Languages

Pages

Legal

M.M.S. - SEM I

FINANCIAL ACCOUNTING

• 1.2. Financial Accounting 100 marks • COURSE CONTENTS

1. Introduction to Accounting : Concept and necessity of Accounting An Overview of Income Statement and Balance Sheet.

2. Introduction and Meaning of GAAP; Concepts of Accounting: Impact of Accounting Concepts on Income Statement and Balance Sheet.

3. Accounting Mechanics: Process leading to preparation of Trial Balance arid Financial Statements; Preparation of Financial Statements with Adjustment Entries

4. Revenue Recognition and Measurement: Capital and Revenue Items: Treatment of Income & Expenses. Preproduction Cost, Deferred Revenue Expenditure etc.

5. Fixed Assets and Depreciation Accounting.

6. Evaluation and Accounting or inventory

7. Preparation and Complete Understanding

of Corporate Financial Statements : ‘T

’Form and Vertical Form of Financial

Statements

8. Important Accounting Standard

9. Corporate Financial Reporting — Analysis

of Interpretation thereof with reference Ratio

Analysis. Fund Flow, Cash Flow.

10. Inflation Accounting

11. Ethics Issues in Accounting

Reference text:

1 Financial Accounting. Text & Case.

Daardon & Bhattacharya

2 Financial Accounting for Managers — T P

Ghosh

3 Financial Accounting - R Narayanaswamy

4 Full Text of Indian Accounting standard — Taxman

Publication

5 Book Keeping & Accountancy – Choudhary Chopade

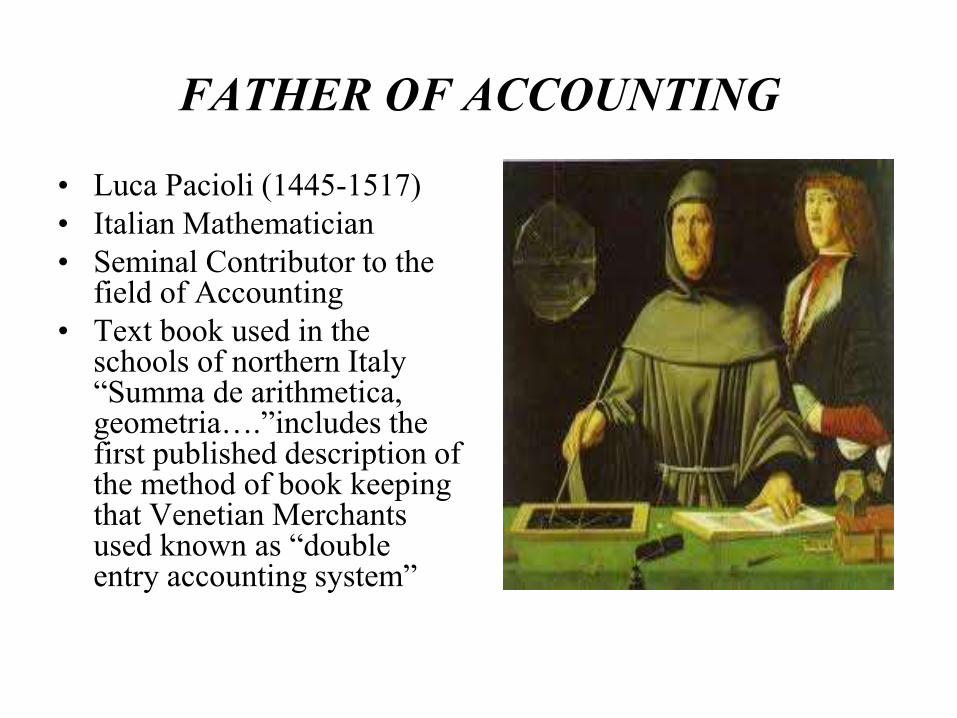

FATHER OF ACCOUNTING

• Luca Pacioli (1445-1517)

• Italian Mathematician

• Seminal Contributor to the field of Accounting

• Text book used in the schools of northern Italy “Summa de arithmetica, geometria….”includes the first published description of the method of book keeping that Venetian Merchants used known as “double entry accounting system”

MEANING & DEFINITIONS

of BOOK KEEPING

• Book Keeping means keeping a written record of business transactions in a set of books.

