Languages

Pages

Legal

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 1/82

THE PROJECT REPORTON

PERCEPTION OF PEOPLE ABOUT MUTUAL

FUND

(Submitted in the partial fulfillment for thedegree of

Master of Business Administration)

PUNJAB TECHNICAL UNIVERSITY, JALANDHER

Session 2010-2012

Submitted To:Submitted By:

Mr. DEEPAK SOOD GurkiratSingh Tiwana

ROLL.NO.105042249860

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 2/82

RIMT COLLEGE, MANDI GOBINDGARH

2

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 3/82

ACKNOWLEDGEMENT

I am really happy and exited in representing this summer trainingproject report before you.

I must express my gratitude towards KARVY SECURITIES LTD for

giving mean opportunity to work with on this report.

And of course I am very much thankful to our honorable Prof. Sunil

(PROJECT GUIDE) for giving me opportunity and his guidance helpsme throughout preparing this report. He has also me valuablesuggestions and excellence guidance about this training, which

proved very helpful to me to utilize my theoretical knowledge inpractical field.

At last I am also thankful to my friends, to all known and unknownindividuals who have given me their constructive advice, educative

suggestions, encouragement, co-operation and motivation to

prepare this report.

3

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 4/82

INTRODUCTION COMPANY DETAILS

Background

Karvy Consultant limited was established in 1982 at Hyderabad. Itwas established by group of Hyderabad- based practicing

chartered accountants. At initial stage it was very small in size. Itwas started with capital of 1, 50,000.

In starting it was only offering auditing and taxation services.

Later it acts into the registrar and share transfer activities andsubsequently into financial services and other services like

financial product distribution, investment advisory services,corporate finance, insurance etc.

All along, Karvy’s strong work ethics and professional background

leveraged with information technology enabled it to deliverquality to the individual. A decade of commitment, professional

integrity and vision helped Karvy achieving a leadership positionin its field when it handled largest number of corporate and retailthat proved to be a sound business synergy.

Today, Karvy has access to millions of Indian shareholders,

besides companies, banks, financial institutions and regulatoryagencies. Over the past one and half decades, Karvy has evolvedas a veritable link between industry, finance and people.

In January 1998, Karvy became first depository participant in

Andhra Pradesh. An ISO 9002 company, Karvy’s commitment toquality and retail reach has made it an integrated FinancialServices company.

Today, Company has230 branch offices in 164 cities all over the

India The Company adds 5 new offices every year to thecompanies ever growing nation network in every nook and cornerof the country. The company services over 16 million individualinvestors, 180corporate and handles corporate disbursement that

exceeds Rs.2500 Cores.

4

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 5/82

WHERE KARVY STAND IN THE MARKET?

Karvy is a legendary name in financial services, Karvy’s credit is

defined by its mission to succeed, passion for professionalism,

excellent work ethics and customer centric values. Today Karvy is well known as a premier financial services

enterprise, offering a broad spectrum of customized services toits clients, both corporate and retail. Services that Karvy

constantly upgrade and improve are because of company’s skillin leveraging technology. Being one of the most tecno-savyorganizations around helps company to deliver even more cost

effective financial solution in the shortest possible time.

What bears sample testimony to Karvy’s success is the faith

response in company by valued investor and customers, allacross the country. Indeed with Karvy wide network touchingevery corner of the country. Even the most remote investor can

easily access Karvy’s services and benefit from company’s expertadvice.

5

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 6/82

MISSION STATEMENT OF “KARVY

An organization exists to accomplish something or achieve

something. The mission statement indicates what an organization

wants to achieve. The mission statement may be changedperiodically to take advantage of new opportunities or respond tonew market conditions.

Karvy’s mission statement is “To bring Industry, Finance and

people together”.

Karvy is work as intermediary between industry and people.Karvy work as investment advisor and helps people to invest their

money same way Karvy helps industry in achieving finance frompeople by issuing shares, debentures, bonds, mutual funds, fixed

deposits etc.

Company’s mission statement is clear and thoughtful which guidegeographically dispersed employees to work independently yet

collectively towards achieving the organization goals.

VISION OF KARVY

Company’s vision is crystal clear and mind frame very directed.“To be pioneering financial services company. Andcontinue to grow at healthy pace, year after year, decadeafter decade. “Company’s foray into IT-enabled services and

internet business has provided an opportunity to explore newfrontiers and business solutions. To build a corporate that sets

benchmarks for others to follow.

6

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 7/82

BEHIND THE PICTURE: WHAT CUSTOMERSMATTER FOR KARVY

The under lying picture forming answer for above question is given

below.

[Fig. 1 Competitive Advantage of

Karvy]

Every year with this picture keeping in mind Karvy accelerate withrecovery revival and reappearance.

Karvy has started 2004 on a strong note with the realization tosignal some of the challenges it faced previous year. In a

competitive market and brand business, Karvy need to carefullymanage itself to avoid down trading or brand shifts by consumer.

Successful implementation of carefully crafted strategy.

Excellence in execution.

Immense learning enabling to set up a launch pad for

revitalizing itself.

Some competitive advantages are long lasting. These are intangibledifficult to replicate and thus more sustainable. Karvy has focused

on some of these to gain competitive advantage. These are:

Winning culture and desire to excel in everything Karvy do.

7

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 8/82

Strong meaningful relationship with customers along withstrategic partners in which Karvy operate and above all, its

own staff.

Karvy value and carefully nature relationships with customers. Karvy

truly believe that more than technological powers and businessprocess innovations, it focuses on relationship which has been thecorner stone of satisfying and successful in India over many years.

This has been possible with deep insight of consumer behavior aswell as market demand drivers, understanding of the arena whereto operate and quality execution-all thanks to a greater team that

makes this happen.

Karvy’s customers consider themself part of Karvy family and share

their experiences and dreams with other customers and thus Karvy

become successful not only in relating customers but also gains newcustomers from satisfied prevailing customers.

Karvy want to create a strong emotional bond with new customerspromoted by prevailing customers.

8

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 9/82

KARVY VALUES

Integrity

Responsibility

Reliability

Unity

Understanding

Excellence

Confidential

Karvy has adequate internal control system and procedurecommensurate with the size nature of its business. These system

and procedures provide reasonable assurance of maintenance of proper accounting records, reliability of financial information,

protection of resources and safe guarding of assets againstunauthorized use.

9

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 10/82

KARVY SERVICES- AN OVERVIEW

1. Stock broking

2. DE mat services

3. Investment product distribution

4. Investment advisory services

5. Corporate finance and merchant banking

6. Insurance

7. Mutual funds services

8. IT enabled services

9. Registrar and transfer agents

10. Loans

1. Stock broking:

Karvy is working as capital market intermediaries. Stock brokers are

regulated by SEBI [Stock brokers and sub brokers] regulations,

1992. The stock broker is a member of stock exchange. Stockbrokers are the intermediaries who are allowed to trade in securitieson the exchange of which they are members. They buy and sell ontheir own behalf of their clients.

Stock brokers expand their business by engaging sub broker. Subbrokers mean ” any person not being a member of stock exchangewho acts on behalf of stock brokers as an agent or otherwise for

assisting the investor in buying”.

2. Demat services

Karvy is depositary participant with the national securities

depository limited (NSDL) for trading and settlement of dematerialized shares.

