Languages

Pages

Legal

accelerate your ambition

2015 Global Contact Centre Benchmarking Report

24 February 2015

CCW Session

Copyright © 2015 Dimension Data

The Global Contact Centre Benchmarking Report

Launched in 1997

by Merchants, Dimension Data’s subsidiary contact centre specialist.

Annual global research study of multichannel interactions in

contact centres

18 years Of trends, performance analysis and

best practice techniques

Supported by over 30 of the world’s leading industry groups and associations

Participants in this year’s report

901

Copyright © 2015 Dimension Data

Why should we care?

Nancy Jamison – Frost & Sullivan

Nancy Jamison, Principal Analyst at Frost & Sullivan said:

“The depth of decades of benchmarking has enabled Dimension Data to clearly see customer service and engagement trends unfolding in advance, rather than in a reactionary way.”

Copyright © 2015 Dimension Data

2015 results at a glance…

75% of companies recognise service as a competitive differentiator Up 18% in 2 years but c-sat levels down 4th year in succession

Up to 40% say IT doesn’t meet current needs And nearly 80% say current systems won’t meet future needs

23% drop in direct ownership models

34% of contact centres are planning for a hosted solution

Social media is already 1st choice for

Gen Y (globally) Yet 57% of contact centres

have no capability

Omnichannel will become a necessity. It requires a joined up approach

74%

see overall interactions increasing in 2 years

Voice to drop 16%

Non-Voice to rise 85%

Analytics will be key in the next 5 years,

But 40% have no capability

Copyright © 2015 Dimension Data

Four insights on engagement models…gone digital

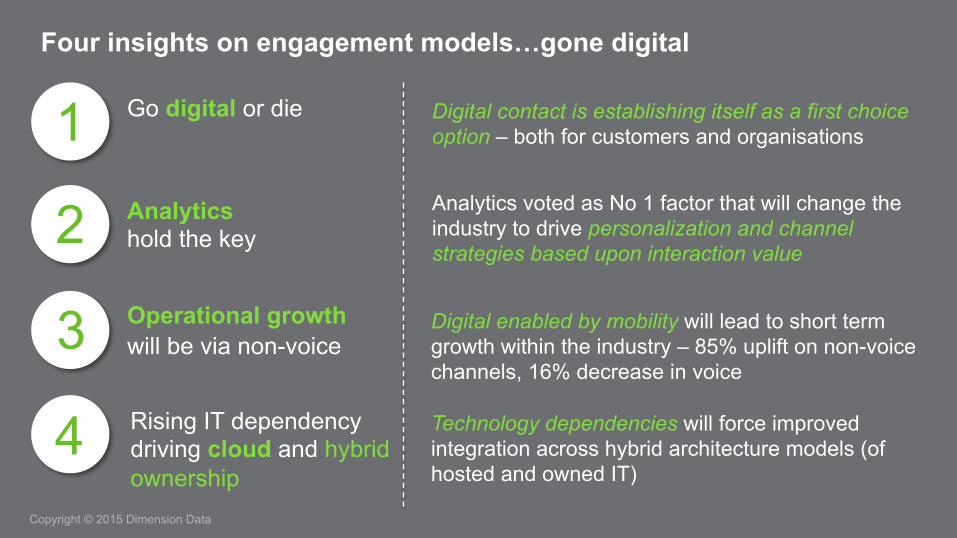

Digital contact is establishing itself as a first choice option – both for customers and organisations

Analytics voted as No 1 factor that will change the industry to drive personalization and channel strategies based upon interaction value

Digital enabled by mobility will lead to short term growth within the industry – 85% uplift on non-voice channels, 16% decrease in voice

Technology dependencies will force improved integration across hybrid architecture models (of hosted and owned IT)

Go digital or die 1Analytics hold the key 2Operational growth will be via non-voice 3Rising IT dependency driving cloud and hybrid ownership

4

Copyright © 2015 Dimension Data

1. Go Digital or Die

Copyright © 2015 Dimension Data

Go Digital or Die As enterprises embrace the potential of digital channels there is a health warning:

Go Digital or Die!

10 years ago there was no social media or smart phone devices and very little web chat. These things have revolutionised the way customer service is delivered

From an operational, technology and people perspective, there are huge challenges and few warning signs to consider as we enter the Digital Age of contact centres

Context:

