Languages

Pages

Legal

Hers Institute

2016

Budgeting

• The Purpose of the

Budgeting Process

• Budget Types

• Approaches to

Budgeting

• The Budget Process

This Session Will Include a

Discussion of:

Why

Budget?

• It is a FINANCIAL MAP of the institution’s strategic plan -- guides an institution on its journey in pursuit of its mission.

• Detailed RESOURCE ALLOCATION PLAN to outline how the institution’s resources will be utilized to achieve institutional goals.

• A FORECAST of the institution’s financial picture at some point in the future.

• A CONTRACT between management and the operating units charged with carrying out plans for the institution.

• Used as a management tool to control or achieve ACCOUNTABILITY from budget managers.

Why do we participate in the budget

process? What is a budget?

Budget

Types

• Operating Budget

• Capital Projects Budget

• Restricted/Special Projects Budget

What are the types of the budgets used

by institutions?

• The most commonly known and discussed

budget type.

• The budget that captures the operating revenues

that are used to finance current expenses (the

vast majority of revenues collected during a

period are expended during that same period;

unexpended revenues are used as reserves).

• Operating budgets capture the “day to day”

expenses incurred by the institution to achieve

its mission.

• EVERYONE CAN CONTROL

SOME PORTION OF THIS

BUDGET

Operating

Budget

Operating

Budget

• Tuition and Fees

• Governmental

– Appropriations; Grants &

Contracts (Direct & Indirect

Cost)

– Federal, State, and Local

• Gifts

• Endowment Income

• Auxiliary Enterprises

• Patient Services

• Other

The Operating Budget

(Revenue Sources)

Operating

Budget

The Operating Budget (Expenses)

Expenses are displayed using either the natural classification or functional classification (programmatic classification).

Natural Classification – expenses are identified by type versus purpose (salaries, benefits, travel and supplies).

Functional (Programmatic) Classification - expenses are organized by the nature of the activity the expenses support (instruction, academic support, student support, and institutional, etc.,)

Most Operating Budgets contain RESERVES for future capital work

Capital

Projects

Budget

• This budget maps out the finances for

construction and other acquisition plans

related to a campus’s physical facilities

and infrastructure.

• It addresses the revenues, expenses and

reserves much like the operating budget.

• The revenue sources might include:

tuition and fees; governmental

appropriations; auxiliary revenues; or

gifts.

• Additional financing considerations

include the use of reserve or borrowed

funds.

Capital

Projects

Budget

Reserve funds – reserve funds are funds that

have been accumulated through savings or

have been funded as a part of the operating

budget. Institutions often specify that a

certain portion of an annual operating budget

be set aside to cover cost that will be incurred

in future periods.

Borrowed funds – borrowed funds are either

construction loans or long-term bonds that are

used to finance the acquisition or construction

of new facilities, major equipment, or

infrastructure upgrades or additions. Colleges

and universities typically use tax-exempt

bonds to fund capital expansion.

Restricted/

Special

Projects

Budgets

Many institutions prepare budgets

focused only on restricted funds. In these

instances resources are provided by

external parties and carry stipulations

about how the resources can be

expended. Restricted budgets indicate

resources and expenses for specific

activities.

Examples include: endowment income

for scholarship or library funds; federal

grant programs (Title III, Upward Bound,

etc.,); externally funded research

projects.

Approaches

to Budgets

• Incremental Budgeting

• Zero-Based Budgeting

• Performance Based Budgeting

• Formula Budgeting

• Responsibility Center

Budgeting

• Initiative Based Budgeting

• Hybrid Model

Incremental

Budgeting

Using incremental budgeting each program or activity’s budget is increased by a specified percentage. The theory supporting the use of incremental budgeting is that the basic aspects of programs and activities does not change significantly from year to year.

At some institutions differential factors are use for various organizational segments. For example, once a certain category of expenses has been budgeted for (salaries, utilities, debt service, etc.,) the institution may apply one percentage increase for academic units and a different increase for non-academic units.

Strengths – most efficient approach. It is simple to implement, more controllable, adaptable and more flexible because it does not include an emphasis on analysis.

Weaknesses – maintains the status quo and does not integrate the impact of planning assumptions or decisions. It does not take into consideration what is being accomplished through the base budget and it avoids the question of whether there are more optimal resource allocations.

