Languages

Pages

Legal

SANDEEP KARGlobal Director,

Automotive & Transportation Research

Global Medium-Heavy Duty Truck Market:

Vision 2022

Vision 2022: Big Picture

2014-2022 CV Industry Senior Management Top-of-Mind Issues

0

1

2

3

4

5

Last frontiers ofglobalization- Next 11,

Africa

2.Regulation compliancepressures

3.Global manufacturingand sourcing shifts

4.Rapid proliferation ofelectronics

5.Urban logistics, bricks-and-clicks, and multi-

modality

6. Autonomous drivenconnected trucks

7. Service andmaintenance revenue

focused businessmodels

8. New truck types (e.g.mega-trucks, city trucks,etc.) and pricing models

Global CV 2020 Vision: Senior Executive Top of Mind Issues, Global, 2014- 2022

Note: Data collected from 2013-2014 interviews and discussions with Sr. Manager to CEO

level executives of truck OEMs and tier-1 suppliers in NA, EU, APAC, China, India, Latin

America and other regions

Source: Frost & Sullivan analysis.

50

100

150

200

250

300

350

55.0

65.0

75.0

85.0

95.0

105.0

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

US Annual Industrial Production Index US Class 8 Actual Units Sold Used Class 8 Estimated Units Sold

Truck Buying Cycles vis-a-vis Economic CyclesIncreasing Volatility

Heavy-duty Truck Dealership Market:

Correlation Between Truck Buying Cycle and Industrial Growth, United States, 1998–2016

Ind

us

tria

l P

rod

uc

tio

n In

de

x (

20

07

=1

00

)

Un

its

So

ld (

‘00

0)

Low Replacement

• Increase in replacement cycle to 5 – 6 years

• Slowdown of economy

• Tremendous demand for used trucks

Artificial Boosters

• Pre-buy activity

• Regulation compliance

• Cheaper trucks

Strong Economy

• Robust economic activity

• Class 8 growth exceeded overall

truck growth sales during much of

the 1990s, peaking in 1999

Pent-up Demand

• Growth in US manufacturing and

industrial production

• Pent-up replacement demand

• Short supply of MY ‘08 and ‘09 used trucks

• Truck cycle peaks occur every 4th / 5th year.

• Truck cycle peaks precede industrial production peak by a year.

• This correlation suggests that the next truck cycle peak could be in 2014–

2015 followed by an potential economic upturn in 2016.

Global GDP & Commercial Truck Market Growth Outlook

Growth in BRIC and Next 11 economies will offer strength to global truck demand. Developed economies to start offering momentum from 2015 onwards

Global CV Vision 2020: World GDP and CV Growth Outlook – Global: 2012 – 2022

RegionGDP Growth Estimates:

2012 – 2022 (%)

MCV Growth

(CAGR%)

HCV Growth

(CAGR%)

Overall CV

Growth

(CAGR%)

Market

Opportunity

North America 2.1 – 2.5 4.3 3.6 3.9 Moderate

South America 4.0 – 5.0 4.4 5.7 5.3 Moderate-High

Europe 1.0 – 1.5 4.2 3.8 3.9 Moderate

China 6.5 – 7.0 2.9 5.4 4.7 Moderate-High

India 6.0 – 7.0 4.4 7.0 5.9 Moderate-High

Russia 3.5 – 4.0 10.3 8.4 8.9 High

Next 11 5.0 – 6.0 7.1 9.2 8.2 High

RoW 4.0 – 5.0 8.4 8.2 8.3 High

Global 4.0 – 4.5 5.1 5.7 5.5 Moderate-High

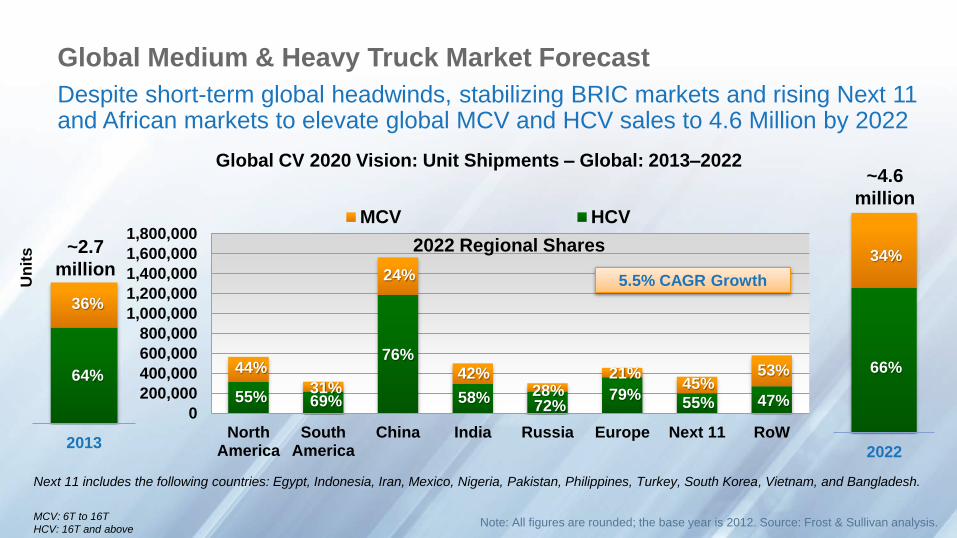

Global Medium & Heavy Truck Market Forecast

Despite short-term global headwinds, stabilizing BRIC markets and rising Next 11 and African markets to elevate global MCV and HCV sales to 4.6 Million by 2022

Global CV 2020 Vision: Unit Shipments – Global: 2013–2022

Note: All figures are rounded; the base year is 2012. Source: Frost & Sullivan analysis.

Next 11 includes the following countries: Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, Philippines, Turkey, South Korea, Vietnam, and Bangladesh.

