Languages

Pages

Legal

1

Global Beauty Trends:Consumer & Product Perspectives

Daniel Bone – PresenterConsumer Insights Director

2

Datamonitor

Grooming for success

Grooming for less

Grooming for the planet

Grooming for results

AgendaQuick introduction to us and then four core themes

3

About usUnderstanding consumers, providing answers

Multiple waves of primary consumer research spanning 20 countries across six continents

4

BACK TO INDEX NEXT SECTION

1. GROOMING FOR SUCCESS

5

Grooming and wellbeing continues to matter despite financial pressures

Majorities are preoccupied with looking good

The trend is inclusive of Asia. More about the Japanese nuances tomorrow

Grooming for success

Source: Datamonitor Consumer Survey, 2011

Think it is important to look their best in day‐to‐day life

6

Grooming for successAttitude behavior‐gaps are apparent. But less so in Asia

Nearly half of consumers are highly attentive to looking their best

Belief in the need for personal care is evidently very high within Asia = potential

73%

67%

62%

55%

31%

Source: Datamonitor Consumer Survey, 2010

Highly attentive to looking their best in day‐to‐day life (select countries)

7

Beauty products are often integral to personal/self‐identity

Majorities globally associate physical attractiveness with enhanced life success

Developing Asian economies place high emphasis on self‐expressive beauty

Grooming for success

Believe that physically attractive people have more opportunities in life

Women: 68% Men: 60%

Source: Datamonitor Consumer Survey, 2010, Brand Management, 2010

"Indian, Chinese and Philippine females…perceived beauty care

products as more important for self‐expression than consumers in the

other countries [Malaysia, Japan and Australia]”

In a finding that reinforce the previously presented survey data…

More likely to pay a premium for beauty brands re‐enforcing their self‐identify

8

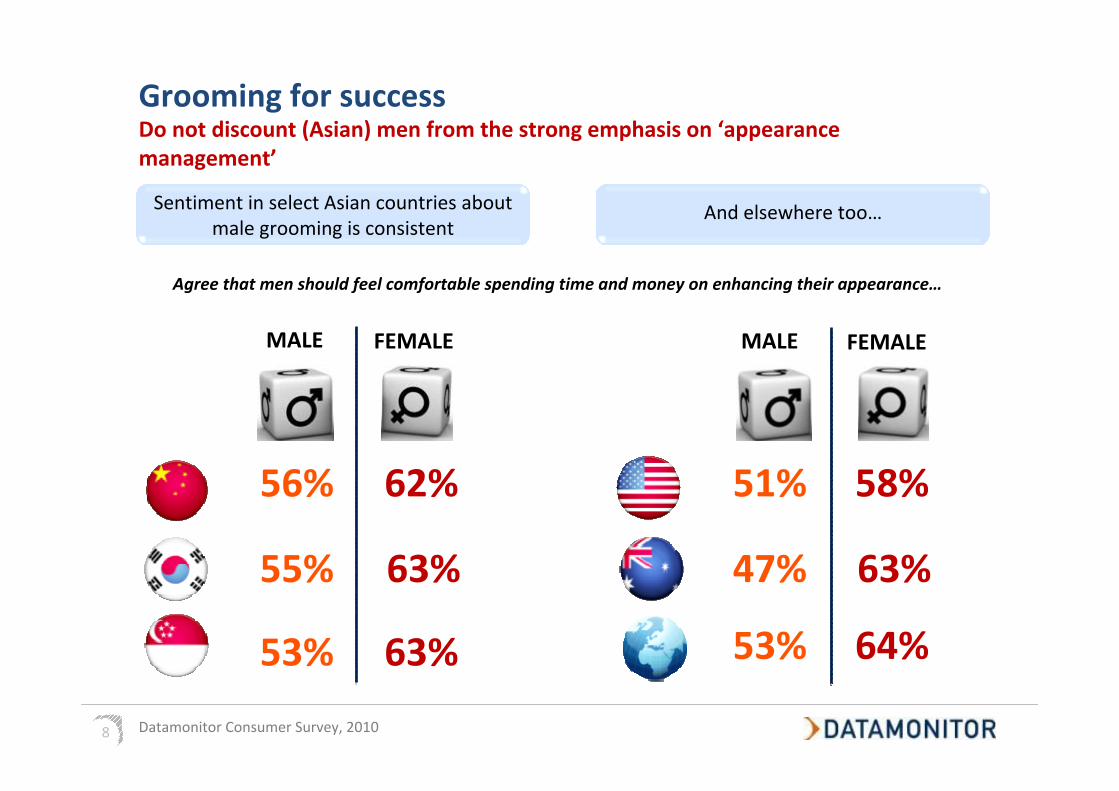

Do not discount (Asian) men from the strong emphasis on ‘appearance management’

Sentiment in select Asian countries about male grooming is consistent

Grooming for success

Datamonitor Consumer Survey, 2010

Agree that men should feel comfortable spending time and money on enhancing their appearance…

56% 62%

55% 63%

53% 63%

51% 58%

47% 63%

53% 64%

And elsewhere too…

MALE FEMALE MALE FEMALE

9

Grooming for successVisual culture also creates anxiety or ‘beauty stress’

For some, personal care is a compulsion rather than pleasure

More than a quarter of emerging market consumers show interest in cosmetic surgery

7%

Source: Datamonitor Consumer Surveys, 2010 and 2011

41%

30%

19%

28%

Would consider cosmetic surgery at some point (select countries)

23%

10%

41%admit to feeling under pressure to look good in day‐

to‐day life

are ‘very satisfied’ with their physical attractiveness

10

Grooming for successCampaigns to bring in lapsed and disengaged users have their place BUT…

Featured a clean‐shaven black man getting ready to discard his scraggly, unshaven head fronted with the words "Re‐Civilize Yourself”

A campaign that was arguably trying to be ethnically diverse backfired, with widespread and rapid criticism emerging to denounce the campaign as racist

The example serves to highlight the ease at which marketing intentions differ markedly from stakeholder perception

Nivea's “Give a Damn Campaign”

11

‘Beauty stress’ is a constant source of negativity for the

industry to address through CSR. Sometimes the industry creates

its own PR problems!

‘Beauty stress’ is a constant source of negativity for the

industry to address through CSR. Sometimes the industry creates

its own PR problems!