Most widely used budgeting technique.

Zero-

Based

Budgeting

(ZBB)

This budget approach assumes no budget from the prior years; instead, each year’s budget begins at a base zero. Each budget unit evaluates its goals and objectives and justifies its activities in terms of the benefits of its activity and the consequences if it were not performed.

A decision package is developed for each activity which includes a description of the activity, a definition of alternate levels of activity, performance measures, and the costs and benefits.

Strengths – the review of the decision packages provides decision makers with a better understanding of the institutional activities than the other budget techniques.

Weaknesses – it does not assume any budget history; it does not recognize commitments that are continuous (tenured faculty members, senior administrators); consumes an enormous amount of time and generates massive volumes of paperwork.

Formula

Based

Budgeting

Primarily used by public institutions, formula based budgeting is

a procedure for estimating resource requirements through the

relationship between program demand and program cost. These

relationships are most often expressed as mathematical formulas

that can be as simple as “student-faculty ratio,” or as complicated

as an array of cost per student credit hour by discipline for

multiple levels of instruction .

The basis for budget formulas can be historical data, projected

trends, or negotiated parameters to provide desired levels of

funding.

Strengths – the quantitative nature of most budget formulas

gives them the appearance of an unbiased distribution of

resources; in a stable economic environment it helps reduce

uncertainty by providing a mechanism for predicting future

resource needs.

Weaknesses – because it often focuses on historical data it can

discourage new programs or revisions to existing programs;

given its focus on quantitative data it can suffer from the same

faults identified in incremental budgeting; they can have an

unequal or even negative impact on participating institutions.

Performance

Based

Budgeting

(PBB)

Performance based budgeting places its focus on outcomes. Specific outcomes are defined in both quantitative and qualitative measures. Explicit indicators of input-output relationships or indexes relating resources to outcomes are defined. Goals are specified in terms of performance measures (desired input-output ratios).

The development of performance measures typically flows from the state to the institution and frequently may not reflect an understanding of the factors influencing the measure.

Strengths – provides a mechanism for allocating supplemental resources when measures are achieved.

Weaknesses – performance measures at high levels of program aggregation are not easily linked with organization divisions and departments - the structure used to allocate resources on most campuses.

Responsibility

Center

Budgeting

(RCB)

“Every Tub

On Its

Bottom”

Also know as “cost center budgeting,” “profit center

budgeting,” “revenue responsibility budgeting,” is the

technique where units manage the revenues that they

generate. Rather than a central focus on budgetary

control, the emphasis shifts to program performance.

Under RCB, schools and colleges and other organizational

units become revenue centers, cost centers, or a

combination of the two. Based on the activity occurring

within the unit, all revenue that it generates are assigned

to it, including tuition & fees, research grants and

contracts, gifts, and endowment income.

Strengths – this technique helps communicate the

message that academic decisions have financial

consequences.

Weaknesses – this technique is accused of focusing too

much attention on the bottom line versus academic quality

or other priorities; a lack of coherence between planning

and budgeting may evolve as a result of unit autonomy;

may encourage competition/duplication between schools;

institutional priorities may be ignored; difficulty in

developing formula for assigning central costs.

Initiative

Based

Budgeting

(IBB)

This technique is considered a structural approach to the establishment of a resource pool for funding new initiatives or enhancing higher-priority activities.

IBB provides the side benefit of assuring that units conduct a review of the existing activities to make certain that they remain productive.

Example: an institution may require that all units reduce their base budgets by 2% to fund a pool. Once funded there are many ways to reallocate the savings but most include a proposal process. All units seeking to obtain funds from the pool are required to submit a proposal identifying the proposed activities, the institutional priority that the activities satisfy, and the amount requested.

It is important to note that IBB is not a technique that can be practiced indefinitely.

Hybrid

Model

• Incremental base budget, with new resources allocated using performance, formula, or initiative models.

• Responsibility centered budget, with a significant tax to be re-allocated on an initiative model.

• Zero-based budget for 1/3 of units each year so that every 3 years every unit is subject to this practice. For 2/3 of units not using zero-based budget in a given year, incremental model is used.