Depository participants (DPs) are described as an agent of depository. They are intermediaries between the depository andthe investor. The relationship between the DPs and the depository is

governed by an agreement made between the two underdepositories act.

A DP can offer depository related services only after obtaining acertificate of registration from SEBI.

10

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 11/82

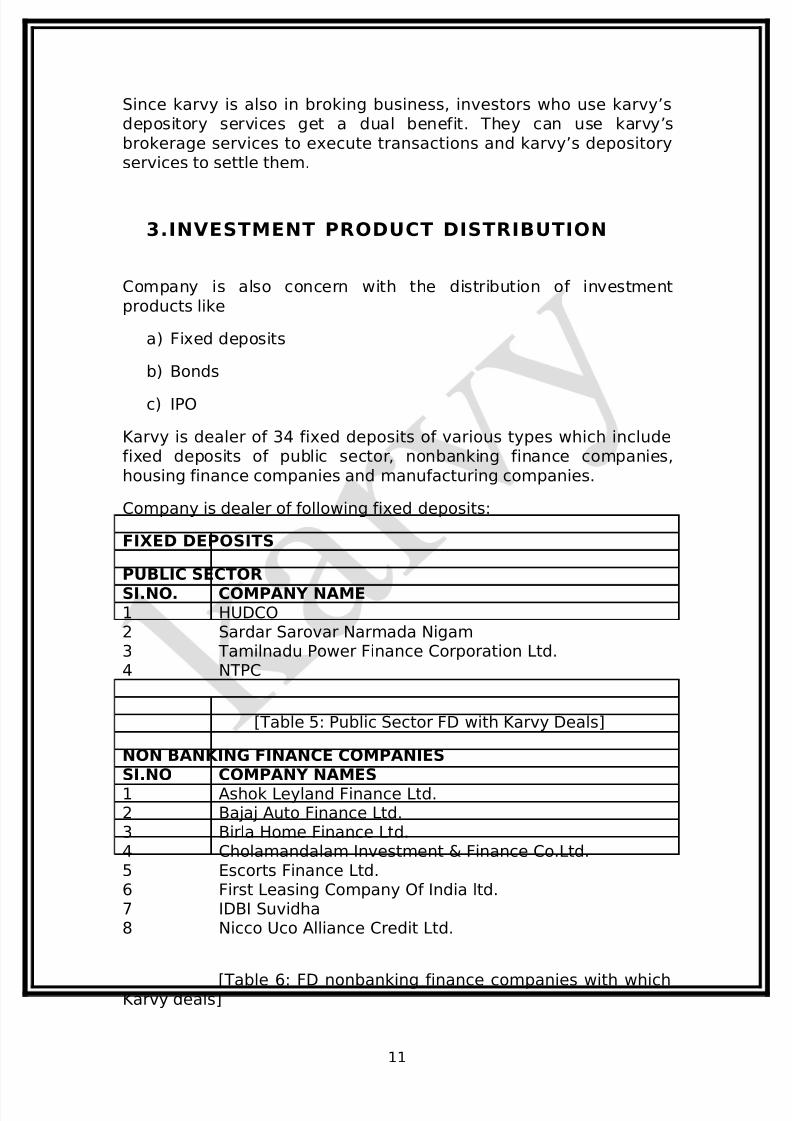

Since karvy is also in broking business, investors who use karvy’sdepository services get a dual benefit. They can use karvy’s

brokerage services to execute transactions and karvy’s depositoryservices to settle them.

3.INVESTMENT PRODUCT DISTRIBUTION

Company is also concern with the distribution of investment

products like

a) Fixed deposits

b) Bonds

c) IPO

Karvy is dealer of 34 fixed deposits of various types which includefixed deposits of public sector, nonbanking finance companies,

housing finance companies and manufacturing companies.

Company is dealer of following fixed deposits:

FIXED DEPOSITS

PUBLIC SECTOR

SI.NO. COMPANY NAME1 HUDCO2 Sardar Sarovar Narmada Nigam3 Tamilnadu Power Finance Corporation Ltd.4 NTPC

[Table 5: Public Sector FD with Karvy Deals]

NON BANKING FINANCE COMPANIESSI.NO COMPANY NAMES1 Ashok Leyland Finance Ltd.2 Bajaj Auto Finance Ltd.3 Birla Home Finance Ltd.4 Cholamandalam Investment & Finance Co.Ltd.5 Escorts Finance Ltd.6 First Leasing Company Of India ltd.7 IDBI Suvidha8 Nicco Uco Alliance Credit Ltd.

[Table 6: FD nonbanking finance companies with whichKarvy deals]

11

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 12/82

HOUSING FINANCE COMPANIESSI.NO COMPANY NAMES1 CAN Fin Homes LTD.2 Dewan Housing Finance Corporation Ltd.3 Gruh Finance Ltd.

4 HDFC Ltd.5 PNB Housing Finance Ltd.6 Sundaram Home Finance Ltd.

[Table 7: FD Housing Finance Companies with Which Karvy Deals]

MANUFACTURING COMPANIESSI.NO COMPANY NAMES1 AP Paper Mills Ltd.2 Amtek India Ltd.3 Ballarpur Industries Ltd.4 Chambal fertilizers& Chemicals Ltd.5 Escorts Ltd.6 Greaves Ltd.7 Gujarat Alkalis & Chemicals Ltd.8 Indian Express9 Indi-Swift Ltd.10 JK Industries Ltd.11 Jindal Steel & Power Ltd.12 Sound Craft Industries ltd.

13 Atul Ltd.14 Supreme Industries Ltd.15 Zauri Industries Ltd.

[Table 8: FD of Manufacturing Companies with Which KarvyDeals]

BONDS:

Karvy is dealer of following bonds

RBI Saving Bonds

NHB

REC

IPO:

12

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 13/82

Company is also provides services related to initial public offer of company. Company provides stationary at the time of IPO as well

as provides information to investor regards IPO and solve theirquarries.

INVESTMENT ADVISORY SERVICES

This division provides portfolio management services to high net-worth individuals and corporate. The expertise of Karvy in

research and stock brocking gives it the right perspective toprovide investment advisory services. Company provides

advisory services to its clients. Financial goal of each individualvaries according to his dream, ambition and family size andfuture financial planning for the children &old age pension for

their self and wife so does the path way to achieve it .Karvy applythe principles of financial planning as both science and art, it

understand the time horizon, risk bearing capacity andinvestment goals of investor to plan their entire life up to

retirement, taxes, insurance needs and other important personalfinancial goals. It design portfolio for investor to invest theirsaving in various financial products like shares, bonds,

debentures, mutual funds, fixed deposits, insurance etc.,company design portfolios by following factors.

Investors requirement of getting money back, Investors willingness to take risk,

Investors tax planning etc.

4. Corporate Finance &Merchant Banking

Corporate finance is the financial activity of corporation. It deals

with the firms operations with regard to investing and financing. It

concerned with how firms raise capital and the consequences of alternative methods of raising capital. Firm’s capital can be raisedby raising loans, issuing shares, and acquiring and merging with

other businesses by public or private companies.

Merchant banking is a financial intermediation that matches entitiesthat need capital and those that have capital. Hence they facilitate

the flow of capital in the market.

