Languages

Pages

Legal

Fixed Assets: Reporting and Analyzing

Publication Date: September 2019

Fixed Assets: Reporting and Analyzing

Copyright 2019

DeltaCPE LLC

All rights reserved. Copies of this document may not be made without expressed written permission from the

author.

The author is not engaged by this text or any accompanying lecture or electronic media in the rendering of legal,

tax, accounting, or similar professional services. While the legal, tax, and accounting issues discussed in this

material have been reviewed with sources believed to be reliable, concepts discussed can be affected by changes

in the law or in the interpretation of such laws since this text was printed. For that reason, the accuracy and

completeness of this information and the author's opinions based thereon cannot be guaranteed. In addition,

state or local tax laws and procedural rules may have a material impact on the general discussion. As a result, the

strategies suggested may not be suitable for every individual. Before taking any action, all references and citations

should be checked and updated accordingly.

This publication is designed to provide accurate and authoritative information in regard to the subject matter

covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other

professional service. If legal advice or other expert advice is required, the services of a competent professional

person should be sought.

—From a Declaration of Principles jointly adopted by a committee of the American Bar Association and a

Committee of Publishers and Associations.

Table of Contents

Course Introduction .......................................................................................................................... 1

Learning Objectives ........................................................................................................................... 2

Chapter 1: Accounting for Fixed Assets ........................................................................................... 3

Learning Objectives ....................................................................................................................................3

Role of the Accountant ...............................................................................................................................3

Classification of Assets ...............................................................................................................................4

Definition of Assets .............................................................................................................................................4

Chapter 1 Section 1 - Review Questions ......................................................................................................8

The Concept of Fixed Assets........................................................................................................................9

The Nature of Fixed Assets .................................................................................................................................9

Recording Fixed Assets .................................................................................................................................... 10

Depreciation of Property, Plant, and Equipment ............................................................................................ 14

Depletion of Natural Resources ................................................................................................................ 22

Definition of Natural Resources ...................................................................................................................... 22

Units of Production Method ............................................................................................................................ 22

Nonmonetary Transactions ....................................................................................................................... 25

Chapter 1 Section 2 - Review Questions .................................................................................................... 31

Intangible Assets ...................................................................................................................................... 33

The Nature of Intangible Assets ...................................................................................................................... 33

General Rules and Concepts ............................................................................................................................ 34

Business Combination under the Acquisition Method .................................................................................... 35

Treatment of Goodwill ............................................................................................................................. 36

Impairment Test .............................................................................................................................................. 37

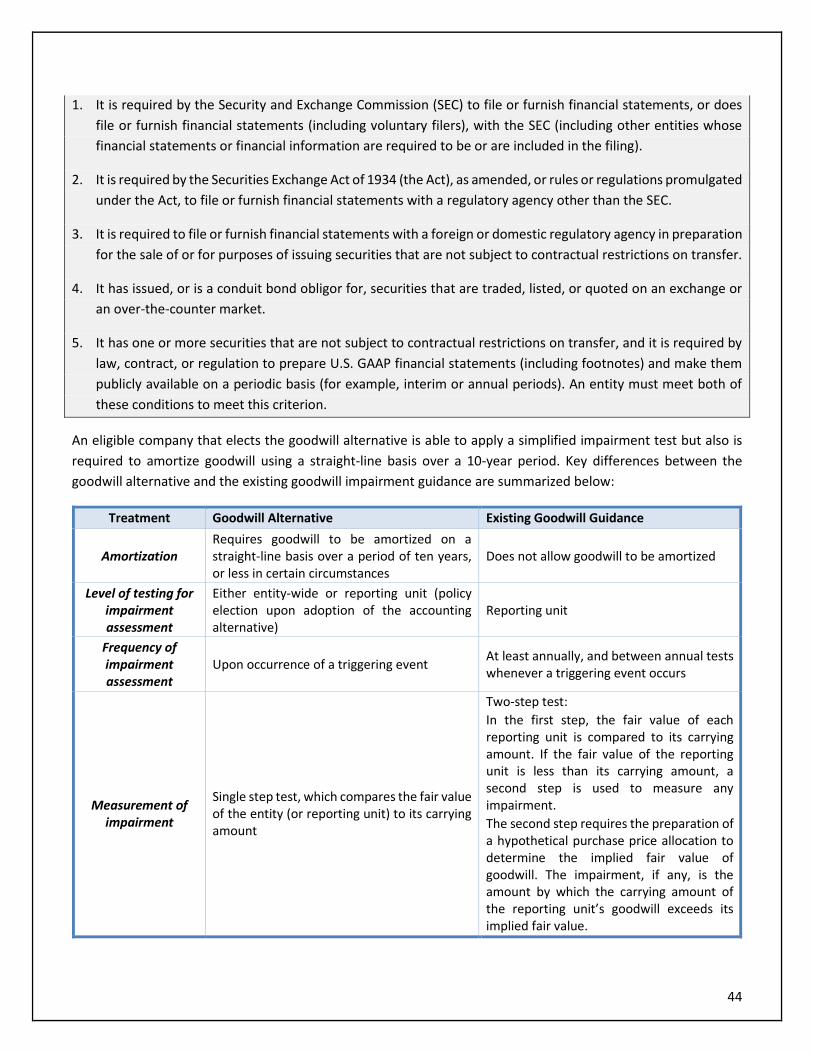

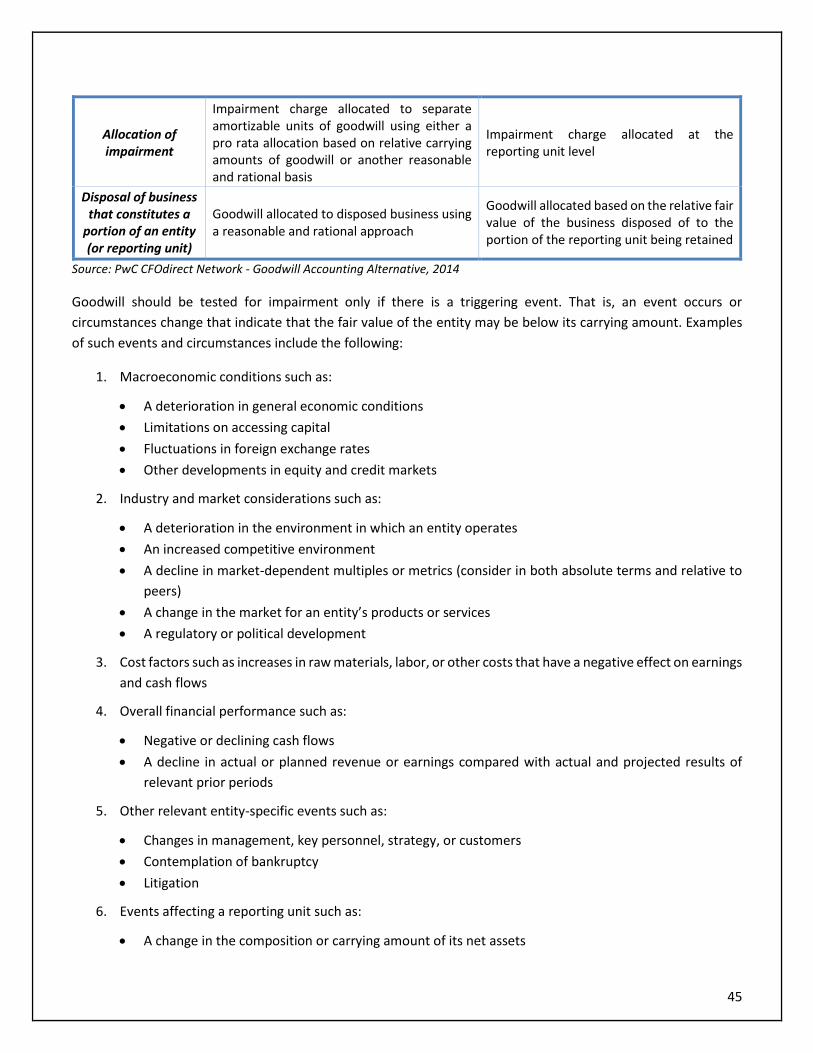

Simplifying the Impairment Test ..................................................................................................................... 41