• Book Keeping is the art of recording business dealings in a set of books ----- J R Batliboi

• Book Keeping is the science and art of correctly recording in the books of accounts all those business transactions that result in the transfer of money or money’s worth ----- R N Carter

NEED OF BOOK KEEPING

• To have permanent record of

all the business transactions

• To know names of customers

& suppliers

• To know net profit & net loss,

assets & liabilities of the

business

• To have important

information for legal & tax

matters

ACCOUNTING• AICPA (American

Association of Certified

Public Accountants)

Accounting is the art of

Recording, Classifying

and Summarizing, in

terms of money,

financial transactions

and events and

interpreting the results

thereof

• AAA (American

Association of Accounting)

Accounting is the

process of Identifying,

Measuring and

Communicating

economic information to

permit informed

judgements and

decisions by users of the

information

OBJECTIVES OF BOOK KEEPING

• To have date-wise record

• To have account-wise record

• To calculate & know yearly

profit or loss

• To know year-end financial

position

• To analyse, interpret &

communicate the accounting

information

PERSONS INTERESTED IN

ACCOUNTING

• OWNER

• EMPLOYEES

• LENDERS

• CUSTOMERS

• SUPPLIERS

• GOVERNMENT

• SOCIETY

• SHAREHOLDERS

• RESEARCHERS

• PROSPECTIVE INVESTORS

FINANCIAL ACCOUNTING

• Financial Accounting is theprocess of summarising financialdata, which is taken from anorganisation’s accounting recordsand publishing it in the form ofannual or quarterly reports, for thebenefit of people outside theorganisation

• It is also concerned with activitiesinvolving strategic planning,control, decision making, problemsolving, performancemeasurement & evaluation, co-ordinating, directing, auditing, taxplanning, cost & managementaccounting, MIS & so on.

Role of Financial Accounting

• Generates key documents like Manufacturing A/c, Trading A/c, Profit & Loss A/c & Balance Sheet

• Records financial transactions showing both inflow & outflow of money from sale, purchase, payments & receipts etc

• Empowers the managers & aids them in managing more efficiently by preparing standard information which includes monthly MIS reports tracing the costs and profits against budgets, sales & investigations of the cost.

Benefits of Financial Accounting

• Keeping proper & chronological record of transactions & events

• Helps to comply with various legal requirements under tax laws, company law etc.

• Protecting and safeguarding the business assets by serving as evidence & preventing unwarranted & unjustified use

• Facilitates rational decision making

• Communicating & Reporting to the end users

Limitations of Financial Accounting

• No clear idea of operating

efficiency. (Profit)

• Weakness not spotted. Does not

disclose the exact cause of

inefficiency (Thermometer)

• Not helpful in price fixation

(non availability of costs)

• Provides only historical

information

• Inadequate information for

reports & decision making

• No Analysis of losses

TERMINOLOGY

• TRANSACTION – Exchange

between two parties. It involves

“Give & Take”

• CASH TRANSACTION –

Goods or services are exchanged

for cash

• CREDIT TRANSACTION –

Goods or services are exchanged

for cash receivable or payable at

future

• GOODS – things, articles or commodities exchanged in a business transaction

• SERVICES – Service means the work done for money. They do not involve any article or commodity

• PROFIT – Excess of Income over expenditure

• LOSS – Excess of Expenses over Income

• INCOME – Amount earned by sale of goods & services

• EXPENSES – Amount paid for goods & services used in the

business

• ASSETS – Properties owned by the business like Building,

Plant, Machinery, Computers, Motor Cars, Furniture & Fixtures

etc.

• LIABILITIES – Loans borrowed from banks, relatives, friends

etc. which must be paid back in future are called liabilities

• CONTINGENT LIABILITY – Future liability. It may or may

not become an actual liability. It is not recorded in the books,

but is shown by way of a note in the balance sheet

• CAPITAL – Money put in the business by the owner.

It also includes goods or assets brought in the

business by the owner

• DRAWINGS – If the owner withdraws any money,

goods or assets from the business for his own use,

such withdrawals are called as drawings. Such

drawings reduce the amount of capital of the owner

• NET WORTH – Difference between total assets and

total outside liabilities. Net Worth = Assets -

Liabilities

• DEBTOR – A debtor buys goods & services from us

and promises to pay the price to us on an agreed date

in future. Debtor is a person who owes money to

business.

• CREDITOR – A creditor sells goods & services to

us and agrees to receive the price in future. Creditor is

a person to whom we owe money.