MCV: 6T to 16T

HCV: 16T and above

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

NorthAmerica

SouthAmerica

China India Russia Europe Next 11 RoW

MCV HCV

20132022

2022 Regional Shares~2.7

million

~4.6

million

34%

36%

64%66%

Un

its

44%

31%

24%

42% 21%45%

53%

55% 69%

76%

58%72%

79%55% 47%

28%

5.5% CAGR Growth

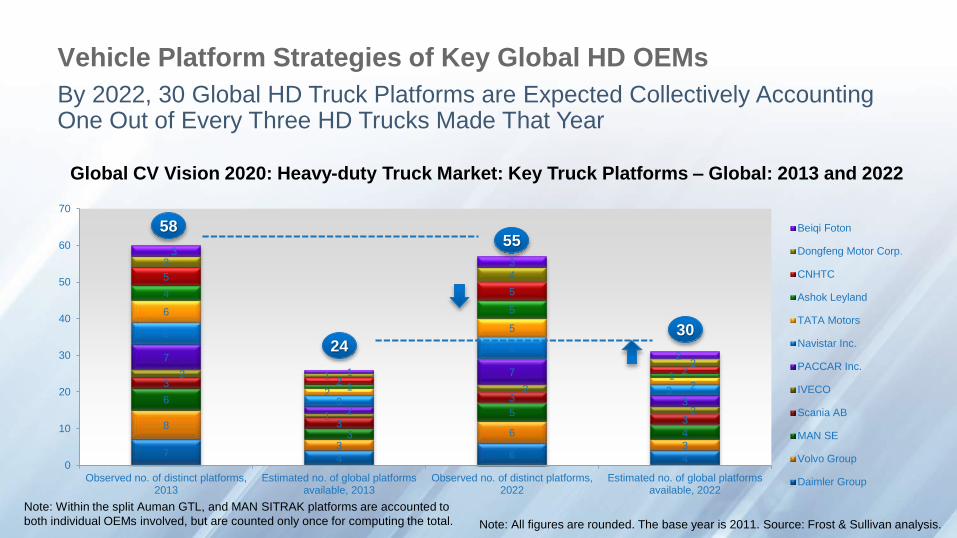

Vehicle Platform Strategies of Key Global HD OEMs

By 2022, 30 Global HD Truck Platforms are Expected Collectively Accounting One Out of Every Three HD Trucks Made That Year

Global CV Vision 2020: Heavy-duty Truck Market: Key Truck Platforms – Global: 2013 and 2022

Note: All figures are rounded. The base year is 2011. Source: Frost & Sullivan analysis.

Note: Within the split Auman GTL, and MAN SITRAK platforms are accounted to

both individual OEMs involved, but are counted only once for computing the total.

74 6 4

8

3

6

3

6

3

5

4

3

3

3

3

2

1

2

2

7

2

7

3

6

3

6

3

6

2

5

2

4

1

5

1

5

2

5

2

3

1

4

2

3

1

3

2

0

10

20

30

40

50

60

70

Observed no. of distinct platforms,2013

Estimated no. of global platformsavailable, 2013

Observed no. of distinct platforms,2022

Estimated no. of global platformsavailable, 2022

Beiqi Foton

Dongfeng Motor Corp.

CNHTC

Ashok Leyland

TATA Motors

Navistar Inc.

PACCAR Inc.

IVECO

Scania AB

MAN SE

Volvo Group

Daimler Group

58

24

55

30

Pri

ce

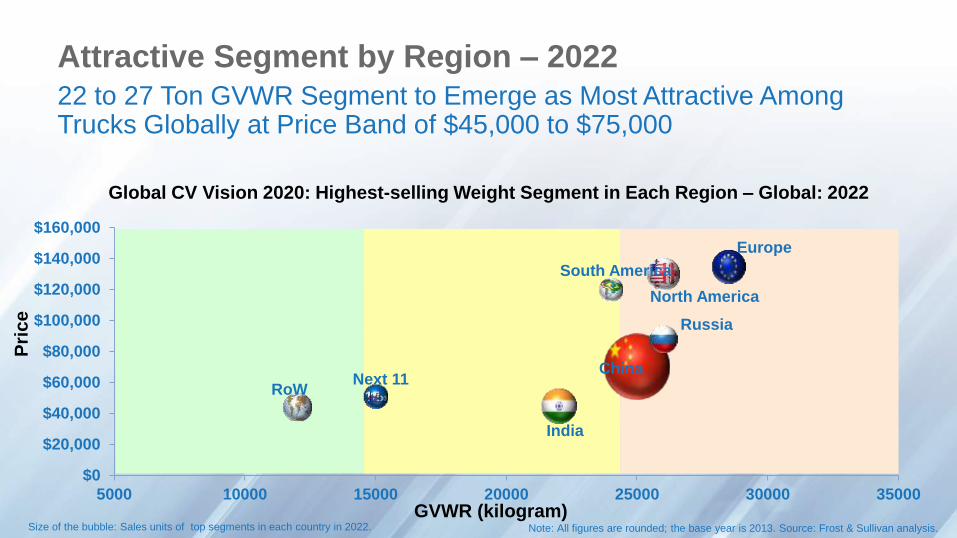

Attractive Segment by Region – 202222 to 27 Ton GVWR Segment to Emerge as Most Attractive Among Trucks Globally at Price Band of $45,000 to $75,000

North America

South America

China

India

Russia

Europe

Next 11RoW

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

5000 10000 15000 20000 25000 30000 35000

Global CV Vision 2020: Highest-selling Weight Segment in Each Region – Global: 2022

GVWR (kilogram)Size of the bubble: Sales units of top segments in each country in 2022. Note: All figures are rounded; the base year is 2013. Source: Frost & Sullivan analysis.