Men are embracing ‘Visual Culture’: ignore the male market opportunity – both in Asia and

beyond – at your peril

Men are embracing ‘Visual Culture’: ignore the male market opportunity – both in Asia and

beyond – at your peril

Still a notable segment seemingly disengaged. These represent lost

occasions and revenues

Still a notable segment seemingly disengaged. These represent lost

occasions and revenues

Grooming for successIn summary

Majorities are preoccupied with looking good. It is associated with success and feeling

confident. Even more so in Asia

Majorities are preoccupied with looking good. It is associated with success and feeling

confident. Even more so in Asia

12

PREVIOUS SECTION BACK TO INDEX NEXT SECTION

2. GROOMING FOR LESS

13

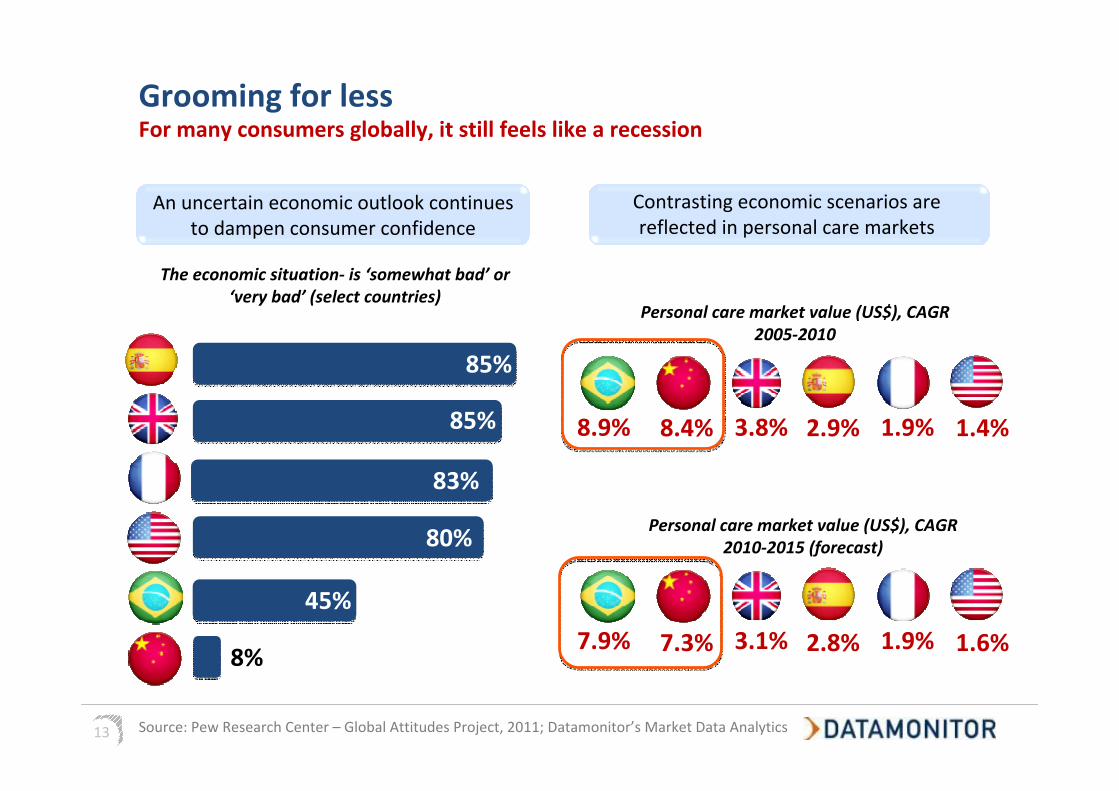

For many consumers globally, it still feels like a recession

An uncertain economic outlook continues to dampen consumer confidence

Contrasting economic scenarios are reflected in personal care markets

Grooming for less

Source: Pew Research Center – Global Attitudes Project, 2011; Datamonitor’s Market Data Analytics

The economic situation‐ is ‘somewhat bad’ or‘very bad’ (select countries)

80%

85%

85%

45%

8%

83%

Personal care market value (US$), CAGR 2005‐2010

8.9% 8.4% 3.8% 2.9% 1.9% 1.4%

Personal care market value (US$), CAGR 2010‐2015 (forecast)

7.9% 7.3% 3.1% 2.8% 1.9% 1.6%

14

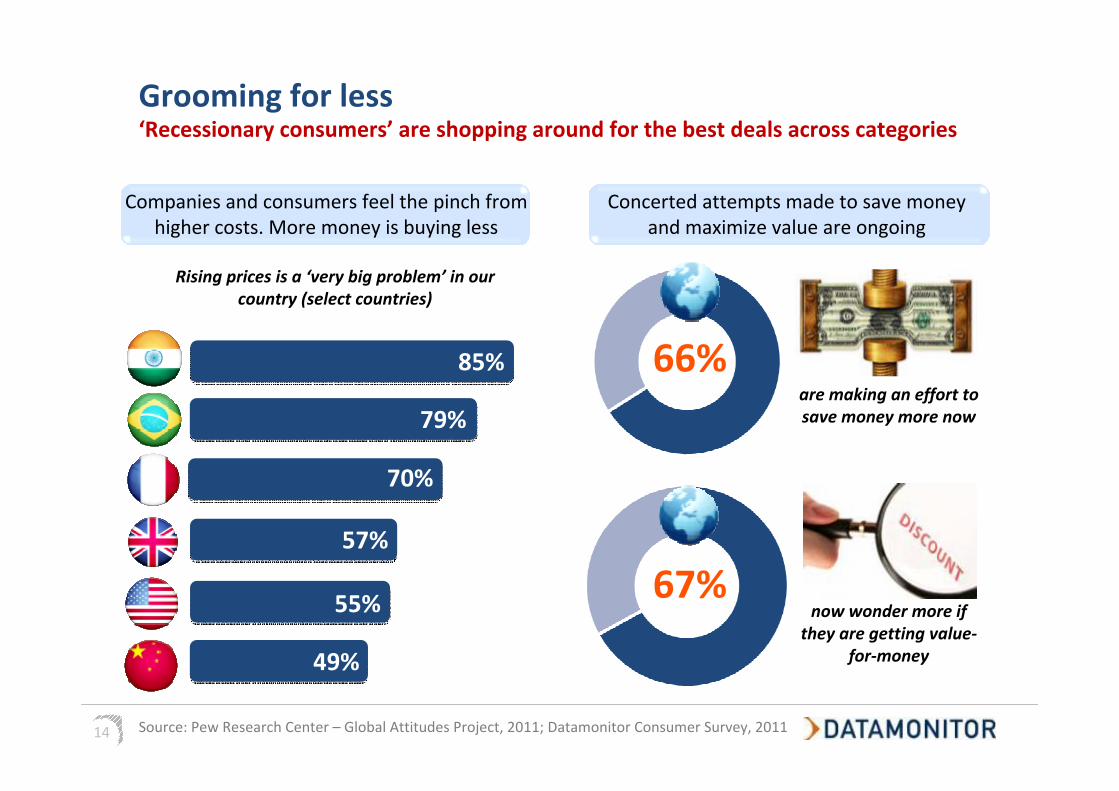

‘Recessionary consumers’ are shopping around for the best deals across categories

Companies and consumers feel the pinch from higher costs. More money is buying less

Concerted attempts made to save money and maximize value are ongoing

Grooming for less

Source: Pew Research Center – Global Attitudes Project, 2011; Datamonitor Consumer Survey, 2011

Rising prices is a ‘very big problem’ in our country (select countries)