! Digital contact is establishing itself as a first choice option – both for customers and organisations

accelerate your ambition 8 Copyright © 2015 Dimension Data

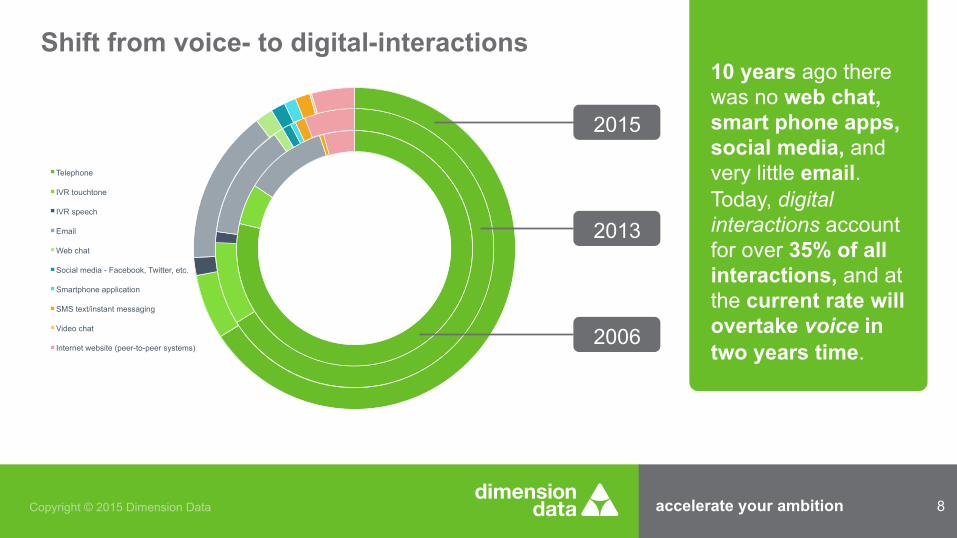

Shift from voice- to digital-interactions 10 years ago there was no web chat, smart phone apps, social media, and very little email. Today, digital interactions account for over 35% of all interactions, and at the current rate will overtake voice in two years time.

Telephone

IVR touchtone

IVR speech

Web chat

Social media - Facebook, Twitter, etc.

Smartphone application

SMS text/instant messaging

Video chat

Internet website (peer-to-peer systems) 2006

2013

2015

accelerate your ambition 9 Copyright © 2015 Dimension Data

0

10

20

30

40

50

60

2006 2008 2009 2011 2012 2015 2016

2006

2008

2009

2011

2012

2015

2016

Forecast Actual

Sources: Dimension Data Global Contact Centre Reports 2006-2015

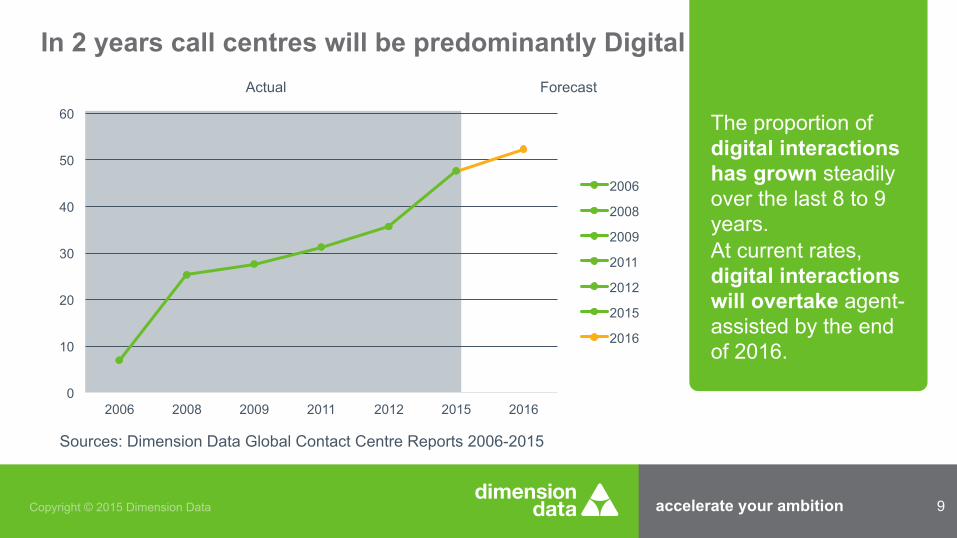

In 2 years call centres will be predominantly Digital

The proportion of digital interactions has grown steadily over the last 8 to 9 years. At current rates, digital interactions will overtake agent-assisted by the end of 2016.

