Languages

Pages

Legal

www.blaige.com

Presentation to the:

Global Packaging Mergers and Acquisitions:Mergers, Acquisitions and Exit Strategies for Flexible PackagingMergers, Acquisitions and Exit Strategies for Flexible Packaging

March 10, 2006 Naples, Florida

Page 2

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global Consolidation

AgendaAgenda SectionSection

Blaige & CompanyBlaige & Company II

Major Challenges Facing US Flexible Packaging in 2006Major Challenges Facing US Flexible Packaging in 2006 IIII

Packaging Industry Global ConsolidationPackaging Industry Global Consolidation IIIIII

The Science: M&A Activity in the Global Plastic Packaging MarketThe Science: M&A Activity in the Global Plastic Packaging Marketss IVIV

The Art: Maximizing Value The Art: Maximizing Value PriorPrior to the Transactionto the Transaction VV

Full or Partial Exit StrategiesFull or Partial Exit Strategies VIVI

The Art: Maximizing Value The Art: Maximizing Value DuringDuring the Transactionthe Transaction VIIVII

Summary CommentsSummary Comments VIIIVIII

AppendixAppendix IXIX

Page 3

© Copyright 2006, all contents Thomas Blaige & Co. LLC

I. Blaige & CompanyI. Blaige & Company

Page 4

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Blaige & CompanyBlaige & CompanyNo Dilution No Dilution –– Exclusive Focus: Plastics, Packaging and ChemicalsExclusive Focus: Plastics, Packaging and Chemicals

Blaige & Co.

Investment Bank —

Practice Group

Generalist Investment Bank

Pure Focus. Premier ValueSM

Limited Focus, Improved Results

Standard Process, Standard Results

Page 5

© Copyright 2006, all contents Thomas Blaige & Co. LLC

II. Major Challenges Facing US II. Major Challenges Facing US Flexible Packaging in 2006Flexible Packaging in 2006

Page 6

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Major Challenges Facing US Flexible Packaging in 2006 Major Challenges Facing US Flexible Packaging in 2006 Factors Which are Rapidly “Raising the Bar”Factors Which are Rapidly “Raising the Bar”

Imports Imports

Continuation of Unprecedented Resin Price Levels, Availability IContinuation of Unprecedented Resin Price Levels, Availability Issuesssues

Competitors, Customers, Suppliers Growing in Size, Gaining LeverCompetitors, Customers, Suppliers Growing in Size, Gaining Leverageage

Machinery & Equipment and Technology Costs IncreasingMachinery & Equipment and Technology Costs Increasing

Substitute Materials and Technologies on the HorizonSubstitute Materials and Technologies on the Horizon

Lack of Management Talent in Middle MarketLack of Management Talent in Middle Market

Risk Associated with Owners “Funding the Next Level of Growth”Risk Associated with Owners “Funding the Next Level of Growth”

Liquidity, Diversification, Succession, Estate Planning, Tax Liquidity, Diversification, Succession, Estate Planning, Tax –– “Value “Value Preservation” Issues for Successful EntrepreneursPreservation” Issues for Successful Entrepreneurs

Page 7

© Copyright 2006, all contents Thomas Blaige & Co. LLC

III. Packaging Industry III. Packaging Industry Global ConsolidationGlobal Consolidation

Page 8

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationConsolidation is being driven by Growth, Scale, and Geographic concerns

Drivers of Consolidation

Supplier Consolidation

Raw Materials Price Volatility

CustomerGlobalization

Customer Consolidation

Need for Differentiation

of Product

Maturing Growth

Packaging Manufacturers and

Converters

Page 9

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationEvolution among packaging types show that Flexible Packaging is due for significant consolidation

SegmentSegment 19801980

Glass BottlesGlass Bottles 19 competitors19 competitors 3 Leaders: 91% share 3 Leaders: 91% share (Anchor, Owens, St. Gobain)(Anchor, Owens, St. Gobain)

25 competitors25 competitors

14 competitors14 competitors

Many competitorsMany competitors

Food CansFood Cans

Beverage CansBeverage Cans 3 Leaders: 78% share 3 Leaders: 78% share (Ball, Crown, Rexam)(Ball, Crown, Rexam)

Plastic PackagingPlastic Packaging 5 Leaders: 32% share 5 Leaders: 32% share (Alcan, Amcor, Bemis, Printpack, (Alcan, Amcor, Bemis, Printpack, Sealed Air)Sealed Air)

20052005

3 Leaders: 81% share3 Leaders: 81% share(Ball, Crown, Silgan)(Ball, Crown, Silgan)

Page 10

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationBuyer Activity: “Global Positioning”: Strategic players are seleBuyer Activity: “Global Positioning”: Strategic players are selectively ctively acquiring and consolidatingacquiring and consolidating

Motivations

Increase Revenues

Lower Costs

Accelerate Strategy

Build brandsCross sell productsExpand markets/geographies

Scale benefits– Fixed (facilities, duplicate costs)– Variable (raw materials, labor)

Technology/R&D/IPManagement talent and labor poolGlobal capabilities/customer importance

Financial– Market access– Balance sheet leverage

Capital: Lower Cost, Better Access

Page 11

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationConsolidation Squeezing the “Middle Market”Consolidation Squeezing the “Middle Market”

Entrepreneurial Companies (Regional)Energetic, creative, responsive

Below competitive radarDesignated laboratory for new ideas, products, markets

Consolidators (Global) Purchasing power (sourcing)

Production scaleDistribution controlPersonnel resources

Research & development and capital funding

Page 12

© Copyright 2006, all contents Thomas Blaige & Co. LLC

U.S. Population Over Ages 50 and 65 from 1970-2010

Over 50

Over 65

0

20,000

40,000

60,000

80,000

100,000

1970 1975 1980 1985 1990 1995 2000 2005 2010

(in m

illio

ns)

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationDemographic of Aging Entrepreneurs Drives ConsolidationDemographic of Aging Entrepreneurs Drives Consolidation

Source: U.S. Bureau of Census

Page 13

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Resin Markets: Global Increase in Resin Demand & Raw Materials CostSupply and Demand DrivenSupply and Demand Driven. Global price increases for crude oil and natural gas . Global price increases for crude oil and natural gas have greatly affected the entire plastics industry. These increhave greatly affected the entire plastics industry. These increases in input costs ases in input costs coupled with greater than expected demand and a constricted Nortcoupled with greater than expected demand and a constricted North American supply h American supply have driven resin prices to record levels and have caused resin have driven resin prices to record levels and have caused resin producers to effect producers to effect force majeure (allocation).force majeure (allocation).

Expected to Remain Relatively HighExpected to Remain Relatively High. North American raw material prices are . North American raw material prices are expected to remain relatively high as record worldwide demand leexpected to remain relatively high as record worldwide demand levels continue on a vels continue on a relatively fixed base of supply, and as natural gas prices and orelatively fixed base of supply, and as natural gas prices and other input costs remain ther input costs remain at high levels.at high levels.