57%

55%

70%

79%

85%

49%

66%

67%now wonder more if

they are getting value‐for‐money

are making an effort to save money more now

15

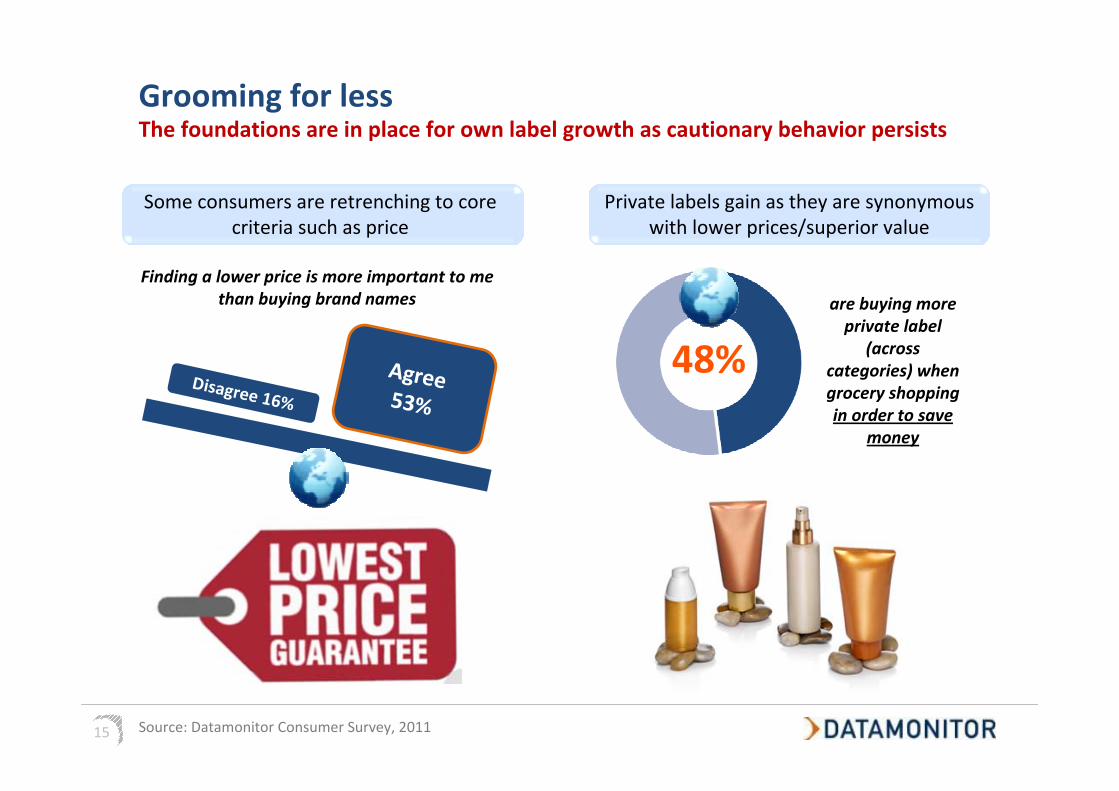

Grooming for lessThe foundations are in place for own label growth as cautionary behavior persists

Some consumers are retrenching to core criteria such as price

48%

are buying more private label

(across categories) when grocery shopping in order to save

money

Private labels gain as they are synonymous with lower prices/superior value

Agree53%

Disagree 16%

Finding a lower price is more important to me than buying brand names

Source: Datamonitor Consumer Survey, 2011

16

Grooming for lessEconomic troubles have meant the steady migration to private label has accelerated

37%agree that that private label beauty products are a good alternative

to famous name brands. Most other

respondents are unsure

Improving perceptions of private label personal care products are apparent

Influenced by widening exposure to such products

1. Private Label2. Natural3. Upscale4. Long‐Lasting5. No Paraben6. Organic7. Anti‐Aging8. High Vitamins9. No Alcohol10. Whitening11. Sensitive Skin12. Kids13. No Artificial Color14. No Animal15. No Allergy

Top 15 claims/ tags of all personal care product launches captured (Dec 2010‐

2011)

Source: Datamonitor Consumer Survey, 2011; Datamonitor’s Product Launch Analytics

17

Grooming for lessConsumers’ first experiences with private labels are typically in the food sector

FOOD &

DRINKS

PERS

ONAL

CARE

ALCOHOLIC

DRINKS

Meat, fish, and poultry

Dairy food

Spirits

Infant formula

Fragrances

Make‐up

Pasta & noodles

Haircare

Coffee

Oral hygiene

Beer, cider, and FABs

Tea

Wine

Skincare

Baby personal care

Product adoption pathway for private label grocery products

Bakery & cereals

Confectionery

Functional drinks

HOUSEHOLD

CA

RE

Spirits

Dishwashing products

Wine

Frozen food

Toilet care

Textile washing products

Air fresheners

Insecticides

18

Grooming for lessThe internet and pricing transparency has empowered bargain hunting consumers

More time55%Less time 5%

Researching or comparing prices of goods‐services in the last year

Shoppers have begun spending more time “shopping outside the aisles”

The range of influences is proliferating amid fragmenting media

Around 1‐in‐5 ROUTINELY USE:

•Social media (e.g. Twitter, Facebook)•Online communities (e.g. forums) •Expert blogs

To help guide their personal care product choices…

Source: Datamonitor Consumer Survey, 2011

19

Grooming for less‘On‐trend’ products

Blemish Balms profiting from time and money being the great scarcities of life

Multi‐market marketing

A chance to simplify skincare routines. Garnier Miracle Skin Protector BB Cream became Australia’s No. 1 product in facial skincare in the first week of TV

Watch for these offering more benefits and going after the male market. Also expect range assortments to be cleaned up

Source: Retail World, December 2011

New budget skincare lines by Sheseido and Kanebo are positioned are positioned as ‘masstige’ brands elsewhere in Asia

Senka and Ururi are ‘flanker brands’ in Japan – countering a rising private label threat

20

Grooming for less‘On‐trend’ products

Walmart shows that private labels can lead the way in technical innovation

Superdrug has used rare and exotic ingredients for added allure

A no‐drip hair colorant called Fat Foam

Launched more than six months ahead of its national competitors

First to market drip free technology enhanced the perceived exclusivity and value of Walmart’s private label range

Optimum anti‐aging serum uses extracts from a rare Swiss apple plant renowned for its anti‐aging benefits

Apple extract provides the same anti‐aging technology as premium brands like Lancôme

21

Consumers are more scrupulous about researching their everyday products, benefitting from access

to information online about where to find lower prices

Consumers are more scrupulous about researching their everyday products, benefitting from access

to information online about where to find lower prices

Private labels compete more intensively with national brands. Just one of many options for

shoppers to get what they want

Private labels compete more intensively with national brands. Just one of many options for

shoppers to get what they want

Exercising restraint and savvy shopping represent the 'new normal‘. No where is this more

evident than Japan

Exercising restraint and savvy shopping represent the 'new normal‘. No where is this more

evident than Japan

Grooming for less In summary

Beauty consumers globally are price‐led, but also value‐driven. Making trade‐offs and brand switching is necessary to save

