Languages

Pages

Legal

1

BEST IN FRANCECASE STUDY : LIDL

Guillaume ADIN

Harold GUERIF

Antoine GUILLIER DE CHALVRON

Maxime ROSENWALD

2

LIDL and the hard discount market

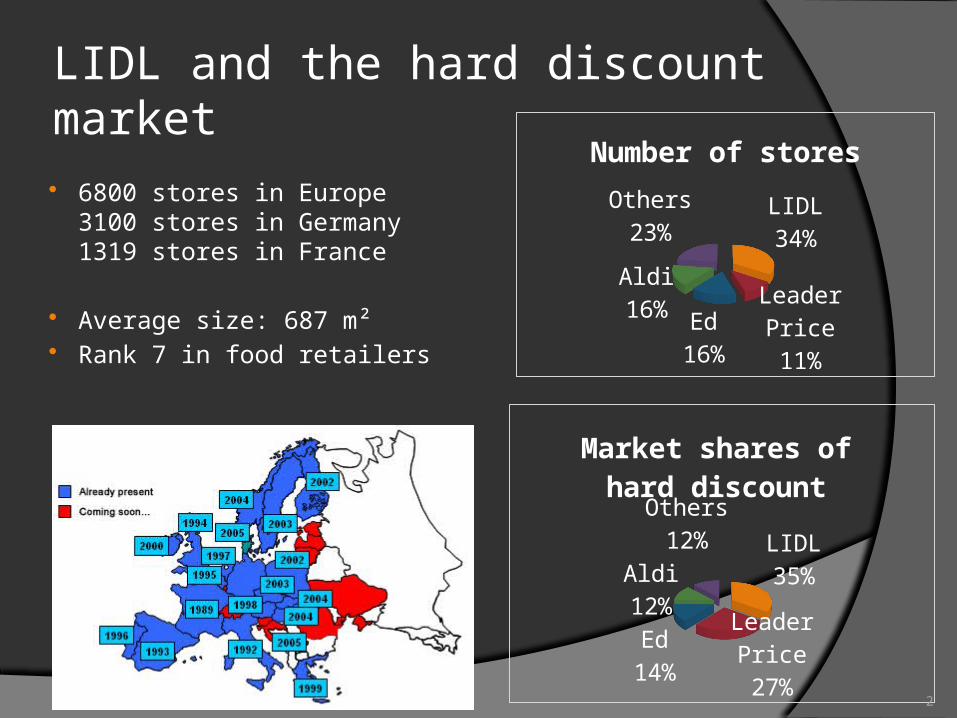

LIDL34%

Leader Price11%

Ed16%

Aldi16%

Others23%

Number of stores

6800 stores in Europe 3100 stores in Germany 1319 stores in France

Average size: 687 m² Rank 7 in food retailers

LIDL35%

Leader Price27%

Ed14%

Aldi12%

Others12%

Market shares of hard discount

3

Background Lidl & Schwarz : 1970 in Souabe

(Germany)

Two mains activities were developed: Food discounters : Lidl Retailers : Kaufland and

Handelshof were grouped into self-service markets and superstores.

Establishement of Lidl in France in 1988 with the opening of the first store in Colmar (Haut-Rhin).In 1989, Lidl opened in the east of France, whereas his major competitor, Aldi, arrived in the north.

4

• Classic supermarkets deal more and more cheap products but keep their good reputation

• Sometimes classic dealers create their own hard-discount brand (Carrefour)

• The security of the stores is not at the top : 6 hold-ups during the month of august 2008

• People want products which are always, but with the same level of quality

• Bio and fair-trade products, are still expensive and could be new markets for the hard discount

• LIDL understood how to use the « loi Raffarin » to optimize their implantation all over the country

• External communication : reduced to the minimum

• The LIDL stores are sinister• Any improvement of the

products’ visual : everything stay in transportation’s boxes

• The working conditions are one the worst of the distribution’s sector

• 1400 stores all over the country• Between 50 and 100 openings a

year• 50% of French consumers go to

a LIDL shop• Located in 24 countries : used to

deal with different cultures• Good knowledge of european

suppliers• Power of negotiation with

classical big brands• Since 1973 in Germany :

efficient logistic system Strengths

WeaknessesThreats

Opportunities

5

WHAT PROBLEMS DID LIDL

ENCOUNTER ?

