Languages

Pages

Legal

Global Economic Turmoil,Catastrophic Loss and Insurance:Implications for Risk Management

in the Post-Crisis WorldAmerican Institute of Marine Underwriters

Insurance Issues SeminarNew York, NY

Download at www.iii.org/presentationsRobert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Presentation Outline

Is the World Becoming a Riskier Place?Recent Events and Implications for the Global P/C (Re)Insurance Industry

The Global Financial Crisis, Risk and the New World Order

Global Economic and Trade Outlook

The Unfortunate Nexus: Opportunity, Risk & InstabilityFuture growth is necessarily fraught with greater riskTypes, magnitude of risk inherent in future growth opportunities

Reshuffling the Global Economic DeckThe Ascendency of China

Foreign Direct Investment (FDI) and insurance exposure/demand

P/C Insurance Financial Overview & Outlook

Q&A

3

What in the World IsGoing On?

Is the World Becoming aRiskier Place?

Are We Really Crawling Out of theAbyss or Falling Into a New One?

4

Uncertainty, Risk and Fear Abound

Resurgent Terrorism Risk (e.g., Bin Laden Killing)Record Tornado Activity & Flooding in the USJapan, New Zealand, Haiti, Chile EarthquakesPolitical Upheaval in the Middle EastEchoes of the Financial CrisisHousing CrisisUS Debt and Budget CrisisSovereign Debt & Currency Crises InflationRunaway Energy & Commodity PricesEra of Fiscal AusterityReshuffling the Global Economic DeckChina Becomes #2 Economy in the WorldNuclear FearsManmade Disasters (e.g., Deepwater Horizon)

Are “Black Swans”everywhere or

does it just seemthat way?

5

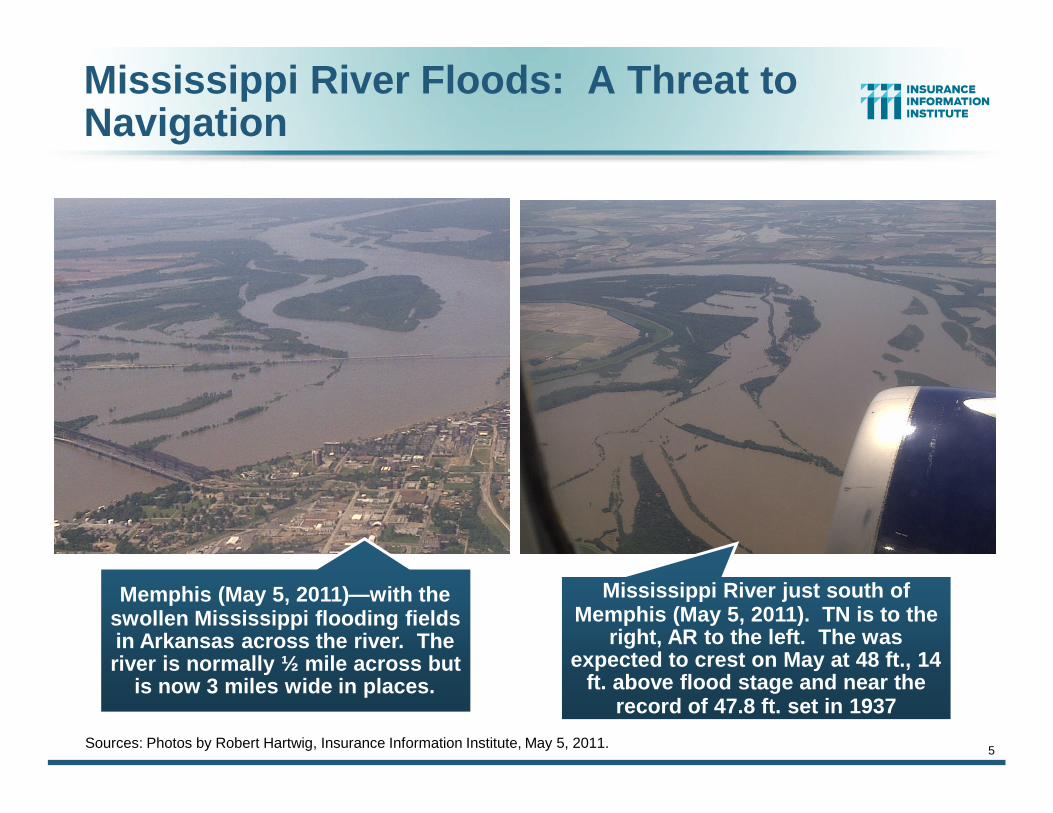

Mississippi River Floods: A Threat toNavigation

Memphis (May 5, 2011)—with theswollen Mississippi flooding fieldsin Arkansas across the river. Theriver is normally ½ mile across but

is now 3 miles wide in places.

Mississippi River just south ofMemphis (May 5, 2011). TN is to the

right, AR to the left. The wasexpected to crest on May at 48 ft., 14

ft. above flood stage and near therecord of 47.8 ft. set in 1937

Sources: Photos by Robert Hartwig, Insurance Information Institute, May 5, 2011.

6

Terrorism, Insurance and theKilling of Osama bin Laden

Is the World Less Risky and Do WeStill Need the Terrorism Risk

Insurance Program?

7

Bin Laden, Justice and the Future ofTerrorism, Risk and Insurance

Sources: Insurance Information Institute.

Property-WTCProperty -

Other

Bin Laden is Dead and Justice Is Served, But What Arethe Implications for the P/C Insurance Industry?

8

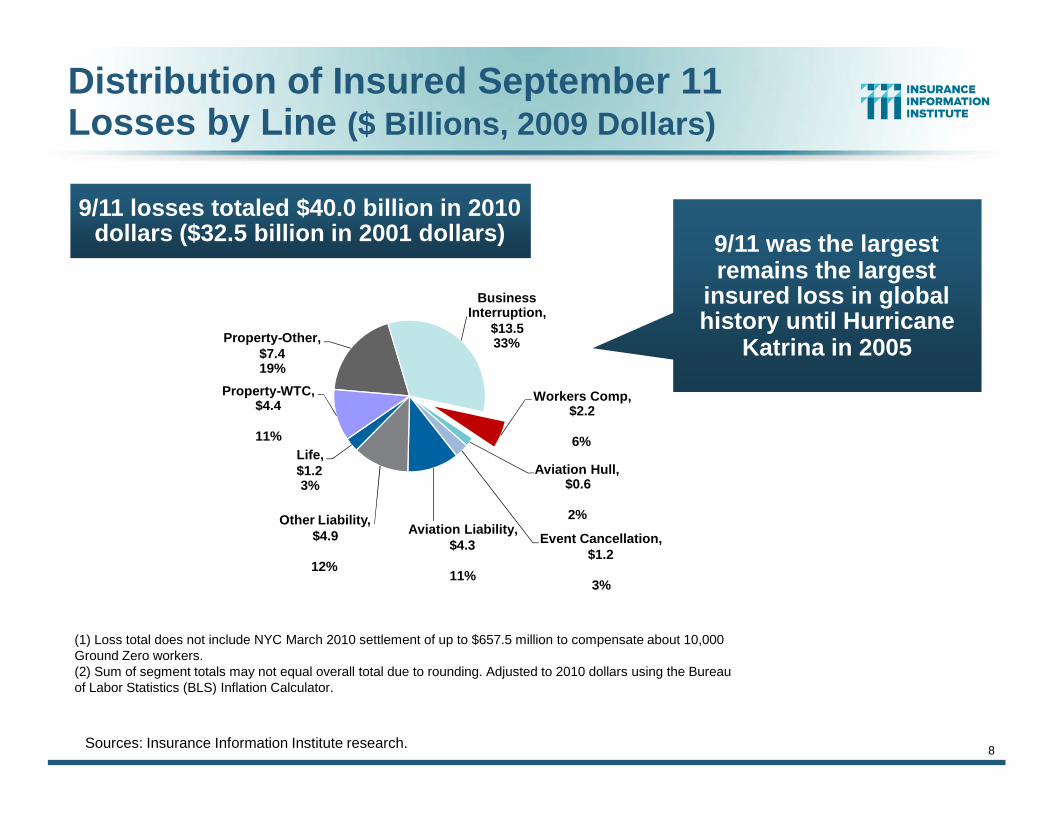

Distribution of Insured September 11Losses by Line ($ Billions, 2009 Dollars)

Sources: Insurance Information Institute research.

Property-WTCProperty -

Other

Property-Other,$7.419%

BusinessInterruption,

$13.533%

Workers Comp,$2.2

6%

Aviation Hull,$0.6

2%

Event Cancellation,$1.2

3%

Aviation Liability,$4.3

11%

Other Liability,$4.9

12%

Life,$1.23%

Property-WTC,$4.4

11%

(1) Loss total does not include NYC March 2010 settlement of up to $657.5 million to compensate about 10,000Ground Zero workers.(2) Sum of segment totals may not equal overall total due to rounding. Adjusted to 2010 dollars using the Bureauof Labor Statistics (BLS) Inflation Calculator.

9/11 losses totaled $40.0 billion in 2010dollars ($32.5 billion in 2001 dollars) 9/11 was the largest

remains the largestinsured loss in globalhistory until Hurricane

Katrina in 2005

9

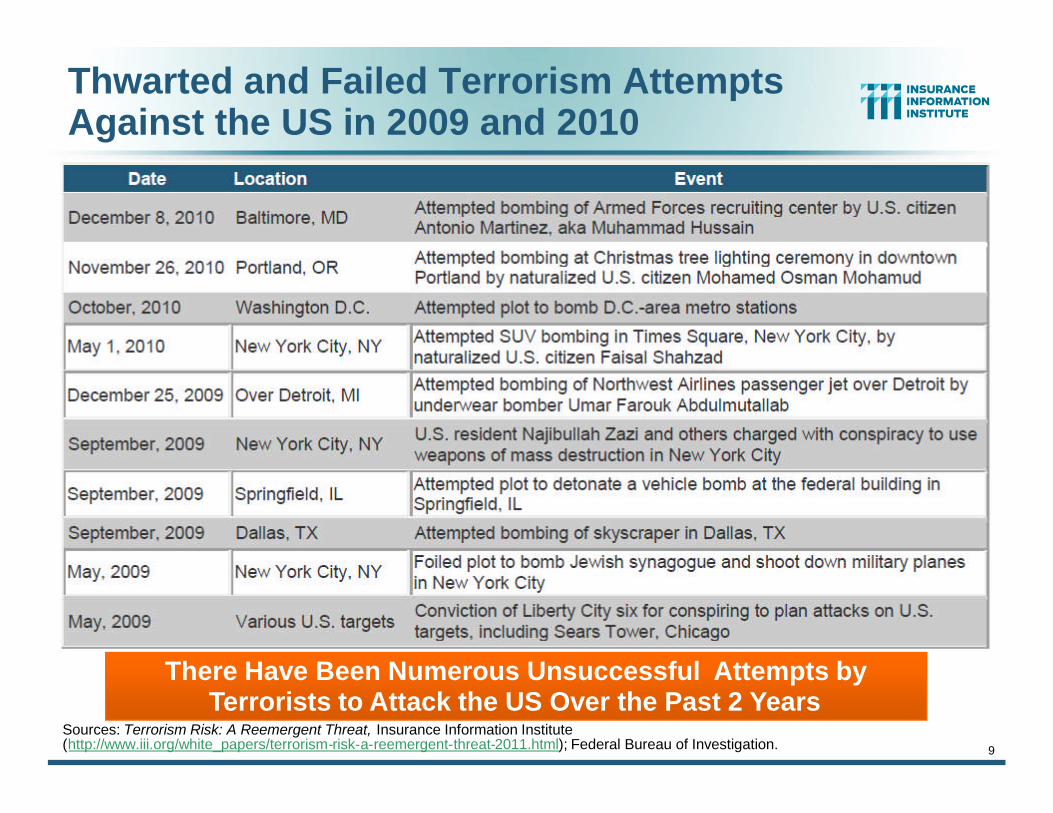

Thwarted and Failed Terrorism AttemptsAgainst the US in 2009 and 2010

Sources: Terrorism Risk: A Reemergent Threat, Insurance Information Institute(http://www.iii.org/white_papers/terrorism-risk-a-reemergent-threat-2011.html); Federal Bureau of Investigation.

Property-WTCProperty -

Other

9/11 remains the largestWC loss in US history($2.2 bn), even though

9/11 property losses weresurpassed by Hurricane

Katrina in 2005

There Have Been Numerous Unsuccessful Attempts byTerrorists to Attack the US Over the Past 2 Years

10

Summary of Japan Earthquake& Impacts on US P/C Markets

The March 11 Quake & Other MajorCATs Are Big Events, But Will They,Can They Impact US P/C Markets?

11

Location of March 11, 2011 EarthquakeNear Sendai, Honshu, Japan

Source: US Geological Service; Insurance Information Institute.

Magnitude 9.0 earthquake struckJapan at 2:46PM local time (2:46AMEastern) off northeast coast ofHonshu, 80 miles east of Sendai

Quake is among the 5 strongest inrecorded history and the strongest inthe 140 years for which recordshave been kept in Japan

12,000+ fatalities

Economic loss: $100 - $300 bn

Insured losses up to $45 bn

Fukushima Nuclear Plant threat levelraised to Category 7 on April 11(highest, same as Chernobyl)

Significant tsunami damage wasrecorded in Japan; relatively minordamage on the U.S. West Coast

March 11 Earthquake Factsas of 4/21/2011

LOCATION130 km (80 miles) E of Sendai, Honshu, Japan178 km (110 miles) E of Yamagata, Honshu, Japan178 km (110 miles) ENE of Fukushima, Honshu, Japan373 km (231 miles) NE of TOKYO, Japan

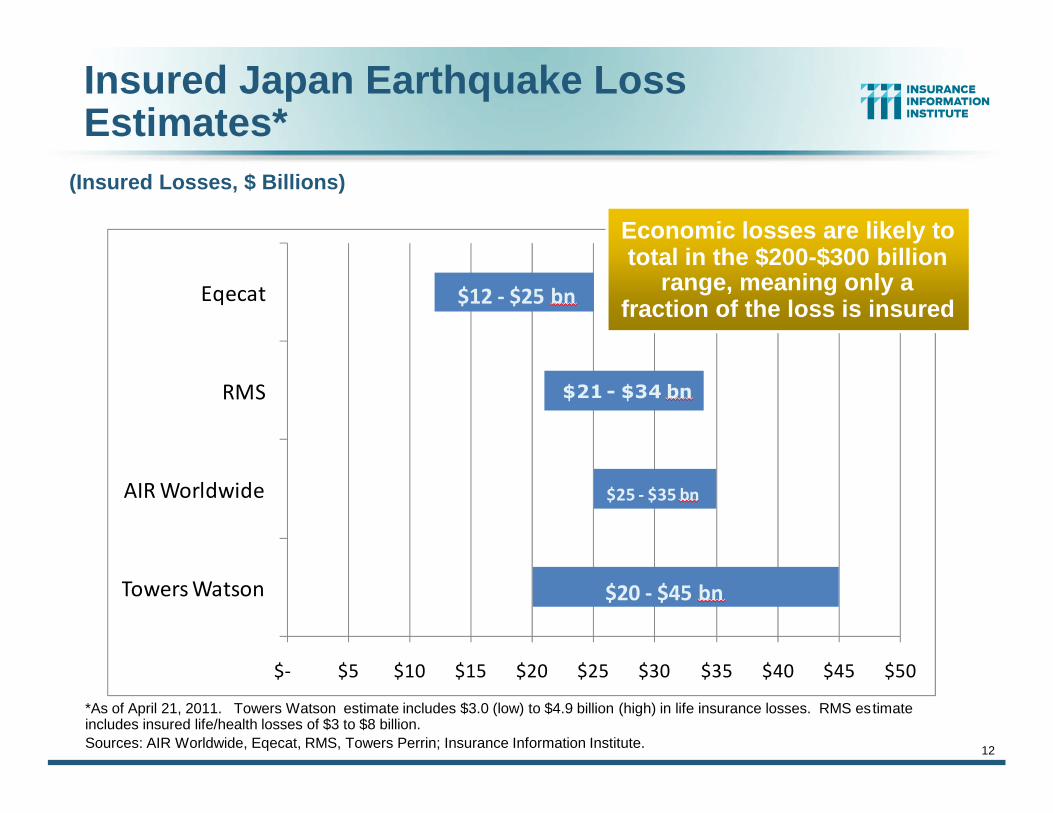

Insured Japan Earthquake LossEstimates*

$- $5 $10 $15 $20 $25 $30 $35 $40 $45 $50

Towers Watson

AIR Worldwide

RMS

Eqecat

$21 - $34 bn

$20 - $45 bn

$12 - $25 bn

$25 - $35 bn

12

*As of April 21, 2011. Towers Watson estimate includes $3.0 (low) to $4.9 billion (high) in life insurance losses. RMS estimateincludes insured life/health losses of $3 to $8 billion.Sources: AIR Worldwide, Eqecat, RMS, Towers Perrin; Insurance Information Institute.

(Insured Losses, $ Billions)

Economic losses are likely tototal in the $200-$300 billion

range, meaning only afraction of the loss is insured

13

Recent Major Catastrophe Losses

(Insured Losses, $US Billions)

Sources: Insurance Council of Australia, Munich Re, AIR Worldwide; Insurance Information Institute.

$30.0

$10.0$8.0

$5.0$2.0$0.5

$0

$5

$10

$15

$20

$25

$30

$35

Cyclone Yasi(Australia) Feb

2011

Australia Floods(Dec - Feb 2011)

New ZealandQuake (Sep 2010)

Chile Earthquake(Feb 2010)

New ZealandQuake (Feb 2011)

Japan Earthquake(Mar 2011)

Insured Losses from Recent Major Catastrophe Events Exceed$55 Billion, an Estimated $53 Billion of that from Earthquakes

The March 2011 earthquake in Japan willbecome among the most expensive in worldhistory in terms of insured losses (current

leader is the 1994 Northridge earthquake with$22.5B in insured losses in 2010 dollars)

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

1985 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1998 1999 2001 2002 2003 2004 2005 2007 2008 2009 2010 2011

Bill

ion

s

Worldwide Direct Insured Losses Reinsured Losses

Reinsurers’ share of majormarket losses was

exceptionally high in 2010and early 2011

Source: Holborn; RAA.

* 2011 events are as of March 31 and are preliminary and may change as loss estimates are refined further.

Significant Market Losses, 1985-2011*

15

Change in Reinsurer Capital, 2007-2010:Q3

16

Potential Impacts of JapanQuake & Other Major CATs on

P/C (Re)Insurance Markets

Impacts Could Be Felt WellBeyond Japan

17

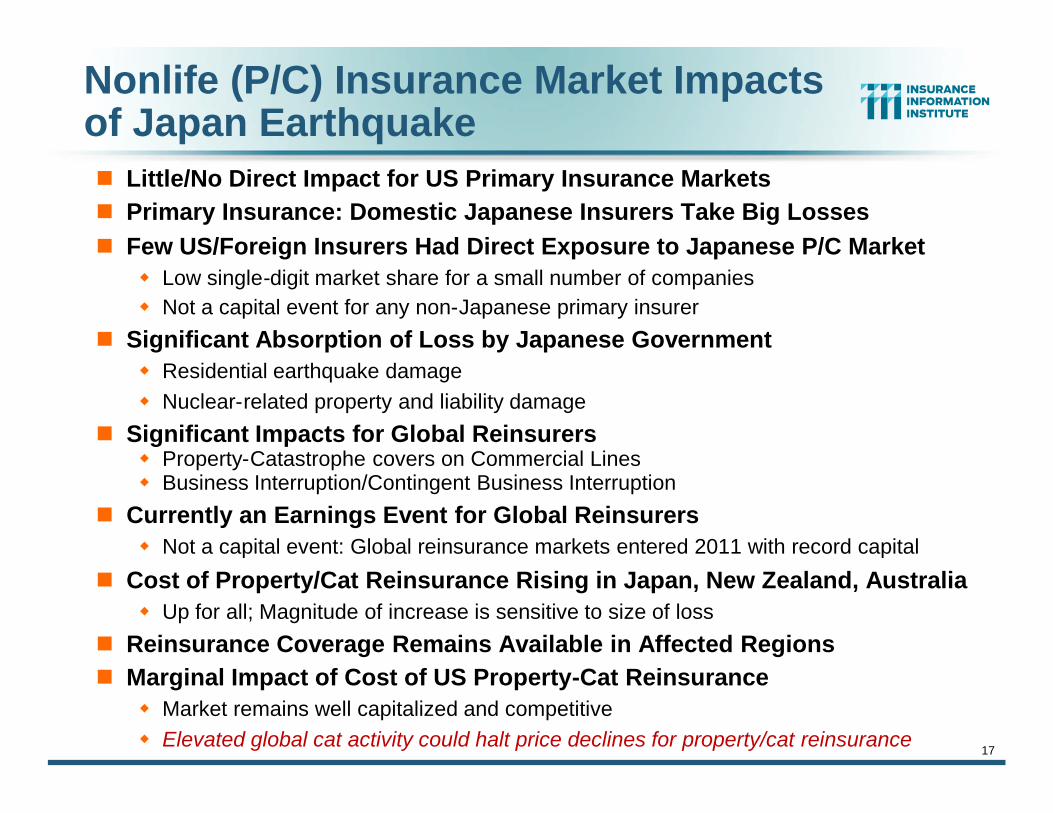

Nonlife (P/C) Insurance Market Impactsof Japan Earthquake Little/No Direct Impact for US Primary Insurance Markets Primary Insurance: Domestic Japanese Insurers Take Big Losses Few US/Foreign Insurers Had Direct Exposure to Japanese P/C Market

Low single-digit market share for a small number of companiesNot a capital event for any non-Japanese primary insurer