Beauty consumers globally are price‐led, but also value‐driven. Making trade‐offs and brand switching is necessary to save

22

PREVIOUS SECTION BACK TO INDEX NEXT SECTION

3. GROOMING FOR THE PLANET

23

Widespread environmental and social concerns drive the sustainability/ethics agenda

Skeptics are outnumbered by those buying into the supporting science

More people are showing a desire to reduce their environmental impact

Grooming for the planet

Datamonitor Consumer Surveys, 2011

Disagree

49%Agree 23%

The scientific and academic community exaggerates the importance of environmental issues

77%deem protecting the environment to be important

55%

63%

of consumers say environmental/ ethical considerations are

important’ in deciding which products or

services are purchased

say a fair trade/socially responsible claim would exert a more favorable perception of a grocery

product

24

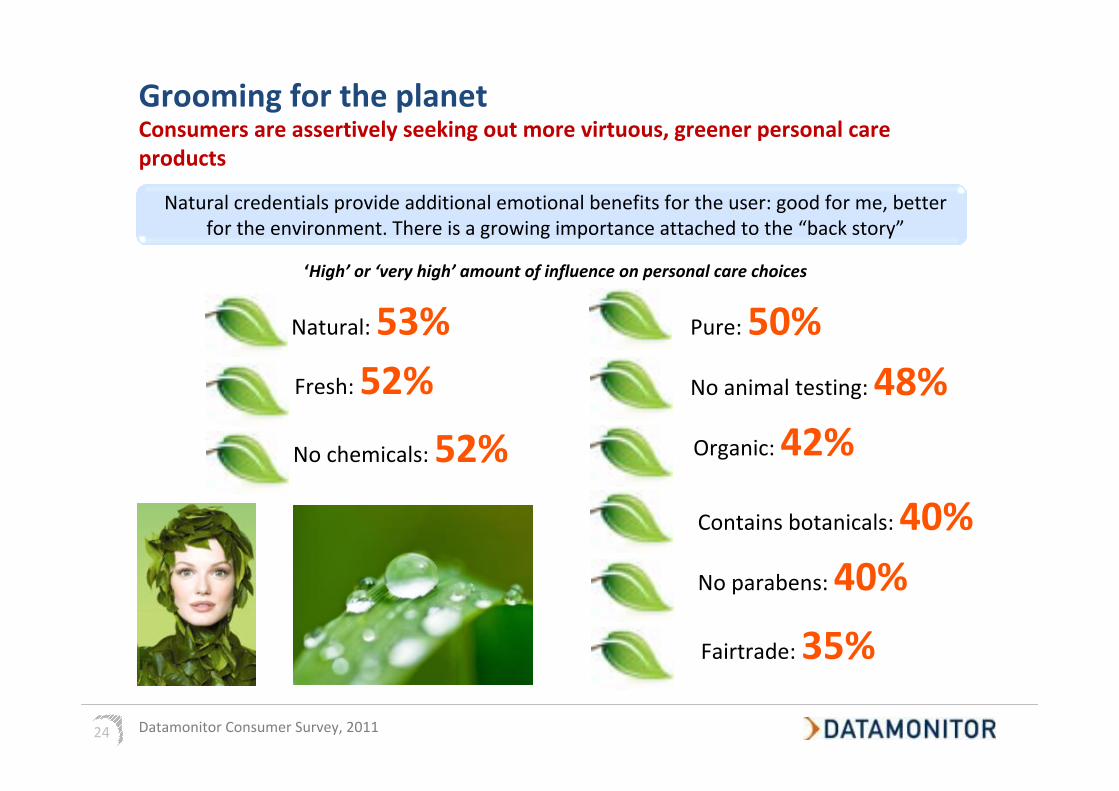

Consumers are assertively seeking out more virtuous, greener personal care products

Grooming for the planet

Datamonitor Consumer Survey, 2011

Natural: 53%Fresh: 52%

No chemicals: 52%

Pure: 50%No animal testing: 48%Organic: 42%

Contains botanicals: 40%No parabens: 40%

Fairtrade: 35%

Natural credentials provide additional emotional benefits for the user: good for me, better for the environment. There is a growing importance attached to the “back story”

‘High’ or ‘very high’ amount of influence on personal care choices

25

Luxury is increasingly about being 'ethically virtuous' and 'personally pleasurable'

Ethicality enhances the ‘permissibility’ of premium/luxury purchases

But there is not an overwhelming willingness to pay for ethical benefits

Grooming for the planet

Datamonitor Consumer Survey, 2011

High quality ingredients 72%

Authenticity/genuineness 65%

After‐sales service 65%

Environmentally friendly 58%

Company's social responsibility 53%

Origin 51%

Exclusivity/uniqueness 48%

Long heritage/tradition 47%

Customization/personalization 46%

Famous brand 45%

TOP 10 (from a list of 17) factors cited as being important in a luxury brand Willing to pay extra for: Fairtrade beauty