accelerate your ambition 10 Copyright © 2015 Dimension Data

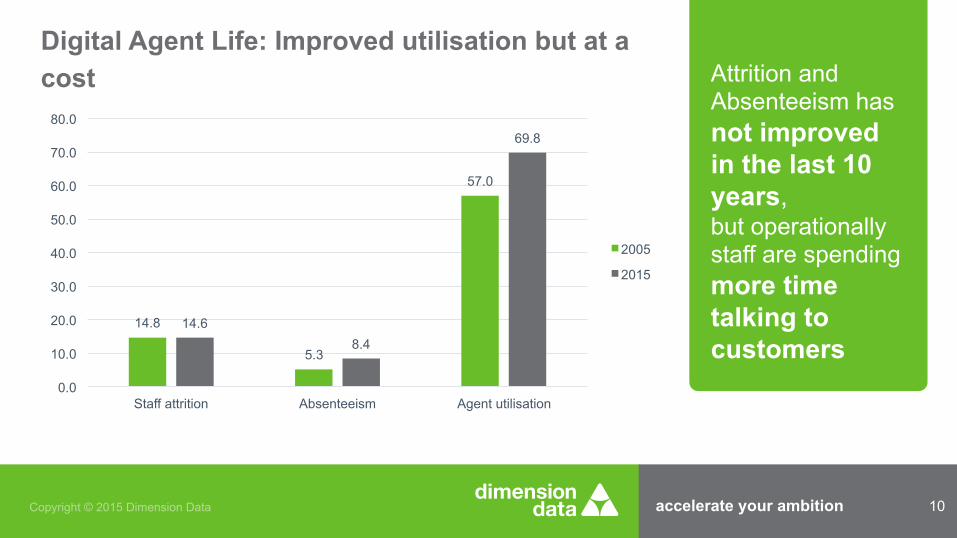

Digital Agent Life: Improved utilisation but at a cost Attrition and

Absenteeism has not improved in the last 10 years, but operationally staff are spending more time talking to customers

14.8

5.3

57.0

14.6 8.4

69.8

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Staff attrition Absenteeism Agent utilisation

2005

2015

accelerate your ambition 11 Copyright © 2015 Dimension Data

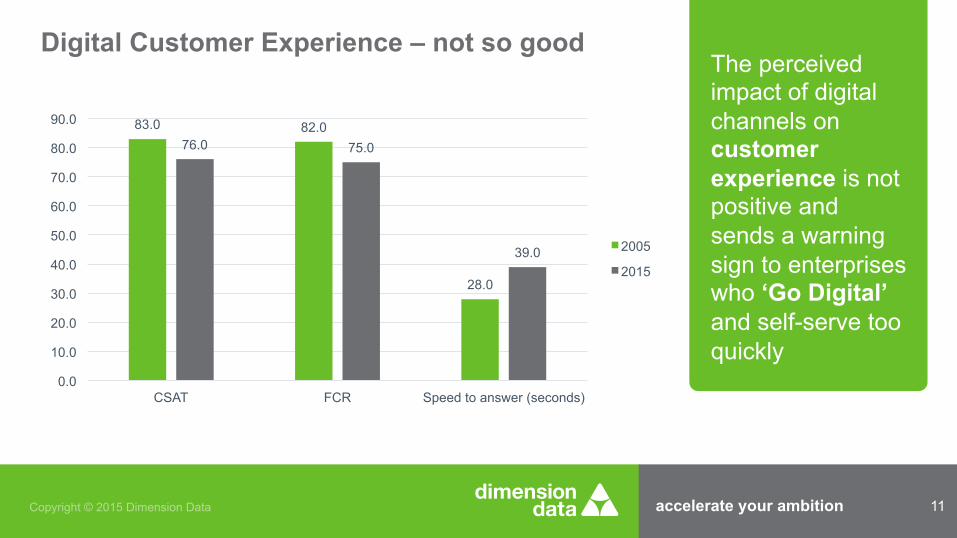

Digital Customer Experience – not so good The perceived impact of digital channels on customer experience is not positive and sends a warning sign to enterprises who ‘Go Digital’ and self-serve too quickly

83.0 82.0

28.0

76.0 75.0

39.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

CSAT FCR Speed to answer (seconds)

2005

2015

Copyright © 2015 Dimension Data

Contact centres have to change

to meet the challenge

Digital is here to stay

Organisations have to adopt new technology and innovative delivery

models to remain relevant and competitive

Customer service in contact centres is undergoing a transformation

Conclusions on the impact of digital

Customer Experience Management is the new mantra for customer service and lifetime value management

Copyright © 2015 Dimension Data

Digital will fuel the need for analytics

Sheila McGee-Smith – McGee-Smith Analytics

Sheila McGee-Smith, founder and principal analyst at McGee-Smith Analytics said: “The most thought-provoking prediction from the 2015 Global Contact Centre Benchmarking Report by Dimension Data - based on data regularly gathered since 2006 - is that digital interactions will overtake agent-assisted by the end of 2016. It is more imperative than ever that businesses find a way to better gather, analyze and ultimately deliver to agent’s predictive information based on prior digital interactions.”