Karvy enjoy’s SEBI category (I) authorization for merchant banking.Karvy offers the full spectrum of merchant banking services,

beginning from identifying the best time for an issue to final stageof marketing it, to harvest unparalleled success.

13

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 14/82

As a merchant banker Karvy offers following services:

Issue management

Instrument designing

Pricing of the issue

Registration process for the issue of shares

Marketing efforts

Final allotment to investors

Listing details on stock exchanges

Loan syndication

Lease financing

Corporative advisory services

Under writing

Portfolio management

5. Insurance:Karvy is also dealer of many private life insurance companies. At

Jamnagar branch, company is associated with dealing of followingcompanies.

ICICI Prudential Life Insurance

HDFC Life Insurance

TATA AIG Insurance

6. Mutual fund Services:

Since its inception in 1982, Karvy has demonstrated a dedicationcoupled with dynamism that has inspired trust from varioussegments- corporate, government bodies and individuals. Karvy has

since been preforming a pivotal role as intermediary- the interface-between these players.

With mutual funds emerging as distinct asset class, Karvy has made

a strategic choice to leverage the power of latest technology to

14

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 15/82

provide a cutting edge to its services. Karvy, today, services nearly80% of the asset management companies (AMCs) across an

extensive network of services centers with assets under services inexcess of Rs. 10,000 crores.

Karvy’s ability to mass customize and offer a diverse range of product for a diverse range of customers has helped mutual fundcompanies to uniquely position themselves in the market place.

These diverse range of services cut across multiple deliverychannels- service centers, web, mobile phones, call center- has

brought home the benefits of technology to investors, distributors,and the mutual funds.

Going forward Karvy shall strive to create new products and

services, which would address the needs of end customer.Company’s single minded focus on delivering products forcustomers has given it the distinguished position of being the

preferred provider of financial services in the country.

List of mutual funds clients of Karvy:

1 Alliance Mutual Fund2 Birla Mutual Fund3 Bank of Baroda Mutual Fund

4 Can Bank Mutual Fund5 Chola Mutual Fund6 Duetsche Mutual Fund7 DSP Merrill Lynch Mutual Fund8 Franklin Templeton Investment9 GIC Mutual Fund10 HDFC Mutual Fund11 HSBC Mutual Fund12 IL & FS Mutual Fund13 JM Mutual fund14 Kotak Mutual Fund15 LIC Mutual Fund16 Punjab National Bank Mutual Fund17 Prudential ICICI Mutual Fund18 Principal Mutual Fund19 Reliance Mutual Fund20 State Bank Of India Mutual Fund21 Standard Chartered Mutual Fund22 Sundaram Mutual Fund23 SUN F&C Mutual Fund24 Tata Mutual Fund

15

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 16/82

[Table 9: List of MF companies with which karvy deals]

7. Income Tax enabled services:

Karvy has started these services since March, 2004. Karvy is work

as TIN Facilitation center it provides following IT enabled services.

a) Distribution of PAN card

b) Distribution of TAN card

c) Services related to e-TDS.

Karvy work as intermediary between NSDL and IT payers. Karvyprovides various form for different IT enabled services and guide

people to fill that forms. It also solves queries of tax payers. It alsodistributes PAN and TAN card to tax payers.

TIN OVERVIEW

National securities depository Ltd. (NSDL) has established

nationwide tax information network (TIN) on behalf of income taxdepartment (ITD). This is designed to make the tax administrationmore effective, furnishing of returns convenient, reduce compliance

cost and bring greater transparency.

While NSDL primary agency responsible for design, implementationand maintenance of TIN as per the requirements of ITD, otheragencies will also play key roles in the TIN system.

Karvy has established infrastructure required to provide IT enabled

services so, Karvy provides TIN facilitation centers all over India onbehalf of NSDL.besides Karvy following companies can also work asintermediary between NSDL and customers.

Alan kit assignments Ltd.

Integrated Enterprise Ltd.

Shell Tran Source Ltd.

16

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 17/82

[Fig 2: TIN system]

The banking system, being the agency that collects the money onbehalf of the ITD against tax obligations from the tax payers will belinked to the TIN central system to provide accounting information

on tax paid by various entities under various heads. As banks is

relatively technology to the TIN central system enabling online taxaccounting.

On the other hand, the entities depositing the tax (deductor) varysubstantially with respect to their computer skills and hence TIN

design provides for TIN facilitation centers managed by NSDL tohelp digitization and upload of tax payment related information to

the TIN central system.

Besides NSDL, UTI an investor service Ltd. May also provides itENABLED SERVICES.

17

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 18/82

8. Registrars & Transfer agents:

In 1985, Karvy entered the registrar and share transfer business to

create a market niche in competitive field of financial services. In1994-95, it reached a milestone when it processed 104 public issues

constituting 46% market share. Now its second decade of existence,Karvy is the leader in the industry: in an opinion poll conducted byan independent market research agency-MARG, Karvy has been

rated as India’s most admired registrar on various parameters:-

Overall Excellence

Handling of volumes

Timely Dispatch

Quality management and technological up gradation.

A SEBI category 1 registrar, so far, Karvy has handled over 675issues as registrar to public issues processed over 52 millionapplications and is servicing over 16 million investors from various

locations spread over205 clients.

9.Loan:

Karvy has recently started his services at selected branches of metro cities. This service has not been started in saurashtra- kucch

region. Karvy provides loans for following.

Vehicle loan

Home loan

Personal loan

18

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 19/82

MARKETING STRATEGY OF KARVY

Market poisoning:

Market positioning statements of Karvy are “At karvy we give you

single window service” we also ensure your comfort.

So, Karvy focus on the consumers who prefer almost all investmentactivities at same place by providing number of various financial

services. At Karvy a person can purchase or sell shares, debenturesetc. at same place also demat it. Karvy also provide other

investment options to the same person at same place like mutualfund, insurance, fixed deposits, bonds etc. Help the person indesigning his portfolio. By this way Karvy comfort to its consumers.

Karvy is also positioned according to rise and trout. Karvy ispromoted as a no. 1 investment product distributor and R&T agentof India.

Target Marketing:

Karvy uses demographic segmentation strategy and segmentpeople based on their occupation. Karvy uses selective

specialization strategy for market targeting. Target person for theKarvy stock broking and Karvy investment services are persons who

can work as sub-brokers for the company. Companies focus onadvisors of insurance and post office, Tax consultants and CAs for

making sub- brokers.

Marketing channel system:

Karvy uses one level marketing channel for investment product

distribution. Sub-brokers work as intermediary between consumerand company. Company has both forward and backward flow of

activity through channel. Company distribute stationary, brokerage,and information forward to its sub-brokers send filled forms, queries,amount of investment etc. back to company.

Training channel members:

Karvy provide the training to the sub-brokers because they will beviewed as the company by the investors. The executive of karvy

explain various new schemes of investment to the sub-brokers with

its objective, risk factor and expected return. Company alsoperiodically arrange seminar to guide sub-brokers.

19

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 20/82

Advertising and promotion:

The objective of advertising of Karvy is to create awareness about

services of Karvy among investors and sub-brokers and increasesub-brokers of karvy.

