Languages

Pages

Legal

GHANA ECOBANK DCA GUARANTEE

EVALUATION

GHANA ECOBANK DCA GUARANTEE

EVALUATION

MARCH 25, 2008

This publication was produced for review by the United States Agency for International Development. It was

prepared by SEGURA/IP3 Partners LLC under SEGIR Global Business, Trade and Investment II – IQC Indefinite

Quantity Contract, Number EEM-I-00-07-00001-00 Task Order # 04, Development Credit Authority Evaluation.

DISCLAIMER The views expressed in this publication do not necessarily reflect the views of the United States Agency for

International Development or the United States Government.

On the Cover: Street vendors in Accra, Ghana. Photo by SEGURA IP3 Partners LLC.

Ghana EcoBank DCA Guarantee Evaluation ii

TABLE OF CONTENTS

TABLE OF FIGURES ................................................................................................................................. iii

TABLE OF TABLES ................................................................................................................................... iii

ACKNOWLEDGEMENTS ......................................................................................................................... iv

ACRONYMS ................................................................................................................................................ v

I. EXECUTIVE SUMMARY ......................................................................................................................... 1 EVALUATION OBJECTIVES ........................................................................................................................ 2 EVALUATION METHODOLOGY ............................................................................................................... 2 KEY FINDINGS AND CONCLUSIONS ....................................................................................................... 2

II. INTRODUCTION ................................................................................................................................... 5

III. THE DEVELOPMENT PROBLEM AND USAID’S RESPONSE ........................................................ 9 PROBLEM STATEMENT .............................................................................................................................. 9 USAID’S INTERVENTION IN RESPONSE .................................................................................................... 9

IV. PURPOSE OF THE EVALUATION ................................................................................................... 11

V. METHODOLOGY AND INDICATORS ............................................................................................. 12 DATA LIMITATIONS ................................................................................................................................ 13

VI. EXOGENOUS INFLUENCES ON GUARANTEE PERFORMANCE .............................................. 14

VII. FINDINGS AND CONCLUSIONS ................................................................................................... 15 OUTPUT LEVEL FINDINGS AND CONCLUSIONS ................................................................................... 15

FINDINGS AND CONCLUSIONS FOR QUESTION 1 ........................................................................... 15 FINDINGS AND CONCLUSIONS FOR QUESTION 2 ........................................................................... 17 FINDINGS AND CONCLUSIONS FOR QUESTION 3 ........................................................................... 17

OUTCOME LEVEL FINDINGS AND CONCLUSIONS ............................................................................... 21 FINDINGS AND CONCLUSIONS FOR QUESTION 4 ........................................................................... 21 FINDINGS AND CONCLUSIONS FOR QUESTION 5 ........................................................................... 24

IMPACT LEVEL FINDINGS AND CONCLUSIONS .................................................................................... 25 FINDINGS AND CONCLUSIONS FOR QUESTION 6 ........................................................................... 25 FINDINGS AND CONCLUSIONS FOR QUESTION 7 ........................................................................... 28

VIII. SUMMARY OF CONCLUSIONS ..................................................................................................... 29 OUTPUT CONCLUSIONS ....................................................................................................................... 29 OUTCOME CONCLUSIONS .................................................................................................................... 29 IMPACT CONCLUSIONS ......................................................................................................................... 29

BIBLIOGRAPHY ....................................................................................................................................... 30

ANNEXES .................................................................................................................................................. 31 Annex A - Evaluation Framework and Interview Guides ............................................................................... 31

GHANA ECOBANK DCA EVALUATION FRAMEWORK ...................................................................... 32 EcoBank Interview Guide....................................................................................................................... 37 Banking Associations Interview Guide .................................................................................................... 40 Donors Interview Guide ........................................................................................................................ 42 Industry Associations Interview Guide .................................................................................................... 43 TA Providers Interview Guide ............................................................................................................... 44 USAID/Ghana Interview Guide .............................................................................................................. 45 MFI Interview Guide .............................................................................................................................. 48 Bank of Ghana (Central Bank) Interview Guide ....................................................................................... 50

Annex B – Contact List.............................................................................................................................. 51

Ghana EcoBank DCA Guarantee Evaluation iii

TABLE OF FIGURES

FIGURE 1: LENDING TO PRIVATE SECTOR AS PERCENT OF GDP .................................................................................. 1

FIGURE 2: GROWTH IN ECOBANK LENDING, 2002-2008 ................................................................................................... 3

FIGURE 3: BANK LENDING RATES 2000-2007 ........................................................................................................................... 7

FIGURE 4: GROWTH IN ECOBANK'S LOAN PORTFOLIO BY VOLUME, 2002-2008 ................................................ 22

FIGURE 5: GROWTH IN ECOBANK'S LOAN PORTFOLIO BY VALUE, 2002-2008 ..................................................... 22

FIGURE 6: DEPOSIT MONEY BANKS CREDIT TO PRIVATE SECTOR AS PERCENT OF REAL GDP .................... 26

FIGURE 7: GROWTH IN CREDIT FROM MICROFINANCE INSTITUTIONS, 2001-2006 ........................................... 27

TABLE OF TABLES

TABLE 1: CHARACTERISTICS OF DCA LOAN GUARANTEES IN GHANA .................................................................... 1

TABLE 2: SUMMARY OF DCA GUARANTEES .......................................................................................................................... 10

TABLE 3: SUMMARY OF LOAN GUARANTEES IN GHANA ............................................................................................... 11

TABLE 4: ECOBANK EXPERIENCE WITH BORROWERS/INDUSTRIES RECEIVING GUARANTEED LOANS ... 16

TABLE 5: DISTRIBUTION OF ECOBANK'S SME LOANS BY SIZE ...................................................................................... 18

TABLE 6: ANTICIPATED VERSUS ACTUAL LOAN CHARACTERISTICS ........................................................................ 19

TABLE 7: LOAN SUMMARY BY INDUSTRY ............................................................................................................................... 20

TABLE 8: CHANGE IN ECOBANK'S LENDING BEHAVIOR SINCE THE GUARANTEES ........................................... 23

Ghana EcoBank DCA Guarantee Evaluation iv

ACKNOWLEDGEMENTS

Many people contributed to the evaluation. Perhaps most important are the many people who generously shared

their time and knowledge with the evaluation team. In this regard, Joana Mensah, Paul Acquah, Gordon Nyamekye-

Pratt, and Abdulai Abdul-Rahman of EcoBank deserve particular thanks for the many hours they spent helping the

evaluation team understand EcoBank’s use of the guarantees and the general lending environment in Ghana. The

team also thanks EcoBank in general for its outstanding cooperation in providing data and resources to support the

evaluation. The evaluation team also interviewed many other people in the course of the evaluation and wishes to

thank them as well for sharing their time and knowledge.

The USAID/Ghana Mission Director, Robert Hellyer, and Brian Dusza, the Director of the Economic Growth

Office also deserve thanks for their support and contribution to the evaluation.

Finally, a sincere thank you to Noshie Iddisah for her invaluable assistance in Ghana.

Ghana EcoBank DCA Guarantee Evaluation v

ACRONYMS

AGI Association of Ghana Industries

BoG Bank of Ghana

CMS Credit Management System

DCA Development Credit Authority

DMB Deposit Money Bank

EGAT/DC Bureau of Economic Growth Agriculture and Trade/Office of Development Credit

GHAMFIN Ghana Microfinance Institutions Network

GDP Gross Domestic Product

GoG Government of Ghana

IFC International Finance Corporation

IMF International Monetary Fund

MCC Millennium Challenge Corporation

MFI Microfinance institution

MPC Monetary Policy Committee

MSED Micro and Small Enterprise Development Program

MSME Micro-, small-, and medium-sized enterprises

NGO Non-Governmental Organization

NTE Non-traditional exports

SME Small- and medium-sized enterprise

TA Technical Assistance

TIPCEE Trade and Investment Program for a Competitive Export Economy

USAID United States Agency for International Development

WB World Bank

I. EXECUTIVE SUMMARY

Macroeconomic conditions in Ghana in the early 2000s severely constrained private sector access to credit

(International Monetary Fund 2003). High levels of government borrowing pushed interest rates up and crowded

the private sector out of financial markets. With government bills paying real interest of 16.8 percent, banks had

little incentive to take on riskier private sector debt. High interest rates and exchange rate volatility also created

financial uncertainty that made both borrowers and lenders hesitant to take on the risks associated with loans,

particularly medium to long-term loans.