6

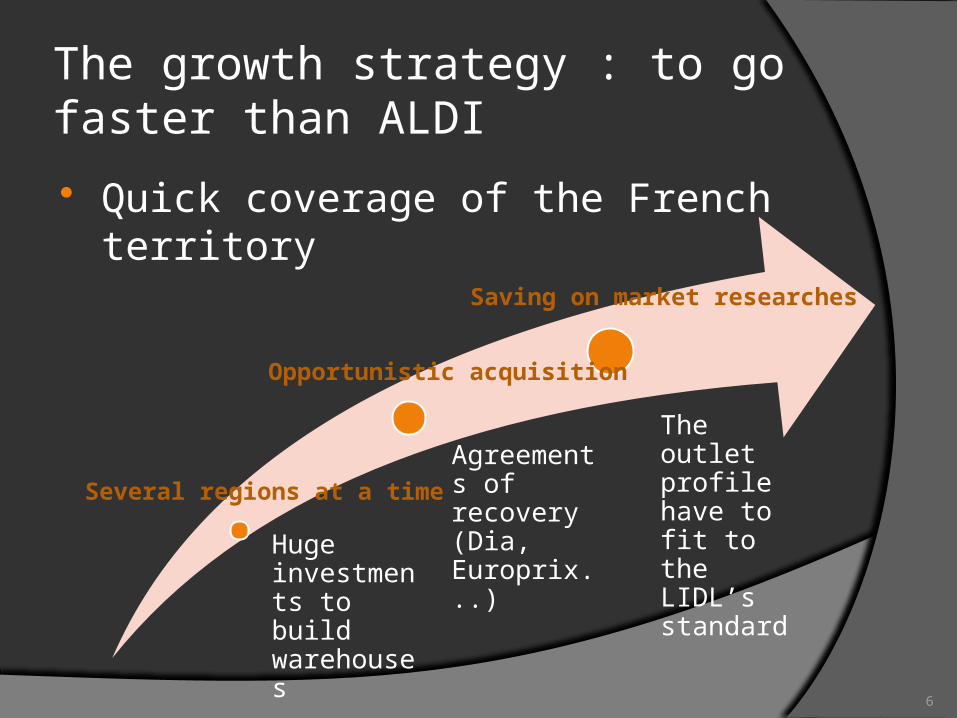

The growth strategy : to go faster than ALDI Quick coverage of the French territory

Huge investments to build warehouses

Agreements of recovery (Dia, Europrix...)

The outlet profile have to fit to the LIDL’s standard

Several regions at a time

Opportunistic acquisition

Saving on market researches

7

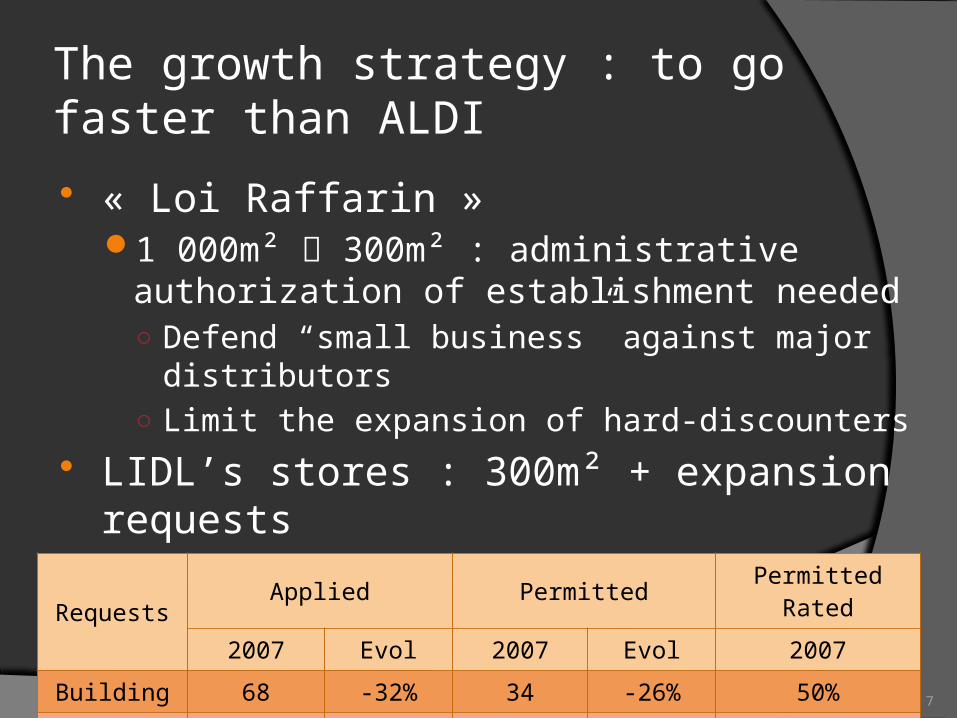

The growth strategy : to go faster than ALDI « Loi Raffarin »

1 000m² 300m² : administrative authorization of establishment needed○ Defend “small business” against major distributors○ Limit the expansion of hard-discounters

LIDL’s stores : 300m² + expansion requestsEasier than build requests

RequestsApplied Permitted Permitted Rated

2007 Evol 2007 Evol 2007

Building 68 -32% 34 -26% 50%

Extension 68 +26% 45 +22% 66%

8

How to fit to the french market ?

German Hard Discount

Little sized shops (less than 600m²)

Single reference by type of product

Lowest prices

Fair Trade

Minimalist presentation of

products

Weekly prices’ reductions on non-

food products

Reduced staff

Only own-label or unbranded

French Hard

Discount

Some of national

and historical

big brands

More fresh vegetables and fruits, more types

of fresh meal…

Fair Trade

9

Relationship between employees and management Difficult working

conditions

Spying of employees

Bad intern communication

Poor picture of the company for the consumers

10

Thank you for your attention

Top Related