products

33%

36%

Willing to pay extra for: organic beauty products

…and even then there is likely to be some idealism conveyed in the responses

26

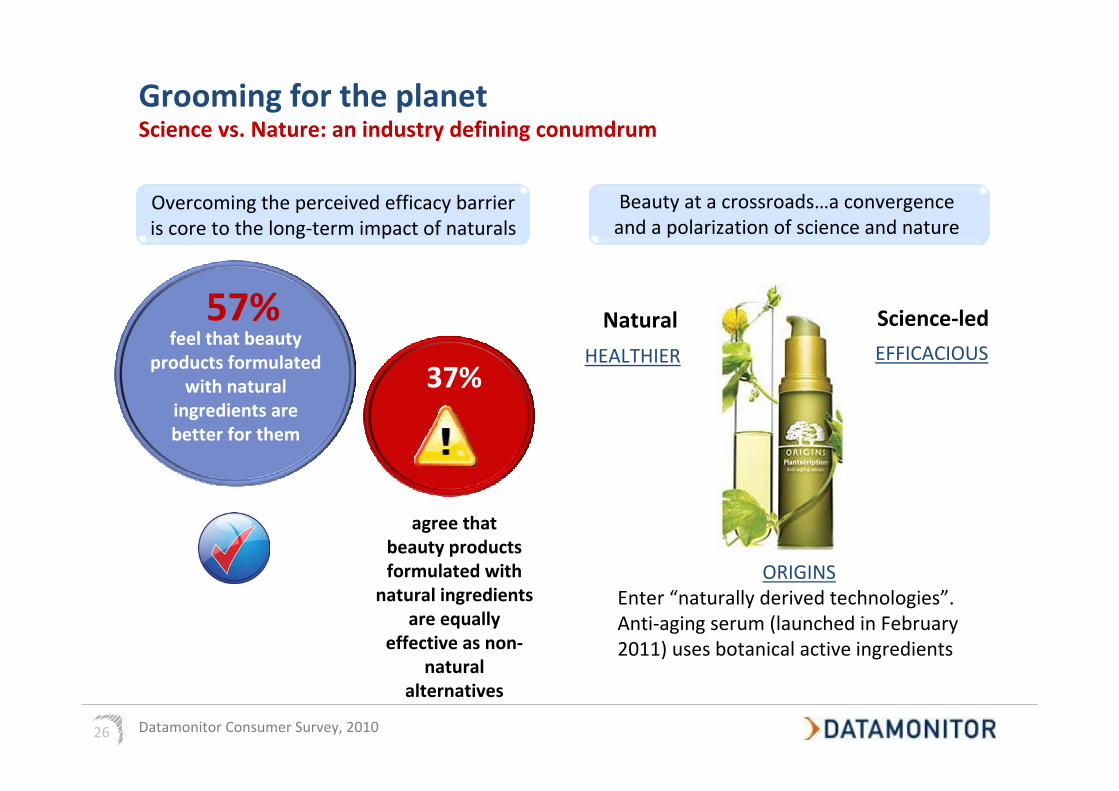

Grooming for the planetScience vs. Nature: an industry defining conumdrum

57%feel that beauty

products formulated with natural

ingredients are better for them

37%

agree that beauty products formulated with

natural ingredients are equally

effective as non‐natural

alternatives

Overcoming the perceived efficacy barrier is core to the long‐term impact of naturals

Natural Science‐led

ORIGINSEnter “naturally derived technologies”. Anti‐aging serum (launched in February 2011) uses botanical active ingredients

HEALTHIER EFFICACIOUS

Beauty at a crossroads…a convergence and a polarization of science and nature

Datamonitor Consumer Survey, 2010

27

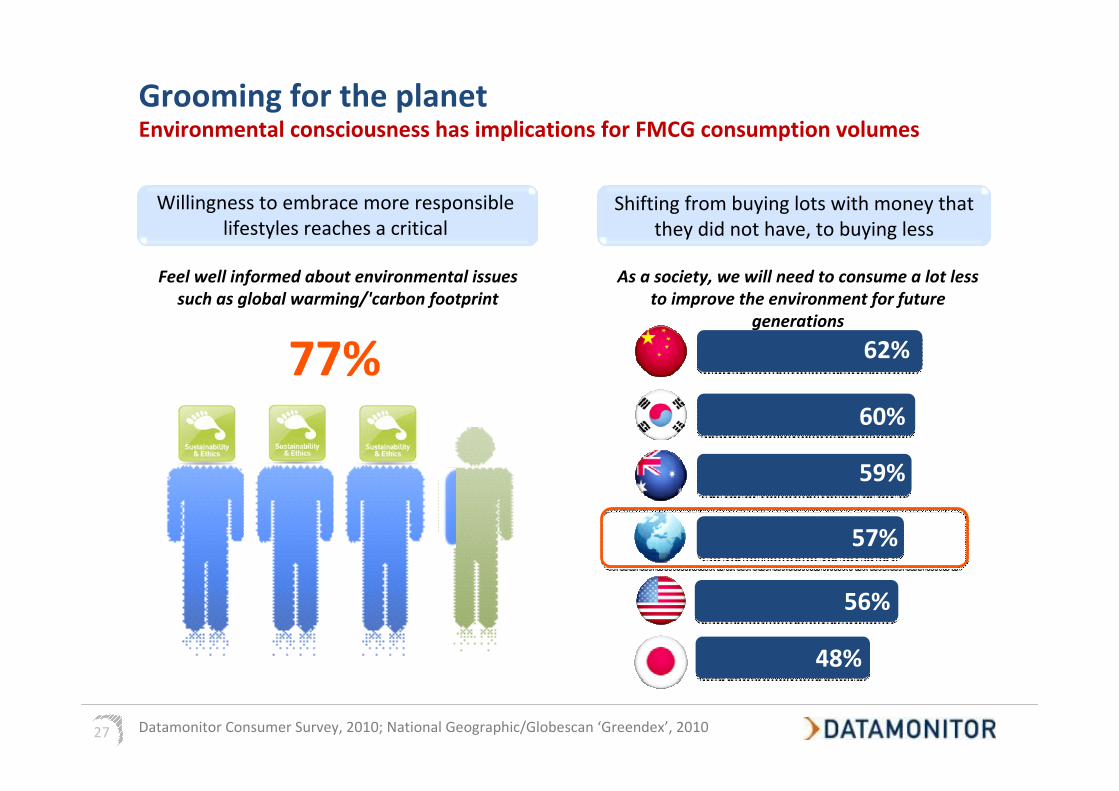

Grooming for the planetEnvironmental consciousness has implications for FMCG consumption volumes

Shifting from buying lots with money that they did not have, to buying less

As a society, we will need to consume a lot less to improve the environment for future

generations

62%

60%

59%

57%

56%

48%

77%

Feel well informed about environmental issues such as global warming/'carbon footprint

Willingness to embrace more responsible lifestyles reaches a critical

Datamonitor Consumer Survey, 2010; National Geographic/Globescan ‘Greendex’, 2010

28

Grooming for the planetSustainable packaging is going to exert more influence on your categories of interest

Sustainability is emerging as an industry defining issue for packagers and their customers

Packaging is inherently

environmentally harming

Sustainability emphasis among packagers and

retailers

Escalating consumer concerns: it

influences choices

Governments and legislation changes

are driving industry change

Agreement that the following contain too much packaging

Grocery products

Food and beverages

Beauty products

Household & laundry

Alcoholic drinks

60% 48% 46% 32% 18%Datamonitor Consumer Survey, 2010

29

Grooming for the planet‘On‐trend’ products

Sanex communicates a “win‐win”scenario for LOHAS

A comprehensive solution to personal care packaging waste

Targets new consumers “looking for a healthy choice for their skin that is also kinder to the environment”

Name is synonymous with the consumer and environmental benefits : 0% parabens, artificial ingredients, and biodegradable

Source: Retail World, December 2011

Exclusive partnership with TerraCycle

Garnier packaging is collected and shipped to a TerraCycle facility where it will be reused to build eco‐friendly playgrounds across the US

30

Expect intensifying focus on ethical and sustainable processes rather than just final products

and services

Expect intensifying focus on ethical and sustainable processes rather than just final products

and services

Consumers want to buy natural, but are not spending that way as

they want highly efficacious products at the same time

Consumers want to buy natural, but are not spending that way as

they want highly efficacious products at the same time

Consumers are making it a point to buy brands from companies whose values are similar to their own. It facilitates feeling good

about choices

Consumers are making it a point to buy brands from companies whose values are similar to their own. It facilitates feeling good

about choices

Grooming for the planet In summary

Resource scarcity, climate change and loss of biodiversity are defining societal challenges serving as a wake‐up 'call to

action‘ for consumers

Resource scarcity, climate change and loss of biodiversity are defining societal challenges serving as a wake‐up 'call to

action‘ for consumers

31

PREVIOUS SECTION BACK TO INDEX NEXT SECTION

4. GROOMING FOR RESULTS

32

This is driving the personalization trend, as well as entrenched brand loyalties

Consumers want products that ‘work for me’ and are in line with their values

The focus on efficacy has an impact on brand loyalty

Grooming for results

Datamonitor Consumer Survey, 2010, 2011

65%Promise lives up to the claimed benefits:

Concerned by the following factors relating to beauty products and appearance

60%Formulated specifically to match needs:

57%Knowing the ingredients used:

55%Tested on animals:

Parabens/petrochemicals used: 51%

Would rather stick with a health & beauty brand that I know works for me, than try out a new one

33

Consumers all too often see new products as additional noise

Is it any wonder that successful innovations are the exception?

