Languages

Pages

Legal

FUND ACCOUNTING UPDATEFUND ACCOUNTING UPDATE

Focus on Private Equity FundsFocus on Private Equity Funds

19 October 200619 October 2006

Outline

Discuss

Overview of US GAAP for PE Funds

Similarities and differences IFRS/UK GAAP/US GAAP

Valuation Issues

SPV’s: Disclosure Issues

Questions

Overview of US GAAP

• ‘Accounting Principles Generally Accepted in the United States of America’

• One of the two most widely used sets of global accounting standards

• Characteristics are:– Industry Focused (eg Accounting and Audit Guide: Investment Companies)– Very Detailed (you never become an expert in US GAAP you need to focus)– A vast number of different organisations participate in the setting of accounting

rules.– Those organisations include:

» FASB (Financial Accounting Standards Board)

» AICPA (American Institute of Certified Public Accountants)

» SEC (Securities & Exchange Commission)

» Other Regulatory Bodies (eg NASD, SBA, FDIC)

» Government (GASB)

Part 1 – Overview of US GAAP

Question : Which of these organisations have set rules which are applicable to me?

From the FASB website:

‘Since 1973, the Financial Accounting Standards Board (FASB) has been the designated organization in the private sector for establishing standards of financial accounting and reporting. Those standards govern the preparation of financial reports. They are officially recognized as authoritative by the Securities and Exchange Commission….’

‘The Securities and Exchange Commission (SEC) has statutory authority to establish financial accounting and reporting standards for publicly held companies under the Securities Exchange Act of 1934. Throughout its history, however, the Commission’s policy has been to rely on the private sector for this function to the extent that the private sector demonstrates ability to fulfil the responsibility in the public interest.’

Answer : Start with the standards set/endorsed by the FASB.

Part 1 – Overview of US GAAP

Question : Okay…but what are those standards?

The FASB Standards

The FASB is a board of seven full time members from the accounting, finance and other professions. They are supported by a staff of 68

The final product of most technical projects undertaken by the FASB is a Statement of Financial Accounting Standards (SFAS).

The last SFAS to be issued was SFAS 155 ‘Accounting for Certain Hybrid Financial Instruments an amendment of FASB Statements No. 133 and 140’

Certain technical projects may result in other standards. For Example

FASB Interpretations (FIN) – These are interpretations of existing GAAP (eg FIN 46 Consolidation of Variable Interest Entities an interpretation of ARB 51)

Accounting Research Bulletins (ARB) – These are accounting standards established by the AICPA Accounting Standards Executive Committee prior to the creation of the FASB which have not yet been superseded by a FASB pronouncement (eg ARB 51)

Part 1 - Overview of US GAAP

Question : Okay…but what are those standards?

Other standard setters

AICPA

The AICPA’s Accounting Standards Executive Committee (AcSEC) establishes task forces which develop industry specific guidance such as:

• Accounting and Audit Guides are designed by task forces of the AcSEC to assist preparers of financial statements in specific industries in the preparation of GAAP compliant statements; and

• Statements of Position (SOP’s) which provide guidance on and amendments to the application of principles contained in the Accounting and Audit Guides (eg SOP 03-4);

The AICPA’s Auditing Standards Board established auditing standards (SAS’s) that auditors are required to comply with when auditing financial statements of private entities in accordance with US GAAS.

Part 1 – Overview of US GAAP

Question : Okay…but what are those standards?

Other standard setters

Public Company Accounting Oversight Board (PCAOB)

Established in 2002, the PCAOB regulates the auditing profession and sets standards for those auditors to follow when auditing financial statements of public companies. When it was established, it adopted all the SAS’s and has been working to develop its own standards to address particular public company audit issues.

