Languages

Pages

Legal

Topics to Discuss

• Which employers have to comply with the employer mandate?

• What must employers do to comply with the employer mandate?

• When do employers have to comply with the employer mandate?

• What changes to the insurance mandates apply in 2016?

• What reporting is required for 2015 filed in 2016?

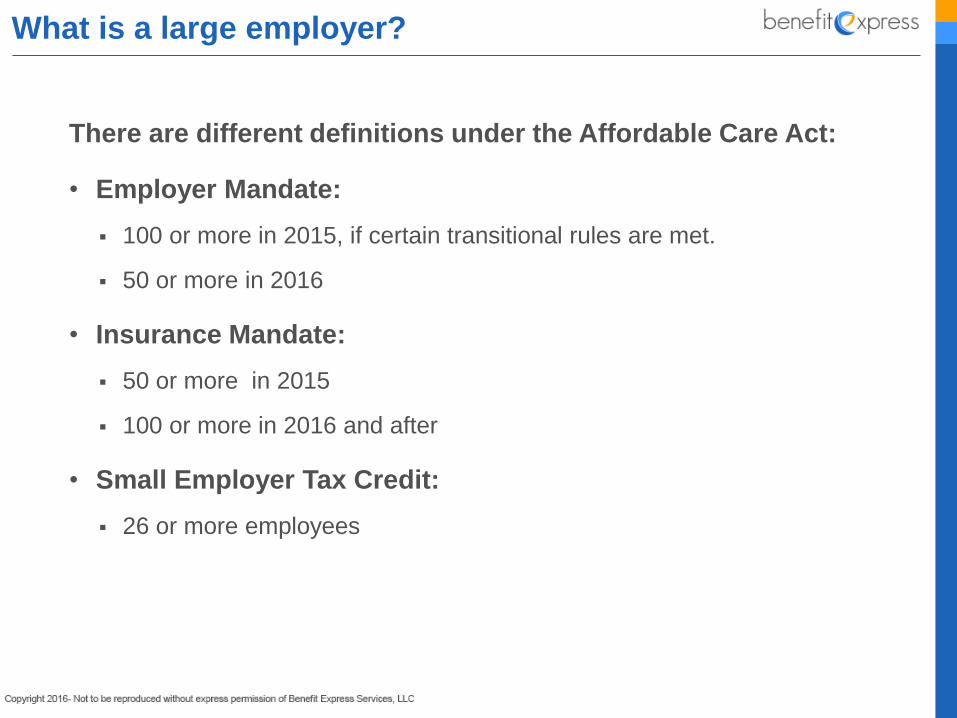

What is a large employer?

There are different definitions under the Affordable Care Act:

• Employer Mandate:

100 or more in 2015, if certain transitional rules are met.

50 or more in 2016

• Insurance Mandate:

50 or more in 2015

100 or more in 2016 and after

• Small Employer Tax Credit:

