Languages

Pages

Legal

Firstcall India Equity Advisors Pvt Ltd 1

Hindustan Unilever Limited (HUL)

BUY Target Price: Rs.327.00

CMP: Rs.282.95 Market Cap. : Rs.617085.66mn.

Date: November 2, 2009

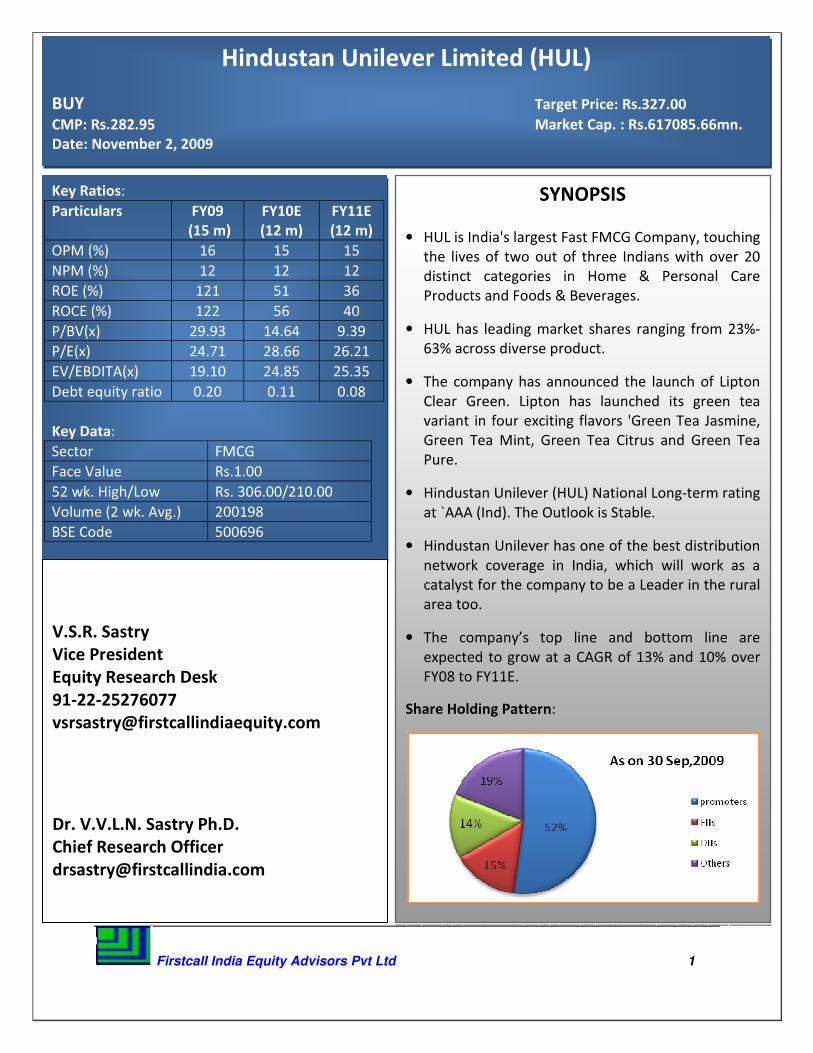

Key Ratios:

Particulars FY09

(15 m)

FY10E

(12 m)

FY11E

(12 m)

OPM (%) 16 15 15

NPM (%) 12 12 12

ROE (%) 121 51 36

ROCE (%) 122 56 40

P/BV(x) 29.93 14.64 9.39

P/E(x) 24.71 28.66 26.21

EV/EBDITA(x) 19.10 24.85 25.35

Debt equity ratio 0.20 0.11 0.08

Key Data:

Sector FMCG

Face Value Rs.1.00

52 wk. High/Low Rs. 306.00/210.00

Volume (2 wk. Avg.) 200198

BSE Code 500696

SYNOPSIS

• HUL is India's largest Fast FMCG Company, touching

the lives of two out of three Indians with over 20

distinct categories in Home & Personal Care

Products and Foods & Beverages.

• HUL has leading market shares ranging from 23%-

63% across diverse product.

• The company has announced the launch of Lipton

Clear Green. Lipton has launched its green tea

variant in four exciting flavors 'Green Tea Jasmine,

Green Tea Mint, Green Tea Citrus and Green Tea

Pure.

