Languages

Pages

Legal

10/16/2013

1

October 16, 2013 I 2 - 3 p.m. CST

Final IRS Tangible Property Regulations –How Will They Affect Your Business?

Rick KlahsenPartnerBKD, LLP

Robert ConnerNational Tax Assistant DirectorBKD, LLP

Scott HumphreyNational Tax Assistant DirectorBKD, LLP

Participate in entire webinarAnswer polls when they are providedIf you are viewing this webinar in a group

Complete group attendance form with Title & date of live webinar Your company name Your printed name, signature & email address

All group attendance sheets must be submitted to [email protected] 24 hours of live webinarAnswer polls when they are provided

If all eligibility requirements are met, each participant will be emailed their CPE certificates within 15 business days of live webinar

TO RECEIVE CPE CREDIT

2 // experience access

2 // experience access

10/16/2013

2

AGENDA

• Overview• Materials & Supplies• Asset acquisitions• Improvements• New proposed disposition rules• Action steps• Questions

3 // experience access

3 // experience access

RECENT HISTORY OF THE REGULATIONS

• Temporary Regulations issued on December 23, 2011o Effective January 1, 2012

• Delayed on November 20, 2012 o Changes to regulations announcedo New effective date of January 1, 2014

• Reissued final & proposed regulations September 13, 2013o Still effective January 1, 2014o Early adoption optionso Additional guidance expected

4 // experience access

4 // experience access

10/16/2013

3

WHAT CHANGED?

• New de minimis safe harbor• Materials & supplies threshold• Small taxpayer safe harbor• Routine maintenance safe harbor for buildings• Disposition rules• General asset accounts

5 // experience access

5 // experience access

WHAT STAYED THE SAME?

• Improvement rules• Unit of property definition• Routine maintenance safe

harbor for property (other than buildings)

6 // experience access

6 // experience access

10/16/2013

4

MATERIALS & SUPPLIES

• Tangible property used & consumed in the taxpayer’s operations that is not inventory &

o Is a component acquired to maintain, repair or improve a unit of tangible property

o Consists of fuel, lubricants, water & similar items reasonably expected to be consumed in 12 months or less

o Is a unit of property with an economic useful life of 12 months or less

o Is a unit of property with a cost of $200 or less oro Identified as a material & supply in other IRS published guidance

7 // experience access

7 // experience access

OTHER DEFINITIONS

• Incidental supplieso No records maintainedo Example, office supplies

• Rotable & temporary spare parts• Standby emergency spare parts

o Used as replacement partso Directly related to particular

machineryo Normally expensiveo Not repaired or reusedo Not interchangeable

8 // experience access

8 // experience access

10/16/2013

5

MATERIALS & SUPPLIES – KEY CHANGES

• Election to capitalize & depreciate limited to rotable, temporary or emergency spare parts

• Reduced confusion on rotable spare parts• Clarified relationship between materials & supplies & de

minimis safe harbor• Increased dollar amount for

UOP from $100 to $200

9 // experience access

9 // experience access

DE MINIMIS SAFE HARBOR

• Removed ceiling calculation• Annual election• New safe harbor based on invoice (or item)

o Final regulations contain anti-abuse rule

• Must have written capitalization policy as of first day of tax year

• Rotable, temporary & emergency spare parts not eligible for de minimis safe harbor

• If de minimis safe harbor used, taxpayer must apply it to materials & supplies as well

10 // experience access

10 // experience access

10/16/2013

6

DE MINIMIS SAFE HARBOR

• Applicable Financial Statement (AFS)o Financial statement filed with SECo Certified audited financial statemento Financial statement required to be provided to federal/state

government or agency

• Taxpayers with AFS o $5,000 per invoice (or item)o Must expense in AFS

• Taxpayers without an AFSo $500 per invoice (or item)

11 // experience access

11 // experience access

EXAMPLE # 1

• Taxpayer has an AFS• Written capitalization policy of

$2,500• Purchased 500 computers for

$1,000,000 including shipping• Entire amount deductible under de

minimis safe harbor

12 // experience access

12 // experience access

10/16/2013

7

EXAMPLE # 2

• Taxpayer does not have an AFS• Written capitalization policy of $2,000• Purchased 100 drill presses for $100,000

including shipping• Entire amount is required to be capitalized for

tax purposes• Still allowed to be deducted on books & records

13 // experience access

13 // experience access

ACQUISITION COSTS

• Capitalize costs that facilitate an acquisitiono 11 specifically identified inherently facilitative costs

• Real property investigatory costs• Employee costs & overhead

o Election to capitalize

• Contingency fees

14 // experience access

14 // experience access

10/16/2013

8

WHEN DO I CAPITALIZE AN IMPROVEMENT?