Fleet Operations Overview – North America

In 2022 Fleets Operating in NA Should Expect an Average Annual Cost of $183,000 or $1.9 Mer Mile, a 10 Percent Increase Over 2013’s Operating Cost

Global CV 2020 Vision: Fleet Cost Overview – North America: 2013 and 2022

33.0 29.0

28.0 31.0

9.0 11.0

10.0 12.04.0 3.011.0 9.0

3.0 3.02.0 2.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2013 2022

Fuel

Driver Wages

Driver Benefits

Tractor / TrailerInsurance

MaintenancePermits / Toll

Tires

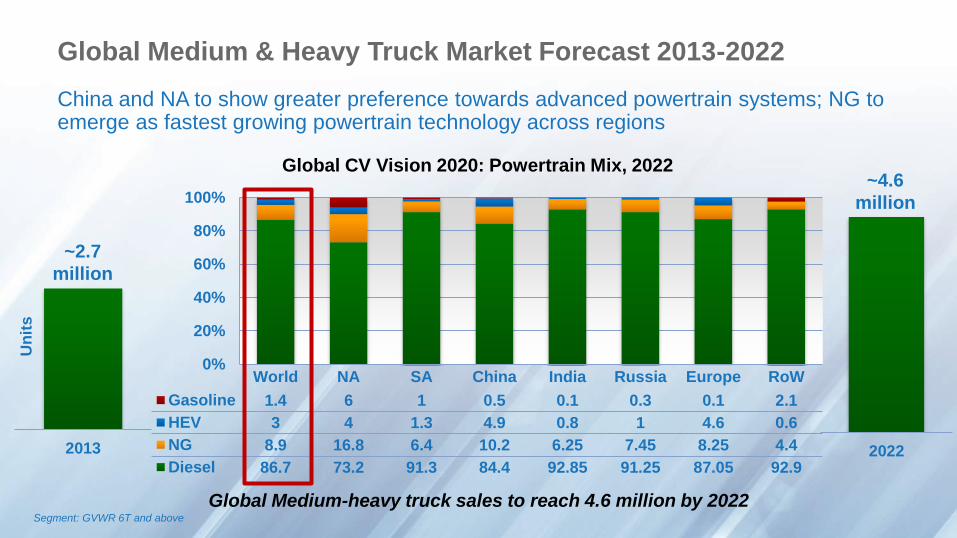

Global Powertrain Market Outlook: 2022

Global Medium & Heavy Truck Market Forecast 2013-2022

China and NA to show greater preference towards advanced powertrain systems; NG to emerge as fastest growing powertrain technology across regions

Segment: GVWR 6T and above

Global CV Vision 2020: Powertrain Mix, 2022

Global Medium-heavy truck sales to reach 4.6 million by 2022

0%

20%

40%

60%

80%

100%

World NA SA China India Russia Europe RoW

Gasoline 1.4 6 1 0.5 0.1 0.3 0.1 2.1

HEV 3 4 1.3 4.9 0.8 1 4.6 0.6

NG 8.9 16.8 6.4 10.2 6.25 7.45 8.25 4.4

Diesel 86.7 73.2 91.3 84.4 92.85 91.25 87.05 92.9

2013 2022

~2.7

million

Un

its

~4.6

million

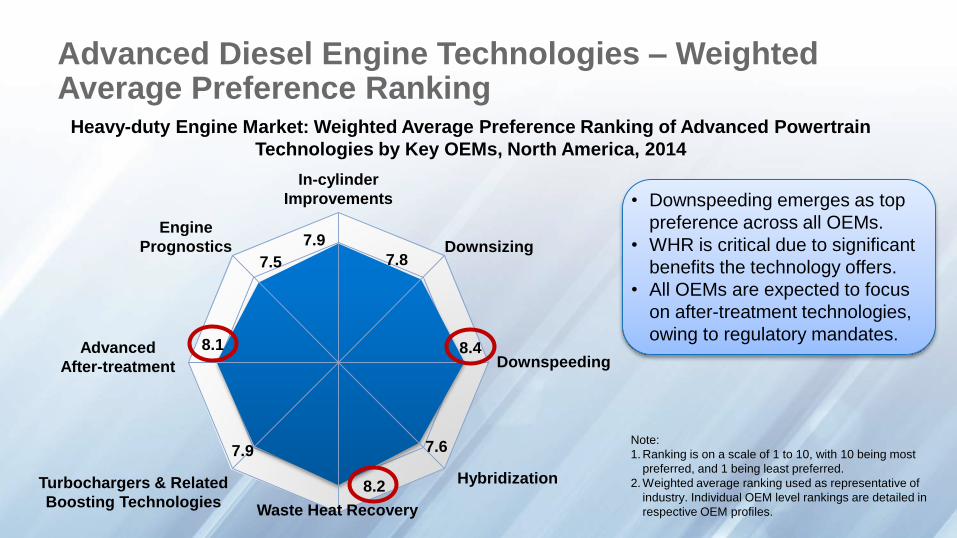

Advanced Diesel Engine Technologies – Weighted Average Preference Ranking

Heavy-duty Engine Market: Weighted Average Preference Ranking of Advanced Powertrain

Technologies by Key OEMs, North America, 2014

• Downspeeding emerges as top

preference across all OEMs.

• WHR is critical due to significant

benefits the technology offers.

• All OEMs are expected to focus

on after-treatment technologies,

owing to regulatory mandates.

Note:

1. Ranking is on a scale of 1 to 10, with 10 being most

preferred, and 1 being least preferred.

2. Weighted average ranking used as representative of

industry. Individual OEM level rankings are detailed in

respective OEM profiles.

