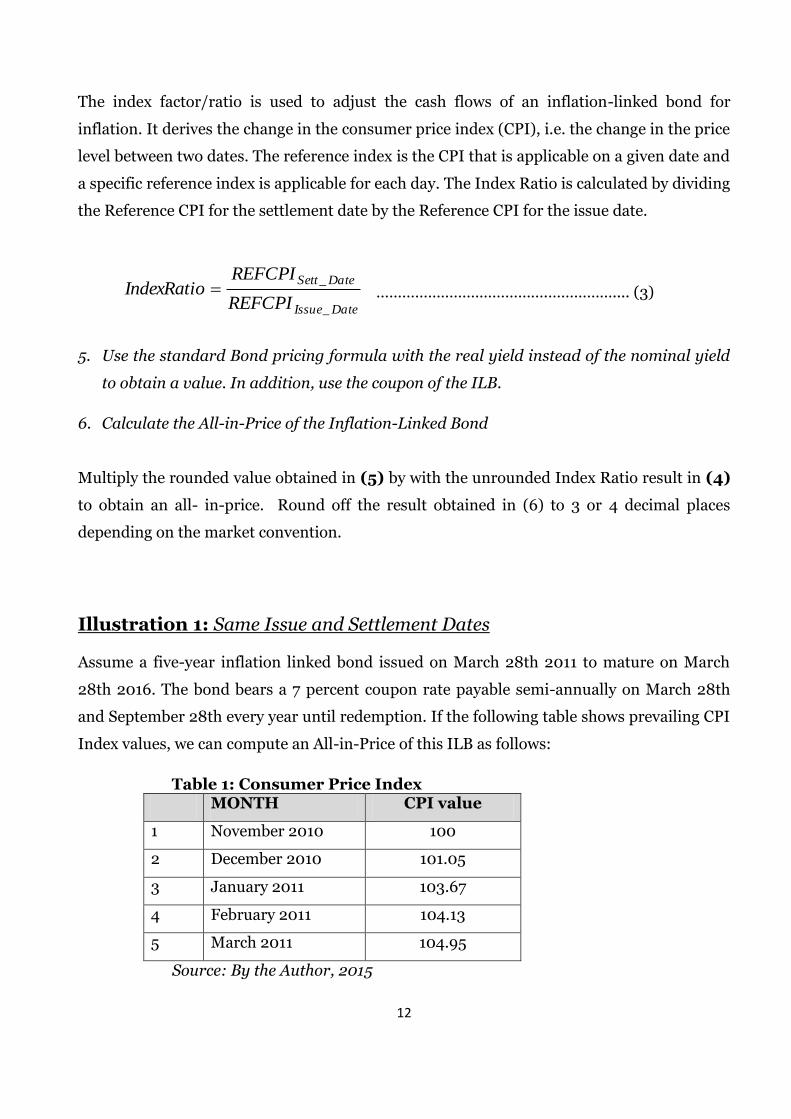

Primary and secondary government bond markets are active hence the reliable yield curve.

Corporate bond market is also vibrant, with more issues in 2013-2014. Treasury bills are

offered in maturities of 91, 182 and 364 days while treasury bonds are issued in a range from

2 year to 30 years. Market participants include banks, insurance companies, pension funds,

cooperatives, and retail. Auctions are open to all; foreign and local, institutional and retail

investors. The central bank offers the rediscount window to support liquidity if the market

is tight. It issues bonds with embedded options such as reopening, amortization, and sell-

buybacks. Kenya has experienced macroeconomic stability.

Overall, a number of MEFMI region countries have necessary conditions for Inflation-

Linked Bonds issuance. This would address the shortage of quality investable assets, the low

volume of securities issued that create a tendency to “buy and hold” among investors; less

transparent markets leading to inaccurate price discovery, and lack of a credible daily mark-

to-market prices; limited foreign investor participation due to yields being distorted by

withholding taxes and other levies, as well as foreign exchange controls; low corporate bond

issuance due to lack of pricing benchmark; no natural hedging products or derivative

markets with illiquid repo markets; narrow investor base dominated by commercial banks

and issuer base dominated by government; and narrow product ranges.

2.2 Pricing Methodology of Inflation Linked Bonds

The Fisher equation provides a basis for pricing real bonds or inflation indexed bonds. The

Fischer Identity hypothesizes that the real yield (r) equals to nominal yield (i) less the

inflation rate ( ). In other words,

Nominal Yield = Real Yield + Expected Inflation + Inflation Risk Premium

Or simply, Real Yield = Nominal - Inflation The pricing methodology for inflation-linked bonds follows 6 steps, largely anchored on the

South African pricing convention. These consist of:

1. Establish the settlement date (value date for primary issue) for the transaction 2. Determine the Reference CPI for the Inflation-Linked Bond’s Issue Date:

11

Reference CPI or “REFCPIIssue_Date” means, in relation to the settlement date on which the

issue took place:

If the Issue Date is the first day of a calendar month, REFCPIIssue_Date is the Consumer Price

Index (CPI) for the fourth calendar month preceding the calendar month in which Issue

Date occurs. However, if the Issue Date occurs on any day other than the first day of a

calendar month, then the REFCPIIssue_Date shall be determined using the following formula:

…………………………. (1)

Where:

(i) CPIJ is the CPI value for the first day of calendar month, 4 months preceding issue date; (ii) CPIJ+1 is the CPI value for the first day of calendar month, 3 months prior to the Issue Date; (iii) t is the calendar day corresponding to Issue Date; and (iv) D refers to the number of days in the calendar month in which Issue Date occurs.