Stress on Plastic ProcessorsStress on Plastic Processors. Unprecedented raw material price inflation has . Unprecedented raw material price inflation has pushed marginal plastic processors and converters to the limit. pushed marginal plastic processors and converters to the limit. Several widelySeveral widely--publicized defaults among plastic processors and converters (Orapublicized defaults among plastic processors and converters (Orange Plastics, Apple nge Plastics, Apple Plastics, Plassein, Uniflex, Desert Plastics, Plastics, Plassein, Uniflex, Desert Plastics, Mercury Plastics,Mercury Plastics, EagleEagle--Picher, Integrated Picher, Integrated Plastics, Laich Industries Corp., and Cornerstone Products) havePlastics, Laich Industries Corp., and Cornerstone Products) have caused resin caused resin suppliers to further tighten terms, which has further exacerbatesuppliers to further tighten terms, which has further exacerbated the problem for d the problem for smaller and weaker processors and converters. smaller and weaker processors and converters.

Page 14

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Resin Pricing: Record Price Levels Prevail - Profound impact on the industry

Since 2001, raw material processors have been hit with resin priSince 2001, raw material processors have been hit with resin prices increases in excess ces increases in excess of 300%. By way of example, consider the following for LLDPE prof 300%. By way of example, consider the following for LLDPE pricing:icing:

Source: Chemical Data, Inc.

0.2000.2200.2400.2600.2800.3000.3200.3400.3600.3800.4000.4200.4400.4600.4800.5000.5200.5400.5600.5800.6000.6200.6400.6600.6800.700

US $/

LB

CDI High

CDI Low

2005

CDI: LLDPE Pound Pricing, 2000 – 2005

2000

Page 15

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global Consolidation Packaging Industry Global Consolidation Packaging Companies are Executing Globalization Strategies, Packaging Companies are Executing Globalization Strategies, in Part to Deal Directly with the “China Threat”in Part to Deal Directly with the “China Threat”

Ampac Packaging LLC China WOFE Flexible packaging (shopping bags)Bemis Company Singapore WOFE Flexible packaging and film productsPactiv Corporation China Joint Venture Flexible packaging productsSealed Air Corporation China, SW Asia WOFE Flexible food, protective and specialty packaging productsTredegar Film Products China WOFE Flexible Packaging

Alcoa Inc. China Joint Venture Polypropylene caps and closuresBlack and Decker Corp China WOFE Injection-molded parts and packaging operationsCrown Cork and Seal Inc. China, SE Asia WOFE Rigid metal and plastic packaging (metal / plastic enclosures)Industrial Molds, Inc. China Joint Venture Injection and compression moldsNypro Inc. China WOFE Injection molding, packaging and finishing operationsOwens Illinois, Inc. China, Singapore WOFE Glass container and plastics operationsPerlos, Ltd. China WOFE Injection molded electronic components (Nokia)Placon Corp. China WOFE Thermoformed packagingPrent Corporation China, Malaysia, Singapore WOFE Thermoformed packagingSCA/Tuscarora SE Asia Strategic Alliance Polystyrene foam, corrugated boxes and industrial sacksTessy Plastics Corp. China WOFE Molding and assembly (Xerox and Delphi)Trend Technologies China WOFE Molding, stamping and assembly operations for electronics

FLEXIBLE PACKAGING OPERATIONS

PACKAGING AND PLASTICS OPERATIONS

Page 16

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global Consolidation Packaging Industry Global Consolidation Top 40 Analysis: Top 40 Analysis: 2000’s Top 40 Flexible Packaging Companies 2000’s Top 40 Flexible Packaging Companies

2000’s Top 40 Flexible Packaging Companies*

Source: Plastics News and Blaige & Co.

AEP Industries Inc. Mitsubishi Polyester Film LLCAET Films Nan Ya Plastics CorpAtlantis Plastics Custom & Stretch Films Pactiv Corp.Bemis Co. Inc. Pechiney Plastic Packaging Inc.Clopay Plastic Products Co. Plassein Packaging Corp.Cryovac Division Pliant Corp.Dow Chemical Inc. Poly America Inc.DuPont Teijin Films Printpack Inc.Essex Plastics Rexam Inc.ExxonMobil Chemical Co. Films Business Reynolds Metals Co. Packaging Geon Engineered Films Sigma Plastics Corp.Glad Products Inc. Sonoco High Density Film Products DivisionGreat Pacific Enterprises Inc. Spartech PlasticsHeritage Bag Co. Toray Plastics America Inc.Honeywell Specialty Chemicals Transilwrap Co. Inc.Inteplast Group Ltd. Tredegar Film Products Corp. International Paper Co. Flexible Packaging Tyco Plastics and Adhesives GroupIntertape Polymer Group Inc. Vanguard Plastics Inc.Kama Corp. VPI LLCKlockner-Pentaplast of America Winpak Ltd.

Page 17

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global Consolidation Packaging Industry Global Consolidation Top 40 Analysis: oTop 40 Analysis: of 2000’s Top 40 Flexible Packaging Companies, 16 f 2000’s Top 40 Flexible Packaging Companies, 16 Companies (40%) Changed Ownership or were Eliminated by ConsolidCompanies (40%) Changed Ownership or were Eliminated by Consolidationation

2000’s Top 40 Flexible Packaging Companies* - Today

•Source: Plastics News and Blaige & Co.

AEP Industries Inc. Mitsubishi Polyester Film LLCAET Films Nan Ya Plastics CorpAtlantis Plastics Custom & Stretch Films Pactiv Corp.Bemis Co. Inc. Pechiney Plastic Packaging Inc.Clopay Plastic Products Co. Plassein Packaging Corp.Cryovac Division Pliant Corp.Dow Chemical Inc. Poly America Inc.DuPont Teijin Films Printpack Inc.Essex Plastics Rexam Inc.ExxonMobil Chemical Co. Films Business Reynolds Metals Co. Packaging Geon Engineered Films Sigma Plastics Corp.Glad Products Inc. Sonoco High Density Film Products DivisionGreat Pacific Enterprises Inc. Spartech PlasticsHeritage Bag Co. Toray Plastics America Inc.Honeywell Specialty Chemicals Transilwrap Co. Inc.Inteplast Group Ltd. Tredegar Film Products Corp. International Paper Co. Flexible Packaging Tyco Plastics and Adhesives GroupIntertape Polymer Group Inc. Vanguard Plastics Inc.Kama Corp. VPI LLCKlockner-Pentaplast of America Winpak Ltd.

Page 18

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global Consolidation Packaging Industry Global Consolidation Top 40 Analysis: oTop 40 Analysis: of 2000’s Top 40 Flexible Packaging Cos., 33 Companies f 2000’s Top 40 Flexible Packaging Cos., 33 Companies (83%) were Involved in an Acquisition or Divestiture (Shaded In (83%) were Involved in an Acquisition or Divestiture (Shaded In Grey). Grey).

2000’s Top 40 Flexible Packaging Companies* - Today

•Source: Plastics News and Blaige & Co.