7.9

7.8

8.4

7.6

8.2

7.9

8.1

7.5

In-cylinder

Improvements

Downsizing

Downspeeding

Waste Heat Recovery

Turbochargers & Related

Boosting Technologies

Advanced

After-treatment

Engine

Prognostics

Hybridization

NA SA China India Russia West Europe Next 11 RoW

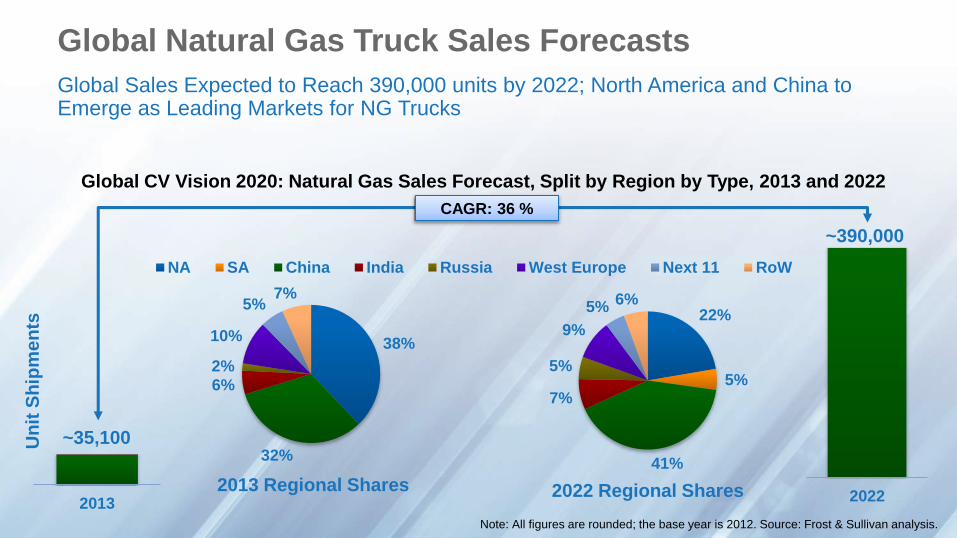

Global Natural Gas Truck Sales Forecasts

Global Sales Expected to Reach 390,000 units by 2022; North America and China to Emerge as Leading Markets for NG Trucks

Global CV Vision 2020: Natural Gas Sales Forecast, Split by Region by Type, 2013 and 2022

Note: All figures are rounded; the base year is 2012. Source: Frost & Sullivan analysis.

2013 2022

38%

32%

6%

2%

10%

5%7%

22%

5%

41%

7%

5%

9%

5%6%

2013 Regional Shares 2022 Regional Shares

Un

it S

hip

me

nts

~390,000

~35,100

CAGR: 36 %

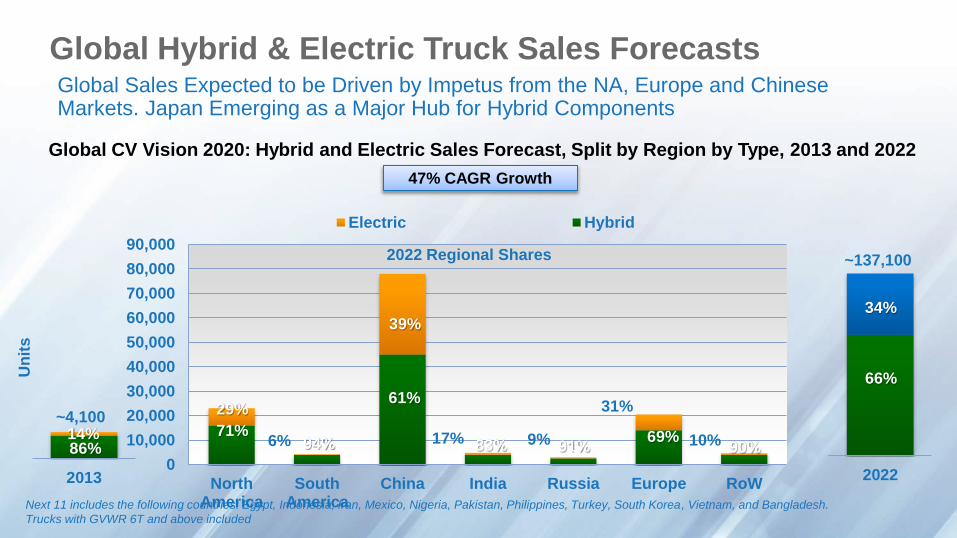

Global Hybrid & Electric Truck Sales ForecastsGlobal Sales Expected to be Driven by Impetus from the NA, Europe and Chinese Markets. Japan Emerging as a Major Hub for Hybrid Components

Global CV Vision 2020: Hybrid and Electric Sales Forecast, Split by Region by Type, 2013 and 2022

Next 11 includes the following countries: Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, Philippines, Turkey, South Korea, Vietnam, and Bangladesh.

