Languages

Pages

Legal

The Rosia Montana Gold & Silver Project:

A Project for Romania

June 2013

2

Legal Notice

The summary information contained herein has been provided by Gabriel Resources Limited (the “Company”) in respect of its interest in the Rosia Montana Gold and Silver

Project (the “Rosia Montana Project” or “Project”). The Project is wholly owned by the Company’s subsidiary Rosia Montana Gold Corporation S.A. (“RMGC”) in which the

Company owns an 80.69% equity interest.

No representation or warranty, express or implied, as to the accuracy, completeness or fairness of the information or opinions contained herein is made or given by the

Company, its subsidiary companies, including RMGC or their respective officers, directors or employees and no responsibility or liability is accepted by any person for such

information or opinions. In all cases, recipients should conduct their own investigation and analysis of the Company and its interest in the Project. The contents of this

presentation are not to be construed as investment, legal, financial or tax advice.

In furnishing this presentation, the Company does not undertake or agree to any obligation to provide you with access to any additional information or to update you or this

presentation or to correct any inaccuracies in, or omissions from, this presentation that may become apparent. Except as otherwise indicated, the information contained herein

is as of June 2013.

The information is neither an offer to sell nor a solicitation of an offer to buy any securities nor shall it or any part of it form the basis of or be relied on in connection with, or act

as an inducement to enter into, any contract or commitment whatsoever. The contents of this presentation are being provided to you solely for your information and must not be

copied, published, reproduced, distributed in whole or in part to others at any time by recipients. Any failure to comply with this restriction may constitute a violation of securities

laws.

The information contained herein contains forward-looking statements relating to the Company and/or the Project that are based on management’s current expectations,

estimates and projections. Such statements may reference timelines, economic impact, job creation, costs estimates, future ability to finance the Project, patrimony plans,

technical specification and Project delivery and other statements that express management's expectations or estimates regarding the timing of completion of various aspects of

the Projects’ development or of future performance.

The words "believe", "expect", "anticipate", "contemplate", "target", "plan", "intends", "continue", "budget", "estimate", “projects”, "may", "will", "schedule", “potential”, and similar

expressions identify forward-looking statements. Forward-looking statements are necessarily based upon a number of estimates and assumptions that, while considered

reasonable by management, are inherently subject to significant procedural, legal, business, economic and competitive uncertainties and contingencies.

This presentation includes many such forward-looking statements which are subject to known and unknown risks, uncertainties and other factors which are difficult to predict

and that may cause the actual outcomes, level of activity, financial results, performance or achievements to differ materially from those expressed or implied by the forward-

looking statements, which are not guarantees of future performance.

These risks, uncertainties and other factors include, but are not limited to: changes in the worldwide price of precious metals; fluctuations in exchange rates; legislative, political

or economic developments including changes to mining and other relevant legislation in Romania; geopolitical uncertainty, uncertain legal enforcement; changes in, and the

effects of, the government policies affecting the Company's and/or RMGC’s operations; uncertainties related to timelines for awaited approvals; changes in general economic

conditions, and the financial markets; operating or technical difficulties in connection with exploration, development or mining; environmental risks; the risks of diminishing

quantities or grades of reserves; and the Company’s requirements for substantial additional funding.

Certain scientific and technical information contained in this presentation is extracted or derived from the Company’s “Technical Report on the Rosia Montana Gold and Silver

Project Transylvania, Romania” with an effective date of October 1, 2012 (the “2012 Technical Report”), which is filed under the Company’s SEDAR profile. SRK Consulting

(UK) Ltd (“SRK”), the author of the 2012 Technical Report, considers the Mineral Reserve and Mineral Resource statements made in the 2012 Technical Report to be in

accordance with the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), CIM Standards on Mineral Resources and Reserves, Definitions and Guidelines (CIM

Standards).

All forward-looking and other statements made in respect of this presentation are expressly qualified in their entirety by this cautionary statement.

3

Contents

Gabriel Resources – Overview

The Rosia Montana Project – Deposit and Mine Plan

Additional Properties – Organic Growth Opportunities

Political & Permitting Overview

The Project Impact in Romania

Summary

4

Investment Highlights

World class asset:

One of the most significant gold deposits outside the

ownership of a “major” mining company;

Measured & Indicated Resource – 17.1M oz Au (+1.4M

Inferred), 81.1M oz Ag1 (Using cut off grade of 0.4g/t Au)

Proven & Probable Reserve - 10.1M oz Au, 47.6M oz Ag1

(Using US$400/oz Au pit shells)

Will be one of Europe’s largest gold mines; permitting

process to be completed

Lowest quartile cash cost anticipated

Potential for Growth:

No resource definition drilling since 2005

Additional exploration properties at Bucium Rodu Frasin

(Au-Ag) and Bucium Tarnita (Cu-Au)

Potential to expand a major mining district

No debt, cash in bank:

$67.1 million in cash as at March 31, 2013

Monthly cash burn $2-4 million per month

(1) Taken from the 2012 Technical Report

5

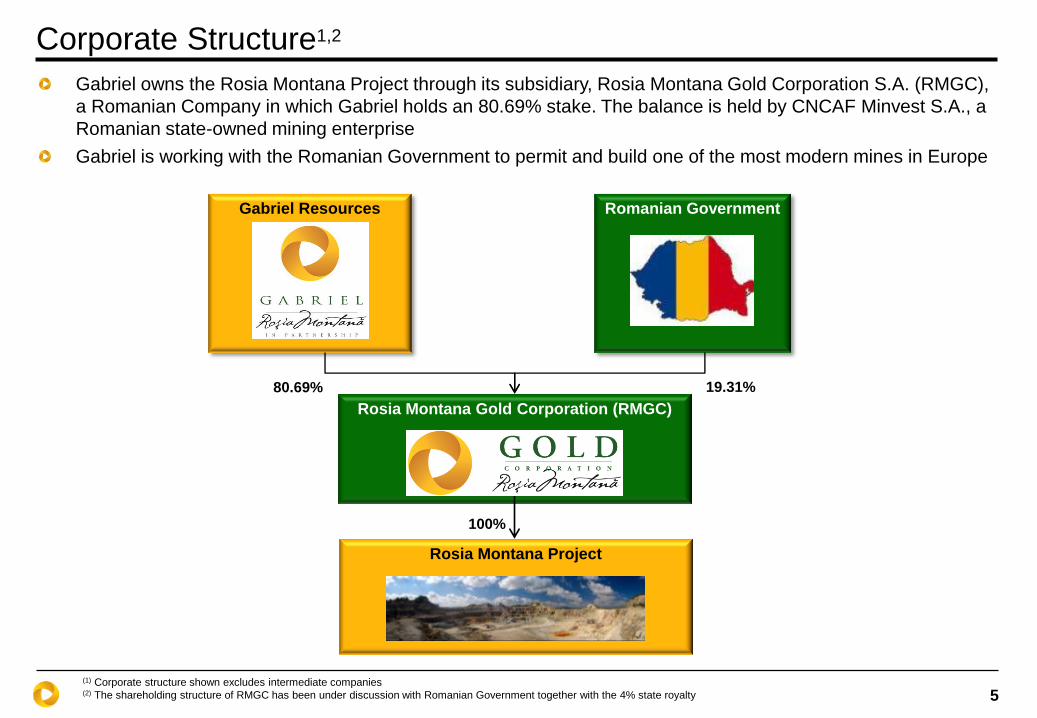

Corporate Structure1,2

Gabriel Resources Romanian Government

Rosia Montana Gold Corporation (RMGC)

Rosia Montana Project

(1) Corporate structure shown excludes intermediate companies (2) The shareholding structure of RMGC has been under discussion with Romanian Government together with the 4% state royalty

Gabriel owns the Rosia Montana Project through its subsidiary, Rosia Montana Gold Corporation S.A. (RMGC),

a Romanian Company in which Gabriel holds an 80.69% stake. The balance is held by CNCAF Minvest S.A., a

Romanian state-owned mining enterprise

Gabriel is working with the Romanian Government to permit and build one of the most modern mines in Europe

80.69% 19.31%

100%

6

Capitalization1

Key information

Share Price $1.36

52 Week High/Low $2.94 / $1.21

Average Daily Trading Vol. (3 months) ~840,000 shares

Ticker GBU.TO

Market TSX

Market Cap $524 million

Shares Outstanding 384 million

Options (incl. DSUs & RSUs) 27 million

Filly Diluted Shares Outstanding

411 million

Cash (as at March 31, 2013) $67.1 million

Debt $0

Paulson & Co 16%

Electrum Global Holdings 16%

BSG Capital 16%

Newmont 13%

Baupost Group 13%

Free-float 26%

Major shareholders

Share price evolution – 12 months

(1) Information provided as at June 14, 2013 unless stated otherwise, and provided in Canadian Dollars