Emerging Issues Task Force

Established in 1984, the task force was established by the FASB and aims to identify at an early stage ‘implementation and emerging issues’. An EITF consensus establishes accounting practice for specific issues. For example EITF 04-5 establishes accounting practice for ‘Determining Whether a General Partner, or the General Partners as a Group, Controls a Limited Partnership or Similar Entity When the Limited Partners Have Certain Rights’

Part 1 – Overview of US GAAP

Question : What happens if all these standards conflicts with each other?

The GAAP Hierarchy

The GAAP hierarchy is currently presented in the AICPA’s SAS 69, The Meaning of Present Fairly in Conformity With Generally Accepted Accounting Principles. It sets out the hierarchy of accounting standards that must be followed when deciding on which standards are applicable in which circumstances. The hierarchy is complex and there are plans to improve on it. The hierarchy is broadly set out as follows:

- Category A – Includes ARB’s, Accounting Principles Board Opinions (APB’s), SFAS’s, and FIN’s;

- Category B – Includes AICPA Accounting and Audit Guides and SOP’s

- Category C – Includes EITF consensuses

- Category D – Includes accepted industry best practice

Part 1 – Overview of US GAAP

Similarities and differencesIFRS/UK GAAP/US GAAP

Accounting Issue

UK GAAP IFRS US GAAP

Overall framework

Nothing fund specific Nothing fund specific AICPA Audit and Accounting Guide: Investment Companies

Presentation of financial statements

Driven by the requirements of multiple standards:

• Profit and Loss Account• Balance Sheet• Cash Flow Statement [unless small’ entity]• Statement of Total Recognised Gains and Losses• Notes to the Financial Statements

Driven by the requirements of IAS 1:

• Income Statement• Balance Sheet• Cash Flow Statement• Statement of Changes in Net Assets Attributable to Partners• Notes to the financial statements

Drive by the requirements of Chapter 7 of the Audit and Accounting Guide:

• Statement of Assets and Liabilities• Schedule of Investments• Statement of Operations• Cash Flow Statement • Notes to the financial statements• Financial Highlights (may be included in the notes)

Part 2 – Similarities and Differences

Accounting Issue

UK GAAP IFRS US GAAP

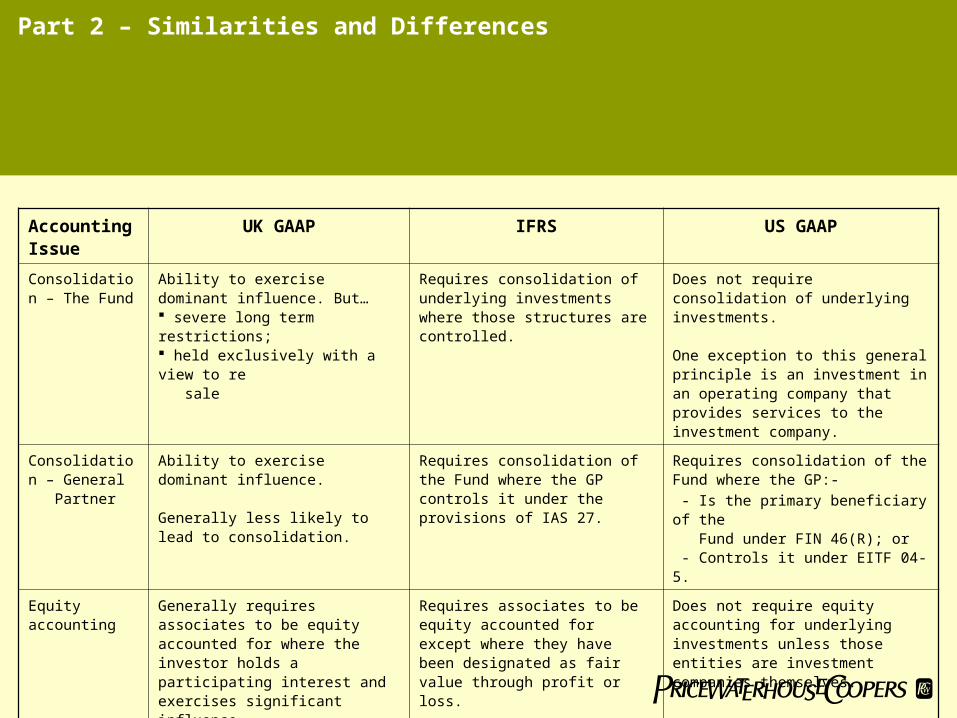

Consolidation – The Fund

Ability to exercise dominant influence. But… severe long term restrictions; held exclusively with a view to re sale

Requires consolidation of underlying investments where those structures are controlled.