Trucks with GVWR 6T and above included

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

NorthAmerica

SouthAmerica

China India Russia Europe RoW

Electric Hybrid

2013 2022

47% CAGR Growth

2022 Regional Shares

~4,100

6%

39%

17% 9% 10%14%86%

29%

94%

61%

83% 91%69%

90%

Un

its

66%

34%

~137,100

31%

71%

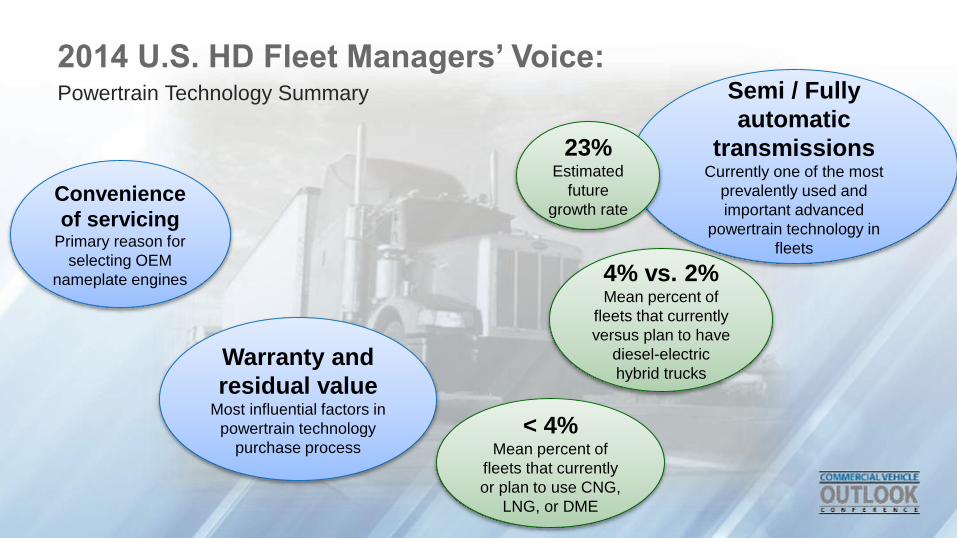

2014 U.S. HD Fleet Managers’ Voice:Powertrain Technology Summary

Warranty and

residual valueMost influential factors in

powertrain technology

purchase process

Semi / Fully

automatic

transmissions Currently one of the most

prevalently used and

important advanced

powertrain technology in

fleets

23%Estimated

future

growth rateConvenience

of servicingPrimary reason for

selecting OEM

nameplate engines 4% vs. 2%Mean percent of

fleets that currently

versus plan to have

diesel-electric

hybrid trucks

< 4%Mean percent of

fleets that currently

or plan to use CNG,

LNG, or DME

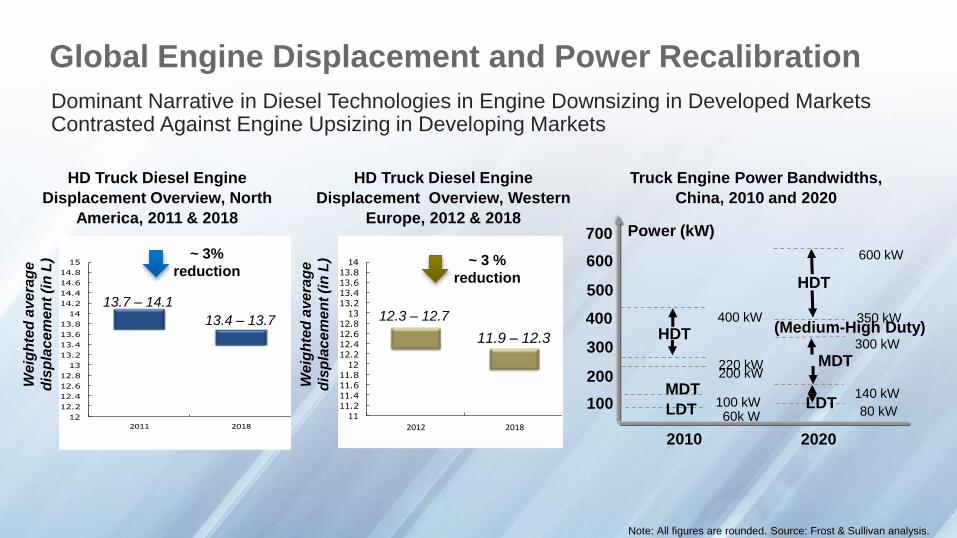

Global Engine Displacement and Power Recalibration

Dominant Narrative in Diesel Technologies in Engine Downsizing in Developed Markets Contrasted Against Engine Upsizing in Developing Markets

Truck Engine Power Bandwidths,

China, 2010 and 2020

HD Truck Diesel Engine

Displacement Overview, North

America, 2011 & 2018

HD Truck Diesel Engine

Displacement Overview, Western

Europe, 2012 & 2018

12

12.2

12.4

12.6

12.8

13

13.2

13.4

13.6

13.8

14

14.2

14.4

14.6

14.8

15

2011 2018

11

11.2

11.4

11.6

11.8

12

12.2

12.4

12.6

12.8

13

13.2

13.4

13.6

13.8

14

2012 2018

2010 2020

100

300

400

500

Power (kW)700

MDT

LDT

200 kW

100 kW60k W

HDT

220 kW

400 kW 350 kW

HDT

600 kW

MDT300 kW

140 kW

(Medium-High Duty)

LDT80 kW

200

600

Note: All figures are rounded. Source: Frost & Sullivan analysis.

~ 3%

reduction~ 3 %

reduction

13.7 – 14.1

13.4 – 13.7 12.3 – 12.7

11.9 – 12.3

We

igh

ted

ave

rag

e

dis

pla

ce

me

nt

(in

L)

We

igh

ted

ave

rag

e

dis

pla

ce

me

nt

(in

L)

Global Telematics Market Outlook 2022

New Fleet Management Systems Vendors Evolving –Expanding Value ChainGoing forward most value chain partners will consider offering proprietary FMS solutions; Consolidations (acquisition / partnership) will be likely outcome

Most of the value chain partners of the

trucking industry are eyeing this market

Tires

Internet Companies

ex: GoogleTruck OEMs ex:

Freightliner, Volvo,

PACCAR, International

Telematics Companies ex: TomTomWireless Companies ex:

Verizon, AT&T

Energy Companies

ex: Shell, Exxon

Tier-I Companies ex:

Cummins, WABCO, Pirelli,

Michelin, Continental After OEMs, it is Tier-1 Suppliers That Are Now Focusing on This

Segment. Cummins, Eaton, WABCO, Michelin

Proliferation of Telematics is a Global Phenomenon:FMS Services by Region / Country

CV Telematics Market: Key FMS services by region, Global, 2014

Turkey

• Digital Tachograph

• Driver Management

• Fuel ManagementIndia

• Vehicle Tracking,

• Fuel Management

• Safety of vehicles and

DriversLatin America

• Stolen Vehicle Recovery.