Private Company Goodwill Alternative ........................................................................................................... 43

Capitalization of Interest .......................................................................................................................... 46

General Rules ................................................................................................................................................... 46

The Amount Capitalized .................................................................................................................................. 47

Asset Retirement Obligations ................................................................................................................... 50

Applicability ..................................................................................................................................................... 50

Requirements .................................................................................................................................................. 50

Present Value Method ..................................................................................................................................... 51

Contract Costs .......................................................................................................................................... 54

Costs to Obtain a Contract .............................................................................................................................. 54

Costs to Fulfill a Contract ................................................................................................................................ 55

Accounting Change in Estimated Useful Lives ............................................................................................ 58

Disclosures ............................................................................................................................................... 60

General Requirements..................................................................................................................................... 60

Intangible Assets .............................................................................................................................................. 61

Goodwill and Other Intangible Assets ............................................................................................................. 62

Asset Retirement Obligations .......................................................................................................................... 62

Change in Estimate .......................................................................................................................................... 64

Chapter 1 Section 3 - Review Questions .................................................................................................... 65

U.S. GAAP vs. IFRS .................................................................................................................................... 67

Property, Plant and Equipment ....................................................................................................................... 67

Intangible Assets and Goodwill ....................................................................................................................... 71

Not-for-Profit Organization: Non-Cash Gifts .............................................................................................. 73

General Rules ................................................................................................................................................... 73

Recognition of In-Kind Contributions .............................................................................................................. 73

Expiration of Donor-Imposed Restrictions ...................................................................................................... 74

Government Fixed Assets ......................................................................................................................... 74

General Rules for Fixed Assets ........................................................................................................................ 75

Works of Art and Historical Treasures ............................................................................................................. 76

Treatment for Leased Assets ........................................................................................................................... 77

Chapter 1 Section 4 - Review Questions .................................................................................................... 79

Chapter 2: Fixed Assets - Controls ................................................................................................. 80

Learning Objectives .................................................................................................................................. 80

Top Fixed Assets Issues ............................................................................................................................. 80

Vulnerability of Fixed Assets ........................................................................................................................... 80

The Risks of Spreadsheets ............................................................................................................................... 81

Overpayment of Property Taxes and Insurance .............................................................................................. 82

Implementation of Strong Controls ........................................................................................................... 83

Control Design Principles ................................................................................................................................. 83

Basic Control Techniques ................................................................................................................................ 84

Leveraging Technology .................................................................................................................................... 88

Audit Readiness ....................................................................................................................................... 90

Audit Focus for the Fixed Asset Process .......................................................................................................... 90

The Typical Audit Approach ............................................................................................................................. 91

Internal Controls Self-Assessment ................................................................................................................... 93

Chapter 2 - Review Questions ................................................................................................................... 98

Chapter 3: Planning and Analyzing ................................................................................................. 99

Learning Objectives .................................................................................................................................. 99

The Concept of Capital Budgeting ............................................................................................................. 99

Significance of Capital Budgeting Decisions .................................................................................................... 99

The Definition of Capital Budgeting .............................................................................................................. 100

Types of Long-Term Investment Decisions .................................................................................................... 100

Features of Investment Projects ................................................................................................................... 101

The Uses of Capital Budgeting ....................................................................................................................... 101

Techniques for Evaluating Investment Proposals ..................................................................................... 102

Discount Rate ................................................................................................................................................ 102

Payback Period Method ................................................................................................................................ 105

Discounted Payback Period ........................................................................................................................... 106

Accounting Rate of Return ............................................................................................................................ 107

Net Present Value .......................................................................................................................................... 108

Internal Rate of Return .................................................................................................................................. 109

Profitability Index .......................................................................................................................................... 110

Chapter 3 Section 1 – Review Questions ................................................................................................. 111

Income Taxes and Investment Decisions ................................................................................................. 112

MACRS and Investment Decisions ........................................................................................................... 114

Working with Ratios ............................................................................................................................... 118

Rate of Return on Total Assets (ROA) ............................................................................................................ 118

Fixed Asset Turnover ..................................................................................................................................... 118

The Lease vs. Purchase Decision .............................................................................................................. 119

Implications for the Lessee ............................................................................................................................ 119

Loan Benefits ................................................................................................................................................. 123

Chapter 3 Section 2 - Review Questions .................................................................................................. 126

Glossary ........................................................................................................................................ 127

Index ............................................................................................................................................ 130

Solutions to Review Questions ...................................................................................................... 131

Chapter 1 Section 1 - Review Questions .................................................................................................. 131

Chapter 1 Section 2 - Review Questions .................................................................................................. 132

Chapter 1 Section 3 - Review Questions .................................................................................................. 134

Chapter 1 Section 4 - Review Questions .................................................................................................. 136

Chapter 2 - Review Questions ................................................................................................................. 137

Chapter 3 Section 1 – Review Questions ................................................................................................. 139

Chapter 3 Section 2 - Review Questions .................................................................................................. 141

1

Course Introduction

Fixed assets can compose a significant amount of the total assets in many companies. For example, fixed assets

usually account for 35-50% of Fortune 500 companies’ total assets and represent the majority of capital

investments for most of the companies. These assets are necessary for companies to operate and, in many cases,

the efficient use of these assets determines the amount of profit that companies will earn. Fixed Assets: Reporting

and Analyzing is designed to address the key accounting principles and concepts of fixed assets and share

meaningful insights and techniques that help accounting professionals build a solid foundation to achieve greater

efficiency. To maximize efficiency, accountants must answer the following questions:

• What are the basic accounting rules and requirements for recording, reporting and disclosing fixed assets?

• How do I properly account for intangible assets and assess goodwill?

• What are the key differences between IFRS and GAAP affecting the reporting of fixed assets?

• What are the top fixed asset issues and how do I address them?

• What are the internal controls for safeguarding valuable assets?

• How can I be “audit-ready” for fixed assets? What are the targeted audit areas and common audit findings?

• How do I make optimal long-term investment decisions regarding fixed assets?

• What are the various aspects of the lease/buy decisions and considerations of new lease accounting

standards?

The content of this course includes the following chapters, which will provide guidance related to these questions

and many more integral questions connected with this topic:

1. Accounting for Fixed Assets: This chapter discusses the concept of fixed assets and accounting rules for major

activities such as acquisition of assets, nonmonetary transactions, depreciation of plant assets, depletion of

natural resources, intangible assets requirements, treatment of goodwill, capitalized interest, asset

retirement obligations, accounting changes in estimated useful life, and disclosure requirements. It also

discusses key differences between IFRS and GAAP affecting fixed assets.

2. Fixed Assets - Controls: This chapter covers the top fixed assets issues including their vulnerable nature, the

risks of spreadsheets, and the impact of ghost assets. It also identifies controls to address these issues. Key

high-risk audit areas and typical audit approach are discussed to help accountants prepare for audits. It

includes an “Audit Checklist” and “Internal Controls Self-Assessment” checklist, which assist companies to be

audit-ready.

3. Planning and Analyzing: This chapter introduces the general concepts behind capital budgeting. It discusses

and illustrates six methods for selecting the best alternatives among capital projects. The risk-return trade-off

method shown in this chapter is one way to help us come to grips with uncertainty. It also describes various

aspects of the lease/buy decisions, lease analysis, and the impact of new lease accounting standards.

This course can be used by accounting professionals as a roadmap to build a well-structured process; from

reporting and controlling to optimizing valuable assets.