• Hindustan Unilever (HUL) National Long-term rating

at `AAA (Ind). The Outlook is Stable.

• Hindustan Unilever has one of the best distribution

network coverage in India, which will work as a

catalyst for the company to be a Leader in the rural

area too.

• The company’s top line and bottom line are

expected to grow at a CAGR of 13% and 10% over

FY08 to FY11E.

Share Holding Pattern:

V.S.R. Sastry

Vice President

Equity Research Desk

91-22-25276077

Dr. V.V.L.N. Sastry Ph.D.

Chief Research Officer

Firstcall India Equity Advisors Pvt Ltd 2

Table of Content

Content Page No.

1. Investment Highlights 03

2. Peer Group Comparison 07

3. Key Concerns 07

4. Financials 08

5. Charts & Graph 10

6. Outlook and Conclusion 12

7. Industry Overview 13

Firstcall India Equity Advisors Pvt Ltd 3

Investment Highlights • Result Updates (Q2FY10)

For the Second quarter, the top line of the company increased 4%YoY and stood at

Rs.42692.30mn against Rs.41109.10mn of the same period of the last year. The bottom

line of the company for the quarter stood at Rs.4285.30mn from Rs.5466.10mn of the

corresponding period of the previous year i.e. a decrease of 22%YoY.

EPS of the company for the quarter stood at Rs.1.96 for equity share of Rs.1.00 each.

Firstcall India Equity Advisors Pvt Ltd 4

Expenditure for the quarter stood at Rs.37524.50mn, which is around 9% higher than

the corresponding period of the previous year. Raw material cost of the company for

the quarter accounts for 39% of the sales of the company and stood at Rs.16539.50mn.

Employee cost stood at Rs.2357.90mn from Rs.2294.70mn. and accounts for 6% of the

revenue of the company for the quarter i.e., an increase of 3%YoY.

OPM and NPM for the quarter stood at 13% and 10% respectively from 16% and 13%

respectively of the same period of the last year.

Firstcall India Equity Advisors Pvt Ltd 5

• Segment-Wise revenue for the quarter

Segment Revenue (Rs. million)

Soaps & Detergents 20,036.90

Personal Products 11,901.80

Beverages 5,215.80

Export 2,270.00

Processed Foods 1,739.20

Ice Creams 503.6

Others 1,070.50

Total 42,737.80

Firstcall India Equity Advisors Pvt Ltd 6

• Hindustan Unilever Ltd. Sings an Amicable Settlement for Erstwhile Sewree Factory

Issue

Hindustan Unilever Ltd. and the Hindustan Lever Employee Union, the Union

representing erstwhile workers at Sewree factory have signed an amicable settlement

with regard to all the pending issues and cases pertaining to the erstwhile undertaking

at Sewree including closure of the factory. The settlement will benefit about 800

workers. The settlement was signed by the parties in the presence of Kavita Gupta, the

Labour Secretary, Government of Maharashtra.

As per the settlement agreed, the workers of the erstwhile Sewri factory will receive the

VRS offered at the time of closure of the factory. The VRS included last drawn salary till

the due date of retirement. The Sewree factory was closed on July 26, 2006 in line with

the order passed by the Labour Commissioner of Maharashtra.

• Hindustan Unilever Ltd. Announces the Launch of Lipton Clear Green

The company has announced the launch of Lipton Clear Green. Lipton has launched its

green tea variant in four exciting flavors 'Green Tea Jasmine, Green Tea Mint, Green Tea

Citrus and Green Tea Pure. Encased in an attractive green color packaging, the all-new

Lipton Clear Green tea is a natural source of anti-oxidants. These will be available in

teabags across India in leading supermarkets. Lipton Clear Green combines the

goodness of the green tea's flavonoid antioxidants (AOX) with the purifying effect of

water to help cleanse your body naturally.

• Rating

Credit rating agency, Fitch Ratings has affirmed India-based Hindustan Unilever (HUL)

National Long-term rating at `AAA (Ind). The Outlook is Stable. The ratings affirmation is

underpinned by HUL`s low business risk and strong financial risk profile. The ratings also

factor in the company`s consistently zero net debt status, positive free cash flows, and

status as the largest Indian FMCG company. HUL has leading market shares ranging from

23%-63% across diverse product.