7

Contents

Gabriel Resources – Overview

The Rosia Montana Project – Deposit and Mine Plan

Additional Properties – Organic Growth Opportunities

Political & Permitting Overview

The Project Impact in Romania

Summary

8

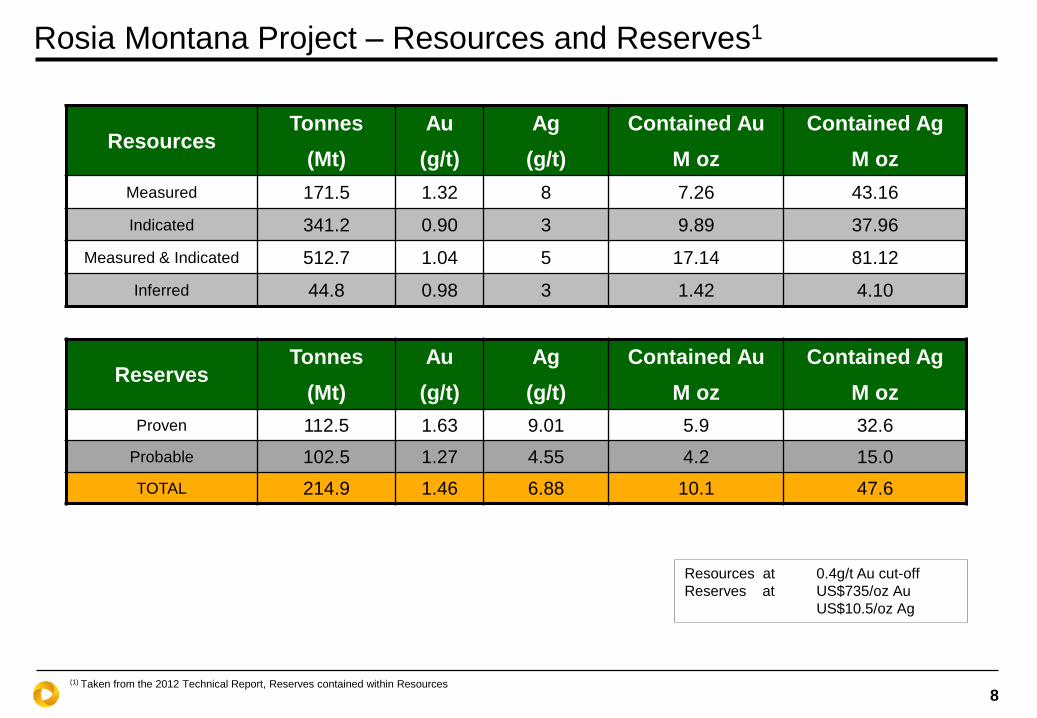

Rosia Montana Project – Resources and Reserves1

Resources Tonnes

(Mt)

Au

(g/t)

Ag

(g/t)

Contained Au

M oz

Contained Ag

M oz

Measured 171.5 1.32 8 7.26 43.16

Indicated 341.2 0.90 3 9.89 37.96

Measured & Indicated 512.7 1.04 5 17.14 81.12

Inferred 44.8 0.98 3 1.42 4.10

Resources at 0.4g/t Au cut-off

Reserves at US$735/oz Au

US$10.5/oz Ag

Reserves Tonnes

(Mt)

Au

(g/t)

Ag

(g/t)

Contained Au

M oz

Contained Ag

M oz

Proven 112.5 1.63 9.01 5.9 32.6

Probable 102.5 1.27 4.55 4.2 15.0

TOTAL 214.9 1.46 6.88 10.1 47.6

(1) Taken from the 2012 Technical Report, Reserves contained within Resources

9

Carnic Cetate

Orlea

Jig

Rosia Montana Project – Reserve Model

Average content of

reserves block (g/t)

10

Rosia Montana Project – Perspective

Carnic Pit

Cetate Pit

Jig Pit

Orlea Pit

Plant Site

Carnic Waste Dump

Rosia Montana

Protected Area

LGS

Tailings Dam

11

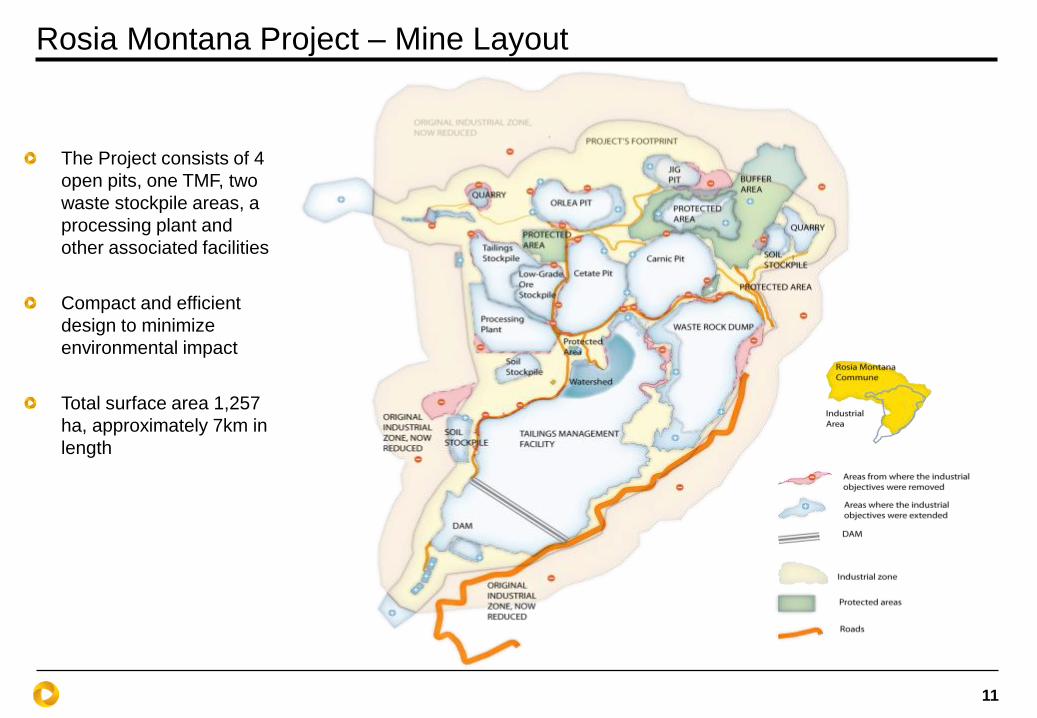

Rosia Montana Project – Mine Layout

The Project consists of 4

open pits, one TMF, two

waste stockpile areas, a

processing plant and

other associated facilities

Compact and efficient

design to minimize

environmental impact

Total surface area 1,257

ha, approximately 7km in

length

12

Project Key Facts

Open pit truck and shovel mining process – 1.2:1 waste:ore strip ratio

Conventional CIL processing (closed circuit) – 14Mtpa design

16 year operating mine life

Old mining district; good infrastructure and access to educated mining talent

Access to grid power supplied from

existing 110kV transmission line

currently passing through the Project

site

Readily available water supply from

local river

Direct road and nearby rail access

Royalty currently 4%

Corporate tax rate 16%

13

Commissioned to reflect current CapEx and OpEx status of the Project

Undertaken by SRK Consulting (UK) Limited

Mineral Resource updated using a cut off grade of 0.4g/t; 2009 Resource was stated

using 0.6g/t cut off grade

No changes to the scope or scale of Project: no change to Mineral Reserve, still using

US$400/oz Au pit shell

Conservative input price assumptions for key consumables

Base case metal price assumptions:

• US$1,200/oz Au

• US$20/oz Ag

2012 NI 43-101 – Highlights of the Update

14

Estimated Production Profile1

Cetate 25%

Carnic 52%

Jig 3%

Orlea 20%

Production by Pit

Pro

du

ctio

n o

zs (

in 0

00

’s)

Year Pit Mined

1-4 Cetate, Carnic

5-6 Carnic

7-8 Carnic, Orlea

9 Cetate, Carnic, Orlea, Jig

10-11 Cetate, Orlea, Jig

12 Cetate, Orlea

13+ Cetate

Year of Mine Life

Annual Gold Production

Annual Silver Production

Pro

du

ctio

n o

zs (

in 0

00

’s)

Year of Mine Life

(1) Taken from the 2012 Technical Report

0

100

200

300

400

500

600

700

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10 Yr11 Yr12 Yr13 Yr14 Yr15 Yr16

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Yr1 Yr2 Yr3 Yr4 Yr5 Yr6 Yr7 Yr8 Yr9 Yr10 Yr11 Yr12 Yr13 Yr14 Yr15 Yr16

15

Cost Structure Estimates1

Initial Capital + Sustaining Capital = Total Capital

US$1.40 billion US$571 million US$1.97 billion

(1) Taken from the 2012 Technical Report. Operating costs have been estimated in accordance with standard industry practices and are valid as at the third quarter of 2012 (2) All figures in US Dollars and royalty based on 4%

Capital Costs:

Mining $102

Processing $263

G&A $52

Freight/Refining $3

Royalty $51

Silver Credit ($72)

LOM Cash

Costs2 of

US$399/oz

Mining $3.67

Processing $9.48

G&A $1.87

Other $1.95

Total Cost2 per Tonne of US$16.97

Operating Costs:

16

Project Economics

Description Units 2012 2009

Gold price (US$/oz) 1,200 750

Silver price (US$/oz) 20 10.5

Life of Mine Cash cost (US$/oz) 399 335

Pre-production capital (US$m) 1,400 876

Sustaining capital (US$m) 571 366

Closure cost (US$m) 146 128

Undiscounted cashflow after tax (US$m) 3,606 1,662

NPV after tax (5% discount rate1) (US$m) 1,836 997

IRR after tax % 19.6 20.4

Payback Years 3.3 3.5

(1) A 5% discount rate was used in the March 2009 43-101 Technical Report. The Base Case discount rate used in the 2012 Technical Report is 10%.