3. In order to determine the Reference CPI for the settlement date, the process is similar

to Reference CPI for the Issue Date.

Reference CPI or “REFCPISett_Date” means, in relation to the settlement date, the date on

which the settlement took place:

If the Settlement Date is the first day of a calendar month, REFCPISett_Date is the

Consumer Price Index for the fourth calendar month preceding the calendar month in

which settlement date occurs; or

If the Settlement Date occurs on any day other than the first day of a calendar month,

then the REFCPISett_Date shall be determined using the following formula:

……………… (2)

Where:

(i) CPIJ is the CPI value for the first day of the calendar month, 4 months preceding settlement date; (ii) CPIJ+1 is the CPI value for the first day of the calendar month, 3 months prior to the settlement date (iii) t is the calendar day corresponding to settlement Date; (iv) D refers to the number of days in the calendar month in which settlement date occurs. 4. Derive the Index Ratio/Factor using the Issue and Settlement Dates:

JJJDateIssue CPICPI

D

tCPIREFCPI 1_

*1

JJJDateSett CPICPI

D

tCPIREFCPI 1_

*1

12

The index factor/ratio is used to adjust the cash flows of an inflation-linked bond for

inflation. It derives the change in the consumer price index (CPI), i.e. the change in the price

level between two dates. The reference index is the CPI that is applicable on a given date and

a specific reference index is applicable for each day. The Index Ratio is calculated by dividing

the Reference CPI for the settlement date by the Reference CPI for the issue date.

………………………………….…………….... (3)

5. Use the standard Bond pricing formula with the real yield instead of the nominal yield

to obtain a value. In addition, use the coupon of the ILB.

6. Calculate the All-in-Price of the Inflation-Linked Bond

Multiply the rounded value obtained in (5) by with the unrounded Index Ratio result in (4)

to obtain an all- in-price. Round off the result obtained in (6) to 3 or 4 decimal places

depending on the market convention.

Illustration 1: Same Issue and Settlement Dates Assume a five-year inflation linked bond issued on March 28th 2011 to mature on March

28th 2016. The bond bears a 7 percent coupon rate payable semi-annually on March 28th

and September 28th every year until redemption. If the following table shows prevailing CPI

Index values, we can compute an All-in-Price of this ILB as follows:

Table 1: Consumer Price Index MONTH CPI value

1 November 2010 100

2 December 2010 101.05

3 January 2011 103.67

4 February 2011 104.13

5 March 2011 104.95

Source: By the Author, 2015

DateIssue

DateSett

REFCPI

REFCPIIndexRatio

_

_

13

If the bond was settled at a real yield of 6 percent on the issue data of 28th March, 2011, we

can compute the price of this ILB, determining the Reference CPI value on the issue date as

follows using formula in equation (1) above:

201020102010201128 *31

128NovDecNovMarch CPICPICPIREFCPI

10005.101*31

27100

= 100.9145

Since Settlement date is the same as Issue Date, our Index Ratio/Factor is as follows:

19145.100

9145.100

IndexRatio

If from the bond pricing calculator, the corresponding trading price at 6% yield to maturity

given nominal yield of 7 percent for settlement on March 28th 2011 is 104.265, then we can

compute an All-in-Price of the inflation-indexed bond as follows:

ILB = Index Ratio × Bond Price = 1 × 104.265 = 104.265.

Illustration 2: Different Issue and Settlement Dates Assume this bond still trades 6 percent real yield on April 10 2011. The reference CPI index will be derived as follows:

201020112010201110 *30

110DecJanuaryDecApril CPICPICPIREFCPI

836.10105.10167.103*30

905.101

Since Settlement date differs from Issue Date, our Index Ratio/Factor is computed as

follows:

0091.19145.100

836.101

IndexRatio

If from the bond pricing calculator, the corresponding trading price at 6 percent yield to

maturity given nominal yield of 7 percent for settlement on April 10th 2011 is 104.265, then

we can compute an All-in-Price of the inflation-indexed bond as follows:

ILB = Index Ratio × Bond Price = 1.0091 × 104.265 = 105.2171.

14

2.3 Inflation-Linked Bonds and Public Policy

A number of studies including Kumar and Chander (2012) have discussed extensively on

how Inflation-Indexed Bonds are emerging as a useful tool from public policy perspective,

for the developed, emerging markets and developing economies. Public policy in this

context encompasses fiscal, monetary and public debt management policies. Viceira (2013)

observed that TIPS are increasingly playing a critical role in policy formulation and

implementation. Central banks, economists and market practitioners/observers keenly

follow the evolution of the breakeven inflation (spread between plain vanilla government

bonds and ILBs of similar maturity) as a leading indicator for real time inflation

expectations from bond market participants (Garcia and Rixtel, 2007).

From the public debt management perspective, governments that have issued ILBs have

reported numerous benefits including cost saving to the extent of inflation risk premium,

anchoring credibility of the monetary policy on inflation expectations, and inflation hedging

role to potential investors. Inflation linked bonds are also easy to price given the underlying

pricing benchmark, the Consumer Price Index, that is widely available across countries.

Fiscal policy guides the level of debt to be raised by the government to finance budget

deficits in any given financial year. The debt manager would however be concerned with the

broad objective of cost minimization in the medium to long term horizon bearing in mind

the prudent degree of risk. The debt manager therefore chooses debt instruments to issue in

line with investors‟ expectations and prevailing market conditions in order to raise the

desired amount to meet fiscal needs, but at the same time caring about the broad objective

of cost minimization. This choice has been dictated by the ever-evolving financial market

conditions that have prompted public debt managers to continuously review the type of debt

instruments they employ in raising money.