Copyright © 2015 Dimension Data

2. Analytics: here to stay

Copyright © 2015 Dimension Data

Contact centres gather huge amounts of customer data Analytics are reshaping the customer management landscape This presents an opportunity and a threat to contact centres

Analytics voted as # 1 factor that will change the industry to drive personalisation and channel strategies based upon interaction value

Context:

accelerate your ambition 16 Copyright © 2015 Dimension Data

1.7

18.4

24.2

25.9

29.0

32.8

33.6

37.9

43.3

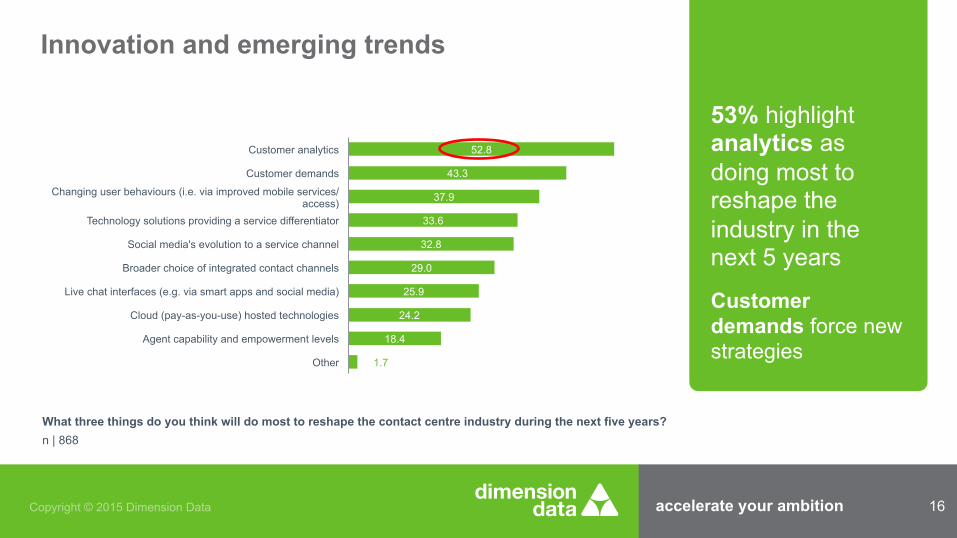

52.8

Other

Agent capability and empowerment levels

Cloud (pay-as-you-use) hosted technologies

Live chat interfaces (e.g. via smart apps and social media)

Broader choice of integrated contact channels

Social media's evolution to a service channel

Technology solutions providing a service differentiator

Changing user behaviours (i.e. via improved mobile services/access)

Customer demands

Customer analytics

Innovation and emerging trends

What three things do you think will do most to reshape the contact centre industry during the next five years? n | 868

53% highlight analytics as doing most to reshape the industry in the next 5 years

Customer demands force new strategies

accelerate your ambition 17 Copyright © 2015 Dimension Data

5.7

13.7

22.8

43.5

52.1

60.1

69.9

78.7

None of these

Automated lesson assignment based on agent QA scores?

Speech/customer voice/text analytics

Data sourcing (i.e. user profile, social media, quality mgt.)

Post-contact survey capability

Data analysis (i.e business performance, Big Data, root cause analysis, trending)

Data presentation - real-time/historic dashboards

Agent performance and capability scorecards

Business information tools available

What business information tools are available within your contact centre? n | 775

40% have no data analysis tools But analytics voted the top factor to change the shape of the industry within the next 5 years

accelerate your ambition 18 Copyright © 2015 Dimension Data

Segmentation: personalised service offerings

What degree of personalised service can you offer based on your segmentation strategy? n | 772

2011 2012 2013/14 2015

Prioritised service channels (e.g. expedited telephone/email channel) Not asked Not asked Not asked 44.4

Prioritised service for specific campaigns/events 8.3 8.8 18.2 34.8

Personalised service for specific customer groups (e.g. high-value/gold card customers) 17.4 19.9 35.1 42.7

We are unable to offer a personalised service at this time based on segmentation levels 17.4 16.7 11.6 10.7

Segmentation isn’t applicable for our customer base 25.8 27.3 26.3 30.3

Personalised service offerings more than doubled in two years: from 20% up to 43%

Demonstrates the impact of improved analytics

Copyright © 2015 Dimension Data

Conclusions on the impact of Analytics

More personalised offers

Improved customer experience

Greater agent productivity

Greater insight

Customer Experience Management is the new mantra for customer service and lifetime value management

Requires focused investment and appreciation of potential across channels

Copyright © 2015 Dimension Data

3. Operational growth: non-voice

Copyright © 2015 Dimension Data

Operational growth non-voice

Context: The opportunity presented by digital channels and interaction is significant in terms of both cost, performance and customer experience

The challenge is to harness the new channels, while improving customer experience