• HUL postpones Capgemini stake sale by a year

The company has decided to defer its plan of divesting 49% stake in its BPO unit to

Capgemini SA by March 2010. The company had earlier scheduled to acquire the stake

by March 2009. It is learnt that the maker of Lifebuoy soaps and Surf detergent has

amended the shareholder's agreement with Capgemini SA allowing it to exit a year later

than originally planned.

Firstcall India Equity Advisors Pvt Ltd 7

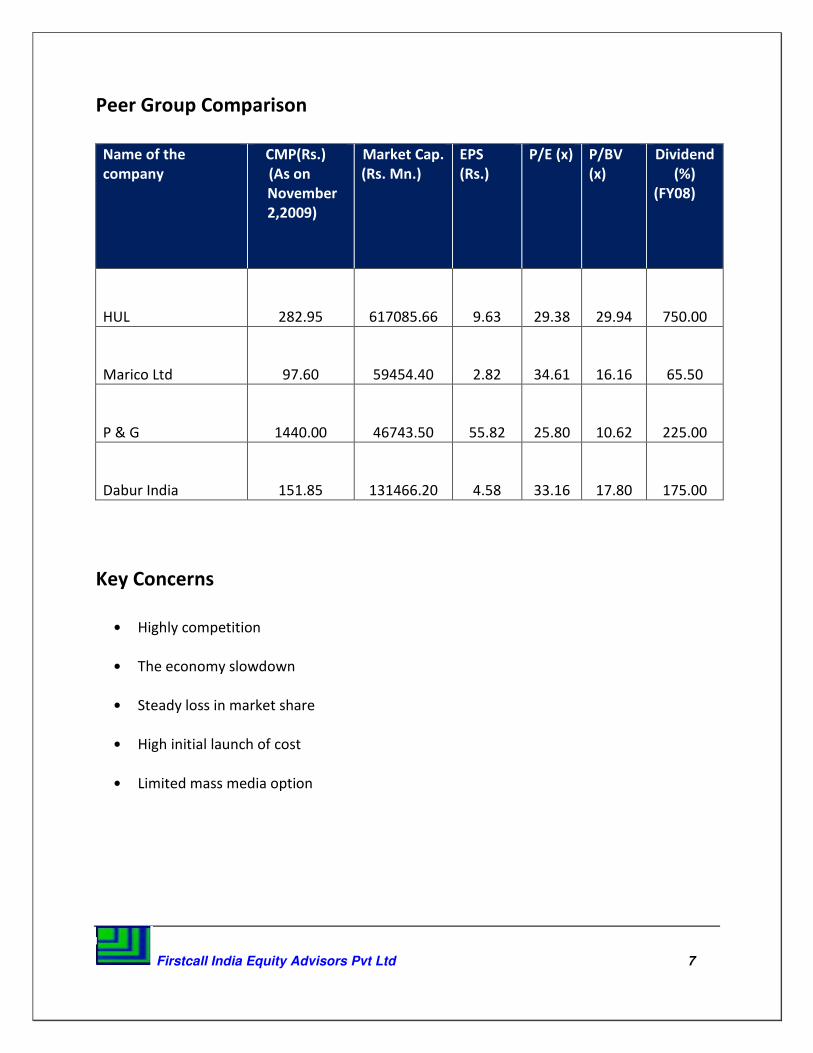

Peer Group Comparison

Name of the

company

CMP(Rs.)

(As on

November

2,2009)

Market Cap.

(Rs. Mn.)

EPS

(Rs.)

P/E (x) P/BV

(x)

Dividend

(%)

(FY08)

HUL 282.95 617085.66 9.63 29.38 29.94 750.00

Marico Ltd 97.60 59454.40 2.82 34.61 16.16 65.50

P & G 1440.00 46743.50 55.82 25.80 10.62 225.00

Dabur India 151.85 131466.20 4.58 33.16 17.80 175.00

Key Concerns

• Highly competition

• The economy slowdown

• Steady loss in market share

• High initial launch of cost

• Limited mass media option

Firstcall India Equity Advisors Pvt Ltd 8

Financials

Results Update

12 months ended Profit and Loss A/C (Standalone):