Increasing market risks and emergence of more risk-takers and risk-averse investors in

equal measure have seen rising demand by potential investors for wider asset classes that

include; floating rate bonds, fixed coupon bonds, bonds with embedded options, inflation

linked bonds, among others. All these mix of bonds not only addresses the primary

objectives of any debt manager given the strategy being pursued, but also play a very

15

important role in meeting the secondary objectives of debt management strategy such as

secondary market development, monetary policy transmission and provision of additional

investment opportunities.

Indexation of public debt has become more widespread across the globe given the benefits7

being cited by the issuers. In some jurisdictions, the debt has been indexed on wages, GDP,

Commodities or foreign currency, but the most commonly used pricing benchmark has been

consumer price index, which is the focus of this paper. Consequently, more and more

leading economists are now in support of debt indexation, from John M. Keynes in 1924 who

proposed to the Royal Commission on National Debt and Taxation that the British

Government should issue indexed bonds. Jevons (1875), Marshall, Musgrave, Milton

Friedman and Robert Barro (Deacon, et al 2004) also emerged as strong proponents of debt

indexation.

Garcia and Rixtel (2007) details three reasons why countries issue ILBs; those countries

which could not raise long term capital through conventional bonds/securities as a result of

high and volatile inflation had to issue ILBs to attract investors; those countries that

intended to use ILBs as a reinforcing tool to enhance credibility of anti-inflationary policy

stance; and lastly, those countries, mainly developed economies that issued ILBs for social

welfare benefits, encompassing completing financial markets and providing an effective

hedge against inflation for long investors.

Aizenman and Marion (2009) observed that countries with excessive nominal debt stock

denominated in domestic currency have been tempted to create inflation through loose

monetary policy or expansionary fiscal policy in order to lower the debt burden. This

temptation was more pronounced if the largest proportion of this debt stock was held by

foreigners, implying that this category of holders will bear the inflation tax if inflation

actually rises. However, the issuance ILBs would protect such investors by creating a

7 ILBs benefits include; Social welfare improvement (transfer of inflationary risks from the investor to the issuer), efficient debt management through cost saving (Deacon and Derry (1994),Penati et al (1995), Breedon (1995)), enhancement of monetary policy and credibility (Calvo and Guidotti, 1989), and development of capital markets. All these form primary and secondary goals of a sound debt management strategy, Baer & Beckerman (1980), Levhari (1983) and Bach & Musgrave (1941).

16

disincentive for the government to create inflation since inflation risk is transferred from

investors to the Government.

The ILBs can also encourage savings and reduce consumption, thus complementing the

monetary policy effectiveness. Samuelson (1988) observed that accelerated savings triggered

by demand to invest in the ILBs provide the Government adequate financial resources to

fund its expenditure in a less inflationary way, thus dampening inflation and lowering

inflation expectations. Levhari (1983), Baer and Beckerman (1980), and Fischer (1975)

noted indexed bonds encourage public and private savings in an environment of inflationary

pressures, lengthens maturity profile of financial assets, and serve well small savers since

information and transaction costs are minimal. Therefore ILBs indirectly reinforces the

central bank‟s inflation anchoring mechanism, thus enhancing its credibility.

Marshall (1988) and Friedman (1974) also argue that ILBs provide distributive benefits

especially to long term savers like pensioners who bear the greatest pain in the event that

government or monetary authorities chose to run unfavourable policies that in turn create

inflation. It thus the responsibility of the policy makers to protect investors‟ wealth through

issuing indexed assets that guarantees real return. Thedeen (2004) observed that Sweden

and other countries have used ILBs for tax-smoothing or simply diversification. He argues

that a more diversified debt instruments reduces fluctuations in the yields on government

debt, thus contributing to stable interest rates, lowering the risk of having to change taxes

and benefits in order to offset rising interest rates. This in effect, contributes significantly to

the overall development of the financial markets.

Price (1997) summarized arguments in favour of the inflation-indexed bonds issued by

countries facing inflation pressures as; cost-saving to the issuer, completing the financial

markets8 benefiting the lender or investors, and strengthening policy tools, credibility and

commitment to monetary policy by the central bank. They also assist in extending the debt

maturity structure and foster capital markets development. Joseph Lowe in 1820s, Stanley

Fischer (1983a), and Jud (1978) have discussed extensively on the role of ILBs in the

development of capital markets, through lowering of risk, improving marketability of the

8 Where markets are complete and efficient, with market frictions such as transaction costs and distorting taxes, the paths

of debt and taxes are irrelevant following the debt neutrality theorem of Barro (1974) and others.

17

securities, encouraging voluntary long term savings, and rendering credibility of the

monetary policy. Countries such as Argentina, Brazil, Colombia, Chile, Hungary and Israel

benefited from ILBs in stabilizing their markets in a high inflationary environment.

Indexation of public debt might have devastating outcome especially if implemented in

absence of other supportive credible policies. Fischer (1983a) discussed in detail cases9

where indexation may exacerbate inflation, especially when an inflationary shock sets in.

Indexation may signal lack of commitment by monetary authority or governments in general

to achieve and maintain price stability. It may also overshadow and erode public confidence

in other nominal anchor like the fixed exchange rate. What is critical is that the introduction

of the ILBs in presence of robust commitment to price stability should not be interpreted to

mean laxity towards fiscal imprudence or monetary policy irresponsibility. As Hallsten

(1993) summarized, the timing for issuance of ILBs is very important – when inflation and

inflation expectations are low, then the ILBs have no impact in fueling inflation

expectations. Authorities also need to manage perceptions and maintain credibility when

issuing ILBs.

