Languages

Pages

Legal

Financing Public Colleges and Universities in an Era of State Fiscal Constraints

1

Edith F. Behr, Vice President/Senior Credit Officer Moody’s Higher Education & Not-for-Profit Team [email protected]

Higher Education Government Relations Conference November 30, 2011

2 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Agenda

Ratings as Window into Public University Financial Risk Mixed sector credit outlook vs. stable ratings? Quantitative data vs. analyst judgment

Public University Business Model Fundamentally Changed Market-driven with a public mission, not government-driven Greater financial stability under student pay-market driven model Means-tested tuition pricing is consistent with public mission Bond market/donors replace state as main capital source

Where are we headed? Governance, management, market strategy key drivers Greater professionalism and efficiency Better disclosure to investors, students, donors, regulators

Questions and Discussion

3 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Ratings as Window into Public University Financial Risk

4 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

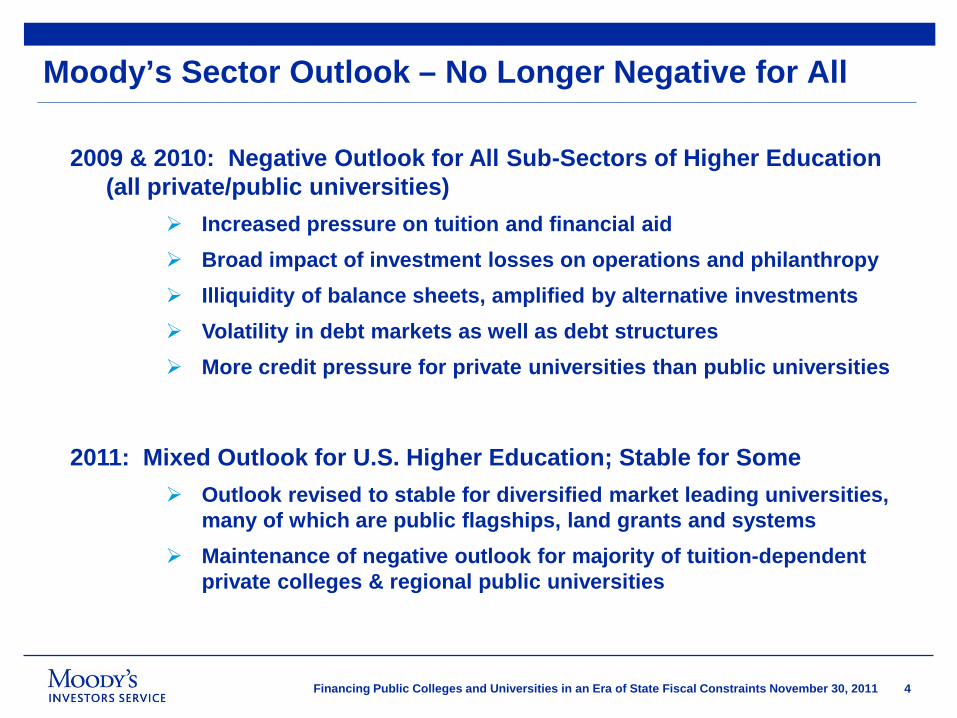

Moody’s Sector Outlook – No Longer Negative for All

2009 & 2010: Negative Outlook for All Sub-Sectors of Higher Education (all private/public universities)

Increased pressure on tuition and financial aid Broad impact of investment losses on operations and philanthropy Illiquidity of balance sheets, amplified by alternative investments Volatility in debt markets as well as debt structures More credit pressure for private universities than public universities

2011: Mixed Outlook for U.S. Higher Education; Stable for Some Outlook revised to stable for diversified market leading universities,

many of which are public flagships, land grants and systems Maintenance of negative outlook for majority of tuition-dependent