• EXPENDITURE – Payment made by a business to

obtain some benefit i.e. assets, goods or services

• CAPITAL EXPENDITURE – Expenditure

for obtaining an asset is known as capital

expenditure. It is an expenditure having future

benefits. It is an expenditure with long term

use (more than 1 year)

• REVENUE EXPENDITURE – Expenditure

on obtaining goods and services is known as

revenue expenditure. It is an expenditure for

running the business. It is an expenditure with

short term use (1 year or less than 1 year)

• DEFERRED REVENUE EXPENDITURE – To defermeans to postpone. It is that expenditure which iscarried forward as it will be of benefit oversubsequent period e.g. heavy advertisementexpenditure to launch a new product. Theproportionate cost related to current year is taken asexpense. The balance cost is carried forward andwritten off in next year.

• ACCOUNTING YEAR – Period of 12 monthsnormally starting in April & ending in March of nextyear. Normally profit is found out for an accountingyear.

• Account – An account is a summarized record of transaction relating to certain person, kind, income or expenditure. It is separately prepared record of the certain transactions

• Asset – Assets are the properties of every type (movable or immovable) owned by a person or an organization

• Casting – Casting means totalling of books of accounts.

• Bad Debt – Bad debts are those debts which are not recoverable and written off from the debtors account. It is a loss for the organization

• Discount – It is a concession or allowance given by the receiver of benefit to giver of the benefit. It is generally given by seller to buyer

• Entry – The entry refers to the recording of business transaction in the books of account

• Narration – It is a brief explanation of a journal entry written exactly after every journal entry starting with the word “being”

• Posting – Transactions recorded in journal are further transferred to ledger accounts. The process of recording the transactions from journal to ledger is called as posting

• Purchases – Goods brought for direct resale or further manufacturing and resale is called as purchase. Thus buying, the commodities for trading or business purpose are termed as purchases.

• Revenue – Revenue refers to the amount generated by the organisation from its business activities. Generally it is the amount collected through making sales efforts

• Sales – When an organisation makes sale of goods (which it purchased for resale) then it directly termed as sale.

• Solvent – A person or an organisation is said to be solvent when its assets are equal to or more than its liabilities

• Stock – Stock refers to the amount of (value of ) unsold goods lying with the businessman on any particular date

TYPES OF ACCOUNTS

• PERSONAL ACCOUNTS – Accounts ofall persons like Dena Bank a/c, GarwareInstitute A/c, Mumbai University A/c,Sachin Tendulkar A/c etc.

• REAL ACCOUNTS – Accounts of allproperties & assets like CASH Account,Plant & Machinery A/c, Building A/C etc.

• NOMINAL ACCOUNTS – Accounts ofall expenses & losses and Incomes & gainslike Telephone charges a/c, Interest RecdA/C, Electricity charges a/c, Salary accountetc.