26 or more employees

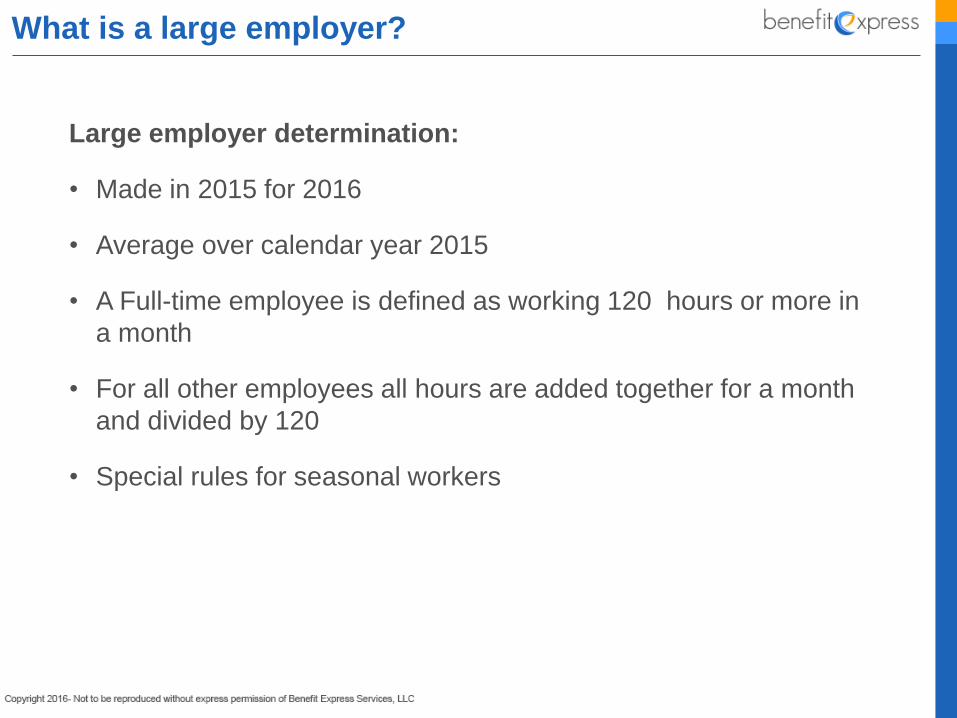

What is a large employer?

Large employer determination:

• Made in 2015 for 2016

• Average over calendar year 2015

• A Full-time employee is defined as working 120 hours or more in

a month

• For all other employees all hours are added together for a month

and divided by 120

• Special rules for seasonal workers

There are 2 employer mandate penalties:

• Failure to offer 95% of full-time employees and their dependent

children with least minimum essential coverage in 2016.

• Failure to offer full-time employees with affordable minimum value

individual coverage and dependent children with minimum

essential coverage.

What employers have to do to comply with the

employer mandate?

Failure to offer minimum essential coverage to 95% in 2016 of

full-time employees and their dependent children:

• Penalty of $2, 000 per employee – minus the first 30 employees

for 2016.

• Applied separately to each member of the controlled group.

• Applies only if one full-time employee receives credits or

subsidies.

• Applies to each full-time employee.

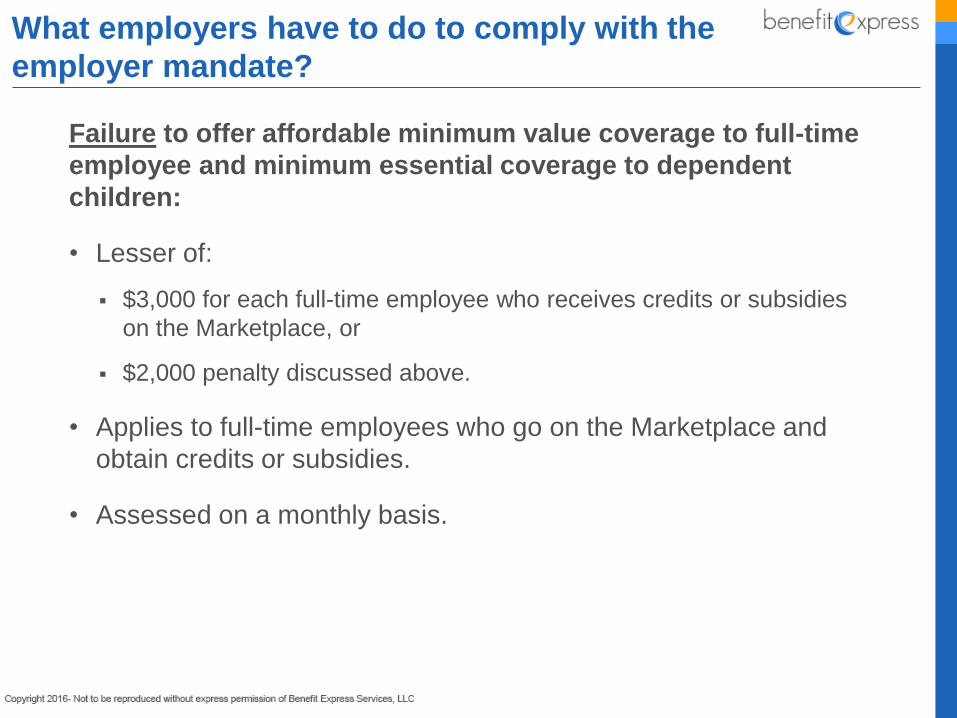

What employers have to do to comply with the

employer mandate?

Failure to offer affordable minimum value coverage to full-time

employee and minimum essential coverage to dependent

children:

• Lesser of:

$3,000 for each full-time employee who receives credits or subsidies

on the Marketplace, or

$2,000 penalty discussed above.