Limited access to credit and its high cost significantly constrained the growth of Ghanaian enterprises. These

constraints hit micro-, small-, and medium-enterprises (MSMEs) particularly hard because of a number of factors

that made it difficult for banks to assess the

risk associated with loans to MSMEs. This

situation was of particular concern to

USAID/Ghana because its current

Economic Growth strategy relied on

growth in the MSME sector.

The International Monetary Fund

(International Monetary Fund 2003) credits

monetary policy and financial sector

reforms since 2001 for substantially

increased banks’ lending to the private

sector (Figure 1). Several studies and

reports, however, found that access to

credit, high interest rates, and prohibitive

collateral requirements, remain significant

constraints to the growth of many MSMEs (Association of Ghana Industries 2007; (Mensah 2004). Access to the

medium to long-term financing necessary for capital investments is particularly tight (Mensah 2004).

In response to this environment USAID/Ghana implemented two Development Credit Authority (DCA) loan

guarantees with EcoBank, a prominent retail bank in Ghana. Under the guarantees USAID/Ghana agreed to cover

50 percent of EcoBank’s losses of principle on guaranteed loans up to a specified ceiling on total loan value. The

guarantees reduce the bank’s risk and thereby encourage it to make loans to specific sectors that support

USAID/Ghana’s development objectives. USAID/Ghana structured the two DCA guarantees to support its

Economic Growth strategy and specified MSMEs, microfinance institutions (MFIs), and NGOs with activities in

manufacturing, agriculture, agricultural processing, salt mining/production, fisheries, tourism, wood products,

textiles and garments, and other potential growth industry sectors as qualified recipients of guaranteed loans. The

guarantees’ Action Packages also emphasized a particular desire to improve access to larger, medium to long-term

loans for these sectors. Table 1 summarizes key characteristics of the two guarantees.

TABLE 1: CHARACTERISTICS OF DCA LOAN GUARANTEES IN GHANA

Starting year

Ending year

Guarantee ceiling ($)

Number of loans

Aggregate amount ($)

Utilization rate

Median loan Size ($)

Average tenor

(months)

2003 2008 $3,000,000 6 $2,208,830 73.63% $359,395 40

2005 2012 $7,000,000 4 $4,446,664 63.52% $1,203,503 27

Source: USAID Credit Management System (CMS) and EcoBank.

0%

5%

10%

15%

20%

25%

30%

2000 2001 2002 2003 2004 2005 2006 2007 2008

Pe

rce

nt

of

rea

l G

DP

Banks

MFIs

Total

Source: Bank of Ghana & Ghana Microfinance Institutions Network (GHAMFIN)

FIGURE 1: LENDING TO PRIVATE SECTOR AS PERCENT OF GDP

Ghana EcoBank DCA Guarantee Evaluation 2

EVALUATION OBJECTIVES

USAID’s Economic Growth Agriculture and Trade Bureau’s Office of Development Credit (EGAT/DC), which

manages the DCA guarantees, commissioned this evaluation of USAID/Ghana’s DCA guarantees. This evaluation

assesses the performance of the DCA guarantees relative to their objectives as defined in the Action Packages.

Action Packages are internal USAID memos that describe the rational for the guarantees and their objectives. In

this case USAID/Ghana developed the Action Packages and

described the guarantees’ objectives as increasing access to

credit, and particularly medium to long-term credit, for firms in

key growth-oriented sectors. Three broad avenues of

questioning – output, outcome, and impact (see box below) –

guided the evaluation. The evaluation framework and interview

guides in Annex A contain the actual evaluation questions.

The scope of the evaluation covers only EcoBank’s behavior and

potential demonstration effects in the broader banking sector. It

does not examine EGAT/DC’s management of the guarantees

nor does it attempt to assess the impacts of the loans on

borrowers or on USAID/Ghana’s strategic objectives. At

EGAT/DC’s request, the evaluation presents only findings and conclusions. It does not extend to making

recommendations or to drawing out lessons learned.

EVALUATION METHODOLOGY

A three-person team conducted the evaluation in February and March of 2009. The team met initially in

Washington, D.C. to refine evaluation objectives and procedures, develop an evaluation framework, and to

interview EGAT/DC personnel. Field work commenced in Accra, Ghana on February 16, 2009 and concluded on

February 27. During that time the team reviewed documents, conducted structured interviews with stakeholders,

and collected secondary quantitative data.

KEY FINDINGS AND CONCLUSIONS

At the output level, the DCA guarantees complemented EcoBank’s ongoing strategy to transition from a

wholesale bank to a fully fledged retail bank with a correspondingly greater focus on the SME sector. The bank

used the guarantees to gain experience with new borrowers and industries and, in compliance with USAID/Ghana

objectives, to provide larger and longer-term loans associated with financing capital expenditures. Guaranteed

loans were much larger, and consequently far fewer in number, than initially anticipated by USAID/Ghana but still

fell within the size and tenor parameters established in the guarantee agreements.

Specific findings in support of these conclusions include:

EcoBank used the guarantees to test new borrowers. Of the nine unique borrowers (there were ten loans but

two were to the same borrower) under the DCA guarantees, six (66 percent) were new clients.

The bank also used the guarantees to gain experience with new sectors/industries. Three of the eight

sectors/industries represented by loan recipients were sectors/industries in which EcoBank had no previous

lending experience.

EcoBank also focused its use of the guarantees on larger loans with longer tenors necessary for capital

investments – a particular objective of the DCA agreements. Guaranteed loans were significantly larger and

had longer tenors than EcoBank’s typical SME loan. All of the guaranteed loans fell within the top eight percent

(by size) of loans in the bank’s SME portfolio and 60 percent fell within the top two percent. The guaranteed

Evaluation Questions

Output level – Did EcoBank’s use the guarantees

conform to guarantee objectives and specifications as

described in the Guarantee Agreements?

Outcome level – Did EcoBank’s experience with the

guarantees improve access to credit for borrowers in

the target sectors outside of the DCA coverage?

Impact level – Did the guarantees have a

demonstration effect that resulted in other banks

improving access to credit for borrowers in the target

sectors?

Ghana EcoBank DCA Guarantee Evaluation 3

loans had an average tenor of 35 months compared to an average 12 month tenor for the bank’s overall SME

portfolio.

All nine of the unique borrowers under the DCA guarantees received medium to long-term loans, eight to

finance capital expenditures and one, an MFI, for on-lending to micro-enterprises. None had received medium

to long-term loans prior to the guarantee.

In spite of the relatively large loan sizes, loan recipients likely fall within target sectors, i.e., they appear to be

largely medium-sized enterprises and MFIs. The World Bank’s International Finance Corporation (IFC) uses

loan sizes of $10,000 to $100,000 as a proxy for small enterprises and loans between $100,000 and $1 million

as a proxy for medium enterprises (IFC undated).

At the outcome level EcoBank has substantially increased lending to SMEs and MFIs since it began utilizing the

DCA guarantees. EcoBank officials admitted, however, that the growth in SME lending largely reflects the bank’s

ongoing strategy to increase retail lending rather than being attributable to the guarantees. Experience with the

guarantees prompted EcoBank to increase lending to some new industries and to extend some long-term loans for

capital expenditures outside of the guarantee coverage. However, these increases were small relative to the bank’s

overall SME portfolio.

Key findings in support of these conclusions

include:

EcoBank has substantially increased its lending

to SMEs. Figure 2 illustrates the growth in

EcoBank’s lending between 2002 (pre-DCA

guarantee) and 2008. The bank increased the

number of loans in its SME portfolio by 380

percent (from 194 to 932) and the value of

the portfolio by 500 percent (from $11.9

million to $72.0 million). The number of loans

in the bank’s entire loan portfolio grew faster

(1944 percent from 461 to 9,422 loans) than

its SME portfolio but the value of overall

portfolio grew more slowly (353 percent

from $93.2 million to $422.0 million) than the

SME portfolio.

EcoBank used the guarantees to develop new clients and markets. The bank has continued to lend outside of

the guarantees to seven of the eight industries/sectors represented by recipients of guaranteed loans. It has

also extended loan tenors for borrowers in these industries as it focuses on financing capital expenditures.