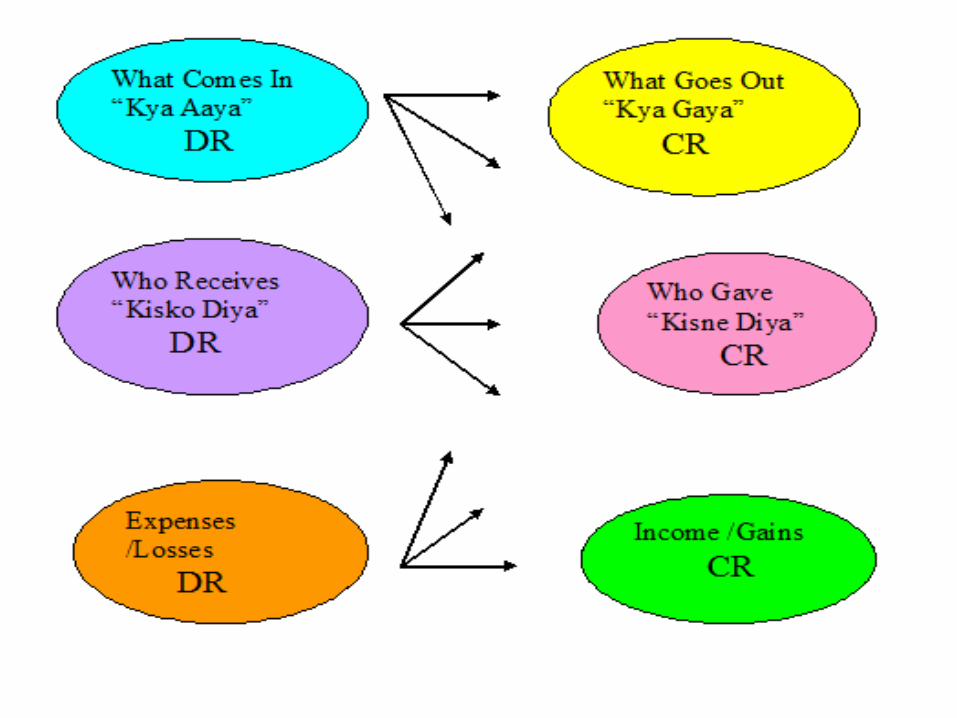

GOLDEN RULES

PERSONAL ACCOUNT

DEBIT - THE RECEIVER

CREDIT – THE GIVER

REAL ACCOUNT

DEBIT – WHAT COMES IN

CREDIT – WHAT GOES OUT

NOMINAL ACCOUNT

DEBIT – ALL EXPENSES & LOSSES

CREDIT – ALL INCOMES & GAINS

DOUBLE ENTRY ACCOUNTING

• Recording of transactions & events follows a

definite rule.

• Each transaction or event has two aspects

DEBIT (Dr.) & CREDIT (Cr.)

• Every Debit has an equal & opposite Credit

• Every transaction should be recorded in such a

way that it affects two sides – DEBIT &

CREDIT

ACCOUNTING CYCLE

1. SELECTION OF TRANSACTION – Select

only those transactions which are

- Financial in nature and

- Which arise in the course of the business

2. ANALYSIS OF TRANSACTION – Analyse

the transaction to find out

a. Whether the business has received any

benefit such as goods, services or assets and

in return , any amount is paid in cash or is

payable

b. Whether any such benefit has gone out of

business and in return any amount is received

in cash or is receivable

3. CLASSIFICATION OF ACCOUNTS – Find

out which items or persons are involved in the

transaction and classify them in to 3 main

types such as

a. Personal A/c

b. Real A/c

c. Nominal A/c

4. APPLYING RULES OF DEBIT OR CREDIT

Depending upon the nature of a transaction

a. DEBIT – The A/c receiving the benefit or

amount

b. CREDIT – The A/c giving the benefit or

amount

• 5. RECORDING IN JOURNAL ORSUBSIDIARY BOOKS – Transactions arerecorded as and when they occur, in a dailybook called Journal including subsidiary bookslike Cash Book, Bank Book, PurchaseRegister, Sales Register etc.

• 6. POSTING AND TOTALLING OFLEDGER ACCOUNTS – From the journal,the amounts debited or credited are transferred(posted) to the debit and credit of theconcerned accounts in a book called Ledger

• 7. TRIAL BALANCE – At the end of the year trialbalance is prepared which shows the closing balancesof all accounts in the ledger

• 8. PROFIT & LOSS A/C – The balances of Incomeand Expenses accounts at the end of the year aresummarised in the P/L A/c. The difference betweenthe income & expenses shows the profit or loss forthe year

• 9. BALANCE SHEET – The balances of assets,liabilities and capital accounts at the end of the yearare summarised in the Balance Sheet.

BRANCHES OF ACCOUNTING

• FINANCIAL ACCOUNTING

• COST ACCOUNTING

• MANAGEMENT/MANAGERIAL ACCOUNTING

• AUDITING

• TAXATION

FINANCIAL ACCOUNTING

• Original Form of Accounting

• Confined to Preparation of

Financial Statements

• Objective is to Calculate

Profit / Loss made during the

year & to exhibit Financial

Position of the Business

COST ACCOUNTING

• Function of cost

accounting is to

ascertain the cost of the

product and to help the

management in the

control of cost

• Costing is a technique

of ascertaining cost of a

particular product or

service

MANAGEMENT ACCOUNTING

• It is an accounting for

management

• Provides information to

the management

• It is reproduction of

financial accounts in such

a way as will enable the

management to take

decisions & control

various activities

AUDITING

• Examination of books,

accounts, vouchers and other

records by a practicing

Chartered Accountant appointed

for the purpose

• Reporting to the members /

management whether the B/S &

P/L A/c as on particular date

shows true & fair view of the

state of affairs of the business

TAXATION

• Computation of

Taxable Income &

Tax Payable thereon

• Reconciliation

between accounting

profit & taxable

profit

• Statutory compliance

Accounting Conventions

• Consistency

• Materiality

• Disclosure

• Conservatism

Consistency

• Means following the

same accounting policies

consistently without

initiating frequent

changes

• Comparison of business

results of one period with

the other is possible only

when accounting policies

are followed consistently.