• Fuel Management

• Insurance Service

Russia

• Emergency Services

• Track and Trace

• Two way messaging

Australia

• Vehicle Tracking,

• Driver Management

• Order Management

China

• Fuel Management

• Driver Management

European Union

• Track and Trace

• Driver Behavior

• Vehicle Management

• Fuel Management

• Regulatory Mandated Services

South Africa

• Track and Trace

• Stolen Vehicle Recovery

• Driver Management

Middle East

• Track and Trace

• Trailer Temperature

Monitoring

North America

• EOBR

• Prognostics / Preventive

maintenance

• Driver Management

• Fuel Management

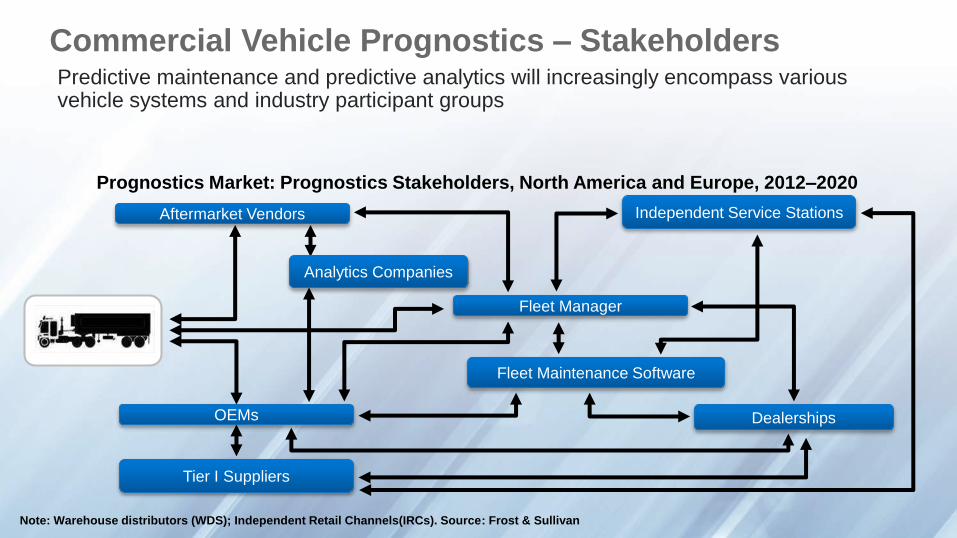

Commercial Vehicle Prognostics – StakeholdersPredictive maintenance and predictive analytics will increasingly encompass various vehicle systems and industry participant groups

Prognostics Market: Prognostics Stakeholders, North America and Europe, 2012–2020

Note: Warehouse distributors (WDS); Independent Retail Channels(IRCs). Source: Frost & Sullivan

OEMs

Tier I Suppliers

Aftermarket Vendors Independent Service Stations

Fleet Manager

Fleet Maintenance Software

Analytics Companies

Dealerships

True Value of Prognostics Will Only Be Realized When Most Vehicular Systems are Encompassed by Using Electronic Interfaces

Fuel

Fuel leakage

Fuel quality

Fuel injectors

Fuel level

Catalytic Converter

Emissions

Tires

Out of balance tires

Low tire pressure

Tire wear

Transmission

Transmission Issues

Coolant

Cooling system failure

Coolant pump failure

Coolant hose failure

Coolant level

Air filter

Dirty air filter

Emissions

Alternator

Alternator problems

Alternator deterioration

Starter failure

Engine

Engine Issues

Emissions

Ignition

Ignition Issues

Brakes

Brake problems

Brake pressure

Hard braking

Oil

Oil change needed

Oil level

Oil temperature

Prognostics Installed Base Estimates – NA & EUBy 2017 Over 1 Million Commercial Vehicles in North America and Western Europe to Subscribe to Prognostics Applications

2012 2013 2014 2015 2016 2017 2018 2019 2020

NORTH AMERICA 102,731 156,094 230,159 323,177 449,550 597,014 783,549 991,008 1,205,29

EUROPE 80,000 113,792 165,486 252,945 361,205 491,239 680,419 859,384 1,064,83

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

Prognostics Market: Prognostics installed base estimates, North America and Europe, 2012-2020

Evolution of prognostics technology, moderately mature business

models and demand from end users to increase vehicles uptime will

push prognostics demand faster beyond 2017

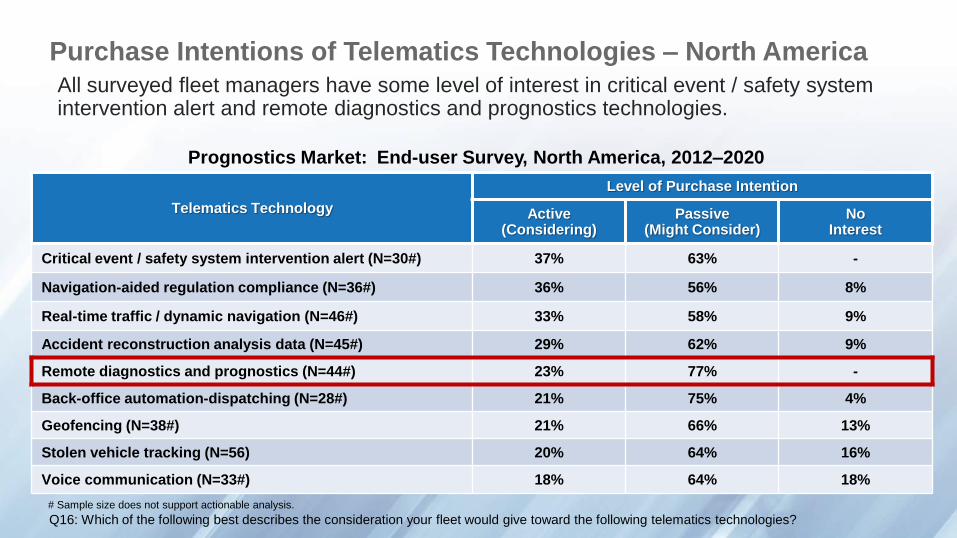

Purchase Intentions of Telematics Technologies – North America

All surveyed fleet managers have some level of interest in critical event / safety system intervention alert and remote diagnostics and prognostics technologies.

Prognostics Market: End-user Survey, North America, 2012–2020

Q16: Which of the following best describes the consideration your fleet would give toward the following telematics technologies?

# Sample size does not support actionable analysis.

Telematics Technology

Level of Purchase Intention

Active (Considering)

Passive (Might Consider)