Significant Absorption of Loss by Japanese GovernmentResidential earthquake damageNuclear-related property and liability damage

Significant Impacts for Global ReinsurersProperty-Catastrophe covers on Commercial LinesBusiness Interruption/Contingent Business Interruption

Currently an Earnings Event for Global ReinsurersNot a capital event: Global reinsurance markets entered 2011 with record capital

Cost of Property/Cat Reinsurance Rising in Japan, New Zealand, AustraliaUp for all; Magnitude of increase is sensitive to size of loss

Reinsurance Coverage Remains Available in Affected Regions Marginal Impact of Cost of US Property-Cat Reinsurance

Market remains well capitalized and competitiveElevated global cat activity could halt price declines for property/cat reinsurance

18

Summary of April 2011Tornado Outbreak

2011 Will Be Among the MostDeadly and Expensive for

Tornadoes in History

19

Summary of Recent Tornado Activity

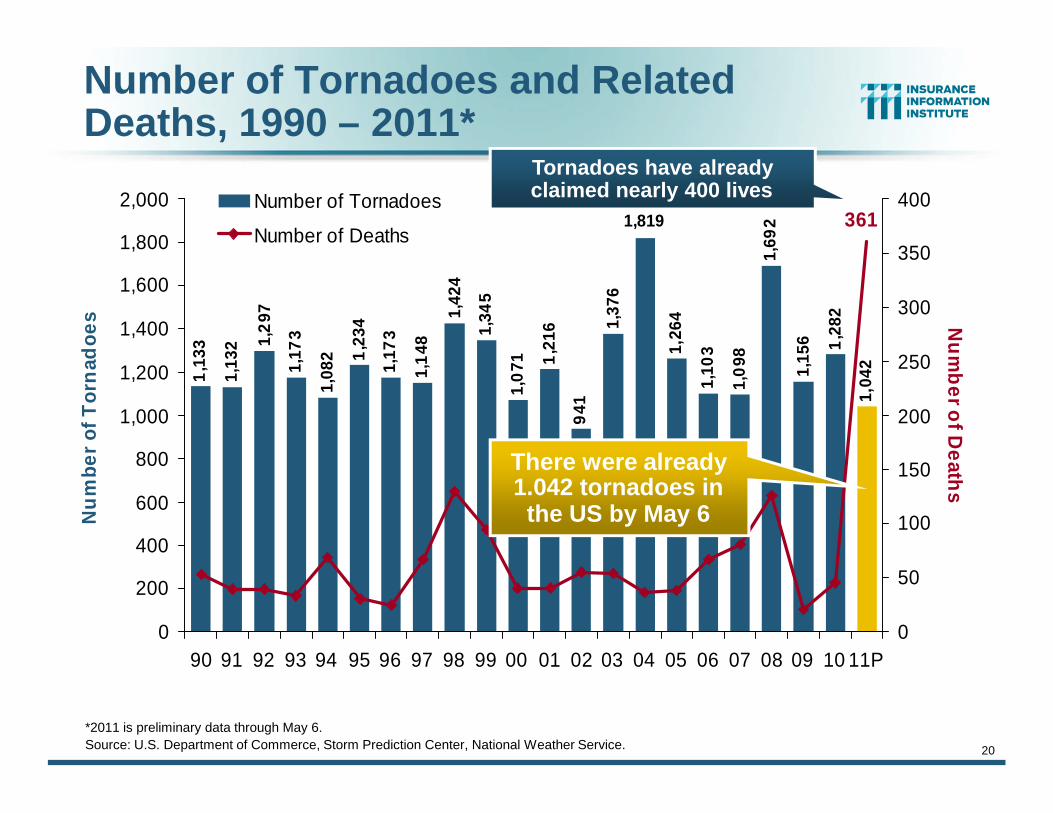

There Have Been 1,042 Tornadoes Through May 6 in the US

At least 361 People Have Been Killedd

The April 27 Tornado Outbreak Killed at Least 342 People

Now the 2nd deadliest outbreak in US history (747 killed in march 1925 event)

States impacted: AR, TN, LA, MS, GA and especially AL

Insured Losses Estimated at $2B to $5B (Eqecat); $3.7B - $5.5B (AIR)

Economic Losses Likely in the $4 Bill to $10 Bill Range

P/C Insurers (and their Reinsurers) Will Settle Tens of Thousands ofHome, Business and Auto Claims

There is Damage to Inland Port Facilities

P/C Insurance Industry is Very Strong and Will Encounter NoDifficulties in Paying these Claims

20

1,1

33

1,13

2 1,2

97

1,17

3

1,08

2 1,2

34

1,17

3

1,1

48

1,42

4

1,34

5

1,0

71 1,2

16

941

1,37

6

1,26

4

1,10

3

1,0

98

1,69

2

1,15

6 1,2

82

1,819

1,04

2

361

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11P

Nu

mbe

rof

Tor

nad

oes

0

50

100

150

200

250

300

350

400

Nu

mb

erofD

eaths

Number of Tornadoes

Number of Deaths

*2011 is preliminary data through May 6.Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service.

Number of Tornadoes and RelatedDeaths, 1990 – 2011*

Tornadoes have alreadyclaimed nearly 400 lives

There were already1.042 tornadoes inthe US by May 6

U.S. Tornado Count, 2010

Source: NOAA 21

There were 1483 tornadoesin the US in 2010, slightly

above average

2011 is shaping tobe a deadlier

version of 2008

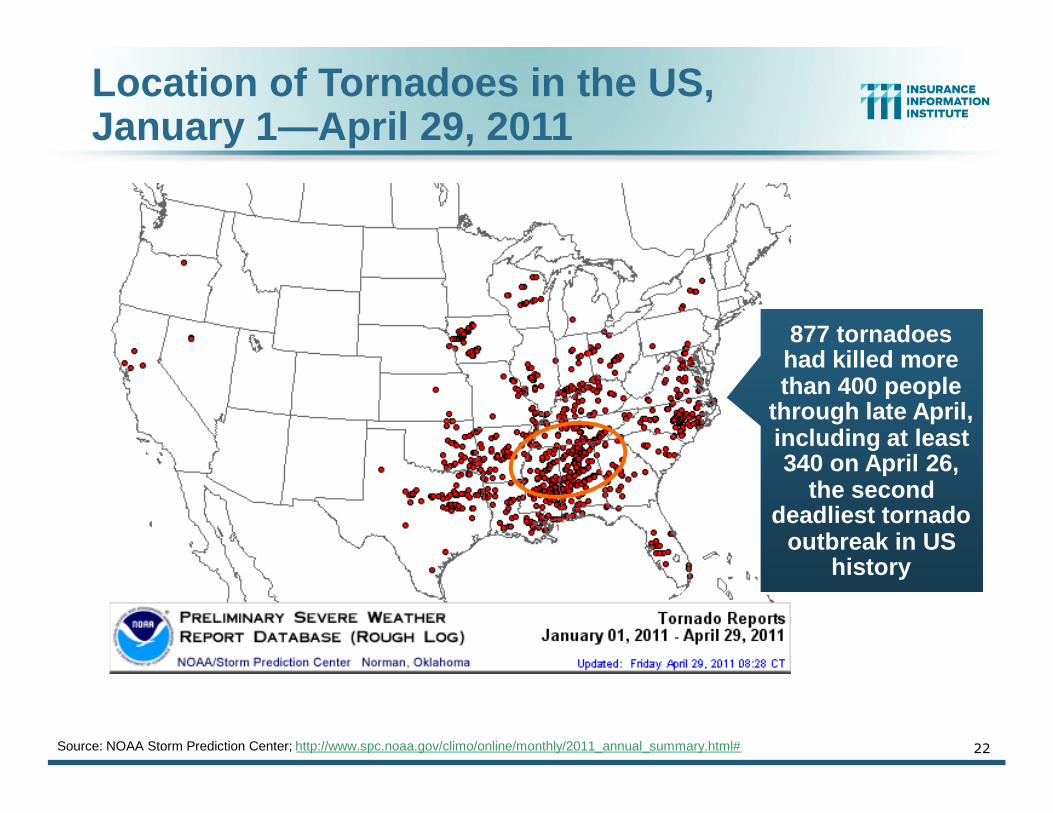

Location of Tornadoes in the US,January 1—April 29, 2011

Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# 22

877 tornadoeshad killed morethan 400 people

through late April,including at least340 on April 26,

the seconddeadliest tornado

outbreak in UShistory

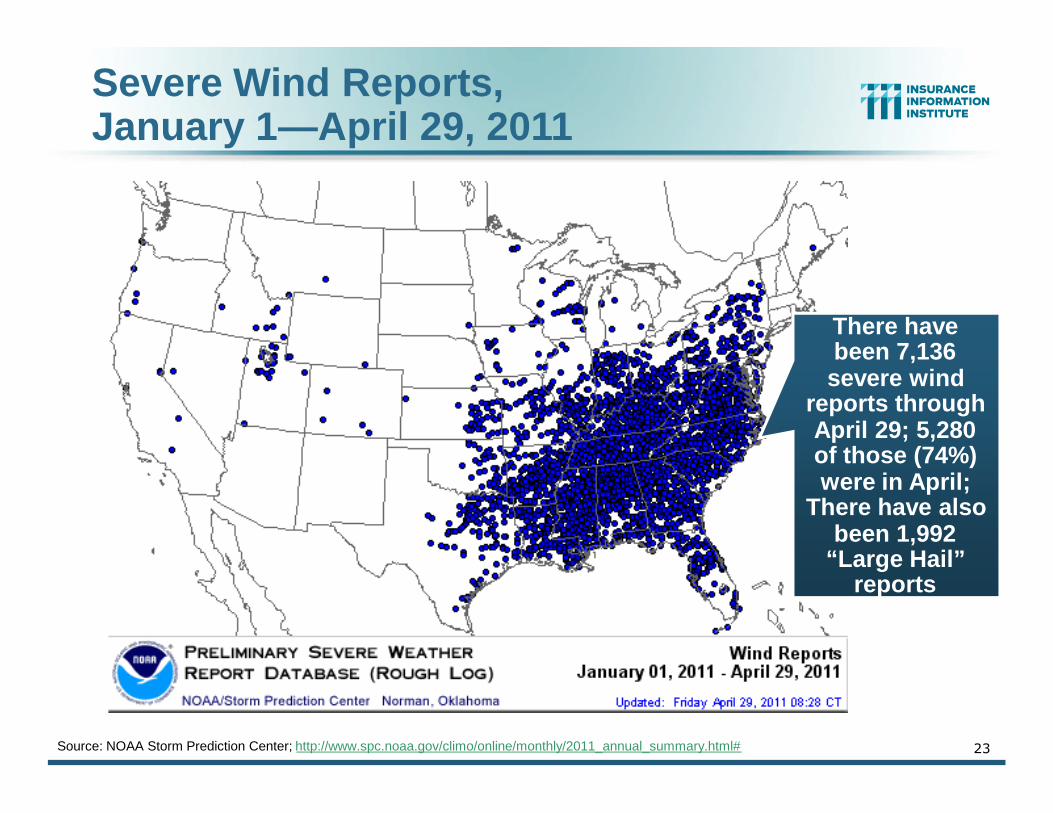

Severe Wind Reports,January 1—April 29, 2011

23

There havebeen 7,136severe wind

reports throughApril 29; 5,280of those (74%)were in April;

There have alsobeen 1,992

“Large Hail”reports

Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html#

24

Global Catastrophe Losses HaveInterrupted Trade Flows

Ships, Ports Damaged

Natural Catastrophes Worldwide,1980 – 2010 (Number of events with trend)

Number

Meteorological events(Storm)

Hydrological events(Flood, mass movement)

Climatological events(Extreme temperature,drought, forest fire)

Geophysical events(Earthquake, tsunami,volcanic eruption)

200

400

600

800

1 000

1 200

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Source: Geo Risks Research, NatCatSERVICE. 25© 2011 Munich Re

Increased claims payingcapacity will be required on

a global scale if currenttrends continue (as is

expected)

Geophysical events(earthquake, tsunami, volcanic activity)Meteorological events(storm)

Hydrological events(flood, mass movement)Climatological events(extreme temperature, drought, wildfire)

Selection of significantloss events (see table)

Natural catastrophes

Volcanic eruptionIsland, March/April

Heat wave/ WildfiresRussia, July-Sept.

Severe storms, floodsUnited States, 13 -15 March

EarthquakeHaiti, 12 Jan.

Hurricane Karl, floodsMexico, 15-21 Sept.

Earthquake, tsunamiChile, 27 Feb.

Winter Storm Xynthia, storm surgeWestern Europe, 26-28 Feb.

Flash floodsFrance,15 June

Floods, flash floodsPakistan, July-Sept.

EarthquakeChina, 13 April

FloodsEastern Europe,2-12 June

Floods, flash floods,landslidesChina, 13-29 June

Landslides, flash floodsChina, 7 Aug.

Hailstorms,severe stormsAustralia, 22 March/6-7 March

EarthquakeNew Zealand, 4 Sept.

Severe storms, hailUnited States, 12-16 May

Severe storms, tornadoes, floodsUnited States, 30 April – 3 May

Typhoon MegiChina, Philippines,Taiwan, 18-24 Oct.

FloodsAustralia, Dec.

Natural Catastrophes, 2010950 loss events

Source: Geo Risks Research, NatCatSERVIC.E 26

Insurance is aglobal business andclaims paying ability

is interconnectedvia reinsurance

markets

27

The Global Financial Crisis,Risk and the New World

Economic Order

The Crisis Made Insurers’ Path toGrowth More Challenging/Risky

28

The New World Order: A New Level ofRisk for BusinessBest Growth Opportunities are No Longer in Low-Risk Markets

(W. Europe, US/Canada, Japan)Growth Rates are 2-3 Times Higher in Developing WorldBusiness investment will remain high, much of it in need of insuranceInvestment conditions will remain challenging for decades

Unemployment Rates Are Much Lower in Emerging EconomiesEstablishment of a middle class and a wealthy upper class

Incomes Are Rising Faster in Emerging EconomiesFueling demand for goods and servicesForeign Direct Investment (FDI) and insurance exposure/demand

Immature Institutions Raise Risk/Possible Systemic RisksLegal system, financial markets, regulation, infrastructure issues

Instability in Emerging Nations Will Remain HighPolitical instability; Corruption in some countriesEconomic vulnerability (trade, xrt risk, credit risk, commodities, energy)

Natural Hazard Risks Are Often Elevated w/Minimal Mitigation

29

World Economic Outlook: 2009-2012F

Sources: IMF, World Economic Outlook, Apr. 2011; Insurance Information Institute.

5.0%

3.0%

2.8%

1.7%

3.9%4.5%

2.6% 2.9%

1.8% 2.1%

-0.5%

-3.4%

2.7%

-2.6%-4.1%

-6.3%

7.3%4.

4%

2.4% 6.

5%

3.0%

1.6%

1.4%6.

5%-8%-6%-4%-2%0%2%4%6%8%

World Output AdvancedEconomies

EmergingEconomies

United States Euro Area Japan

2009 2010 2011F 2012F

Outlook uncertain: The world economy continues to recover from theglobal economics, but activity is reviving at different speeds in differentparts of the world, according to the IMF. A clear set of “winners” hasemerged with direct implications for all industries and their insurers.

IMF says growth in emerging and developing economieswill outpace advanced ones in 2011/12. The impact will

be to accelerate the relative growth of insuranceexposures outside the US, W. Europe and Japan.

March 11 Japanquake will slow

2011 growth

30

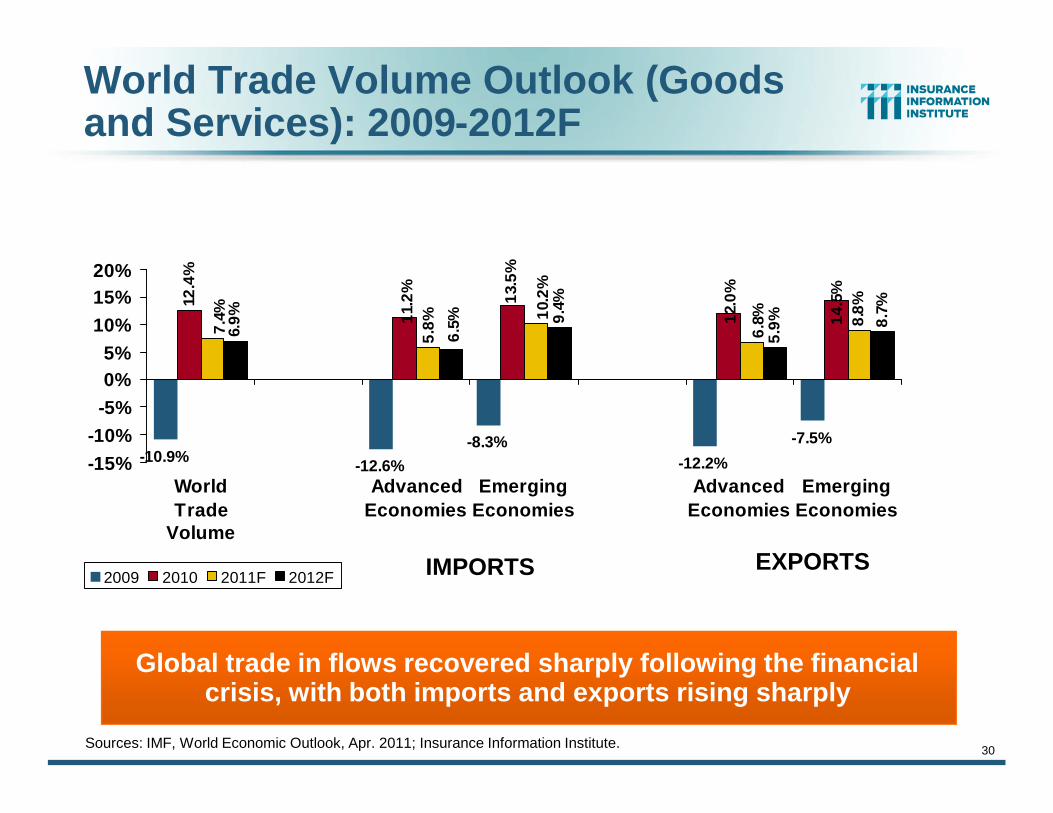

World Trade Volume Outlook (Goodsand Services): 2009-2012F

Sources: IMF, World Economic Outlook, Apr. 2011; Insurance Information Institute.

-7.5%

12.4

%

13.5

%

8.8%

6.9% 9.

4%

5.9% 8.

7%

-10.9% -12.6%-8.3%

-12.2%

14.5

%

12.0

%

11.2

%

7.4%

5.8%

10.2

%

6.8%

6.5%

-15%-10%

-5%0%5%

10%15%20%

WorldTrade

Volume

AdvancedEconomies

EmergingEconomies

AdvancedEconomies

EmergingEconomies

2009 2010 2011F 2012F

Global trade in flows recovered sharply following the financialcrisis, with both imports and exports rising sharply