Company doesn’t give advertisement in media like TV, Newspaper,and Magazines etc. Karvy’s advertisement is made indirectly by the

companies associate with it. Karvy is R&T agent of around 700companies. They publish name, address and logo of karvy on their

annual report.

Karvy also publish its weekly stock market newsletter “karvybazaar” baatein’ and monthly magazine” the fin polis” to guide

investors and sub-brokers about market.

20

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 21/82

HR POLICY OF KARVY

Recruitment and Selection Policy: The upper level members like zonal managers, regional members,branch managers and senior executives are recruited by publishing

recruitment advertisement in leading national level newspaper. Thequalified applicant are then called for interview and selected.

The regional manager has authority to select lower level employeelike peon, marketing executives, accountant etc. by approval of zonal manager.

Training and Development:

Continuous training and upgrading technical, behavioral andmanagerial skills is a way of life in Karvy. Karvy encouragesemployees to hone their skills regularly to enable them to face the

challenges of the changing requirements of customers that fitmarket up and down.

Training needs analysis is done on a regular basis and systematic

methodologies are ensured that skills and capabilities of allemployees are constantly upgraded to enable them to perform in

the challenging work environment.

New employee has given training under experienced employee. Thenew employee work under experience employee and observe his all

activities. When company employs new technology or there is anychance in the working of the company the training program is

arranged.

21

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 22/82

HR POLICY OF KARVY

[Fig 4 Branch level structure of Karvy]

22

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 23/82

Quality Policy of Karvy:

To achieve and retain leadership, Karvy shall aim for complete

customer satisfaction, by combining its human and technologicalresources, to provide superior quality financial services. In theprocess, Karvy will strive to exceed customer’s expectations.

Quality Objectives of Karvy:

Build in- hours processes that will ensure transparent

and harmonious relationship with its clients andinvestors to provide high quality of services.

Establish a partner relationship with its investor servicesand agents and vendors that will help in keeping up its

commitment to the customers.

Provide high quality of work life for all its employees and

equip them with adequate knowledge and skills so as torespond to customers needs.

Continue to uphold the value of honesty and integrityand strive to establish unparalleled standards in

business ethics.

Use state-of-the art information technology indeveloping new and innovative financial products and

services to meet the changing needs of investors andclients.

Strive to be a reliable source of value added financial

product and services aand constantly guide theindividuals and institutions in making a judious choice of

same.

Strive to keep all the stake holders ( shareholders,

clients, investors, employ, suppliers, and regulatoryauthorities) proud and satisfied.

23

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 24/82

Achievements of Karvy:

Largest mobilizer of funds as per PRIME DATABASE

First ISO – 9002 certified registrar in india

A category- 1Registrar to public issues

A category- 1 Merchant Banker

Ranked as “The most admired registrar” by MARG

Handled the largest – ever public issues – IDBI

Strategic tie-up with jardine fleming India securities Ltd.

Handled over 500 public issues as registrars

Handling the reliance account which accounts for nearly 10

million account holders

First depository participant from Andhra Pradesh

24

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 25/82

SWOT ANALYSIS OF KARVY Strengths:

Employees are highly empowered.

Strong communication network.

Good co-operation between employees.

Number 1 registrar andtransfer agent in India

Number 1 dealer of investment products in india.

Weaknesses:

High employee turnover.

Opportunity:

Growth rate of mutual fund industry is 40 to 50% during lastyear and it expected that this rate will be maintained in future

also.

Marketing at rural and semi-urban areas.

Threats:

Increasing number of local players.

Past image of mutual fund.

25

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 26/82

1.1 GENERAL INTRODUCTION

Mutual fund is a pool of funds which is divided into units of equalvalue and sold to investing public and the funds so collected are

utilized for collective investments in various capitals and money

market instrument. In today’s market people invest money to gain

more. So when they take into account, they mostly look out for

Investment Company where they can get more income.

Investment companies can be classified into closed-end and open-

end investment companies. Closed-end is when it is readily

transferable in the market. Open-end funds sell their own shares to

investors and ready to buy back their old shares. If we talk about

the investment options today, in India we have so many investment

companies like UTI, LIC etc, all have their own special ways of

servicing the customers. The investors also feel that they are worth

to be the part of that company. These days’ people mainly look for

avoiding tax so normally they look out for some investments which

can help them in doing so. When it comes to this point of view,

people mainly look out for mutual fund.

Mutual fund is a trust at law; it is a special type of managed, pooled

portfolio financial company or financial service organization that

sells shares/units/stocks in itself, to the public to obtain its resources

and it invests the savings so mobilized or pooled in a large,

diversified, & sound portfolio of equity shares, bonds, money market

instruments etc., Redeemable trust certificates are sold to investors

at net asset value (NAV) plus a small commission. All

interest/dividend and principal repayments are distributed to the

holders of the certificates.

26

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 27/82

1.2 THEORETICAL BACKGROUND

Meaning of Mutual Funds

Mutual fund is a pool of funds which is divided into units of equal

value and sold to investing public and the funds so collected are

utilized for collective investment in various capital and money

market instrument. Investment is a commitment of a person’s funds

to derive future income in the form of interest, dividends, rent,

premiums, pension benefits or the appreciation of the value of their

principal capital. Investments have a return but there can be no

return without risk.

Definitions

Different persons in different words have defined mutual fund.

The SEBI (MF) Regulations, 1993 defines mutual fund as “A fund

established in the form of a trust by a sponsor to raise money by the

trustees through the sale of units to the public under one or more

schemes for investing in securities in accordance with these

regulations.”

Investment is the allocation of monetary resources to assets

that are expected to yield some gain or positive return over a given

period of time. These assets range from safe investments to risky

investments. Investments in this form are also called ‘Financial

Investments’.

27

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 28/82

Characteristics of MF

A mutual fund actually belongs to the investors who have

pooled their funds. The ownership of the MF is in the hands of

the investors.

A MF is managed by investment professionals and other

service providers, who earn a fee for their services from the

fund.

The pool of funds is invested in a portfolio of marketable

investment. The value of the portfolio is updated every day.

The investor’s share in the fund is denominated by units. The

value of the units changes with change in the portfolio’s value,

every day. The value of one unit of investment is called as the

net assets value or NAV.

The investment portfolio of the Mutual fund is vested

according to the stated Investment objectives of the fund.

Investment Company

A company or trust that uses its capital to invest in other

companies. There are two principal types – closed-ended and the

open-ended. Shares in closed-ended investment companies, some

of which are listed on the New York Stock Exchange are readily

transferable in the open market and are bought and sold like other

shares.

28

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 29/82

Open-ended funds sell their own shares to investors, stand ready to

buy back their old shares and are not listed. These funds are so

called because their capitalization is not fixed; they issue more

shares as people want them.

Fig.1.1 Concept of Mutual Fund Industry

When an investor subscribes for the units of a mutual fund, hebecomes part owner of the assets of the fund in the same

29

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 30/82

proportion as his contribution amount put up with the corpus (thetotal amount of the fund). Mutual Fund investor is also known as a

mutual fund shareholder or a unit holder. Any change in the value of the investments made into capital market instruments (such as

shares, debentures etc) is reflected in the Net Asset Value (NAV) of

the scheme. NAV is defined as the market value of the Mutual Fundscheme's assets net of its liabilities. NAV of a scheme is calculated

by dividing the market value of scheme's assets by the total numberof units issued to the investors.