• E.g. Depreciation

Materiality

• An item should be

regarded as material, if

there is a reason to

believe that knowledge of

it would influence the

decision of the informed

investor

• Significant & important

information should be

properly reported

Disclosure

• Full disclosure of all the material facts with the true and fair view

• It does not mean disclosure of each and everything

• It simply means providing information of significance to the relevant users

Conservatism

• It refers to policy of playing safe

• All the probable losses are taken in to consideration but not the probable gains

• E.g. making provision for doubtful debts, discount on debtors, valuation of stock at cost or market price whichever is less etc.

ACCOUNTING CONCEPTSElephant, Monkey, Cat, Goat, Parrot & Ant Playing Match for Victory

Cost

Going

ConcernPeriodicity

Accrual

Prudence

Matching

EntityMoney

Measurement

Verifiable

Evidence

ACCOUNTING CONCEPTS

EXPLAINED

• The Entity Concept – A business is anartificial entity distinct & separate from itsowner. For accounting purposes abusiness & its owner are two separatepersons

• Money Measurement Concept – Foraccounting purposes each transaction &event must be expressible in monetaryterms.

• The Cost Concept - Assets such as Land,Buildings, Plant & Machinery etc. andobligations such as Loans, Public Depositsetc. should be recorded at historical cost(acquisition)

• The Going Concern Concept – It isassumed that the business organizationwould continue its operations for a longtime

• Periodicity Concept – The results of

operations of entity are measured

periodically i.e. in each accounting period.

Calendar Year – January to December

Fiscal Year – April to March

As per Income Tax Act, Accounting Period

should always be starting from April -

March

• Accrual Concept – Incomes & Expenses

should be recognized as and when they

are earned and incurred, irrespective of

whether the money is received or paid in

connection thereof. E.g. Rent paid for 15

months in advance on January 2009. In

this case Rent for 3 months should be

recognized in FY 08-09 & Rent for 12

months should be recognized in FY 09-10

• Concept of Prudence – It states that

anticipate no profits but provide for all

possible losses. Prudence is the inclusion

of a degree of caution in the judgment of

estimates. Expected losses should be

accounted for but not anticipated gains

• Matching Concept – Revenue earned in anaccounting year is matched with all theexpenses incurred during the same period togenerate that revenue. Matching conceptsuggest that to find out the profitability, theexpenses incurred to generate revenue are tobe matched against that revenue

• Verifiable Evidence – All accounting transactionsshould be evidenced and supported by thedocuments. Such supporting documents providethe basis for making accounting entries and formaking verification by the auditor later on.

ACCOUNTING SEQUENCE

Transaction

/ Event

Preparation

Of Vouchers

Recording in

Primary Books

JOURNAL

Postings in

Secondary

Books

LEDGER

Preparation

Of

Trial Balance

Preparation

Of Financial

Statements

Trading A/C,

Profit & Loss A/C,

Balance Sheet etc.

VOUCHER PREPARATION

• After the event is happened, physical

vouchers based on certain documents like

Bill, Delivery Challan, Receipt, Reports,

Purchase Order, Quotations etc. are

prepared & the same are filed for future

reference

Voucher with Supporting Documents

RECORDING IN PRIMARY BOOK• All the events are recorded in primary book called “JOURNAL”

in a double entry system of book keeping.

• Format of JOURNAL is as follows

Sr.No. Date Particulars

Dr. /

Cr.

Vr.

No. L/F

Dr.

Amt

Cr.

Amt.

1 24.04.2009 Plant & Machinery A/C Dr. 1 12 500

To Cash Cr. 1 14 500

(Being Purchase of

Machinery for cash from Mr.

Sam)

SECONDARY BOOKS - LEDGER

DR. Plant & Machinery Account CR.

Date Particulars JF Amount Date Particulars JF Amount

24.04.09 To Cash 500 30.04.09 By Balance 500

500 500

DR. Cash Account CR.