Does not require consolidation of underlying investments.

One exception to this general principle is an investment in an operating company that provides services to the investment company.

Consolidation – General Partner

Ability to exercise dominant influence.

Generally less likely to lead to consolidation.

Requires consolidation of the Fund where the GP controls it under the provisions of IAS 27.

Requires consolidation of the Fund where the GP:-

- Is the primary beneficiary of the Fund under FIN 46(R); or - Controls it under EITF 04-5.

Equity accounting

Generally requires associates to be equity accounted for where the investor holds a participating interest and exercises significant influence.However, PE funds holding such investments as part of their portfolio are exempted.

Requires associates to be equity accounted for except where they have been designated as fair value through profit or loss.

Does not require equity accounting for underlying investments unless those entities are investment companies themselves.

Part 2 – Similarities and Differences

Accounting Issue

UK GAAP IFRS US GAAP

Valuation of investments

Entities required to apply FRS 26 - same as IFRS.

Other entities - less prescriptive. May carry investments as cost less any provisions for impairment.

Requires investments (designated as ‘fair value through profit or loss’ or ‘available for sale’) to be stated at fair value.

Requires investments to be stated at fair value. A new Fair Value Standard issued in September 2006 will also require, amongst other things, new disclosures around the inputs used to determine fair value.

Valuation of quoted securities

Less prescriptive – general practice is to value at quoted prices.

Requires quoted securities in active markets to be stated at bid price multiplied by the number of shares. Marketability discounts are generally not permitted.

Requires quoted securities in active markets to be stated at end of day market prices. Where a legal, contractual or regulatory restriction exists then the market price should be adjusted for the effect of the restriction (requirement of new Fair Value Standard).

Treatment of Partners’ Capital

Where the Fund has a finite life, partners’ capital is generally treated as debt under FRS 25.Applicable to all entities (not just listed)

Where the Fund has a finite life, partners’ capital is generally treated as debt under IAS 32.

Partners’ capital is generally treated as equity unless there is an obligation to redeem the capital at a specific date at a specific amount.