AEP Industries Inc. Mitsubishi Polyester Film LLCAET Films Nan Ya Plastics CorpAtlantis Plastics Custom & Stretch Films Pactiv Corp.Bemis Co. Inc. Pechiney Plastic Packaging Inc.Clopay Plastic Products Co. Plassein Packaging Corp.Cryovac Division Pliant Corp.Dow Chemical Inc. Poly America Inc.DuPont Teijin Films Printpack Inc.Essex Plastics Rexam Inc.ExxonMobil Chemical Co. Films Business Reynolds Metals Co. Packaging Geon Engineered Films Sigma Plastics Corp.Glad Products Inc. Sonoco High Density Film Products DivisionGreat Pacific Enterprises Inc. Spartech PlasticsHeritage Bag Co. Toray Plastics America Inc.Honeywell Specialty Chemicals Transilwrap Co. Inc.Inteplast Group Ltd. Tredegar Film Products Corp. International Paper Co. Flexible Packaging Tyco Plastics and Adhesives GroupIntertape Polymer Group Inc. Vanguard Plastics Inc.Kama Corp. VPI LLCKlockner-Pentaplast of America Winpak Ltd.

Page 19

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationThe “Leaders”, “Followers” and “Others”The “Leaders”, “Followers” and “Others”

Top Consolidators (“Leaders”)

Static Participants(“Others”)

Consolidatees(“Followers”)

• 20% of Universe• Rapidly Gaining Share• Aggressive Acquisitions and

Divestitures• Market Domination via Best

Acquisitions, Selective Divestitures

• 60% of Universe• Erosion• Mergers and Selective

Acquisitions• Pursue Niche Leadership

• 20% of Universe• Rapidly Losing Share• Restructuring and

Divestitures • Sell at Maximum Price

Page 20

© Copyright 2006, all contents Thomas Blaige & Co. LLC

IV. The Science:IV. The Science:M&A Activity in the Global Plastic M&A Activity in the Global Plastic

Packaging MarketsPackaging Markets

Page 21

© Copyright 2006, all contents Thomas Blaige & Co. LLC

390

198

0100200300400

2002 2005E

118

50

050

100150

2002 2005E

M&A Activity in the Global Plastic Packaging Markets M&A Activity in the Global Plastic Packaging Markets 20022002--2005: Plastic Packaging Sector Outpaces Overall Plastics M&A2005: Plastic Packaging Sector Outpaces Overall Plastics M&A

Plastic packaging deals more than doubled from 50 deals in Plastic packaging deals more than doubled from 50 deals in 2002 to 118 in 2005E, driven by dramatic increases in:2002 to 118 in 2005E, driven by dramatic increases in:–– International Activity (reflecting move to globalization)International Activity (reflecting move to globalization)–– Divestiture Activity and “Trading” Among Top ConsolidatorsDivestiture Activity and “Trading” Among Top Consolidators–– Financial Buyer Acquisition Activity (both platforms and add onsFinancial Buyer Acquisition Activity (both platforms and add ons))

Source: Blaige & Co.Source: Blaige & Co.

Global Plastic Packaging M&A ActivityGlobal Plastic Packaging M&A ActivityGlobal Plastics M&A ActivityGlobal Plastics M&A Activity

# of

Dea

ls

# of

Dea

ls

97% 136%

Page 22

© Copyright 2006, all contents Thomas Blaige & Co. LLC

M&A Activity in the Global Plastic Packaging Markets M&A Activity in the Global Plastic Packaging Markets Plastic Packaging Accounts for nearly 1/3 of All Plastics DealsPlastic Packaging Accounts for nearly 1/3 of All Plastics Deals

Plastic Packaging % of Total Plastics Deals(390 Total Transactions in 2005E)

Source: Thomas Blaige & Company LLC

Other Plastics70%

Plastic Packaging30%

Page 23

© Copyright 2006, all contents Thomas Blaige & Co. LLC

US Only31%

Foreign Participant69%

M&A Activity in the Global Plastic Packaging Markets M&A Activity in the Global Plastic Packaging Markets Global Deals: Over 2/3 of Deals Involve a Foreign ParticipantGlobal Deals: Over 2/3 of Deals Involve a Foreign Participant

US Only Vs. Foreign Participants Plastic Packaging Deals(118 Total Transactions in 2005E)

Source: Blaige & Co.

Page 24

© Copyright 2006, all contents Thomas Blaige & Co. LLC

M&A Activity in the Global Plastics Packaging Markets M&A Activity in the Global Plastics Packaging Markets Film & Sheet most active with 49% of 2005E VolumeFilm & Sheet most active with 49% of 2005E Volume

2005E Plastics Packaging M&A active in both flexible and rigid p2005E Plastics Packaging M&A active in both flexible and rigid plastics lastics segments. segments. –– Film & Sheet sector most active with 58 deals (49%).Film & Sheet sector most active with 58 deals (49%).–– Blow Molding and Injection Molding sectors together register 40 Blow Molding and Injection Molding sectors together register 40 deals (34%).deals (34%).

Injection Molding19%

Raw Materials5%

Misc.10%

Film & Sheet49%

Extrusion (Pipe, Profile, Tube)2%

Blow Molding15%

Source: Thomas Blaige & Company LLC

Page 25

© Copyright 2006, all contents Thomas Blaige & Co. LLC

M&A Activity in the Global Plastics Packaging MarketsM&A Activity in the Global Plastics Packaging MarketsPlastics Packaging Segment Profile: Film & SheetPlastics Packaging Segment Profile: Film & Sheet

Private / Other Sales

66%

Financial Divestiture8%

Corporate Divestitures26% Strategic

Buyers65%

Financial Strategic11%

Private Equity Platforms24%

44 46 3266 74 76

0

20

40

60

80

2000 2001 2002 2003 2004 2005E

Deal Activity

2005E Sellers 2005E Buyers

Source: Blaige & Co.Source: Blaige & Co.

Source: Thomas Blaige & Company LLC

Page 26

© Copyright 2006, all contents Thomas Blaige & Co. LLC

M&A Activity in the Global Plastic Packaging Markets M&A Activity in the Global Plastic Packaging Markets Private Equity Interest is Also Driving Volume in Plastic PackagPrivate Equity Interest is Also Driving Volume in Plastic Packaging ing ––Including Flexible Packaging SpecificallyIncluding Flexible Packaging Specifically

Bank of America CapitalBank of America Capital(FlexSol Packaging Corporation, (FlexSol Packaging Corporation, AlfathermAlfatherm SpASpA, Rex Packaging*), Rex Packaging*)

Red Diamond CapitalRed Diamond Capital(Allied Extruders, P&O (Allied Extruders, P&O Packaging, Packaging, InterflexInterflex, Hi, Hi--Tech Tech Rubber)Rubber)

TrivestTrivest Partners LP Partners LP (Atlantis Plastics, Inc., Jet (Atlantis Plastics, Inc., Jet Plastica, Rutland Plastics*, Plastica, Rutland Plastics*, Plassein Packaging*)Plassein Packaging*)