Value(Rs. in million) CY07A *FY09A FY10E FY11E

Description 12m 15m 12m 12m

Net Sales 137,177.50 206,015.60 181074.30 199181.73

Other Income 4,626.80 2,055.50 2096.61 2138.54

Total Income 141,804.30 208,071.10 183170.91 201320.27

Expenditure -118,320.50 -175,776.70 -155361.75 -170897.92

Operating Profit 23,483.80 32,294.40 27809.16 30422.35

Interest -255 -253.2 -167.09 -183.80

Gross Profit 23,228.80 32,041.20 27642.07 30238.55

Depreciation -1,383.60 -1,953.00 -1701.83 -1872.01

Profit before Tax 21,845.20 30,088.20 25940.24 28366.54

Tax -4,154.60 -5,035.60 -4409.84 -4822.31

Profit after Tax 17,690.60 25,052.60 21530.40 23544.22

Extraordinary items 1,564.10 -88.1 - -

Net Profit 19,254.70 24,964.50 21530.40 23544.22

Equity Capital 2,177.50 2,179.90 2180.90 2180.90

Reserves 12,208.20 18,428.50 39958.90 63503.12

EPS 8.84 11.45 9.87 10.80

Firstcall India Equity Advisors Pvt Ltd 9

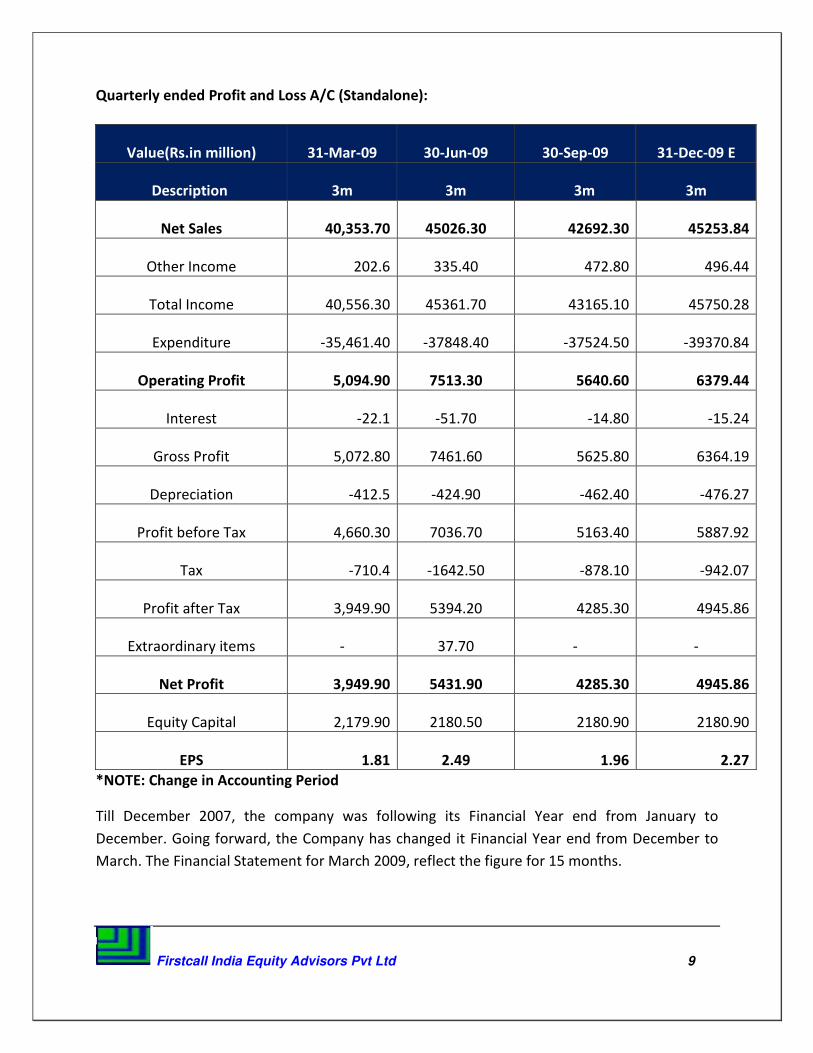

Quarterly ended Profit and Loss A/C (Standalone):