• Applies to full-time employees who go on the Marketplace and

obtain credits or subsidies.

• Assessed on a monthly basis.

What employers have to do to comply with the

employer mandate?

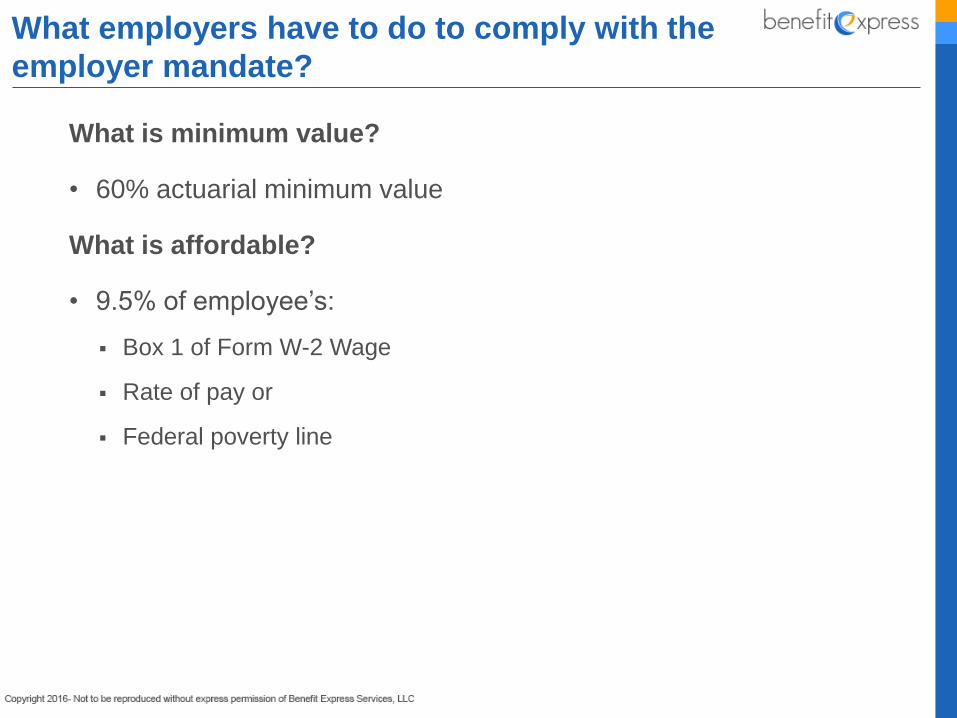

What is minimum value?

• 60% actuarial minimum value

What is affordable?

• 9.5% of employee’s:

Box 1 of Form W-2 Wage

Rate of pay or

Federal poverty line

What employers have to do to comply with the

employer mandate?

• Who is a full-time employee?

30 hours per week, 130 hours per month.

• Full-time employee must be offered coverage after completing a

waiting period (UP TO 90 DAYS).

• Special rules for variable hour employees

Offered coverage after completing a look back measurement period or

a monthly measurement period.

• Employment status must be determined when ALE is subject to

employer mandate.

What employers have to do to comply with the

employer mandate?

• When hired, must determine if an employee is:

Full-time

Part-time or

Variable hour employee

• If an employee is variable hour, must determine if full-time over:

a monthly measurement period, or

a look back measurement period

What employers have to do to comply with the

employer mandate?

Use Monthly Measurement Period:

• Must use if have not measured hours in the past.

• Must re-measure each month if employee has worked 130 hours.

• Must offer coverage by the beginning of the fourth month after

employee is determined to be full-time.

• Administrative nightmare because employees are going on and off

coverage during year.

What employers have to do to comply with the

employer mandate?

Use of look back measurement period:

• 3 to 12 months in length.

• One measurement period is for new employees and another is for

ongoing employees.

• Use administrative period to enroll any variable hour employee

that qualifies.

• For any variable hour employees who qualify, the coverage period

is called the stability period.

What employers have to do to comply with the

employer mandate?

If variable hour employee is determined to be full-time:

• Must offer coverage during the stability period.

• Generally the stability period is the same length as the

measurement period.

• Employer must continue to offer coverage during the stability

period even if employee is not working full time.

What employers have to do to comply with the

employer mandate?

Employers with 100 or more full-time & full time equivalent

employees:

• January 1, 2015 or renewal date in 2015

• To use renewal date, ALE must meet requirement of transitional

rule

It depends how many full- time or all employees covered in the past.