17

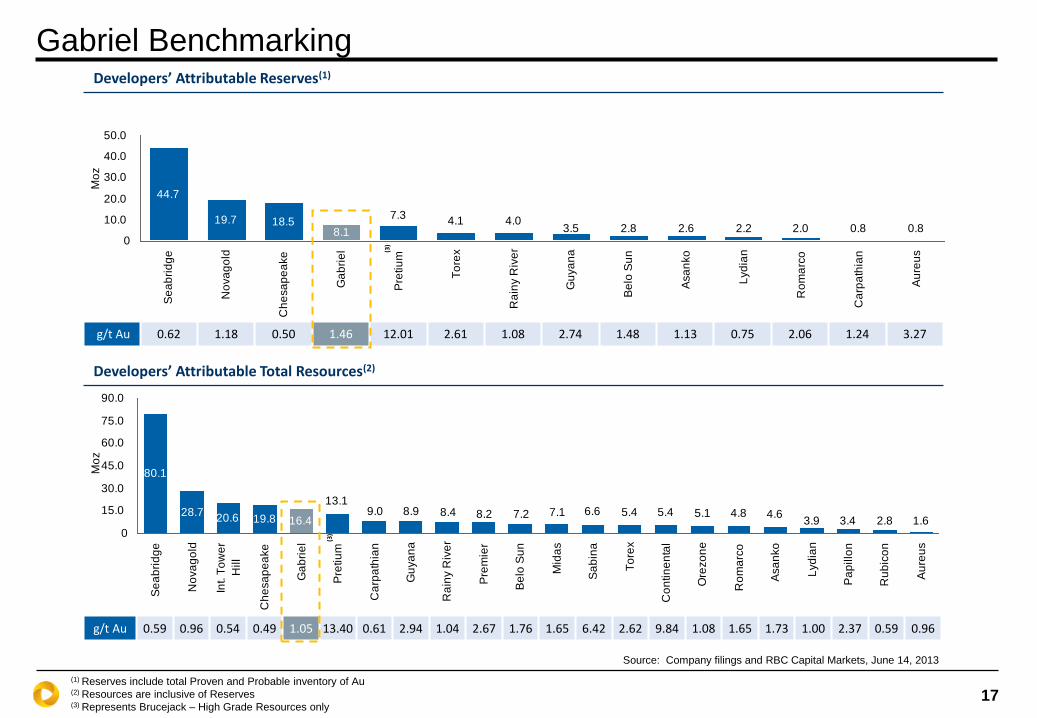

Gabriel Benchmarking

3.9 3.4 2.8 1.6

80.1

28.720.6 19.8 16.4

13.19.0 8.9 8.4 8.2 7.2 7.1 6.6 5.4 5.4 5.1 4.8 4.6

0

15.0

30.0

45.0

60.0

75.0

90.0

Se

ab

rid

ge

No

va

go

ld

Int. T

ow

er

Hill

Ch

esa

pe

ake

Ga

bri

el

Pre

tiu

m

Ca

rpa

thia

n

Gu

ya

na

Ra

iny R

ive

r

Pre

mie

r

Be

lo S

un

Mid

as

Sa

bin

a

To

rex

Co

ntin

en

tal

Ore

zo

ne

Ro

ma

rco

Asa

nko

Lyd

ian

Pa

pillo

n

Ru

bic

on

Au

reu

s

Mo

z

3.5 2.8 2.6 2.2 2.0 0.8 0.84.04.1

7.3

8.118.519.7

44.7

0

10.0

20.0

30.0

40.0

50.0

Se

ab

rid

ge

No

va

go

ld

Ch

esa

pe

ake

Ga

bri

el

Pre

tiu

m

To

rex

Ra

iny R

ive

r

Gu

ya

na

Be

lo S

un

Asa

nko

Lyd

ian

Ro

ma

rco

Ca

rpa

thia

n

Au

reu

s

Mo

z

(1) Reserves include total Proven and Probable inventory of Au (2) Resources are inclusive of Reserves (3) Represents Brucejack – High Grade Resources only

Developers’ Attributable Total Resources(2)

Developers’ Attributable Reserves(1)

g/t Au 0.62 1.18 0.50 1.46 12.01 2.61 1.08 2.74 1.48 1.13 0.75 2.06 1.24 3.27

g/t Au 0.59 0.96 0.54 0.49 1.05 13.40 0.61 2.94 1.04 2.67 1.76 1.65 6.42 2.62 9.84 1.08 1.65 1.73 1.00 2.37 0.59 0.96

(3)

Source: Company filings and RBC Capital Markets, June 14, 2013

(3)

18

10 Year Industry Average Cash Costs vs Gold Price1

180 224 253 271 317 395

467 478 557

643 738

55 53

60 68 84

99

118 139

166

166

190

235 277

313 339 401

494

585 617

723

809

928

-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US

$/o

z

Operating Cash Cost Depreciation and Amortization Avg. Annual Gold Price

Average 2012

Production Margin:

$740/oz

Rosia Montana

LOM Cash Cost:

$399/oz

(1) Source RBC Capital Markets

19

4 Year Industry Average All-In Sustaining Costs vs Gold Price1

462 537

611 699

16

20

32

39

239

300

400

473

717

857

1,043

1,211

-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2009 2010 2011 2012

US

$/o

z

Mine Site Cash Cost Smelting, Refining, Royalties

D&A, Corp. G&A, Int. Exp., Sust. Capex Avg. Annual Gold Price

Average 2012

All-In Margin:

$457/oz

Rosia Montana LOM

Average All-In Cash Cost:

$653/oz

Rosia Montana

LOM Cash Cost:

$399/oz

(1) Source RBC Capital Markets

20

Contents

Gabriel Resources – Overview

The Rosia Montana Project – Deposit and Mine Plan

Additional Properties – Organic Growth Opportunities

Political & Permitting Overview

The Project Impact in Romania

Summary

21

Rosia Montana – A Mining District

Rosia Poieni: A state owned working mine Rosia Montana: Historical workings at

the Cetate pit

22

Organic Growth Opportunities – Additional Properties

Rosia Montana

Rosia Poieni

Bucium Rodu-Frasin

Bucium Tarnita

Bucium Rodu Frasin – Resource Estimate

Category Tonnage

(Mt)

Grade

Au

(g/t)

Grade

Ag

(g/t)

Contained

Au (oz)

Contained

Ag (oz)

Indicated 7.9 1.92 5 491,000 1,385,000

Inferred 35.4 1.16 3 1,320,000 3,271,000

Bucium Rodu-Frasin1:

Gold and silver low sulphidation epithermal system

Dominantly disseminated with associated stockworks and

breccias, veins

• Block size 40mE x 40mN x 10mRL

• Ordinary Kriging

• 0.6 g/t Au cut off

Bucium Tarnita:

A copper/gold porphyry deposit covering a surface area

of 700m x 700m

Potential to host large tonnage deposit - Untested at

depth

Resource estimate not yet published by the Company

(1) Certain scientific and technical information contained in this slide is extracted or derived from the RSG Global report dated November 2004 (“Bucium Technical Report”), which is f

filed under the Company’s SEDAR profile. The Mineral Resource Estimates reported therein have been estimated by Julian Verbeek, MAusIMM, of RSG Global in accordance with

the Canadian Institute of Mining, Metallurgy and Petroleum’s standards and definitions and are dated as of November 2004.

23

Contents

Gabriel Resources – Overview

The Rosia Montana Project – Deposit and Mine Plan

Additional Properties – Organic Growth Opportunities

Political & Permitting Overview

The Project Impact in Romania

Summary

24

Romania Rosia Montana

2,000 years of mining history with reports of up

to 50 million ounces of gold produced, together

with significant silver and copper

In the 5 years leading to EU accession in 2007,

in excess of 500 mines were closed, with over

200,000 jobs lost

Romania is in the European Union;

governed by EU rules and regulations

Coalition Government

(PSD/PNL) returned to power in

December 2012 General

Election

With the current GDP per

capita among the lowest in

the EU, the Romanian

government may look to

harness the potential of its

natural resources

Educated and skilled

workforce

Located in a highly prospective mining district

Rosia Montana has been mined for 2,000 years

and most recently by the state until 2006

Unemployment in the Rosia Montana region is

approximately 65% - RMGC employment has

brought this number down from over 90%

The Project will assist in the clean-up of pollution

from years of unregulated mining in the Rosia

Montana region

Designed to comply with

Romanian laws and EU

directives

Key infrastructure already in

place

Long-lead time equipment

already purchased and

stored in warehouses

• SAG mill

• 2 x Ball mills

• Crusher

25

Romanian Parliament structure – 412 deputies, 176 senators

PSD leading Parliamentary party has a total of 223 seats. The USL coalition, plus Minorities have 417 seats.