2

Learning Objectives

Upon completion of this course, you will be able to:

1. Identify the characteristics of fixed assets

2. Recognize the impact of fixed assets and depreciation on financial statements

3. Identify the various types of depreciation methods

4. Identify the procedures for amortizing intangible assets

5. Recognize the concept of capitalized interest

6. Recognize how to account for asset retirement obligations

7. Identify the impact of accounting changes in depreciation method

8. Identify the disclosures required in the financial statements regarding fixed assets

9. Recognize key differences between IFRS and GAAP fixed asset reporting requirements

10. Identify the top issues and control activities related to fixed assets

11. Recognize common testing procedures for fixed asset audits

12. Identify the different techniques used to evaluate business investments and their applications

13. Recognize various aspects of lease vs. buy decisions

14. Identify the primary types of leases

3

Chapter 1: Accounting for Fixed Assets

Learning Objectives

Upon completion of this chapter, you will be able to:

• Identify the characteristics of fixed assets

• Recognize the impact of fixed assets and depreciation on financial statements

• Identify the various types of depreciation methods

• Identify the procedures for amortizing intangible assets

• Recognize the concept of capitalized interest

• Recognize how to account for asset retirement obligations

• Identify the impact of accounting changes in depreciation method

• Identify the disclosures required in the financial statements regarding fixed assets

• Recognize key differences between IFRS and GAAP fixed asset reporting requirements

Role of the Accountant

Fixed assets, such as plant, and manufacturing equipment, can compose a significant amount of the total assets

of most companies. The accounting department (AD) is involved in almost all decisions regarding the company's

fixed assets, from pre-acquisition planning to the ultimate disposal or sale of those assets. For example, the

accountant investigates all the benefits, both financial and intangible, and compares these benefits to the costs.

By determining whether or not the assets, such as equipment or plant, will be a good investment for the company,

the AD assists the company in making sound strategic business decisions. In addition, to operate a profitable

business, management must have information regarding the current location, use, condition, and future

usefulness of its assets. The AD is responsible for ensuring that a system is in place to provide the information.

Examples of fixed assets tasks performed by the AD include:

• Making decisions regarding the purchase, use, and disposal of assets

• Developing a fixed assets tracking process

• Protecting the fixed assets through internal control and assuring proper insurance coverage

• Determining the value of the asset and the period over which it will extend benefits to the company

• Recording the acquisition of, changes to, and disposal of fixed assets

4

• Providing necessary reports to both management and custodians

Classification of Assets

A clear and correct understanding of the basic divisions of the assets, what they represent and the amounts at

which they should be recorded is essential for a proper perspective of financial position of a business.

Definition of Assets

An asset is a resource controlled by an entity as a result of past events and from which future economic benefits

are expected to flow to the entity. ‘Future economic benefits’ refers to the capacity of an asset to benefit the

entity by being:

• Exchanged for something else of value to the enterprise;

• Used to produce something of value to the enterprise, or

• Used to settle its liabilities

The future economic benefits of assets usually result in net cash inflows to the enterprise. Assets are recognized

in the financial statements when:

1. The item meets the definition of an asset;

2. It can be measured with sufficient reliability;

3. The information about the item is reliable

Assets may have definite physical forms such as buildings, machinery, or supplies. On the other hand, some assets

exist not in physical or tangible form, but in the form of valuable legal claims or rights, such as accounts receivables

from customers and notes receivables from debtors.

The concept of the historical cost principle, also known as the cost principle, applies to most assets. This principle

states that assets should be recorded in the accounting system at the original acquisition cost when acquired by

the company. The carrying value of these assets is adjusted for subsequent improvements, depreciation and

impairments.

Current Assets

Assets which will likely be converted into cash or realized within one year or one operating cycle, whichever is

longer, are classified as current. An operating cycle is the average time taken by a company to convert the funds

used to purchase inventory or raw materials into cash proceeds from sales to customers. Current assets include

cash and cash equivalents, short-term investments, accounts receivable, inventories, accrued revenues (assets),

and prepaid expenses.

5

Cash and Cash Equivalents

Cash and cash equivalents represents money on hand and in bank accounts as well as highly liquid securities that

generally mature in less than 90 days. Cash includes coins, checks, money orders, bank drafts, and any item

acceptable to a bank for deposit. A compensating balance arises when a bank lends funds to a customer and

requires that a minimum balance be retained at all times in the customer’s checking account. If compensating

balances are not disclosed, misleading inferences about the company’s liquidity and interest costs might be made.

Short-Term Investments

Short-term investments may include investments in marketable debt and equity securities. These investments

are short-term, low risk, highly liquid, low yield. Examples are treasury bills and commercial paper. Investments

in debt securities are classified as trading debt, available-for-sale debt, or held-to-maturity debt securities. Equity

securities represent an ownership interest in an entity (for example, common, preferred, or other capital stock)

or the right to acquire (e.g. warrants, rights, forward purchase contracts, call options) or dispose of (e.g. put

options, forward sale contracts) an ownership interest in an entity at fixed or determinable prices.

Accounts Receivable

Accounts receivable represent amounts due from customers arising from sales of goods or services. The allowance

for doubtful accounts shown on most balance sheets is a contra asset account. The allowance represents a

reduction of the accounts receivable that is established to adjust this item to an estimate of the amount realizable.

Notes receivable are unconditional promises in writing to pay definite sums of money at certain or determinable

dates, usually with a specified interest rate.

Inventories

Inventories represent merchandise, work in process, and raw materials that a business normally uses in its

manufacturing and selling operations. Inventories are usually reported at cost or at the lower of cost or market

value. Accountants determine cost by using one of many methods, each based on a different assumption of cost

flows. Typical cost flow assumptions include the following:

1. First-in, first-out (FIFO). The costs of the first items purchased are assigned to the first items sold and the

costs of the last items purchased are assigned to the items remaining in inventory.

2. Last-in, first-out (LIFO). The costs of the last items purchased are assigned to the first items sold; the cost

of the inventory on hand consists of the cost of items from the earliest purchases. Note: IFRS does not

allow LIFO.

3. Average-cost method. Each item carries an equal cost, which is determined by dividing the total of the

goods available for sale by the number of units to arrive at an average unit cost.

4. Specific identification method. The actual cost of a particular inventory item is assigned to the item.

Major impacts of FIFO and LIFO inventory costing methods on financial statements in times of rising prices and

stable or rising inventory levels are shown here:

6

FIFO LIFO

Ending inventory Higher Lower

Current assets Higher Lower

Cost of goods sold Lower Higher

Gross profit Higher Lower

Net income Higher Lower

Taxable income Higher Lower

Income taxes Higher Lower

The major accounting objective in selecting an inventory method should be to choose the one which, under the

conditions and circumstances in practice, most clearly reflects periodic income.

Prepaid Expenses

Prepaid expenses are expenses that have been paid prior to the company’s receipt of the benefits (i.e. goods or

services). The benefits will usually be received within the next year and therefore they are classified as current

assets. Examples of prepaid expenses include prepaid rent, prepaid insurance, or prepaid advertising

Accrued Revenue

An accrued asset or accrued revenue is revenue that has been earned (i.e. the service has been performed or the

goods have been delivered) for which payment has not been received and/or that has not been recorded in the

accounts. For example, a company performs a service for a customer but has not yet billed the customer. Since

the company has earned the revenue, the company must make an entry in the accounting records to increase

accounts receivable and revenue to properly reflect this transaction.

Noncurrent Assets

Assets having a useful life of more than one year and expected to provide benefits for several years are classified

as noncurrent. Examples are long-term investments, property, plant, and equipment.

Long-Term Investments (Financial Assets)

Long-term investments in stocks, bonds, and other investments owned by a company that are to be held for a

period of time exceeding the normal operating cycle of the business or one year, whichever is longer, are classified

as investments on the balance sheet. Investments in common stock in which an investor is able to exercise

significant influence over the operating and financial policies of an investee require the use of the equity method

of accounting. An investment of between 20% and 50% in the outstanding common stock of the investee is a

presumption of significant influence. When the equity method is used, income from the investment is recorded

by the investor when it is reported by the investee. The amount of the income recognized is based on the

investor’s percentage of ownership in the investee. Dividends are recorded as reductions in the carrying value of

the investment account when they are paid by the investee. When ownership is less than 20%, the cost method

is used - the investment is recorded at cost.