TricorTricor Pacific CapitalPacific Capital((TharcoTharco Packaging, Keyes Packaging, Keyes Packaging, Matrix Packaging, Packaging, Matrix Packaging, Beresford Box, Pacifica Papers)Beresford Box, Pacifica Papers)

CandoverCandover PLCPLC((InnoviaInnovia Films, Films, ClondalkinClondalkin*)*)

Sun Capital Partners Sun Capital Partners ((ExoPackExoPack, Cello, Cello--Foil, Atlas Die*)Foil, Atlas Die*)

Stonebridge PartnersStonebridge Partners(Delta Plastics, Alpha Packaging)(Delta Plastics, Alpha Packaging)

Oak Tree Capital ManagementOak Tree Capital Management(Nordenia International)(Nordenia International)

Key Principal Partners Key Principal Partners ((AmpacAmpac, , NampakNampak*, Imperial *, Imperial Plastics, MidPlastics, Mid--America Packaging America Packaging Group)Group)

Linsalata Linsalata (Paradigm Packaging, Snyder (Paradigm Packaging, Snyder Industries*)Industries*)

Sterling GroupSterling Group((ExoPackExoPack*, Sterling Chemicals*, *, Sterling Chemicals*, Pawnee Industries*, Vista Pawnee Industries*, Vista Chemical*)Chemical*)

Castle HarlanCastle Harlan(Associated Packaging Tech)(Associated Packaging Tech)

Apollo ManagementApollo Management(Tyco Plastics)(Tyco Plastics)

Susquehanna Capital Susquehanna Capital (C(C--P Flexible Packaging)P Flexible Packaging)

Glencoe CapitalGlencoe Capital((PolyairPolyair Inter Pack, Inc.)Inter Pack, Inc.)

Kohlberg & CompanyKohlberg & Company((ThilmanyThilmany/Packaging Dynamics, /Packaging Dynamics, RanpakRanpak*)*)

EM Warburg EM Warburg PincusPincus & Co & Co --((ClondalkinClondalkin Group)Group)

Bridgepoint Bridgepoint (CFP Flexible Packaging)(CFP Flexible Packaging)

* Indicates legacy investment

Page 27

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Packaging Industry Global ConsolidationPackaging Industry Global ConsolidationRecentRecent Flexible PackagingFlexible Packaging Headline DealsHeadline DealsTransactionTransaction SellerSeller BuyerBuyer

FinancialFinancial Tyco Plastics and AdhesivesTyco Plastics and Adhesives Apollo Capital ManagementApollo Capital Management

FinancialFinancial AEP (Australia Div.)AEP (Australia Div.) Prudential / Catalyst Capital ManagementPrudential / Catalyst Capital Management

Financial Financial NordeniaNordenia AGAG Oak Tree PartnersOak Tree Partners

FinancialFinancial Allied ExtrudersAllied Extruders Red Diamond CapitalRed Diamond Capital

Financial Financial Plastics Packaging TechnologyPlastics Packaging Technology Stonehenge Partners Stonehenge Partners

StrategicStrategic PCL (Coastal Div.)/Mercury PlasticsPCL (Coastal Div.)/Mercury Plastics Sigma Plastics GroupSigma Plastics Group

StrategicStrategic FlexiaFlexia Corp/FibCorp/Fib--PakPak IntertapeIntertape Polymer GroupPolymer Group

Financial / StrategicFinancial / Strategic Plastics Packaging TechnologyPlastics Packaging Technology Stonehenge Partners (Wisconsin Film & Bag)Stonehenge Partners (Wisconsin Film & Bag)

Financial Financial PactivPactiv Flexible Packaging Div. (Flexible Packaging Div. (PregisPregis)) AEA Investors LLCAEA Investors LLC

Financial / StrategicFinancial / Strategic ExopackExopack/Cello/Cello--Foil/TPGFoil/TPG Sun Capital PartnersSun Capital Partners

Financial / StrategicFinancial / Strategic Vanguard PlasticsVanguard Plastics Dewberry Dewberry CesingerCesinger Hodgson (Hodgson (HilexHilex--Poly)Poly)

Financial / StrategicFinancial / Strategic Packaging DynamicsPackaging Dynamics Kohlberg & Co. (Kohlberg & Co. (ThilmanyThilmany))

Financial / StrategicFinancial / Strategic P&O PackagingP&O Packaging Red Diamond Capital (Allied Extruders)Red Diamond Capital (Allied Extruders)

StrategicStrategic Dixie TogaDixie Toga Bemis Inc.Bemis Inc.

StrategicStrategic New England ExtrusionNew England Extrusion AppletonAppleton

Page 28

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Watch List: Active Acquirers in the Flexible Packaging SectorWatch List: Active Acquirers in the Flexible Packaging Sector

AEPAEP AlcoaAlcoa FlexSolFlexSol LinpacLinpac SCASCA--TuscaroraTuscarora

AlcanAlcan

AmcorAmcor

AmpacAmpac

AppletonAppleton ExopackExopack KlocknerKlocknerPentaplastPentaplast

PrintpackPrintpack ViapackViapack

BemisBemis GenpakGenpak MondiMondiPackagingPackaging

Sealed AirSealed Air

ClondalkinClondalkin / / FortuneFortune

HPCHPC NordeniaNordeniaInternationalInternational

Sigma Sigma PlasticsPlastics

DuPontDuPont ITWITW PactivPactiv Tyco Tyco PlasticsPlastics

Page 29

© Copyright 2006, all contents Thomas Blaige & Co. LLC

M&A Activity in the Global Plastic Packaging MarketsM&A Activity in the Global Plastic Packaging MarketsPackaging Industry Focus

Valuation Trends: Transaction pricing among major deals has remaValuation Trends: Transaction pricing among major deals has remained ined in a relatively tight band (averaging 6.8x EBITDA) over the pastin a relatively tight band (averaging 6.8x EBITDA) over the past several several years.years.

Packaging Precedent Transactions LTM FV / EBITDA Multiples

8.3x

7.8x

6.1x

8.0x

6.7x7.0x

7.9x

7.4x

6.0x

6.4x

6.9x

6.5x

7.0x 7.1x

6.0x 5.9x6.1x

6.8x

6.1x 6.0x

7.6x

5.0x

5.5x

6.0x

6.5x

7.0x

7.5x

8.0x

8.5x

9.0x

Uniflex

Blessin

gsUltra

PacExxo

n Films

Rex Int

l

Alfathe

rme S

pA Ivex

Caffaro

SpA

Walki F

ilms

Rexam H

ealthc

are Pkg

VAW Flex Pkg

Landis

Plastic

sClon

dalki

nPech

iney

Hilex Poly

Dixi

e Tog

a

AEP Aust

ralasi

an D

ivisio

n

Pactiv

Prot. Pkg

Exopa

ck Hold

ing Corp

.Tyco

Plastic

s

Packagi

ng D

ynam

ics

Mean = 6.8x

Page 30

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Conclusion: M&A is an Essential Tool for Success in the Conclusion: M&A is an Essential Tool for Success in the Packaging IndustryPackaging Industry

Selecting and Executing the Right Strategy is Key…Selecting and Executing the Right Strategy is Key…

ARE YOU A CONSOLIDATOR?ARE YOU A CONSOLIDATOR?