Adoption and issuance of ILBs should not spillover to other contracts in the economy such

as wages, credit facilities, taxation, bank deposits exchange rates or other financial markets.

Countries such as Iceland, Israel, Argentina, among others have all reported downside risks

to excessive indexation if not implemented properly.

9 A strong one-time effect of an inflationary shock on an indexed economy than a non-indexed one; through a higher inflation rate; and equilibrium price level becomes unstable yielding erratic price changes, are cases that may make indexation inflationary.

18

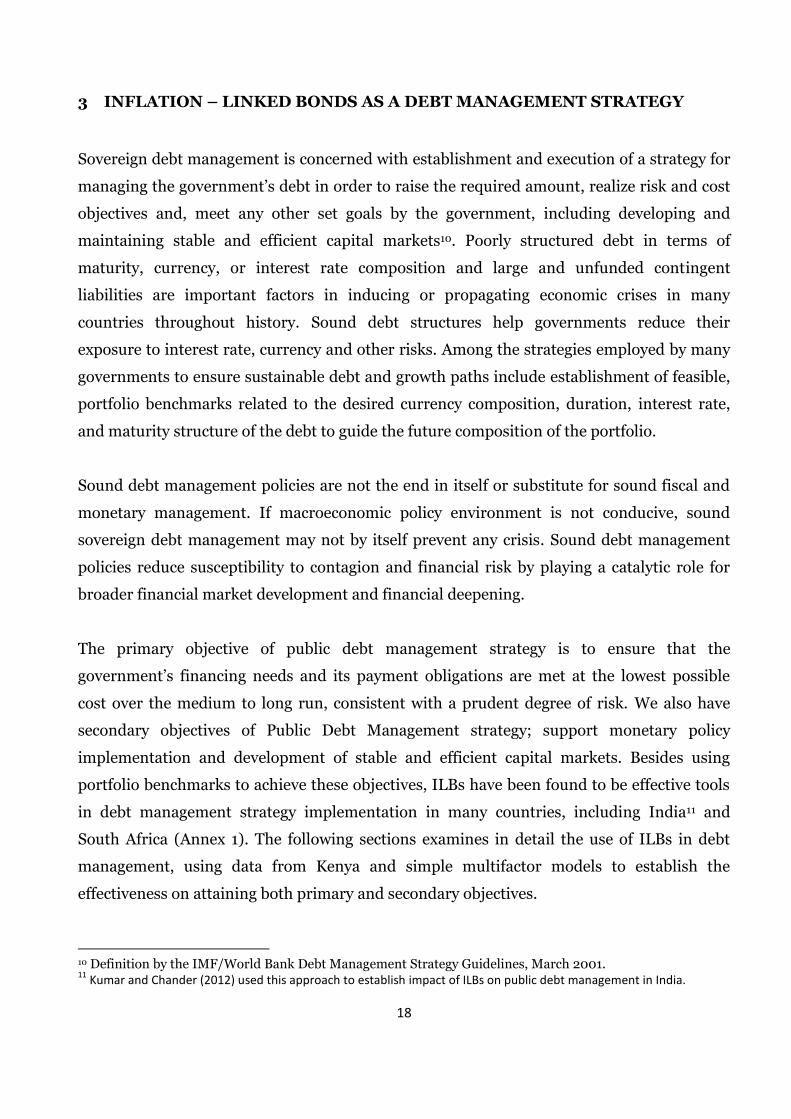

3 INFLATION – LINKED BONDS AS A DEBT MANAGEMENT STRATEGY

Sovereign debt management is concerned with establishment and execution of a strategy for

managing the government‟s debt in order to raise the required amount, realize risk and cost

objectives and, meet any other set goals by the government, including developing and

maintaining stable and efficient capital markets10. Poorly structured debt in terms of

maturity, currency, or interest rate composition and large and unfunded contingent

liabilities are important factors in inducing or propagating economic crises in many

countries throughout history. Sound debt structures help governments reduce their

exposure to interest rate, currency and other risks. Among the strategies employed by many

governments to ensure sustainable debt and growth paths include establishment of feasible,

portfolio benchmarks related to the desired currency composition, duration, interest rate,

and maturity structure of the debt to guide the future composition of the portfolio.

Sound debt management policies are not the end in itself or substitute for sound fiscal and

monetary management. If macroeconomic policy environment is not conducive, sound

sovereign debt management may not by itself prevent any crisis. Sound debt management

policies reduce susceptibility to contagion and financial risk by playing a catalytic role for

broader financial market development and financial deepening.

The primary objective of public debt management strategy is to ensure that the

government‟s financing needs and its payment obligations are met at the lowest possible

cost over the medium to long run, consistent with a prudent degree of risk. We also have

secondary objectives of Public Debt Management strategy; support monetary policy

implementation and development of stable and efficient capital markets. Besides using

portfolio benchmarks to achieve these objectives, ILBs have been found to be effective tools

in debt management strategy implementation in many countries, including India11 and

South Africa (Annex 1). The following sections examines in detail the use of ILBs in debt

management, using data from Kenya and simple multifactor models to establish the

effectiveness on attaining both primary and secondary objectives.

10 Definition by the IMF/World Bank Debt Management Strategy Guidelines, March 2001. 11

Kumar and Chander (2012) used this approach to establish impact of ILBs on public debt management in India.