IMPORTS EXPORTS

31

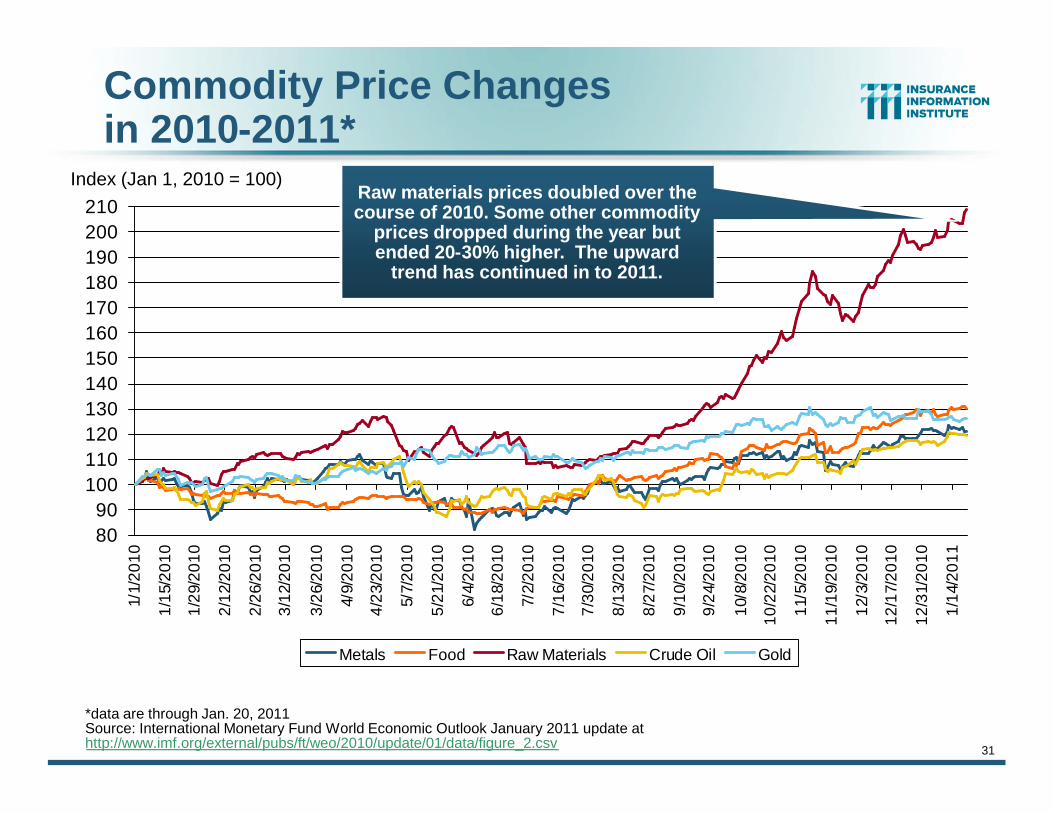

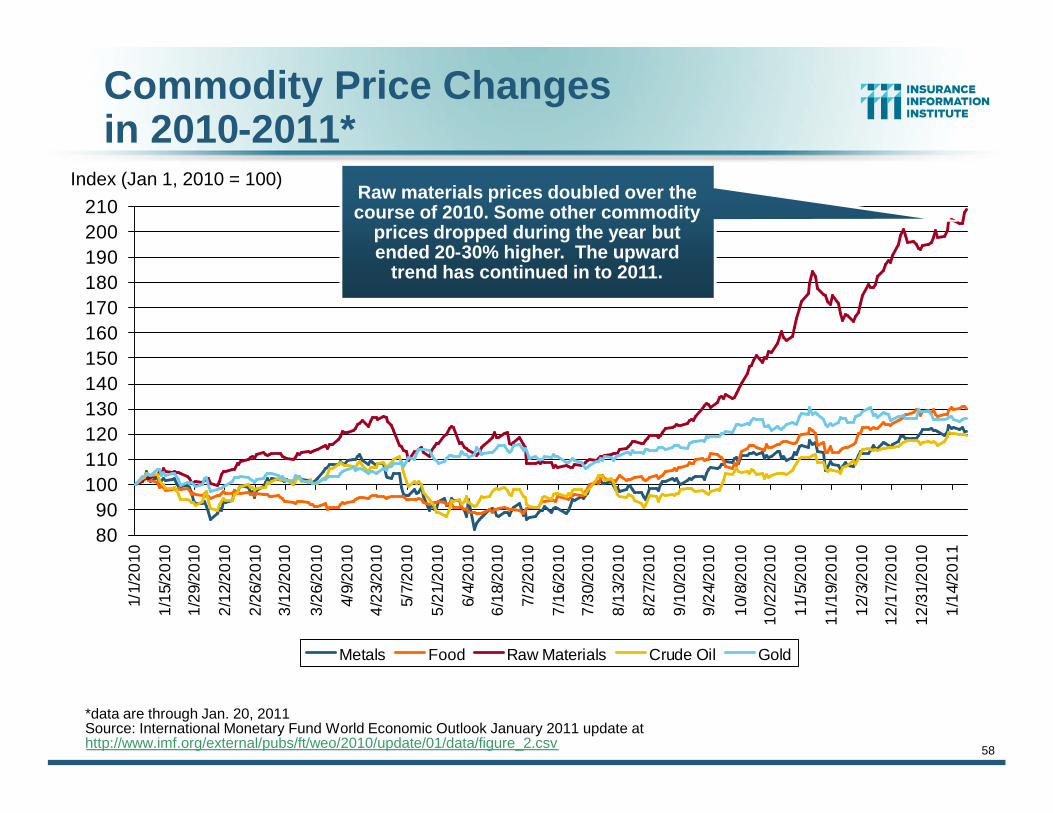

Commodity Price Changesin 2010-2011*

8090

100110120130140150160170180190200210

1/1/

2010

1/15

/201

0

1/29

/201

0

2/12

/201

0

2/26

/201

0

3/12

/201

0

3/26

/201

0

4/9/

2010

4/23

/201

0

5/7/

2010

5/21

/201

0

6/4/

2010

6/18

/201

0

7/2/

2010

7/16

/201

0

7/30

/201

0

8/13

/201

0

8/27

/201

0

9/10

/201

0

9/24

/201

0

10/8

/201

0

10/2

2/20

10

11/5

/201

0

11/1

9/20

10

12/3

/201

0

12/1

7/20

10

12/3

1/20

10

1/14

/201

1

Metals Food Raw Materials Crude Oil Gold

*data are through Jan. 20, 2011Source: International Monetary Fund World Economic Outlook January 2011 update athttp://www.imf.org/external/pubs/ft/weo/2010/update/01/data/figure_2.csv

Index (Jan 1, 2010 = 100)Raw materials prices doubled over thecourse of 2010. Some other commodity

prices dropped during the year butended 20-30% higher. The upward

trend has continued in to 2011.

65

70

75

80

85

90

95

100

105

110

115

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Jan11

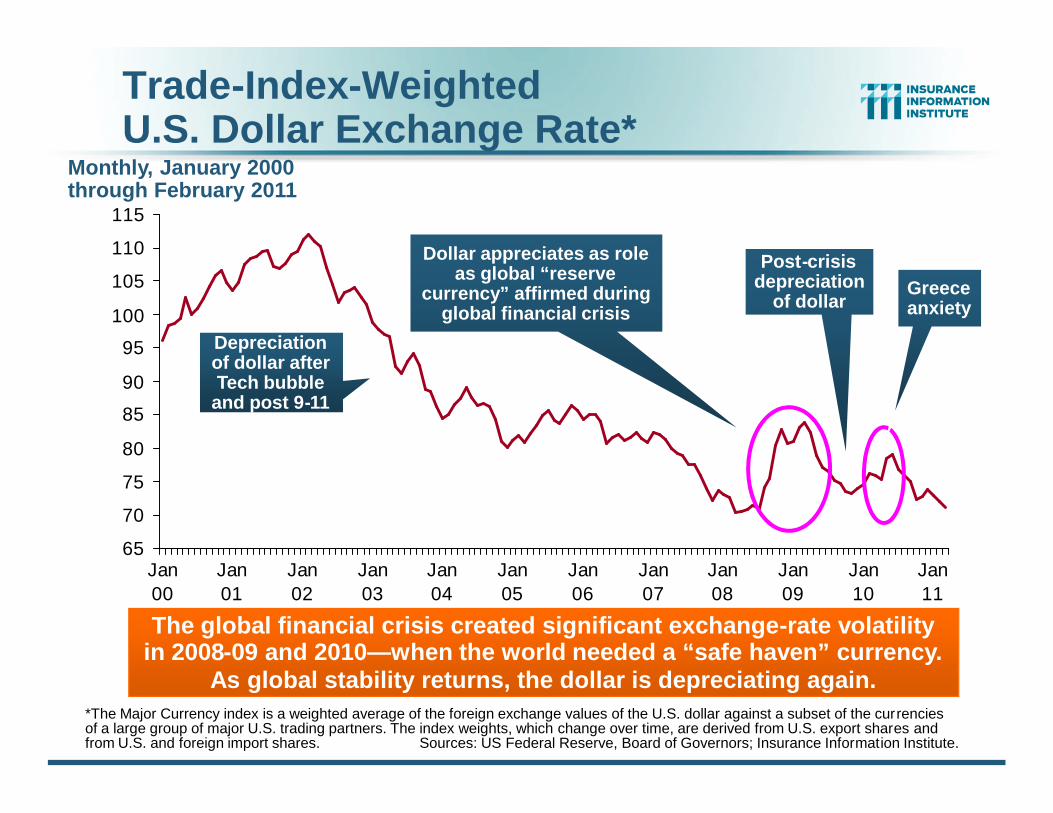

Trade-Index-WeightedU.S. Dollar Exchange Rate*

*The Major Currency index is a weighted average of the foreign exchange values of the U.S. dollar against a subset of the currenciesof a large group of major U.S. trading partners. The index weights, which change over time, are derived from U.S. export shares andfrom U.S. and foreign import shares. Sources: US Federal Reserve, Board of Governors; Insurance Information Institute.

The global financial crisis created significant exchange-rate volatilityin 2008-09 and 2010—when the world needed a “safe haven” currency.

As global stability returns, the dollar is depreciating again.

Monthly, January 2000through February 2011

Depreciationof dollar afterTech bubble

and post 9-11

Post-crisisdepreciation

of dollar

Dollar appreciates as roleas global “reserve

currency” affirmed duringglobal financial crisis

Greeceanxiety

33

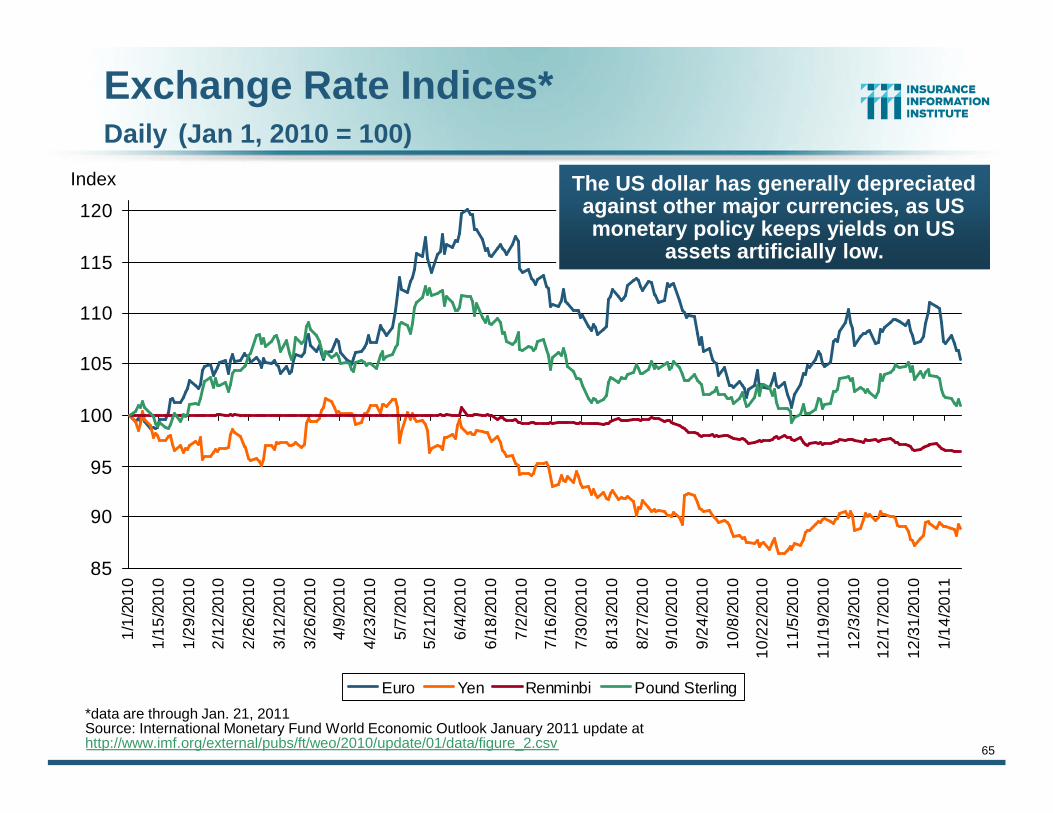

Exchange Rate Indices*Daily (Jan 1, 2010 = 100)

85

90

95

100

105

110

115

120

1/1/

2010

1/15

/201

0

1/29

/201

0

2/12

/201

0

2/26

/201

0

3/12

/201

0

3/26

/201

0

4/9/

2010

4/23

/201

0

5/7/

2010

5/21

/201

0

6/4/

2010

6/18

/201

0

7/2/

2010

7/16

/201

0

7/30

/201

0

8/13

/201

0

8/27

/201

0

9/10

/201

0

9/24

/201

0

10/8

/201

0

10/2

2/20

10

11/5

/201

0

11/1

9/20

10

12/3

/201

0

12/1

7/20

10

12/3

1/20

10

1/14

/201

1

Euro Yen Renminbi Pound Sterling

*data are through Jan. 21, 2011Source: International Monetary Fund World Economic Outlook January 2011 update athttp://www.imf.org/external/pubs/ft/weo/2010/update/01/data/figure_2.csv

Index The US dollar has generally depreciatedagainst other major currencies, as USmonetary policy keeps yields on US

assets artificially low.

34

Real GDP Growth Forecasts forAdvanced Economies: 2011 - 2012

Sources: Blue Chip Economic Indicators (4/2011 issue); Insurance Information Institute.

2.9%

1.7%

2.7%

1.8%

0.7%

2.9%3.

2%

2.2% 2.3%

2.0%

1.5%

3.0%

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%

UnitedStates

UnitedKingdom

Germany France Japan Canada

2011F 2012F

Growth projections could slow for 2011 if supplies of middle-eastern oil (politicaldisruption), developments involving sovereign debt (the PIGS or other countries)

or Japanese exports (earthquake/tsunami effects) are worse than expected.

35

9.0%

8.0%

4.5%

4.4%

4.1%

9.0%

8.0%

4.5% 4.

8%

3.9%

0%

4%

8%

12%

China India Russia Brazil Mexico

2011F 2012F

Growth in emerging and developing economies will greatly outpace advancedcountry growth in 2011/12. This will accelerate the growth of insurance

exposures in emerging markets relative to the U.S., W. Europe and Japan.

Real GDP Growth Forecasts for KeyDeveloping Economies: 2011 - 2012

Sources: Blue Chip Economic Indicators (4/2011 issue); Insurance Information Institute.

Growth in China and India remain high,though China is “tapping on the breaks”

to slow inflation. These markets arepromising but foreign firms must

contend with many barriers to entry.

36

4.3% 4.5%

1.8%

4.9%

3.0%

4.3% 4.

9%

1.8%

4.5%

3.6%

0%

4%

8%

South Korea Taiwan Netherlands Hong Kong Australia

2011F 2012F

Growth in industrialized Asian economies will greatly outpace much of therest of the world in 2011/12. This will accelerate the growth of insurance

exposures in emerging markets relative to the U.S., W. Europe and Japan.

Real GDP Growth Forecasts for OtherKey Trading Economies: 2011 - 2012

Sources: Blue Chip Economic Indicators (4/2011 issue); Insurance Information Institute.

Asia/Pacific trading nations shouldshow strong growth in 2011/12

compared to Europe and the US

(4.0)

(2.0)

0.0

2.0

4.0

6.0

8.0

10.0

70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Advanced economies Emerging and developing economies World

Source: International Monetary Fund, World Economic Outlook Update, January 2011; Ins. Info. Institute.

Emerging economies (ledby China) are expected togrow by 6.5% in 2011 and

2012. Role of FDI inexposure growth key.

GDP Growth: Advanced & EmergingEconomies vs. World, 1970-2012F

Advanced economies are expectedto grow at a relative modest 2.5% in

both 2011 and 2012.

World output is forecast to grow by4.4% in 2011 and 4.5% in 2011,

following growth of 3.0% in 2010and a 0.6% drop in 2009.

GDP Growth (%)

38

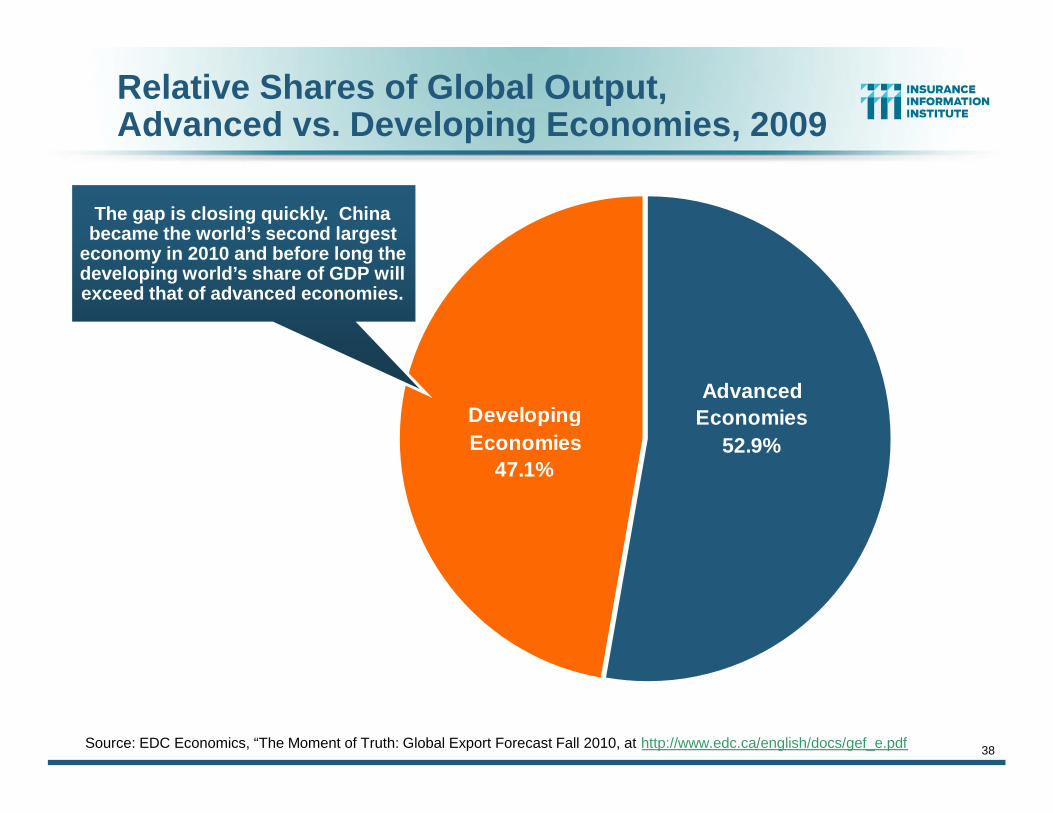

Relative Shares of Global Output,Advanced vs. Developing Economies, 2009

DevelopingEconomies

47.1%

AdvancedEconomies

52.9%

Source: EDC Economics, “The Moment of Truth: Global Export Forecast Fall 2010, at http://www.edc.ca/english/docs/gef_e.pdf

The gap is closing quickly. Chinabecame the world’s second largest

economy in 2010 and before long thedeveloping world’s share of GDP willexceed that of advanced economies.

(40)

(30)

(20)

(10)

0

10

20

30

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

Advanced economies Emerging economies Machinery & Equipment

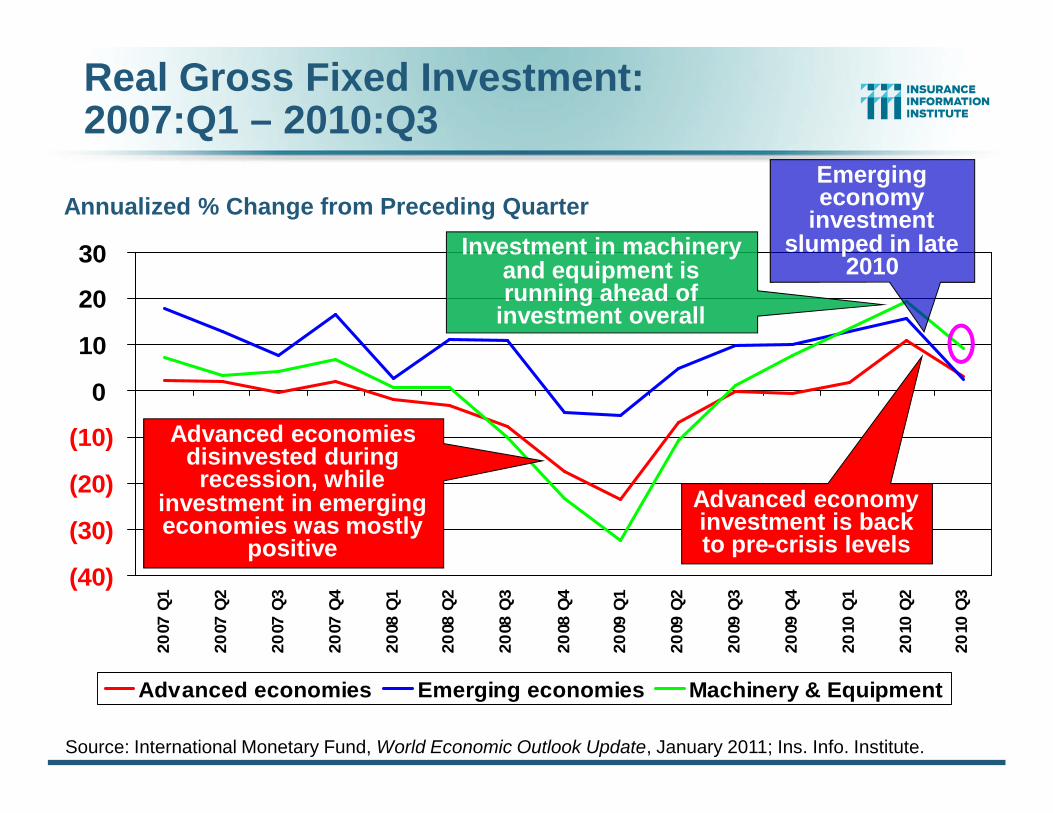

Source: International Monetary Fund, World Economic Outlook Update, January 2011; Ins. Info. Institute.

Emergingeconomy

investmentslumped in late

2010

Real Gross Fixed Investment:2007:Q1 – 2010:Q3

Advanced economyinvestment is backto pre-crisis levels

Investment in machineryand equipment isrunning ahead of

investment overall

Annualized % Change from Preceding Quarter

Advanced economiesdisinvested duringrecession, while

investment in emergingeconomies was mostly

positive

-30-25-20-15-10

-505

101520

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Source: International Monetary Fund, World Economic Outlook Update, Jan. 26, 2010; Ins. Info. Institute.

