Languages

Pages

Legal

Foreign Exchange Markets

and Exchange Rates

Foreign Exchange Markets

• A network of systems and mechanisms through which currencies are traded

• Market actors:• Banks • Brokers (Brokerage firms)• Business entities (merchants, corporations, etc.) • Individuals • Governments • Central banks • International organizations

Foreign Exchange Rates

• A foreign exchange rate is the price of (one unit of) a currency in terms of another currency

• There are nearly 200 currencies of which few than 50 are commonly traded internationally

• Most currency trades take place in the form of transfer of bank deposits and clear without actual currency notes changing hands

Currency Quotes

• Today: UK pound: $/Pd: 1.83 Pd/$: 0.546

Euro: $/Er: 1.25 Er/$: 0.80

• A year ago: UK pound: $/Pd: 1.64 Pd/$: 0.609

Euro: $/Er: 1.08 Er/$: 0.925

• Currency cross rates

FX and Portfolio Management

• An asset portfolio is a set or basket of assets owned by an individual or a business entity

• An asset has a value if it brings returns either in the form of incomes (earnings) or pleasure

• A portfolio containing FX denominated assets could change in value as FX rates change

Types of FX Transactions

• Spot transactions• Forward and futures transactions • Transactions in FX derivatives (options) Forward and futures transactions: Buying or

selling a certain amount of a currency at a predetermine (agreed upon) price for future delivery

Currency options: Buying and selling options to buy or options to sell specific amounts of a currency at a preset price in the future

The Reasons Behind FX Trading • Clearing transactions • Arbitrage transactions: taking advantage of rate

differentials (discrepancies) in different markets• Hedging transactions: Long and short positions

• Hedging in the spot market • Other types of hedging

• Speculation: Taking a long or a short position in a currency in the hope of profiting from a favorable change in the exchange rate

• A person having a long position in the British pound hopes to see the pound appreciate.

Hedging

• Hedging: A transaction made for the purpose of avoiding or reducing a business (FX fluctuation) risk.

Positions in FX: No position

Long position

Short position

Balanced or closed position• Hedging could be done in the spot market as well

as in other FX markets

Hedging in the Forward Market

• Suppose an American merchant has purchased five full container loads of German beer at a total price of € 150,000. She has agreed to pay for the merchandise 90 days after the merchandise is placed aboard the ship; she holds a short position in the euro.

• To close her position she can purchase €150,000 in the forward market today. That would enable her to buy the amount of euros she would need in 90 days at a pre-determined rate. The forward contract would protect her from FX risk.

FX Markets and FX Rates: How Are FX Rates Determined?

The Interest Parity Model:A note: A currency forward rate is an agreed-upon rate of exchange at which a certain amount of a currency is traded (bought or sold) on a certain (agreed-upon) day in the future.

In the forward market a currency could be at a “premium” or at a “discount”

ef - es Discount or premium (rate)= p = ----------- (12/n)

es

Discount: p < 0Premium: p > 0

I. Uncovered Interest Arbitrage

Comparing rates of returns on assets

denominated in different currencies:

Suppose:

US interest rate: 12%

UK interest rate: 16%

One-year CDs in US vs. One-year CDs in UK

Spot rate: 1.80

Expected (future) spot rate in a year: 1.70

Interest differential vs. Currency Appreciation or Depreciation

Interest differential: (i$ - i £)