19

3.1 Cost-Risk Management Objective of the Issuer (and Investor)

Cost management is one of the primary strategic objectives of public debt management

strategy. The cost associated with public debt can be interpreted as that actual interest costs

and other debt administrate costs paid by the debt manager, and/or the costs arising from

the failure of the debt manager to meet maturing obligations when they fall due. Technical

default or actual default has significant costs to the debt manager in terms of restoring

market confidence, other policies disruption, interest rates levels and even legal suits that

may arise. The debt manager must always be alert to the debt portfolio management to

prevent any form of default, whether actual or perceived. The debt manager will therefore be

concerned about the actual costs in terms of interest rates payouts and cost structure

stability in terms of matching cash flows accruing on the debt stock and revenues to pay off

these maturing cash flows.

The Government can borrow from domestic markets directly through loans from

commercial banks or indirectly through money and capital markets. Borrowing through the

former channel has negative impact in terms of credit markets allocations, policy

sustainability and overall credibility of any government, therefore leaving the second option

as the best choice. The Government may therefore issue fixed rate instruments or the linkers

(inflation-linked bonds and floating rate bonds priced on an underlying benchmark) to raise

the desired amount from domestic markets. The linkers have emerged as alternative credible

tools to effectively deliver cost-effective debt to the public debt managers.

To understand how ILBs assist in cost management, we need to decompose the pricing

framework of a typical ILB from which we explain its impact on cost management. Following

Fischer Identity, the yield (η) on nominal or plain vanilla bond consists of three

components; real return (γ), average expected inflation (ρe) and term/uncertainty premium

(ψ). Symbolically;

e……………………………… (4)

The term premia captures uncertainty arising from future expected inflation risks premium

and bonds illiquidity premium. The higher the uncertainty about average expected inflation

over the maturity spectrum of the bond, the higher will be the term premia sought by

investors as compensation for holding such security. The term premia demanded by

20

potential investors in the nominal bonds normally reflects the maturity period of nominal

bonds, especially if the uncertainty about average expected inflation is perceived to equal the

term of the bond.

The investors in ILBs however are protected from uncertainty induced by term premia since

these instruments pay returns linked to inflation. This implies that if inflation increases, the

holder will receive higher returns since they are linked to the inflation. Consequently, the

issuer of ILBs is likely to incur lower borrowing costs to the extent of inflation risk premium

normally on plain vanilla bonds given that investors do not seek term premia associated with

inflation uncertainty. This however assumes that actual inflation equals the break-

even12/expected inflation. The issuer of ILBs typically enjoys the cost savings of borrowing

using the instruments if the outstanding stock reaches critical mass that in turn provide

adequate liquidity, hence minimizing illiquidity premium that would otherwise outweigh

cost benefit arising from absence of uncertainty premium.

The Dutch Central Bank Working Group (2005) estimated that inflation risk premia range

from 0.1 to 1 percentage points. Cappiello and Guene (2005) using data on German and

French long term bonds found that inflation risk premia ranged between 10 basis points and

20 basis points. This supports the argument that nominal bonds issuers pay higher yield as

compensation for higher inflation risk premia given that investors are generally risk averse.

This risk is however minimized or eliminated in case of the ILBs, and thus the Issuer enjoys

cost savings, Garcia and Rixtel (2007).

The ILBs may also contribute to the Issuer‟s cost savings through lowering of inflation risks

premium on nominal bonds channel. In this case, the assumption is that ILBs improves the

credibility and commitment of monetary and fiscal policies authorities towards price

stability13. Reschreiter (2004) using the U.K data concluded that the Government‟s long run

borrowing costs could be cut remarkably through issuance ILBs in its debt stock. The best

12

Breakeven inflation refers to the difference between the yield on ILBs and that on Nominal fixed coupon bond of the

same tenor. If actual inflation exceeds the breakeven inflation rate, cost of saving arising from lack on uncertainty

premia is actually the difference between the realized inflation and breakeven inflation rate.

13 Where issuance of ILBs reaches critical mass, relative gains from higher inflation may be insignificant, hence improves

credibility of anti-inflationary policy. Consequently, higher inflation would penalize the government heavily but investors are fully insured against rising inflation. Therefore the government must strive to keep inflation low.

21

way to calculate the cost of savings realized from the ILBs is to evaluate for the entire life of

the bond and not at the end of calendar or fiscal year since inflation vary from year to year.

Keynes and other leading economists have all along argued that the government can reduce

its borrowing costs by issuing ILBs. This occurs when the market overestimates future

inflation given that most investors‟ expectations are not entirely forward-looking or rational.

The government would therefore reduce the cost of debt by issuance of ILBs rather than

nominal bonds. In addition, the government has ability to influence inflation dynamics

through its policies, and therefore has better information on future inflation developments.

Given this information monopoly over the future course of inflation, the government can

benefit greatly from issuing ILBs.

Active debt manager should continuously manage outstanding portfolio of bonds by

switching between the ILBs and nominal bonds provided the guiding rule is the real return

in the market. This requires better inflation or market forecasting ability so that the issuer

gets correct timing14 to issue ILBs. The perception that inflation expectations were excessive

partially explains why the U.K introduced ILBs, so was the New Zealand15. In both countries,

anti-inflation policies lacked credence, hence the market ignored, making inflation

expectations reflected in the yield curve exceed inflation expectations by the authorities.

The government can also benefit from ILBs through stability of borrowing costs in real

terms since the real component of the coupon remain unchanged. Given that the coupon

rate of nominal bonds is set with current inflationary expectations, such bonds when issued

during high inflation period remain very costly even when inflation declines and vice versa.

Therefore, in a volatile inflationary environment as is the case in many emerging and

developing economies, the costs structure becomes volatile as well, posing major challenges

to the debt manager. Therefore ILBs enables the Treasury to stabilize the real cost of its

debt since the real tax revenue closely track inflation, thus enabling the government to better

match with expenditure streams.