The Opposition has 153 seats.

64

50

8

23 20

9

1 1

0

10

20

30

40

50

60

70

PSD PNL PC PD-L PP-DD UDMR Independents Vacancy

Senators mandates

PSD PNL PC PD-L PP-DD UDMR Independents Vacancy

159

101

17 18

4934

18 13

10

20

40

60

80

100

120

140

160

PSD PNL PC Ethnic

Minorities

PD-L PP-DD UDMR Independents Vacancy

Deputies mandates

PSD PNL PC Ethnic Minorities PD-L PP-DD UDMR Independents Vacancy

26

Romanian Government structure and Ministries

27

Permitting Process The Rosia Montana Project with annual production of >5M tonnes is deemed a project of “national interest” and as such has

to be permitted at the National level

Progress:

Q3 2010 – resumption of the Technical Analysis Committee (TAC) review of the Environmental Impact Assessment (EIA)

2011 – received Environmental Approval of the PUZ for the Industrial Project and Archaeological Discharge Certificate for

Carnic (ADC #4)

2011 – TAC visits Project, TAC concludes all technical matters completed; await process confirmation

X 2012 – austerity protests; changes to Government; local council elections; presidential impeachment; general elections

Q4 2012 – Local referendum held: “Do you agree with the resumption of mining in the Apuseni Mountain region and

specifically at the Rosia Montana Project?” - 62.5% voted in favour

Q4 2012 – National elections held; landslide victory for USL providing a stable platform for government not seen in years

Engagement with USL government to finalize permitting process; further TAC Meetings May 10th and 31st, 2013

Next Steps:

Completion of TAC → cabinet approval of EIA → issuance of Environmental Permit → ratification by Parliament

Completion of PUZ for the Industrial Project Area and Historical Area

Once the Environmental Permit is obtained from the Romanian Government, and the PUZ are approved, in the absence

of any other extraordinary events (legal or otherwise) it would take approximately one year to:

• Complete the majority of outstanding surface rights acquisitions

• Receive the majority of other permits and approvals, including initial construction permits

• Finalise the project build details and advance financing for the project

Following this, construction is estimated to take approximately 30 months

28

Romanian Political Overview

2007 - 2009 2010 2011 2012 2013 2014 2015 2016

Electoral years Non-electoral years

May ’07

Presidential

impeachment

Jun ’08

Local Elections

Nov ‘08

National Elections

Romanian Parliament

Dec ’09

Presidential

Elections

Dec ‘12

National Elections

Romanian Parliament

End ’16

National Elections

Romanian Parliament

End ’14

Presidential

Elections

Jun ’12

Local Elections Mid ’16

Local Elections

29

USL Government – Recent Media Statements Minister Delegate of Large Projects, Dan Sova:

“All what I can say now is that a political decision will be taken within the next two or three months, if it (the Project) would be

implemented, or not” 1

Prime Minister, Victor Ponta:

“If all environmental standards are complied with, if the Romanian state gets a much higher interest and if we collect royalties at

European level, if the Romanian Parliament will decide, not only about that case, but also in the case of all mining exploitations,

reopening of mines, creation of jobs, investments in the environment and so on, revenues to the budget, I think I will keep my promise

to the people – we create jobs, we preserve the environment and we obtain more money – this is what I want to do.” 2

Minister of Environment, Rovana Plumb:

“Any authorization of an investment requires an integrated environmental approval from the environment authorities. An integrated

environmental approval cannot be approved, cannot be adopted without political debates. The Government will work transparently, but I

repeat, in the form I took it over last year, the Project cannot be sustained. If the additional guarantees related to the environmental

risks are observed, if the requirements regarding the benefits for Romania are met and if a new sustainable project is proposed, then

we will discuss. Until then, the Government has made no decision.” 3

Minister of Culture, Daniel Barbu:

“Looking at the whole political-technical debate on cyanides, jobs, and I look at the monuments... What do I see? That, in a locality of

300 houses, half have been restored on the money paid by the company...The underground; I have seen restored Roman galleries,

including wooden devices recovered from the times of the Romans. The Romanian State has never had the necessary money to

restore these. I say that from what I read on paper, I repeat; in addition I also read the opinions of both sides. I have seen a team of

archaeologists led by a French woman – who I understand is an authority in the field – who preserved these galleries, some can be

even visited, there is a museum with mining equipment used throughout time. What I see on paper does not seem discouraging in

terms of heritage valorization.” 4

Government of Romania:

The Official Gazette Reported: “The establishment of the new company is motivated by the Government by claiming that the project

operating in Rosia Montana can generate operating revenues and direct contributions for the state budget estimated at several billion

dollars, and can also be a major contributor to the recovery of the mining industry Romania and the creation of a significant number of

jobs in an area, an area concerned by major unemployment.” 5

(1) Antena 3, March 16, 2013 (2) Antena 3, May 7, 2013 (3) Antena 3, May 18, 2013 (4) Interview, May 13, 2013 (5) Official Gazette, May 29, 2013

30

60% of total

surface

already

secured

To date RMGC has secured 757ha of

land, amounting to 60% the total

surface area required for Project

construction – this includes 78% of the

number of homes in the Project footprint

Surface Rights Status

61%

belongs to

residential

owners

39% are

institutional

properties

Of the total remaining surface to be

acquired, 39% (196ha) are institutional

properties

The remaining 304ha (61%) of the total

surface to be acquired belongs to

private owners

A total of 155 households located

under the Project footprint are still to be

relocated

Once the Environmental Permit is granted the Company will resume the surface rights acquisition process; the acquisition

programme ceased soon after the 2007 permitting process was put on hold

Project

Objective:

Secure 100% of

the surface rights

and hand over to

the construction

team 40% of total

surface still

to be secured

Resettlement to Date:

125 families opted for resettlement in the Recea neighbourhood at Alba Iulia – a

location chosen by the community and built by RMGC

Construction began in 2006 and was completed in 2010

Resettlement and community support is an ongoing commitment of the

Company

Land is available and in possession for expansion of up to 80 additional houses

for those opting for resettlement

31

Contents

Gabriel Resources – Overview

The Rosia Montana Project – Deposit and Mine Plan

Additional Properties – Organic Growth Opportunities

Political & Permitting Overview

The Project Impact in Romania

Summary

32

Today The vision

Economy High unemployment / poverty rate

Lack of opportunities for businesses

Harsh macroeconomic conditions

>3,000 in direct jobs over the Project’s lifetime

Opportunities for local businesses

>$24 billion(1) in total contribution to Romania’s GDP

Environment

Current pollution

Acid waters; heavy metal

contamination in local water system

Abandoned open pits

Soil contamination

Acid waters are cleaned by operation

Pits are closed and planted or transformed into lakes

Pilot water treatment plant currently operating

Establishment of a $146 million financial guarantee for

closure, environmental restoration and post-closure

monitoring

Patrimony

Most Roman galleries not accessible

Limited historical monuments exhibited

Cultural heritage houses in

advanced degradation, no government

money to preserve

Allocation of significant expenditure for the

conservation of heritage

Many Roman galleries restored and open for visitors

Restoration of historical town center; most historical

houses renovated and used for sustainable

development programs

Community Young leaving the area in search of a

better life

Poverty affects social cohesion

Community life and traditions are restored

Sustainable development strategies ( professional

reconversions, business plans for post mining

activities)

OVERALL Impoverished community with no real

alternative

SOLUTION - Prosperity, growth, clean environment,

tourist destination, cultural heritage rehabilitated.