No Interest

Critical event / safety system intervention alert (N=30#) 37% 63% -

Navigation-aided regulation compliance (N=36#) 36% 56% 8%

Real-time traffic / dynamic navigation (N=46#) 33% 58% 9%

Accident reconstruction analysis data (N=45#) 29% 62% 9%

Remote diagnostics and prognostics (N=44#) 23% 77% -

Back-office automation-dispatching (N=28#) 21% 75% 4%

Geofencing (N=38#) 21% 66% 13%

Stolen vehicle tracking (N=56) 20% 64% 16%

Voice communication (N=33#) 18% 64% 18%

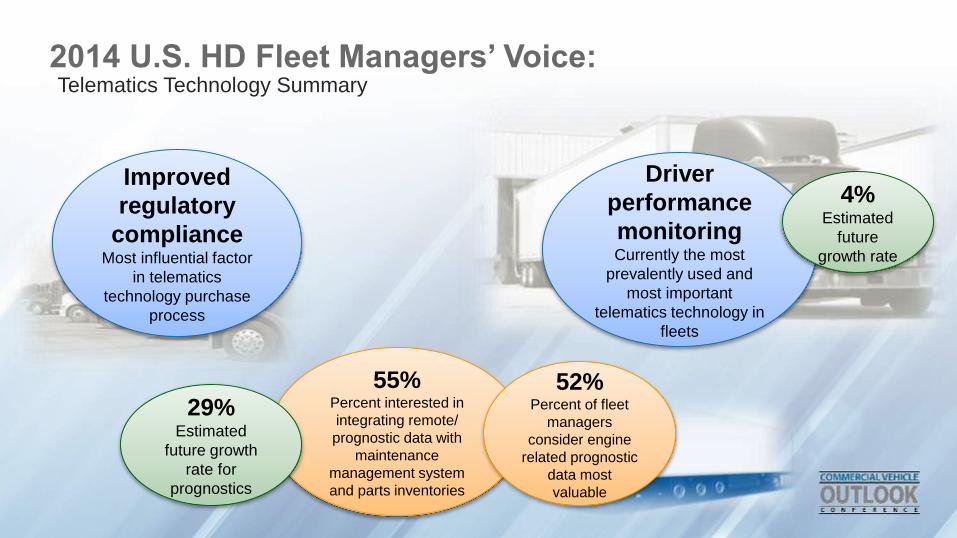

2014 U.S. HD Fleet Managers’ Voice:Telematics Technology Summary

Improved

regulatory

compliance Most influential factor

in telematics

technology purchase

process

Driver

performance

monitoring Currently the most

prevalently used and

most important

telematics technology in

fleets

4%Estimated

future

growth rate

55%Percent interested in

integrating remote/

prognostic data with

maintenance

management system

and parts inventories

52%Percent of fleet

managers

consider engine

related prognostic

data most

valuable

29%Estimated

future growth

rate for

prognostics

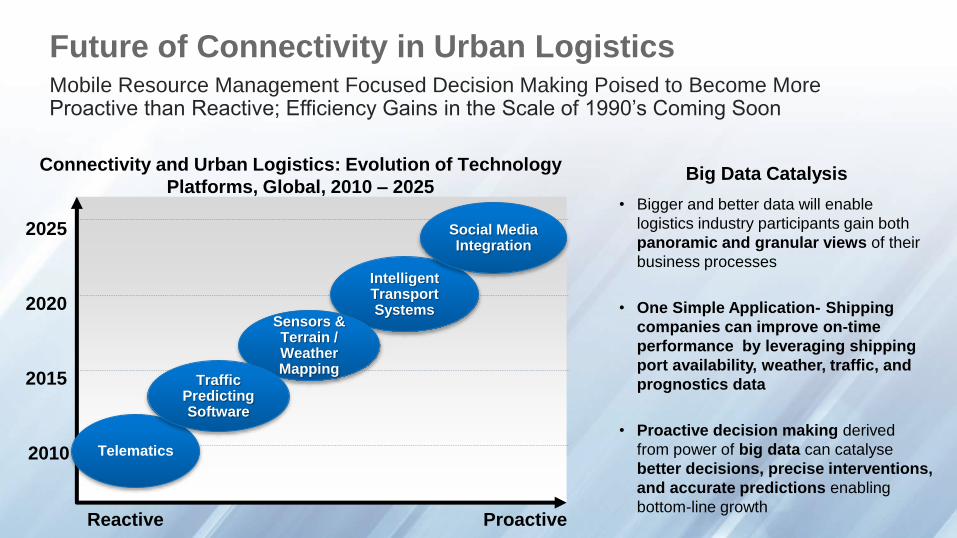

Future of Connectivity in Urban LogisticsMobile Resource Management Focused Decision Making Poised to Become More Proactive than Reactive; Efficiency Gains in the Scale of 1990’s Coming Soon

Reactive Proactive

2010

2015

2020

2025

Telematics

Intelligent Transport Systems

Social Media Integration

Sensors & Terrain / Weather Mapping

Traffic Predicting Software

Connectivity and Urban Logistics: Evolution of Technology

Platforms, Global, 2010 – 2025Big Data Catalysis

• Bigger and better data will enable

logistics industry participants gain both

panoramic and granular views of their

business processes

• One Simple Application- Shipping

companies can improve on-time

performance by leveraging shipping

port availability, weather, traffic, and

prognostics data

• Proactive decision making derived

from power of big data can catalyse

better decisions, precise interventions,

and accurate predictions enabling

bottom-line growth

Global Safety Market Outlook 2020

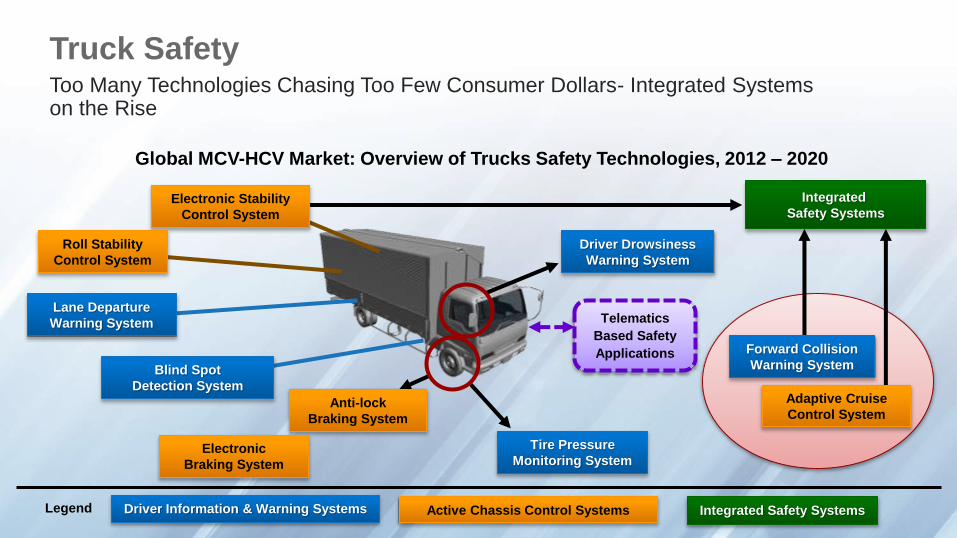

Truck SafetyToo Many Technologies Chasing Too Few Consumer Dollars- Integrated Systems on the Rise