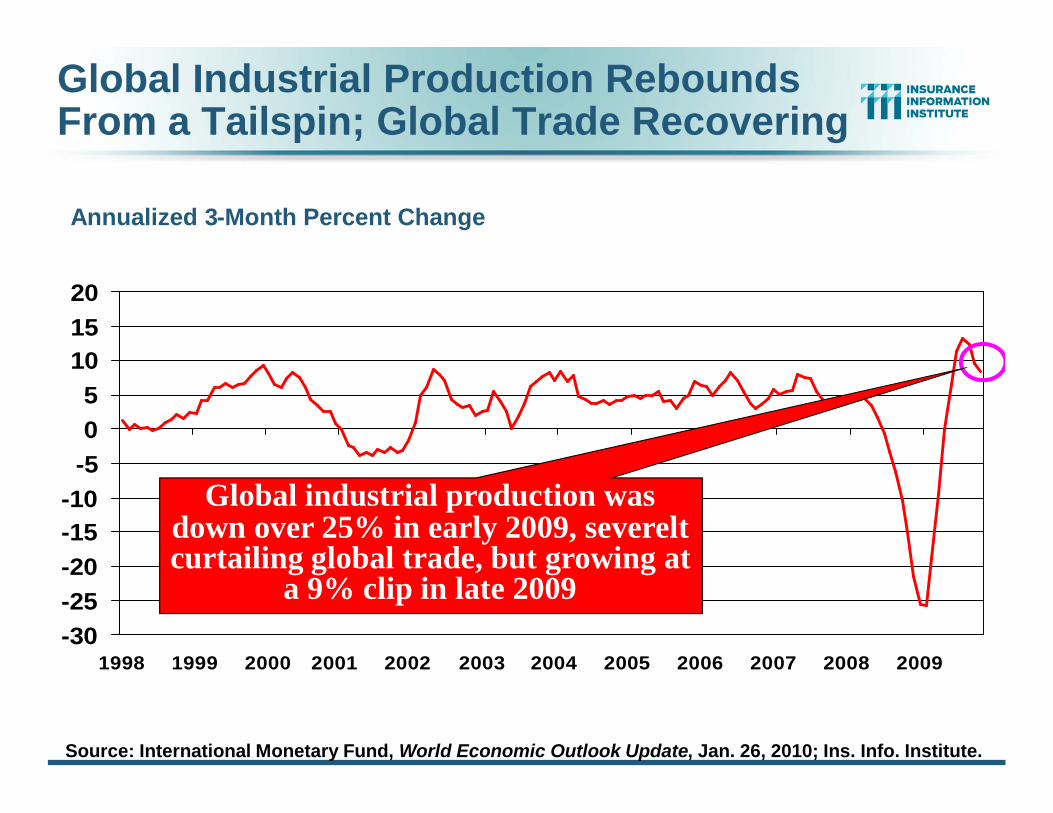

Global Industrial Production ReboundsFrom a Tailspin; Global Trade Recovering

Global industrial production wasdown over 25% in early 2009, severeltcurtailing global trade, but growing at

a 9% clip in late 2009

Annualized 3-Month Percent Change

41

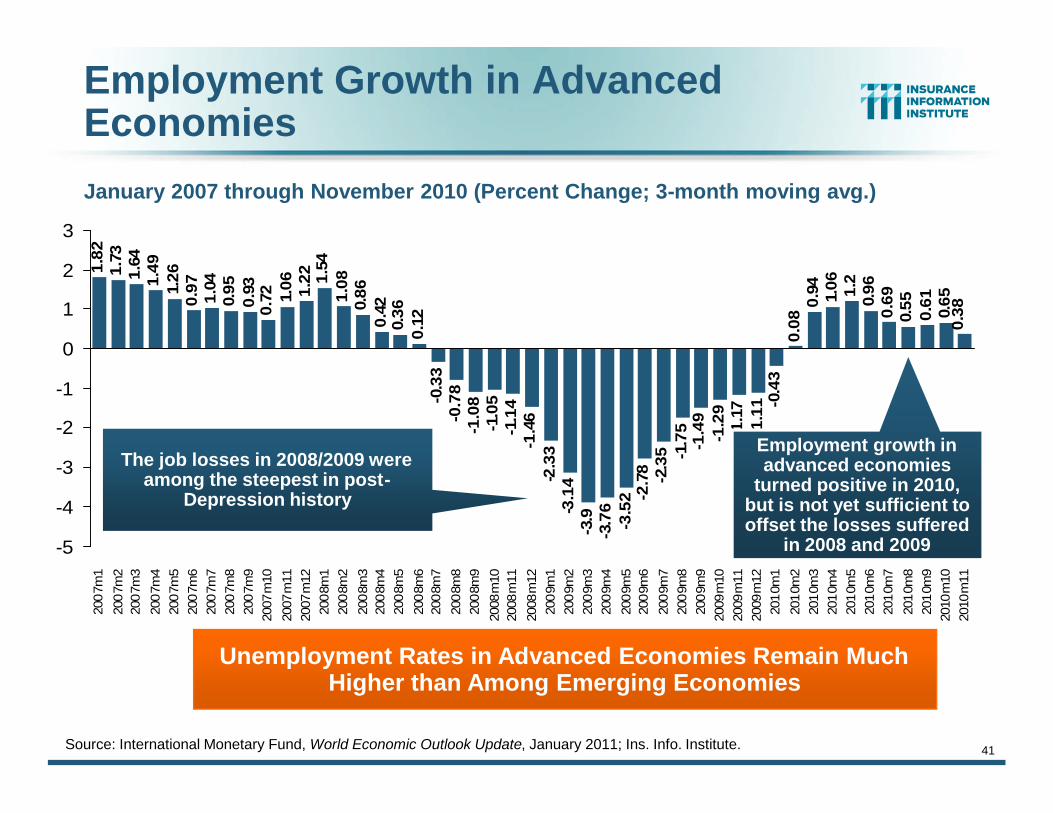

Employment Growth in AdvancedEconomies

1.82

1.73

1.64

1.49

1.26

0.97

1.04

0.95

0.93

0.72 1.

06 1.22 1.

541.

080.

860.

420.

360.

12-0

.33

-0.7

8-1

.08

-1.0

5-1

.14

-1.4

6-2

.33

-3.1

4-3

.9-3

.76

-3.5

2 -2.7

8 -2.3

5 -1.7

5-1

.49

-1.2

9-1

.17

-1.1

1 -0.4

30.

080.

94 1.06 1.2

0.96

0.69

0.55

0.61

0.65

0.38

-5

-4

-3

-2

-1

0

1

2

3

200

7m1

200

7m2

200

7m3

200

7m4

200

7m5

200

7m6

200

7m7

200

7m8

200

7m9

2007

m10

2007

m11

2007

m12

200

8m1

200

8m2

200

8m3

200

8m4

200

8m5

200

8m6

200

8m7

200

8m8

200

8m9

2008

m10

2008

m11

2008

m12

200

9m1

200

9m2

200

9m3

200

9m4

200

9m5

200

9m6

200

9m7

200

9m8

200

9m9

2009

m10

2009

m11

2009

m12

201

0m1

201

0m2

201

0m3

201

0m4

201

0m5

201

0m6

201

0m7

201

0m8

201

0m9

2010

m10

2010

m11

Employment growth inadvanced economies

turned positive in 2010,but is not yet sufficient tooffset the losses suffered

in 2008 and 2009

Unemployment Rates in Advanced Economies Remain MuchHigher than Among Emerging Economies

January 2007 through November 2010 (Percent Change; 3-month moving avg.)

The job losses in 2008/2009 wereamong the steepest in post-

Depression history

Source: International Monetary Fund, World Economic Outlook Update, January 2011; Ins. Info. Institute.

42Sources: IMF, World Economic Outlook, Oct. 2010; Insurance Information Institute.

8.3%

3.8%

10.1%

4.7%

9.7%9.3%

4.9%

9.4%

4.3%

8.0%9.6%

4.6%

10.0%

3.7%

8.2%

0%

2%

4%

6%

8%

10%

12%

AdvancedEconomies

NewlyIndustrializedEconomies

Euro Zone Asia US

2009 2010F 2011F

Persistently high unemployment is amongthe greatest obstacles to insurer

exposure/demand growth (nonlife and life)

Unemployment in Advanced Economies is more thandouble that of Emerging Economies

Unemployment Rates forMajor Global Economies, 2009-2011F

(6)

(4)

(2)

0

2

4

6

8

10

12

2007Q1

2007Q2

2007Q3

2007Q4

2008Q1

2008Q2

2008Q3

2008Q4

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

Advanced economies Emerging economies

Consumers in Emerging and Developing Markets AreIncreasingly Important to the Global Economy

Consumer spending is recovering on aglobal scale, but much more powerfully inemerging markets (up about 8% vs. 2% in

advanced economies)

Real Private Consumption:2007:Q1 – 2010:Q3

Annualized % Change from Preceding Quarter

Source: International Monetary Fund, World Economic Outlook Update, January 2011; Ins. Info. Institute.

44

Nonlife Real Premium Growth Ratesby Region: 1999-2008 and 2009

Source: Swiss Re, sigma, No. 2/2010.

-12% -8% -4% 0% 4% 8% 12% 16%

World

Industrialised countriesNorth America

Western EuropeContinental Europe

Japan and newly industrialised Asian economiesOceania

Emerging marketsSouth and East Asia

Latin America and the CaribbeanCentral and Eastern Europe

AfricaMiddle East and Central Asia

Real Premium Growth Rates

Growth rate 2009Annual average growth rate 1999-2008

Everyemerging

market regionexcept Central

and EasternEurope

experiencedgrowth duringthe financial

crisis

Many emerging market economiescontinued to grow during the global

financial crisis and continued tobenefit from foreign direct investment

45

Distribution of Nonlife Premium:Industrialized vs. Emerging Markets, 2009

Sources: NAIC; Insurance Information Institute research.

Although premium growththroughout the industrializedworld was negative in 2009, itsshare of global nonlifepremiums remained very highat nearly 86%--accounting fornearly $1.5 trillion in premiums.

The financial crisis and sluggishrecovery in the major insurancemarkets will accelerate theexpansion of the emergingmarket sector

Premium Growth Facts

14.3%85.7%

IndustrializedEconomies

$1, 485.8

EmergingMarkets$248.8

2009, $Billions

Developing markets nowaccount for 47% of global

GDP but just 14% of nonlifepremiums

46

The Unfortunate Nexus:Opportunity, Risk & Instability

Most of the Global Economy’s FutureGains Will be Fraught with Much

Greater Risk and Uncertainty than inthe Past—Insurance Is There to Help

47

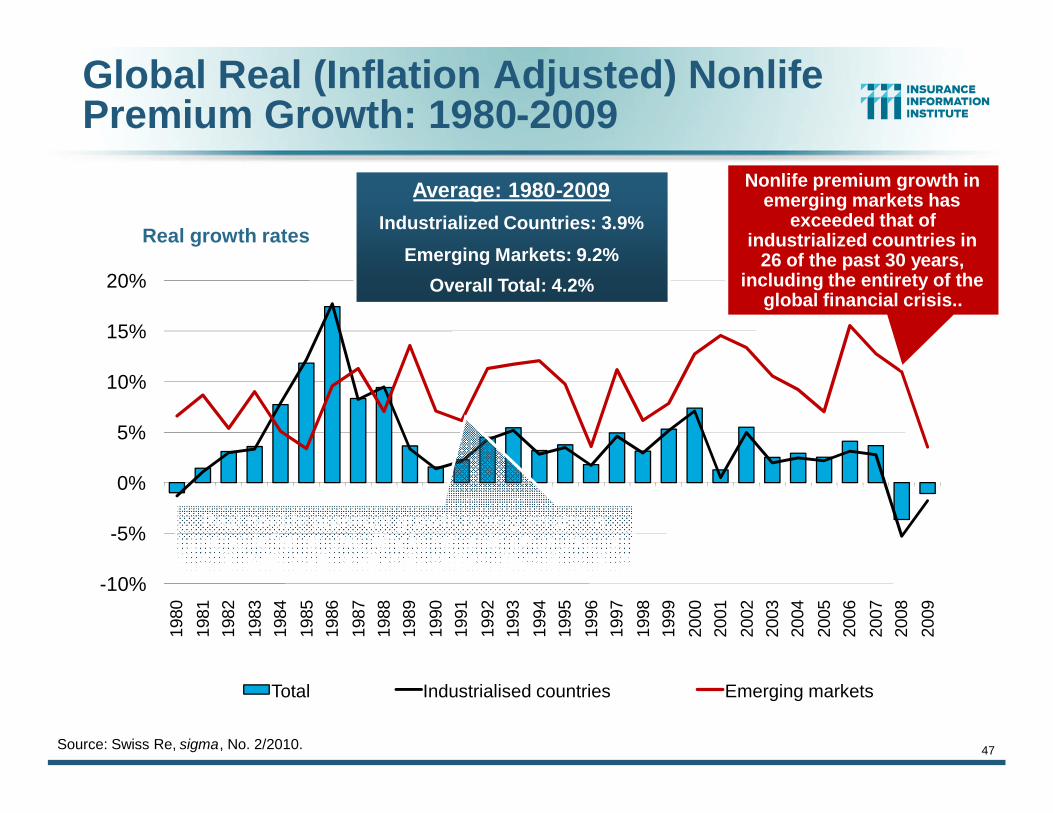

Global Real (Inflation Adjusted) NonlifePremium Growth: 1980-2009

Source: Swiss Re, sigma, No. 2/2010.

-10%

-5%

0%

5%

10%

15%

20%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Real growth rates

Total Industrialised countries Emerging markets

Nonlife premium growth inemerging markets has

exceeded that ofindustrialized countries in

26 of the past 30 years,including the entirety of the

global financial crisis..

Real nonlife premium growth is very erratic inpart to inflation volatility in emerging markets as

well as a lack of consistent cyclicality

Average: 1980-2009Industrialized Countries: 3.9%

Emerging Markets: 9.2%

Overall Total: 4.2%

48

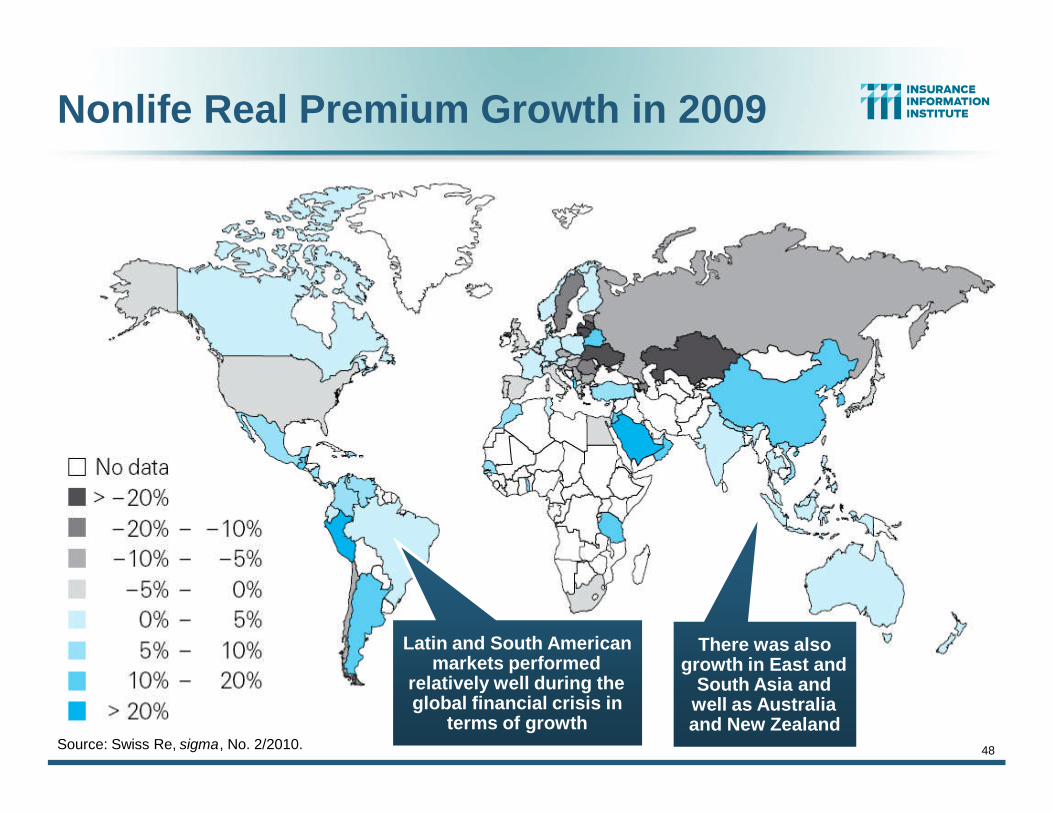

Nonlife Real Premium Growth in 2009

Source: Swiss Re, sigma, No. 2/2010.

Latin and South Americanmarkets performed

relatively well during theglobal financial crisis in

terms of growth

There was alsogrowth in East and

South Asia andwell as Australiaand New Zealand

49

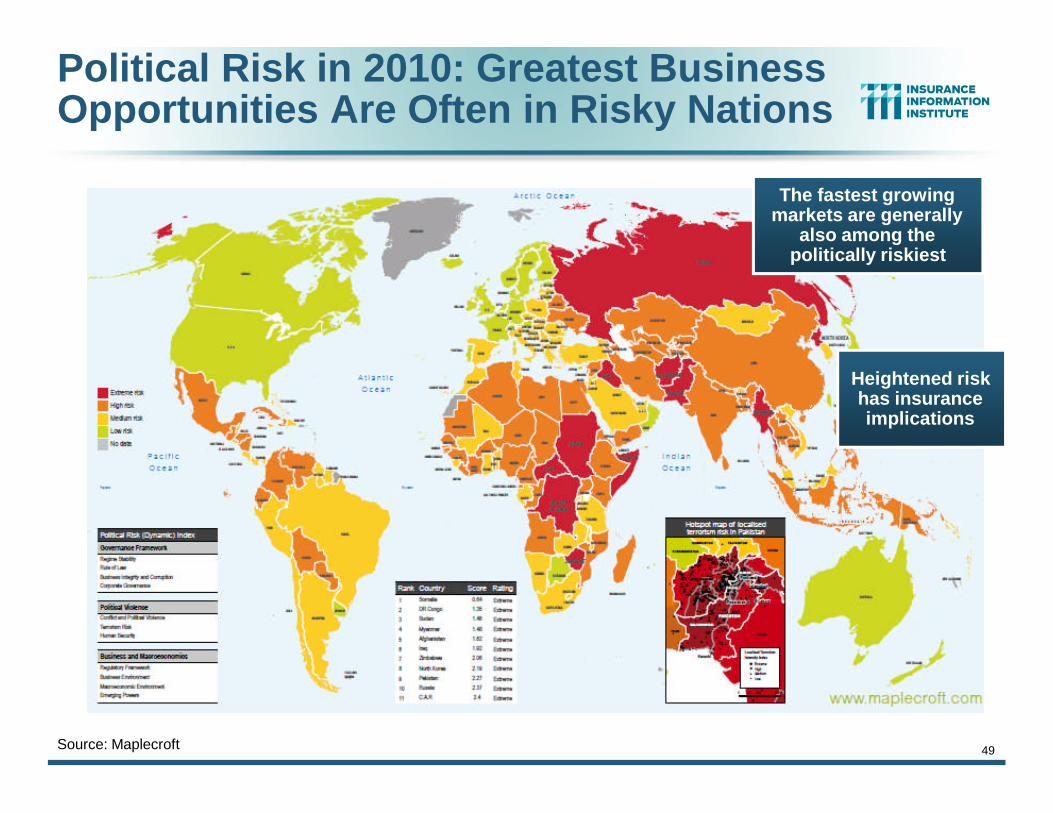

Political Risk in 2010: Greatest BusinessOpportunities Are Often in Risky Nations

Source: Maplecroft

The fastest growingmarkets are generally

also among thepolitically riskiest

Heightened riskhas insuranceimplications

50

Economic Threatsto Global Economy &

(Re)Insurance Industries

At Least Eight to Monitor:Near-Term and Longer-Term Risks

51

Near-Term Issues with PotentiallyAdverse Impacts to Global Growth

Japan Earthquake: Effects of the March 11Earthquake/Tsunami/ Nuclear Reactor AccidentLost final production

Disrupted supply chains

Lost Japanese consumption

Potential (modest) impact on GDP

Political spillover in Europe (e.g., Germany)

Political Unrest in the Middle East

Higher energy prices

Military action

Elevated political uncertainty

Safety of property and employees abroadSource: Insurance Information Institute.

52

Near-Term Issues with PotentiallyAdverse Impacts to Global Growth

Inflation Transmitted Globally

China, Brazil and other countries

Soaring food, energy and other commodity prices

Oil prices and supply reliability

Tighter Monetary/Fiscal Policy/AusteritySlower Growth?Europe, US

Source: Insurance Information Institute.