The DCA guarantees contributed to changes in EcoBank’s lending behavior. EcoBank personnel stated that

the bank’s experience with the DCA guarantees was crucial to the bank increasing the number of larger, long-

term loans for capital expenditures in recent years. EcoBank has increased lending to MFIs outside of the

guarantees and is now extending medium to long-term credit to MFIs.

The DCA guarantees prompted EcoBank to expand lending into new sectors/industries. Bank personnel said

that the ability to test new industries/sectors within the guarantee was critical to the bank’s lending in these

industries/sectors outside of the guarantee coverage but said that the guarantees made, at most, a minor

contribution to the growth in EcoBank’s SME portfolio. Guaranteed loans accounted for only one percent of

the number and nine percent of the value of all SME loans in 2008.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2002 2003 2004 2005 2006 2007 2008

Nu

mb

er

of

loa

ns

Po

rtfo

lio

va

lue

(m

illi

on

s $

)

Entire portfolio value SME portfolio value

Entire portfolio numbers SME portfolio numbers

FIGURE 2: GROWTH IN ECOBANK LENDING, 2002-2008

Ghana EcoBank DCA Guarantee Evaluation 4

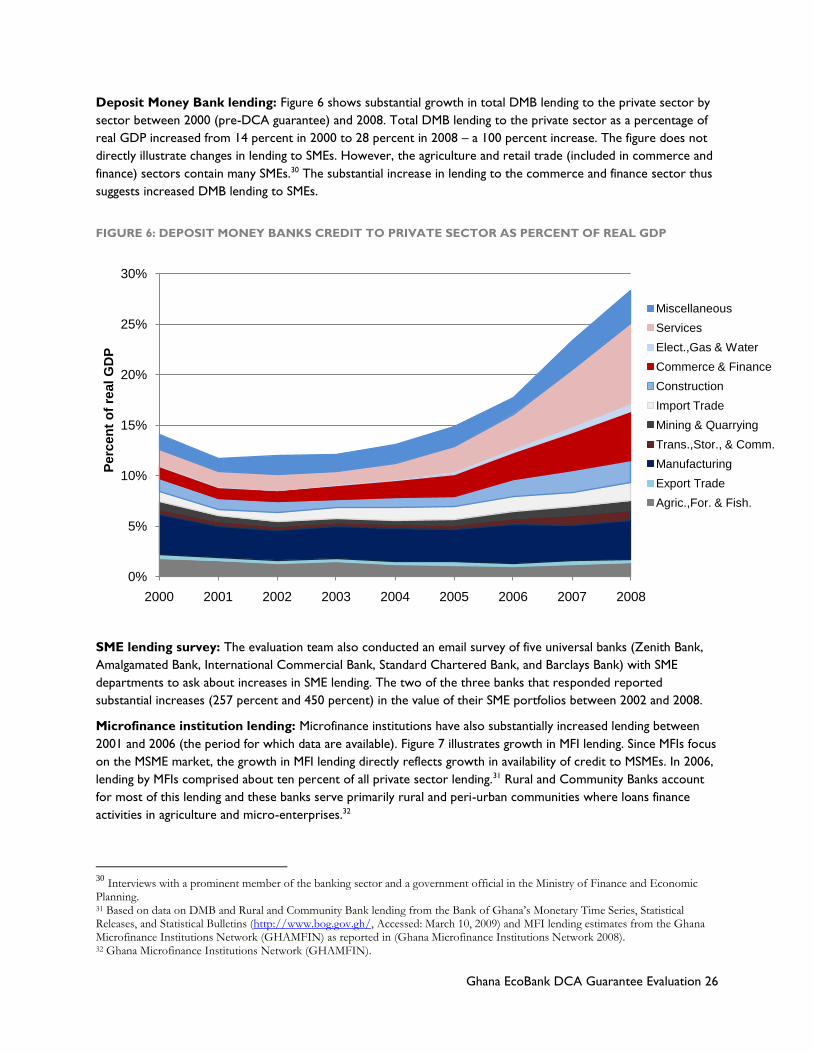

At the impact level, lending to MSMEs (a proxy for the target sectors of the guarantee) has increased

substantially in Ghana since 2002 (pre-guarantee). Anecdotal evidence suggests that loan guarantees may be

responsible for some of this increase. However, given the small number of industries/sectors represented by

EcoBank’s guaranteed loans, the effect of the DCA guarantees is likely modest. Factors external to the guarantees

are likely responsible for most of the observed increase in lending to MSMEs.

Key findings in support of the conclusion of increased financial sector lending to MSMEs include:

Bank lending to the private sector (as a percentage of real GDP to control for inflation and overall growth in

the economy) increased from 14.0 percent to 28.8 percent (a 106 percent increase) between 2000 and 2008.

Lending to the commerce and finance sector, a sector dominated by SMEs according to a banking official and a

government SME specialist, grew substantially more than most other sectors increasing by 300 percent from

1.2 percent to 4.8 percent.

At least three Ghanaian universal banks have established relationships with MFIs to gain access to savings

mobilization and lending in the micro-enterprise sector.

Microfinance institutions (lenders to micro-enterprises) increased lending from 0.3 percent to 1.8 percent of

real GDP between 2002 and 2006, a 500 percent increase.

The Bank of Ghana’s SME Survey in 2005 found that “the share of SMEs in total exposure of banks has

increased from 0.95 percent of GDP in 2001 to 1.54 percent of GDP by 2004.”

Two of the three banks that responded to a survey of five banks with SME departments reported increases in

SME lending of 257 and 450 percent between 2002 and 2008.

Qualitative findings on the potential for EcoBank’s DCA guarantees to influence broader MSME lending include:

Three individuals prominent in the banking and development sectors said they had witnessed banks observing

and learning from other banks’ experience when deciding to enter new industries or sectors.

The three banks that responded to the evaluation team’s survey of five banks that competed with EcoBank in

the SME market said that other banks’ experience in new industries and with different loan sizes and tenors

were either “somewhat” or “very” important in determining the banks’ lending strategy.

Two recipients of guaranteed loans have received long-term financing from other banks since receiving the

guaranteed loans.

Ghana EcoBank DCA Guarantee Evaluation 5

II. INTRODUCTION

The International Monetary Fund (International Monetary Fund 2003) described macro-economic conditions in

Ghana in 2000 that significantly constrained private sector access to credit. High levels of government debt (117

percent of GDP in 2000, a quarter of which was incurred in 19991) crowded the private sector out of financial

markets. With government treasuries paying nominal interest rates of 42.0 percent (16.8 percent real), banks had

little incentive to take on riskier private sector debt. High rates of inflation (25.2 percent in 2000) and exchange

rate volatility increased financial uncertainty and discouraged both borrowers and lenders from taking on the risks

associated with loans, particularly medium to long-term loans. Weak competition in the banking industry

exacerbated the problem as banks faced little competitive pressure to seek new markets or improve access to

credit.

In addition to macro-economic conditions that discouraged lending, banks viewed business lending, and particularly

lending to MSMEs to be particularly risky.2 Many businesses lacked the accounting and management capacity to

demonstrate their ability to service a loan, land tenure issues limited businesses’ ability to raise the collateral banks

required to allay perceived risk, the legal and court systems made it difficult for banks to seize collateral when

borrowers defaulted, and the absence of credit bureaus made it difficult for banks to assess borrowers’ credit

history. To add to the risk, the International Monetary Fund (International Monetary Fund 2003) concluded that,

because they have focused largely on government debt, banks may have limited expertise in evaluating risks

associated with private sector lending.

Conditions have improved significantly since 2000. Government policy and financial sector reforms focused on

increasing liquidity in the financial sector and strengthening the regulatory underpinnings of the banking system.

Key policies and reforms include:

Reduced government borrowing lowered Treasury bill interest rates, reduced government demands on

the credit system, and created space for private sector lending.

Eliminating the secondary reserve requirement3 freed up capital for lending to the private sector. The

International Monetary Fund’s (IMF) 2003 Financial Sector Assessment (International Monetary Fund

2003) concluded that, “the secondary reserve requirements … are beginning to bind for some of the

larger banks that would like to engage in more lending to the private sector.” The Bank of Ghana reduced

the secondary reserve requirement from 35 percent to 15 percent in July of 2005 and eliminated it

entirely in August of 2006.

Banking Act of 2004 – the act strengthened the regulatory and supervisory functions of the Bank of Ghana

over the banking industry and has strengthened and stabilized the banking sector.