private colleges & regional public universities

5 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

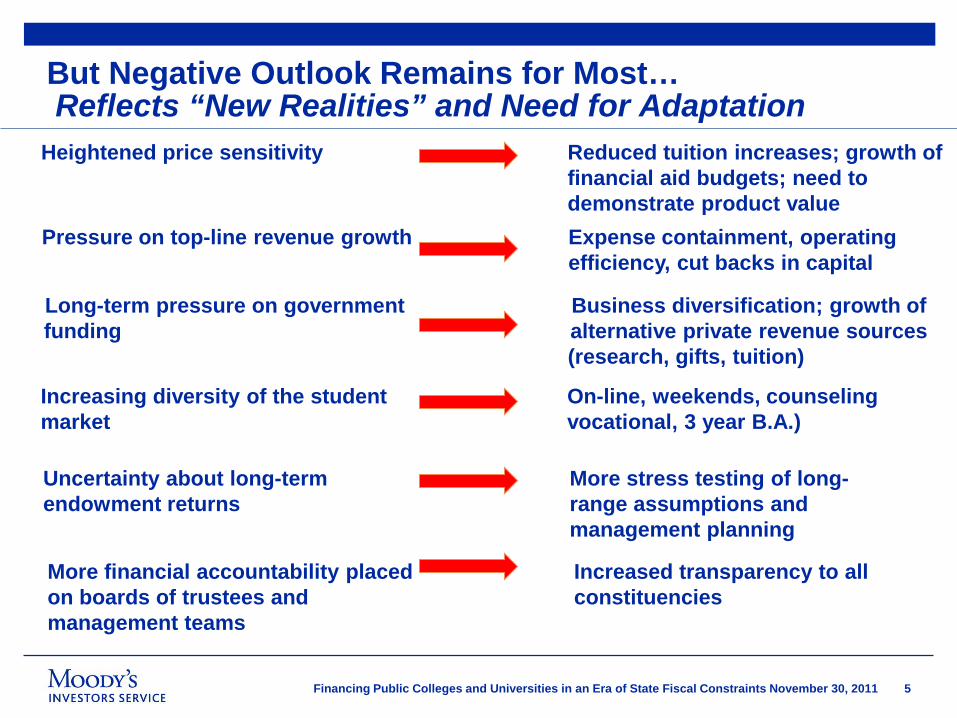

But Negative Outlook Remains for Most… Reflects “New Realities” and Need for Adaptation

Heightened price sensitivity Reduced tuition increases; growth of financial aid budgets; need to demonstrate product value

Pressure on top-line revenue growth Expense containment, operating efficiency, cut backs in capital

Long-term pressure on government Business diversification; growth of funding alternative private revenue sources

(research, gifts, tuition)

Increasing diversity of the student On-line, weekends, counseling market vocational, 3 year B.A.)

Uncertainty about long-term More stress testing of long-endowment returns range assumptions and management planning

More financial accountability placed Increased transparency to all on boards of trustees and constituencies management teams

6 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

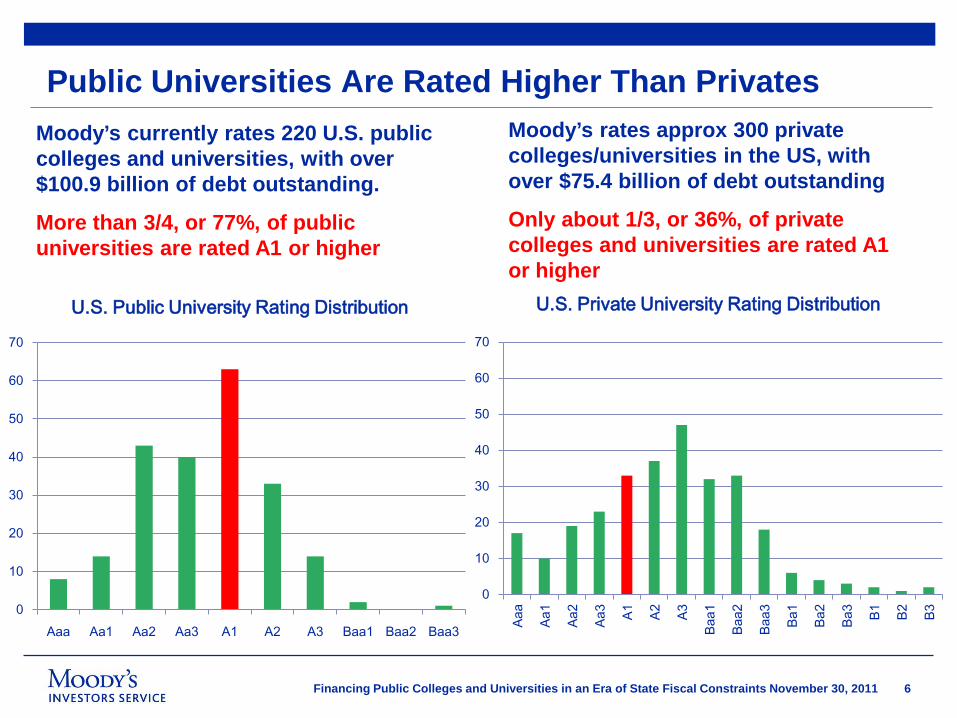

Public Universities Are Rated Higher Than Privates Moody’s rates approx 300 private

colleges/universities in the US, with over $75.4 billion of debt outstanding

Only about 1/3, or 36%, of private colleges and universities are rated A1 or higher