53

Political Risk in 2010: Greatest BusinessOpportunities Are Often in Risky Nations

Source: Maplecroft

The fastest growingmarkets are generally

also among thepolitically riskiest

Heightened riskhas insuranceimplications

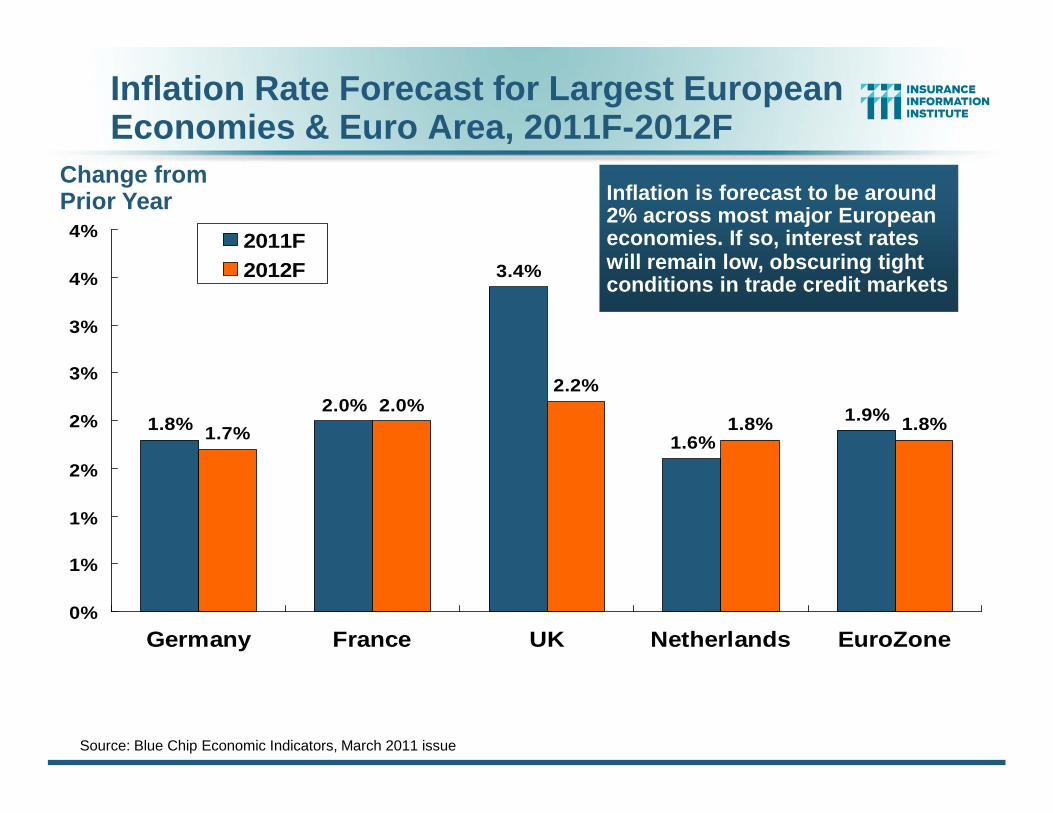

Inflation Rate Forecast for Largest EuropeanEconomies & Euro Area, 2011F-2012F

1.8%2.0%

3.4%

1.6%

1.9%1.7%

2.0%2.2%

1.8% 1.8%

0%

1%

1%

2%

2%

3%

3%

4%

4%

Germany France UK Netherlands EuroZone

2011F2012F

Source: Blue Chip Economic Indicators, March 2011 issue

Change fromPrior Year Inflation is forecast to be around

2% across most major Europeaneconomies. If so, interest rateswill remain low, obscuring tightconditions in trade credit markets

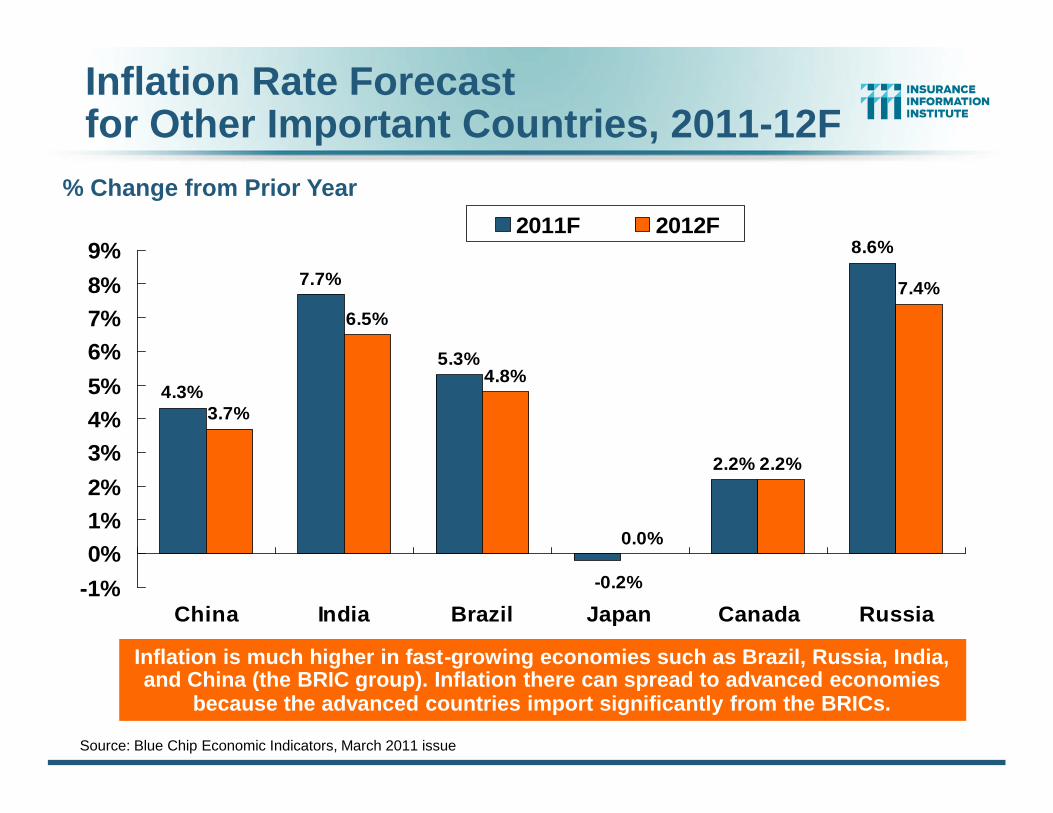

Inflation Rate Forecastfor Other Important Countries, 2011-12F

4.3%

7.7%

5.3%

2.2%

8.6%

3.7%

6.5%

4.8%

0.0%

2.2%

7.4%

-0.2%-1%

0%1%2%

3%4%5%

6%7%8%

9%

China India Brazil Japan Canada Russia

2011F 2012F

Source: Blue Chip Economic Indicators, March 2011 issue

% Change from Prior Year

Inflation is much higher in fast-growing economies such as Brazil, Russia, India,and China (the BRIC group). Inflation there can spread to advanced economies

because the advanced countries import significantly from the BRICs.

56

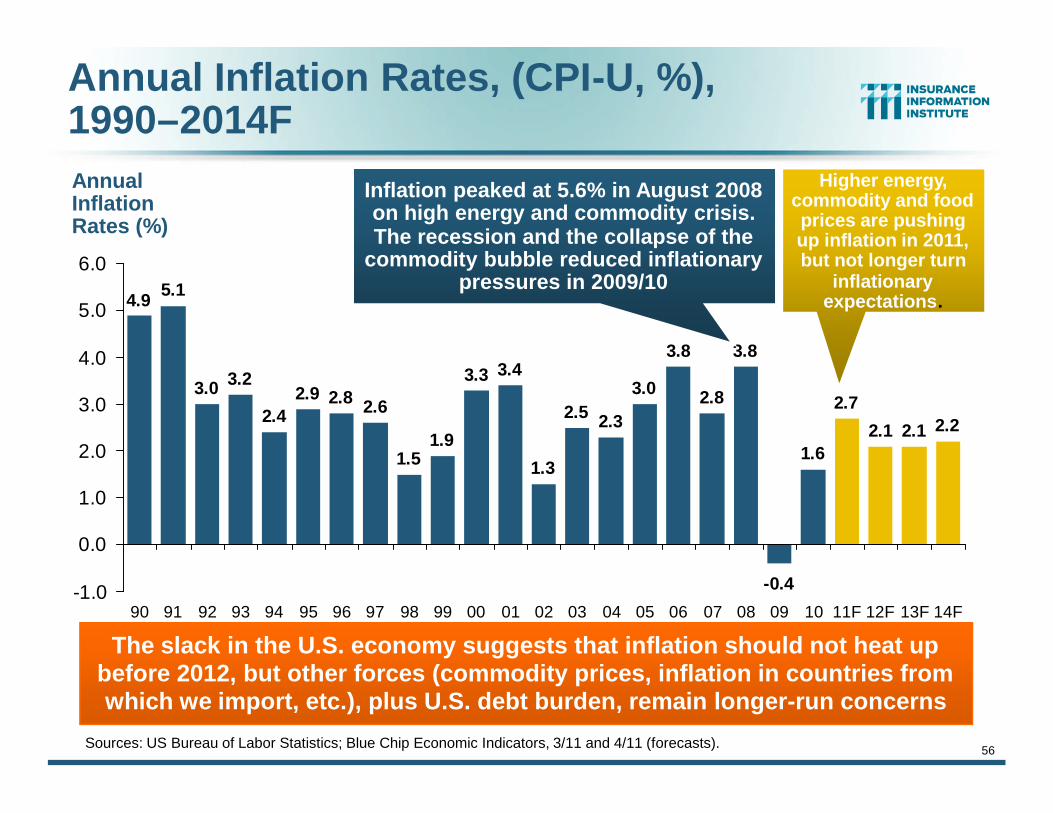

Annual Inflation Rates, (CPI-U, %),1990–2014F

2.8 2.6

1.51.9

3.3 3.4

1.3

2.5 2.3

3.0

3.8

2.8

3.8

-0.4

1.6

2.7

2.1 2.1 2.2

2.92.4

3.23.0

5.14.9

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11F 12F 13F 14F

Sources: US Bureau of Labor Statistics; Blue Chip Economic Indicators, 3/11 and 4/11 (forecasts).

The slack in the U.S. economy suggests that inflation should not heat upbefore 2012, but other forces (commodity prices, inflation in countries fromwhich we import, etc.), plus U.S. debt burden, remain longer-run concerns

AnnualInflationRates (%)

Inflation peaked at 5.6% in August 2008on high energy and commodity crisis.The recession and the collapse of the

commodity bubble reduced inflationarypressures in 2009/10

Higher energy,commodity and foodprices are pushingup inflation in 2011,but not longer turn

inflationaryexpectations.

U.S. P/C Insurance Claim Cost Drivers GrowFaster than even the Medical CPI Suggests

Source: Bureau of Labor Statistics; Insurance Information Institute.

1.6%1.0%

3.4%

8.8%

6.1%

3.3%

4.3%

3.1%

0%

3%

6%

9%

Overall CPI "Core" CPI Medical CPI InpatientHospitalServices

OutpatientHospitalServices

Physicians'Services

PrescriptionDrugs

Medical CareCommodities

Price Changesin 2010

Healthcare costs are a major liability, med pay, and PIP claim cost driver.They are likely to grow faster than the CPI for the next few years, at least

57

ExcludesFood and

Energy

58

Commodity Price Changesin 2010-2011*

8090

100110120130140150160170180190200210

1/1/

2010

1/15

/201

0

1/29

/201

0

2/12

/201

0

2/26

/201

0

3/12

/201

0

3/26

/201

0

4/9/

2010

4/23

/201

0

5/7/

2010

5/21

/201

0

6/4/

2010

6/18

/201

0

7/2/

2010

7/16

/201

0

7/30

/201

0

8/13

/201

0

8/27

/201

0

9/10

/201

0

9/24

/201

0

10/8

/201

0

10/2

2/20

10

11/5

/201

0

11/1

9/20

10

12/3

/201

0

12/1

7/20

10

12/3

1/20

10

1/14

/201

1

Metals Food Raw Materials Crude Oil Gold

*data are through Jan. 20, 2011Source: International Monetary Fund World Economic Outlook January 2011 update athttp://www.imf.org/external/pubs/ft/weo/2010/update/01/data/figure_2.csv

Index (Jan 1, 2010 = 100)Raw materials prices doubled over thecourse of 2010. Some other commodity

prices dropped during the year butended 20-30% higher. The upward

trend has continued in to 2011.

59

Longer-Term Issues

Persistently Low Interest Rates/Int. Rate Policy Lower investment income, more pressure on u/w profit Policy Dilemma: Stimulus/Low UnN or Price Stability

Currency Market InstabilityExchange rate volatilityFuture of the euroSovereign Bond Market ConcernsPortugal, Greece, Ireland, Spain, etc.Strong Capital Flows to Emerging/DevelopingEconomies => Asset Price Bubbles?Regulatory Backlash/Developments Solvency II, Basel III US Financial Services Reform (Dodd-Frank)

Source: Insurance Information Institute.

Internationally, Most Short-Term InterestRates Are Generally Still Quite Low

Central Bank CurrentInterest Rate

LastChanged

Bank of Canada 1.00% Sept. 8, 2010Bank of England 0.50% March 5, 2009Bank of Japan 0.10% Dec 19, 2008

European Central Bank 1.00% May 7, 2009

U.S. Federal Reserve 0.25% Dec 16, 2008The Reserve Bank of Australia 4.75% Nov. 2, 2010China 6.06% Feb. 8, 2011Hong Kong SAR 0.50% Dec 17, 2008

Korea, Republic of 3.00% March 10, 2011

Hungary 6.00% Jan. 24, 2011

Source: http://www.fxstreet.com/fundamental/interest-rates-table/

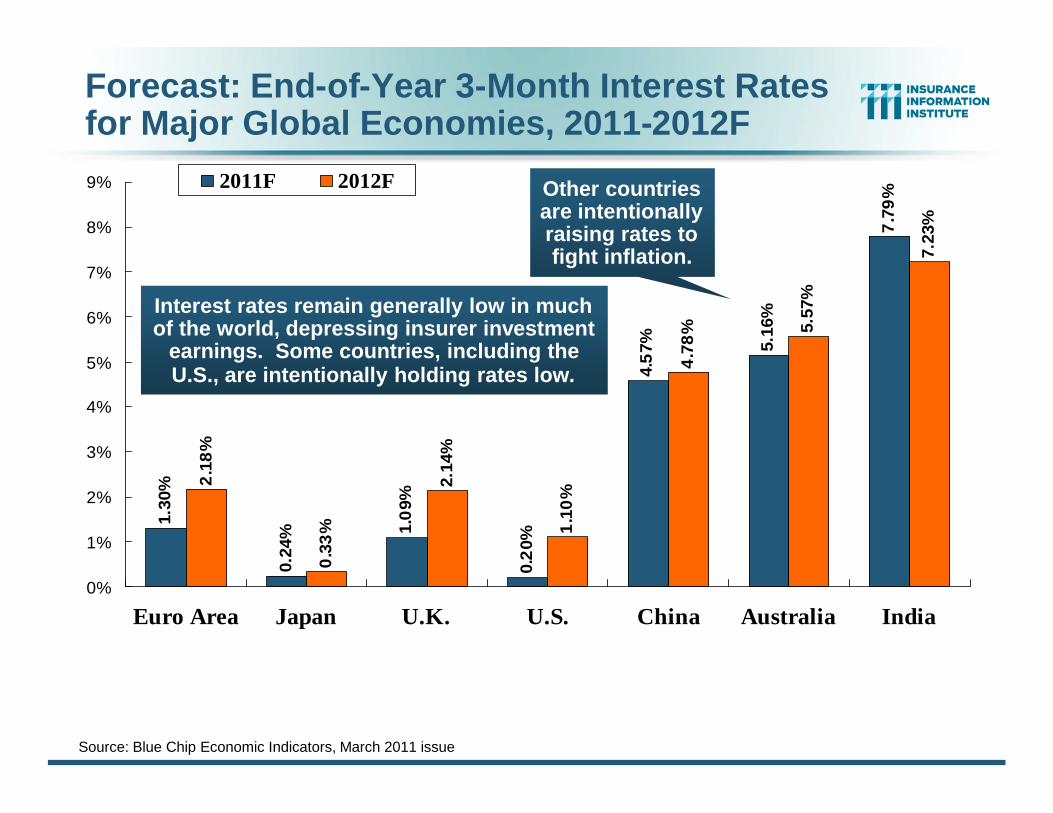

Forecast: End-of-Year 3-Month Interest Ratesfor Major Global Economies, 2011-2012F

1.30

%

0.24

% 1.0

9%

0.2

0%

4.5

7% 5.16

%

7.7

9%

2.1

8%

0.3

3%

2.14

%

1.1

0%

4.7

8% 5.

57%

7.23

%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Euro Area Japan U.K. U.S. China Australia India

2011F 2012F

Source: Blue Chip Economic Indicators, March 2011 issue

Interest rates remain generally low in muchof the world, depressing insurer investment

earnings. Some countries, including theU.S., are intentionally holding rates low.

Other countriesare intentionallyraising rates tofight inflation.

3.40%

3.60%

3.80%

4.00%

4.20%

4.40%

4.60%

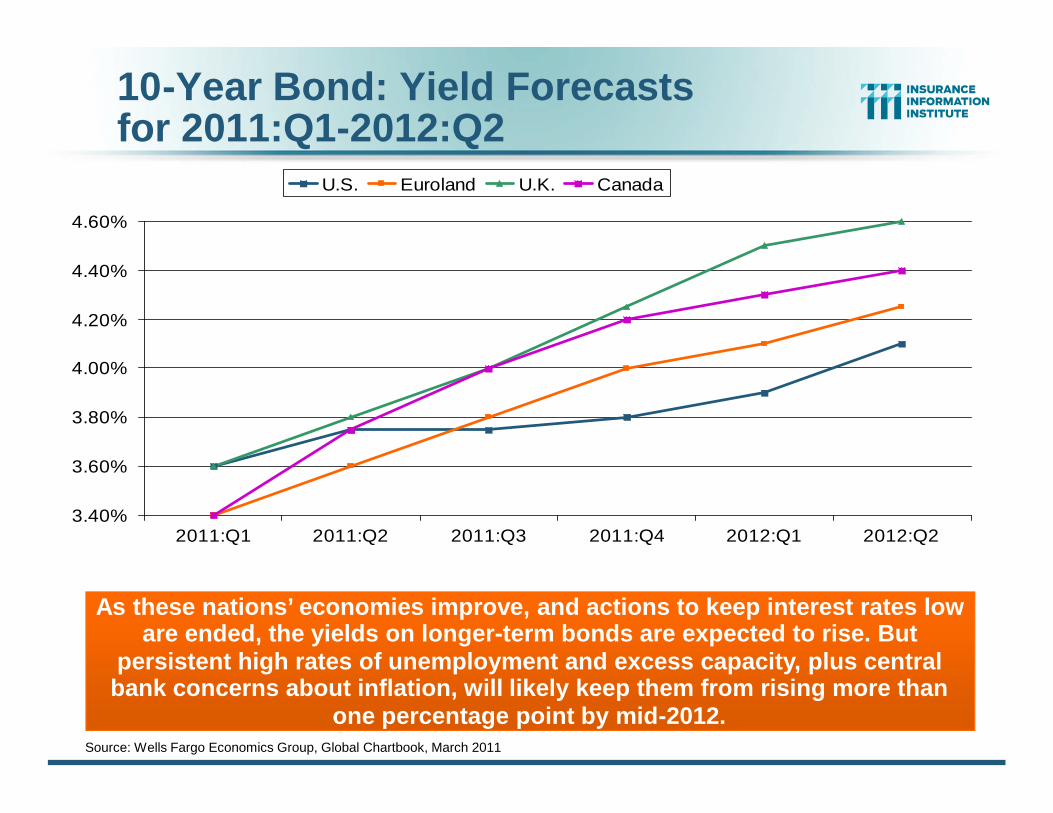

2011:Q1 2011:Q2 2011:Q3 2011:Q4 2012:Q1 2012:Q2

U.S. Euroland U.K. Canada

Source: Wells Fargo Economics Group, Global Chartbook, March 2011

As these nations’ economies improve, and actions to keep interest rates loware ended, the yields on longer-term bonds are expected to rise. But

persistent high rates of unemployment and excess capacity, plus centralbank concerns about inflation, will likely keep them from rising more than

one percentage point by mid-2012.

10-Year Bond: Yield Forecastsfor 2011:Q1-2012:Q2

63

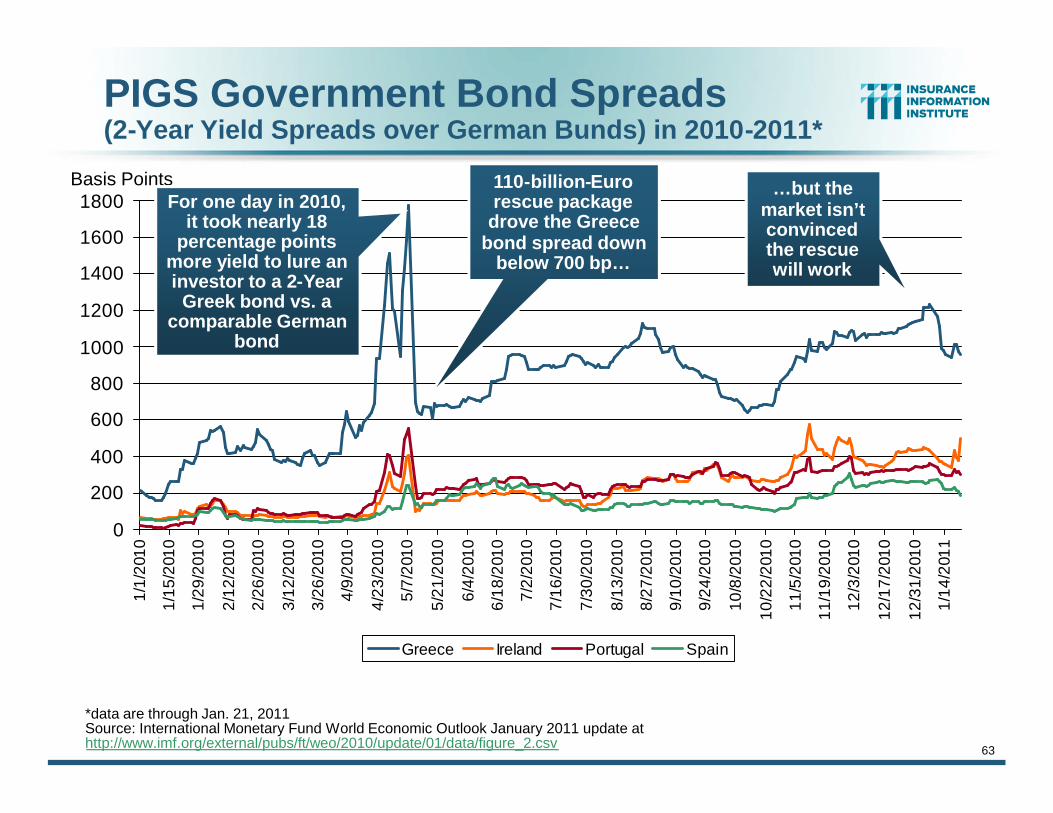

PIGS Government Bond Spreads(2-Year Yield Spreads over German Bunds) in 2010-2011*

0

200

400

600

800

1000

1200

1400

1600

1800

1/1/

2010

1/15

/201

0

1/29

/201

0

2/12

/201

0

2/26

/201

0

3/12

/201

0

3/26

/201

0

4/9/

2010

4/23

/201

0

5/7/

2010

5/21

/201

0

6/4/

2010

6/18

/201

0

7/2/

2010

7/16

/201

0

7/30

/201

0

8/13

/201

0

8/27

/201

0

9/10

/201

0

9/24

/201

0

10/8

/201

0

10/2

2/20

10

11/5

/201

0

11/1

9/20

10

12/3

/201

0

12/1

7/20

10

12/3

1/20

10

1/14

/201

1

Greece Ireland Portugal Spain

*data are through Jan. 21, 2011Source: International Monetary Fund World Economic Outlook January 2011 update athttp://www.imf.org/external/pubs/ft/weo/2010/update/01/data/figure_2.csv

Basis PointsFor one day in 2010,

it took nearly 18percentage points

more yield to lure aninvestor to a 2-Year

Greek bond vs. acomparable German

bond

110-billion-Eurorescue package

drove the Greecebond spread down

below 700 bp…

…but themarket isn’tconvincedthe rescuewill work

65

70

75

80

85

90

95

100

105

110

115

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Jan11

Trade-Index-WeightedU.S. Dollar Exchange Rate*

*The Major Currency index is a weighted average of the foreign exchange values of the U.S. dollar against a subset of the currenciesof a large group of major U.S. trading partners. The index weights, which change over time, are derived from U.S. export shares andfrom U.S. and foreign import shares. Sources: US Federal Reserve, Board of Governors; Insurance Information Institute.