7

Property, Plant, and Equipment

Property, plant, and equipment are often called plant assets or fixed assets. They represent tangible, long-lived

assets such as land, buildings, machinery, and tools acquired for use in normal business operations (and not

primarily for sale) during a period of time greater than the normal operating cycle or one year, whichever is longer.

Depreciation is recorded each year of an asset’s useful life to reduce the asset’s carrying value for the deterioration

in value (e.g. wear and tear). Depreciation methods are discussed in the “Depreciation of Property, Plant, and

Equipment” section.

Wasting Assets

Natural resources or wasting assets represent inventories of raw materials that can be consumed (exhausted)

through extraction or removal from their natural location. Natural resources include ore deposits, mineral

deposits, oil reserves, gas deposits, and timber tracts. Natural resources are classified as a separate category

within the property, plant, and equipment section. Natural resources are typically recorded at their acquisition

cost plus exploration and development cost. Natural resources are subject to depletion. Depletion is the

exhaustion of a natural resource that results from the physical removal of a part of the resource. On the balance

sheet, natural resources are reported at total cost less accumulated depletion.

Intangible Assets

Intangible assets are long-lived assets representing nonphysical rights, values, privileges, and so on - exclusive of

receivables and investments. Goodwill, patents, trademarks, trade names, copyrights, and franchise licenses are

examples of intangible assets. Goodwill is the excess of the cost of an acquired business over the value assigned

to the tangible and other identifiable intangible assets of the firm. Goodwill is recorded and reported only when

it is acquired in the purchase of a business. A franchise license is the right (acquired by paying a fee) to use another

firm’s brand name, business model, etc. to conduct business. One well known example of a business that operates

through a franchise arrangement is McDonald's.

Other Assets

Other assets are assets that cannot be classified elsewhere on the balance sheet, including prepayments for

services or benefits that will not be received within 12 months, are reported as other assets or deferred charges

and are classified as noncurrent (or long term) assets. Deferred charges include long- term bond issue costs.

Deferred charges are similar to prepaid expenses in that they both arise from advance payments. The primary

difference between these two types of assets is that the benefits from such deferred charges will be obtained

over several years whereas the benefits of prepaid expenses will generally be obtained in less than one year.

This course focuses on property, plant, equipment, natural resources, and intangible assets. It also discusses

depreciation and amortization, and techniques to allocate the cost of long-lived assets over their estimated useful

lives.

8

Chapter 1 Section 1 - Review Questions

1. What is an asset?

A. A resource with economic value that a corporation controls with the expectation that it will provide a

future benefit

B. Fees earned from selling goods or providing services

C. An obligation that may occur in the future depending on the outcome of a specific event

D. Funds from the equity holders that are made available to the company as capital contributions and

retained profits

2. Which of the following accounting principles dictates that purchased assets are initially recorded at historical cost?

A. Revenue recognition principle

B. Full disclosure principle

C. Matching principle

D. Cost principle

3. Which of the following accounts captures anything of value owned by a company?

A. Revenue

B. Owner’s equity

C. Asset

D. Liability

4. Which of the following assets is easily liquidated into cash?

A. Trademark

B. Accrued revenue

C. Building

D. Franchise license

9

The Concept of Fixed Assets

The Nature of Fixed Assets

Fixed assets are also known as Property, Plant, and Equipment. U.S. Generally Accepted Accounting Principles

(GAAP) for the accounting, reporting, and disclosures associated with fixed assets are included in ASC 360-10-50

Property, Plant and Equipment - Disclosure and ASC 360-10-35, Subsequent Measurement. Fixed assets range from

tangible equipment and vehicles to intangible copyrights or trademarks and compose more than one-half of total

assets in many corporations. These resources are expected to provide benefits over current and future accounting

periods because they are used by a company for the production or supply of goods and services, for rentals to

others, or for administrative purposes. In many cases, the efficient use of these resources determines the amount

of profit corporations will earn.

Examples of common types of fixed assets include:

Fixed Tangible Assets Fixed Intangible Assets

Assets have physical characteristics such as:

− Land

− Buildings

− Motor Vehicles

− Furniture

− Office Equipment

− Computers

− Plant and Machinery

Assets have no physical characteristics such as:

− Goodwill

− Patents

− Copyrights

− Software

− Trademarks/Trade Names

− Franchises

− Licenses

Companies buy fixed assets for long-term use in their routine business activities and do not typically intend to

resell them. Therefore, fixed assets are considered to be less liquid than current assets. For example, inventories

are not considered fixed assets because they are not long-lived and are held for sale rather than for use. What

represents a fixed asset to one company may be inventory to another. For example, a business such as a retail

store may classify a truck as a fixed asset because the truck is used to deliver merchandise whereas a business

such as a truck dealership classifies the same truck as inventory because the truck is held for sale. Land held for

speculation or not yet put into service is a long-term investment rather than a plant asset because the land is not

being used by the business.

The fixed asset life cycle begins with acquisition, continues with depreciation and maintenance and ends with

disposal. The accounting treatment of each phase is discussed in the following sections.

Acquisition DepreciationRepair &

MaintenanceDisposal

10

Recording Fixed Assets

Initial Recording

The Cost of Fixed Assets

The original cost of a depreciable asset includes more than the asset's purchase price. It takes into consideration

all of the items that can be attributed to its purchase and preparing the asset for its intended use. Therefore, cost

includes all normal, reasonable, and necessary expenditures to obtain the asset and get it ready for use, such as:

• Transportation

• Installation

• Testing, breaking in, and setup

• Assembling

• Trial runs

• Warehousing

• Sales taxes

• Title fees

• Insurance

• Commission

• Warranties

Cost of a depreciable asset = Purchase cost + Costs attributable to preparing the asset for its intended use

Generally, for purchased depreciable assets, the initial tax basis will be the same as the original cost of the asset

as defined above.

Abnormal costs are not charged to the asset but are expensed, such as for repairs of a fixed asset that was

damaged during shipment because of mishandling. If two or more assets are purchased at a lump-sum price, cost

is allocated to the assets based on their fair market values as follows:

Specific asset’s fair market value ÷ Total fair market value of all assets acquired = rate x total acquisition cost =

specific asset’s acquisition cost

EXAMPLE 1-1

AMC Inc. purchases a piece of equipment with a price tag of $30,000. The purchase also involves:

• Sales tax: $1,500

• Shipping and delivery: $450

• Set-up by contractor: $300

• Warranty: $1,000

11

For depreciation purposes, the cost of the equipment is $33,250, computed as follows:

Invoice price $30,000

Sales tax 1,500

Shipping and delivery 450

Set-up 300

Warranty 1,000

Total cost $33,250

Equipment $33,250

Cash $33,250

EXAMPLE 1-2

Beta Inc. purchased a computer, copier, and printer with a total acquisition cost of $8,000. However, the invoice

does not break down the cost of each item. How is the acquisition cost of each asset calculated?

Beta Inc. estimates the fair market value of each asset as:

Computer $ 5,000

Copier 4,000

Printer 1,000

Total fair market value $10,000

Beta Inc. computes each asset’s portion of the total $8,000 acquisition cost, as follows:

Computer: $5,000 (computer fair market value) ÷ $10,000 (total fair market value) = 0.5 x $8,000 (total acquisition

cost) = $4,000 (acquisition cost for the computer)

Copier: $4,000 (copier fair market value) ÷ $10,000 (total fair market value) = 0.4 x $8,000 (total acquisition cost)

= $3,200 (acquisition cost for the copier)

Printer: $1,000 (printer fair market value) ÷ $10,000 (total fair market value) = 0.1 x $8,000 (total acquisition cost)

= $800 (acquisition cost for the computer)

The acquisition cost of each asset, individually:

Computer $4,000

Copier 3,200

Printer 800

Total acquisition cost $8,000

12

Self-Constructed Assets

Self-constructed assets are recorded at the incremental or direct costs to build (material, labor, and variable

overhead) assuming idle capacity. Fixed overhead is excluded unless it increases because of the construction

effort. However, self-constructed assets should not be recorded at an amount in excess of the outside cost.