0

10

20

30

40

50

60

70

Aaa Aa1 Aa2 Aa3 A1 A2 A3 Baa1 Baa2 Baa3

U.S. Public University Rating Distribution

Moody’s currently rates 220 U.S. public colleges and universities, with over $100.9 billion of debt outstanding.

More than 3/4, or 77%, of public universities are rated A1 or higher

0

10

20

30

40

50

60

70

Aaa

Aa1

Aa2

Aa3 A1

A2

A3

Baa1

Baa2

Baa3

Ba1

Ba2

Ba3 B1

B2

B3

U.S. Private University Rating Distribution

7 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

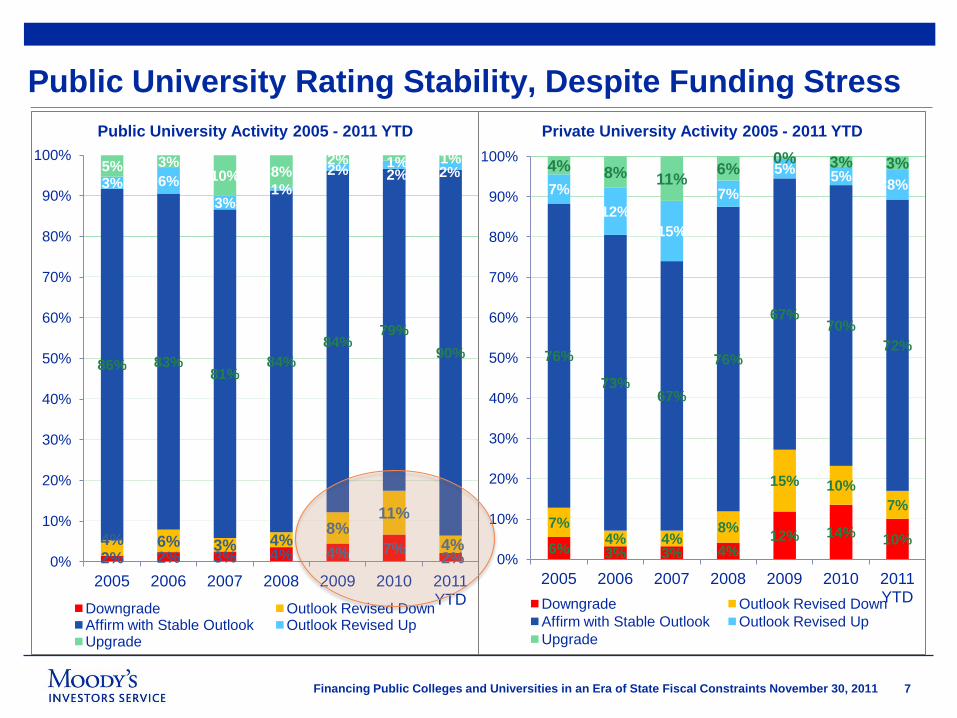

Public University Rating Stability, Despite Funding Stress

2% 2% 3% 4% 4% 7% 2% 4% 6% 3% 4%

8% 11%

4%

86% 83% 81%

84% 84%

79% 90%

3% 6% 3%

1% 2% 2% 2% 5% 3%

10% 8% 2% 1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 YTD

Public University Activity 2005 - 2011 YTD

Downgrade Outlook Revised Down Affirm with Stable Outlook Outlook Revised Up Upgrade

6% 3% 3% 4% 12% 14% 10%

7% 4% 4%

8%

15% 10% 7%

76%

73% 67%

76%

67% 70%

72%

7% 12%

15%

7% 5% 5% 8%

4% 8% 11% 6% 0% 3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 YTD

Private University Activity 2005 - 2011 YTD

Downgrade Outlook Revised Down Affirm with Stable Outlook Outlook Revised Up Upgrade

8 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Public University Business Model Fundamentally Changed