Universal Banking License – In 2003 the Bank of Ghana established the Universal Banking Business License

which has increased competition in the banking sector. Most major banks have now transitioned to

universal banks and the banking sector has expanded. Between 2000 and 2007 the number of deposit

money banks 4 in Ghana increased from 17 in 2000 to 23 in 20075 and 27 in 2009.6 During the same

1 (International Monetary Fund 2003). 2 Reported by every member of the banking industry the evaluation team interviewed. 3 In addition to a nine percent reserve requirement, banks were required in 2003 to hold a secondary reserve of 35 percent, at least 20 percent in treasury bills and 15 percent in inflation-indexed government bonds. 4 Deposit money banks include Commercial Banks, Merchant Banks, Development Banks, and Universal Banks. Since the Banking Law of 2004, most merchant and commercial banks in Ghana have transitioned to universal banks. 5 Bank of Ghana Annual Reports, Online: http://www.bog.gov.gh/index1.php?linkid=157, Accessed: March 10, 2009. 6 Personal communication with Jude Kofi Arthur, President, Ghana Association of Bankers.

Ghana EcoBank DCA Guarantee Evaluation 6

period the number of Rural and Community Banks increased from 113 to 126 (2007), and the number of

non-bank financial institutions7 increased from 37 to 41 (2007).8

Borrowers and Lenders Act (2008) and Non-Bank Financial Institutions Act (2007) – These acts are part

of a comprehensive package aimed at improving financial intermediation. The borrowers and Lenders Act

clarifies the rights and obligations of lenders and borrowers. It improves transparency in lending and

should ultimately increase access to credit. It also reduces the barriers banks face in seizing collateral

when borrowers default on loans (Economist Intelligence Unit 2009).

Credit Reporting Act (2007) – The act provides the foundation for establishing credit bureaus in Ghana –

one of which is now in operation. Widespread adoption of credit bureaus will reduce information

asymmetry between borrowers and lenders and reduce the cost of lending and interest rate spreads.

As a result of these policies and reforms, the Ghanaian banking sector now (2009) has excess liquidity. The entry

of new banks, and especially Nigerian banks after bank consolidation in that country, has increased competition and

banks are actively seeking new markets. In fact, each of the five representatives of the banking and microfinance

sectors, as well as TA contractors and government officials, that the evaluation team interviewed said that the

banking sector had become much more competitive and that banks were moving down market in search of savings

mobilization and lending opportunities. At least three banks - UniBank, EcoBank, and Barclays - have established

formal partnerships with MFIs to gain access to the lower end of the lending market.

A prominent representative of the banking industry believed that actively engaging the SME market would be

critical for banks’ survival. He stated that 70 percent of the cash in Ghana was outside of the banking system and

believed that future growth in lending depended on bringing this cash into the formal banking sector. The ability to

mobilize savings from the non-banked sectors would be key to reducing the cost of funds and remaining

competitive.

Competition does not yet seem to have substantially affected interest rates. While real lending interest rates have

declined since 2002 (linear trend in Figure 3), several studies of interest rate spreads in Ghana attribute the decline

largely to the macroeconomic environment (i.e., reserve requirements, inflation, prime rates), rather than bank

competition (Bawumia, Belnye, and Ofori Martin Enoch 2005; Gockel and Mensah 2006). In fact, Bawumia, et al.

concluded that lack of price competition among banks was the most important factor in explaining persistent large

spreads between banks’ borrowing and lending rates. Officials of the one bank interviewed during the evaluation

stated that they were reluctant to reduce interest rates because it would be difficult to increase them for

subsequent loans. The bank would reduce rates for good customers who asked but would not offer lower rates as

a marketing strategy. All of the individuals the evaluation team interviewed who were cognizant of the financial

sector said that bank competition had not significantly reduced interest rates.

7 Non-bank financial institutions consist of savings and loan companies, finance companies, leasing companies, mortgage finance companies, and discount houses. 8 Bank of Ghana Annual Reports, Online: http://www.bog.gov.gh/index1.php?linkid=157, Accessed: March 10, 2009.

Ghana EcoBank DCA Guarantee Evaluation 7

FIGURE 3: BANK LENDING RATES 2000-2007

Likewise, competition does not appear to have affected loan tenors or collateral requirements. The evaluation

team found no quantitative data on loan tenors or collateral requirements. However, a USAID technical assistance

contractor working in the agricultural sector had observed some reduction in collateral requirements for SME

borrowers in the agricultural sector but did not believe the practice was widespread. EcoBank reported changing

the composition of what it would accept as collateral (allowing up to 50 percent of the collateral requirement in

cash as opposed to all in landed property) but had not changed the total value of collateral required.

Respondents to the 2007 Business Climate Survey conducted by the Association of Ghana Industries ranked access

to credit and cost of credit among the five greatest barriers to growth.9 Another survey of SMEs in Ghana found

that over 50 percent of SMEs surveyed said that access to credit and the high cost of credit adversely affected their

operations (Bank of Ghana 2007). Access to medium to long-term financing necessary for capital investments

remains a particularly acute problem for SMEs (Mensah 2004).

Remaining barriers to credit for SMEs include:

All individuals the evaluation team interviewed in the financial sector stated that banks’ perceived risk

associated with lending to MSMEs was a key constraint to providing credit. This perceptions stems from

the limited capacity of many MSMEs to demonstrate creditworthiness, information asymmetry, and limited

bank experience with MSMEs. It results in higher interest rates, short tenors, and high collateral

requirements.

Limited acceptance and capacity among MSME owners to adhere to the requirements of obtaining credit

(e.g., disclosing accurate financial information, perception that loans are grants, unwillingness to invest in

capacity building) (Mensah 2004).

Difficulties demonstrating free-and-clear ownership of collateral.

9 The Association of Ghana Industries surveyed 451 businesses in the manufacturing, trade, tourism, services, construction, and finance sectors in seven regions of Ghana. Small businesses made up more than 66 percent of the sample. Almost half of respondents (49 percent) ranked the cost of credit among the five greatest barriers to growth and 43 percent said the same of access to credit.

0

10

20

30

40

50

60

2000 2001 2002 2003 2004 2005 2006 2007

Perc

en

t

Nominal lending rate Inflation rate

Real lending rate Linear (Real lending rate)

Ghana EcoBank DCA Guarantee Evaluation 8

Ghanaian banks’ cash for lending consists primarily of short-term savings deposits. Limited access to long-

term funds thus constrains banks’ ability to make medium to long-term loans.10

High bank delivery costs associated with smaller loans.11

The evaluation assessed the extent to which the DCA loan guarantees to the guarantee partner (EcoBank) have

improved access to credit for the target sectors (i.e., MSMEs) in Ghana. In particular, it asked the following

questions.

How did the DCA guarantees fit into EcoBank’s ongoing strategy? What market potential did the DCA

guarantee help open for EcoBank?

How did EcoBank implement its loan guarantee programs (e.g., marketing campaigns, changed terms,

training, revised staff structure and responsibilities, improved communications with branch offices, etc.)?

And why?

Did EcoBank’s use of the DCA guarantees improve access to credit for the target sectors? (i.e., did

characteristics of guaranteed loans differ from other loans in ways that improved access?)

Did EcoBank improve access to credit to the target sectors outside of the DCA guarantees (i.e., did the

bank move into any new sectors/industries, types of borrowers, types of loans, or loan terms)? If so, how

and why and to what extent were the DCA guarantees responsible for improving access to credit outside

of the guarantees?

What factors at EcoBank were responsible for achieving desired outcomes (e.g., TA; bank staff training;

revised bank strategy, procedures and structure; new management, etc.)?

Did other, non-partner banks initiate or increase lending to the target sectors? If so, to what extent was

the DCA guarantee to EcoBank responsible? How and why?

Did access to loans (or loan terms) improve for loans to the target sectors? If so, how and why?

10 Although this was not a formal interview question, two representatives of the banking sector, an SME expert, and representatives of the Bank of Ghana and Ministry of Finance mentioned it as a key constraint to medium to long-term credit. 11 2003 USAID DCA Action Package and (Bawumia, Belnye, and Ofori Martin Enoch 2005).

Ghana EcoBank DCA Guarantee Evaluation 9

III. THE DEVELOPMENT PROBLEM AND USAID’S RESPONSE

In 2003, USAID/Ghana’s Economic Growth strategy emphasized private sector-led growth fueled by increased

non-traditional exports, and especially agricultural exports. The strategy recognized the critical role of MSMEs in

attaining these objectives and its Trade and Investment Reform Program (TIRP) focused on increasing the

competitiveness of Ghana’s private sector exports in world markets.