Employer with 50 to 99 full-time & full time equivalent

employees:

• Renewal date in 2016.

• Must meet the requirements of transitional rules.

When do employers have to comply with the

employer mandate?

For Employers with 50 to 99 full-time & full time equivalent

employees:

• Limited Workforce Size. The employer must employ on average

at least 50 full-time employees (including full-time equivalents) but

fewer than 100 full-time employees (including full-time

equivalents) on business days during 2014.

• Maintenance of Workforce and Aggregate Hours of Service.

During the period beginning on Feb. 9, 2014 and ending on Dec.

31, 2014, the employer may not reduce the size of its workforce or

the overall hours of service of its employees in order to qualify for

the transition relief.

When do employers have to comply with the

employer mandate?

For Employers with 50 to 99 full-time & full time equivalent

employees:

• Maintenance of Previously Offered Health Coverage. During

the period beginning on Feb. 9, 2014 and ending on Dec. 31,

2015 (or, for employers with non-calendar-year plans, ending on

the last day of the 2015 plan year) the employer does not

eliminate or materially reduce the health coverage, if any, it

offered as of Feb. 9, 2014.

• Certification of Eligibility for Transition Relief The ALE certifies

on a Form 1094-C that it meets the eligibility requirements set

forth above.

• Employer cannot change plan year after February 9, 2014.

When do employers have to comply with the

employer mandate?

• As of January 1, 2016, the Affordable Care Act definition of “small”

group employer (for purposes of insurance market size) increases

from 50 to 100 employees.

• One significant impact of this change is that the ACA’s small group

rating limitations (e.g., age-banded rates) will apply to employers

with 51-100 employees.

• These employers were previously considered “large” employers

so their rates were set using various factors such as claims

history, industry and location.

• In the small group market, carriers can set rates based only on

age, family size, geography and tobacco use (although California

has prohibited tobacco use as a rating factor).

What the changes to the insurance mandates

will occur in 2016?

• Under a special transitional rule, however, employers with 51-100

employees who will be re-defined as small employers as of

January 1, 2016, will have the option of delaying this impact by

renewing their current large group policies on or before October 1,

2016.

• Since the last date to renew in 2016 will be October 1, many

carriers are suggesting that such employers renew by October 1,

2015, so their 12-month renewal date will be October 1, 2016.

What the changes to the insurance mandates

will occur in 2016?

Should You Renew Early to Delay Small Group Rating?

• Renewing early to delay small group rating may be a good

strategy for many employers with 51-100 employees, but for

certain employers this will NOT be a good strategy.

• There are various factors an employer must consider.

The health risk and age of the group, for example, an employer in a

high-risk industry that has a young workforce may have lower rates as

a small employer than as a large employer.

The employer’s claims history and industry, for example, an employer

in a low-risk industry with good claims experience may have higher

rates under small group rating than it did in the past under large group

rating.

Whether an employer will lose its delayed effective date under the

Employer Mandate provisions of the ACA.

What the changes to the insurance mandates

will occur in 2016?

Why Renewing Early Might Cause Employer Mandate Penalties to

Apply Earlier

• Possibly losing the delayed effective date under the Employer Mandate is

critical to consider and requires some additional explanation.

• The definition of “small” employer varies under different provisions of the

ACA.

• For purposes of the Employer Mandate, employers with 50 or more

employees (including “full time equivalents”) are “large” employers.

• The effective date of these provisions generally is 2015; however, many

employers with 50-99 employees qualified for a one-year delay to 2016

because they met certain requirements.

• One of the requirements is that the employer cannot change its plan year

after February 9, 2014.

What the changes to the insurance mandates

will occur in 2016?

• Signed By President on October 7, 2015.

• It amends the “small employer” definition for purposes of health

care reform’s insurance market and Exchange provisions.

• It repeals the mandatory expansion of the small group market to

employees with up to 100 employees and reverts to the prior

definition of up to 50 employees.

• States maintain flexibility to define the small market as up to 100

employee.

Protecting Affordable Coverage for Employees

Act

What reporting is required for 2015?

• Employers who have 50 or more full-time and full-equivalent full-

time employees in 2014 must report what coverage was offered to

full-time employees during calendar year 2015.

• Forms serve three purposes:

Report coverage for individual mandate purposes.