EXAMPLE 1-3

Incremental costs to self-construct equipment are $80,000. The equipment could be bought from an

unaffiliated third party for $76,000. The journal entry is:

Equipment $76,000

Loss 4,000

Cash $80,000

EXAMPLE 1-4

Mavis Company uses its excess capacity to build its own machinery. The associated costs are direct material

of $80,000, direct labor of $20,000, variable overhead of $10,000, and fixed overhead of $5,000. The cost

of the self-constructed machine is $110,000. The fixed overhead is excluded because it is not affected by

the construction effort.

Donation of Fixed Assets

As per ASC 958-605, a company receiving a fixed asset from a donor should record the asset at its fair value by

debiting fixed assets and crediting contribution revenue. ASC 958 states that the company donating a

nonmonetary asset recognizes an expense for the fair value of the donated asset. The difference between the

book value and fair value of the donated asset represents a gain or loss.

EXAMPLE 1-5

Harris Company donates land costing $50,000 with a fair value of $70,000. The journal entry is:

Contribution expense $70,000

Land $50,000

Gain on disposal of land 20,000

If a company pledges unconditionally to give an asset in the future, contribution expense and payable are accrued.

This includes a conditional promise where all conditions have been satisfied which, in effect, has now made the

promise unconditional. However, if the pledge is conditional, an entry is not made until the asset is, in fact,

transferred. If it is unclear whether the promise is conditional or unconditional, the former is presumed.

13

Subsequent Measurement

Expenditures incurred that increase the capacity, life, or operating efficiency of a fixed asset are capitalized.

However, insignificant expenditures are usually expensed as incurred. Additions to an existing asset are capitalized

and depreciated over the shorter of the life of the addition or the life of the original asset. Rearrangement and

reinstallation costs should be capitalized if future benefits exist. Otherwise, they should be expensed. If fixed

assets are obsolete, they should be written down to salvage value, recognizing a loss, and reclassified from

property, plant, and equipment to other assets.

Ordinary repairs such as a tune-up for a delivery truck are expensed because they only benefit less than one year.

Extraordinary repairs are capitalized to the fixed asset if they benefit more than one year. An example is a new

motor for a salesperson's automobile. Extraordinary repairs either increase the asset's life or make the asset more

useful. Capital expenditures enhance the quality or quantity of services to be obtained from the asset.

If a fixed asset is to be disposed of, it should not be depreciated. Further, it should be recorded at the lower of its

book value or net realizable value. Net realizable value equals fair value less costs to sell. Expected costs to sell

beyond one year should be discounted. Idle or obsolete fixed assets should be written down and reclassified as

other assets. The loss on the write-down is presented in the income statement.

As per ASC 410-30-25-16, Asset Retirement and Environmental Obligations: Environmental Obligations, the costs

to prevent, contain, or remove environmental contamination should be expensed. Exception: These costs can be

capitalized to the fixed asset in the following cases:

• The costs increase the asset's life or capacity or improve its efficiency or safety.

• The costs are incurred to prepare the property for sale.

According to ASC 410-30-45-6, Asset Retirement and Environmental Obligations: Environmental Obligations, the

cost to treat property bought having an asbestos problem should be deferred to the asset. Disclosure should be

made of the asbestos problem and related costs to correct.

The following table summarizes the accounting treatment for various costs incurred subsequent to the

acquisition of capitalized assets.

14

The Accounting Treatment for Costs Incurred Subsequent to the Acquisition of Capitalized Assets

Type of Expenditure Normal Accounting Treatment

Additions Capitalize cost of addition to asset account.

Improvements & Replacements

• Carrying value known: Remove cost of and accumulated depreciation on old asset, recognizing any gain or loss. Capitalize cost of improvement/replacement.

• Carrying value unknown:

1. If the existing asset's useful life is extended, debit accumulated depreciation for cost of improvement/replacement.

2. If the quantity or quality of the asset's productivity is increased, capitalize cost of improvement/replacement to existing asset account.

Rearrangement & Reinstallation

• If original installation cost is known, account for cost of rearrangement/ reinstallation as a replacement (carrying value known).

• If original installation cost is unknown and rearrangement/reinstallation cost is material in amount and benefits future periods, capitalize as an asset.

• If original installation cost is unknown and rearrangement/reinstallation cost is not material or future benefit is questionable, expense the cost when incurred.

Repairs • Ordinary: Expense cost of repairs when incurred.

• Major/material: As appropriate, treat as an addition, improvement, or replacement.

Depreciation of Property, Plant, and Equipment

General Rules

The carrying value of these assets should be systematically and gradually decreased by charging “depreciation”.

Depreciation is the decline in economic potential of fixed assets due to physical deterioration (e.g. wear, tear),

inadequacy for future needs, and normal obsolescence. When a specific asset is determined to be obsolete it is

written down or off. Land is not depreciated because its benefits do not decrease over time. However,

improvements to land, such as paving or fences, are capitalized as separate assets (i.e. not as land) and

depreciated since these improvements decrease in value and wear out over time.

The main accounting purpose of depreciation is to allocate the cost of an asset over its useful life. The use of a

plant asset in operations transforms the asset cost into an operating expense. Thus, depreciation is an operating

expense resulting from the consumption of a depreciable asset even though it does not involve cash or credit

payment. The reason for the expense is to comply with the matching principle required by accrual accounting.

According to the principle, revenue and related expenses should be recorded in the same accounting period. In

this way, sacrifices (expenses) are matched against benefits or accomplishments (revenues). This matching of

15

expenses and revenues is necessary for the income statement to present an accurate picture of the profitability

of a business.

Depreciation expense not only reduces an accounting period’s earnings but also reduces the book value of an

asset. The book value of an asset is its recorded cost less accumulated depreciation. Accumulated depreciation is

a contra asset account which represents the accumulation of depreciation charges resulting from allocating the

cost of an asset over its useful life.

Acquisition cost – Accumulated depreciation = Book value

Depreciation for each asset is usually computed separately based on the following factors:

1. The cost of an asset

2. The estimated useful life of an asset

3. The salvage value of an asset

4. The method of depreciation used

Although companies are free to choose from several methods to calculate depreciation expense, companies

should apply depreciation methods that closely reflect the operations’ economic circumstances in accordance

with accounting theory. Therefore, companies should select methods that systematically and rationally allocate

asset cost to accounting periods according to benefits received from the use of the assets. Some companies select

one method for certain assets and other methods for other assets. It should also be noted that companies may

use a different depreciation method (or basis or life/recovery period) for tax purposes than they use for book

purposes. When this occurs, deferred tax assets or liabilities must be calculated, recorded and reflected in the

financial statements. A detailed discussion of deferred taxes is beyond the scope of this course.

The Asset’s Estimated Useful Life and Salvage Value

An asset’s useful life is the estimated number of years that the company expects the asset to last or the amount

of production it expects from the machine measured in operating hours, units produced, miles, or other standards.

For instance, a machine’s life may be measured in years, units produced, or hours operated. A vehicle is usually

measured in miles driven or years of use. Although there is no predetermined useful life under U.S. GAAP, general

guidelines that are frequently used include:

• Land – Not a depreciable asset

• Land improvements – 15 years

• Buildings – 30-40 years

• Computer equipment – 5 years

• Furniture and equipment – 10 years

• Software – 3 years

For tax purposes, the Internal Revenue Service (IRS) dictates the allowable depreciation methods and the recovery

period/depreciable life for each asset category.

16

The salvage value (residual value) is an estimated amount that a company expects the asset to be worth at the

end of its useful life. This amount cannot be depreciated. The depreciable base equals the acquisition cost minus

the salvage value.