CONSTITUENTS OF MUTUAL FUND

There are many entities involved and the diagram below illus

trates the constitution of a mutual fund:

Fig.1.2 Constituents of Mutual Fund Industry

30

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 31/82

Formation process starts from sponsor {the investment advisor or

manager}. Sponsor selects & appoints the Board of Trustees.

Trustees again hire or contract a separate AMC that is run by

professional managers. The AMC conducts the necessary research &

based on it, manages the fund or portfolio. It is responsible for

floating, managing, redeeming the schemes; it also handles the

administrative chares. It receives the fees for the services rendered

by it. The custodian is responsible for co-ordination with brokers, the

actual transfer & storage of stocks, & handling the property of the

trust.

Finally the unit holders are investors from who a pool of money is

collected & invested according to the stated investment objectives.

Mutual fund investors are like share holders & they own the fund.

They are neither lenders nor the deposit holders in the fund. Unlike

a holder of stock of company, unit holders have no voting rights.

Organization of a Mutual Fund

All mutual funds comprise four constituents – Sponsors, Trustees,

Asset Management Company (AMC) and Custodians.

1. Sponsors:

The sponsors initiate the idea to set up a mutual fund. It could be a

registered company, scheduled bank or financial institution. A

sponsor has to satisfy certain conditions, such as capital, record (at

least five years’ operation in financial services), de-fault free

dealings and general reputation of fairness. The sponsors appoint

the Trustee, AMC and Custodian. Once the AMC is formed, thesponsor is just a stakeholder.

31

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 32/82

2. Trust/ Board of Trustees:

Trustees hold a fiduciary responsibility towards unit holders by

protecting their interests. Trustees float and market schemes, and

secure necessary approvals. They check if the AMC’s investments

are within well-defined limits, whether the fund’s assets are

protected, and also ensure that unit holders get their due returns.

They also review any due diligence by the AMC. For major decisions

concerning the fund, they have to take the unit holders consent.

They submit reports every six months to SEBI; investors get an

annual report. Trustees are paid annually out of the fund’s assets –

0.5 percent of the weekly net asset value.

3. Fund Managers/ AMC:

They are the ones who manage money of the investors. An AMC

takes decisions, compensates investors through dividends,

maintains proper accounting and information for pricing of units,

calculates the NAV, and provides information on listed schemes. It

also exercises due diligence on investments, and submits quarterly

reports to the trustees. A fund’s AMC can neither act for any other

fund nor undertake any business other than asset management. Its

net worth should not fall below Rs. 10 crore. And, its fee should not

exceed 1.25 percent if collections are below Rs. 100 crore and 1

percent if collections are above Rs. 100 crore. SEBI can pull up an

AMC if it deviates from its prescribed role.

4. Custodian:

Often an independent organization, it takes custody of securities

and other assets of mutual fund. Its responsibilities include receipt

and delivery of securities, collecting income-distributing dividends,

safekeeping of the units and segregating assets and settlements

32

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 33/82

between schemes. Their charges range between 0.15-0.20 percent

of the net value of the holding. Custodians can service more than

one fund.

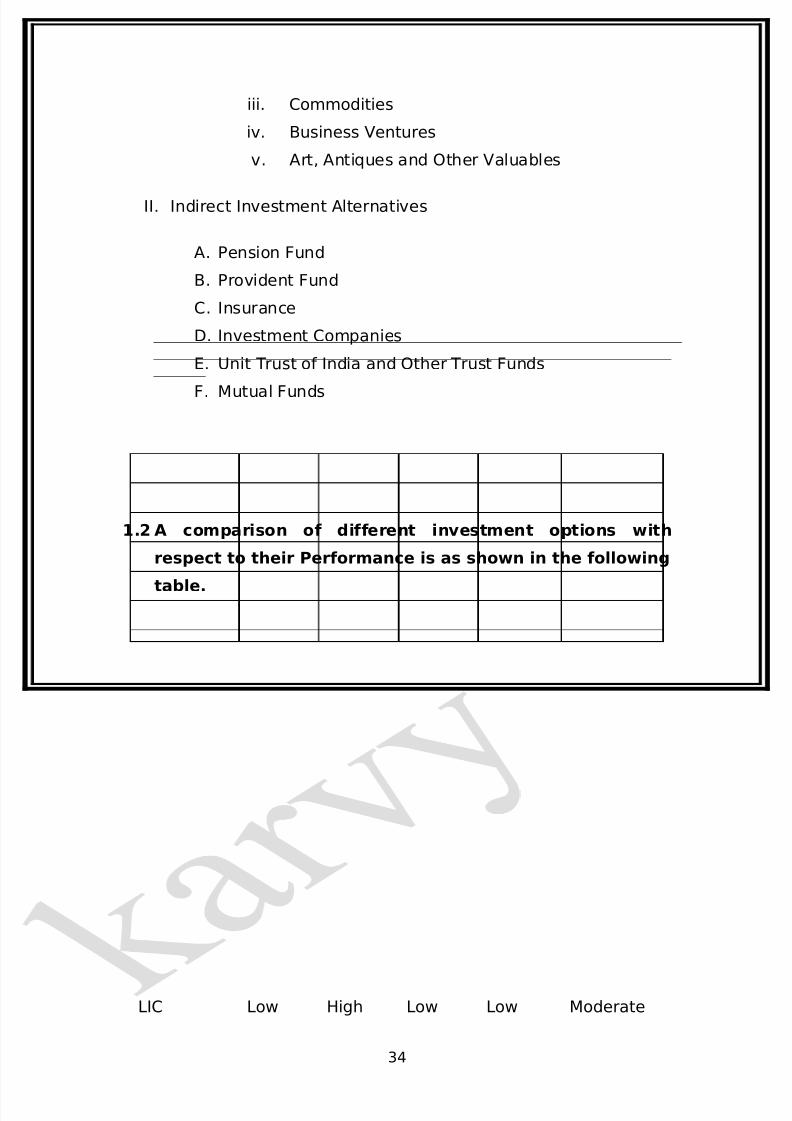

Investment Alternatives

I. Direct Investment Alternatives

A. Fixed Principal Investments

i. Cash

ii. Savings account

iii. Savings Certificate

iv. Government Bonds

v. Corporate Bonds and Debentures

B. Variable Principle Securities

i. Equity Shares

ii. Convertible Debentures or Preference

Securities

C. Non-Security Investments

i. Real Estate

ii. Mortgages

33

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 34/82

iii. Commodities

iv. Business Ventures

v. Art, Antiques and Other Valuables

II. Indirect Investment Alternatives

A. Pension Fund

B. Provident Fund

C. Insurance

D. Investment Companies

E. Unit Trust of India and Other Trust Funds

F. Mutual Funds

1.2 A comparison of different investment options with

respect to their Performance is as shown in the following

table.