This is proving difficult and many organisations are on a steep learning curve

Digital enabled by mobility will lead to short term growth within the industry – 85% uplift on non-voice channels, 16% decrease in voice

accelerate your ambition 22 Copyright © 2015 Dimension Data

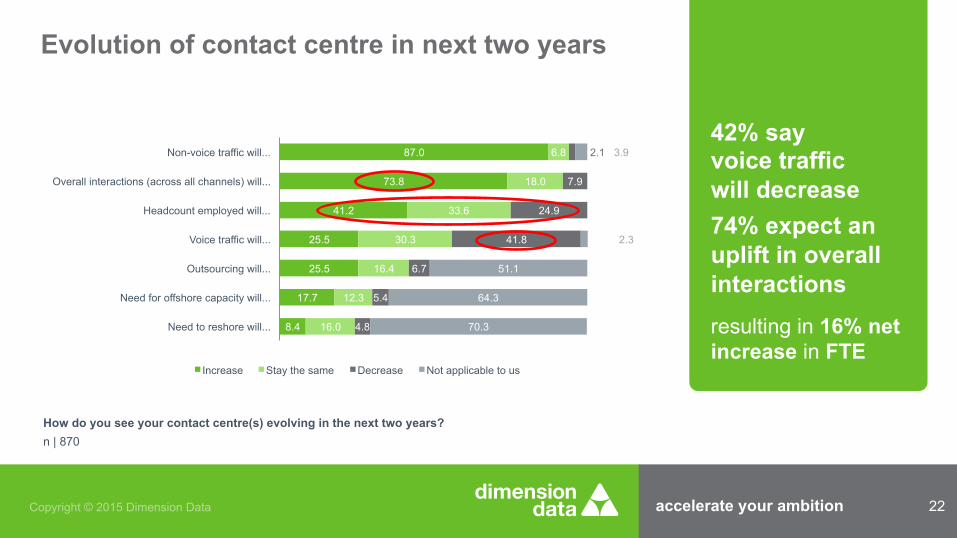

8.4

17.7

25.5

25.5

41.2

73.8

87.0

16.0

12.3

16.4

30.3

33.6

18.0

6.8

4.8

5.4

6.7

41.8

24.9

7.9

2.1

70.3

64.3

51.1

2.3

3.9

Need to reshore will...

Need for offshore capacity will...

Outsourcing will...

Voice traffic will...

Headcount employed will...

Overall interactions (across all channels) will...

Non-voice traffic will...

Increase Stay the same Decrease Not applicable to us

Evolution of contact centre in next two years

How do you see your contact centre(s) evolving in the next two years? n | 870

42% say voice traffic will decrease 74% expect an uplift in overall interactions resulting in 16% net increase in FTE

accelerate your ambition 23 Copyright © 2015 Dimension Data

5.9

10.2

22.9

27.3

32.3

36.5

51.1

56.3

56.8

Other

Cloud (pay-as-you-use) hosted technologies

Speed of technological advancement

Security risks and compliance

Information management

Changing user behaviours (e.g. social media, smart devices)

Staff multiskilling/managing increased complexity

Process optimisation or automation

Migrating customers to self- or assisted-service channels

Industry trends affecting contact centre

What are the top three industry trends currently affecting your contact centre? n | 875

Efficiency dominates

Call deflection emerges as top priority for contact centres

The next step: optimise the experience and benefit and up-skill staff

accelerate your ambition 24 Copyright © 2015 Dimension Data

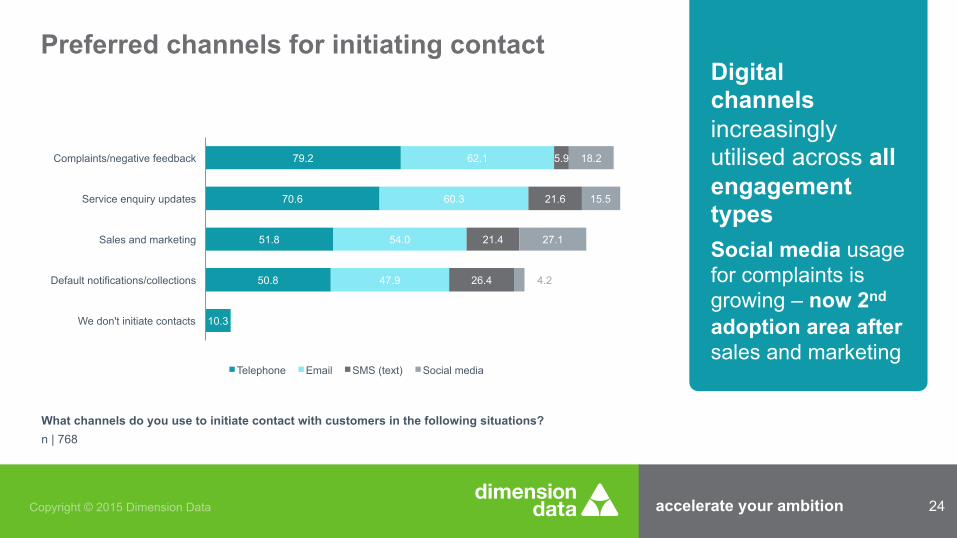

10.3

50.8

51.8

70.6

79.2

47.9

54.0

60.3

62.1

26.4

21.4

21.6

5.9

4.2

27.1

15.5

18.2

We don't initiate contacts

Default notifications/collections

Sales and marketing

Service enquiry updates

Complaints/negative feedback

Telephone Email SMS (text) Social media

Preferred channels for initiating contact

What channels do you use to initiate contact with customers in the following situations? n | 768