Global MCV-HCV Market: Overview of Trucks Safety Technologies, 2012 – 2020

Driver Information & Warning Systems Active Chassis Control Systems Integrated Safety SystemsLegend

Lane Departure

Warning System

Blind Spot

Detection System

Anti-lock

Braking System

Electronic

Braking System

Forward Collision

Warning System

Adaptive Cruise

Control System

Tire Pressure

Monitoring System

Driver Drowsiness

Warning System

Electronic Stability

Control System

Roll Stability

Control System

Integrated

Safety Systems

Telematics

Based Safety

Applications

Growth Opportunities in Safety Systems Market (2010-2022)

TPMS, Stability Control Systems, and ABS to Experience Highest Traction in Global Markets; Integrated Safety Systems and Telematics Based Systems to Experience Rising penetration in North America and Europe

TRIAD = North America, EU, Japan BRIC = Brazil, Russia, India, China Next 11 countries

Moderate Noticeable HighRegional / Global Penetration:

Global CV Vision 2020: Safety Systems Adoption Potential Snapshot (Global), 2010-2022

Anti-lock braking systemsElectronic stability control systems

Roll-over stability control systemsAdaptive cruise control systems

Electronic braking systems

Integrated safety systems

Telematics based safety applications

DIWS

ACCS

ISS

TBSA

Tire pressure monitoring systems TRIAD, BRIC, Next 11

Lane departure warning systems TRIAD, Next 11

Forward collision warning systems TRIAD

Blind spot detection systems TRIAD, BRIC, Next 11

Driver drowsiness warning systems TRIADGlobal

GlobalTRIAD

TRIAD

TRIAD, BRIC (select)

TRIAD

TRIAD, BRIC, Next 11

2014 U.S. HD Fleet Managers’ Voice:

Advanced Safety Technology SummaryImproved Safe

Driving

PracticesMost influential factors in

advanced safety

technology purchase

process

Tire Related

Safety Systems Gaining significant

increase in fleet

manager interest

Stability

Control

Systems Most important

advanced safety

technology in fleets

19%Estimated

future growth

rate for RSC

12%Estimated

future growth

rate for ESC

32%Fleet managers

expect to use

trailer tire inflation

systems in 2015

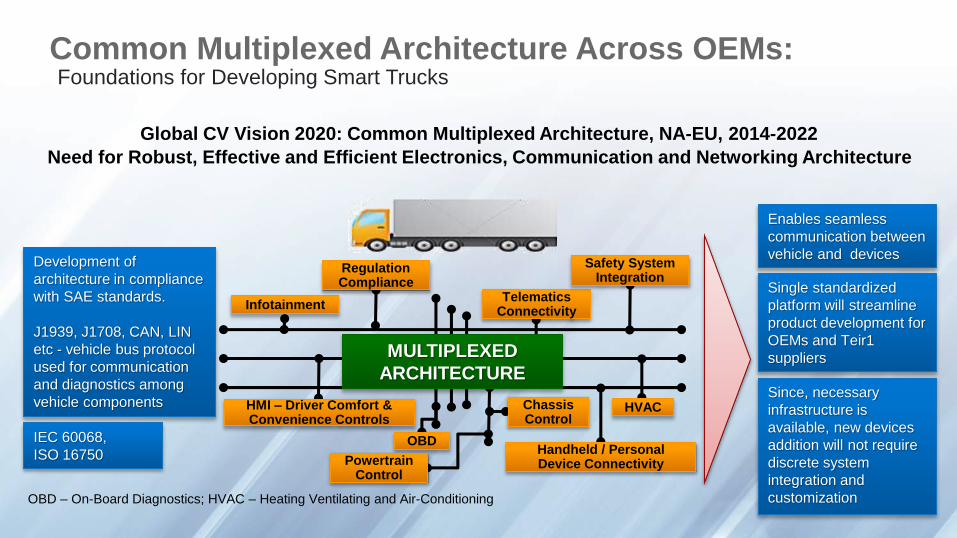

Common Multiplexed Architecture Across OEMs:Foundations for Developing Smart Trucks

Global CV Vision 2020: Common Multiplexed Architecture, NA-EU, 2014-2022

Need for Robust, Effective and Efficient Electronics, Communication and Networking Architecture

Enables seamless

communication between

vehicle and devices

Single standardized

platform will streamline

product development for

OEMs and Teir1

suppliers

Since, necessary

infrastructure is

available, new devices

addition will not require

discrete system

integration and

customizationOBD – On-Board Diagnostics; HVAC – Heating Ventilating and Air-Conditioning

Development of

architecture in compliance

with SAE standards.

J1939, J1708, CAN, LIN

etc - vehicle bus protocol

used for communication

and diagnostics among

vehicle components

Infotainment

Regulation Compliance

OBD

HMI – Driver Comfort & Convenience Controls

Handheld / Personal Device Connectivity

Telematics Connectivity

Safety System Integration

HVAC

Powertrain Control

Chassis Control

MULTIPLEXED

ARCHITECTURE

IEC 60068,

ISO 16750

Vision 2022Profit from Volume and Margins

andTruck of the Future

Volume Growth from Developing Markets, Margin Growth from Advanced Technologies:Product Focus on HD Trucks and City Trucks

Volume Growth

BRIC

Next 11

Africa

North America

APAC

Eurasia

LatAm

Margin Growth

Advanced Powertrain

Telematics

Safety

Health,

Wellness,

Wellbeing

Platforms

Autonomous Driving

Vision 2022:What Will be the Traits of Truck of The Future?

Green

Safe

Connected

Smart

Key Contacts

Sandeep Kar

Global Director- Automotive & Transportation Research

Direct: 416.490.7796

Fax: 416.490.1533

Email: [email protected]

Top Related