9 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

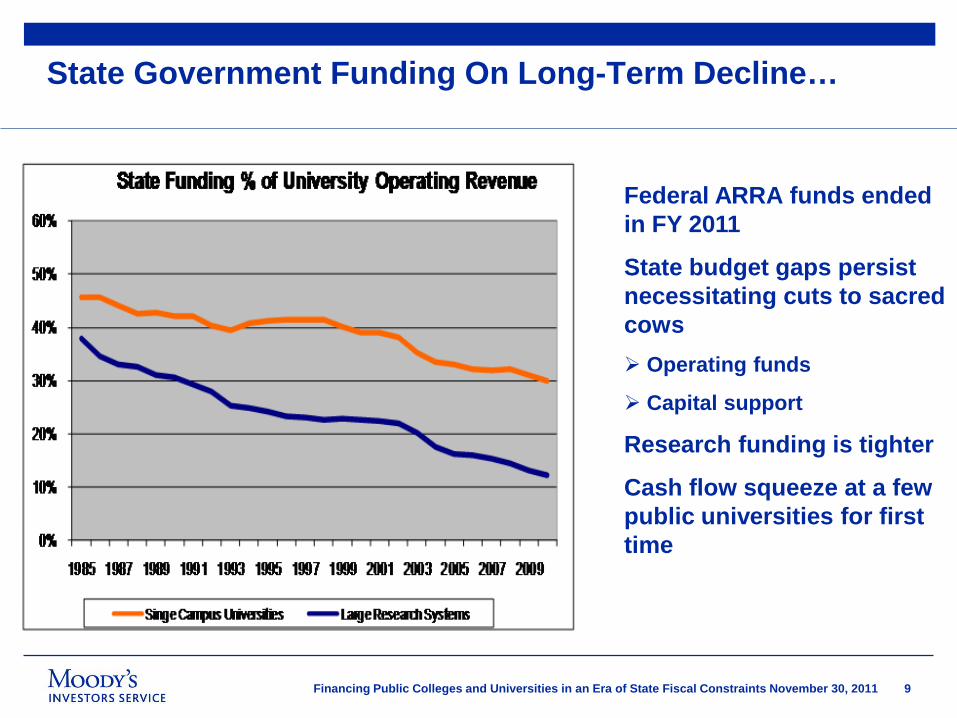

State Government Funding On Long-Term Decline…

Federal ARRA funds ended in FY 2011

State budget gaps persist necessitating cuts to sacred cows Operating funds

Capital support

Research funding is tighter

Cash flow squeeze at a few public universities for first time

10 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

As State Funding Has Declined, Student Based Revenue Has Filled the Gap

Students are paying more: like progressive income taxing

Publics acting just like privates:

Higher tuition and higher aid

National/international student recruitment

20

25

30

35

40

45

50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 est

2012 est

Student Funding Now Drives Public Universities Source: Moody’s Median MFRA Data (Share of Revenues by Source

for US Public Universities (%))

Student Revenues % Government Appropriations %

11 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Public Universities Exercise Their Market Pricing Power…

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010 2011 est

Publics Net Tuition/Student Rises Faster than Privates

Source: Moodys Median MFRA Data % Change

Publics (Left) Privates (Left) Pub/Pri Ratio (Right)

Public sector net pricing rising 3x faster than private sector tuition

Reaction from state government varies from attempts at WWII-era price controls to laissez faire, hands off realism

Reaction from students is generally accepting despite events in California

California sudden sharp tuition spikes reveal unstable model used by government in that state vs Big Ten pricing model