Part 2 – Similarities and Differences

Accounting Issue

UK GAAP IFRS US GAAP

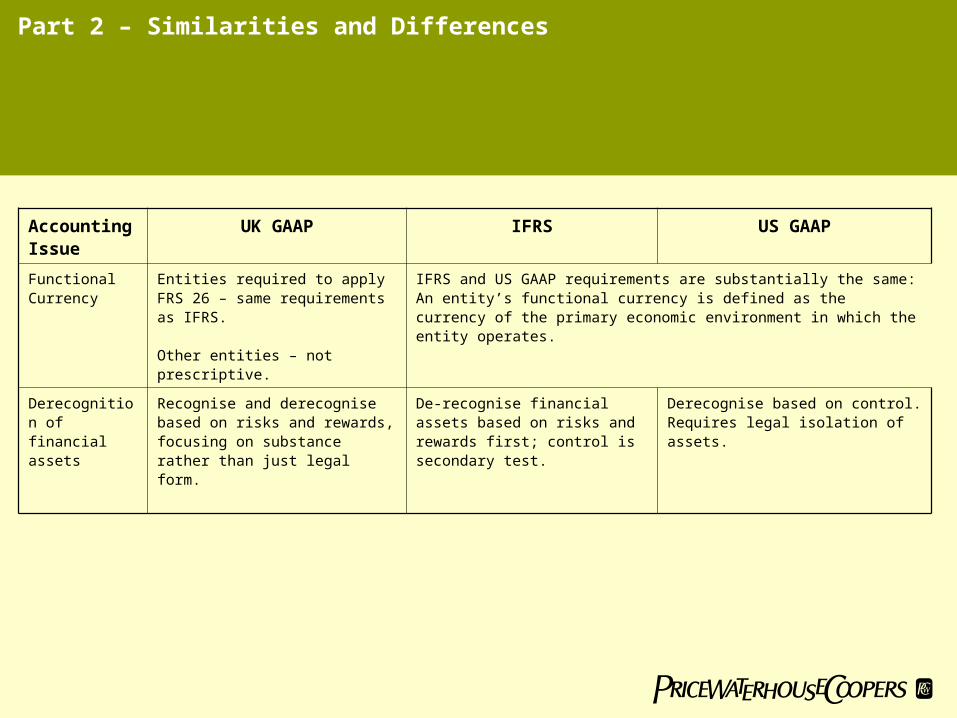

Functional Currency

Entities required to apply FRS 26 – same requirements as IFRS.

Other entities – not prescriptive.

IFRS and US GAAP requirements are substantially the same: An entity’s functional currency is defined as the currency of the primary economic environment in which the entity operates.

Derecognition of financial assets

Recognise and derecognise based on risks and rewards, focusing on substance rather than just legal form.

De-recognise financial assets based on risks and rewards first; control is secondary test.

Derecognise based on control. Requires legal isolation of assets.

Part 2 – Similarities and Differences

Fair Value - IFRS

‘the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length transaction.’

How should we calculate Fair Value?

IAS 39 is not prescriptive but recommends the following “estimation techniques”

• When a quoted market price is available– “Current bid price”

• When a quoted market price is not available– “Reference to the current market value of another instrument that is

substantially the same”– “Discounted cash flow analysis”– “Option pricing models”

Part 3 – Valuation Issues

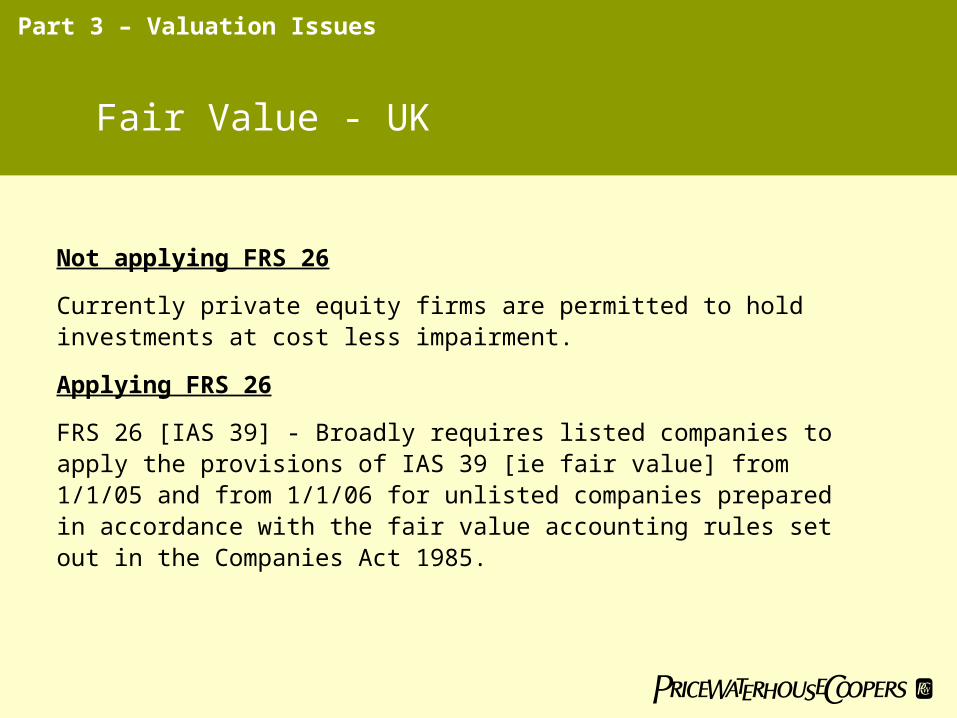

Fair Value - UK

Not applying FRS 26

Currently private equity firms are permitted to hold investments at cost less impairment.