OR A CONSOLIDATEE?OR A CONSOLIDATEE?

Page 31

© Copyright 2006, all contents Thomas Blaige & Co. LLC

V. The Art:V. The Art:Maximizing Value Maximizing Value PriorPrior to the to the

TransactionTransaction

Page 32

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value PriorPrior to the Transaction to the Transaction 1. Start Early 1. Start Early –– Establish a Five Year PlanEstablish a Five Year Plan

Consult with Professionals who have Actual Operating Consult with Professionals who have Actual Operating Experience in your Industry to:Experience in your Industry to:–– Evaluate your options, establish your target price, structure anEvaluate your options, establish your target price, structure and d

termsterms–– Determine what strategic and tactical actions are necessary to Determine what strategic and tactical actions are necessary to

achieve target price and termsachieve target price and terms

Don’t Wait Until You are Ready to Retire:Don’t Wait Until You are Ready to Retire:–– Realize that you may need to stay on for 1 to 3 yearsRealize that you may need to stay on for 1 to 3 years–– Develop and implement a succession plan Develop and implement a succession plan –– Identify “perks” in the context of a transaction Identify “perks” in the context of a transaction

title, board seat, office, car, club, compensation, real estate title, board seat, office, car, club, compensation, real estate lease, lease, protection of family members, key management in the businessprotection of family members, key management in the business

Page 33

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value PriorPrior to the Transaction to the Transaction 2. Implement Actions which will Create the Most Appeal to Potent2. Implement Actions which will Create the Most Appeal to Potential Investorsial Investors

Maintain OperationsMaintain Operations–– Don’t milk value out by underinvesting in PP&E Don’t milk value out by underinvesting in PP&E

maintain core infrastructuremaintain core infrastructure

–– Invest to accommodate capacity required over next 2 Invest to accommodate capacity required over next 2 yearsyears

Complete major capital investments 6 months prior to Complete major capital investments 6 months prior to transactions so that benefits can show up in earningstransactions so that benefits can show up in earnings

–– Invest in technology and systems which are at least Invest in technology and systems which are at least comparable to those of your competitorscomparable to those of your competitors

–– Establish well developed “metrics” by which to operate Establish well developed “metrics” by which to operate the business, know how you “stack up”the business, know how you “stack up”

Page 34

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value PriorPrior to the Transaction to the Transaction 2. Implement Actions which will Create the Most Appeal to Potent2. Implement Actions which will Create the Most Appeal to Potential Investorsial Investors

Market LeadershipMarket LeadershipClearly define your niche, communicate internally and externallyClearly define your niche, communicate internally and externally

Strengthen position and maximize share of core market nicheStrengthen position and maximize share of core market niche

Establish meaningful presence in new marketsEstablish meaningful presence in new markets

Concentrate on growing marketsConcentrate on growing markets

Minimize Customer and Supplier ConcentrationMinimize Customer and Supplier ConcentrationEstablish customer integration and intimacy Establish customer integration and intimacy –– deep knowledge deep knowledge and broad contacts across both organizationsand broad contacts across both organizations

Establish sole source positions, value versus price orientation,Establish sole source positions, value versus price orientation,high switching costshigh switching costs

Obtain written contractsObtain written contracts

Page 35

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value PriorPrior to the Transaction to the Transaction 3. Capture Value Typically Realized by Buyers3. Capture Value Typically Realized by Buyers

Create Internal Liquidity, EfficiencyCreate Internal Liquidity, Efficiency–– Aggressively manage working capital Aggressively manage working capital –– RE sale/leaseback, unload marginal operationsRE sale/leaseback, unload marginal operations–– Pay down as much debt as possiblePay down as much debt as possible

Consider Acquisition OpportunitiesConsider Acquisition Opportunities–– Identify, visit and create “warm” acquisition Identify, visit and create “warm” acquisition

opportunities opportunities –– Opportunistically acquire a competitor, product line or Opportunistically acquire a competitor, product line or

technologytechnology

Page 36

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value PriorPrior to the Transaction to the Transaction 3. Capture Value Typically Realized by Buyers (cont.)3. Capture Value Typically Realized by Buyers (cont.)

Professionalize and Institutionalize Organization to Handle Professionalize and Institutionalize Organization to Handle an Operation Twice its Sizean Operation Twice its Size–– Hire an outside CEO and CFO, bring in outside board, develop Hire an outside CEO and CFO, bring in outside board, develop

bench strengthbench strength–– Make the tough decisions Make the tough decisions –– remove dead wood, improve metrics remove dead wood, improve metrics

Elevate Importance of Financial ManagementElevate Importance of Financial Management–– Audited financials, monthly reporting package by the 5Audited financials, monthly reporting package by the 5thth

–– Keep clean financials Keep clean financials –– take lumps on bad inventory and A/R, take lumps on bad inventory and A/R, identify and track discretionary expenses (add backs) identify and track discretionary expenses (add backs)

–– CEO and CFO must be savvy with regard to capital sourcing and CEO and CFO must be savvy with regard to capital sourcing and structuring, RE and M&A deal makingstructuring, RE and M&A deal making

Page 37

© Copyright 2006, all contents Thomas Blaige & Co. LLC

VI. Full or Partial Exit StrategiesVI. Full or Partial Exit Strategies

Page 38

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Full or Partial Exit Strategies Full or Partial Exit Strategies 1. Partial Exit Strategies1. Partial Exit Strategies

Divestiture of an Operation / Product LineDivestiture of an Operation / Product Line

JV / Strategic Alliance JV / Strategic Alliance

Private Placement of Equity or Debt (Typically Growth Private Placement of Equity or Debt (Typically Growth Capital)Capital)

Initial Public Offering of Stock / High Yield DebtInitial Public Offering of Stock / High Yield Debt

ESOPESOP

Inside Buy / Sell Inside Buy / Sell –– Partner, Management or FamilyPartner, Management or Family

Hire Professional Management, Take Out the ProfitsHire Professional Management, Take Out the Profits

Page 39

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Full or Partial Exit Strategies Full or Partial Exit Strategies 2. Full Exit Strategies2. Full Exit Strategies

Sale to Strategic BuyerSale to Strategic Buyer–– ObviousObvious–– Not obvious Not obvious

Sale to Financial Buyer (LBO)Sale to Financial Buyer (LBO)–– Currently there are 2,000 LBO funds in operation!Currently there are 2,000 LBO funds in operation!