Options Returns Safety Volatilit

y

Liquidity Convenien

ceEquity High Low High High/Lo

w

Moderate

FI Bond Modera

te

High Modera

te

Moderat

e

High

Debentures Modera

te

Modera

te

Modera

te

Low Low

Company

FD

Modera

te

Low Low Low Moderate

PPF Modera

te

High Low Moderat

e

High

LIC Low High Low Low Moderate

34

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 35/82

Gold Modera

te

High Modera

te

Moderat

e

Low

Real Estate High Modera

te

High Low Low

Mutual

Fund

High High Modera

te

High High

Bank

Deposit

Low High Low High High

Financial Institutions:

Financial institutions are business organizations that act as

mobilizes & depositors of savings & purveyors of credit or finance.

Financial Institutions are engaged in these activities

Financing by way of loans, advances, and so on any activity

except its own.

Acquisition of shares/ stocks/ bonds/ debentures/ securities

Hire- purchase

Any class of insurance, stock- broking, etc.

Chit funds and

35

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 36/82

Financial

Financial

MarketsFinancial

Instruments

Financial

Services

Intermediaries

Banking

OthersNon-

intermediaries

Regulat

Financial

Institutions

Collection of money by way of subscription/ sale of units or

other instruments/ any other manner and their disbursement.

Fig 1.4. Typical Financial System

36

Non-

banking UnorganizedPrimaryOrganizShor

Secondary

SecondaryMoney

Market

Capital

Market

Long

term

Medium

term

Primary

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 37/82

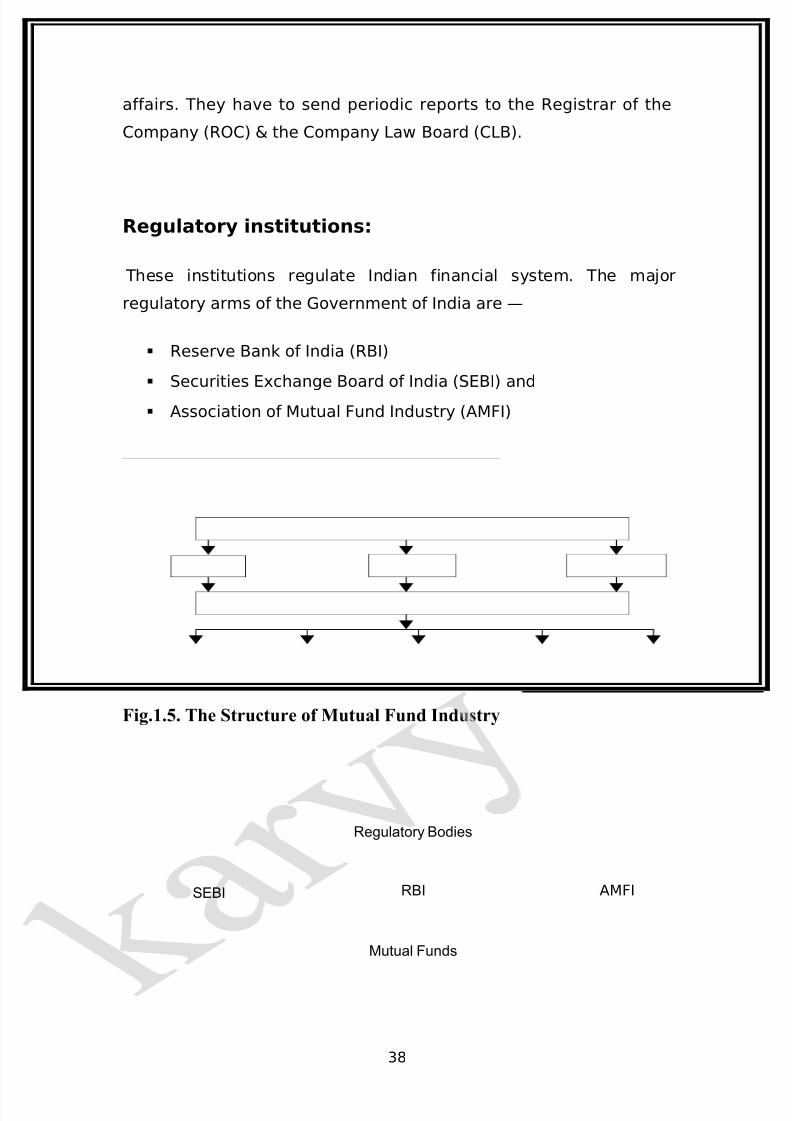

LEGAL & REGULATORY FRAME WORK:

Mutual funds are regulated by the SEBI (Mutual Fund) Regulations1996. SEBI is the regulator of all funds except off share funds.

Where as Bank-sponsored mutual funds are jointly regulated jointly

by SEBI & RBI.

RBI also regulates money market & Government. Securities Markets,

in which mutual funds invest. Since the AMC & Trustee Company is

Companies, they are regulated by the department of Company

37

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 38/82

affairs. They have to send periodic reports to the Registrar of the

Company (ROC) & the Company Law Board (CLB).

Regulatory institutions:

These institutions regulate Indian financial system. The major

regulatory arms of the Government of India are —

Reserve Bank of India (RBI)

Securities Exchange Board of India (SEBI) and

Association of Mutual Fund Industry (AMFI)

Fig.1.5. The Structure of Mutual Fund Industry

38

AMFISEBI RBI

Mutual Funds

Regulatory Bodies

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 39/82

THE RESERVE BANK OF INDIA ( RBI ):

The RBI as the central bank of the country is the center of the Indian

financial and monetary system. As the apex institution it has been

guiding monitoring, regulating controlling and promoting the destiny

of the Indian Financial System since its inception. It started

functioning from April 1, 1935 on the terms of the reserve Bank of

India Act 1934. It was a shareholders’ institution till January 1949,

after which it become a state-owned institution under the reserve

Bank (transfer to public ownership) of India Act, 1948.

39

Sponsor AMC CustodianTrustee

Public Sector Funds Private Sector Funds

Investor

Bank

Sponsored

Financial Institutions

Sponsored

Domestic

Schemes

Offshore

Closed ended

UTI

Open ended

Growth

Funds

Income

Funds

Balanced

Funds

Sect oral

Funds

Special purpose

Funds

Tax saving

Funds

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 40/82

FUNCTIONS OF RBI

SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI)

The SEBI was established on April.12.1982 through an

administrative order, but it became a statutory and really powerful

organization only since 1992. SEBI was set up on 21st

February.1992 through an ordinance issued on 30th January.1992.

The SEBI Act on 4th April.1992 replaced the ordinance. The SEBI is

under the overall control of the ministry of Finance, and it has head

office at Mumbai. It has now become a very important constituent of

the financial regulatory framework in India.

OBJECTIVES:

40

Central banking functions

Supervisory functions

Promotional functions

Monetary planning and

control system

F

U

N

C

T

I

O

N

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 41/82

To regulate stock exchanges & securities industry to promote

their orderly functioning.

To protect the interest of investors so that there is a steadyflow of savings in to the capital market and educating

individual investors.

To prevent trading malpractices and aims at achieving a

balance between self-regulation by securities industry and its

statutory regulation.

ASSOCIATION OF MUTUAL FUND INDUSTRY (AMFI)

AMFI is an Industry Association. AMFI is not yet the Self

Regulatory Organization (SRO), though SEBI consults AMFI on a

number of issues. AMFI can only issue guidelines. The objectives of

AMFI are-

To define and maintain high professional and ethical

standards in all areas of operation of mutual fund industry

41

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 42/82

To interact with the Securities and Exchange Board of India

(SEBI) and to represent to SEBI on all matters concerning the

mutual fund industry.