Acquisition cost – Salvage value = Depreciable base

Methods of Depreciation

Among the commonly used depreciation methods are straight-line and accelerated methods. The two major

accelerated methods are sum-of-the-years'-digits (SYD) and double-declining-balance (DDB). Each of these

methods is explained below.

Straight-Line Method

Most companies use the straight-line method for financial statement purposes because this method is the

simplest to compute, results in fewer errors, and the amount is consistent each year. This method is most

appropriate when an asset's usage is uniform from period to period, as is the case with furniture. The annual

depreciation expense is calculated by using the following formula:

Depreciation Expense = Cost - Salvage Value

Number of Years of Useful Life

EXAMPLE 1-6

An auto is purchased for $20,000 in Year 1 and has an expected salvage value of $2,000. The auto's estimated life

is 8 years. Its annual depreciation is calculated as follows:

Depreciation Expense = $20,000 - $2,000

= $2,250/year 8 Years

An alternative means of computation is to multiply the depreciable cost ($18,000) by the annual depreciation rate,

which is 12.5 percent in this example. The annual rate is calculated by dividing the number of years of useful life

into one (1/8 = 12.5%). The result is the same: $18,000 x 12.5% = $2,250.

Sum-of-the-Years'-Digits (SYD) Method

Under this method, depreciation charges are highest in the initial years and decrease over the useful life of the

asset. To calculate the percentage to be taken each year, use the number of years of life expectancy in reverse

order as the numerator, and sum of the digits as the denominator. For example, if the life expectancy of a machine

is 8 years, write the numbers in reverse order: 8, 7, 6, 5, 4, 3, 2, 1. The sum of these digits is 36, or (8 + 7 + 6 + 5 +

4 + 3 + 2 + 1). Thus, the fraction for the first year is 8/36, while the fraction for the last year is 1/36. The sum of

17

the eight fractions equals 36/36, or 1. Therefore, at the end of 8 years, the machine is completely written down

to its salvage value. The following formula may be used to quickly find the sum-of-the-years' digits (S):

S = (N)(N+1)

2 N represents the number of years of expected useful life

EXAMPLE 1-7

Using the information from Example 1-6, the depreciable cost is $18,000 ($20,000 - $2,000). Using the SYD

method, the computation for each year's depreciation expense is:

S = (N)(N+1)

= 8(9)

= 36 2 2

Year Fraction x Depreciable Cost = Depreciation Expense

1 8/36 $18,000 $4,000

2 7/36 18,000 3,500

3 6/36 18,000 3,000

4 5/36 18,000 2,500

5 4/36 18,000 2,000

6 3/36 18,000 1,500

7 2/36 18,000 1,000

8 1/36 18,000 500

Total $18,000

Double-Declining-Balance (DDB) Method

Under this method, depreciation expense is highest in the earlier years and lower in later years. First, a

depreciation rate is determined by doubling the straight-line rate. For example, if an asset has a useful life of 10

years, the straight-line rate is 1/10 or 10 percent, and the double-declining rate is 20 percent. Second,

depreciation expense is computed by multiplying the rate by the book value of the asset at the beginning of each

year. Since book value declines over time, the depreciation expense decreases each successive period. This

method ignores salvage value in the computation. However, the book value of the fixed asset at the end of its

useful life cannot be below its salvage value.

EXAMPLE 1-8

Assume the data in Example 1-6. Since the straight-line rate is 12.5 percent (1/8), the double-declining-balance

rate is 25% (2 x 12.5%). The depreciation expense is computed as follows:

18

Year

Book Value at Beginning of Year x Rate (%) = Depreciation Expense Year-end Book Value

1 $20,000* 25% $5,000 $15,000

2 15,000 25% 3,750 11,250

3 11,250 25% 2,813 8,437

4 8,437 25% 2,109 6,328

5 6,328 25% 1,582 4,746

6 4,746 25% 1,187 3,559

7 3,559 25% 890 2,669

8 2,669 25% 667 2,002

*Note: The Book Value at the Beginning of Year 1 is equal to cost which is $20,000 in this example.

If the original estimated salvage value had been $2,100 instead of $2,000, the depreciation expense for the eighth

year would have been $569 ($2,669 - $2,100) rather than $667, since the asset cannot be depreciated below its

salvage value.

Units of Production Method

The units-of-production depreciation method allocates asset cost based on the level of production. As production

varies, so will the depreciation expense. Each unit is charged with a constant amount of depreciation equal to the

cost of the asset minus salvage value, divided by the total units expected to be produced.

Depreciation per unit = Cost - Salvage Value

Estimated total units that can be produced in the asset's lifetime

Depreciation = Units of output for year x Depreciation per unit

EXAMPLE 1-9

The cost of a machine is $11,000 with a salvage value of $1,000. The estimated total units are 5,000. The units

produced in the first year are 400.

Depreciation per unit = $11,000 - $1,000

= $2 per unit

5,000

Depreciation in year 1 = 400 units x $2 = $800

19

Journal Entries

The following table lists typical fixed asset journal entries.

Fixed Assets xxx

Cash/Accounts Payable xxx

Purchase of fixed assets

Depreciation Expense xxx

Accumulated Depreciation xxx

Record Depreciation

Cash xxx

Accumulated Depreciation xxx

Fixed Assets xxx

Gain on Disposal xxx

Gain on sale of asset

Cash xxx

Accumulated Depreciation xxx

Loss on Disposal xxx

Fixed Assets xxx

Loss on sale of asset

Accumulated Depreciation xxx

Fixed Asset xxx

To remove a fully depreciated asset with no salvage value

If a company fails to capitalize a fixed asset at the correct amount, this error will affect the company’s income

statement and balance sheet. If a company does not capitalize the full purchase amount, or capitalizes too much,

the balance sheet will be under or over stated as a result of the error. Since depreciation expense is calculated

based on the asset’s recorded value and directly effects the calculation of net income, the valuation error will

impact the income statement as well.

Other Considerations

Purchase during the Year

If a fixed asset is bought during the year, the annual depreciation amount will need to be prorated to reflect the

number of months the asset was in service.

20

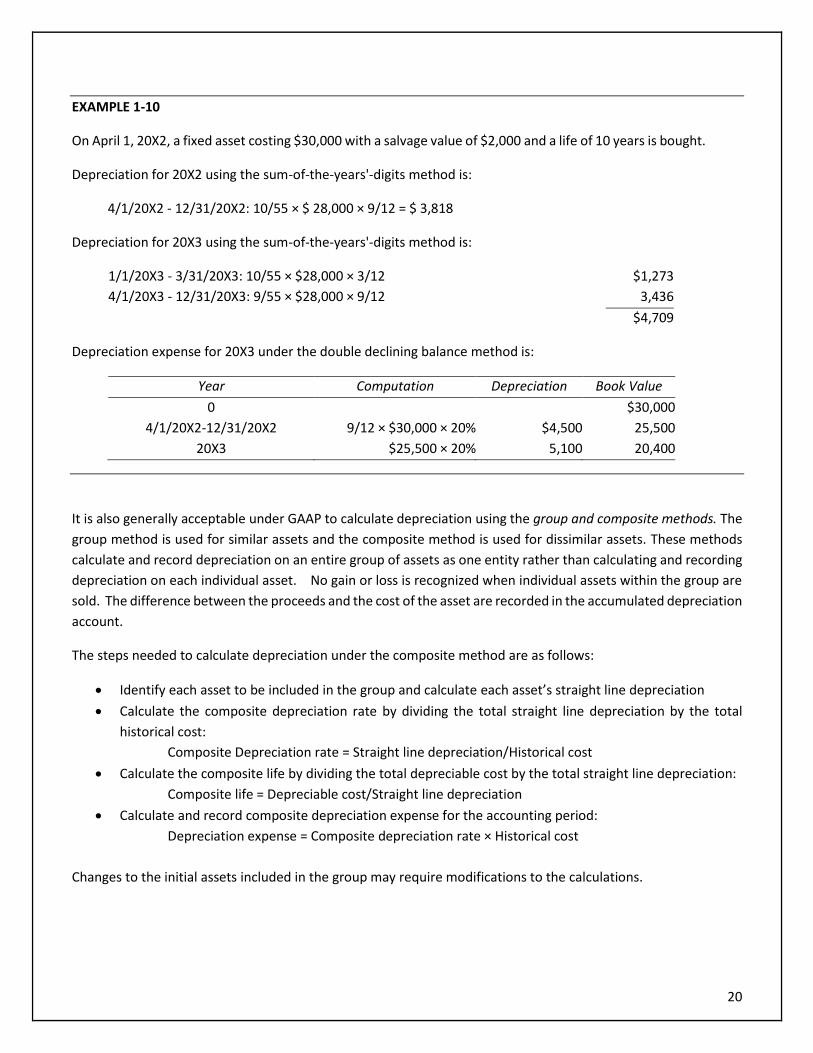

EXAMPLE 1-10

On April 1, 20X2, a fixed asset costing $30,000 with a salvage value of $2,000 and a life of 10 years is bought.