14

If the public underestimates the level of future inflation, then the issuer would benefit by issuing nominal bonds and the reverse is true. 15

The Governor of the Reserve Bank of New Zealand commented that while Australia and UK borrowed at real rates of 3.8% and 5.5% via ILBs, New Zealand borrowed at 7% - 8.5% real yields for similar maturity implying high inflation expectations given that actual inflation averaged 1% during the life of the bond. So the government paid huge penalty by issuing nominal bonds.

22

Barro (1979) supported this argument by noting that since the government real tax revenues

are correlated to inflation, issuance of ILBs would enable the government to better match its

revenue with expenditure (debt servicing). Hence stabilizing real cost of debt implicitly

amounts to tax smoothing by minimizing future budget constraints, which is key to effective

debt management strategy. In 1983, Italy issued ILBs that successfully helped to fix part of

the country‟s real borrowing costs for a period of 10 years, something which could not be

achieved using nominal debt given the high level of inflation and very low investor

confidence in the market.

To the investors, ILBs minimizes rent-seeking or information search costs that are

associated with inflation risk premia for long term NFRBs. Investors in emerging and

developing economies are not in a position to obtain robust forecasts about average expected

future inflation in order to accurately price the NFRBs due to the volatile nature of actual

inflation. To obtain real returns, they resort to expensive advisory from market agents or

researchers, whose forecasts sometimes town out to be inaccurate. This leaves ILBs as the

best placed assets to anchor inflationary expectations and therefore minimize investor‟s

search costs. Indeed, Shen (1995), Garcia and Rixtel (2007) showed that other assets earlier

perceived to hedge against inflation, such as rollover of short term debt securities, equities,

commodities or even the real estate do not effectively provide investors with fixed long term

yields that are free from inflation risk.

Campbell and Viceira (2002) , while affirming that ILBs are safe asset for long term,

supported the argument that these instruments are truly risk-free since they provide

effective hedging mechanism against two risks; inflation risk and credit (including liquidity)

risk. They are therefore ideal for long term investors and for portfolio diversification,

especially when inflation is quite uncertain. Fischer (1975) also supported this view by

urging potential issuers, both government and private issuers to exploit this market.

3.2 Cash Management Objective of the Issuer (Government)

Effective Cash management is one of the important pillars of a successful Public Debt

management strategy. It has implications on the credibility of the government as an issuer,

can impact greatly on the cost of borrowing especially if the issuer fails to meet obligations

23

when they fall due, and can disrupt financial markets significantly if not managed well.

Therefore whatever instruments the government chooses to use in borrowing, effective cash

management must remain one of the key overriding objective of the debt manager.

Effective cash management contributes to efficient debt management and assists in the

implementation of fiscal and monetary policies. The government debt manager requires

assurance that sufficient cash is available to meet debt obligations as they fall due.

Attempting to meet this basic requirement when cash management practices are inadequate

can result in large idle balances and over-borrowing, with associated negative fiscal

consequences in terms of interest expense. The central bank requires accurate government

cash forecasts to manage banking system liquidity efficiently. Therefore effectiveness of

monetary and fiscal policies relies heavily on successful cash management framework

implemented by a debt manager.

The ILBs have been found to contribute immensely to the effective cash management since

coupon and principal amounts payments are matched with tax revenues collection by the

Government. The government taxes are implicitly indexed to inflation since taxes are

collected in nominal terms. The nominal interest payments on ILBs are anchored on actual

inflation just like tax collections and therefore no mismatch on account of inflation (Price,

1997). To empirically explain this argument, we use a simple econometric model of Ordinary

Least Square to establish the relationship between inflation and ordinary government taxes.

3.2.1. Data and Diagnostic Tests

The study uses Kenya‟s quarterly data on real Gross Domestic Product (GDP), Consumer

Price Index and ordinary Tax Collections for the period 2004 to 2014. Following the

rebasing of the county‟s GDP data series, there was a structural break in 2009 where the new

GDP series begin, which are quite high compared to the period 2004 to 2008. Consequently,

to ensure data quality and to avoid estimating the model with structural breaks, the author

generates new GDP series for the period 2004-2008 using backward GDP forecasting

method also known as backcasting technique. This has introduced consistency in the data,

making it more reliable to use in the estimation. Given the streamlined data, the first step is

conduct basic diagnostic tests including seasonality and the order on integration in order to

24

establish how many times the data series of the variables need to be differenced to achieve

stationarity. The aim is to eliminate noise and spurious results that yield wrong conclusions.

Plotting the data series of the three macro-variables indicate the presence of seasonality in

Tax Collections and the GDP but not in the CPI. For GDP, there was more noise in pre-

rebasing period than in post-rebasing period compared to tax collections data where

periodicity can be observed throughout the period of study (figure 1).

Figure 1: Real GDP, Tax Collections and CPI (Logs)

40,000

80,000

120,000

160,000

200,000

240,000

280,000

04 05 06 07 08 09 10 11 12 13 14

TAXES

500,000

600,000

700,000

800,000

900,000

1,000,000

04 05 06 07 08 09 10 11 12 13 14

RGDP

60

80

100

120

140

160

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

CPI

Source: Generated from the data

In order to minimize complications of periodicity in testing the presence of Unit Roots in the

data series, seasonal adjustment to remove Plotting Real GDP and tax collections data

further confirms seasonality with tend in both the variables (figure 2).