Date Particulars JF Amount Date Particulars JF Amount

30.04.09 To Balance 500 24.04.09 By P&M 500

500 500

TRIAL BALANCE

• It is a list of various accounts showing theirbalances (either DR. or CR.) as on particulardate. Based on such TB financial statementsare prepared.

Trial Balance as on 31.03.2009

Sr.No. Name of the Account Dr. Bal. Cr.Bal.

1 Plant & Machinery 500

2 Cash 500

Total 500 500

Trading Account

TRADING A/C for the year ended 31.03.2009

Dr. Cr.

Particulars (Trad Exp) Amount Particulars (Trad Income) Amount

To Opening Stock xx By Sales xx

To Purchases xx By Closing Stock xx

To Wages xx

To Gross Profit c/d xx

xxx xxx

Profit & Loss Account

PROFIT & LOSS A/C for the year ended 31.03.2009

Dr. Cr.

Particulars (Expenses) Amount Particulars (Incomes) Amount

To Salary xx By Gross Profit b/d xx

To Printing & Station xx By Commission Recd xx

To Telephone xx By Discount Recd xx

To Advertisement xx By Interest Recd xx

To Electricity xx By Remuneration Recd xx

To Postage xx By Profit on Sale of Asset xx

To Fax Exp xx

To Net Profit c/d xx

xxx xxx

JOURNAL

• Journal means a daily book

• Journal means a book to record daily transactions

• As soon as any financial transaction takes place, it is recorded in the Journal. Hence it is called the book of First, Original or Prime entry

• Journal entry is passed according to the rules of Debit & Credit.

LEDGER

• JOURNAL – Date wise record

• LEDGER – Account wise record

• Ledger A/c is a statement showing the summary of transactions and the final balance in respect of a person or an item. Each A/c is kept on a separate page or folio. All the pages/folios are bound together in a book called LEDGER

FORMAT OF LEDGER A/C

DR. ……………. A/c (Name of the Ledger A/c) CR.

DATE PARTICULARS J/F AMT DATE PARTICULARS J/F AMT

xx To …….. A/c - xxx xx By …….. A/c - xxx

xxxx xxxx

TRIAL BALANCE

• TRIAL BALANCE is a statement containing the list of the balances of all Ledger Accounts on a particular day

• It is a concise summary of ledger balances

• It gives an idea of balances of various accounts of persons, assets, income and expenses at a glance

• It is a link between ledger and the final accounts

FORMAT OF TRIAL BALANCETRIAL BALANCE OF …………. AS ON …………

Sr.No

. Particulars / Name of the Ledger A/c L/F

Debit

Amt

Credit

Amt

1 Purchases A/c xx

2 Sales A/c xx

3 Purchase Returns A/c xx

4 Sales Returns A/c xx

5 Cash A/c xx

6 Bank A/c xx

7 Capital A/c xx

8 Salaries A/c xx

9 Furniture A/c xx

10 Sundry Debtors A/c xx

11 Sundry Creditors A/c xx

Total xxxx xxxx

STEPS IN EXTRACTING TRIAL

BALANCE

• RECORDING - the transactions in Journal

• POSTING - the transactions in Ledger

• BALANCING - the Ledger Accounts

• TRIAL BALANCE – writing the balances of the Ledger Accounts

Ledger Accounts

Normally Having Dr. & Cr. Balances

• DR. BALANCES

1. Drawings

2. Sundry Debtors

3. Bills Receivable

4. Bank

5. Loans Given

6. Deposits Given

7. Advances Given

8. Cash A/c

9. Assets A/c

10. Purchases

11. Return Inwards

12. Opening Stock

13. Expenses & Losses

• CR. BALANCES

1. Capital A/c

2. Sundry Creditors

3. Bills Payable

4. Bank Overdraft

5. Loans Taken from

6. Deposits Taken from

7. Advances Taken from

8. Sales

9. Return Outwards

10. Income & Gains

INDIVIDUAL PROJECT/ASSIGNMENT

• TOPIC

ACCOUNTING STANDARDS ISSUED TILL DATE

- Meaning, Who sets, Factors considered, Points Covered, Objective, Benefits etc.

- List along with AS-No.

- Explanation in full details for any 4 accounting standards

• Submission Date

15th October, 2013

• Neatly typed

/printed/handwritten &

spiral bounded

• Specify the name, roll

no. division, subject etc.

• Total Marks 40

Thank You

• For More:

– Visit

– www.guide2startup.blogspot.com

Top Related