Unsustainable political compacts vs Market Gradualism

12 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

… And Lowest Cost Competitors

$11,000

$11,500

$12,000

$12,500

$13,000

$13,500

$14,000

$0

$5,000

$10,000

$15,000

$20,000

$25,000

2004 2005 2006 2007 2008 2009 2010 2011 est

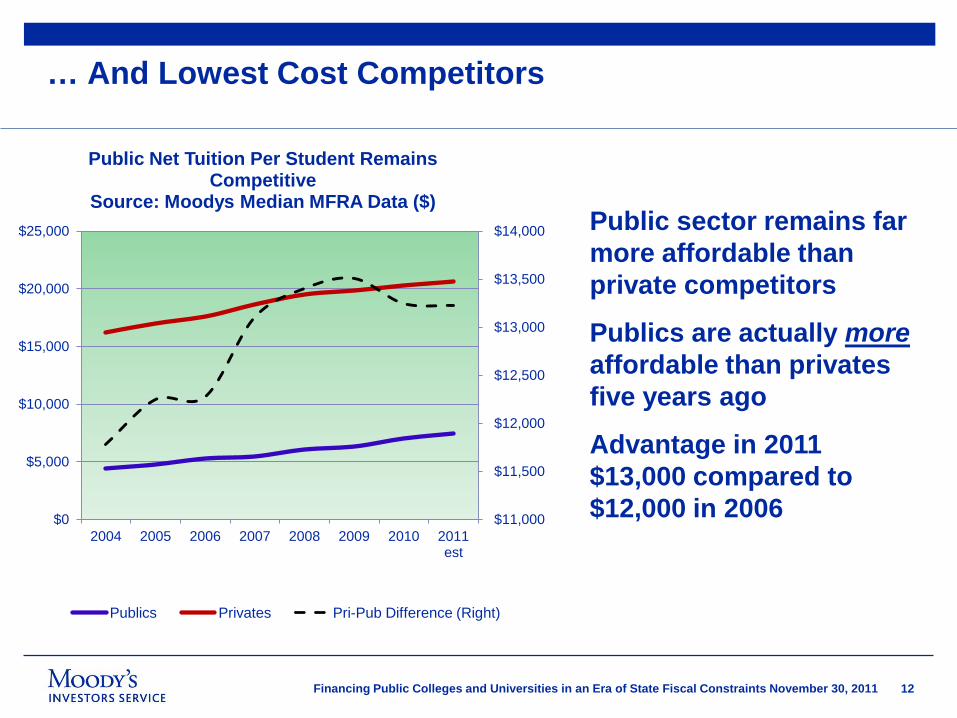

Public Net Tuition Per Student Remains Competitive

Source: Moodys Median MFRA Data ($)

Publics Privates Pri-Pub Difference (Right)

Public sector remains far more affordable than private competitors

Publics are actually more affordable than privates five years ago

Advantage in 2011 $13,000 compared to $12,000 in 2006

13 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Will Public Universities Use Up Their Pricing Power?

5.7% 5.6% 6.0% 5.3% 4.2%

2.6% 2.7%

-15%

-10%

-5%

0%

5%

10%

-$15

-$10

-$5

$0

$5

$10

2005 2006 2007 2008 2009 2010 2011

Slowed Net Tuition Growth Lags Steep Decline in U.S. Net Worth

Change in Net Worth of Households & Not for Profit Organizations ($, trillion)

Demand is function of net worth, income & demographics

Political and public pressure to

improve affordability Moderation of tuition increases Expanded financial aid budgets Need to become more efficient

Source: Change in Net Worth 1980-2010, Federal Reserve; 2011 Forecast from Moody’s Analytics ; Median Net Tuition per Student: Moody’s

14 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Will Pell Continue to Pick up the Slack?

Dependence on Pell and other aid for low income students is increasing, but it is covering a smaller portion of net tuition per student.

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

0%

20%

40%

60%

80%

100%

120%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Maxim

um Pell Aw

ard per Student

% N

et T

uitio

n pe

r Stu

dent

Cov

ered

Maximum Pell Award is Covering a Smaller Portion of Net Tuition Per Student, Especially for Public Universities

Maximum Pell Award % of Net Tuition Per Student Covered by Pell Award - Public

Source: Moody’s, NCES & The College Board

15 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Publics Are Biggest …

• 20% All Campuses > 5,000 FTE

Average US FTE Enrollment By Degree Granting Type Priv/NFP Prop Public

Associate's Degree 568 579 4,200

Bachelor's Degree 951 938 3,288

Master's Degree or Doctor's Degree 2,613 3,127 11,011

First Professional Degree 488 451 660

Grand Total 2,013 986 6,428

Bachelor's thru Professional Only 2,105 1,649 9,860

• 6% 4Yr Publics <1,000 FTE

• 46% 4Yr Private NFP <1,000 FTE • 60% All Publics > 5,000 FTE

• 8% All Private NFPs > 5,000

16 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Publics Have Size/Price Advantages; Privates Have Leadership Edge

PUBLIC UNIVERSITIES

• Economies of Scale

• Low Price Competitor

• Public Subsidy/Ultimate Support

• More Diversified Revenues

• Management Slow but Improving

• Governance Lagging

• Some Exposed to Pensions/OPEB

• Political Limits of Tuition

PRIVATE COLLEGES

• Much Smaller on Average

• Moderate to High Price Competitor

• Philanthropic Subsidy

• Most Highly Tuition Dependent

• Management More Nimble

• Governance Mostly Better

• Investments/ Liquidity Challenges

• Economic Limits on Tuition

17 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Where are we headed?