Sale to Financial/Strategic Buyer Sale to Financial/Strategic Buyer –– Add on acquisition to existing portfolio companyAdd on acquisition to existing portfolio company

Recapitalization with Retained OwnershipRecapitalization with Retained Ownership–– Liquidity and diversification without stigma of “selling” Liquidity and diversification without stigma of “selling” –– Grow business aggressively with “OPM”Grow business aggressively with “OPM”–– Second “bite at the apple”Second “bite at the apple”

Page 40

© Copyright 2006, all contents Thomas Blaige & Co. LLC

VII. The Art:VII. The Art:Maximizing Value Maximizing Value DuringDuring the the

TransactionTransaction

Page 41

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value DuringDuring the Transaction Processthe Transaction ProcessImportant Quote: The Art Versus the Science of Deal MakingImportant Quote: The Art Versus the Science of Deal Making

“The merger business is 10% financial analysis and “The merger business is 10% financial analysis and

90% psychoanalysis”90% psychoanalysis”

–– Financier: The Biography of André Meyer: A Story of Financier: The Biography of André Meyer: A Story of Money, Power, and the Reshaping of American BusinessMoney, Power, and the Reshaping of American Business

Page 42

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value DuringDuring the Transaction Processthe Transaction ProcessEstablish and Stick to a Strict Marketing StrategyEstablish and Stick to a Strict Marketing Strategy

Don’t Do It YourselfDon’t Do It Yourself–– Sends Negative Signal Sends Negative Signal –– appearance of weakness and lack of appearance of weakness and lack of

sophistication to professional buyers (who as a rule never sell sophistication to professional buyers (who as a rule never sell on on their own)their own)

–– Distracting Distracting –– focus on maximizing performance of the business focus on maximizing performance of the business –– Effective Execution Essential Effective Execution Essential –– can add millions to the price, hire a can add millions to the price, hire a

firm that can understand your business firm that can understand your business andand deliver the best deliver the best buyers/investorsbuyers/investors

–– Ego Factor Ego Factor -- all owners “negotiate every day,” “personally know the all owners “negotiate every day,” “personally know the best buyers,” don’t want to be “on the market,” and already havebest buyers,” don’t want to be “on the market,” and already have a a “stable of buyers” who can “quietly” do a “quick deal”“stable of buyers” who can “quietly” do a “quick deal”

Don’t Assume that Competitors, Employees and Most Don’t Assume that Competitors, Employees and Most Likely Buyers Will Provide the Best DealLikely Buyers Will Provide the Best Deal

Page 43

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value DuringDuring the Transaction Processthe Transaction ProcessRarely Do Obvious Buyers Pay the Top PriceRarely Do Obvious Buyers Pay the Top Price

Do Most Likely Buyers Pay Top Price?

No87%

Yes13%

Source: Survey of previous clients

Page 44

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value During the Transaction ProcessMaximizing Value During the Transaction ProcessEstablish and Stick to a Strict Marketing Strategy (cont.)Establish and Stick to a Strict Marketing Strategy (cont.)

Create Competition Through a Highly Orchestrated Create Competition Through a Highly Orchestrated ProcessProcess–– Puts you in charge of selecting your partners not vice versaPuts you in charge of selecting your partners not vice versa–– Establish position of strength in negotiationsEstablish position of strength in negotiations–– Minimize risk of “broken deal” after the LOI is signedMinimize risk of “broken deal” after the LOI is signed

LOI best case scenario, only to be reduced as due diligence procLOI best case scenario, only to be reduced as due diligence proceedseeds

Purchase agreement contains one line indicating what you get, 50Purchase agreement contains one line indicating what you get, 50pages indicating what you may give backpages indicating what you may give back

Broken Deal and/or “Leaks” are DevastatingBroken Deal and/or “Leaks” are Devastating

Page 45

© Copyright 2006, all contents Thomas Blaige & Co. LLC

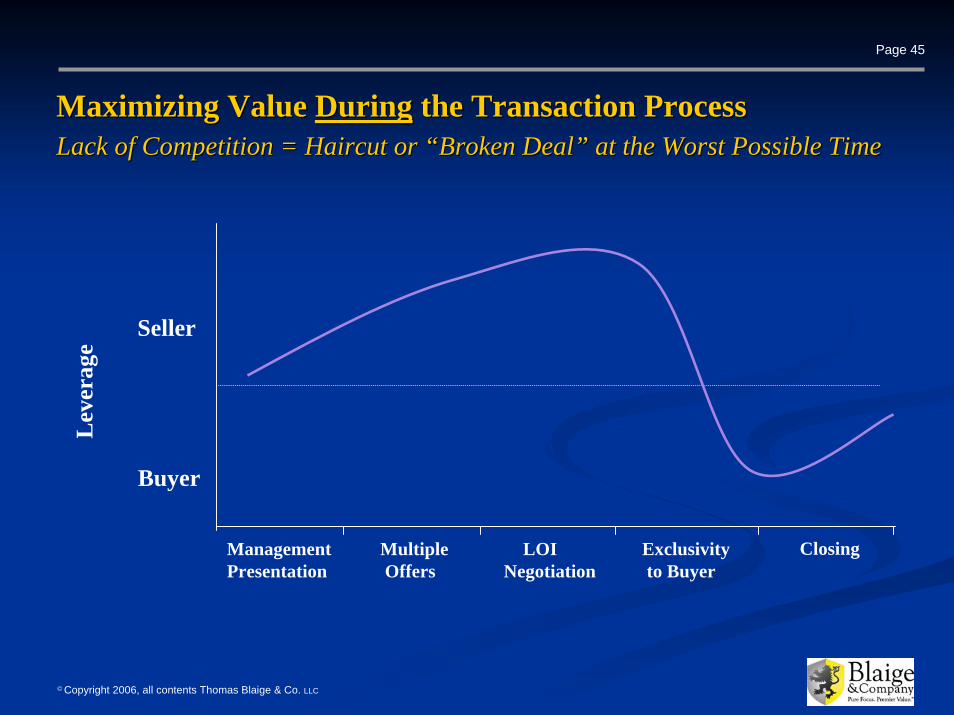

Maximizing Value Maximizing Value DuringDuring the Transaction Processthe Transaction ProcessLack of Competition = Haircut or “Broken Deal” at the Worst PossLack of Competition = Haircut or “Broken Deal” at the Worst Possible Timeible Time

Seller

Buyer

ManagementPresentation

MultipleOffers

LOINegotiation

Exclusivityto Buyer

Closing

Lev

erag

e

Page 46

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value During the Transaction ProcessMaximizing Value During the Transaction ProcessEstablish and Stick to a Strict Marketing Strategy (cont.)Establish and Stick to a Strict Marketing Strategy (cont.)