Report compliance for employer mandate purposes.

Report who offered coverage for eligibility for credits and subsidies.

• Each full-time employee will receive a form.

• If medical coverage is self-funded, each individual covered by

medical plan must receive a form, including those on COBRA and

retired.

• If under 50 employees and insured, the insurer will report on Form

1095-B.

• If under 50 employees and self-insured, the employer must report.

Employers Subject to the Reporting

Requirement

Forms Used for Filing

• The forms operationalize the information reporting requirements.

• The forms issued include:

1095-B - Health Coverage. Insurers and self-insured plans will provide one

to each enrollee. The form provides information on the coverage provided.

1094-B -Transmittal of Health Coverage Information Returns.

Transmittal form insurers and self-insured plans will file with IRS along with all

the Forms 1095-B.

1095-C - Employer-Provided Health Insurance Offer and Coverage. Large

employers will provide one to each enrollee. The form provides information on

the coverage provided, and on to whom and when the coverage was offered.

1094-C - Transmittal of Employer-Provided Health Insurance Offer and

Coverage Information Returns. Transmittal form insurers and self-insured

plans will file with IRS along with all the Forms 1095-C.

1095-A Health Insurance Marketplace Statement. Exchanges will provide to

their enrollees.

• The timelines track the Form W-2 rules.

• For example, the form is generally filed with the IRS by Feb. 28

(May 31) (March 31 for electronic filing), (June 30) and furnished

to full-time employees or responsible individuals by February 1,

2016. (March 31)

• The information on the form pertains to the prior calendar year

and the first forms are due in 2016 (reporting information for

2015).

When do the forms need to be provided and

filed?

• The Employer is responsible for providing form 1095-C to union

employees.

• Can complete by inserting code 1H in line 14 and Code 2E in line

16.

• Employer must determine if coverage is affordable minimum value

coverage.

What reporting is necessary for union

employees?

What Information is needed to be Collected?

For each employee:

• Employment date of each employee who became full time during 2015.

• Months during 2015 in which the employee was full -time or part-time.

• Months during 2015 in which employee was subject to a waiting or measurement period.

• Months during 2015 in which the employee was offered minimum essential coverage with

minimum value in 2015.

• Months during 2015 in which the employee was covered by minimum essential coverage with

minimum value in 2015.

• Months in 2015 in which minimum essential coverage offered to spouse and dependent

children.

• If the employee waived coverage , which affordability safe harbor applies.

• For each month . the amount of the employee contribution for the lowest-cost monthly

premium for self-only minimum essential coverage that provides minimum value.

• For self-insured plan, the names and social security numbers for each member of the

employee’s family and for what months they were covered.

What Information is needed to be Collected?

For each employer:

• Were they members of a controlled group?

• If yes, the names of each member.

• The total number of full-time employees for each month in 2015.

• The total number of all employees for each month in 2015.

• Does any transitional rules apply for any month during 2015?

• For what months during 2015 were at least 70% of full-time

employees offered minimum essential coverage?

• Which certifications of eligibility apply?

Penalties for Noncompliance

• A reporting entity that fails to comply with the Code § 6055 or

6056 reporting requirements may be subject to the general

reporting penalties for failure to file correct information returns and

failure to furnish correct payee statements.

• Two different sections of the Internal Revenue Code discuss the

penalties for not complying with Code §§ 6055 and 6056

reporting:

Code § 6721 discusses failing to send correct returns to the IRS.

• The basic penalty is $250 for each incorrect return.

• The total fine during any calendar year will not exceed $3,000,000.

Code § 6722 discusses failing to provide employee statements.

• The penalty is the same as above but applies for not providing individual

statements.

Penalties for Noncompliance

• However, penalties may be waived if the failure is due to reasonable

cause and not to willful neglect.

• The final regulations also include short term relief from penalties to allow

additional time to develop appropriate procedures for data collection and

compliance with these new reporting requirements.

• For returns and statements filed and furnished in 2016 to report offers of

coverage in 2015, the IRS will not impose penalties on reporting entities

that can show they make good faith efforts to comply with the information

reporting requirements.

• This relief is provided only for incorrect or incomplete information

reported on the return or statement, including social security numbers,

TINs or dates of birth.

• No relief is provided for reporting entities that do not make a good faith

effort to comply with these regulations or that fail to timely file an

information return or statement.

Questions?

Top Related