Depreciation for 20X2 using the sum-of-the-years'-digits method is:

4/1/20X2 - 12/31/20X2: 10/55 × $ 28,000 × 9/12 = $ 3,818

Depreciation for 20X3 using the sum-of-the-years'-digits method is:

1/1/20X3 - 3/31/20X3: 10/55 × $28,000 × 3/12 $1,273

4/1/20X3 - 12/31/20X3: 9/55 × $28,000 × 9/12 3,436

$4,709

Depreciation expense for 20X3 under the double declining balance method is:

Year Computation Depreciation Book Value

0 $30,000

4/1/20X2-12/31/20X2 9/12 × $30,000 × 20% $4,500 25,500

20X3 $25,500 × 20% 5,100 20,400

It is also generally acceptable under GAAP to calculate depreciation using the group and composite methods. The

group method is used for similar assets and the composite method is used for dissimilar assets. These methods

calculate and record depreciation on an entire group of assets as one entity rather than calculating and recording

depreciation on each individual asset. No gain or loss is recognized when individual assets within the group are

sold. The difference between the proceeds and the cost of the asset are recorded in the accumulated depreciation

account.

The steps needed to calculate depreciation under the composite method are as follows:

• Identify each asset to be included in the group and calculate each asset’s straight line depreciation

• Calculate the composite depreciation rate by dividing the total straight line depreciation by the total

historical cost:

Composite Depreciation rate = Straight line depreciation/Historical cost

• Calculate the composite life by dividing the total depreciable cost by the total straight line depreciation:

Composite life = Depreciable cost/Straight line depreciation

• Calculate and record composite depreciation expense for the accounting period:

Depreciation expense = Composite depreciation rate × Historical cost

Changes to the initial assets included in the group may require modifications to the calculations.

21

EXAMPLE 1-11

Computations under the composite depreciation method follow:

Asset Historical Cost Salvage

Depreciable

Cost /Life =

Straight Line

Depreciation

X $ 50,000 $10,000 $ 40,000 10 $ 4,000

Y 80,000 4,000 76,000 5 15,200

Z 104,000 8,000 96,000 6 16,000

$234,000 $22,000 $212,000 $35,200

Composite depreciation rate = Straight Line Depreciation/Historical Cost = $35,200/$234,000 = 15%

Composite life = Depreciable cost/Straight Line Depreciation

= $212,000/$35,200 = 6 years

Composite annual depreciation = Composite rate x historical cost = .15 x $234,000 = $35,100

The entry to record depreciation is:

Depreciation expense $35,100

Accumulated depreciation $35,100

The journal entry to record the sale of asset X for $43,000 is:

Cash $43,000

Accumulated depreciation 7,000

Fixed asset $50,000

Which Method to Use

• At the end of the useful life of the fixed asset, the total depreciation charges will be the same regardless of

whether straight-line or accelerated depreciation is used for both book and tax purposes; only the timing of

the tax savings will differ. If assets are disposed of before the end of their useful life, the gain or loss on the

disposition will differ depending on the depreciation method used.

• The depreciation method used for financial reporting purposes should be realistic for that type of fixed asset.

For example, depreciation on an automobile may be based on mileage.

• For IRS reporting, companies generally must use MACRS (Modified Accelerated Cost Recovery System). It is

the primary depreciation method for claiming a tax deduction. The depreciation rate used varies depending

on the type of asset being depreciated. Consult the IRS depreciation tables and literature for more

information. Details of MACRS are discussed in chapter 2 “MACRS and Investment Decisions” section.

22

Depletion of Natural Resources

Definition of Natural Resources

Natural resources are wasting assets, such as petroleum, timber, and minerals. They are characterized as being

subject to complete removal and being replaced only by an act of nature. Natural resources are subject to

depletion. Depletion is the physical exhaustion of a natural resource from usage. It is a process of allocating the

cost of the natural resource over its anticipated life and is similar to depreciation except that it relates to a natural

resource instead of a fixed asset.

Units of Production Method

The most common method of recording depletion for accounting purposes is the units of production method. An

estimate of how much of the natural resource will be extracted in terms of tons, barrels, units, or other measures

is required to calculate depletion. The cost of the natural resource is divided by the total recoverable units to

arrive at the depletion per unit. Depletion expense equals the units extracted for the year multiplied by the

depletion per unit. A change in estimate requires the use of a new depletion rate per unit. Depletion expense is

presented in the income statement; accumulated depletion reduces the carrying value of the natural resource in

the noncurrent asset section of the balance sheet. In some cases, depletion is charged to inventory (or cost of

sales). For example, if depletion on a coal mine equals $20,000, the entry would be to debit coal inventory (or cost

of sales) for $20,000 and credit accumulated depletion (or land rights) for $20,000.

The basis on which depletion is computed is called the depletion base. The depletion base is generally made up

of three components, consisting of the following:

1. Acquisition cost of the depletable property: Property may be acquired in hope of finding natural resources

or may already have been determined to have proved resources on it. Alternatively, the property may

also be leased, with subsequent royalties being paid to the owner if resources are found on it.

2. Exploration costs: When the rights to explore the property are secured (through acquisition or lease),

exploration costs are incurred to determine the existence of natural resources. For most natural

resources, the costs of exploration are expensed in the period in which they are incurred. However, for

certain industries, such as oil-and gas-producing enterprises, certain specialized guidelines prevail. For

example, oil and gas entities may choose between the successful efforts method and the full cost method

of accounting for exploration costs. In the successful efforts approach, only those exploratory costs

related to successful wells are capitalized. Exploratory costs related to unsuccessful wells are expensed.

In the full cost method, exploratory costs related to both successful wells and unsuccessful wells are

capitalized as part of the depletion base.

3. Development costs: These are the costs incurred in extracting the natural resource from the ground,

making it ready for production or sale. Costs incurred on machinery and equipment that can be used for

different wells or mines are generally not considered part of the depletable base and should be separately

depreciated as they are utilized. On the other hand, intangible costs incurred on specific wells or mines

which cannot benefit to any other well or mine should be considered part of that resource's depletion

23

base. Such costs primarily include the costs incurred to dig, physically secure, and utilize the wells, mines,

tunnels, shafts.

In general, the components of the depletion base of a natural resource upon which depletion should be computed

include:

• Acquisition costs

• Capitalized exploratory costs, and

• Development costs

After a depletable asset has been fully consumed, local, state, and federal laws may require that the company pay

for any restoration costs that may be required so that the residual property that remains does not represent a

detriment to the local area in which it is situated. Estimated restoration costs represent a negative salvage value

that should be added to the components of the depletion base of the natural resource. The property's estimated

salvage value should, of course, be subtracted from the depletion base in computing depletion expense.

EXAMPLE 1-12

In January 20X7, LevSe Company incurred costs of $3,500,000 in connection with the acquisition of a mineral mine.