15 // experience access

DETERMINE IF EXPENDITURE IS IMPROVEMENT

Betterment Restoration Adaptation

IDENTIFY UNIT OF PROPERTY

Buildings Plant Property Network Assets Functional Interdependence

POTENTIAL EXCEPTIONS TO CAPITALIZATION

Routine Maintenance Safe Harbor

De Minimis Safe Harbor Small Taxpayer Safe Harbor

IF EXCEPTIONS DO NOT APPLY THEN PROCEED

ROUTINE MAINTENANCE SAFE HARBOR

16 // experience access

• Buildingso Reasonably expected to occur more than

once during a 10-year period

• Property other than buildingso Reasonably expected to occur more than

once during class life of property

• Does not apply too Bettermentso Adaptation oro Items for which a partial disposition or

casualty loss has occurred

16 // experience access

10/16/2013

9

SMALL TAXPAYER SAFE HARBOR

17 // experience access

• Average annual gross receipts of $10 million or less • Applies to buildings with unadjusted basis of $1 million or

less• Expense building improvements• Lesser of

o $10,000 oro 2 percent of unadjusted basis of

the building

17 // experience access

WHEN DO I CAPITALIZE AN IMPROVEMENT?

18 // experience access

DETERMINE IF EXPENDITURE IS IMPROVEMENT

Betterment Restoration Adaptation

IDENTIFY UNIT OF PROPERTY

Buildings Plant Property Network Assets Functional Interdependence

POTENTIAL EXCEPTIONS TO CAPITALIZATION

Routine Maintenance Safe Harbor

De Minimis Safe Harbor Small Taxpayer Safe Harbor

IF EXCEPTIONS DO NOT APPLY THEN PROCEED

10/16/2013

10

UNIT OF PROPERTY

• Functional interdependence standard• Special rules for

o Buildings Building structure Building system

o Plant propertyo Network assetso Leased property

19 // experience access

19 // experience access

FUNCTIONAL INTERDEPENDENCE

• Functional interdependence standardo Applies if not already definedo Placing in service one component is dependent upon another

20 // experience access

20 // experience access

10/16/2013

11

BUILDINGS

• Building Structureo Includes building shell & anything not included in a system

• Building Systemso HVAC Systemso Plumbing Systemso Electrical Systemso Escalatorso Elevatorso Fire-protection & alarm systemso Security systemso Gas distribution systemso Other systems identified in published IRS guidance

21 // experience access

21 // experience access

PLANT PROPERTY

• Functionally interdependent machinery or equipment• Unit of Property

o Further divided into components that perform a discrete & major function

22 // experience access

22 // experience access

10/16/2013

12

WHEN DO I CAPITALIZE AN IMPROVEMENT?

23 // experience access

DETERMINE IF EXPENDITURE IS IMPROVEMENT

Betterment Restoration Adaptation

IDENTIFY UNIT OF PROPERTY

Buildings Plant Property Network Assets Functional Interdependence

POTENTIAL EXCEPTIONS TO CAPITALIZATION

Routine Maintenance Safe Harbor

De Minimis Safe Harbor Small Taxpayer Safe Harbor

IF EXCEPTIONS DO NOT APPLY THEN PROCEED

WHAT IS AN IMPROVEMENT?