PROBLEM STATEMENT

Several studies identified limited access to credit as a significant barrier to growth in the MSME sector in Ghana

(Mensah 2004; International Monetary Fund 2003; Association of Ghana Industries 2007). In fact, respondents to

the 2007 Business Climate Survey conducted by the Association of Ghana Industries (AGI) reported that access to

credit and cost of credit were among the five top challenges to growth. Mensah (2004) reported that “long term

financing in terms of equity capital, needed by growth-oriented mainly small and medium companies, is virtually

non-existent for SMEs.”

USAID’S INTERVENTION IN RESPONSE

To address these constraints and thus support its Economic Growth strategy, USAID/Ghana implemented two

DCA loan guarantees with EcoBank in 2003 and 2005. USAID/Ghana originally provided guarantees to two partner

banks in 2003 but then withdrew one because the partner was not utilizing the guarantee. The Mission then

redirected the funds from the terminated guarantee to establish a second guarantee with EcoBank (the 2005

guarantee) to focus on encouraging larger loan sizes than the initial guarantee. Both guarantees were specifically

structured to encourage EcoBank to provide longer-term loans to sectors with the potential to make substantial

contributions to growth. These included MSMEs, microfinance institutions (MFIs), and NGOs with activities in

agriculture, agricultural processing, salt mining/production, fisheries, tourism, value-added processing of wood

products, and textiles and garments. The Action Packages provide additional detail about qualifying loans. In

particular, they place a strong emphasis on loans to support non-traditional exports (NTEs) in specific sectors with

growth potential and spoke to the importance of improving access to long-term loans. The following excerpts

from the Action Packages illustrate the intended targets of guaranteed loans.

“The scope of the DCA program will leverage financing from local funds to both emerging SMEs and to

the micro-enterprise sector.” (2003 and 2005 Action Packages)

“The sectors that the Mission is seeking to strengthen through this assistance are primarily those that

have the most potential in non-traditional exports (NTEs). These are the tourism, textile, and garment

sectors.” (2003 and 2005 Action Packages)

“Specifically, the DCA activity will attempt to introduce medium and long-term capital to industries and

economic sectors that have, to date, been under-represented in the Ghanaian financial sector for various

reasons.”

Table 2 summarizes key characteristics of the two DCA Guarantee Agreements (the legal agreements between

EcoBank and USAID/Ghana).

Ghana EcoBank DCA Guarantee Evaluation 10

TABLE 2: SUMMARY OF DCA GUARANTEES

2003 DCA 2005 DCA

AUTHORITY DCA DCA

TYPE Loan Portfolio Guarantee (LPG) Loan Portfolio Guarantee (LPG)

GUARANTEED

PARTY EcoBank Ghana Limited EcoBank Ghana Limited

MAXIMUM

PORTFOLIO

AMOUNT

$3,000,000 of which not more than

$1,200,000 for projects not designed to

produce or market products for export

$7,000,000

USAID

GUARANTEE

PERCENTAGE

50% 50%

GUARANTEE

CEILING $1,500,000 $3,500,000

TERM OF

GUARANTEE 5 years (7/18/03 - 7/17/2008) 7 years (3/21/05 - 3/23/12)

ORIGINATION FEE 0.50% of guarantee ceiling ($7,500) 0.50% of guarantee ceiling ($17,500)

UTILIZATION FEE 0.25% per annum of portion of the

outstanding principle guaranteed by USAID

0.50% per annum of portion of the

outstanding principle guaranteed by USAID

MAXIMUM LOAN

AMOUNT $600,000 $1,400,000

TENOR 18 months to 5 years Less than or equal to 36 months

QUALIFYING

BORROWERS

Any small, medium, or large enterprises or

microfinance institutions carrying out

Qualified Projects in Ghana

Non-sovereign Ghanaian micro-, small-, and

medium-sized enterprises (MSMEs),

microfinance institutions (MFIs), and non-

governmental organizations (NGOs),

established under Ghanaian law that are

private enterprises in sectors such as

manufacturing, agro-processing, tourism,

textile, garment, and other potential growth

industries.

QUALIFYING

PROJECTS

Revenue-generating activities in agriculture

(excluding cocoa), agricultural processing,

salt mining/production, fisheries, tourism,

value added processing of wood products

(excluding financing related to the harvesting

or export of unprocessed timber), and

textiles and garments.

Investments designed to encourage growth

of Qualifying Borrowers in manufacturing,

agro-processing, tourism, textile, garment,

and other potential growth industry sectors.

The DCA guarantees continued a history of loan guarantees to EcoBank dating back to two Micro and Small

Enterprise Development (MSED) program guarantees in 1996 and 2001. The MSED guarantees provided the

foundation for EcoBank’s SME portfolio growth. The 118 loans guaranteed under the 1996 MSED agreement

Ghana EcoBank DCA Guarantee Evaluation 11

represented 61 percent of the 194 loans in the bank’s SME portfolio in 2002. This is not a perfect comparison

because the MSED loans were distributed over the five years between 1996 and 2001 while the 194 loans in 2002

represent outstanding loans at that time. However, the numbers do illustrate the importance of the MSED-

guaranteed loans to the bank’s SME portfolio. In 2002, the value of outstanding MSED-guaranteed loans accounted

for 26 percent of the EcoBank’s total SME portfolio value. The DCA guarantees build on the foundation of the

MSED guarantees by focusing on progressively larger loans and longer tenors. Table 3 summarizes key

performance characteristics of the four credit guarantees to date.

TABLE 3: SUMMARY OF LOAN GUARANTEES IN GHANA

Starting year

Ending year Type Ceiling ($)

Utilization Amount

($) Utilization Rate (%)

Number of

Loans

Average size of

Loans($)

Average tenor of

Loans(days)

Number of

Claims Value of

Claims($)

1996 2001 MSED $2,000,000

$4,521,617 100.00% 118 $38,319 272 2 $3,320

2001 2006 MSED $2,000,000

$6,877,153 100.00% 138 $49,834 612 8 $116,313

2003 2008 DCA $3,000,000

$2,208,830 73.63% 6 $368,132 1206 2 $341,675

2005 2012 DCA

$7,000,000

$4,446,664 63.52% 4

$1,111,666 619 0 $ -

IV. PURPOSE OF THE EVALUATION

The Ghana DCA loan guarantee evaluation is the first in a series of about 20 evaluations of EGAT’s Office of

Development Credit (EGAT/DC) Development Credit Authority (DCA) credit guarantees which will be

conducted over a four-year period. Each individual evaluation will address the performance of a particular

guarantee. A meta evaluation will synthesize results from the individual evaluations to address broad questions of

the performance of the DCA program. With the meta evaluation, EGAT/DC desires information “to (1) shape the

dialogue about when/how to engage the private sector in development, (2) strengthen USAID’s application of DCA

as a tool for achieving development results, and (3) influence the project design of new guarantees.” This report,

however, deals only with the individual Ghana DCA guarantees. It does not directly address meta evaluation

questions.

The individual evaluations address the performance of the guarantees from the perspective of EGAT/DC rather

than that of the respective USAID Missions. The evaluations address the guarantees’ performance at three levels –

output, outcome, and impact defined as follows.

Output level – Did EcoBank’s use of the guarantees conform to guarantee objectives and specifications as

described in the Guarantee Agreements?

Outcome level – Did EcoBank’s experience with the guarantees improve access to credit for enterprises

in the target sectors outside of guarantee coverage?

Impact level – Did the guarantees have a demonstration effect that improved access to credit for

enterprises in the target sectors from the broader banking sector?

The scope of this evaluation thus extends only to the guarantee partner’s behavior at the output and outcome

levels and on the behavior of the broader banking sector at the impact level. The evaluation does not examine

EGAT/DC’s management of the guarantees nor does it attempt to assess the impacts of the loans on borrowers

or on USAID/Ghana’s objectives.

Ghana EcoBank DCA Guarantee Evaluation 12

V. METHODOLOGY AND INDICATORS

A three-person team conducted the evaluation in Accra, Ghana between February 16 and 27, 2009. Prior to

departing for Ghana, the team met with EGAT/DC to discuss evaluation objectives and procedures and to

interview EGAT/DC personnel. The evaluation team also obtained and reviewed the following literature and data

relevant to the evaluation prior to arriving in Ghana.