This approach combines several of the

methodologies we’ve discussed in order to

take advantage of strengths and minimize

weaknesses. For example,

The

Budget

Process

• Centralized versus Decentralized

Budgeting

• The Budget Cycle

• Factors Affecting the Budget

Process

• Critical Steps in the Budget

Process

Centralized vs. Decentralized Budgeting (Smaller institutions = centralized; larger institutions typically = decentralized)

Practice Centralized Decentralized

Budgets are estimates, subject to change President, VPs make changes Deans/ dept. heads

Faculty Hiring Decisions Provost approves Dean/ dept. heads

Level of Budgetary Control At object level At fund level

Capital Investment Funded from central reserve Funding at school, dept. level

Recruitment Packages Funded from central reserve Funding from school’s reserves

Contingency Reserves Held centrally Deans/dept. heads planning for contingencies

Budget Reductions Decisions Pres, VPs make changes Deans/dept. heads make changes

Priority Setting Centrally driven School driven

Annual Giving/Fundraising Central effort Coordinated centrally, achieved in schools

Faculty/Staff Positions Managed centrally Managed at dean’s level

Faculty/Staff Vacancy Savings Reverts centrally Retained by dean/department head

Year-end Surplus/Deficit Reverts centrally Retained by dean/department head

F&A/Local Funds Managed centrally Managed at dean’s level

The

Budget

Cycle

Operating Budget Cycle

The operating budget cycle runs from the beginning of the

initial research phase and analysis through the completion

of the audited financial statements. Once the audited

financial statements have been completed an analysis is

typically completed to determine the accuracy of the

original budget projections.

Timeline: Typically 12- 24 months, although the timeline

can be longer for public institutions.

Capital Budget Cycle

Capital budget cycles are typically longer than the

operating budget cycle due to the types of projects

covered by these budgets. This budget cycle begins with

the conception of the capital project and runs until the

final product is placed into service.

Timeline: It is customary for capital budgets to span

multiple years (2 – 6 years).

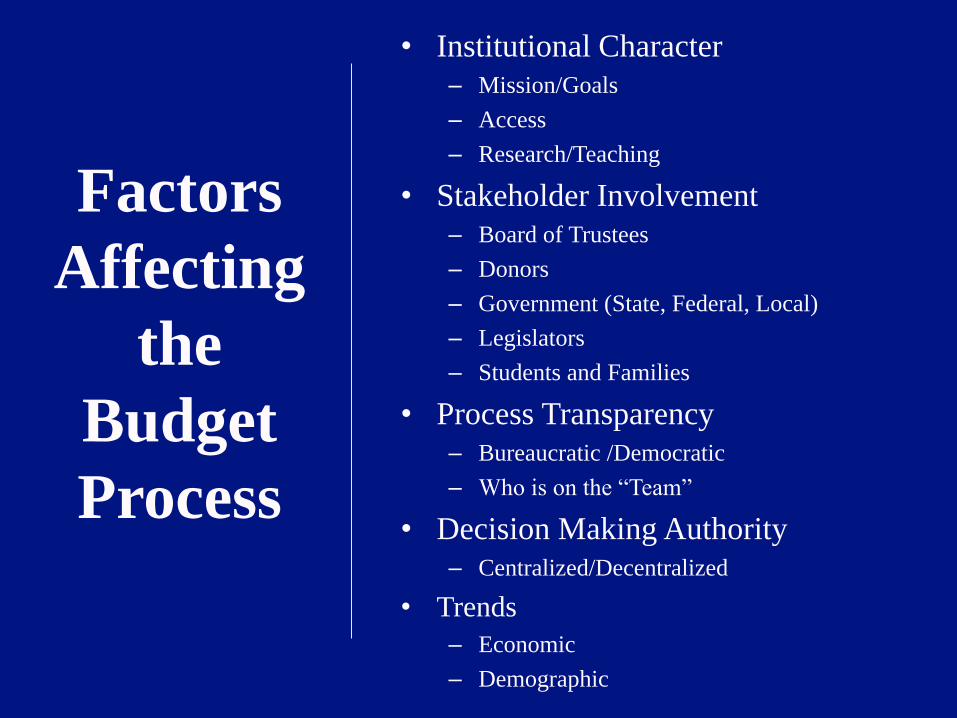

Factors

Affecting

the

Budget

Process

• Institutional Character

– Mission/Goals

– Access

– Research/Teaching

• Stakeholder Involvement

– Board of Trustees

– Donors

– Government (State, Federal, Local)