24 // experience access

Improvement

Adaptation1. New or different use not

consistent with intended ordinary use at time UOP is placed into service

Restoration1. Replacement of component

deducted for loss or included in adjusted basis for realizing gain/loss

2. Returns UOP to ordinary efficient operating condition if property has deteriorated to state of disrepair & is no longer functional for intended use

3. Rebuild UOP to like-new condition after end of class life

4. Replacement of part(s) that comprise major component or substantial structural part of UOP

Betterments1. Ameliorates material

condition or defect existing prior to acquisition or during production of UOP

2. Material addition to UOP3. Material increase in

capacity, productivity, efficiency, strength , quality or output of UOP

24 // experience access

10/16/2013

13

CAPITALIZING REPAIRS & MAINTENANCE

• Annual election to capitalize repairs & maintenance expense

• Applies to all amounts capitalized for financial reporting purposes

• Adds conformity between book & tax

25 // experience access

25 // experience access

DISPOSITIONS

• Disposition occurs when ownership of asset is transferred or when asset is permanently withdrawn from use either in the taxpayer’s trade or business or in production of income

Fixed asset life cycle

26 // experience access

Asset Acquisition

Capitalization versus

Expense

Asset Placed in Service for Depreciation

Disposition: Asset Taken Off Books

26 // experience access

10/16/2013

14

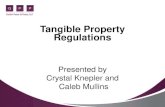

DISPOSITIONS – GUIDANCE FOR DECISIONS

2012 or 2013 Dispositions

2013 Prop. Reg Guidance

Temp Reg Guidance

Pre-Temp Reg

Guidance

27 // experience access

2014 Dispositions

Final Guidance

27 // experience access

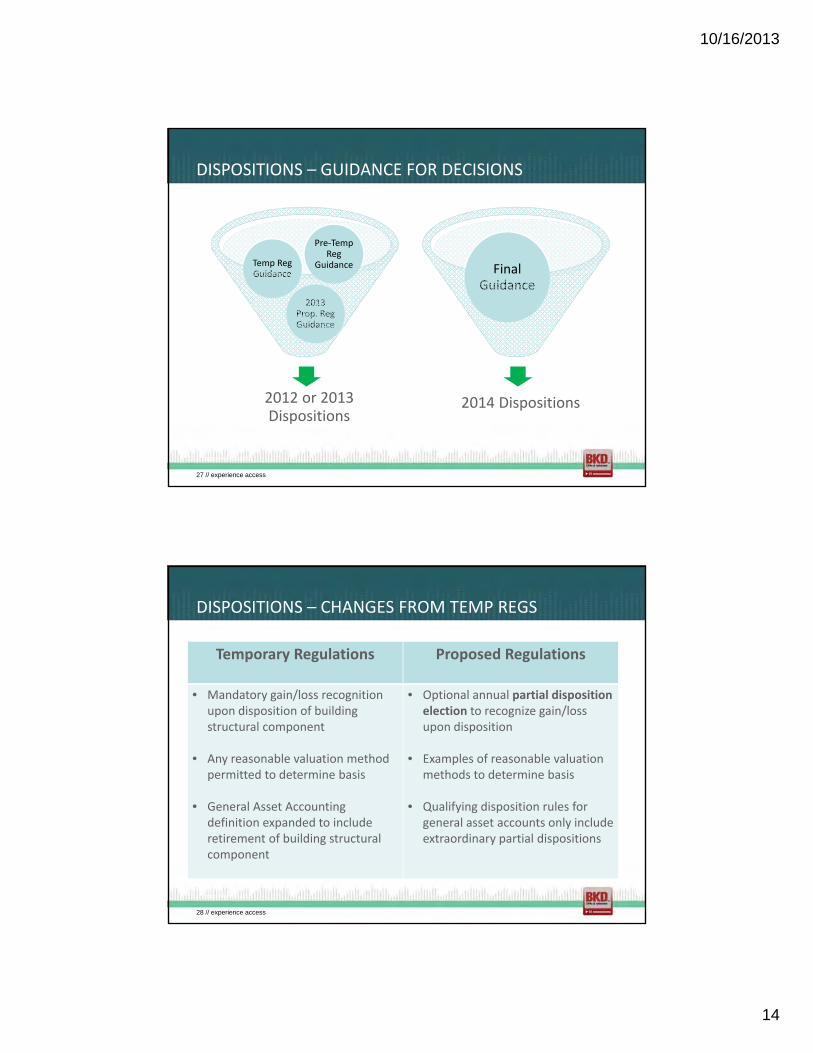

DISPOSITIONS – CHANGES FROM TEMP REGS

28 // experience access

Temporary Regulations Proposed Regulations

• Mandatory gain/loss recognition upon disposition of building structural component

• Any reasonable valuation method permitted to determine basis

• General Asset Accounting definition expanded to include retirement of building structural component