Putting it into perspective in the context of the full responses

Grooming for results

Datamonitor Consumer Survey, 2011

Product type %

Suncare 54%

Make‐up/cosmetics 51%

Oral hygiene 44%

Facial skin creams 49%

Shampoo/conditioner 41%

Bath & shower gels 43%

Deodorants 45%

Fragrances 46%

I don't seem to notice new products…

Across personal care products %

I don't seem to notice new products 49%I keep an eye out for new products 42%I actively monitor new products 10%

34

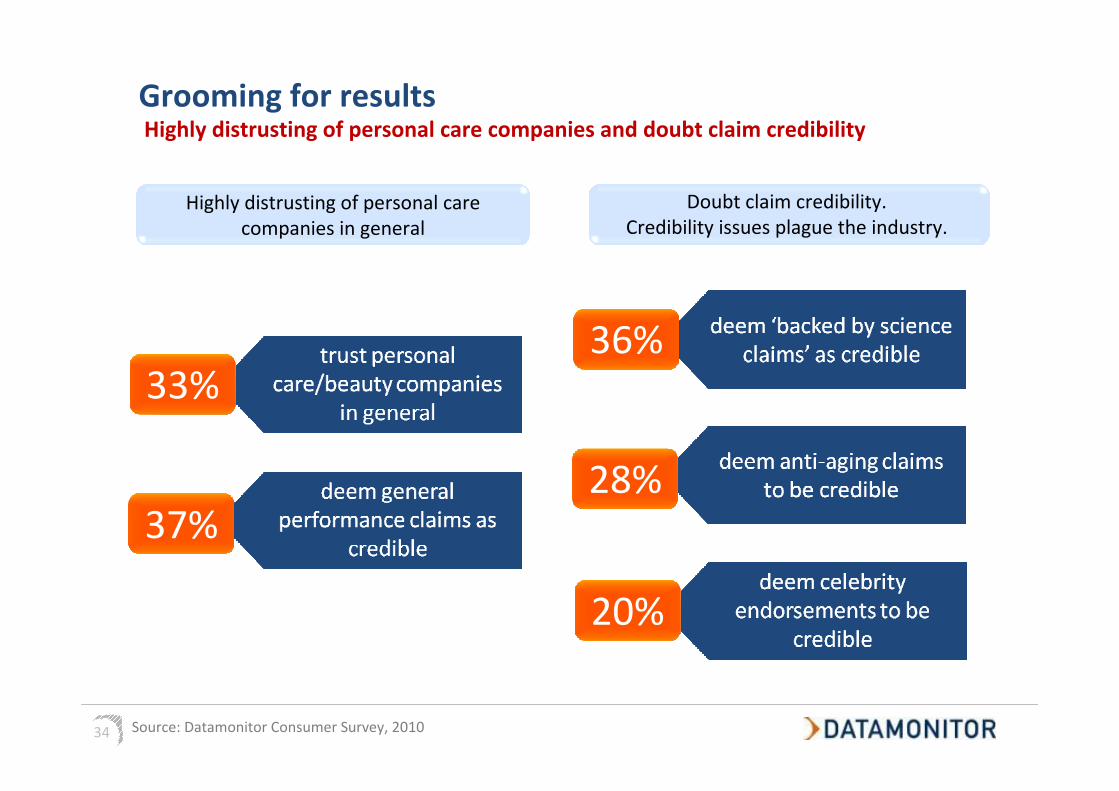

Highly distrusting of personal care companies and doubt claim credibility

Highly distrusting of personal care companies in general

Doubt claim credibility. Credibility issues plague the industry.

Grooming for results

Source: Datamonitor Consumer Survey, 2010

33%

37%

36%

28%

20%

35

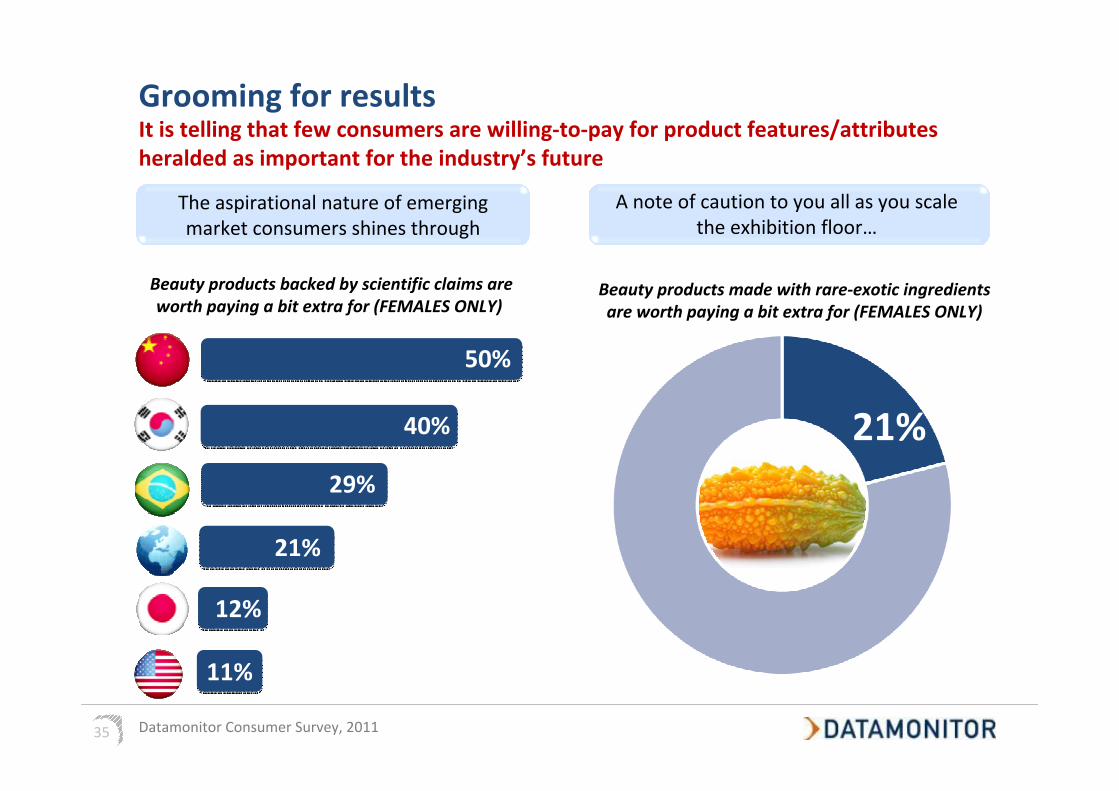

It is telling that few consumers are willing‐to‐pay for product features/attributes heralded as important for the industry’s future