Credit Monitoring System data for both the 2003 and 2005 guarantees

Action Packages for both the 2003 and 2005 guarantees

Guarantee Agreements for both guarantees

Biennial Reviews for both guarantees

Credit Review Board meeting notes

Data (two spreadsheets and partial response to a data request) sent by Ecobank

TIPCEE Annual Report, 10/05 – 9/06

Ghana at a Glance (World Bank)

Ghana Economic Memorandum (World Bank)

IMF Survey (w/Ghana article)

Ghana: Selected Issues (International Monetary Fund)

Ghana: 2008 Article IV Consultation (International Monetary Fund)

Economist Intelligence Unit (EIU) Country Report

EIU Country Profile

After reviewing the data and literature, the team worked with EGAT/DC to refine an evaluation framework that

defined the evaluation questions, data sources, data collection methods, and uses of the data. The evaluation

framework provided the foundation for developing detailed interview guides for each potential source of data.

Annex A contains the evaluation framework and the interview guides. Prior to departure the team also developed

a work plan for conducting evaluation activities in Ghana.

Upon arrival in Ghana the team scheduled and conducted structured interviews with key stakeholders and others

who could provide evidence for the evaluation.12 The team also collected literature and secondary data to support

the evaluation. Appendix B contains a list of interviews the evaluation team conducted. The Bibliography contains a

complete list of documents reviewed by the evaluation team.

Based on the Action Packages, the Guarantee Agreements, the literature review, and data availability, the primary

indicators of access to credit that are relevant to this evaluation are:

Change in the number of MSMEs with loans and/or the value of lending to MSMEs.

Change in interest rates for MSME borrowers.

Change in collateral requirements for MSME borrowers.

Change in loan tenors for MSME borrowers.

The evaluation attempted to obtain measures of each of these indicators at each relevant level of the evaluation

(i.e., output, outcome, and impact).

12 The evaluation team interviewed representatives of EcoBank; USAID/Ghana; the Millennium Challenge Corporation; TechnoServe; Chemonics/TIPCEE; the Ministry of Finance and Economic Planning; the Ghana Association of Microfinance Networks; the Ministry of Trade and Industry; the Ghana National Chamber of Commerce and Industry; the World Bank Institute of Statistical, Social, and Economic Research; the Bank of Ghana; the Ghana Association of Bankers; the International Finance Corporation; the World Bank; the Association of Rural Banks; Opportunity International; Millennium Development Authority; and the Association of Financial NGOs. See Annex B for a complete contact list.

Ghana EcoBank DCA Guarantee Evaluation 13

DATA LIMITATIONS

The evaluation team encountered a number of limitations on the type and quality of data available to conduct the

evaluation. The limited depth of data available to address some questions represented one such deficiency. For

example, output and outcome level questions focused on the behavior of the guarantee partner and EcoBank and

USAID were the sole authoritative sources for these data.13 Similarly, few Ghanaian banks (perhaps five) have SME

lending departments and could speak to impact level results. The result is that qualitative data presented in this

report is often thin.

The target sectors (i.e., MSMEs’ MFIs, and NGOs engaged in particular activities) presented another challenge.

These sectors do not match sector definitions used by economic data sources. Specifically, financial data in Ghana

is reported for 11 sectors -- Agriculture, forestry, and fisheries; Export trade; Manufacturing; Transport, storage,

and communication; Mining and quarrying; Import trade; Construction; Commerce and finance; Electricity, gas, and

water; Services; and Miscellaneous. The sectors targeted by the guarantees may cut across all of these sectors

under which data are typically reported.

The divergence between the sectors targeted by the guarantees and those under which economic data are

reported made it impossible to directly examine lending or other economic activity for the targeted sectors on a

broad scale. Many organizations, however, focus on the SME sector and there is, therefore, some limited data on

SMEs. Therefore, much of the analysis in this evaluation uses data on SMEs as a proxy for the target sectors of the

guarantees. However, the SME sector is so large and varied that national-level data on the sector is very thin.

13 Borrowers of guaranteed loans could have spoken to the issue of the impact of EcoBank’s use of the guarantees on access to credit but the evaluation framework developed with EGAT/DC did not include data collection from borrowers.

Ghana EcoBank DCA Guarantee Evaluation 14

VI. EXOGENOUS INFLUENCES ON GUARANTEE PERFORMANCE

Changes in macro-economic conditions and government policy have led to a substantial transformation of the

Ghanaian banking sector during the period of performance of the DCA guarantees. These changes have

substantially improved access to credit for individuals and for all range of businesses. To determine the impact of

the DCA guarantees on access to credit, the evaluation must, to the extent possible, separate the impacts of the

guarantees from the effects of factors external to the guarantees. The report’s introduction described the broader

lending environment in which EcoBank implemented the DCA guarantees and the host of external forces that have

affected access to credit between 2002 (prior to the DCA guarantees) and the present. This section frames those

factors in the context of their potential impact on the indicators used in the evaluation.

The general expansion of the banking sector, and corresponding increase in lending activity, is the most significant

external factor affecting the number of MSMEs with loans or the aggregate value of lending to MSMEs. As discussed

in the introduction, the reasons for the growth in the sector are many including macro-economic policy and

regulatory reforms which created additional liquidity in the banking system, increased competition, and a

strengthened lending environment. In fact, a particular challenge at the outcome and impact levels of this evaluation

was to determine the impact of a very small number of guaranteed loans on the substantial growth in lending for

EcoBank and for the larger banking sector.

Another indicator of improved access to credit is a change (reduction) in interest rates. However, other factors

such as the country’s fiscal policy (i.e., prime rate), bank’s operational expenses, and competition among banks are

likely to have a greater impact on interest rates than a small number of guaranteed loans. The same can be said of

changes in collateral requirements, i.e., that government actions with respect to land tenure, credit bureaus,

courts, and the rights of borrowers and lenders are likely to have a much greater impact on collateral

requirements than will a small number of guaranteed loans to a single bank.

The capacity of potential MSME borrowers represents a significant barrier to credit in Ghana. USAID and other

donors are making substantial investments in improving the capacity of MSMEs to contribute to economic growth.

To the extent that these activities are successful, they should increase access to credit. This factor did not appear

to be significant at the output level of this evaluation because the evaluation discovered no overlap between the

clients of capacity-building technical assistance projects and recipients of guaranteed loans. It was not possible to

determine the effect of capacity-building at the outcome or impact levels. As these activities mature and expand,

they may become significant external determinants of access to credit.

Finally, the efforts of other donors and the Ghanaian government to improve access to credit will, if they are

successful, represent external forces affecting the indicators used for this evaluation. Mensah (2004) identified 17

donor-supported efforts supporting MSMEs as well as at least one government-supported loan guarantee program.

Ghana EcoBank DCA Guarantee Evaluation 15

VII. FINDINGS AND CONCLUSIONS

This section reviews evaluation findings and conclusions. Separate sections examine findings and conclusions at the

output, outcome, and impact levels. Each section begins with a summary of the evaluation questions and then

addresses each question separately stating first the conclusion and then presenting the findings to support the

conclusion.

OUTPUT LEVEL FINDINGS AND CONCLUSIONS

At the output level the evaluation asked whether EcoBank used the guarantees to improve access to credit for

enterprises in the target sectors. The evaluation framework specified three questions at the output level.

Question 1: How did the DCA guarantees fit into EcoBank’s ongoing strategy? What market potential did

the DCA guarantee help open for EcoBank?

Question 2: How did EcoBank implement its loan guarantee programs (e.g., marketing campaigns, changed

terms, training, revised staff structure and responsibilities, improved communications with branch offices,

etc.)? And why?

Question 3: Did EcoBank’s use of the DCA guarantees improve access to credit for the target sectors?

(i.e., did characteristics of guaranteed loans differ from other loans in ways that improved access?)

The output level questions address EcoBank’s behavior in utilizing the guarantees. Sources of evidence to answer

the evaluation questions depended primarily on interviews with four senior individuals with EcoBank (the

Country/Regional Risk Manager, Head of the Credit Administration Department, Retail Risk Manager, and the SME

Department Head) who were most involved in administering the guarantees; EcoBank annual reports; data on the

guaranteed loans obtained from EcoBank and USAID’s Credit Management System (CMS); and reviews of USAID’s

Action Packages, Guarantee Agreements, and Biennial Reviews for both guarantees.