• Optional annual partial dispositionelection to recognize gain/loss upon disposition

• Examples of reasonable valuation methods to determine basis

• Qualifying disposition rules for general asset accounts only include extraordinary partial dispositions

28 // experience access

10/16/2013

15

DISPOSITIONS – PARTIAL DISPOSITION ELECTION

• Definition of disposition is modified to include retirement of a structural component (or portion thereof) of a building if partial disposition election is made

• For assets not included in general asset account, partial disposition rule is mandatory when

o The disposition of a portion of asset results from casualty evento The disposition of a portion of asset results in deferred gain

under Sections 1031 or 1033o The transfer of a portion of asset is considered a step-in-the-

shoes transaction o A portion of asset is sold

29 // experience access

29 // experience access

DISPOSITIONS – CONSIDERATIONS

30 // experience access

30 // experience access

Capitalized Repair, i.e.,

Improvement

Elect Partial Disposition

Rule

Write-Off Old Basis & Depreciate New

Cost

No Partial Disposition

Election

Depreciate Old Basis & New Cost

Deductible Repair e.g., de minimis rule, routine maintenance safe-harbor, or

not betterment/restoration/adaptation

Continue to Depreciate Old Basis

10/16/2013

16

DISPOSITIONS – PARTIAL DISPOSITION ELECTION

• Partial disposition election made in taxable year in which disposition occurs

• Late election may be made through accounting method change only when on exam, repair deduction is recharacterized as capital improvement

31 // experience access

31 // experience access

DISPOSITIONS – DETERMINING ASSET BASIS

• For partial dispositions When specific identification of unadjusted depreciable basis is impractical, i.e., disposition asset is a component of larger asset—use any reasonable, consistent method to determine basis of disposition

• The following are nonexclusive reasonable methods from proposed regulations

o Discounting cost of replacement asset to its placed-in-service year cost using Consumer Price Index

o A study allocating cost of asset to its individual components

32 // experience access

32 // experience access

10/16/2013

17

DISPOSITIONS – PARTIAL DISPOSITION EXAMPLE

• July 1, 2011 – $20,000,000 multistory officebuilding placed in service

• June 30, 2014 – Elevator replaced/partialdisposition election

• Discounted cost of replacement elevator toJuly 1, 2011 using CPI = $150,000

• Depreciation allowed or allowable throughJune 30, 2014 on retired elevator = $11,221

• Partial disposition election results in $138,779loss on retired elevator ($150,000 - $11,221)

• Capitalization required for replacementelevator

33 // experience access

33 // experience access

DISPOSITIONS – GENERAL ASSET ACCOUNTS

• No loss on disposition recognized until all assets in GAA disposed of

o Limited qualified disposition availability

o Gain/loss recognized on disposition of all or last asset in GAA

• Special rules for partial dispositions of assets included in a GAA

34 // experience access

GAA ELECTION FOR OWNER OR LESSEE OF REAL PROPERTYNO LONGER GENERALLY RECOMMENDED BECAUSE OF NEW

PARTIAL DISPOSITION RULES

34 // experience access

10/16/2013

18

WHAT YOU NEED TO DO NOW

• Meet with BKD tax advisoro Tailor rules to you

• Discern written capitalization policyo Revisit expensing thresholds

• Inventory existing repair expense versus capitalization methods

o Document decision processes

• Scrub depreciation scheduleso Potential additional tax write-offs

• Prepare strategy – accounting method changes

35 // experience access

Questions?

10/16/2013

19

Thank You!

Rick Klahsen | Partner | 816.221.6380 | [email protected] Conner | National Tax Assistant Director | 417.831.4763 | [email protected] Humphrey | National Tax Assistant Director | 417.831.4763 | [email protected]

CONTINUING PROFESSIONAL EDUCATION (CPE) CREDITS

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org.

The information in BKD webinars is presented by BKD professionals, but applying specific information to your

situation requires careful consideration of facts & circumstances. Consult your BKD advisor before acting

on any matters covered in these webinars.

38 // experience access

10/16/2013

20

CPE CREDIT

• Up to 1 CPE credit will be awarded upon verification of participant attendance; however, credits may vary depending on state guidelines

• For questions, concerns or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected]

39 // experience access

Top Related