– Legislators

– Students and Families

• Process Transparency

– Bureaucratic /Democratic

– Who is on the “Team”

• Decision Making Authority

– Centralized/Decentralized

• Trends

– Economic

– Demographic

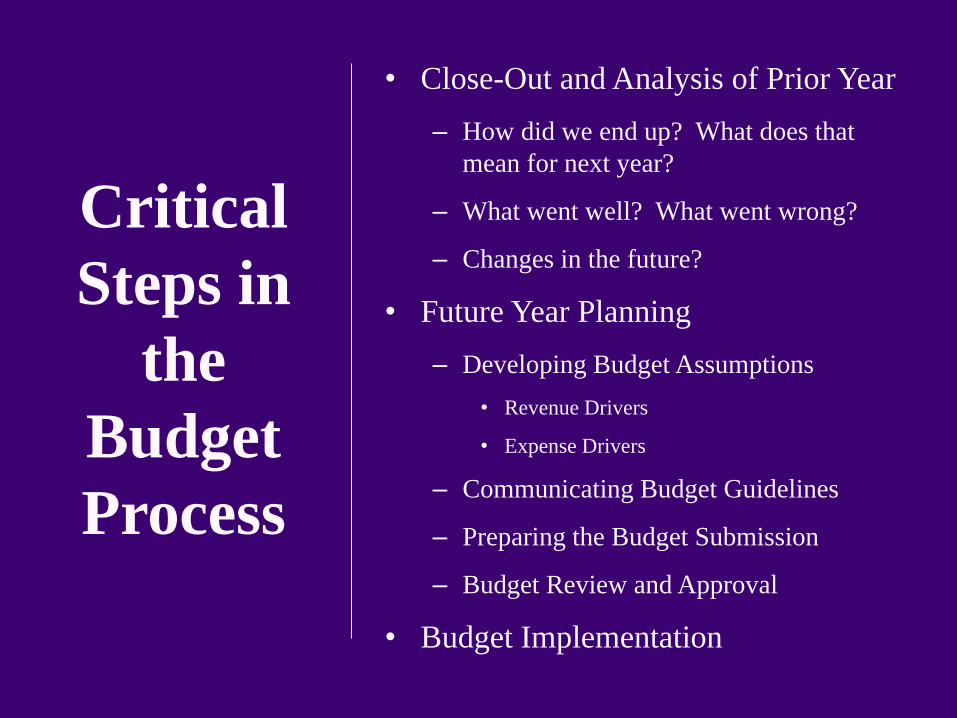

Critical

Steps in

the

Budget

Process

• Close-Out and Analysis of Prior Year

– How did we end up? What does that

mean for next year?

– What went well? What went wrong?

– Changes in the future?

• Future Year Planning

– Developing Budget Assumptions

• Revenue Drivers

• Expense Drivers

– Communicating Budget Guidelines

– Preparing the Budget Submission

– Budget Review and Approval

• Budget Implementation

Research

Definitions

Two types of research funding:

Sponsored research (external funds;

deliverables)

Non-sponsored research (gifts and

internal funds)

Two types of research costs:

Direct Costs – identified specifically

with a particular sponsored project,

relatively easily with a high degree of

accuracy.

Facilities and Administrative (F&A)

Costs (indirect or overhead costs) –

incurred for common/joint objectives,

not identified readily and specifically;

OMB A-21 says you must have a

negotiated F&A Rate to recover

indirect costs. 23

F&A (Indirect Cost) Rate

F&A Costs

Organized Research Base

– F&A Costs: Indirect Costs Related to Research • Facilities Costs: Capital and Equipment, Operations and

Maintenance Costs, Interest on Debt, Depreciation

• Administrative Costs

– Organized Research Base: Total Direct Research Expenses • Some Costs are NOT allowed including equipment and capital

expenditures, space rental costs, student benefits, etc.

UMass Amherst FY11 Rate = 58%

RISD FY13 Rate = 45%

F&A Revenue Distribution

• Varies by Institution

– Centralized: All F&A Revenue is retained centrally AND indirect costs are born centrally

– Decentralized: All F&A Revenue is distributed to research departments AND all indirect costs are allocated to research departments

– Hybrid: A portion of the F&A Revenue is distributed to research departments and a portion is retained centrally to cover indirect costs funded centrally

Top Related