The global financial crisis created significant exchange-rate volatilityin 2008-09 and 2010—when the world needed a “safe haven” currency.

As global stability returns, the dollar is depreciating again.

Monthly, January 2000through February 2011

Depreciationof dollar afterTech bubble

and post 9-11

Post-crisisdepreciation

of dollar

Dollar appreciates as roleas global “reserve

currency” affirmed duringglobal financial crisis

Greeceanxiety

65

Exchange Rate Indices*Daily (Jan 1, 2010 = 100)

85

90

95

100

105

110

115

120

1/1/

2010

1/15

/201

0

1/29

/201

0

2/12

/201

0

2/26

/201

0

3/12

/201

0

3/26

/201

0

4/9/

2010

4/23

/201

0

5/7/

2010

5/21

/201

0

6/4/

2010

6/18

/201

0

7/2/

2010

7/16

/201

0

7/30

/201

0

8/13

/201

0

8/27

/201

0

9/10

/201

0

9/24

/201

0

10/8

/201

0

10/2

2/20

10

11/5

/201

0

11/1

9/20

10

12/3

/201

0

12/1

7/20

10

12/3

1/20

10

1/14

/201

1

Euro Yen Renminbi Pound Sterling

*data are through Jan. 21, 2011Source: International Monetary Fund World Economic Outlook January 2011 update athttp://www.imf.org/external/pubs/ft/weo/2010/update/01/data/figure_2.csv

Index The US dollar has generally depreciatedagainst other major currencies, as USmonetary policy keeps yields on US

assets artificially low.

66

But Exchange-Rate Changes GenerallyHave Little Effect on U.S. Import Prices

In theory, a change in the value of the dollar should raise or lower thecost of foreign goods, thereby reducing or increasing U.S. demand forimports.

However, numerous economic studies have shown that when thedollar fluctuates against foreign currencies, U.S. import prices tend toshow much less change. This can crimp profits.

Using data for 1999 to 2008, a recent paper estimates exchange ratepass-through to U.S. import prices for aggregate U.S. imports (allimports excluding oil and consumer goods), and for prices of importsfrom Japan, the European Union (EU), Canada, the NIEs, and LatinAmerica.

The exchange rate pass-through estimates were found to be low (0.47 forall imports excluding oil and 0.26 for consumer goods) over 4 quarters.

Estimates of bilateral exchange- rate pass-through range from 0.59 forLatin America (largely Mexico) to 0.0 for the NIEs (Taiwan, Singapore,South Korea, and Hong Kong).

Source: U.S. International Trade Commission at http://www.usitc.gov/publications/332/working_papers/ID-21_revised.pdf.

67

Reshuffling the GlobalEconomic Deck ThroughForeign Direct Investment

The Global Financial CrisisConcentrates Growth Opportunities

in Risky Places/Industry Groups

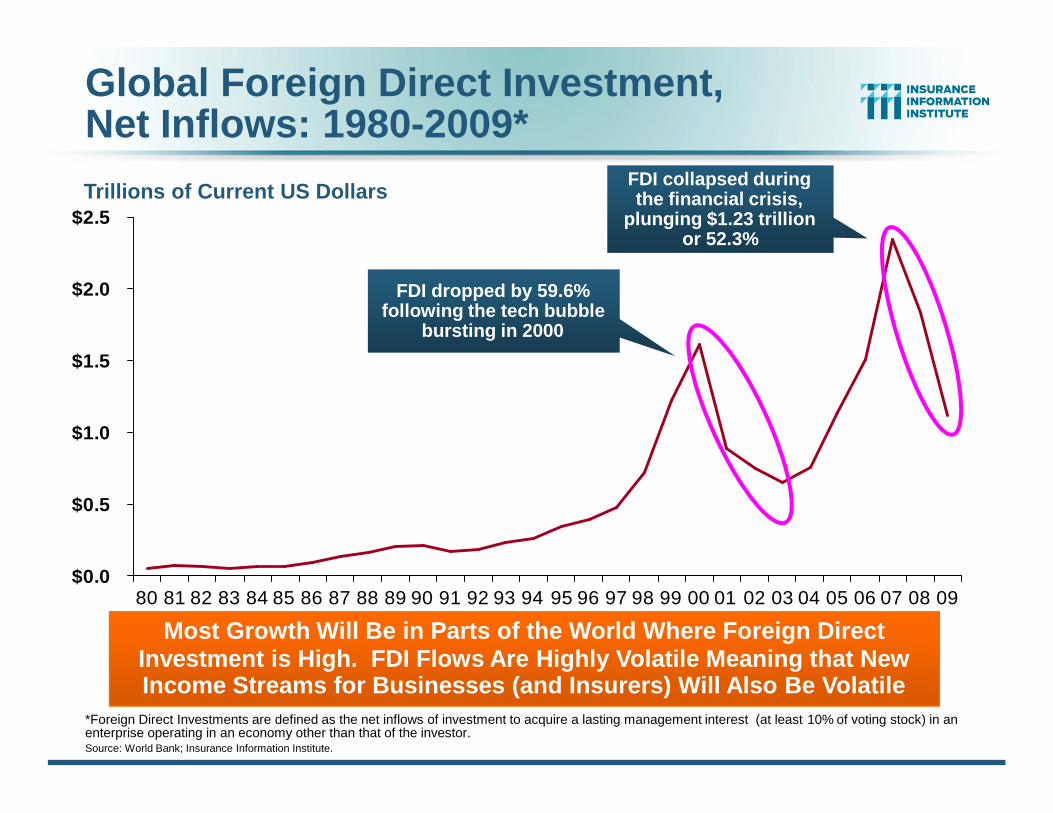

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

*Foreign Direct Investments are defined as the net inflows of investment to acquire a lasting management interest (at least 10% of voting stock) in anenterprise operating in an economy other than that of the investor.Source: World Bank; Insurance Information Institute.

Most Growth Will Be in Parts of the World Where Foreign DirectInvestment is High. FDI Flows Are Highly Volatile Meaning that NewIncome Streams for Businesses (and Insurers) Will Also Be Volatile

Trillions of Current US DollarsFDI collapsed duringthe financial crisis,

plunging $1.23 trillionor 52.3%

FDI dropped by 59.6%following the tech bubble

bursting in 2000

Global Foreign Direct Investment,Net Inflows: 1980-2009*

69

Following the Money Trail:Foreign Direct Investment

Source: The Economist, Nov. 13 -19, 2010

70

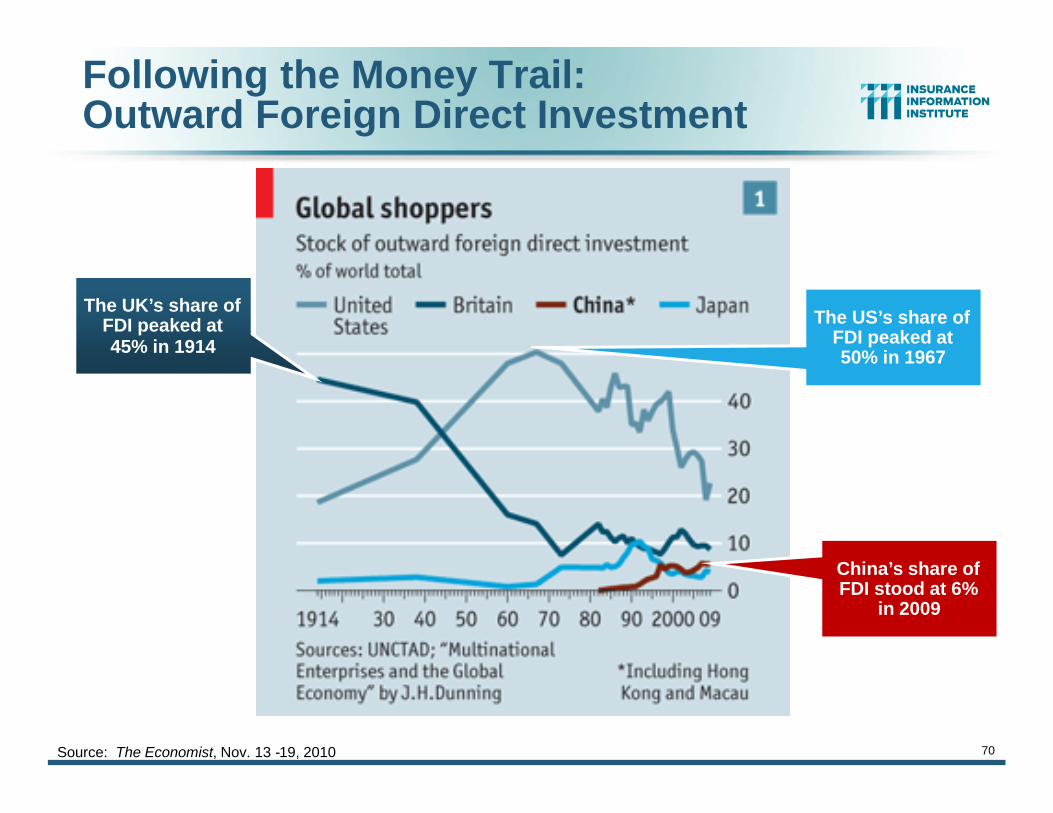

Following the Money Trail:Outward Foreign Direct Investment

Source: The Economist, Nov. 13 -19, 2010

The UK’s share ofFDI peaked at45% in 1914

The US’s share ofFDI peaked at50% in 1967

China’s share ofFDI stood at 6%

in 2009

71

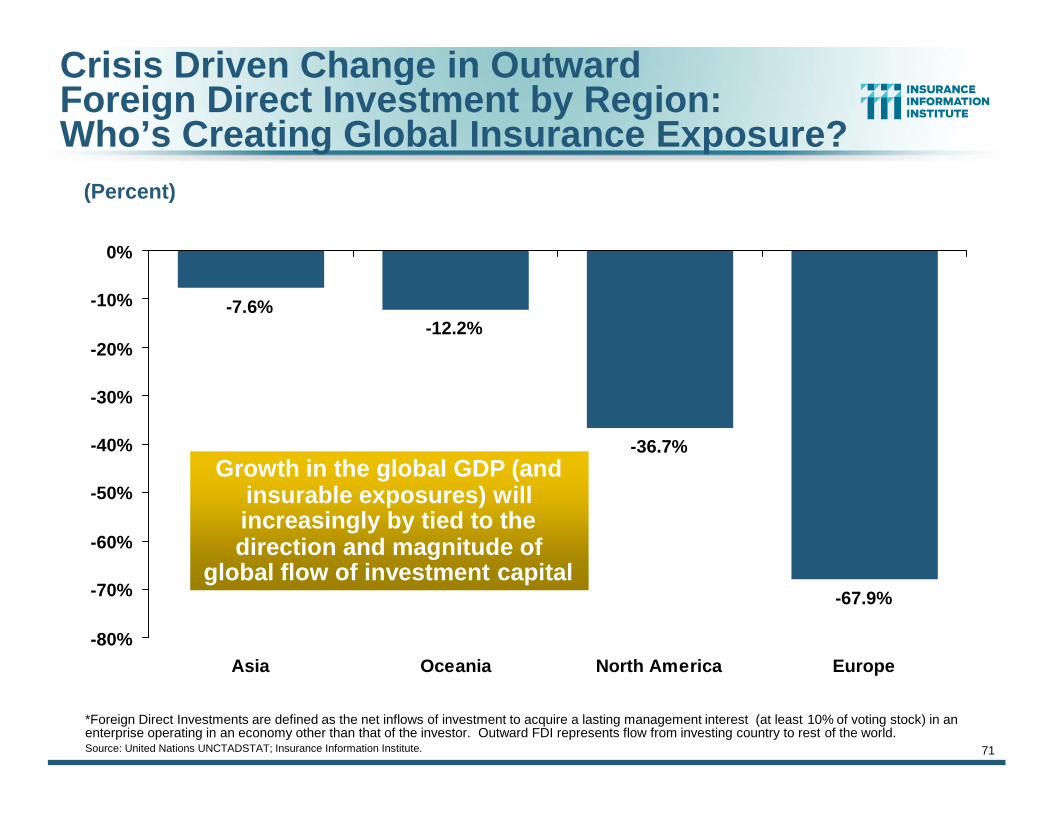

Crisis Driven Change in OutwardForeign Direct Investment by Region:Who’s Creating Global Insurance Exposure?

-7.6%-12.2%

-36.7%

-67.9%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Asia Oceania North America Europe

(Percent)

*Foreign Direct Investments are defined as the net inflows of investment to acquire a lasting management interest (at least 10% of voting stock) in anenterprise operating in an economy other than that of the investor. Outward FDI represents flow from investing country to rest of the world.Source: United Nations UNCTADSTAT; Insurance Information Institute.

Growth in the global GDP (andinsurable exposures) willincreasingly by tied to thedirection and magnitude of

global flow of investment capital

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

*Foreign Direct Investments are defined as the net inflows of investment to acquire a lasting management interest (at least 10% of voting stock) in anenterprise operating in an economy other than that of the investor. Outward FDI represents flow from investing country to rest of the world.Source: United Nations UNCTADSTAT; Insurance Information Institute.

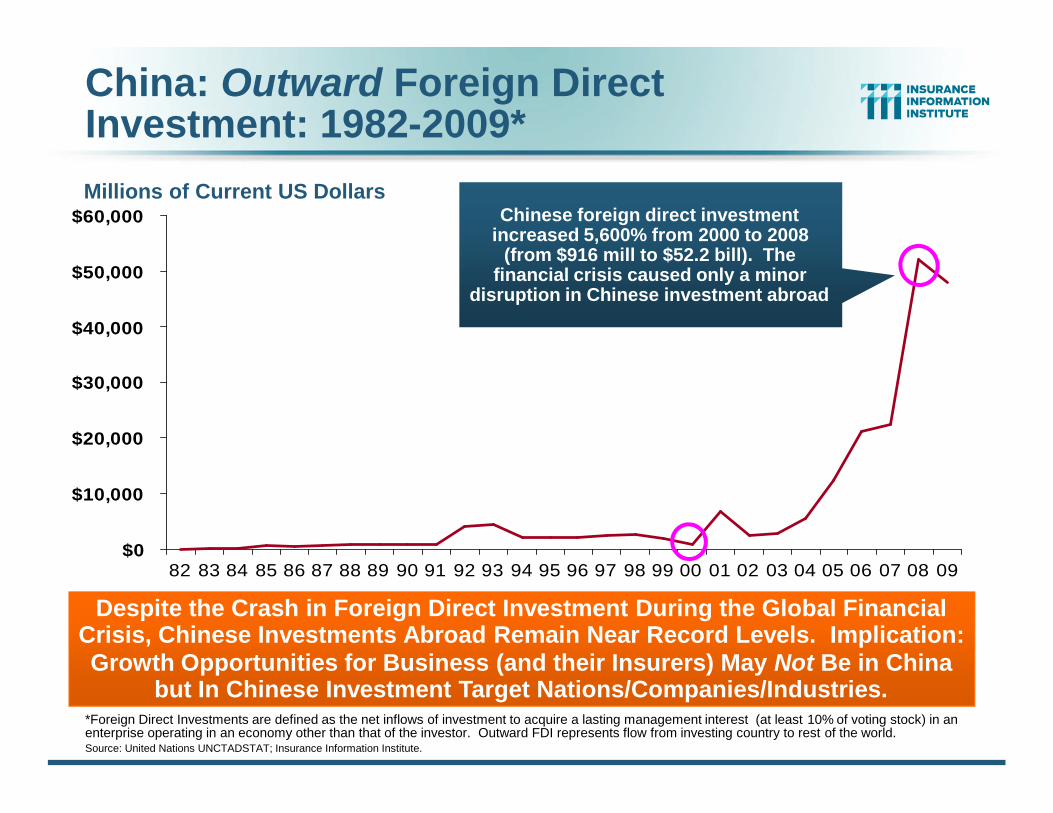

Despite the Crash in Foreign Direct Investment During the Global FinancialCrisis, Chinese Investments Abroad Remain Near Record Levels. Implication:Growth Opportunities for Business (and their Insurers) May Not Be in China

but In Chinese Investment Target Nations/Companies/Industries.

Millions of Current US DollarsChinese foreign direct investment

increased 5,600% from 2000 to 2008(from $916 mill to $52.2 bill). The

financial crisis caused only a minordisruption in Chinese investment abroad

China: Outward Foreign DirectInvestment: 1982-2009*

73

$0

$100

$200

$300

$400

$500

2006 2007 2008 2009

(Billions of US $)

Source: Data estimated from The Economist, Nov. 13-19, 2010 from: ICBC, China Construction Bank, China Development Bank, Bank of China and China Eximbank.

Major Chinese Banks’ Loans Abroad:2006-2009

Chinese banks are willing to loanheavily, despite global economic

turmoil, to expand Chinese investmentabroad. The health and investment

policies of Chinese will take on an ever-greater impact in the ability to financial

insurable exposures worldwide.Financial risk is an issue.

Chinese Banks’ Lending Activity Abroad Showed Little Impact from theGlobal Financial Crisis, but Eventually, Bank Crises Will Originate in China

Dim Sun Bonds??

America’s industrial rise began 50-60years before it became a global

financial power in the 1920s. Will ittake China that long? Probably not.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

*Foreign Direct Investments are defined as the net inflows of investment to acquire a lasting management interest (at least 10% of voting stock) in anenterprise operating in an economy other than that of the investor. Outward FDI represents flow from investing country to rest of the world.Source: United Nations UNCTADSTAT; Insurance Information Institute.

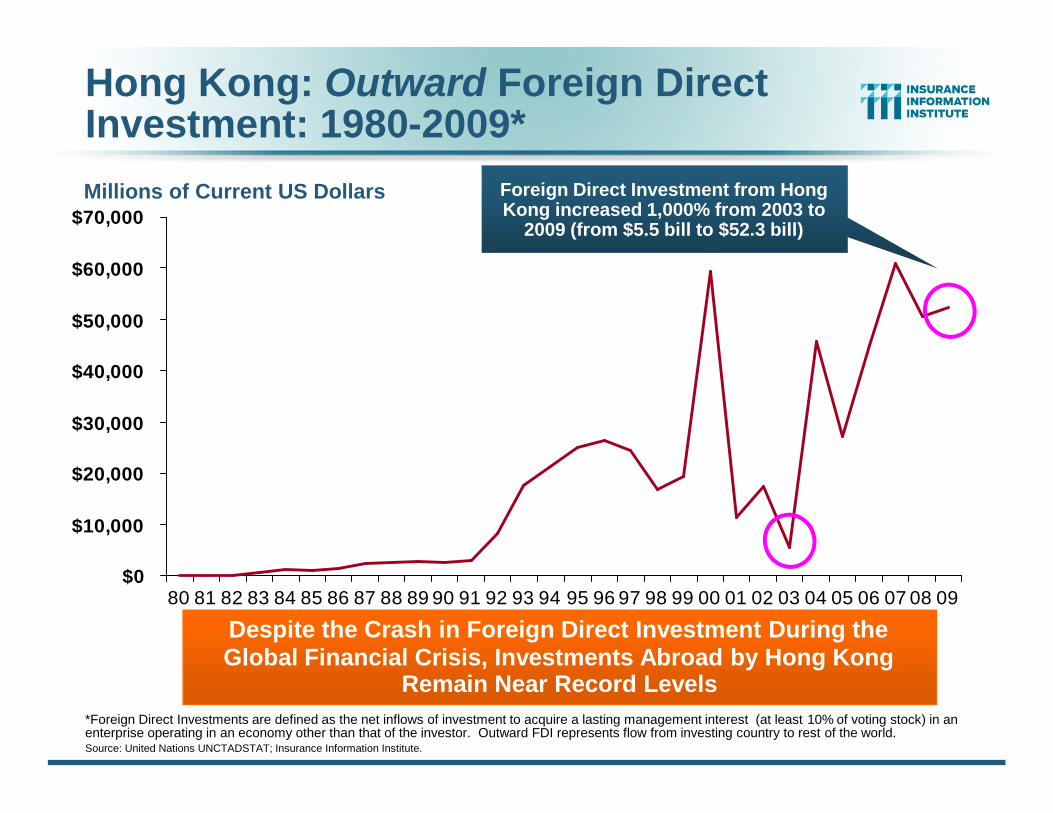

Despite the Crash in Foreign Direct Investment During theGlobal Financial Crisis, Investments Abroad by Hong Kong

Remain Near Record Levels

Millions of Current US Dollars Foreign Direct Investment from HongKong increased 1,000% from 2003 to

2009 (from $5.5 bill to $52.3 bill)

Hong Kong: Outward Foreign DirectInvestment: 1980-2009*

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

*Foreign Direct Investments are defined as the net inflows of investment to acquire a lasting management interest (at least 10% of voting stock) in anenterprise operating in an economy other than that of the investor. Outward FDI represents flow from investing country to rest of the world.Source: United Nations UNCTADSTAT; Insurance Information Institute.