Applying FRS 26

FRS 26 [IAS 39] - Broadly requires listed companies to apply the provisions of IAS 39 [ie fair value] from 1/1/05 and from 1/1/06 for unlisted companies prepared in accordance with the fair value accounting rules set out in the Companies Act 1985.

Part 3 – Valuation Issues

FAS 157 has the same general concept of fair value as IAS 39.

FAS 157’s objective is to use the valuation technique or combination of valuation techniques that provide the best estimate of fair value in the circumstances.

Fair value hierarchy

The standard establishes a fair value hierarchy to prioritise the inputs used in the valuation techniques:

• Level 1: Observable inputs (which are based on market data obtained from

independent sources) that reflect quoted prices (unadjusted) for identical assets in

active markets;

• Level 2: Inputs other than quoted prices included in Level 1that are observable for

the asset through corroboration with observable market data;

• Level 3: Unobservable inputs (e.g. a company’s own data).

The above hierarchy is designed to indicate the relative reliability of the fair value measures.

17

Fair Value - US

Part 3 – Valuation Issues

International Private Equity & Venture Capital Valuation Guidelines

FRS 26/IAS 39/FAS 157…..

• Require fair value accounting • Very little guidance on how to reach fair value….

The International Private Equity and Venture Capital Valuation Guidelines were developed by the BVCA, the EVCA and the AFIC (the British, European and French Venture Capital Associations) and were issued in their final form in March 2005. They have been adopted internationally by over 20 Venture Capital Associations. The guidelines are intended to provide a framework for arriving at a Fair Value for private equity and venture capital investments. The guidelines define fair value as:

‘the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length transaction.’

This is consistent with the definition contained within IAS 39.

Part 3 – Valuation Issues

Valuation methodologies: Unquoted co’s

‘The Valuer should exercise his or her judgement to select the methodology that is the most appropriate for a particular investment.’:

• Price of recent [within one year] investment - consider the background to the transaction

• Earnings multiple - an established investment with maintainable earnings

• Net Assets – value derived from assets rather than earnings [eg property holding or investment business]

• Discounted Cash Flow – flexible but subjective since many assumptions are used. Useful as a cross-check.

• Industry Valuation Benchmarks - limited situations. Useful as a cross-check.

Part 3 – Valuation Issues

Comparison to GAAP

The Valuation Guidelines state that valuers who are required to follow GAAP should do so. However:

- It gives advice on the application of marketability discounts (which generally are not permitted under GAAP).

- IAS 39 suggests the use of Discounted Cash Flow models as a valuation technique. However, the Valuation Guidelines state that DCF should only be used as a ‘cross-check’ given the number of variables involved.

Generally the IPEVC Guidelines are GAAP compliantBut be wary of advice highlight by the guidelines as non-GAAP compliant

Part 3 – Valuation Issues

SPV’s: Disclosure Issues

• Increasing use of Special Purpose Vehicles to structure Private Equity investments in a manner which is tax efficient for its investors.

• These investment structures are becoming more and more complex

• Generally, we find that the monitoring over these structures needs improvement

• Preparers of financial statements should take the following into account:

• Contingent liabilities at the SPV level may need disclosure at the fund level;

• In particular, loan arrangements put in place at the SPV level may need disclosure at the fund level;

• Transactions undertaken by the SPV may dilute the value of the fund’s investment.

Part 4 – SPV’s: Disclosure Issues

Questions

Top Related