A long term future for Rosia Montana

Rosia Montana Project Benefits: Summary

(1) At a gold price of USD $1,200/oz

33

Contents

Gabriel Resources – Overview

The Rosia Montana Project – Deposit and Mine Plan

Additional Properties – Organic Growth Opportunities

Political & Permitting Overview

The Rosia Montana Project – Impact in Romania

Summary

34

Summary

Bringing one of the world’s largest

undeveloped gold projects to production

Rosia Montana will become one of

Europe’s largest gold mines

Production profile of c.500,0001 oz Au per

annum at lowest quartile cash costs

Project economics robust at current

gold/silver prices - >US$0.5 billion free

cash flow generated per annum with a

substantial reinvestment into the

Romanian economy

>US$24 billion2 direct and indirect

potential impact from the Project on the

Romanian economy at current gold prices

Continual efforts to rehabilitate the

historical center of Rosia Montana

Local community support remains strong

Romanian public support through

December 9, 2012 positive referendum

vote

Working with new Romanian

Government to bring the first modern

mine to the Romanian people

Environmental permitting process to be

completed

TSX listing with strong supportive global

shareholder base

Permitting Europe’s largest gold mine……… Gabriel Resources, Romania and Rosia Montana

(1) Taken from the 2012 Technical Report (2) At a gold price of USD $1,200/oz

35

ANNEXES

36

Analyst Coverage1

Institution Analyst Contact Information

BMO Capital Markets John Hayes (416) 359-6189

CIBC World Markets Cosmos Chiu (416) 594-7106

Cormark Securities Inc. Mike Kozak (416) 943-6749

Cowen Securities Adam Graf (646) 562-1344

RBC Capital Markets Stephen Walker (416) 842-4120

Scotia Capital Inc. Trevor Turnbull (416) 863-7427

(1) Gabriel is followed by the analysts listed above. Please note that any opinions, estimates or forecasts regarding Gabriel's performance made by these (or any other) analysts are theirs

alone and do not represent the opinions, forecasts or predictions of Gabriel or its directors or officers. Gabriel does not by its reference above or distribution imply its endorsement of, or

concurrence with, such information, conclusions or recommendations

37

Largest Shareholder Ownership History

Source: Bloomberg, as of June 2013

Current

Shareholders >10% 31-Dec-04 31-Dec-05 31-Dec-06 31-Dec-07 31-Dec-08 31-Dec-09 31-Dec-10 31-Dec-11 Latest

millions % of total millions % of total millions % of total millions % of total millions % of total millions % of total millions % of total millions % of total millions % of total

Paulson & Co. - - - - - - - - 46.0 18.0% 61.4 18.1% 61.4 17.6% 61.4 16.2% 61.4 16.0%

Electrum Strategic

Holdings - - - - - - - - 50.8 19.9% 61.4 18.1% 61.4 17.6% 61.4 16.2% 60.4 15.7%

BSG Capital Markets - - - - - - - - - - 30.0 8.8% 30.0 8.6% 60.0 15.8% 60.0 15.6%

Newmont Canada 15.0 10.2% 33.4 18.9% 33.4 15.9% 46.8 18.4% 50.3 19.7% 50.3 14.8% 50.3 14.4% 50.3 13.2% 50.3 13.1%

The Baupost Group - - - - - - - - - - - - - - 48.6 12.8% 48.6 12.7%

Total 15.0 10.2% 33.4 18.9% 33.4 15.9% 46.8 18.4% 147.1 57.6% 203.1 59.9% 203.1 58.3% 281.7 74.2% 281.7 73.1%

38

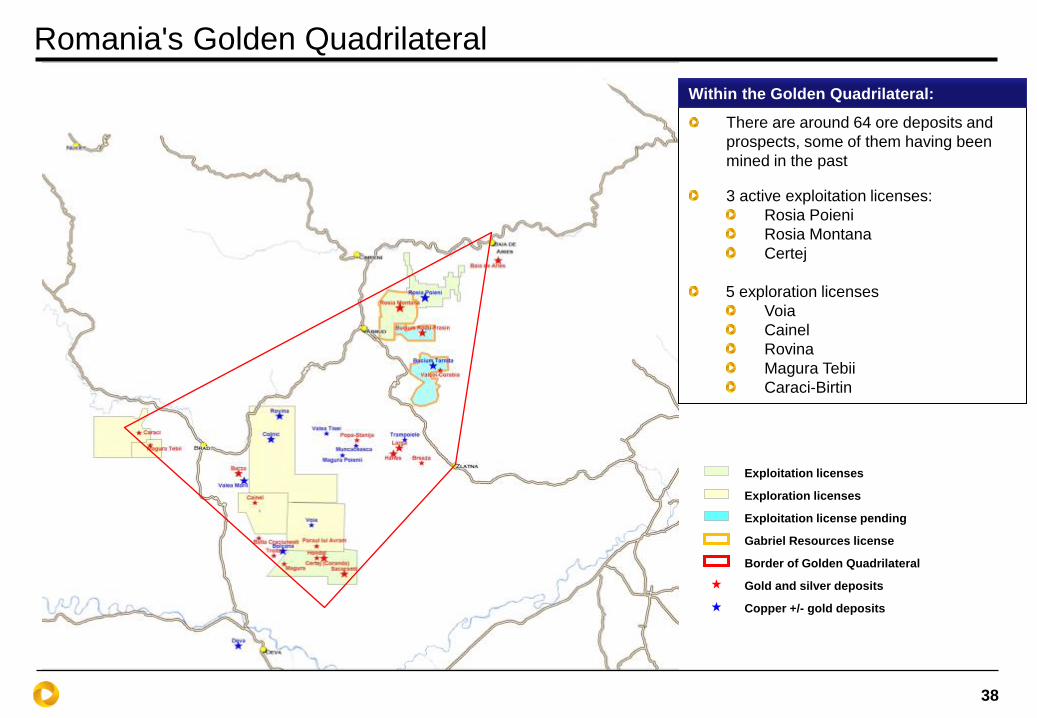

Romania's Golden Quadrilateral

Copper +/- gold deposits

Gold and silver deposits

Exploitation licenses

Exploration licenses

Exploitation license pending

Gabriel Resources license

Border of Golden Quadrilateral

There are around 64 ore deposits and

prospects, some of them having been

mined in the past

3 active exploitation licenses:

Rosia Poieni

Rosia Montana

Certej

5 exploration licenses

Voia

Cainel

Rovina

Magura Tebii

Caraci-Birtin

Within the Golden Quadrilateral:

39

Project – Geology

40

Project Geology– Cetate and Carnic Cross Section

Marine Sediments Dacite

Tuffaceous

Vent Breccia

Andesite

Black

Breccia

W E

Cirnic Cetate

Polymictic breccia

41

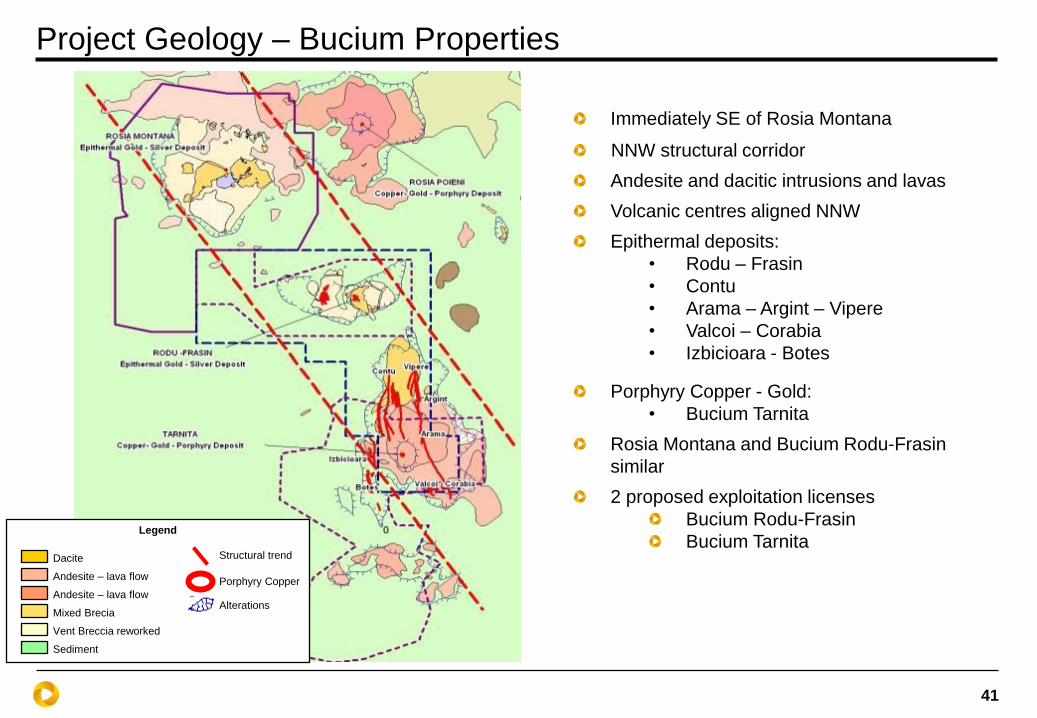

Immediately SE of Rosia Montana

NNW structural corridor

Andesite and dacitic intrusions and lavas

Volcanic centres aligned NNW

Epithermal deposits:

• Rodu – Frasin

• Contu

• Arama – Argint – Vipere

• Valcoi – Corabia

• Izbicioara - Botes

Porphyry Copper - Gold:

• Bucium Tarnita

Rosia Montana and Bucium Rodu-Frasin

similar

2 proposed exploitation licenses

Bucium Rodu-Frasin

Bucium Tarnita

Project Geology – Bucium Properties

Legend

Dacite

Andesite – lava flow

Andesite – lava flow

Mixed Brecia

Vent Breccia reworked

Sediment

Alterations

Structural trend

Porphyry Copper

42

The Proposed Mining Process

• An illustration of the most modern mining project in Romania

Process tailings

Processing

Pit

Pit setup Blasting Ore loading

and transport Crushing

Grinding

Leaching

Gold recovery

with active

carbon Electrolysis

Melting CN

neutralisation

Clear water Settled tailings Final dam

Secondary dam

Primary dam Runoff recirculated

Proposed

Rosia Montana Project

CONCRETE PLATFORM lined with high density polyethylene

43

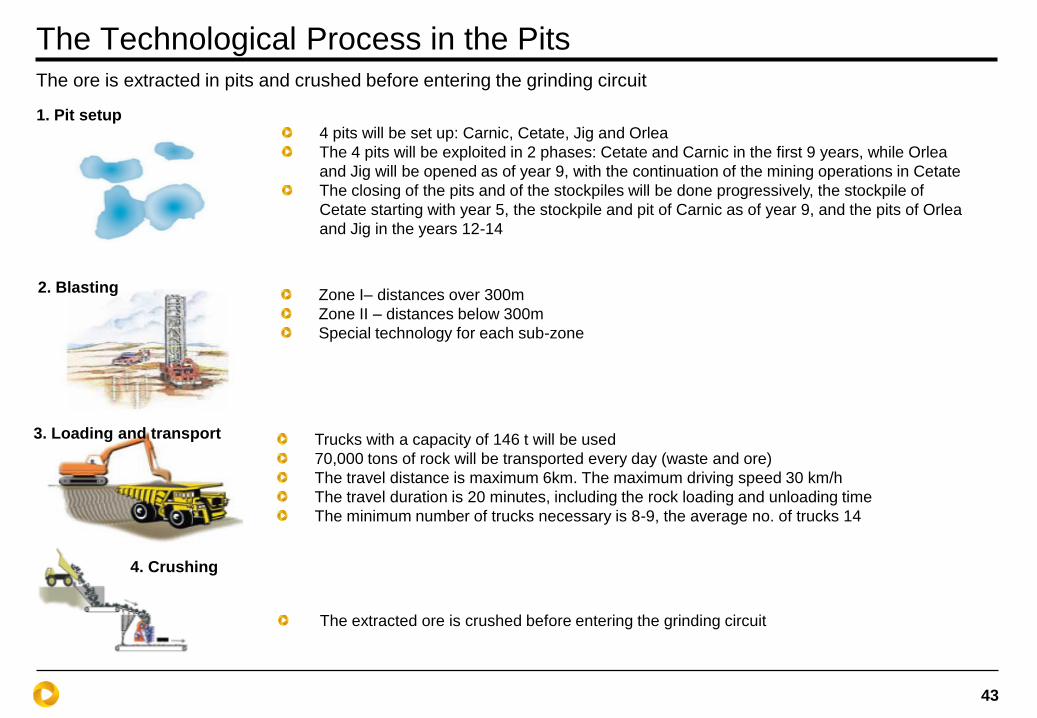

The ore is extracted in pits and crushed before entering the grinding circuit

The Technological Process in the Pits

2. Blasting

3. Loading and transport

4. Crushing

1. Pit setup

Zone I– distances over 300m

Zone II – distances below 300m

Special technology for each sub-zone

Trucks with a capacity of 146 t will be used

70,000 tons of rock will be transported every day (waste and ore)

The travel distance is maximum 6km. The maximum driving speed 30 km/h

The travel duration is 20 minutes, including the rock loading and unloading time

The minimum number of trucks necessary is 8-9, the average no. of trucks 14

The extracted ore is crushed before entering the grinding circuit

4 pits will be set up: Carnic, Cetate, Jig and Orlea

The 4 pits will be exploited in 2 phases: Cetate and Carnic in the first 9 years, while Orlea

and Jig will be opened as of year 9, with the continuation of the mining operations in Cetate

The closing of the pits and of the stockpiles will be done progressively, the stockpile of

Cetate starting with year 5, the stockpile and pit of Carnic as of year 9, and the pits of Orlea

and Jig in the years 12-14

44

Wet grinding of the crushed ore in 2 ball crushers and one semi-autogenous mill;

Leaching of the ore in a CN solution, in closed tanks; the CN solution dissolves the gold

and silver from the ore.

Gold and silver recovery from the pores of the activated charcoal, by acid washing: CN

bound to silver and gold settles in the pores of the activated charcoal, which floats in the

solution from the leaching tanks. The coal is recovered by backwash pumping, and the

gold and silver sludge is washed out from the pores with a HCl solution.

Gold and silver recovery from the gold-bearing sludge by electrolysis; the gold-bearing

sludge is purified/enriched through electrolysis.

Gold/silver melting/casting in ingots – the gold alloy is cast in ingots in an electric furnace.

CN neutralization from the process tailings before leaving the plant, using the INCO

procedure – slurry oxidation in the presence of sodium metabisulfite and copper sulfate.

The CN concentration is reduced as a result of the oxidation process.

5. Grinding

6. Leaching

7. Gold and silver

recovery on activated

charcoal

8. Electrolysis

9. Melting

10. CN neutralization

The Technological Flow in the Processing Plant

45

Tailings Management Facility

13 sites were reviewed initially

Corna Valley is the only site which fulfils all requirements:

Storage capacity;

Favorable geology;

Easy to exploit;

Low environmental impact – almost non-existent

phreatic layer

Itinerary

Designed capacity – 250 million tonnes

Necessary storage capacity – 215 million tonnes

Designed to resist earthquakes of 8 degrees Richter

Designed to resist two consecutive rainfall events, which

can occur once every 10,000 years

Slopes generally 1.75H:1V to 2H:1V (RMGC 3H:1V)

Final height 185 m + 20 m under the valley floor

Length 1,182 m

Secondary catchment dam 22 m

NGI Report: The Norwegian Geotechnical Institute

conducted a risk assessment in order to assess the safety

of the tailings dam of the Rosia Montana Project. The

assessments took into account critical scenarios,

including all possible ways in which the Corna dam could

fail in extreme situations, such as an unusually large

earthquake, which appears extremely rarely, and an

extreme 24-hour rainfall. The conclusion formulated by

the report published in April 2009 was clear: as it was

designed, the dam will be among the safest in the world.