Value(Rs.in million) 31-Mar-09 30-Jun-09 30-Sep-09 31-Dec-09 E

Description 3m 3m 3m 3m

Net Sales 40,353.70 45026.30 42692.30 45253.84

Other Income 202.6 335.40 472.80 496.44

Total Income 40,556.30 45361.70 43165.10 45750.28

Expenditure -35,461.40 -37848.40 -37524.50 -39370.84

Operating Profit 5,094.90 7513.30 5640.60 6379.44

Interest -22.1 -51.70 -14.80 -15.24

Gross Profit 5,072.80 7461.60 5625.80 6364.19

Depreciation -412.5 -424.90 -462.40 -476.27

Profit before Tax 4,660.30 7036.70 5163.40 5887.92

Tax -710.4 -1642.50 -878.10 -942.07

Profit after Tax 3,949.90 5394.20 4285.30 4945.86

Extraordinary items - 37.70 - -

Net Profit 3,949.90 5431.90 4285.30 4945.86

Equity Capital 2,179.90 2180.50 2180.90 2180.90

EPS 1.81 2.49 1.96 2.27

*NOTE: Change in Accounting Period

Till December 2007, the company was following its Financial Year end from January to

December. Going forward, the Company has changed it Financial Year end from December to

March. The Financial Statement for March 2009, reflect the figure for 15 months.

Firstcall India Equity Advisors Pvt Ltd 10

Charts

• Net sales & PAT

• P/E Ratio (x)

Firstcall India Equity Advisors Pvt Ltd 11

• P/BV (X)

• EV/EBITDA(X)

Firstcall India Equity Advisors Pvt Ltd 12

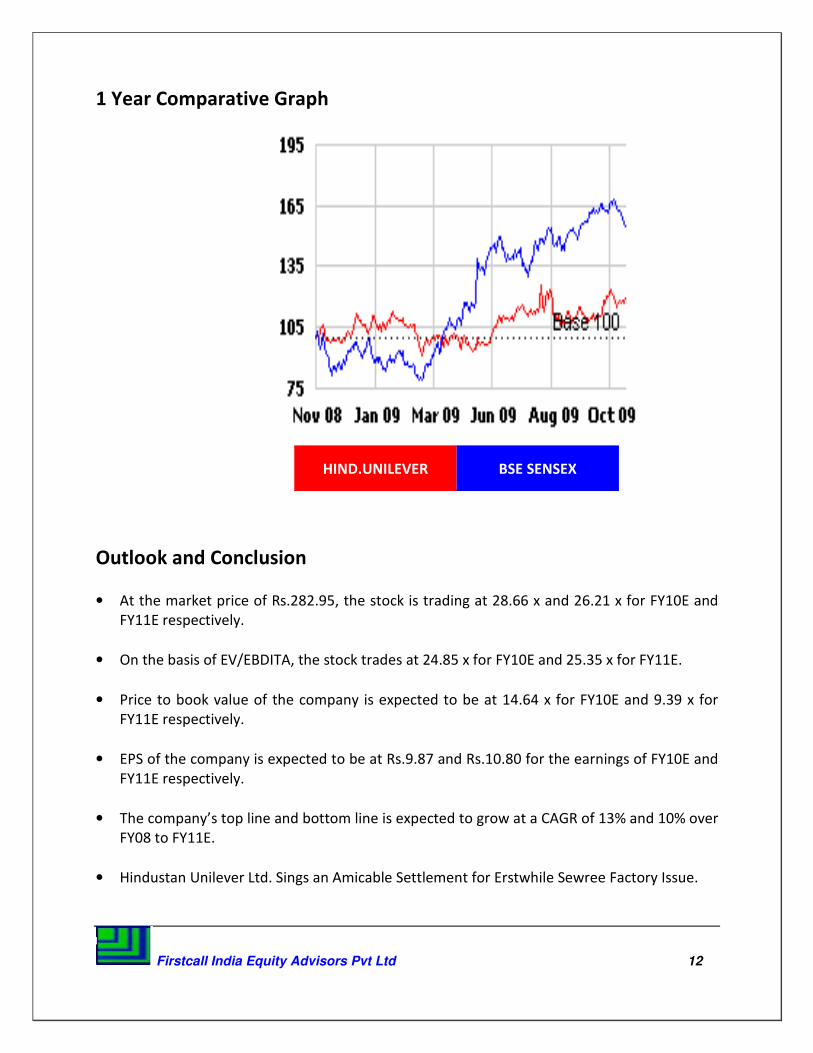

1 Year Comparative Graph

Outlook and Conclusion

• At the market price of Rs.282.95, the stock is trading at 28.66 x and 26.21 x for FY10E and

FY11E respectively.