25

Figure 2: Real GDP and Tax Collections

10.5

11.0

11.5

12.0

12.5

13.0

13.2

13.4

13.6

13.8

14.0

04 05 06 07 08 09 10 11 12 13 14

LNGDP LNTAX

Real GDP and Tax Collections

Real GDP (logs)

Tax C

ollec

tions

(Log

s)

Source: Generated from the data

To ensure that we filter noise from data of the two variables, we perform seasonal

adjustment using the International Monetary Fund Census X12 procedure (figure 3)

Figure 3: Seasonally Adjusted Real GDP and Tax Collections Data

13.0

13.2

13.4

13.6

13.8

10.8

11.2

11.6

12.0

12.4

04 05 06 07 08 09 10 11 12 13 14

LNTAX_SA LNGDP_SA

Source: Generated from the data

The time series data is also prone to presence of unit roots (non-stationary). In the event

that the model is estimated without testing for unit roots in all the variables, we run the risk

of obtaining spurious results that in turn lead to wrong conclusions.

26

Using the Augmented Dickey Fuller Test of Unit, the results indicate that the CPI data is

stationary in level at the trend and intercept. The series however become stationary with

first Difference with or without intercept and trend, implying the CPI data is an I(1) process.

Using the same process, the results indicate that after performing two out three tests (with

intercept, trend and intercept, and none), real GDP becomes stationary, implying an I(1)

process at first Difference. The unit root test results of tax collections (LnTax) also indicate

that this variable is an I(1) process.

Table 2: Unit Root Tests based on Seasonally Undjusted Data Variable ADF Test Statistic t-statistic Prob* Lag Length: SIC

D(lnTax) -4.79021 -3.54033** 0.0024 Max (9)

D(lnCPI) -3.90236 -2.93500** 0.0045 Max(9)

D(lnrGDP) -3.82497 -2.94343** 0.0059 Max(9)

** Rejects the Null Hypothesis at the 5% significance level SIC refers to Schwarz Information Criterion The results indicate that the seasonally unadjusted variables became stationary after first difference, confirming an I(1) process.

3.2.2. Model Specification and Results

The simple OLS model estimation is based on Kenya‟s quarterly data on differenced values

of real GDP, CPI and Tax Collections. The model is specified as;

sarGDPCPIcsaTAX _lnln_ln ……………………………………….. (5)

The estimated results of the model without a constant are presented in table 3 as:

Table 3: Summary Results (with a Constant)

Source: Estimated Results

Dependent Variable: LNTAX_SA

Method: Least Squares

Sample: 2004Q1:2014Q4 (44 Observations)

Variable Coefficient Std. Error t-Statistic Prob.

C -10.74549 3.526668 -3.046924 0.0040

(LNGDP_SA) 1.433837 0.343332 4.176245 0.0002

D(LNCPI) 0.656616 0.242366 2.709191 0.0098

R-squared 0.984958 Adjusted R-squared 0.984224

F-statistic 1342.362 Schwarz criterion -2.686173 S.D. dependent var 0.457912 Akaike info criterion -2.807823

Prob(F-statistic) 0.000000 Durbin-Watson stat 1.143835

27

The results indicate the changes in CPI explain up to 65 percent of rate of change in tax

collections in Kenya, implying significant sensitivity of tax collections to inflation pressures.

In addition, changes in the overall economy, measured by real GDP, have huge impact on

the level of tax collected. There is however significant but negative relationship with a

constant. This may mean that in the absence of taxes, the government is likely to default on

its obligations falling due including debt service or liquidate its assets in order to meet its

obligations.

The same model is re-estimated without an intercept using equation (6) to establish the

sensitivity of the two explanatory variables on tax collections and implicitly on the cost

structure of public debt. The results in table 4 show that inflation has even a greater impact

on tax collections.

sarGDPCPIsaTAX _lnln_ln ………………………… (6)

Table 4: Summary Results (no Constant) Dependent Variable: LNTAX_SA Method: Least Squares Sample: 2004Q1 2014Q4 (44 Observations)

Variable Coefficient Std. Error t-Statistic Prob.

D(LNGDP_SA) 0.388657 0.015797 24.60256 0.0000 D(LNCPI) 1.383807 0.046174 29.96934 0.0000

R-squared 0.981552 Adjusted R-squared 0.981113 F-statistic 1342.362 S.D. dependent var 0.457912 Schwarz criterion -2.568068 Akaike info criterion -2.649167 Prob(F-statistic) 0.000000 Durbin-Watson stat 0.911999

Source: Estimated Results

This implies a 1 percent change in the tax collections is explained by a 1.38 percent change in

inflation and 0.39 changes in GDP. In both cases therefore, inflation and GDP are critical on

tax collections and therefore ability of the government to issue and service its debt. It is

therefore in the interest of the government to ensure that inflation remain low in order to

effectively manage its cost of debt.

Kumar and Chander (2012) estimated similar model using the logs of real GDP, Tax

Collections and Whole Sale Price Index annual data for the period 1990-91 to 2012-13 and

found the coefficient on D(WPI) to be 1.06, implying almost a one-to-one relationship.

28

Theny concluded that Inflation Linked Bonds issuance contributed to efficient Cash

Management objective of the Government. Barro (1997) while supporting this view noted

that optimal tax approach to public debt taking into account the Government‟s balance sheet

would always favour issuance of long term inflation-linked bonds. These analyses point to

the fact that tax-smoothening objective has implications on how a debt manager wants to

build an optimal composition of public debt portfolio so that all maturities falling due,

including interest payments and any contingencies are honoured effectively. In other words,

all cash flows relating to the debt portfolio are properly matched with the tax base, leaving

very little exposure to excessive costs and risks by the debt manager. From the investor‟s

perspective, there is likelihood of improved demand and fair pricing of newly issued debt by

the Government if potential investors, especially the buy and hold category like pensions and

insurance sectors know that their income is protected from future inflationary risks through

Inflation-Linked Bonds.