46

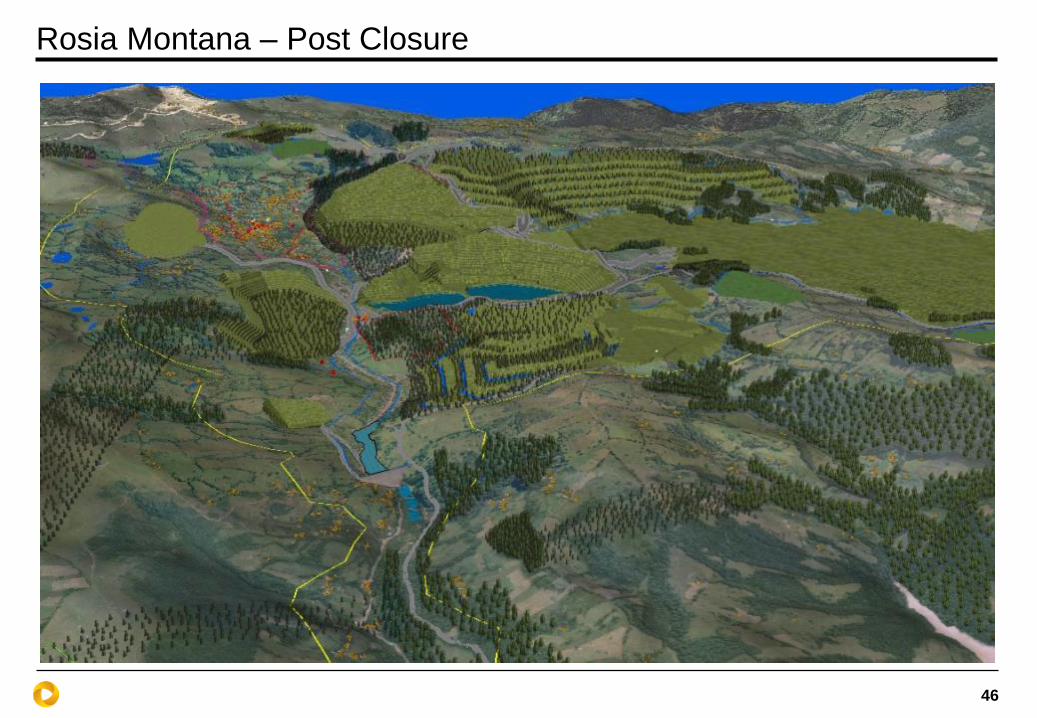

Rosia Montana – Post Closure

47

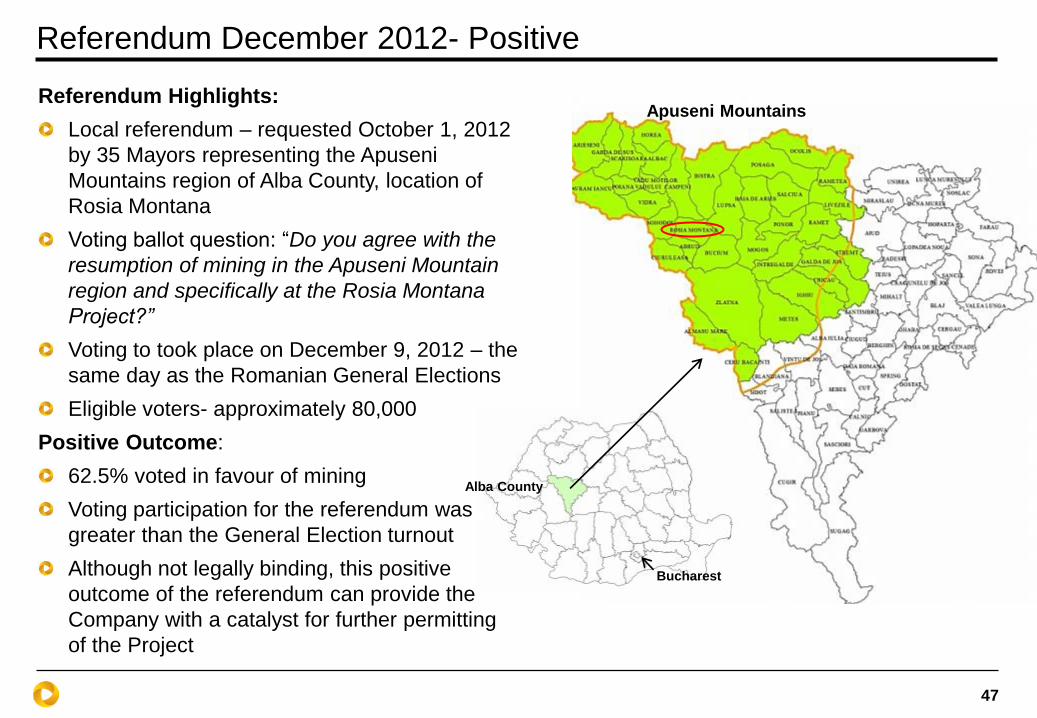

Referendum December 2012- Positive

Referendum Highlights:

Local referendum – requested October 1, 2012

by 35 Mayors representing the Apuseni

Mountains region of Alba County, location of

Rosia Montana

Voting ballot question: “Do you agree with the

resumption of mining in the Apuseni Mountain

region and specifically at the Rosia Montana

Project?”

Voting to took place on December 9, 2012 – the

same day as the Romanian General Elections

Eligible voters- approximately 80,000

Positive Outcome:

62.5% voted in favour of mining

Voting participation for the referendum was

greater than the General Election turnout

Although not legally binding, this positive

outcome of the referendum can provide the

Company with a catalyst for further permitting

of the Project

Alba County

Apuseni Mountains

Bucharest

48

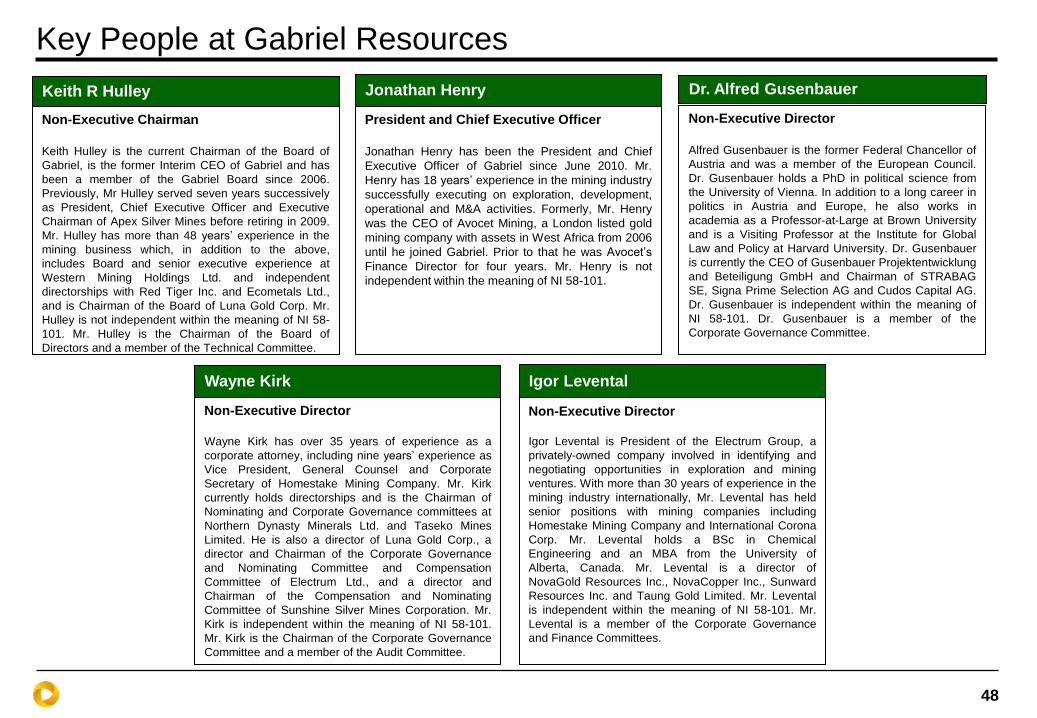

Key People at Gabriel Resources

Non-Executive Chairman

Keith Hulley is the current Chairman of the Board of

Gabriel, is the former Interim CEO of Gabriel and has

been a member of the Gabriel Board since 2006.

Previously, Mr Hulley served seven years successively

as President, Chief Executive Officer and Executive

Chairman of Apex Silver Mines before retiring in 2009.

Mr. Hulley has more than 48 years’ experience in the

mining business which, in addition to the above,

includes Board and senior executive experience at

Western Mining Holdings Ltd. and independent

directorships with Red Tiger Inc. and Ecometals Ltd.,

and is Chairman of the Board of Luna Gold Corp. Mr.

Hulley is not independent within the meaning of NI 58-

101. Mr. Hulley is the Chairman of the Board of

Directors and a member of the Technical Committee.

Keith R Hulley

President and Chief Executive Officer

Jonathan Henry has been the President and Chief

Executive Officer of Gabriel since June 2010. Mr.

Henry has 18 years’ experience in the mining industry

successfully executing on exploration, development,

operational and M&A activities. Formerly, Mr. Henry

was the CEO of Avocet Mining, a London listed gold

mining company with assets in West Africa from 2006

until he joined Gabriel. Prior to that he was Avocet’s

Finance Director for four years. Mr. Henry is not

independent within the meaning of NI 58-101.

Jonathan Henry

Non-Executive Director

Alfred Gusenbauer is the former Federal Chancellor of

Austria and was a member of the European Council.

Dr. Gusenbauer holds a PhD in political science from

the University of Vienna. In addition to a long career in

politics in Austria and Europe, he also works in

academia as a Professor-at-Large at Brown University

and is a Visiting Professor at the Institute for Global

Law and Policy at Harvard University. Dr. Gusenbauer

is currently the CEO of Gusenbauer Projektentwicklung

and Beteiligung GmbH and Chairman of STRABAG

SE, Signa Prime Selection AG and Cudos Capital AG.

Dr. Gusenbauer is independent within the meaning of

NI 58-101. Dr. Gusenbauer is a member of the

Corporate Governance Committee.

Dr. Alfred Gusenbauer

Non-Executive Director

Wayne Kirk has over 35 years of experience as a

corporate attorney, including nine years’ experience as

Vice President, General Counsel and Corporate

Secretary of Homestake Mining Company. Mr. Kirk

currently holds directorships and is the Chairman of

Nominating and Corporate Governance committees at

Northern Dynasty Minerals Ltd. and Taseko Mines

Limited. He is also a director of Luna Gold Corp., a

director and Chairman of the Corporate Governance

and Nominating Committee and Compensation

Committee of Electrum Ltd., and a director and

Chairman of the Compensation and Nominating

Committee of Sunshine Silver Mines Corporation. Mr.

Kirk is independent within the meaning of NI 58-101.

Mr. Kirk is the Chairman of the Corporate Governance

Committee and a member of the Audit Committee.

Wayne Kirk

Non-Executive Director

Igor Levental is President of the Electrum Group, a

privately-owned company involved in identifying and

negotiating opportunities in exploration and mining

ventures. With more than 30 years of experience in the

mining industry internationally, Mr. Levental has held

senior positions with mining companies including

Homestake Mining Company and International Corona

Corp. Mr. Levental holds a BSc in Chemical

Engineering and an MBA from the University of

Alberta, Canada. Mr. Levental is a director of

NovaGold Resources Inc., NovaCopper Inc., Sunward

Resources Inc. and Taung Gold Limited. Mr. Levental

is independent within the meaning of NI 58-101. Mr.

Levental is a member of the Corporate Governance

and Finance Committees.