Digital channels increasingly utilised across all engagement types Social media usage for complaints is growing – now 2nd adoption area after sales and marketing

accelerate your ambition 25 Copyright © 2015 Dimension Data

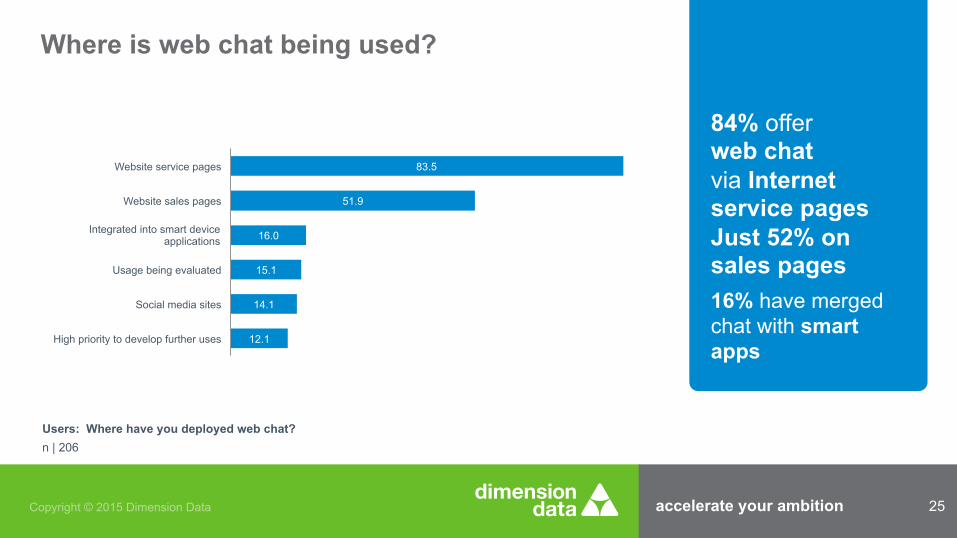

12.1

14.1

15.1

16.0

51.9

83.5

High priority to develop further uses

Social media sites

Usage being evaluated

Integrated into smart device applications

Website sales pages

Website service pages

Where is web chat being used?

Users: Where have you deployed web chat? n | 206

84% offer web chat via Internet service pages Just 52% on sales pages 16% have merged chat with smart apps

accelerate your ambition 26 Copyright © 2015 Dimension Data

24.3

38.7

48.0

49.8

60.5

Web chat facility is available

Personal information can be updated

Contact me facility is available

Services can be ordered/amended/cancelled

Shortcuts to smartphone-configured website pages

Smart app functionality

Users: What smartphone/tablet application (‘smart app’) functionality is available to customers? n | 160

50% can order/amend/cancel services via interactive smart apps 39% can update personal information (up to 66% in media and entertainment)

accelerate your ambition 27 Copyright © 2015 Dimension Data

Customer experience performance levels

What is your average customer experience score for: n | 430

Customer experience is top strategic performance measure But has fallen four years in a row

Percentage Customer

satisfaction % - Actual

2015 76.3

2013/14 77.6

2012 80.4

2011 82.1

Copyright © 2015 Dimension Data

Conclusions on the impact of Operational non-voice

Customers are showing strong preference to self-serve and adopt Apps and web-chat

The shift is gathering pace: Digital will overtake voice in CC’s inside 2 years

Customer experience is suffering: Organisations still not able to affect customer experience as effectively in digital channels as they do in voice.

Copyright © 2015 Dimension Data

4. IT dependency: cloud and hybrid

Copyright © 2015 Dimension Data

IT dependencies driving cloud and hybrid Systems in contact centres have consistently fallen short of expectations

Availability of different procurement and consumption models is set to change the landscape

Organisations are exploring options and seeing almost instant benefits

Technology dependencies will force improved integration across hybrid architecture models (of hosted and owned IT)

Context:

accelerate your ambition 31 Copyright © 2015 Dimension Data

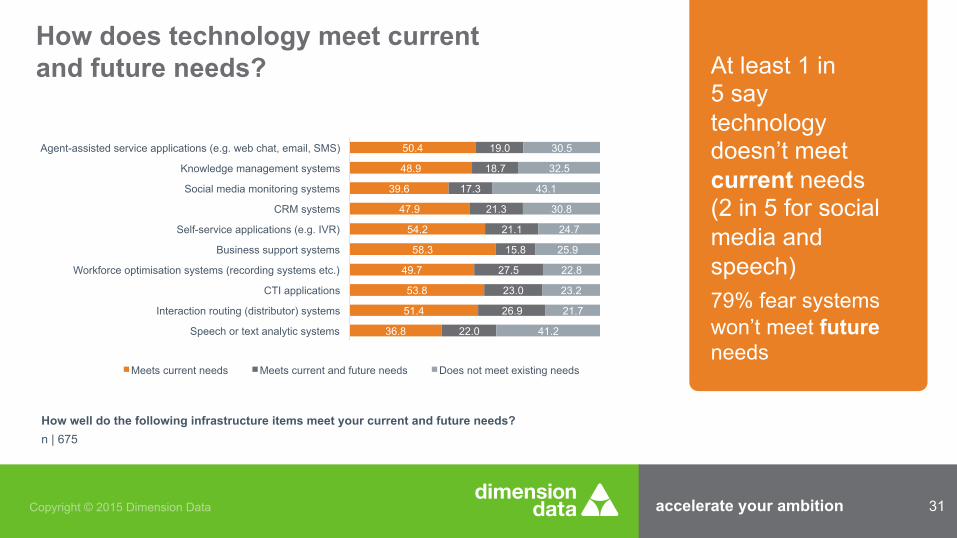

36.8

51.4

53.8

49.7

58.3

54.2

47.9

39.6

48.9

50.4

22.0

26.9

23.0

27.5

15.8

21.1

21.3

17.3

18.7

19.0

41.2

21.7

23.2

22.8

25.9

24.7

30.8

43.1

32.5

30.5

Speech or text analytic systems

Interaction routing (distributor) systems

CTI applications

Workforce optimisation systems (recording systems etc.)

Business support systems

Self-service applications (e.g. IVR)

CRM systems

Social media monitoring systems

Knowledge management systems

Agent-assisted service applications (e.g. web chat, email, SMS)

Meets current needs Meets current and future needs Does not meet existing needs

How does technology meet current and future needs?

How well do the following infrastructure items meet your current and future needs? n | 675

At least 1 in 5 say technology doesn’t meet current needs (2 in 5 for social media and speech) 79% fear systems won’t meet future needs

accelerate your ambition 32 Copyright © 2015 Dimension Data

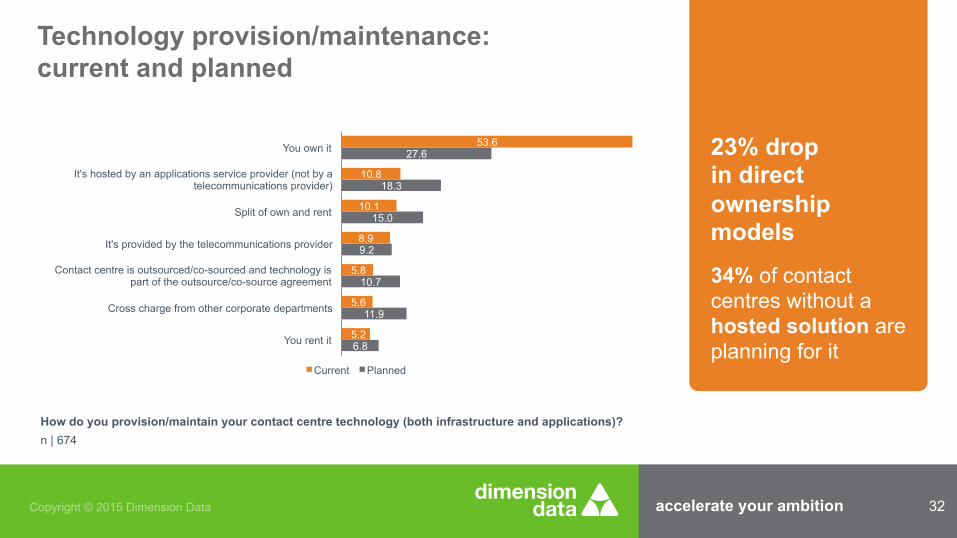

6.8

11.9

10.7

9.2

15.0

18.3

27.6

5.2

5.6

5.8

8.9

10.1

10.8

53.6

You rent it

Cross charge from other corporate departments

Contact centre is outsourced/co-sourced and technology is part of the outsource/co-source agreement

It's provided by the telecommunications provider

Split of own and rent

It's hosted by an applications service provider (not by a telecommunications provider)

You own it

Current Planned

Technology provision/maintenance: current and planned

How do you provision/maintain your contact centre technology (both infrastructure and applications)? n | 674