The aspirational nature of emerging market consumers shines through

A note of caution to you all as you scale the exhibition floor…

Grooming for results

Datamonitor Consumer Survey, 2011

Beauty products backed by scientific claims are worth paying a bit extra for (FEMALES ONLY)

Beauty products made with rare‐exotic ingredients are worth paying a bit extra for (FEMALES ONLY)

21%

29%

40%

50%

11%

12%

21%

36

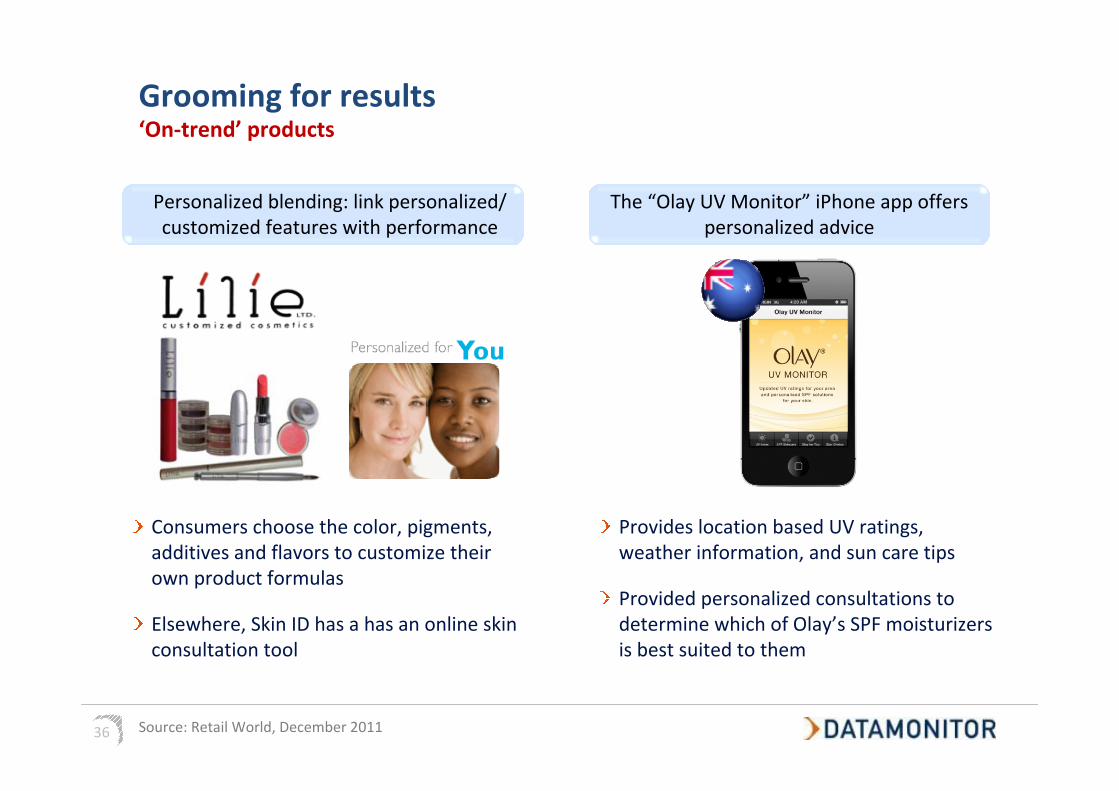

Grooming for results‘On‐trend’ products

Personalized blending: link personalized/ customized features with performance

The “Olay UV Monitor” iPhone app offers personalized advice

Consumers choose the color, pigments, additives and flavors to customize their own product formulas

Elsewhere, Skin ID has a has an online skin consultation tool

Source: Retail World, December 2011

Provides location based UV ratings, weather information, and sun care tips

Provided personalized consultations to determine which of Olay’s SPF moisturizers is best suited to them

37

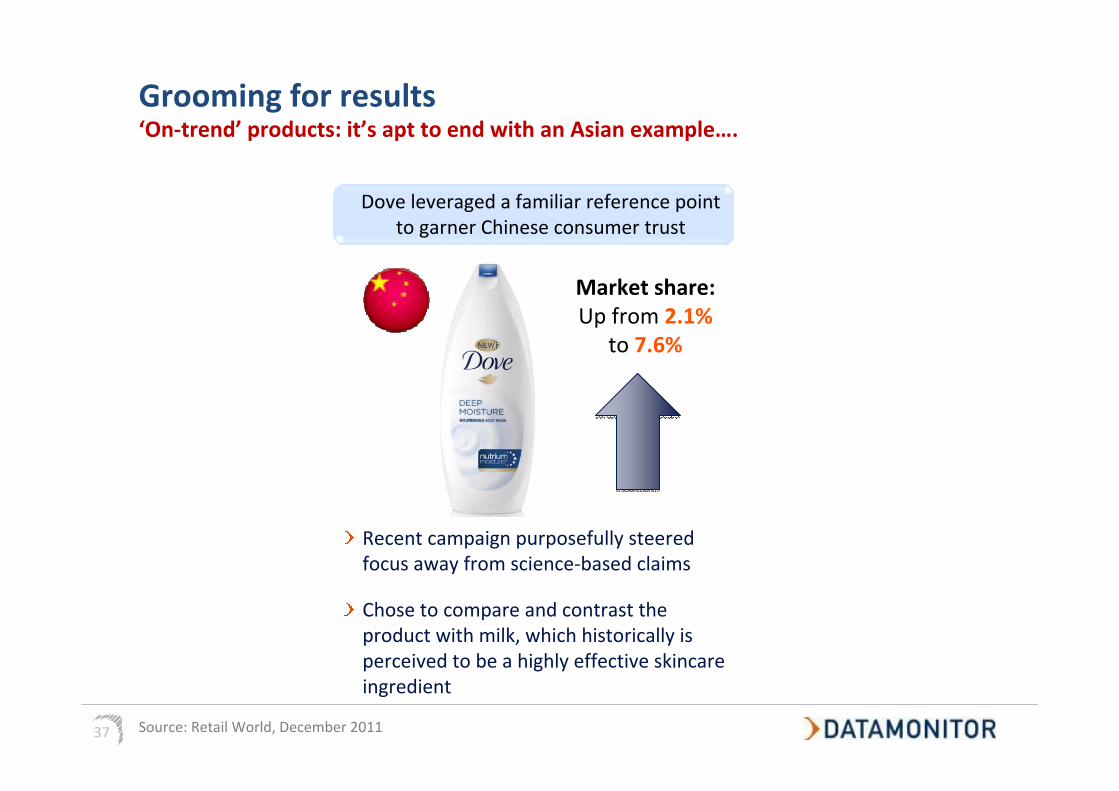

Grooming for results‘On‐trend’ products: it’s apt to end with an Asian example….