• On the basis of EV/EBDITA, the stock trades at 24.85 x for FY10E and 25.35 x for FY11E.

• Price to book value of the company is expected to be at 14.64 x for FY10E and 9.39 x for

FY11E respectively.

• EPS of the company is expected to be at Rs.9.87 and Rs.10.80 for the earnings of FY10E and

FY11E respectively.

• The company’s top line and bottom line is expected to grow at a CAGR of 13% and 10% over

FY08 to FY11E.

• Hindustan Unilever Ltd. Sings an Amicable Settlement for Erstwhile Sewree Factory Issue.

HIND.UNILEVER BSE SENSEX

Firstcall India Equity Advisors Pvt Ltd 13

• The company has announced the launch of Lipton Clear Green. Lipton has launched its

green tea variant in four exciting flavors 'Green Tea Jasmine, Green Tea Mint, Green Tea

Citrus and Green Tea Pure.

• Credit rating agency, Fitch Ratings has affirmed India-based Hindustan Unilever (HUL)

National Long-term rating at `AAA (Ind). The Outlook is Stable.

• The company has decided to defer its plan of divesting 49% stake in its BPO unit to

Capgemini SA by March 2010.

• We recommend ‘BUY’ this stock with a target price of Rs.327.00 for long term perspective.

Industry Overview

Fast Moving Consumer Goods (FMCG) goods are popularly named as consumer packaged

goods. Items in this category include all consumables (other than groceries/pulses) people buy

at regular intervals. The most common in the list are toilet soaps, detergents, shampoos,

toothpaste, shaving products, shoe polish, packaged foodstuff, and household accessories and

extends to certain electronic goods. These items are meant for daily of frequent consumption

and have a high return.

A major portion of the monthly budget of each household is reserved for FMCG products. The

volume of money circulated in the economy against FMCG products is very high, as the number

of products the consumer use is very high. Competition in the FMCG sector is very high

resulting in high pressure on margins.

FMCG companies maintain intense distribution network. Companies spend a large portion of

their budget on maintaining distribution networks. New entrants who wish to bring their

products in the national level need to invest huge sums of money on promoting brands.

Manufacturing can be outsourced. A recent phenomenon in the sector was entry of

multinationals and cheaper imports. Also the market is more pressurized with presence of local

players in rural areas and state brands.

Scope of the Sector

The Indian FMCG sector with a market size of US$13.1 billion is the fourth largest sector in the

economy. A well-established distribution network, intense competition between the organized

and unorganized segments characterizes the sector. FMCG Sector is expected to grow by over

60% by 2010. That will translate into an annual growth of 10% over a 5-year period. It has been

estimated that FMCG sector will rise from around Rs 56,500 crores in 2005 to Rs 92,100 crores

Firstcall India Equity Advisors Pvt Ltd 14

in 2010. Hair care, household care, male grooming, female hygiene, and the chocolates and

confectionery categories are estimated to be the fastest growing segments, says an HSBC

report. Though the sector witnessed a slower growth in 2002-2004, it has been able to make a

fine recovery since then.

For example, Hindustan Levers Limited (HUL) has shown a healthy growth in the last quarter.

An estimated double-digit growth over the next few years shows that the good times are likely

to continue.