Effective Positioning is CriticalEffective Positioning is Critical–– Detail strengths and opportunities in a thoughtfully prepared Detail strengths and opportunities in a thoughtfully prepared

Confidential MemorandumConfidential Memorandum–– Focus on the future potential and synergies, not past historyFocus on the future potential and synergies, not past history–– Involve key managers Involve key managers –– they must “own” the process as they must “own” the process as

much as you do to maximize valuemuch as you do to maximize value–– Identify and address the negative issues up frontIdentify and address the negative issues up front–– Prepare a compelling Management Presentation to showcase Prepare a compelling Management Presentation to showcase

your team’s vision and capabilitiesyour team’s vision and capabilities–– Absolutely do not miss your budgets during the processAbsolutely do not miss your budgets during the process

Page 47

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Value to Prospective BuyerValue to Prospective Buyer

Maximizing Value Maximizing Value DuringDuring the Transaction Processthe Transaction ProcessFranchise Value Can Far Exceed Financial ValueFranchise Value Can Far Exceed Financial Value

M&AValuation

Lowest

Highest

Valuation Multiples

Lowest Multiples

Highest Multiples

Market Share Fold-ins

Key Customer Relationships

Geographic Market Expansion

Complementary Products

New Product Market Beachhead

New Brands or Franchises

New Technologies

Page 48

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value During the Transaction ProcessMaximizing Value During the Transaction ProcessEstablish and Stick to a Strict Marketing Strategy (cont.)Establish and Stick to a Strict Marketing Strategy (cont.)

Do Not Establish an Asking Price or TermsDo Not Establish an Asking Price or Terms–– The party which mentions price first is disadvantagedThe party which mentions price first is disadvantaged–– An asking price establishes a ceiling on valueAn asking price establishes a ceiling on value–– Franchise value can far exceed financial valueFranchise value can far exceed financial value–– Non cash, deferred consideration and retained ownership can provNon cash, deferred consideration and retained ownership can provide ide

opportunities to achieve the highest overall priceopportunities to achieve the highest overall price–– Negotiation of soft value issues should be done early in the proNegotiation of soft value issues should be done early in the processcess–– Negotiation of escrows, indemnification caps, baskets and survivNegotiation of escrows, indemnification caps, baskets and survival al

periods should be done prior to signing an LOIperiods should be done prior to signing an LOI

Page 49

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Maximizing Value Maximizing Value DuringDuring the Transaction Processthe Transaction ProcessA Single Offer is Likely to Converge at 70% of the Final PriceA Single Offer is Likely to Converge at 70% of the Final Price

Imperfect MarketImperfect Market

Serious Indications of Interest(typically 10 data points)

0% 15%

30%

45%

60%

75%

90%

Valuation (% of Final Transaction Price)

Num

ber

of B

uyer

s

Final Transaction Price

Page 50

© Copyright 2006, all contents Thomas Blaige & Co. LLC

VIII. SummaryVIII. Summary

Page 51

© Copyright 2006, all contents Thomas Blaige & Co. LLC

SummarySummaryKey TakeawaysKey Takeaways

Create a Credible, Concrete Vision of How the Create a Credible, Concrete Vision of How the Business Can Grow SignificantlyBusiness Can Grow Significantly

Do Not Establish an Asking Price Do Not Establish an Asking Price

Involve Multiple Bidders Involve Multiple Bidders

Create Transaction Options for YourselfCreate Transaction Options for Yourself

The Best Deal Will be ObviousThe Best Deal Will be Obvious

Page 52

© Copyright 2006, all contents Thomas Blaige & Co. LLC

IX. AppendixIX. Appendix

Page 53

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Blaige & CompanyBlaige & CompanyPackaging Industry CredentialsPackaging Industry Credentials

BlaigeCo bankers are believed to have completed more strategic transactions in the plastic packaging space than any other middle market advisor. Examples include transactions with:

Alloyd Corp., BWAY Corp., Empire Plastics, FlexSol Holdings, Caraustar Industries, Clondalkin Group, DuPont Corporation, Fleming Packaging, Honeywell International, Illinois Tool Works Inc., International Paper, Klockner Pentaplast, Koch Industries, Mitsubishi International, Pac One Corp., PCL Packaging Corp., Plastic Packaging Technologies, Pliant Corp., Renaissance Mark, Republic Bag, Reunion Industries, Rexam PLC, SCA, Sealed Air Corp., Sigma Plastics Group, Smurfit-Stone Corp., Sonoco Products Company, Tyco International Ltd., Viapack / Red Diamond Capital, Winpak, Ltd., Wisconsin Film & Bag, Inc.

BlaigeCo bankers have also completed transactions with or on behalf of nearly 50 private equity groups.

BlaigeCo possesses the industry standard in plastics M&A research, having tracked over 1,500 transactions in the past 5 years.

Strategic Value-added. Our specific focus and extensive deal and operating experience allow us to work as true strategic partners. We look beyond “the deal”.

Page 54

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Introduction to Blaige & CompanyPure Focus: Extensive Market PresencePure Focus: Extensive Market PresenceBlaige & Company sets the Industry Standard in Proprietary Global M&A Research:

Plastics DealBriefing Plastic Packaging DealBriefing Label Market DealBriefing

Page 55

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Thomas E. Blaige, Chief Executive Officer and Managing PartnerTom is widely published and a frequent speaker on M&A, buyouts and restructurings in the plastics, packaging and chemicals sectors. Tom has been quoted over twenty times in the past two years in leading industry publications. Tom has over 20 years of industry experience, having completed over 80 M&A, buyout and restructuring transactions. Over the past decade, he was managing director and established and led plastics industry groups at both Lincoln Partners and Goldsmith Agio. Tom was also an investment banker with a unit of Citigroup/Salomon Smith Barney and a private equity and debt investor with Prudential Capital Group.

Tom has extensive experience in structuring complex transactions including mergers, acquisitions, divestitures, buyouts, recapitalizations and restructurings on behalf of public companies, private companies, private equity investors and financial institutions. Tom combines strong negotiating, analytical and deal execution capabilities with extensive industry knowledge to orchestrate highly tailored acquisition and sale processes in which key value drivers are customized to each potential target or acquirer, thereby obtaining the best pricing and certainty of closing.

Tom is a member of the Society of Plastics Industry, its Molders Division and its Film & Bag Federation (4 years), and the Society of Plastics Engineers. He is also a member of the Association for Corporate Growth and the Turnaround Management Association. Tom earned a Master of Management degree, with Distinction, from the Kellogg Graduate School of Management at Northwestern University, where he was elected to Beta Gamma Sigma, and a Bachelor of Business Administration degree from Loyola University of Chicago. He has been certified as a NASD Series 24 Securities Principal, and a Series 7 and 63 Registered Representative.

Introduction to Blaige & CompanyIntroduction to Blaige & CompanyPure Focus. Premier ValuePure Focus. Premier ValueSMSM

Page 56

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Jonathan T. White, PresidentJonathan brings both direct industry experience and investment banking experience in plastics and packaging markets. Jonathan leads transaction execution, markets the firm’s services, and provides support to all firm clients.

Jonathan developed a strong base in the packaging industry through several years of hands on experience with Rexam PLC, one of the world’s largest packaging firms. While with Rexam, Jonathan was in corporate development for Rexam’s businesses based in North and South America, and then more intensively led corporate development efforts for Rexam’s Healthcare Packaging businesses. While at Rexam, Jonathan reviewed over 50 packaging transactions in the medical, food & beverage, industrial, and other industries. Jonathan also spent two years in production management with Rexam, helping greenfield a plant as a floor production manager and as interim materials manager. Jonathan uses these experiences to gain insight into the operations and practices of client, target, and acquiring firms.