FINDINGS AND CONCLUSIONS FOR QUESTION 1

Question 1: How did the DCA guarantees fit into EcoBank’s ongoing strategy? What market potential did the

DCA guarantee help open for EcoBank?

Conclusion: The DCA guarantees complemented EcoBank’s strategy to transition from a largely wholesale bank

to a fully fledged retail bank with a corresponding increased emphasis on MSMEs. The guarantees allowed the bank

to gain experience with new industries/sectors and types of lending (i.e., financing capital investments) that

complemented this strategy.

Findings: Since its transition from a merchant bank to a universal bank in 2003, EcoBank has shifted its focus from

being a predominantly wholesale bank to a fully fledged retail bank.14 Bank personnel stated that EcoBank seeks to

elevate retail banking to 50 percent of its business although the economic downturn in 2008 has delayed

attainment of this goal. Retail banking implies includes a greater focus on MSMEs, high net worth individuals,

salaried workers, religious organizations, educational institutions, health institutions, and clubs and associations.15

The strategy thus generally coincides with an increased focus on the industries/sectors targeted by the DCA

guarantees (i.e., MSMEs). As one element of its pursuit of this strategy, EcoBank formed a partnership (EB-

ACCION Savings and Loan) with a leading microfinance institution in 2006 to extend its reach into microfinance

savings mobilization and lending.16

14 EcoBank Annual Report, 2005. 15 EcoBank Annual Report, 2006. 16 http://www.eb-accion.com/. Accessed: March 8, 2009.

Ghana EcoBank DCA Guarantee Evaluation 16

An EcoBank official familiar with the bank’s SME lending strategy spoke to the importance of the guarantees in

providing EcoBank the opportunity to test the potential of new firms, industries, and types of lending in which the

bank had little or no previous experience. EGAT/DC’s Biennial Reviews of the guarantees corroborated this

finding stating that the guarantees (and especially the MSED guarantees) “are used by Ecobank as an exploratory

research laboratory for testing the creditworthiness of potential clients.”

Information provided by EcoBank on pre-guarantee lending to the firms that received guaranteed loans and to the

industries/sectors they represent suggests that EcoBank used the guarantees to test new customers, new

industries/sectors, and longer-term financing for capital expenditures. Table 4 summarizes EcoBank’s pre- and

post-guarantee experience with the firms and industries to which it provided guaranteed loans. The first column

lists individual borrowers by their industry. The second and third columns show EcoBank’s pre-guarantee lending

experience with each individual borrower. The final column shows the type of loan provided under the guarantee.

TABLE 4: ECOBANK EXPERIENCE WITH BORROWERS/INDUSTRIES RECEIVING GUARANTEED

LOANS

Borrower and industry Pre-guarantee

Experience with borrower

Pre-guarantee Experience with

industry

Guaranteed loan type

Agricultural processing (vegetable oil milling)

None Long-term and

short-term loans Long-term loan

Rubber and plastics products manufacturing

None Short-term loans Long-term loan

Garment manufacturer None Short-term loans Long-term loan

Garment manufacturer None Short-term loans Long-term loan

Land development Short-term loans None Long-term loan

Well drilling Short-term loans Short-term loans Long-term loan

Mining and quarrying None None Long-term loan

Microfinance institution Short-term loans Short-term loans Long-term loan

Microfinance institution Short-term loans Short-term loans Long-term loan

Shore handling None None Long-term loan

Key findings include:

Ghana EcoBank DCA Guarantee Evaluation 17

Of the nine unique borrowers (one borrower received two loans) under the DCA guarantees, six

represented new clients for EcoBank.

Of the nine unique borrowers under the DCA guarantees, eight received long-term loans to finance

capital expenditures. None had received such loans prior to the guarantee. The ninth, an MFI, received

two large, long-term loans for on-lending to micro-enterprises.

Of the eight sectors/industries represented by the borrowers of guaranteed loans, EcoBank had no

previous experience with three and had provided long-term loans to only one.

An EcoBank official intimately involved in the guarantees and in lending strategy stated that the DCA guarantees

were critical to increasing the bank’s capacity to structure long-term investment transactions.

FINDINGS AND CONCLUSIONS FOR QUESTION 2

Question 2: How did EcoBank implement its loan guarantee programs (e.g., marketing campaigns, changed terms,

training, revised staff structure and responsibilities, improved communications with branch offices, etc.)? And why?

Conclusion: EcoBank integrated the guarantee into its normal loan assessment process. It did not provide any

special training or alter normal loan assessment procedures. It did not actively market the guarantee to potential

borrowers because of the risk of moral hazard.

Findings: EcoBank integrated the implementation of the guarantee program into its existing loan assessment

process. The normal process is for branch-level relationship managers to meet with loan applicants and make an

accept/reject recommendation to the branch manager who then makes a recommendation to the credit

committee at EcoBank headquarters in Accra. The credit committee makes the final ruling on loans but will not

over-rule a branch’s decision to reject a loan because the branch bears the responsibility for bad loans.

Consideration of the guarantees enters into the process in two places. First, EcoBank informed relationship

managers and branch managers by email or telephone of the availability and function of the guarantee. The

relationship managers and branch managers take this into consideration when deciding whether to recommend a

loan to the credit committee. The branches may, and do according to the one EcoBank official, recommend loans

specifically for the guarantees that they would not have recommended without the guarantee. Second, the credit

committee may also advise a branch to reconsider a rejection in light of the guarantee.

EcoBank does not advertise or market the guarantees to potential borrowers because of the risk of moral hazard.

Three people the evaluation team interviewed (two representatives of the banking sector and one government

representative) spoke of a history in Ghana of government-backed loan guarantees with little penalty for default.

These individuals, including EcoBank, believed that borrower awareness of the guarantees would increase the

likelihood of default.

FINDINGS AND CONCLUSIONS FOR QUESTION 3

Question 3: Did EcoBank’s use of the DCA guarantees improve access to credit for the target sectors? (i.e., did

characteristics of guaranteed loans differ from other loans in ways that improved access?)

Conclusion: EcoBank’s use of the guarantees improved access to medium and long-term credit for some firms in

the target sectors. The guarantees gave EcoBank the protection from risk necessary to extend loan sizes and

tenors beyond its typical range. The guaranteed loans focused on the upper end of the spectrum of qualified

borrowers by size. In fact, loan sizes appear consistent with lending almost exclusively to medium-sized

enterprises. Guaranteed loans were larger, and consequently fewer in number, than anticipated by USAID/Ghana

but still fell within the size and tenor parameters established in the Guarantee Agreements. Special waivers (2003

guarantee) and overly broad and imprecise definitions of target sectors (2005 guarantee) rendered the target

sectors defined in the Guarantee Agreements irrelevant.

Ghana EcoBank DCA Guarantee Evaluation 18

Findings: At the output level (i.e., EcoBank behavior within the guarantees) improved access to credit means that

EcoBank used the guarantees to provide new credit or new types of credit to borrowers who would not have

received the credit without the guarantees. The bank may make credit, or types of credit, more available by

offering larger and longer-term loans, reducing interest rates to make loan more affordable, or reducing collateral

requirements. These criteria reflect the objectives articulated in the Action Packages of “introducing medium and

long-term capital to industries and economic sectors that have, to date, been under-represented in the Ghanaian

financial sector,” encouraging a reduction in collateral requirements, and extending average loan maturity periods.

The findings presented here show first that EcoBank’s use of the guarantees improved access to credit (i.e., that

loan recipients would not likely have received the loans without the guarantee) and then that the characteristics of

guaranteed loans were generally consistent with [imprecisely defined] USAID/Ghana objectives.

The guaranteed loans represent improved access to credit only if EcoBank would not have made the loans, or

would not have offered the terms, outside of the guarantees’ coverage. Two sources of evidence – statements by

EcoBank personnel responsible for approving guaranteed loans and a comparison of the characteristics of

guaranteed loans to those of the bank’s overall SME portfolio – suggest that this is so.

The small number of guaranteed loans afforded the evaluation team the opportunity to review each loan

individually with EcoBank personnel. The team asked bank personnel, including those responsible for authorizing

the guaranteed loans, whether the bank would have extended the loans without the guarantees and the primary

reasons the bank chose to place the loans under the guarantees. These personnel said that EcoBank would have

extended the type of loans it did (i.e., long-term capital financing) to only one of the loan recipients without the

guarantee. Even in this case (the MFI), the bank would have required much greater security without the guarantee.