To represent to the Government, Reserve Bank of India and

other bodies on all matters relating to the Mutual Fund

Industry.

To undertake nation wide investor awareness programme so

as to promote proper understanding of the concept and

working of mutual funds.

To disseminate information on Mutual Fund Industry and to

undertake studies and research directly and/or in association

with other bodies.

INDIAN MUTUAL FUND INDUSTRY

Structure Of The Indian Mutual Fund Industry

Structure wise Mutual fund Industry can be classified in to three

categories:

Unit Trust of India

42

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 43/82

The Indian Mutual Fund industry is dominated by the Unit Trust of

India, which has a total corpus of Rs.51,100 crore collected from

over 20 million investors. The UTI has many funds/ schemes in all

categories i.e. Equity, Balanced, Debt, Money Market etc. With somebeing open ended and some being closed ended. The Unit scheme

1964 commonly referred to as US 64, which is a balanced fund, it is

the biggest scheme with a corpus of about 10,000 crore.

Public Sector Mutual Funds

The second largest categories of mutual funds are the ones floated

by nationalized banks. Canbank asset management floated by

Canara Bank and SBI Funds Management floated by State Bank of

India are the largest of these. GIC AMC floated by General Insurance

Corporation and Jeevan Bima Sahayog AMC floated by the LIC are

some of the other prominent ones. The aggregate corpus of the

funds managed by this category of AMC’s is around Rs. 8,300 crore.

Private Sector Mutual fund

The third largest categories of mutual funds are the ones floated by

the Private Sector Domestic Mutual funds and the Private Sector

Foreign Mutual Funds. The largest of these in Private Sector

Domestic Mutual funds are Cholamandalam Asset Management

Co.Ltd., J.M Capital Management Co. Ltd., Escort Asset Management

Ltd., Birla Sun Life Asset Management Pvt.Ltd., and in Private Sector

Foreign Mutual Funds these are Alliance Capital Asset Management

Pvt.Ltd., Prudential ICICI Management Co. Ltd. The aggregate corpus

of the assets managed by this category of AMC’s is about Rs. 42,200

crore .

History of the Indian Mutual Fund Industry

The mutual fund industry in India started in 1963 with the formation

of Unit Trust of India, at the initiative of the Government of India and

43

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 44/82

Reserve Bank the. The history of mutual funds in India can be

broadly divided into four distinct phases

First Phase – 1964-87

An Act of Parliament established Unit Trust of India (UTI) on 1963. It

was set up by the Reserve Bank of India and functioned under the

Regulatory and administrative control of the Reserve Bank of India.

In 1978 UTI was de-linked from the RBI and the Industrial

Development Bank of India (IDBI) took over the regulatory and

administrative control in place of RBI. The first scheme launched by

UTI was Unit Scheme 1964. At the end of 1988 UTI had Rs.6, 700

crores of assets under management.

Second Phase – 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set

up by public sector banks and Life Insurance Corporation of India

(LIC) and General Insurance Corporation of India (GIC). SBI Mutual

Fund was the first non- UTI Mutual Fund established in June 1987

followed by Can bank Mutual Fund (Dec 87), Punjab National Bank

Mutual Fund (Aug 89), Indian Bank Mutual Fund (Nov 89), Bank of

India (Jun 90), Bank of Baroda Mutual Fund (Oct 92). LIC established

its mutual fund in June 1989 while GIC had set up its mutual fund in

December 1990. At the end of 1993, the mutual fund industry had

assets under management of Rs.47, 004 crores.

Third Phase – 1993-2003 (Entry of Private Sector Funds)

44

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 45/82

With the entry of private sector funds in 1993, a new era started in

the Indian mutual fund industry, giving the Indian investors a wider

choice of fund families. Also, 1993 was the year in which the first

Mutual Fund Regulations came into being, under which all mutualfunds, except UTI were to be registered and governed. The erstwhile

Kothari Pioneer (now merged with Franklin Templeton) was the first

private sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a

more comprehensive and revised Mutual Fund Regulations in 1996.

The industry now functions under the SEBI (Mutual Fund)

Regulations 1996. The number of mutual fund houses went on

increasing, with many foreign mutual funds setting up funds in India

and also the industry has witnessed several mergers and

acquisitions. As at the end of January 2003, there were 33 mutual

funds with total assets of Rs. 1,21,805 crores. The Unit Trust of India

with Rs.44, 541 crores of assets under management was way ahead

of other mutual funds.

Fourth Phase – since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was

bifurcated into two separate entities. One is the Specified Undertaking of the Unit

Trust of India with assets under management of Rs.29,835 crores as at the end of

January 2003, representing broadly, the assets of US 64 scheme, assured return and

certain other schemes. The Specified Undertaking of Unit Trust of India, functioning

under an administrator and under the rules framed by Government of India and does

not come under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is

registered with SEBI and functions under the Mutual Fund Regulations. With the

bifurcation of the erstwhile UTI which had in March 2000 more than Rs.76,000 crores

of assets under management and with the setting up of a UTI Mutual Fund,

conforming to the SEBI Mutual Fund Regulations, and with recent mergers taking

place among different private sector funds, the mutual fund industry has entered its

45

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 46/82

current phase of consolidation and growth. As at the end of October 31, 2003, there

were 31 funds, which manage assets of Rs.126726 crores under 386 schemes.

The graph indicates the growth of assets over the

years.

GROWTH IN ASSETS UNDER MANAGEMENT

46

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 47/82

47

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 48/82

Future of Mutual Funds in India

By December 2004, Indian mutual fund industry reached Rs

1,50,537 crore. It is estimated that by 2010 March-end, the

total assets of all scheduled commercial banks should be Rs

40,90,000 crore.

The annual composite rate of growth is expected 13.4%

during the rest of the decade. In the last 5 years we have

seen annual growth rate of 9%. According to the current

growth rate, by year 2010, mutual fund assets will be

double.

Some facts for the growth of mutual funds in India :

• 100% growth in the last 6 years.

• Number of foreign AMC's are in the que to enter the

Indian markets like Fidelity Investments, US based, with

over US$1trillion assets under management worldwide.

• Our saving rate is over 23%, highest in the world.

Only channelizing these savings in mutual funds sector is

required.

• We have approximately 29 mutual funds which is

much less than US having more than 800. There is a big

scope for expansion.

• 'B' and 'C' class cities are growing rapidly. Today most

of the mutual funds are concentrating on the 'A' class cities.

Soon they will find scope in the growing cities.

• Mutual fund can penetrate rurals like the Indian

insurance industry with simple and limited products.

• SEBI allowing the MF's to launch commodity mutual

funds.

• Emphasis on better corporate governance.

• Trying to curb the late trading practices.

48

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 49/82

• Introduction of Financial Planners who can provide

need based advice.

INDIAN INDUSTRY DETAILS

Following are the list of mutual fund companies in India.