%Change in e = (ee – es)/es

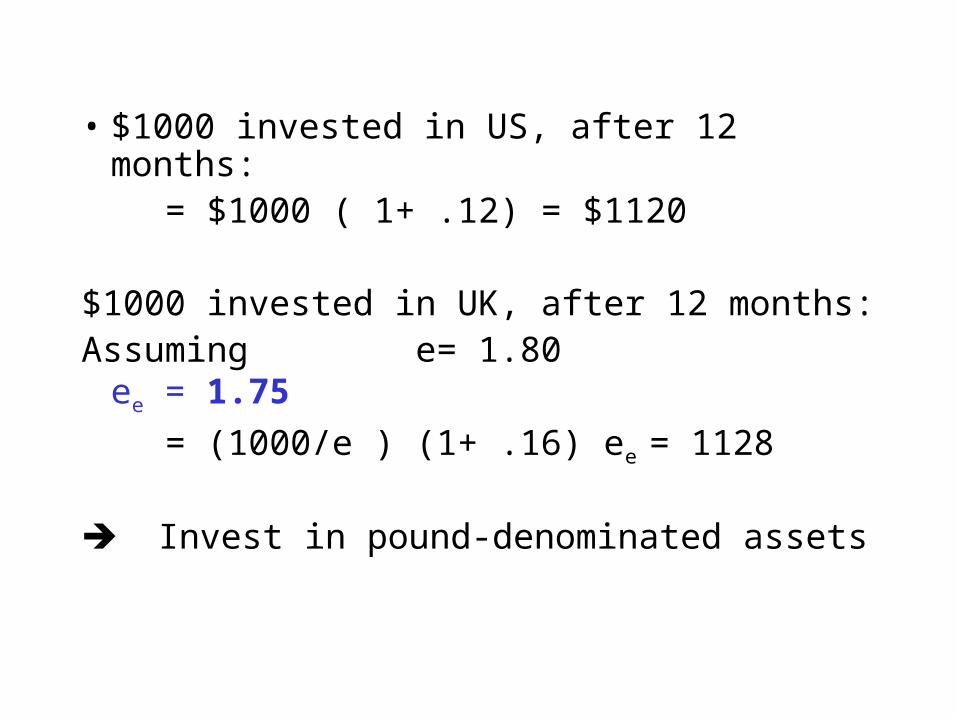

• $1000 invested in US, after 12 months: = $1000 ( 1+ .12) = $1120

$1000 invested in UK, after 12 months:

Assuming e= 1.80 ee = 1.75

= (1000/e ) (1+ .16) ee = 1128

Invest in pound-denominated assets

• $1000 invested in US, after 12 months: = $1000 ( 1+ .12) = $1120

$1000 invested in UK, after 12 months:

Assuming e= 1.80 ee = 1.70

= (1000/e ) (1+ .16) ee = 1095

Invest in pound-denominated assets

What are we comparing? • Interest in the US, i$ , and the return on a pound-

denominated asset; this return is affected not only by the UK interest rate, but also the (expected) change in the exchange rate:

That is:

i£ (ee/e) + (ee –e )/e

If i$ < i£ (ee/e) + (ee –e )/e , investors will invest in pound-denominated assets.

If i$ > i£ (ee/e) + (ee –e )/e , investors will invest in $-denominated assets.

Alternatively,

• We can compare

(i$ - i£ ) and (ee –e )/e

If (i$ - i£ ) > (ee –e )/e ,

dollar denominated assets will be chosen

At parity : (i$ - i£ ) = (ee –e )/e

Covered Interest Parity • Investing a dollar in the US at %10:

After 12 months: =$1 (1+ i$) = $1.10

• Investing the same dollar in a pound-denominated asset (at 16%) and covering in the forward market, assuming e = 1.80 and ef = 1.75:

= ($1/e) ( 1+ i£ ) ef

= (ef /e) + (ef /e) i£ = 1.127

$1 (1+ i$) < (ef /e) + (ef /e) i£

1.10 < 1.127

Or,

(1+ i$) ? (ef /e) + (ef /e) i£

Subtract 1 from both sides

i$ ? (ef /e) + (ef /e) i£- 1

i$ ? ([ef –e]/e) + (ef /e) i£

Assuming (ef /e) 1, and subtraction i£ from both sides, we write

(i$ - i£) ? ([ef –e]/e)

If (i$ - i£) < ([ef –e]/e), funds will..?

If (i$ - i£) > ([ef –e]/e), funds will..?

At parity: (i$ - i£) = ([ef –e]/e),

Does interest parity hold?

The effects of changes in i$ , i£, ee, and ef on e?

Recall: (i$ - i£ ) = (ee –e )/e

and (i$ - i£ ) = (ef –e )/e

For example, if i£ increases, other things unchanged, e must rise. ($depreciation)

Or, if ef decreases, other things unchanged, e must fall. ($appreciation)

FX Markets: Supply of and Demand for FX

• Asset Demand

• Transaction Demand

Asset demand: Recall that the return on a FX asset:

([ef –e]/e) + (ef /e) i£ or ([ee –e]/e) + (ee /e) i£, given i$, i£, ee, and ef , is inversely related to FX rate, e.

• As “e” increases the return on the FX asset decreases, making it less attractive.

Demand for and Supply of FX

0

e($/£)

D {i$, i£, ee,ef}

S

£

Shifts in the Demand Curve

• US interest rates : (-)

• UK interest rates: (+)

• The pound forward rate (+)

• The expected future £ spot rate (+)

FX Rate Regimes • Flexible (floating) rates

» Appreciation

» Depreciation

• Fixed (pegged) rates » Revaluation

» Devaluation

• Managed floating rates

• Exchange control

The Effective Exchange Rate

• A bilateral exchange rate of a currency may not reflect the real value of a currency.

• A currency may appreciate against some currencies while depreciating against others

• The effective exchange rate of a currency is a weighted index reflecting the value of a currency relative to a multiple ( basket) of other currencies. (Often the currencies of the country’s major trading partners)

Top Related