Jonathan was previously a vice president with Mesirow Financial’s Investment Banking Group in Chicago, where he was instrumental in building the plastics and packaging expertise within that firm. Jonathan originated and executed transactions including sell-side advisory services for privately-held corporations and private placements of equity.

Jonathan earned a Masters of Business Administration from Darden Graduate School of Business Administration at the University of Virginia, and a Bachelor of Science in Business Administration degree from the University of North Carolina, where he was elected Phi Beta Kappa. Jonathan has been certified as a NASD Series 7 and 63 Registered Representative.

Introduction to Blaige & CompanyIntroduction to Blaige & CompanyPure Focus. Premier ValuePure Focus. Premier ValueSMSM

Page 57

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Edwin W. Parkinson, Executive AdvisorEd has over thirty years of experience in the plastics, packaging, and chemicals industries, including several board and senior management positions, as well as extensive experience in strategic acquisitions and divestitures worldwide. Ed currently serves on the board of directors of Sencorp, a leading producer of packaging equipment owned by private equity sponsor, Management Capital, and has served as a board member of Amrep, Inc., Alloyd Inc. and Avborne Inc. Ed’s experience with private equity sponsors also includes senior positions with Viasystems Inc.

Ed has a history of quickly and effectively creating value through managing middle market companies on behalf of professional investors. His experiences at the firms below are indicative of his unique capabilities:

Amrep, Inc. (Blue Point Capital Partners & MCM Capital Partners portfolio company) – Ed became president & CEO of this leading US producer of janitorial/sanitation and automotive chemicals in 2004 and completed a strategic repositioning of the company. Alloyd, Inc. (Wind Point Partners portfolio company) – Ed joined as Chairman & CEO of this leading North American Thermoformer serving consumer packaging and retail markets. He divested its calendering operation to Klockner Pentaplast and subsequently sold the entire company to SCA/Tuscarora (Sweden) in a $97 million cross-border strategic transaction.Avborne, Inc. (Trivest Partners portfolio company) – Ed was president & CEO of this leading aircraft heavy maintenance and accessory services provider on the Miami airport property.Viasystems, Inc. (Hicks, Muse, Tate and Furst portfolio company) – Ed held the post of President, Viasystems Europe, based in London, and completed several acquisitions in Europe with this global printed circuit board and contract manufacturing company.

Ed earned a Bachelor of Science in Marketing from The Pennsylvania State University.

Introduction to Blaige & CompanyIntroduction to Blaige & CompanyPure Focus. Premier ValuePure Focus. Premier ValueSMSM

Page 58

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Clas M. Nilstoft, Executive AdvisorClas brings a long record of achievements in the plastics, packaging and chemicals markets. Serving as an Executive Advisor, he brings particular insights in marketing, operations, and deal dynamics that provide support throughout the transaction process for the firm’s clients.

Clas has over thirty years experience in injection molding of industrial products and in consumer packaging. His key experiences were at ITW and Rexam, where he managed business units ranging from $35 to $200 million in revenues, with the distinction of achieving sustained, double-digit organic growth in profits and sales. Clas has been responsible for establishing new businesses, as well as acquiring, integrating, and consolidating operations in global markets. Over the years, Clas has gained first-hand knowledge of plastics manufacturing as a tool apprentice in Sweden, a financial analyst, a product manager, and as a CEO. He is currently a Board member of Creative Forming, a Wisconsin-based thermoformer.

As an entrepreneur, Clas successfully acquired Walboro and developed it into Nortec Precision Plastics, which he subsequently sold to Cambridge Industries (now Meridian). Clas has been involved in 22 acquisitions, 10 joint ventures, and 12 divestitures. Other transaction highlights include:

Clas earned a Masters of Business Administration from American University and has completed Executive Programs at both Northwestern University and the University of Michigan.

Introduction to Blaige & CompanyIntroduction to Blaige & CompanyPure Focus. Premier ValuePure Focus. Premier ValueSMSM

For Carborundum/BPFor Carborundum/BP For ITWFor ITW For Rexam PLCFor Rexam PLC

Acquisition of Astrel (from 3M)Acquisition of Astrel (from 3M) Acquisition of DevconAcquisition of Devcon Acquisition of Plasticos DumexAcquisition of Plasticos Dumex

Acquisition of Dielectix (from DuPont)Acquisition of Dielectix (from DuPont) Acquisition of DuPont Adhesives DivisionAcquisition of DuPont Adhesives Division Divestitures of 4 molding operationsDivestitures of 4 molding operations

JV with Sumitomo ChemicalJV with Sumitomo Chemical Sale of Eclipse DivisionSale of Eclipse Division Development of Chinese SubsidiaryDevelopment of Chinese Subsidiary

Sale of Pine Bluff Drill DivisionSale of Pine Bluff Drill Division

Page 59

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Thomas P. Sullivan, Vice PresidentTom brings significant transaction experience, including transactions in the plastics, packaging and chemicals industries, having worked as a banker for two of the largest financial institutions in the world.

Tom was most recently a Vice President with Bank of America. Transactions included providing financing for buyouts, restructurings and recapitalizations. Prior to joining Bank of America, Tom was an Associate with Deutsche Bank Securities Inc. where he acted in a similar capacity. Tom began his career in public accounting at PricewaterhouseCoopers LLP.

Tom earned a Masters of Business Administration, with honors, from the University of Chicago Graduate School of Business, where he was elected to Beta Gamma Sigma, and a Bachelor of Business Administration in Accountancy from the University of Notre Dame, graduating summa cum laude. Tom also has his CPA certificate.

Introduction to Blaige & CompanyIntroduction to Blaige & CompanyPure Focus. Premier ValuePure Focus. Premier ValueSMSM

Page 60

© Copyright 2006, all contents Thomas Blaige & Co. LLC

Blaige & CompanyBlaige & CompanyContact SheetContact Sheet

Blaige & Company (www.blaige.com)Blaige & Company (www.blaige.com)100 East Huron Street100 East Huron StreetSuite 2703Suite 2703Chicago, IL 60611Chicago, IL 60611Tel: (312) 335Tel: (312) 335--54175417Fax: (312) 335Fax: (312) 335--54185418

Thomas E. BlaigeThomas E. Blaige Jonathan T. WhiteJonathan T. WhiteCEO & Managing Partner CEO & Managing Partner President President Cell: 312Cell: 312--925925--88268826 Cell: 773Cell: [email protected]@blaige.com [email protected]@blaige.com

Edwin W. Parkinson Edwin W. Parkinson Clas M. NilstoftClas M. NilstoftExecutive Advisor Executive Advisor Executive Advisor Executive Advisor Cell: 404Cell: 404--276276--3636 3636 Cell: 812Cell: [email protected]@blaige.com [email protected]@blaige.com

Top Related