Dove leveraged a familiar reference point to garner Chinese consumer trust

Recent campaign purposefully steered focus away from science‐based claims

Chose to compare and contrast the product with milk, which historically is perceived to be a highly effective skincare ingredient

Source: Retail World, December 2011

Market share: Up from 2.1%

to 7.6%

38

Launching ‘meaningful innovations’ is an important innovation imperative (rather

than launching a lot of products)

Launching ‘meaningful innovations’ is an important innovation imperative (rather

than launching a lot of products)

Lack of trust = lapsed users, lost occasions, lost revenues

Lack of trust = lapsed users, lost occasions, lost revenues

A legacy impact: because the industry has been over‐

promising, the (legitimate) claims made by brands fail to resonate. Contrast to other industries

A legacy impact: because the industry has been over‐

promising, the (legitimate) claims made by brands fail to resonate. Contrast to other industries

Grooming for results In summary

Beauty consumers are somewhat anchored by brands that work for them. Switching is even riskier in uncertain times

Beauty consumers are somewhat anchored by brands that work for them. Switching is even riskier in uncertain times

39

Thank You

Contact detailsQueries regarding this presentation should be addressed to:

Contact: Daniel Bone

Email: [email protected]

40

Date/Time: 14 Dec 201111:45‐12:30

Location:Marketing Trends Theatre

Mr Daniel Bone, Consumer Insights Director, Datamonitor

Seminar DetailsBeauty brands are competing in an ‘Era of Consequences’. A more careful consideration of the risks and consequences associated with consumption characterizes buying behavior. The industry must cater towards a more assured, claim savvy and ultimately demanding shopper who expresses more acute, need‐specific beauty demands. Personal values are also being more forcefully expressed through their product preferences. This creates opportunities for premiumization and more progressive product and marketing innovation.In this presentation, Daniel will reveal some key findings from some of Datamonitor’s most recent proprietary consumer research, including insight into the claims that hold greatest resonance with today’s health and beauty shoppers across 20 countries. It will also explore a basic fundamental outlook driving personal care demand: to what extent do consumers actually care about looking good on a day‐to‐day basis?

41

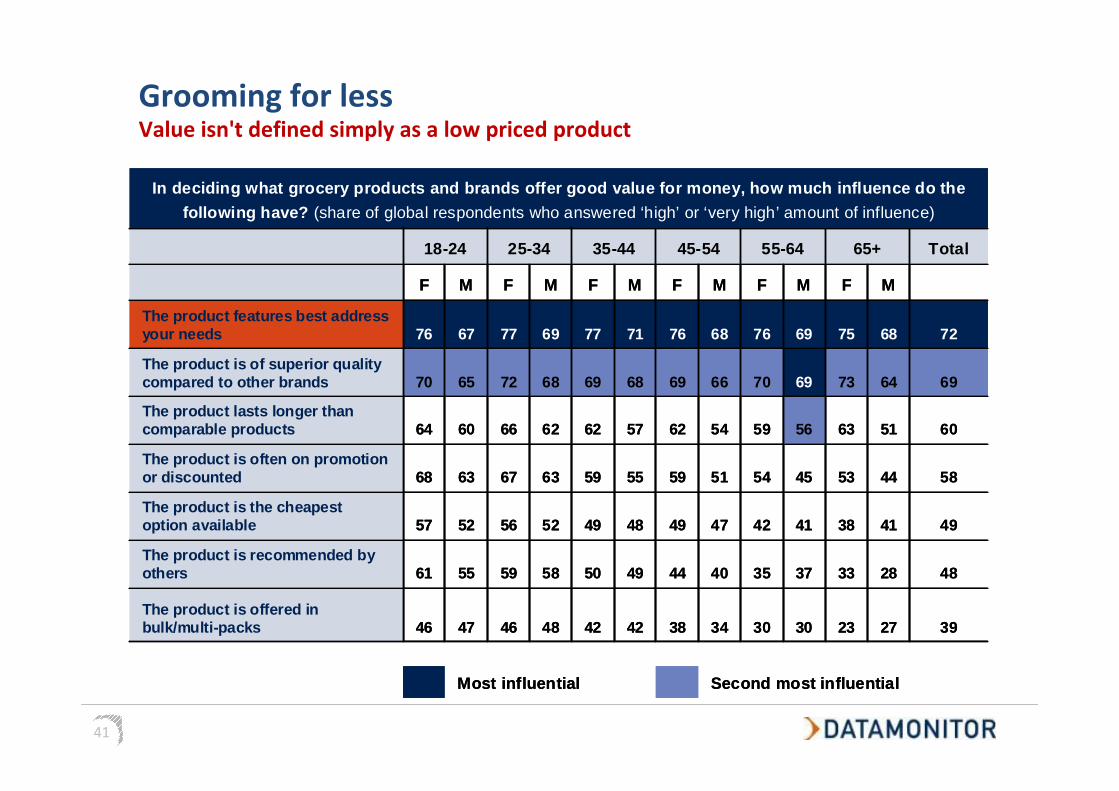

Grooming for lessValue isn't defined simply as a low priced product

In deciding what grocery products and brands offer good value for money, how much influence do the following have? (share of global respondents who answered ‘high’ or ‘very high’ amount of influence)

18-24 25-34 35-44 45-54 55-64 65+ Total

F M F M F M F M F M F M

The product features best address your needs 76 67 77 69 77 71 76 68 76 69 75 68 72

The product is of superior quality compared to other brands 70 65 72 68 69 68 69 66 70 69 73 64 69

The product lasts longer than comparable products 64 60 66 62 62 57 62 54 59 56 63 51 60

The product is often on promotion or discounted 68 63 67 63 59 55 59 51 54 45 53 44 58

The product is the cheapest option available 57 52 56 52 49 48 49 47 42 41 38 41 49

The product is recommended by others 61 55 59 58 50 49 44 40 35 37 33 28 48

The product is offered in bulk/multi-packs 46 47 46 48 42 42 38 34 30 30 23 27 39

Most influential Second most influential

In deciding what grocery products and brands offer good value for money, how much influence do the following have? (share of global respondents who answered ‘high’ or ‘very high’ amount of influence)

18-24 25-34 35-44 45-54 55-64 65+ Total

F M F M F M F M F M F M

The product features best address your needs 76 67 77 69 77 71 76 68 76 69 75 68 72

The product is of superior quality compared to other brands 70 65 72 68 69 68 69 66 70 69 73 64 69

The product lasts longer than comparable products 64 60 66 62 62 57 62 54 59 56 63 51 60

The product is often on promotion or discounted 68 63 67 63 59 55 59 51 54 45 53 44 58

The product is the cheapest option available 57 52 56 52 49 48 49 47 42 41 38 41 49

The product is recommended by others 61 55 59 58 50 49 44 40 35 37 33 28 48

The product is offered in bulk/multi-packs 46 47 46 48 42 42 38 34 30 30 23 27 39

Most influential Second most influential

Top Related