In addition, $200,000 of development costs were incurred in preparing the mine for production. It is estimated

that 1,200,000 tons of ore will be removed from the mine over its useful life, at which point it is estimated that

the company can sell the property for $250,000. After all the ore has been extracted, it is estimated that it will

cost the company $100,000 to restore it to an acceptable level as required by law. During 20X7, 30,000 tons of

ore were extracted and sold. On its 20X7 income statement, what amount should LevSe report as depletion?

DEPLETION BASE

Acquisition cost $3,500,000

Development costs 200,000

Restoration costs—negative salvage value 100,000

Estimated salvage value (250,000)

Depletion base $3,550,000

20X7 production 30,000 tons

Depletion rate: $3,550,000/1,200,000 tons $ 2.96/ton

Depletion—20X7 $2.96 × 30,000 tons $ 88,800

24

The annual report of International Paper Company in Exhibit 1-1 shows an acceptable disclosure. It uses

condensed balance sheet data supplemented with details and policies in notes to the financial statements.

EXHIBIT 1-1: Disclosures for Property, Plant, Equipment, and Natural Resources International Paper Company

Consolidated Balance Sheet In millions at December 31 20X7 20X6 Assets Total current assets $ 6,735 $ 8,637 Plants, properties and equipment, net 10,141 8,993 Forestlands 770 259 Investments 1,276 641 Goodwill 3,650 2,929 Assets held for exchange 1,324

Deferred charges and other assets 1,587 1,251

Total assets $24,159 $24,034

Note 1 (partial)

Plants, Properties and Equipment - Plants, properties and equipment are stated at cost, less accumulated depreciation. Expenditures for betterments are capitalized, whereas normal repairs and maintenance are expensed as incurred. The units-of-production method of depreciation is used for major pulp and paper mills, and the straight-line method is used for other plants and equipment. Annual straight-line depreciation rates are, for buildings-2 1/2% to 8 1/2%, and for machinery and equipment-5% to 33%.

Forestlands. At December 31, 20X7, International Paper and its subsidiaries owned or managed about 300,000 acres of forestlands in the United States, approximately 250,000 acres in Brazil, and through licenses and forest management agreements, had harvesting rights on government-owned forestlands in Russia. Costs attributable to timber are charged against income as trees are cut. The rate charged is determined annually based on the relationship of incurred costs to estimated current merchantable volume.

Note 11 (partial)

Plants, properties and equipment by major classification were:

In millions at December 31 20X7 20X6

Pulp, paper and packaging facilities Mills $18,579 $16,665 Packaging plants 5,205 5,093 Other plants, properties and equipment 1,262 1,285

Gross cost 25,046 23,043 Less: Accumulated depreciation 14,905 14,050

Plants, properties and equipment, net $10,141 $ 8,993

25

Nonmonetary Transactions

General Requirements

Nonmonetary transactions involve the exchange of nonmonetary assets, such as inventories, plant and

equipment, or property. In general, in a nonmonetary exchange, the asset received is recorded at the amount

given up for it. Typically, this would include the fair value of the asset given up plus any cash paid. If cash is

received, the amount of fair value given up is reduced. In addition, a gain or loss may be recognized on the transfer

or disposal. The gain or loss is the difference between the fair value and book value of the asset given up.

Nonmonetary transactions may or may not have commercial substance. If a transaction has commercial

substance, a gain or loss on the disposal is fully recognized. However, if the transaction lacks commercial

substance, then a loss is always recognized but a gain may or may not be recognized based on the circumstances.

The latter situation is more complicated and is discussed further below.

In general, in exchanges of nonmonetary assets, if the fair value of the asset given up is not reliably measurable,

then the fair value of the asset received should be used. Also in this case, if a transaction has commercial

substance, fair value is used to measure the value of the asset acquired. ASC 845-10-50-1 requires note disclosure

for a period in which an entity engages in one or more nonmonetary exchanges that includes a description of the

nature of the transaction(s), the method used to account for transferred assets, and the gain or loss on the

exchanges. ASC 845-10-05-6 addresses nonmonetary transactions and covers the accounting for exchanges or

distributions of fixed assets.

Determining Commercial Substance

Commercial substance occurs when future cash flows change as a result of an exchange of nonmonetary assets

resulting in the modification of the economic positions of the two parties involved.

EXAMPLE 1-13

X Company exchanges machinery for Y Company's land. It is probable that the timing and dollar amount of cash

flows from the land received will be materially different from the equipment's cash flows. Hence, both companies

now have different economic positions indicating an exchange with commercial substance.

Even in the case of an exchange of similar assets (machine for a machine), a change in economic position may

occur. Assuming that the life of the machine received is much longer than that of the machine given up, the cash

flows for the machines can be materially different. Consequently, there is commercial substance to the transaction

and fair value should be used as the measurement basis for the machine received in the exchange. On the other

hand, if the difference in cash flows is not significant, the company is still in the same economic position as before

and a loss is recognized immediately and the measurement basis of the asset received will be equal to the basis

in the asset given up plus or minus cash received or paid. However, as noted above, a gain is recognized in only

certain circumstances.

26

Business entities must analyze the cash flow features of the assets exchanged to ascertain whether there is

commercial substance to the transaction. In determining whether future cash flows change:

1. Analyze cash flows before and after the exchange and compare them or

2. Determine whether the timing, amount, and risk of cash flows resulting from the asset received are

different from the cash flows of the asset given up.

Another consideration is whether the value of the asset received differs from that transferred, and whether the

difference is significant relative to the fair values of the assets exchanged.

Commercial Substance Exists

Following is an example of the calculations and entries related to a nonmonetary exchange when commercial

substance exists..

EXAMPLE 1-14

XYZ Company exchanged autos plus cash for land. The autos have a fair value of $100,000. They cost $130,000

with accumulated depreciation of $50,000 so the book value is $80,000. Cash paid is $35,000. The cost of the land

to XYZ equals:

Fair value of autos exchanged $100,000

Cash paid 35,000

Cost of land $135,000

The journal entry to record the exchange transaction is:

Land $135,000

Accumulated depreciation—autos 50,000

Autos $130,000

Cash 35,000

Gain on disposal of autos 20,000

The gain equals the fair value of the autos less their book value as computed below:

Fair value of autos—given up $100,000

Book value

Cost of autos $130,000

Less: accumulated depreciation 50,000 80,000

Gain $ 20,000

However, if the autos had a fair value of $78,000 rather than $100,000, there would be a loss recognized of $2,000

($80,000 less $78,000). In either situation, the company is in a different economic position and thus the

transaction has commercial substance. Hence, a gain or loss is recognized.

27

EXAMPLE 1-15

ABC Company exchanges its old equipment for new. The used equipment has a book value of $40,000 (cost

$60,000 less accumulated depreciation of $20,000) with a fair value of $30,000. The list price of the new

equipment is $80,000. The trade-in allowance is $45,000. Assuming that commercial substance exists, cash to be

paid equals:

List price of new equipment $80,000

Less: trade-in allowance 45,000

Cash to be paid $35,000

The cost of the new equipment equals:

Fair value of old equipment—given up $30,000

Cash due 35,000

Cost of new equipment $65,000

The journal entry to record this exchange transaction is:

Equipment $65,000

Accumulated depreciation 20,000

Loss on disposal of equipment 10,000

Equipment—old $60,000

Cash 35,000

The loss is computed as follows:

Fair value of old equipment $30,000

Book value of old equipment 40,000

Loss $10,000

Commercial Substance Does Not Exist

Because assets should not be valued in excess of their fair value, a loss is recognized immediately when the fair

value of the asset given up in an exchange is greater than its book value instead of being added to the cost of the

newly acquired asset. Exchanges lacking commercial substance may occur in the real estate industry for example,

when there is a “swap” of real estate properties.

When a transaction lacks commercial substance, and a loss occurs, it is fully recognized. However, ASC 845-10-25-