The Global Financial Crisis Hit South Korean Foreign Direct InvestmentAbroad Harder than Was the Case in Several of Its Neighbors

Millions of Current US DollarsForeign Direct Investment from SouthKorea increased 437% from 2001 to2009 (from $2.4 bill to $10.6 bill), but

plunged 44% during the financial crisis

South Korea: Outward Foreign DirectInvestment: 1980-2009*

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

*Foreign Direct Investments are defined as the net inflows of investment to acquire a lasting management interest (at least 10% of voting stock) in anenterprise operating in an economy other than that of the investor. Outward FDI represents flow from investing country to rest of the world.Source: United Nations UNCTADSTAT; Insurance Information Institute.

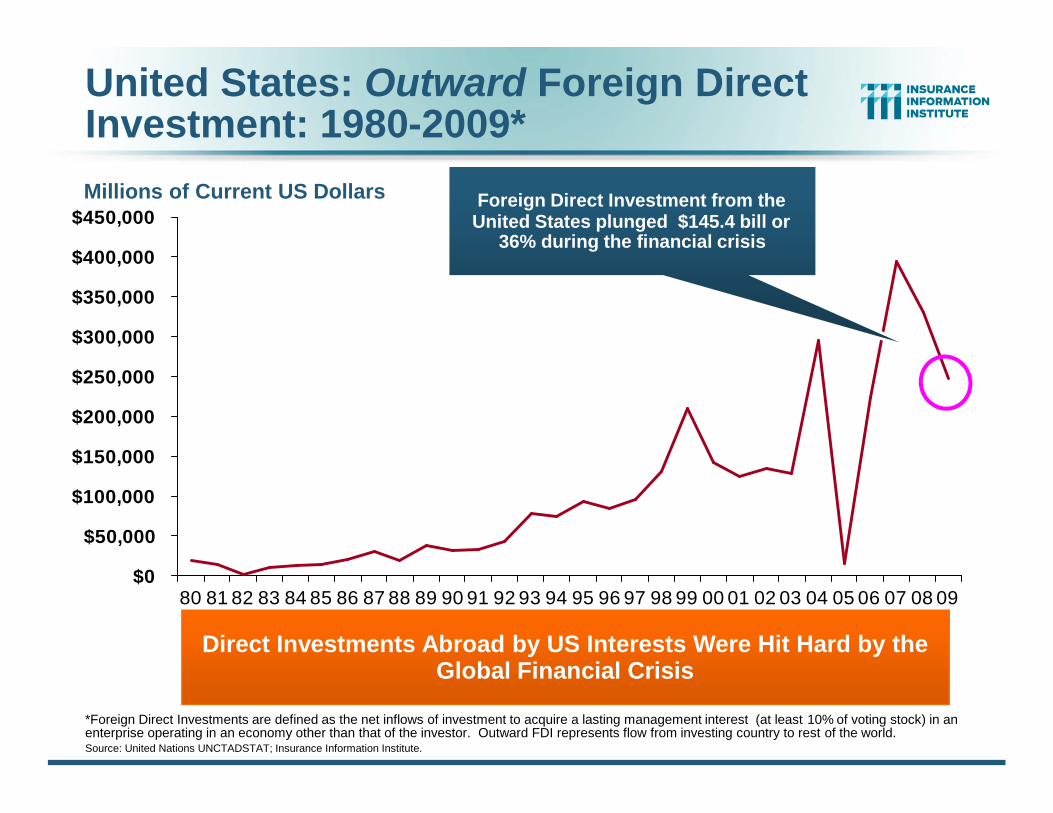

Direct Investments Abroad by US Interests Were Hit Hard by theGlobal Financial Crisis

Millions of Current US Dollars Foreign Direct Investment from theUnited States plunged $145.4 bill or

36% during the financial crisis

United States: Outward Foreign DirectInvestment: 1980-2009*

77

P/C Insurance IndustryFinancial Overview

Profit Recovery ContinuesEarly Stage Growth Begins

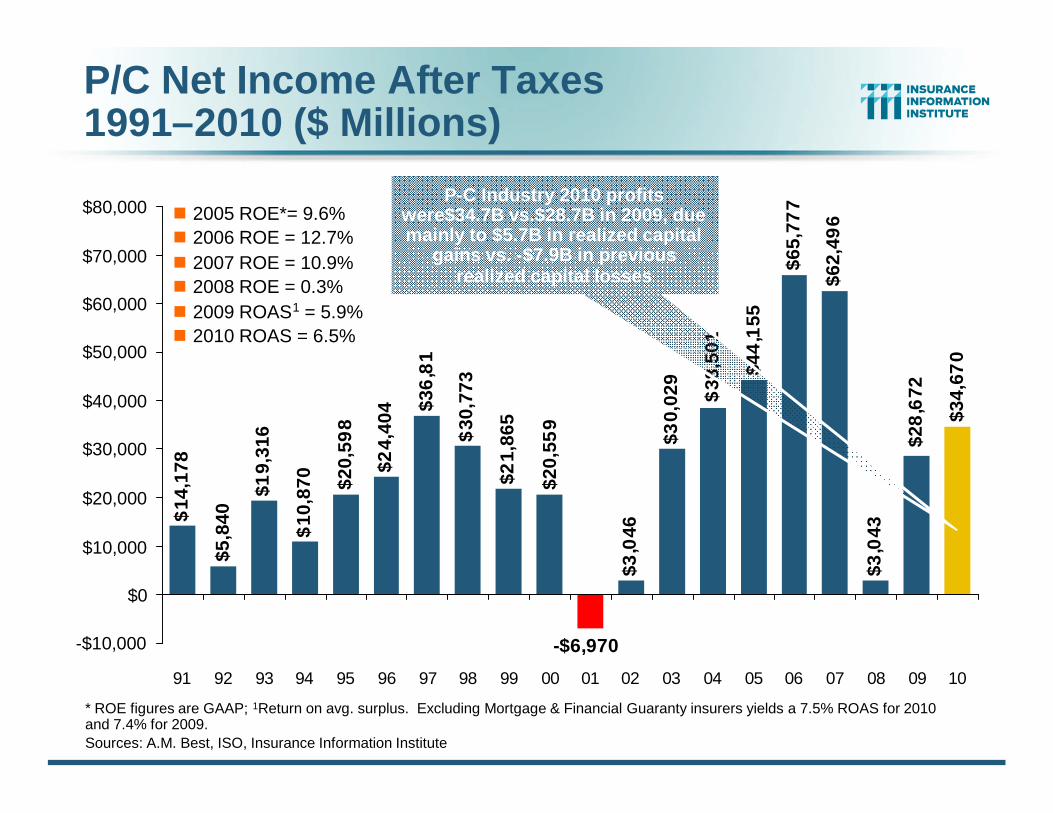

P/C Net Income After Taxes1991–2010 ($ Millions)

$14

,178

$5,8

40

$19,

316

$10

,870 $2

0,59

8

$24,

404 $3

6,8

19

$30

,773

$21,

865

$3,0

46

$30,

029

$62,

496

$3,0

43

$34,

670

$28

,672

-$6,970

$65,

777

$44

,155

$20,

559

$38

,501

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

2005 ROE*= 9.6%2006 ROE = 12.7%2007 ROE = 10.9%2008 ROE = 0.3%2009 ROAS1 = 5.9%2010 ROAS = 6.5%

P-C Industry 2010 profitswere$34.7B vs.$28.7B in 2009, duemainly to $5.7B in realized capital

gains vs. -$7.9B in previousrealized capital losses

* ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 7.5% ROAS for 2010and 7.4% for 2009.Sources: A.M. Best, ISO, Insurance Information Institute

79

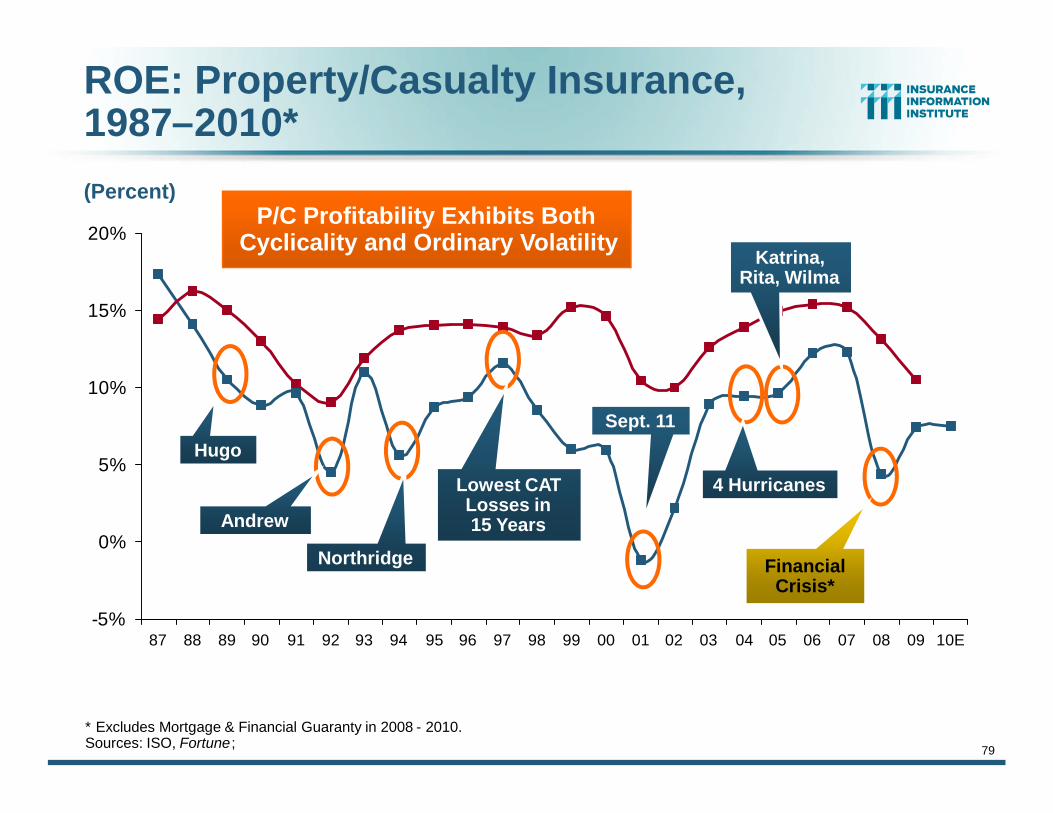

ROE: Property/Casualty Insurance,1987–2010*

* Excludes Mortgage & Financial Guaranty in 2008 - 2010.Sources: ISO, Fortune ;

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10E

P/C Profitability Exhibits BothCyclicality and Ordinary Volatility

Hugo

Andrew

Northridge

Lowest CATLosses in15 Years

Sept. 11

Katrina,Rita, Wilma

4 Hurricanes

FinancialCrisis*

(Percent)

A 100 Combined Ratio Isn’t What ItOnce Was: Investment Impact on ROEs

Combined Ratio / ROE

* 2009 and 2010 figures are return on average statutory surplus. 2008, 2009 and 2010 figures exclude mortgage and financialguaranty insurers

Source: Insurance Information Institute from A.M. Best and ISO data.

97.5

100.6 100.1 100.7

92.6

99.3100.8101.0

7.5%7.4%

9.6%

15.9%14.3%

12.7%

4.4%

8.9%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2008* 2009* 2010*0%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s DepressedInvestment Environment to Generate Risk Appropriate ROEs

A combined ratio of about 100generated ~7.5% ROE in 2009/10,

10% in 2005 and 16% in 1979

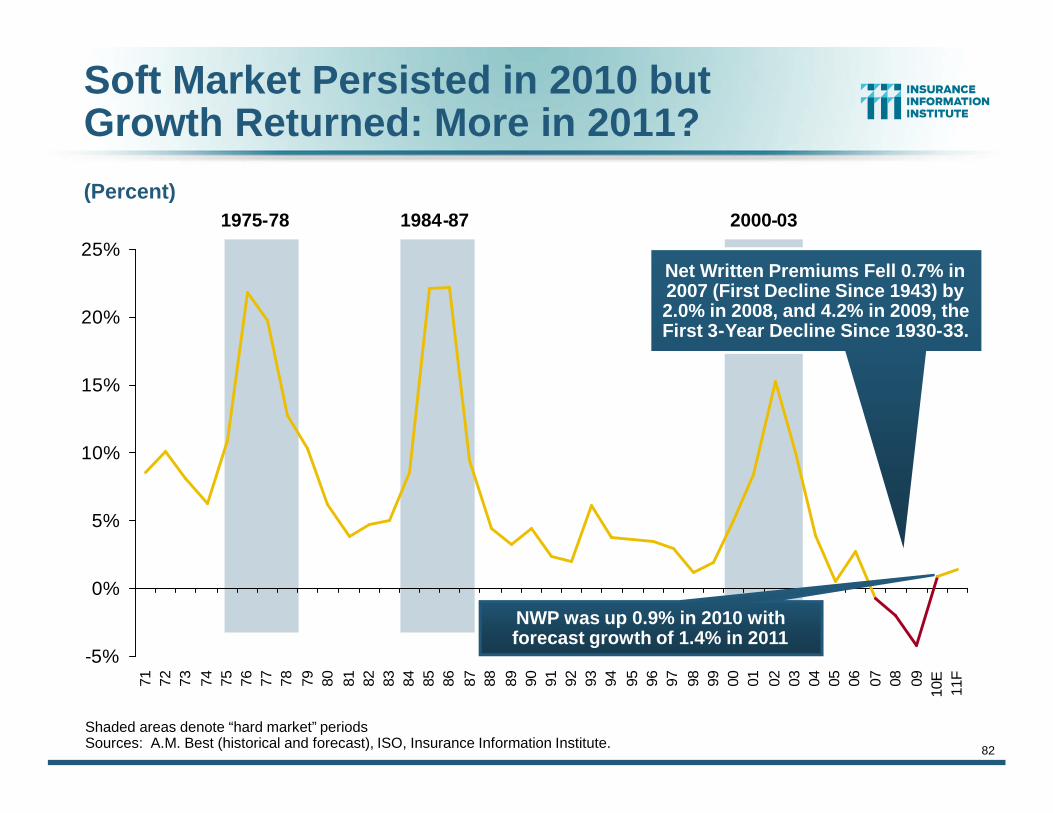

PREMIUM GROWTH TRENDS

81

Winds of Change orMoving Sideways?

82

-5%

0%

5%

10%

15%

20%

25%

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 0910

E11

F

Soft Market Persisted in 2010 butGrowth Returned: More in 2011?

(Percent)1975-78 1984-87 2000-03

Shaded areas denote “hard market” periodsSources: A.M. Best (historical and forecast), ISO, Insurance Information Institute.

Net Written Premiums Fell 0.7% in2007 (First Decline Since 1943) by2.0% in 2008, and 4.2% in 2009, theFirst 3-Year Decline Since 1930-33.

NWP was up 0.9% in 2010 withforecast growth of 1.4% in 2011

83

P/C Net Premiums Written: % Change,Quarter vs. Year-Prior Quarter

Sources: ISO, Insurance Information Institute.

Finally! Back-to-back quarters of net written premium growth(vs. the same quarter, prior year)

10.2

%15

.1%

16.8

%16

.7%

12.5

%10

.1%

9.7%

7.8%

7.2%

5.6%

2.9%

5.5%

-4.6

%-4

.1%

-5.8

%-1

.6%

10.3

%10

.2% 13

.4%

6.6%

-1.6

%2.

1%0.

0%-1

.9%

0.5%

-1.8

%-0

.7%

-4.4

%-3

.7%

-5.3

%-5

.2%

-1.4

%-1

.3%

1.3% 2.

3%1.

3%

-10%

-5%

0%

5%

10%

15%

20%

2002

:Q1

2002

:Q2

2002

:Q3

2002

:Q4

2003

:Q1

2003

:Q2

2003

:Q3

2003

:Q4

2004

:Q1

2004

:Q2

2004

:Q3

2004

:Q4

2005

:Q1

2005

:Q2

2005

:Q3

2005

:Q4

2006

:Q1

2006

:Q2

2006

:Q3

2006

:Q4

2007

:Q1

2007

:Q2

2007

:Q3

2007

:Q4

2008

:Q1

2008

:Q2

2008

:Q3

2008

:Q4

2009

:Q1

2009

:Q2

2009

:Q3

2009

:Q4

2010

:Q1

2010

:Q2

2010

:Q3

2010

:Q4

The long-awaited uptick:

mainlypersonal lines

84

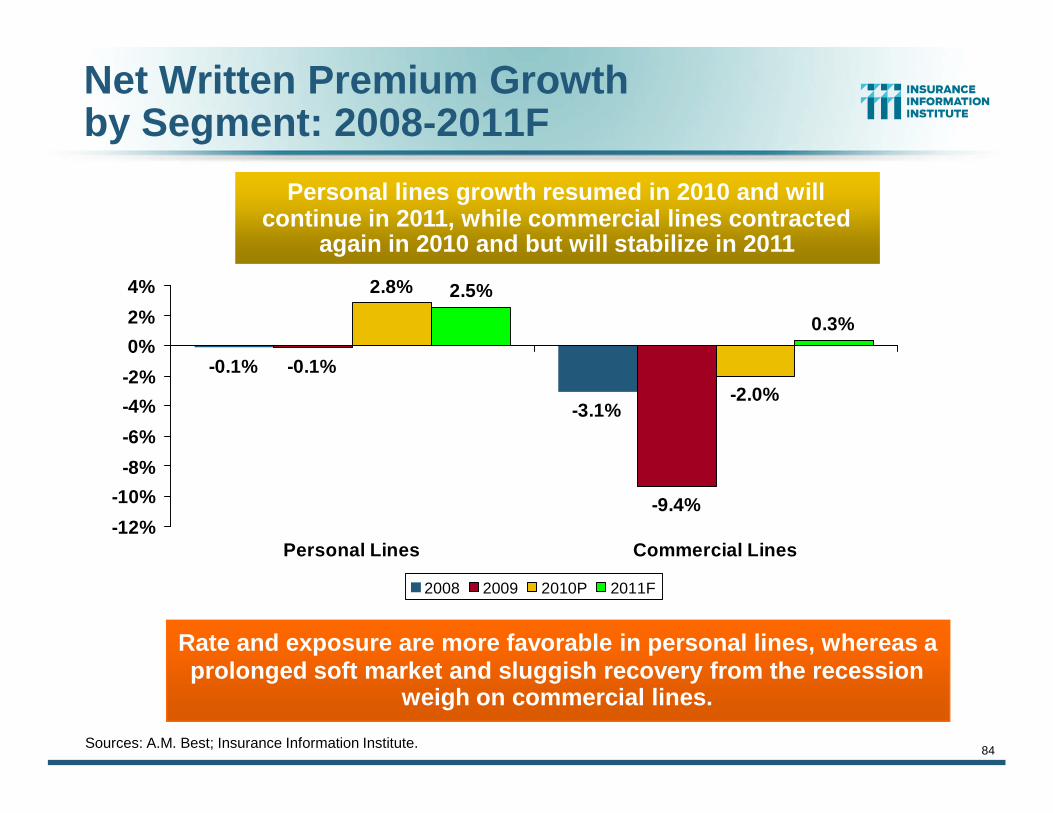

Net Written Premium Growthby Segment: 2008-2011F

-0.1%

-9.4%

2.8%

-2.0%

2.5%

0.3%

-3.1%

-0.1%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

Personal Lines Commercial Lines

2008 2009 2010P 2011F

Rate and exposure are more favorable in personal lines, whereas aprolonged soft market and sluggish recovery from the recession

weigh on commercial lines.

Personal lines growth resumed in 2010 and willcontinue in 2011, while commercial lines contracted

again in 2010 and but will stabilize in 2011

Sources: A.M. Best; Insurance Information Institute.

UNDERWRITING

85

Cyclicality is Driven Primarilyby the Industry’s Underwriting

Cycle, Not the Economy

86

P/C Insurance IndustryCombined Ratio, 2001–2010*

* Excludes Mortgage & Financial Guaranty insurers in 2008, 2009 and 2010. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4Sources: A.M. Best, ISO.

95.7

99.3100.8101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

BestCombinedRatio Since1949 (87.6)

As Recently as 2001,Insurers Paid Out

Nearly $1.16 for Every$1 in Earned

Premiums

RelativelyLow CATLosses,Reserve

Releases

CyclicalDeterioration

Heavy Use ofReinsuranceLowered Net

Losses

RelativelyLow CATLosses,ReserveReleases

Avg. CATLosses,

MoreReserveReleases

87

Calendar Year Combined Ratiosby Segment: 2008-2011F

Sources: A.M. Best . Insurance Information Institute.