23% drop in direct ownership models

34% of contact centres without a hosted solution are planning for it

accelerate your ambition 33 Copyright © 2015 Dimension Data

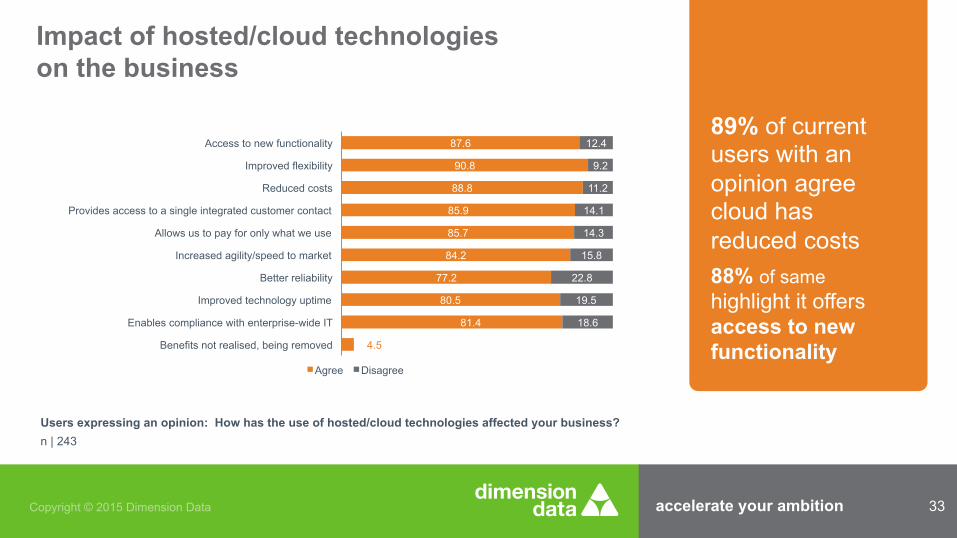

4.5

81.4

80.5

77.2

84.2

85.7

85.9

88.8

90.8

87.6

18.6

19.5

22.8

15.8

14.3

14.1

11.2

9.2

12.4

Benefits not realised, being removed

Enables compliance with enterprise-wide IT

Improved technology uptime

Better reliability

Increased agility/speed to market

Allows us to pay for only what we use

Provides access to a single integrated customer contact

Reduced costs

Improved flexibility

Access to new functionality

Agree Disagree

Impact of hosted/cloud technologies on the business

Users expressing an opinion: How has the use of hosted/cloud technologies affected your business? n | 243

89% of current users with an opinion agree cloud has reduced costs 88% of same highlight it offers access to new functionality

Copyright © 2015 Dimension Data

Faster time to deploy and use

Lower cost to win and maintain

Easier access to new functionality and new

channel solutions

Improved performance and

flexibility

Conclusions on Cloud and Hybrid Technology

Challenge is in creating the collaborative approach between the business and IT to create the roadmap for change and prioritise investments based on tangible ROI

Copyright © 2015 Dimension Data

The Portal

accelerate your ambition 36 Copyright © 2015 Dimension Data

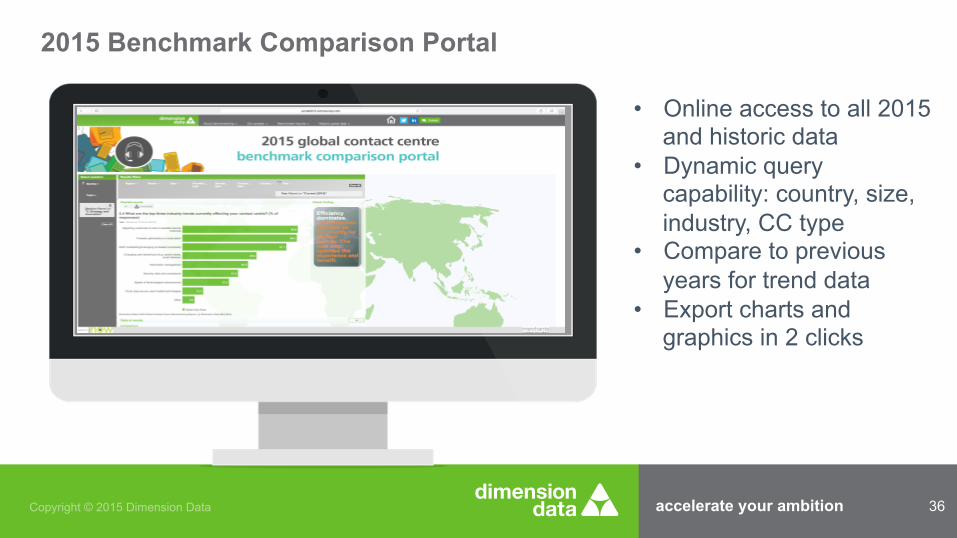

2015 Benchmark Comparison Portal

• Online access to all 2015 and historic data

• Dynamic query capability: country, size, industry, CC type

• Compare to previous years for trend data

• Export charts and graphics in 2 clicks

Copyright © 2015 Dimension Data

Further information… 2015 Global Contact Centre Benchmarking Report

Contact us: Hall 2.1 Stand B10 Andrew McNair – Head of Benchmarking Tel: +1 778 991 0055 (Canada - PST) [email protected]

Robert Allman – Principal Director, Communications Tel: +44 7964 194 643 [email protected]

Richard Holmes – Benchmarking Manager Tel: +44 7812 009 588 (UK) [email protected]

Paul Scott – Consulting Executive, Communications Tel: +44 7812 009 569 (UK) [email protected]

accelerate your ambition

Questions?

Top Related