18 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Arguably, Public Universities Are More Stable with Less State Funding

Reduced public operating funding of public universities is irreversible

Higher tuition dependence makes revenue less volatile – better

for planning

Challenges Access at affordable tuition rates for low income, first generation

students With less state capital funding, borrowing will keep rising

19 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Strategies to Cope with Pressing Issues

Community colleges as cost-effective capacity relief; also partnerships with for-profits and traditional private colleges

Enable graduation in shorter periods of time Public universities have large economies of scale and can reap

many more operating efficiencies– much more capacity can be freed

Private fundraising will follow same pattern as private

universities, most especially for financial aid

20 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Improved Governance in the Public Sector will be Necessary Outcome

Commitment to market disclosure

Strong accountability and oversight of management without government dominance

Diversification of board members to include those with sector expertise as well as strong philanthropic capacity

Competitive strategies and culture driven to succeed financially as well as meet public mandate for more affordable education

Use of detailed, multi-year financial plans linking budget and capital plans with key assumptions to guide annual budgets

Use of self-assessment, benchmarking

Openness to new organizational partnerships, campus closure, and even mergers in some cases

21 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Government Relations to Combat Cut-Backs is Especially Important

Pressure to restrict access to capital, reduce tax subsidies, and increase regulatory oversight

University leaders can promote:

New political partnership with state fostering operating independence and ultimately allowing universities the flexibility to promote an entrepreneurial climate and promote economic development

Continuance of state financial support for operations and capital projects

Special programs which provide additional support for public higher education such as debt service reimbursement, intercept programs, and funds established to support one or more universities

22 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Additional Areas of State/Public University Intersection

Tuition

Procurement

Zoning and construction regulations

Personnel Benefits

Health Care

Pensions

Compensated Absences

Investment of public funds

23 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

So… A New Business Model for Publics and Privates? “Moody’s rates large majority of higher education measured by enrollment and not one rated college or university has ever defaulted on its debt”– Moody’s Higher Ed team, November 2011

“The American system of higher education is going to change dramatically in the 21st century,” said Aoun. “Our existing college campuses are based on a model that we imported from England in the 17th century. This model cannot meet the full demands of contemporary society”– Joseph Aoun, President of Northeastern University, November 2011

“The institutions to which the country would turn to help tackle this (competitive) challenge—its colleges and universities—are facing a crisis of their own…(this) presents an opportunity to rethink many of the age-old assumptions about higher education—its processes, where it happens, and what its goals are—and to use the disruptive start-up organizations to create institutions that operate very differently and more appropriately to address the country’s challenges.”– Clay Christianson, Harvard Business School, from Center for American Progress “Disrupting College”, February, 2011

24 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Why the Business Model Still Works…for now

States need public universities even more now despite funding cuts Labor force training, job growth, research/tech transfer, health care

No real substitute for face-to-face

But, cost structure is too high

Public universities offer an expensive bundled product Content delivery not valuable part, easily replicated more cheaply by for-

profits Customers pay for transformation of the late adolescent into a young-adult

with judgment, thinking skills, communication ability and career connections

But can the wealth and income levels of the country support the model?

25 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Questions and Discussion

26 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

Edith F. Behr Vice President/Senior Credit Officer Higher Education & Not-for-Profit Team [email protected] 212.553.0566

27 Financing Public Colleges and Universities in an Era of State Fiscal Constraints November 30, 2011

© 2011 Moody’s Investors Service, Inc. and/or its licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ARE MOODY'S INVESTORS SERVICE, INC.'S (“MIS”) CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MIS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. CREDIT RATINGS DO NOT CONSTITUTE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS ARE NOT RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. CREDIT RATINGS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MIS ISSUES ITS CREDIT RATINGS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT. All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Except as expressly stated otherwise, MOODY’S has not verified, audited or validated independently any information received in the rating process, nor will it do so. Under no circumstances shall MOODY’S have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of MOODY’S or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if MOODY’S is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities. Each user of the information contained herein must make its own study and evaluation of each security it may consider purchasing, holding or selling. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

MIS, a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MIS have, prior to assignment of any rating, agreed to pay to MIS for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Shareholder Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Any publication into Australia of this document is by MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657, which holds Australian Financial Services License no. 336969. This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001.

Top Related