3.3 Inflation-Linked Bonds and Monetary Policy Implementation

Among the key pillars of an effective Public Debt management strategy objectives is the

interaction between debt management strategy policy and other economic policies, implying

policy coordination is very critical. At times, governments and monetary authorities may

misuse these policies to achieve their own objectives. Various studies have shown that some

countries experiencing debt explosion and strong political economy may try to use inflation

as a tool to reduce the real value of their debt and contain it to GDP ratio. Aizenman and

Marion (2009) for instance observed that a government with excess domestic currency

denominated debt may try to use inflation to reduce the real debt burden by running loose

monetary policy regime. The incentive is even more if major holders of this debt are

foreigners. This incentive however disappears if a large proportion of the total debt portfolio

is ILBs and therefore the Government and monetary authorities will take all measures to

contain inflation in order to reduce high interest rates that may accrue on ILBs.

ILBs may also encourage accelerated savings and reduce pressure on consumption, thus

dampening inflationary pressures which monetary policy often seeks to address. These two

arguments show that ILBs contribute to commitment and credibility of the public policy,

especially monetary policy that in turn contributes to price stability.

29

Tobin (1963) argued that a government that issued ILBs would have a superior instrument

for economic control because indexed bonds are closer to physical assets or equities than

conventional bonds. The government and central banks are likely to influence equilibrium

supply price of capital if they chose to use ILBs in the fiscal and monetary operations.

Changes on real interest rates on indexed bonds could signal valuable information on

investments and savings, and ultimately the prospects of economic growth. Policy makers

can also infer information about inflation expectations and credibility of monetary policy

just by observing developments in real yields of ILBs. It is in this spirit that Hetzel (1992)

proposed that the U.S Treasury should issue half of its debt as TIPS and the rest as nominal

debt to help the Federal Reserve in its conduct of monetary policy and enhance Board‟s

credibility on fighting inflation. Since the two sets of bonds trade continuously in the

market, any changes in policy or even a shock on demand and supply would automatically be

reflected in prices/yields of these bonds. Therefore the dynamics in the yield spread of the

two bonds provide current measure of inflation expectations by the public.

Kapur (1980) views indexation as a favourable policy choice for newly liberalized, less

developed economies. It mitigates potentially adverse short-run effects of dealing with

inflation shocks and therefore enables the country to remain on course for reforms,

especially in adverse economic developments. Indexation however succeeds if it is supported

other policies that effectively manage inflation, a common phenomenon developing markets.

Otherwise indexation alone will lead to instability, compounding the inflationary problems

in such economies.

Many central banks globally use information about inflation expectations to assess their

credibility towards discharging their core mandate, which is price stability. Consequently,

monetary authorities undertake appropriate monetary policy actions where necessary to

achieve and sustain credibility. To extract any meaningful information from the market to

aid monetary policy formulation, the bonds market must reach a critical mass in terms of

liquidity so that changes in the yield spread or breakeven inflation rate (difference between

real yield on ILB and nominal yield on NFRB of similar maturity) will signal change in

average inflation expectations of market participants over the residual maturity of the

bonds. This however assumes that inflation risk premium and liquidity premium remain

insignificant. Shen (1995) indeed concluded that without information on the real yield, it is

30

difficult for policymakers to know if change in nominal yield reflects change in inflation

outlook or is just the change in real yield. One however needs to be cautious in interpreting

the behaviour of the breakeven inflation rate (BEIR) is it may be mainly driven by liquidity

premium since ILBs are largely illiquid due to the nature of investors who purchase them –

pensions and insurance firms who buy and hold to maturity. Garcia and Rixtel (2005) guide

that for monetary policy purposes; it would be useful to focus on the changes rather the

levels of BEIR when trying to infer about long term inflation expectations. India uses regular

issuance of ILBs across a wide maturity spectrum to extract information about inflationary

expectations across the term structure, hence supporting monetary policy formulation by the

Reserve Bank of India.

At the overall macroeconomic policies level, supporters of indexation including Jevons,

Marshall, Irving Fisher, and even Milton Friedman argued that comprehensive indexation

could effectively modulate business cycles and reduce unemployment costs of policies to

stabilize the price level. This arises when as a result of rigidities, real wages and other factor

costs tend to fluctuate counter-cyclically with inflation, thus increasing the amplitudes of

business cycles.

3.4 Inflation-Linked Bonds and Capital Markets Development

Development of stable and efficient domestic financial markets is one of the secondary

strategic goals of a Public Debt Management Strategy. Stable and efficient domestic capital

markets not only provide reliable funding needs for both government and private sector, but

also acts as a shock absorber to external shocks and provides critical information to

monetary policy formulation and implementation.

British economist Joseph Lowe (1822) in supporting indexation of government bonds wrote

that indexed bonds could help development of capital markets through lowering risk and

improving marketability of these securities. Stanley Fischer (1983a) also noted that

“Governments in inflationary difficulties issue indexed bonds and those that can do it, do

not”. Indexed bonds have proven very useful in countries with nascent financial markets or

those economies experiencing inflation problem and have not established credible monetary

policy. In fact, the ILBs were very effective in raising money for government and restoring

31

sanity in financial markets in countries experiencing hyperinflation situations. Such

countries include Argentina, Brazil, Turkey and Chile, Hungary, with Israel using ILBs to

prevent collapse of its long term capital markets.

Jud (1978) observed that debt indexation contributed greatly in promoting the growth and