Growth Prospects

With the presence of 12.2% of the world population in the villages of India, the Indian rural

FMCG market is something no one can overlook. Increased focus on farm sector will boost rural

incomes, hence providing better growth prospects to the FMCG companies. Better

infrastructure facilities will improve their supply chain. FMCG sector is also likely to benefit

from growing demand in the market. Because of the low per capita consumption for almost all

the products in the country, FMCG companies have immense possibilities for growth. And if the

companies are able to change the mindset of the consumers, i.e. if they are able to take the

consumers to branded products and offer new generation products, they would be able to

generate higher growth in the near future. It is expected that the rural income will rise in 2007,

boosting purchasing power in the countryside. However, the demand in urban areas would be

the key growth driver over the long term. Also, increase in the urban population, along with

increase in income levels and the availability of new categories, would help the urban areas

maintain their position in terms of consumption. At present, urban India accounts for 66% of

total FMCG consumption, with rural India accounting for the remaining 34%. However, rural

India accounts for more than 40% consumption in major FMCG categories such as personal

care, fabric care, and hot beverages. In urban areas, home and personal care category,

including skin care, household care and feminine hygiene, will keep growing at relatively

attractive rates. Within the foods segment, it is estimated that processed foods, bakery, and

dairy are long-term growth categories in both rural and urban areas.

Indian Competitiveness and Comparison with the World Markets

The following factors make India a competitive player in FMCG sector:

• Availability of raw materials

Because of the diverse agro-climatic conditions in India, there is a large raw material base

suitable for food processing industries. India is the largest producer of livestock, milk,

sugarcane, coconut, spices and cashew and is the second largest producer of rice, wheat and

fruits &vegetables. India also produces caustic soda and soda ash, which are required for the

production of soaps and detergents. The availability of these raw materials gives India the

location advantage.

Firstcall India Equity Advisors Pvt Ltd 15

• Labor cost comparison

Low cost labor gives India a competitive advantage. India's labor cost is amongst the lowest in

the world, after China & Indonesia. Low labor costs give the advantage of low cost of

production. Many MNC's have established their plants in India to outsource for domestic and

export markets.

• resence across value chain

Indian companies have their presence across the value chain of FMCG sector, right from the

supply of raw materials to packaged goods in the food-processing sector. This brings India a

more cost competitive advantage. For example, Amul supplies milk as well as dairy products

like cheese, butter, etc.

_________________________________________________________

Disclaimer:

This document prepared by our research analysts does not constitute an offer or solicitation

for the purchase or sale of any financial instrument or as an official confirmation of any

transaction. The information contained herein is from publicly available data or other

sources believed to be reliable but we do not represent that it is accurate or complete and it

should not be relied on as such. Firstcall India Equity Advisors Pvt. Ltd. or any of it’s

affiliates shall not be in any way responsible for any loss or damage that may arise to any

person from any inadvertent error in the information contained in this report. This document

is provide for assistance only and is not intended to be and must not alone be taken as the

basis for an investment decision.

Firstcall India Equity Advisors Pvt Ltd 16

Firstcall India Equity Research: Email – [email protected]

B. Harikrishna Banking

B. Prathap IT

A. Rajesh Babu FMCG

C.V.S.L.Kameswari Pharma

U. Janaki Rao Capital Goods

E. Swethalatha Oil & Gas

D. Ashakirankumar Automobile

Rachna Twari Diversified

Kavita Singh Diversified

Nimesh Gada Diversified

Priya Shetty Diversified

Tarang Pawar Diversified

Neelam Dubey Diversified

Firstcall India also provides

Firstcall India Equity Advisors Pvt.Ltd focuses on, IPO’s, QIP’s, F.P.O’s, Takeover

Offers, Offer for Sale and Buy Back Offerings.

Corporate Finance Offerings include Foreign Currency Loan Syndications,

Placement of Equity / Debt with multilateral organizations, Short Term Funds

Management Debt & Equity, Working Capital Limits, Equity & Debt

Syndications and Structured Deals.

Corporate Advisory Offerings include Mergers & Acquisitions (domestic and

cross-border), divestitures, spin-offs, valuation of business, corporate

Restructuring-Capital and Debt, Turnkey Corporate Revival – Planning &

Execution, Project Financing, Venture capital, Private Equity and Financial

Joint Ventures

Firstcall India also provides Financial Advisory services with respect to raising

of capital through FCCBs, GDRs, ADRs and listing of the same on International

Stock Exchanges namely AIMs, Luxembourg, Singapore Stock Exchanges and

other international stock exchanges.

For Further Details Contact:

3rd Floor, Sankalp, The Bureau, Dr.R.C.Marg, Chembur, Mumbai 400 071

Tel.: 022-2527 2510/2527 6077/25276089 Telefax: 022-25276089

E-mail: [email protected]

www.firstcallindiaequity.com

Top Related