The primary reasons for placing the loans under the guarantees were the increased risk associated with lending to

firms/industries in which the bank had little experience and the relatively large size and long tenor of loans

associated with capital financing.

The size and tenor of the guaranteed loans also differ significantly from those of the bank’s overall SME portfolio.

This provides additional evidence that the guarantees improved access to credit by encouraging EcoBank to make

loans that it would not have made without the guarantees. Table 5 shows the distribution of loans by size for

EcoBank’s SME portfolio and for the guaranteed loans. All of the guaranteed loans fall within the top eight percent

of loans by size and 60 percent fall within the top two percent. Guaranteed loans account for 43 percent of loans

over $1 million and 22 percent of loans over $250,000.

TABLE 5: DISTRIBUTION OF ECOBANK'S SME LOANS BY SIZE

SME portfolio Guaranteed loans

Loan size ($) Number Cumulative

percent Number Cumulative

percent

$1 - $50,000 504 63.6% 0 0.0%

$51,000 - $99,000 137 80.9% 0 0.0%

$100,000 - $249,000 92 92.6% 1 10.0%

$250,000 - $499,000 32 96.6% 3 40.0%

$500,000 - $749,999 13 98.2% 3 70.0%

$750,000 - $999,000 7 99.1% 0 70.0%

$1,000,000 - $4,999,999 7 100.0% 3 100.0%

Source: EcoBank

Ghana EcoBank DCA Guarantee Evaluation 19

The guaranteed loans also had longer tenors than the bank’s typical SME loans. Guaranteed loans had tenors of

between 22 and 60 months (Table 7) with average tenors of 40 months (2003 guarantee) and 27 months (2005

guarantee). These tenors are well above the average tenor of 12 months in EcoBank’s overall SME portfolio.17

The longer tenors and larger loan sizes reflect the bank’s focus on using the guarantees to finance relatively risky

capital investments rather than working capital and are entirely consistent with Action Package objectives. Capital

investment loans are riskier because they are relatively large and require longer tenors for repayment.

Nevertheless, loans placed under the guarantees were much larger and consequently far fewer in number, than

anticipated by USAID/Ghana. Table 6 illustrates the divergence between anticipated and actual loan characteristics

under the 2003 and 2005 guarantees. EcoBank placed only six loans under the guarantee in 2003 with an average

value ten times that anticipated in the Action Package. In 2005 the bank placed less than one-seventh of the

anticipated number of loans under the guarantee with average values more than five times the anticipated average

loan size.

TABLE 6: ANTICIPATED VERSUS ACTUAL LOAN CHARACTERISTICS

2003 DCA

Anticipated 2003 DCA

Actual 2005 DCA

Anticipated 2005 DCA

Actual

Number of loans 80 6 35 4

Size of loans ($) $37,000 $368,132 $200,000 $1,111,666

Tenor (months) 24 40 36 21

Source: 2003 and 2005 Action Packages, EcoBank loan records.

USAID/Ghana and EcoBank developed the target loan sizes and numbers based on characteristics of EcoBank’s

SME portfolio at the time the guarantees were put in place. They thus reflect past experience more than a

considered attempt to select loan sizes consistent with accomplishing USAID/Ghana’s objectives. The anticipated

loan numbers and sizes were not binding, however, and EcoBank used the guarantees specifically to expand its

outreach into the market for larger loans required for capital investments – a direction that is entirely consistent

with the Action Package objective of “introducing medium and long-term capital to industries and economic

sectors that have, to date, been under-represented in the Ghanaian financial sector.”

The evaluation also examined the size of the guaranteed loans and sectors represented by recipient enterprises

relative to the target sectors described in the Guarantee Agreements. Table 7 summarizes guaranteed loans by

industry. The Guarantee Agreement for the 2003 guarantee defined specific qualifying borrowers and projects as

any small, medium, or large enterprises or microfinance institutions (MFIs) with activities in agriculture, agricultural

processing, salt mining/production, fisheries, tourism, value added processing of wood products, and textiles and

garments. The comparison of guaranteed loan sizes with all of EcoBank’s SME loans (Table 4) suggests that the

guaranteed loans were to enterprises at the upper end of the small-medium-large spectrum. Many of the loans

under the 2003 guarantee also do not appear to satisfy the definitions of qualifying sectors/industries as defined in

the Guarantee Agreement. USAID/Ghana, however, approved each loan under the 2003 guarantee and explicitly

waived the target sector requirement.18

17 Based on data provided by EcoBank. 18 Personal communication from Kofi Owusu-Boakye, EGAT/DC.

Ghana EcoBank DCA Guarantee Evaluation 20

TABLE 7: LOAN SUMMARY BY INDUSTRY

Type of enterprise Purpose of loan Loan amount

($) Loan tenor (months)

Agricultural processing (vegetable oil milling)

Capital equipment, working capital, and other expenses

$500,000 51

Rubber and plastics products manufacturing

Capital equipment purchase $240,000 24

Garment manufacturer Capital equipment purchase $250,000 48

Garment manufacturer Capital equipment purchase $500,000 60

Land development Capital equipment purchase $260,145 30

Well drilling Capital equipment purchase $458,644 25

Mining and quarrying Capital equipment purchase $1,400,000 22

Microfinance institution On-lending to micro-enterprises $1,007,005 25

Microfinance institution On-lending to micro-enterprises $1,400,000 24

Shore handling Capital equipment purchase $665,188 36

The 2005 guarantee focused on somewhat smaller enterprises than the 2003 guarantee adding micro-enterprises

and NGOs and dropping large enterprises. It is less specific about qualifying projects than is the 2003 guarantee

authorizing loans for growth-enhancing investments in sectors such as manufacturing, agro-processing, tourism,

textile, garment, and other potential growth industries. In spite of eliminating large enterprises, however, loans

under the 2005 guarantee were even larger than those under the 2003 guarantee. Virtually any sector/industry

could qualify for a guaranteed loan under the broad definitions of the 2005 Guarantee Agreement. All loans were

thus to qualified borrowers.

In spite of relatively large loan sizes under both guarantees, the sizes appear generally consistent with the SME

target.19 Nevertheless, one person outside of EcoBank who was intimately familiar with the rationale for and

details of the guarantee agreements questioned whether the shore handling company was an SME. He

acknowledged, however, that there was no formal definition of SMEs in Ghana.20 Furthermore, two of the largest

loans went to start-up companies which would have been relatively small at the time the loans were disbursed.

The 2003 Action Package restricts qualifying loans to no more than $600,000 and tenors to between 18 and 60

months. The 2005 Action Package specified a maximum loan size of $1,400,000 and tenors of no more than 36

months. The loans placed under the guarantees generally satisfied these criteria although two of the loans

(representing 54 percent of the loan value disbursed) placed under the 2005 guarantee were for the maximum

allowable size. As with the anticipated loan sizes and numbers, the maximum loan sizes defined in the Guarantee

Agreements likely reflect standard agreement language rather than any deliberate decision by USAID/Ghana.

19 When identifying SMEs from bank loan records in developing countries, the World Bank’s International Finance Corporation uses loan sizes of $10,000 to $100,000 as a proxy for small enterprises and loans between $100,000 and $1 million as a proxy for medium enterprises (IFC undated). 20 In fact, EcoBank defines SMEs as enterprises with less than $250,000 in assets (excluding land and buildings) and between $250,000 and $5 million in annual turnover. Alternative definitions include the number of employees (Bank of Ghana 2007). The EcoBank definition is more restrictive than that used by the National Board for Small Scale Industries which defines medium-sized enterprises as having fixed assets up to $1 million (Mensah 2004).

Ghana EcoBank DCA Guarantee Evaluation 21

Guarantee Agreements can specify any maximum allowable loan size up to 20 percent. Both agreements specified

the standard 20 percent maximum.

While direct recipients of guaranteed loans were generally larger enterprises, the loans to the MFI likely improved

access to credit for MSMEs indirectly. Guaranteed loans to the MFI totaled over $2.4 million and accounted for 54

percent of the value of loans under the 2005 guarantee. The MFI is large with $20.9 million disbursed to 117,528

borrowers in 2007.21 Its portfolio in 2007 consisted of 82 percent micro-enterprises and 18 percent SMEs. Most of

the MFI’s borrowers (60 to 70 percent) are traders, about 20 percent are production and manufacturing