Igor Levental

49

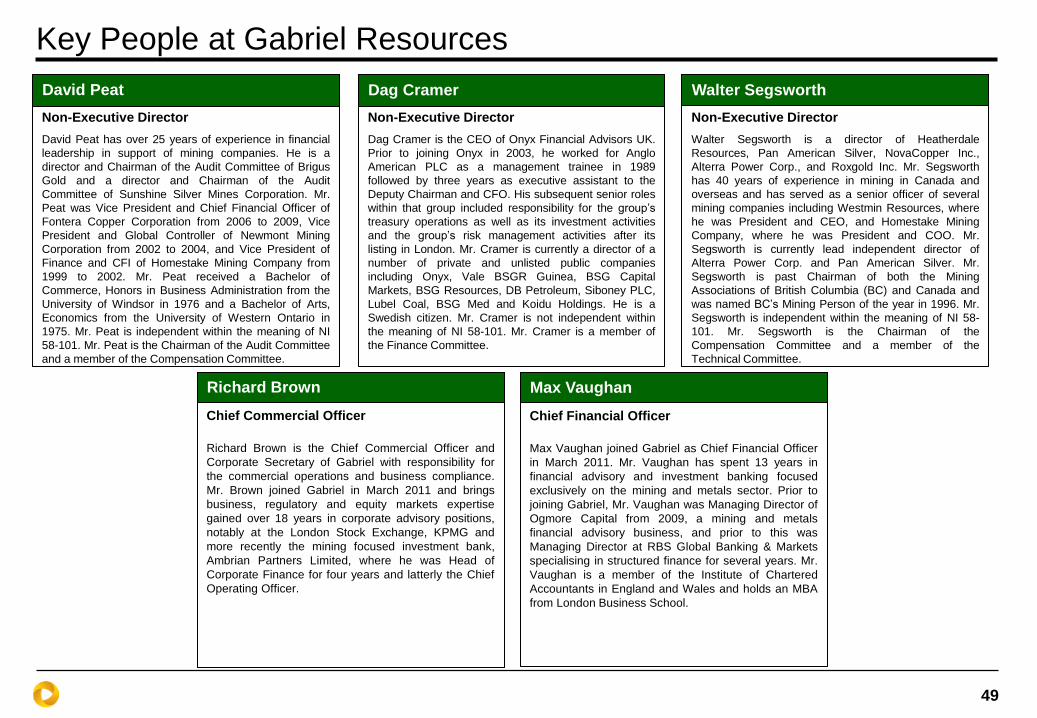

Key People at Gabriel Resources

Non-Executive Director

David Peat has over 25 years of experience in financial

leadership in support of mining companies. He is a

director and Chairman of the Audit Committee of Brigus

Gold and a director and Chairman of the Audit

Committee of Sunshine Silver Mines Corporation. Mr.

Peat was Vice President and Chief Financial Officer of

Fontera Copper Corporation from 2006 to 2009, Vice

President and Global Controller of Newmont Mining

Corporation from 2002 to 2004, and Vice President of

Finance and CFI of Homestake Mining Company from

1999 to 2002. Mr. Peat received a Bachelor of

Commerce, Honors in Business Administration from the

University of Windsor in 1976 and a Bachelor of Arts,

Economics from the University of Western Ontario in

1975. Mr. Peat is independent within the meaning of NI

58-101. Mr. Peat is the Chairman of the Audit Committee

and a member of the Compensation Committee.

David Peat

Non-Executive Director

Dag Cramer is the CEO of Onyx Financial Advisors UK.

Prior to joining Onyx in 2003, he worked for Anglo

American PLC as a management trainee in 1989

followed by three years as executive assistant to the

Deputy Chairman and CFO. His subsequent senior roles

within that group included responsibility for the group’s

treasury operations as well as its investment activities

and the group’s risk management activities after its

listing in London. Mr. Cramer is currently a director of a

number of private and unlisted public companies

including Onyx, Vale BSGR Guinea, BSG Capital

Markets, BSG Resources, DB Petroleum, Siboney PLC,

Lubel Coal, BSG Med and Koidu Holdings. He is a

Swedish citizen. Mr. Cramer is not independent within

the meaning of NI 58-101. Mr. Cramer is a member of

the Finance Committee.

Dag Cramer

Non-Executive Director

Walter Segsworth is a director of Heatherdale

Resources, Pan American Silver, NovaCopper Inc.,

Alterra Power Corp., and Roxgold Inc. Mr. Segsworth

has 40 years of experience in mining in Canada and

overseas and has served as a senior officer of several

mining companies including Westmin Resources, where

he was President and CEO, and Homestake Mining

Company, where he was President and COO. Mr.

Segsworth is currently lead independent director of

Alterra Power Corp. and Pan American Silver. Mr.

Segsworth is past Chairman of both the Mining

Associations of British Columbia (BC) and Canada and

was named BC’s Mining Person of the year in 1996. Mr.

Segsworth is independent within the meaning of NI 58-

101. Mr. Segsworth is the Chairman of the

Compensation Committee and a member of the

Technical Committee.

Walter Segsworth

Chief Commercial Officer

Richard Brown is the Chief Commercial Officer and

Corporate Secretary of Gabriel with responsibility for

the commercial operations and business compliance.

Mr. Brown joined Gabriel in March 2011 and brings

business, regulatory and equity markets expertise

gained over 18 years in corporate advisory positions,

notably at the London Stock Exchange, KPMG and

more recently the mining focused investment bank,

Ambrian Partners Limited, where he was Head of

Corporate Finance for four years and latterly the Chief

Operating Officer.

Richard Brown

Chief Financial Officer

Max Vaughan joined Gabriel as Chief Financial Officer

in March 2011. Mr. Vaughan has spent 13 years in

financial advisory and investment banking focused

exclusively on the mining and metals sector. Prior to

joining Gabriel, Mr. Vaughan was Managing Director of

Ogmore Capital from 2009, a mining and metals

financial advisory business, and prior to this was

Managing Director at RBS Global Banking & Markets

specialising in structured finance for several years. Mr.

Vaughan is a member of the Institute of Chartered

Accountants in England and Wales and holds an MBA

from London Business School.

Max Vaughan

50

Key People at RMGC

General Manager RMGC

Mr. Tánase joined RMGC in February 2008, coming from the largest cable communications operator in Romania, UPC. Within UPC, Mr. Tánase coordinated the merger of two large cable operators, UPC and Astral, which combined employed a workforce of 3,600 people and held the position of CFO for 7 years. Previously, Mr. Tánase - an expert in financial management - worked in financial and business consultancy, first at the Ministry of Finance and then with Arthur Andersen.

Dragos Tanase

Senior Vice-President Governmental Affairs

and Community Relations

Mr. Suciu began working for RMGC in 2006, initially as a Legal Manager, then as a Legal Director, and subsequently as a Legal Vice-President. In June 2009, Mr. Suciu became Senior Vice-President in charge of coordinating the Legal and Community Relations Departments, as well as the team managing the dialogue with the governmental institutions responsible for assessing the mining project.

Nicolae Suciu

Vice-President Environment

Mr. Avram has been Vice-President of Environment at RMGC since January 2007, and was previously Environmental Monitoring Officer (2003-2006) and then Environment Director (2006-2007) of RMGC. His main responsibilities include coordinating the project permitting process in terms of environmental protection and drafting RMGC's environmental strategy and policy. Between 1996 and 2003, Mr. Avram occupied various positions in the governmental sector, being responsible for environmental matters.

Horea Avram

Vice-President Patrimony and Sustainable

Development

Mr. Gligor has been working for RMGC since 2002 in the Patrimony department, which he has been running since 2005. He has also been in charge of the sustainability strategy since 2008. Mr. Gligor is responsible for identifying the best solutions for the preservation and valorisation of the cultural heritage from Rosia Montana, within the context of the mining project. Mr. Gligor graduated from "1 decembrie 1918" University of Alba Iulia, specialising in history-archaeology. Mr. Gligor is now completing his PhD within the same University.

Adrian Gligor

Vice-President Communication

Mrs. Plesa joined RMGC in June 2008 to develop and coordinate RMGC's internal and external communication strategy, and transform RMGC into a communicative company, open for dialogue with all relevant stakeholders. Mrs. Plesa has 15 years of experience in marketing, communication and lobbying, and her professional achievements include the creation and consolidation of UPC Romania's reputation, from the third position of the cable communication market to market leadership.

Andreea Plesa

Vice-President Human Resources

Mr. Mátáuan joined RMGC in September 2010 and coordinates RMGC's HR and Social Responsibility (CSR) activities. With 20 years of experience in human resources management, Mr. Mátáuan held for the last ten years the position of Human Resources and Public Relations Director of Lafarge Romania, a world leader in building materials industry. Mr. Mátáuan is a graduate of the Commerce Faculty within the Academy of Economic Studies in Bucharest and holds a PhD degree in sociology from the University of Bucharest.

Gabriel Măţăuan

Top Related