102.4

98.9100

106

99.5

108

103.8104.5

9092949698

100102104106108110

Personal Lines Commercial Lines

2008 2009 2010P 2011F

Overall deterioration in 2011 underwriting performance is due to expectedreturn to normal catastrophe activity along with deteriorating underwriting

performance related to the prolonged commercial soft market

Personal lines combined ratio is expected to remain stable in2010 while commercial lines and reinsurance deteriorate

88

2.3

-2.1

-8.3

-2.6-6.6

-9.9-9.8

-4.1

1

11.7

23.2

13.79.9

7.3

-6.7-9.5

-14.6-16 -15

-5

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

$25

$309

2

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10E

11E

Pri

or

Yr.

Re

serv

eR

elea

se

($B

)

-6

-4

-2

0

2

4

6

8 Imp

acton

Co

mb

ined

Ra

tio(P

oin

ts)

Prior Yr. ReserveDevelopment ($B)

Impact onCombined Ratio

P/C Reserve Development, 1992–2011E

Reserve Releases Are Remained Strong in2010 But Should Begin to Taper Off in 2011

Note: 2005 reserve development excludes a $6 billion loss portfolio transfer between American Re and Munich Re. Including thistransaction, total prior year adverse development in 2005 was $7 billion. The data from 2000 and subsequent years excludesdevelopment from financial guaranty and mortgage insurance.Sources: Barclay’s Capital; A.M. Best.

Prior year reservereleases totaled$8.8 billion in the

first half of 2010, upfrom $7.1 billion in

the first half of 2009

EXPENSES

89

Expense Ratios Are Highly Cyclicaland Contribute DeterioratingUnderwriting Performance

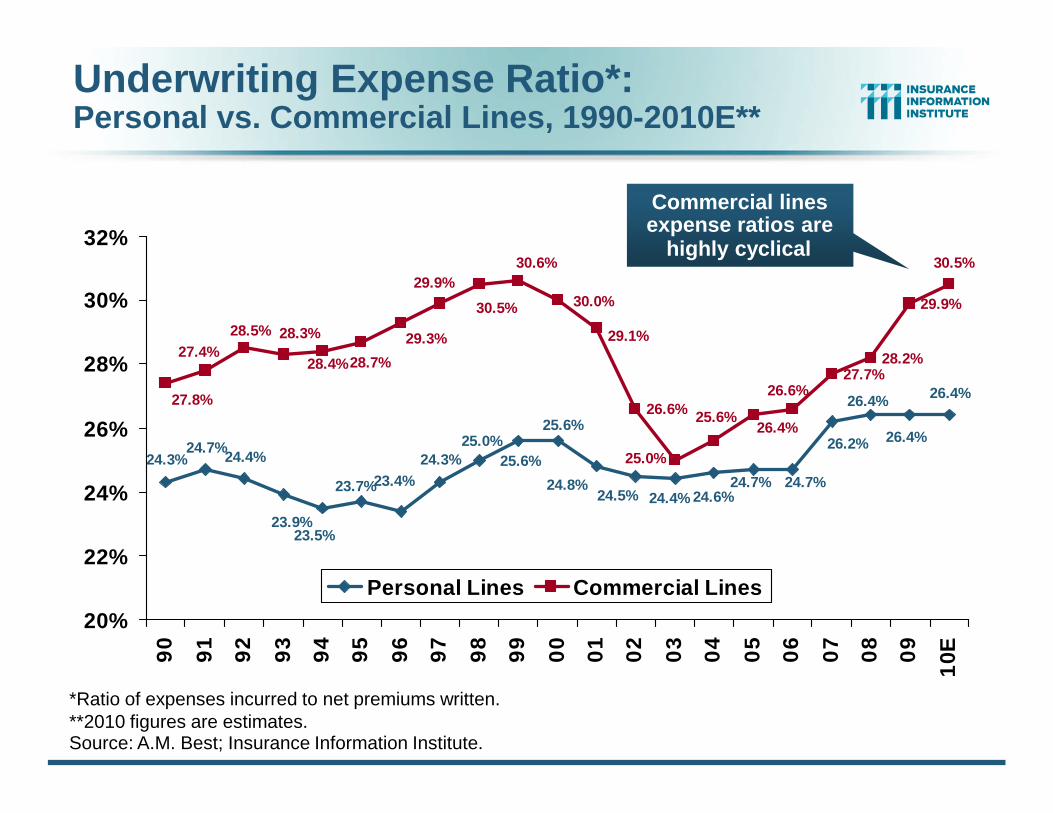

Underwriting Expense Ratio*:Personal vs. Commercial Lines, 1990-2010E**

24.3%24.7%

24.4% 24.3%

26.4%26.6%

27.7%28.2%

29.9%

24.5%

26.4%

26.4%26.2%

24.7%24.7%24.6%24.4%

23.4%23.7%

23.5%

25.0%

23.9%

25.6%

25.6%

24.8%

30.5%30.6%

25.6%

28.5%

26.4%

26.6%

25.0%

29.1%

30.0%30.5%

28.4%

28.3%27.4%

27.8%

28.7%

29.3%

29.9%

20%

22%

24%

26%

28%

30%

32%

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10E

Personal Lines Commercial Lines

*Ratio of expenses incurred to net premiums written.**2010 figures are estimates.Source: A.M. Best; Insurance Information Institute.

Commercial linesexpense ratios are

highly cyclical

INVESTMENTS:THE NEW REALITY

91

Investment Performance is aKey Driver of Profitability

Does It InfluenceUnderwriting or Cyclicality?

Property/Casualty Insurance IndustryInvestment Gain: 1994–20101

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.2

$52.9$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09 10

Investment Gains Recovered Significantly in 2010 Due to RealizedInvestment Gains; The Financial Crisis Caused Investment Gains to

Fall by 50% in 20081 Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.* 2005 figure includes special one-time dividend of $3.2B.Sources: ISO; Insurance Information Institute.

($ Billions)

Investment gains in2010 were the best

since 2007

93

-1.8

%

-1.8

%

-2.0

%

-3.6

%

-3.3

%

-3.3

%

-3.7

%

-4.3

%

-5.2

%

-5.7

%

-7.3%

-1.9

%

-2.1

%

-3.1

%

-8%-7%-6%-5%-4%-3%-2%-1%0%

Perso

nal L

ines

PvtPass

Auto

PersPro

p

Commer

cial

Comm

lAuto

Credit

CommPro

p

Comm

Cas

Fidelity/

Surety

Warra

nty

Surplu

s Lines

MedM

al

WC

Reinsura

nce**

Lower Investment Earnings Place a Greater Burden onUnderwriting and Pricing Discipline

*Based on 2008 Invested Assets and Earned Premiums**US domestic reinsurance onlySource: A.M. Best; Insurance Information Institute.

Reduction in Combined Ratio Necessary to Offset1% Decline in Investment Yield to MaintainConstant ROE, by Line*

Financial Strength &Underwriting

94

Cyclical Pattern is P-C ImpairmentHistory is Directly Tied to

Underwriting, Reserving & Pricing

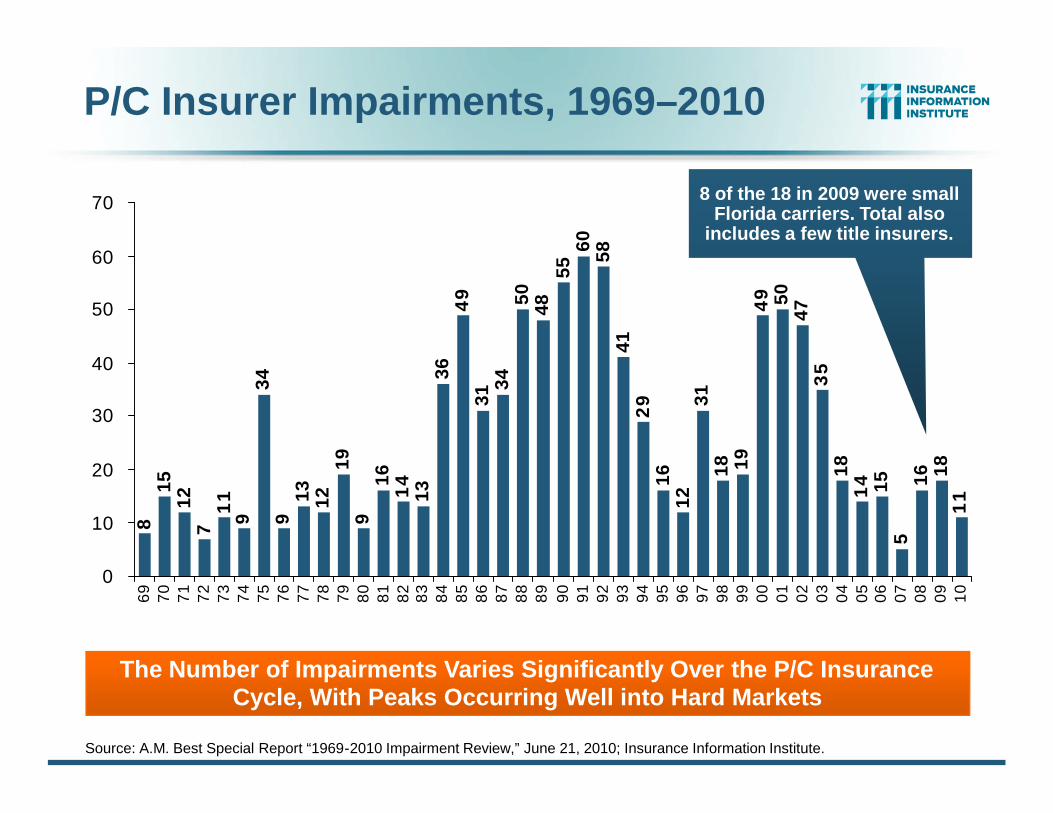

P/C Insurer Impairments, 1969–20108

1512

71

19

349

13 1219

916

14

1336

49

3134

50 4855

60 5841

29

1612

3118 19

49 50

473

518

14 15 16 18

11

5

0

10

20

30

40

50

60

70

69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

Source: A.M. Best Special Report “1969-2010 Impairment Review,” June 21, 2010; Insurance Information Institute.

The Number of Impairments Varies Significantly Over the P/C InsuranceCycle, With Peaks Occurring Well into Hard Markets

8 of the 18 in 2009 were smallFlorida carriers. Total also

includes a few title insurers.

96

P/C Insurer Impairment Frequency vs.Combined Ratio, 1969-2010

90

95

100

105

110

115

1206

97

07

17

27

37

47

57

67

77

87

98

08

18

28

38

48

58

68

78

88

99

09

19

29

39

49

59

69

79

89

90

00

10

20

30

40

50

60

70

80

91

0

Co

mb

ine

dR

atio

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Imp

airmen

tR

ate

Combined Ratio after Div P/C Impairment Frequency

Source: A.M. Best; Insurance Information Institute

2010 impairment rate was 0.35%, down from 0.65% in 2009 andnear the record low of 0.17% in 2007; Rate is still less than

one-half the 0.81% average since 1969

Impairment Rates Are Highly Correlated With Underwriting Performanceand Reached Record Lows in 2007

97

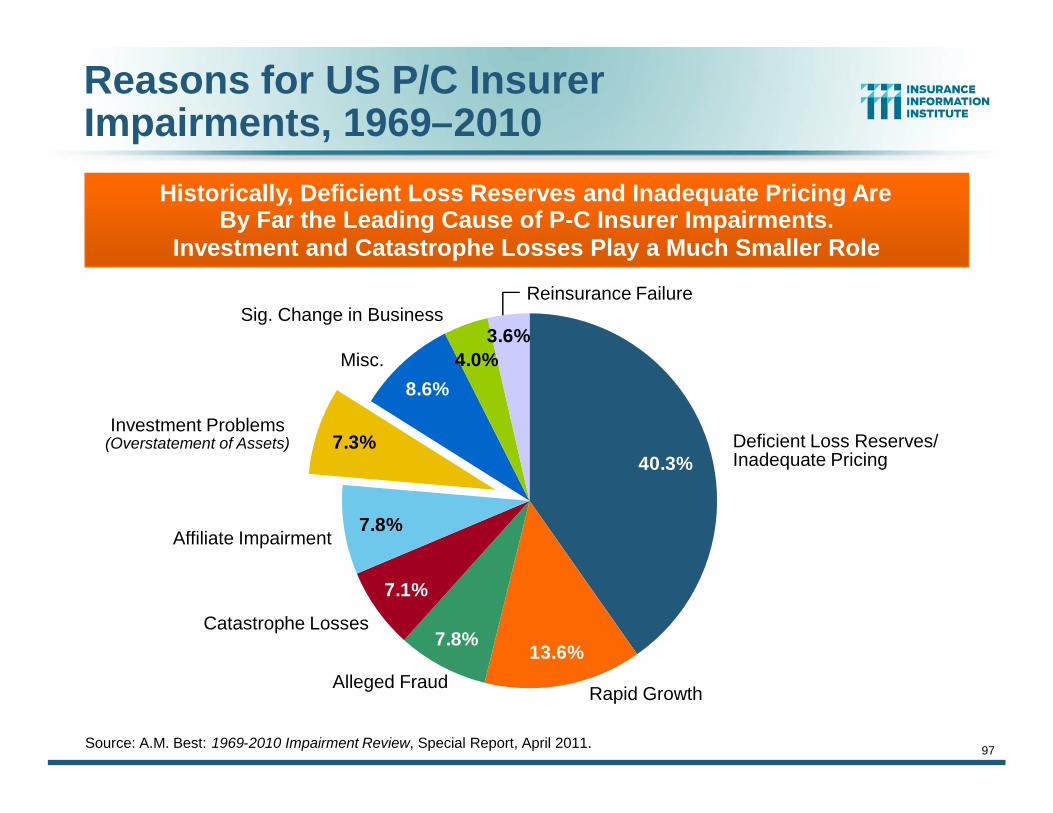

Reasons for US P/C InsurerImpairments, 1969–2010

3.6%4.0%

8.6%

7.3%

7.8%

7.1%

7.8%13.6%

40.3%

Source: A.M. Best: 1969-2010 Impairment Review, Special Report, April 2011.

Historically, Deficient Loss Reserves and Inadequate Pricing AreBy Far the Leading Cause of P-C Insurer Impairments.

Investment and Catastrophe Losses Play a Much Smaller Role

Deficient Loss Reserves/Inadequate Pricing

Reinsurance Failure

Rapid GrowthAlleged Fraud

Catastrophe Losses

Affiliate Impairment

Investment Problems(Overstatement of Assets)

Misc.

Sig. Change in Business

98

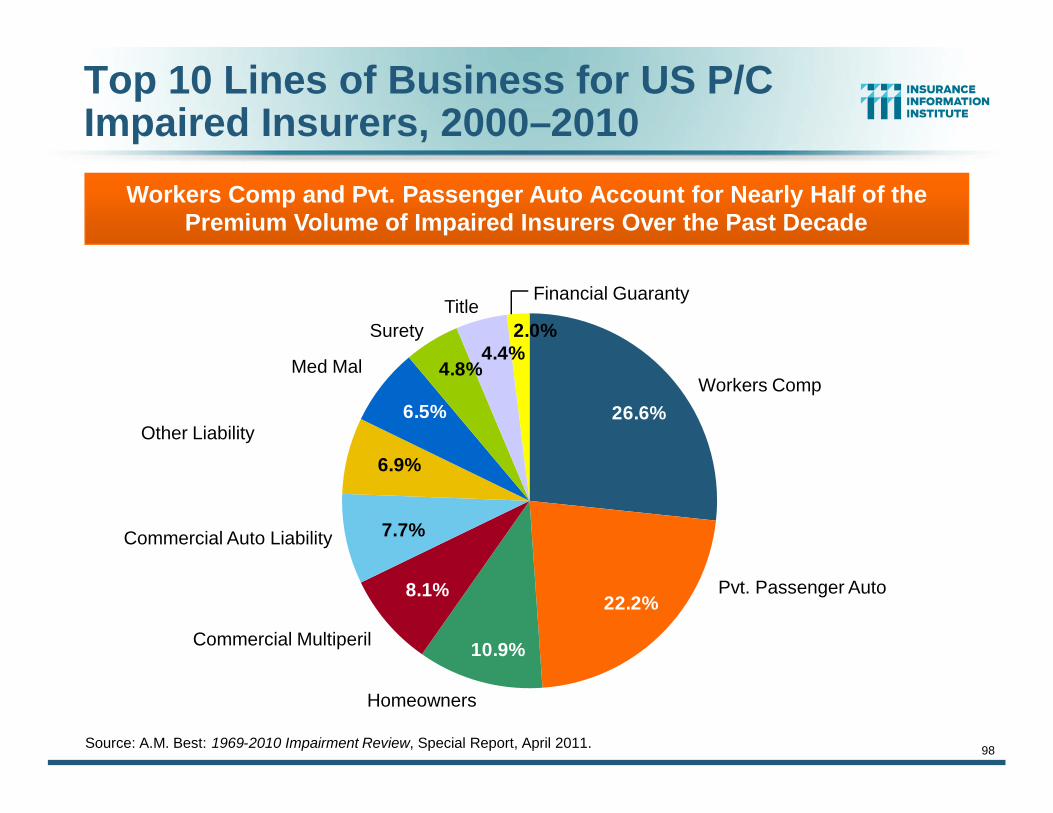

Top 10 Lines of Business for US P/CImpaired Insurers, 2000–2010

2.0%4.4%

4.8%

6.5%

6.9%

7.7%

8.1%

10.9%

22.2%

26.6%

Source: A.M. Best: 1969-2010 Impairment Review, Special Report, April 2011.

Workers Comp and Pvt. Passenger Auto Account for Nearly Half of thePremium Volume of Impaired Insurers Over the Past Decade

Workers Comp

Financial Guaranty

Pvt. Passenger Auto

Homeowners

Commercial Multiperil

Commercial Auto Liability

Other Liability

Med Mal

SuretyTitle

CAPITAL MANAGEMENT &LEVERAGE

99

Excess Capital is a Major Obstacleto a Market Turn;

Capital Management Decisions WillImpact Market Direction

100

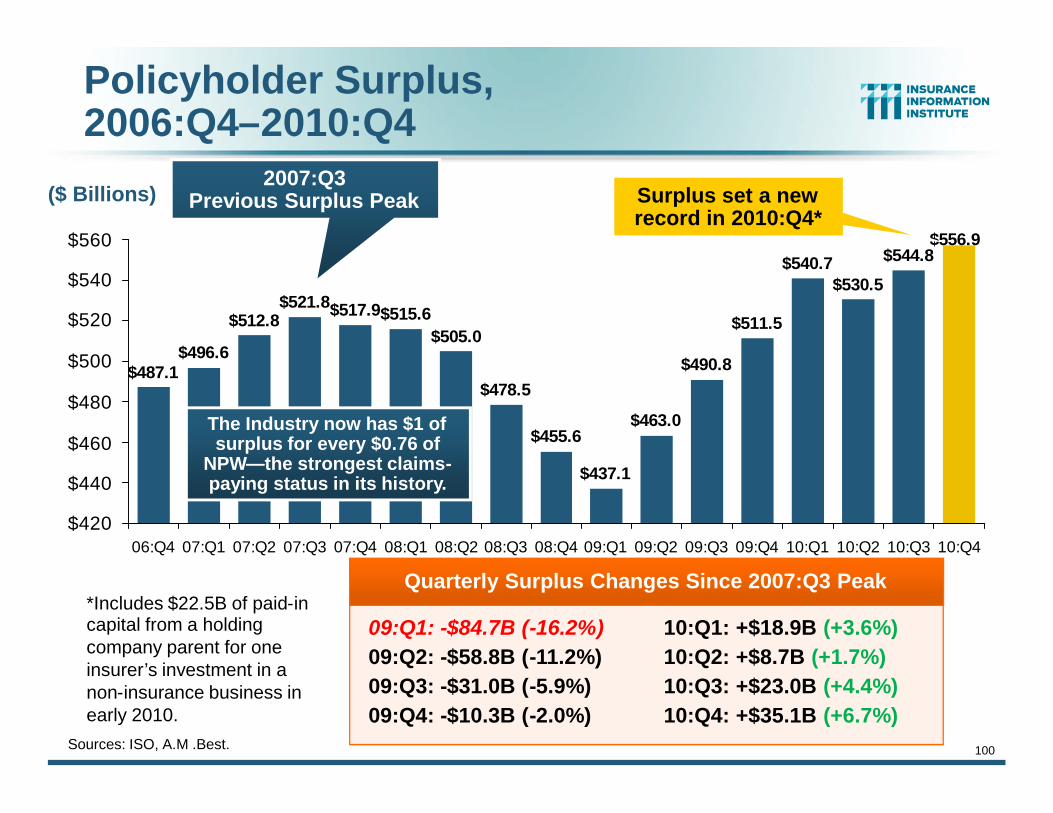

Policyholder Surplus,2006:Q4–2010:Q4

Sources: ISO, A.M .Best.

($ Billions)

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$490.8

$511.5

$540.7$530.5

$544.8$556.9

$505.0$515.6$517.9

$420

$440

$460

$480

$500

$520

$540

$560

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2 10:Q3 10:Q4

2007:Q3Previous Surplus Peak

Quarterly Surplus Changes Since 2007:Q3 Peak

09:Q1: -$84.7B (-16.2%)09:Q2: -$58.8B (-11.2%)09:Q3: -$31.0B (-5.9%)09:Q4: -$10.3B (-2.0%)

10:Q1: +$18.9B (+3.6%)10:Q2: +$8.7B (+1.7%)10:Q3: +$23.0B (+4.4%)10:Q4: +$35.1B (+6.7%)

Surplus set a newrecord in 2010:Q4*

*Includes $22.5B of paid-incapital from a holdingcompany parent for oneinsurer’s investment in anon-insurance business inearly 2010.

The Industry now has $1 ofsurplus for every $0.76 of

NPW—the strongest claims-paying status in its history.

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_hartwigDownload at www.iii.org/presentations

Insurance Information Institute Online:

Top Related