SI.NO Mutual fund name No. of schemes

1 Alliance Mutual Fund 362 Benchmark Mutual Fund 53 Birla Mutual Fund 74

4 Bank Baroda Mutual Fund 175 Can Mutual Fund 256 Chola Mutual Fund 457 Deutsche Mutual Fund 408 DSP Merrill Lunch Mutual Fund 409 Escort Mutual Fund 1510 Franklin Templeton Investment 13011 GIC Mutual Fund 512 HDFC Mutual Fund 7913 HSBC Mutual Fund 32

14 IL & FS Mutual Fund 4315 ING Vysya Mutual Fund 5516 JM Mutual Fund 5517 Kotak Mutual Funds 5618 LIC Mutual Funds 3519 Morgan Stanley Mutual Fund 120 Punjab National Bank Mutual Fund 421 Prudential ICICI Mutual Fund 12422 Principal Mutual Fund 6823 Reliance Mutual Fund 74

24 Sahara Mutual Fund 1225 State Bank Of India Mutual Fund 5926 Standard Chartered Mutual Fund 10027 Sundaram Mutual Fund 5228 SUN F & C Mutual Fund 129 Tata TD Mutual Fund 10030 Taurus Mutual Fund 931 Unit Trust Of India 4232 UTI Mutual Fund 66

[Table 10: Mutual Fund In India]

49

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 50/82

ADVANTAGES OF MUTUAL FUNDS: -

If mutual funds are emerging as the favorite investment vehicle, it is

because of the many advantages they have over other forms and

avenues of investing, particularly for the investor who has limited

resources available in terms of capital and ability to carry out

detailed research and market monitoring. The following are the

major advantages offered by mutual funds to all investors:

• Portfolio diversification:

Mutual Funds normally invest in a well-diversified portfolio or

securities. Each investor in a fund is a part owner of all of the

fund’s assets. This enables him to hold a diversified

investment portfolio even with a small amount of investment

that would otherwise require big capital.

• Professional Management:

Even if and investor has a big amount of capital available to

him, he benefits from the professional management skills

brought in the management of the investor’s portfolio. The

investment management skills, along with the needed

research into available investment options, ensure a much

better return than what an investor can manage on his own.

Few investors have the skills and resources of their own to

succeed in today’s fast moving, global and sophisticated

markets.

• Reduction/Diversification of Risk:

50

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 51/82

An investor in a mutual fund acquires a diversified portfolio,

no matter how small his investment. Diversification reduces

the risk of loss, as compared to investing directly in one or two

shares or debentures or other instruments. When and investorinvests directly, all in the pool of funds with other investors,

any loss on one or two securities is also shared with other

investors. This risk reduction is one of the most important

benefits of a collective investment vehicle like the mutual

fund.

• Reduction of transaction cost:

What is true of risk is also true of the transaction costs. A

direct investor bears all the costs of investing such as

brokerage or custody of securities. When going through a

fund. He has the benefit of economies of scale; the funds pay

lesser costs because of larger volumes, a benefit passed on to

its investors.

• Liquidity:

Often, investors hold shares or bonds they cannot directly,

easily and quickly sell. Investment in a mutual fund, on the

other hand, is more liquid. An investor can liquidate the

investment, by selling the units to the fund if open-end or

selling them in the market if the fund is closed-end, and

collect funds at the end of a period specified by the mutual

fund or the stock market.

• Convenience and Flexibility:

Mutual Fund management companies offer many investor

services that a direct market investor cannot get. Investors

can easily transfer their holdings from one scheme to the

other; get updated market information, and so on.

51

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 52/82

RISK FACTORS ASSOCIATED WITH MUTUAL FUNDS

Mutual funds & securities investments are subject to

market risks and there is no assurance or guarantee

that the objectives of the Scheme will be achieved.

Past performance of the Sponsor or that of existing

Schemes of the Fund does not indicate the future

performance of the Schemes.

As with any securities investment, the NAV of the Units

issued under the scheme can go up or down depending

on the factors and forces affecting the capital and

money market.

Tax laws may change, affecting the return on

investment in Units.

TYPES OF MUTUAL FUND SCHEMES

I. Schemes according to Maturity Period:

A mutual fund scheme can be classified into open-ended scheme or

close-ended scheme depending on its maturity period.

i. Open-ended Fund/ Scheme

An open-ended fund or scheme is one that is available for

subscription and repurchase on a continuous basis. These schemes

do not have a fixed maturity period. Investors can conveniently buy

and sell units at Net Asset Value (NAV) related prices which are

52

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 53/82

declared on a daily basis. The key feature of open-end schemes is

liquidity.

ii. Close-ended Fund/ Scheme

A close-ended fund or scheme has a stipulated maturity period e.g.

5-7 years. The fund is open for subscription only during a specified

period at the time of launch of the scheme. Investors can invest in

the scheme at the time of the initial public issue and thereafter they

can buy or sell the units of the scheme on the stock exchanges

where the units are listed. In order to provide an exit route to the

investors, some close-ended funds give an option of selling back the

units to the mutual funds NAV related prices. SEBI Regulations

stipulate that at least one of the two exit routes is provided to the

investor i.e. either repurchase facility or through listing on stock

exchanges. These mutual funds schemes disclose NAV generally on

weekly basis.

II. Schemes according to Investment Objective:

A scheme can also be classified as growth scheme, income scheme,

or balanced scheme considering its investment objective. Such

schemes may be open-ended or close-ended schemes as described

earlier. Such schemes may be classified mainly as follows:

i. Growth / Equity Oriented Scheme

The aim of Growth funds is to provide capital appreciation over the

medium to long-term. Such schemes normally invest a major part of

their corpus in equities. Such funds have comparatively high risks.

These schemes provide different options to the investors like

dividend option, capital appreciation, etc. and the investors may

choose an option depending on their preferences. The investors

must indicate the option in the application form. The mutual funds

also allow the investors to change the options at a later date.

53

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 54/82

Growth schemes are good for investors having a long-term outlook

seeking appreciation over a period of time.

ii. Income / Debt Oriented Scheme

The aim of the income funds is to provide regular and steady

investors. Such scheme generally invests in fixed income securities

such as bonds, corporate debentures, Government securities and

money market instruments. Such funds are less risky compared to

equity schemes. These funds are not affected because of

fluctuations in equity markets. The NAVs of such funds are affected

because of change in interest rates in the country.

iii. Balance Fund

The aim of balance funds is to provide both growth and regular

income as such schemes invest both in equities and fixed income

securities in the proportion indicated in their offer documents. These

are appropriate for investors looking for moderate growth. They

generally invest 40-60% in equity and debt instruments. These

funds are also affected because of fluctuations in share prices in the

stock markets. However, NAVs of such funds are likely to be less

volatile compared to pure equity funds.

iv. Gilt Fund

These funds invest exclusively in government securities.

Government securities have no default risk. NAVs of these schemes

also fluctuate due to change in interest rates and other economic

factors as are the case with income or debt oriented schemes.

54

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 55/82

v. Index Funds

Index Funds replicate the portfolio of a particular index such as the

BSE Sensitive index, S&P NSE 50 index (Nifty), etc. These schemes

invest in the securities in the same weight age comprising of an

index. NAVs of such schemes would rise or fall in accordance with

the rise or fall in the index, though not exactly by the same

percentage due to some factors known as “tracking error” in

technical terms.

vi. Money-Market Mutual Funds

These funds invest in highly liquid and safe securities like

commercial paper, banker’s acceptances, and certificates of

deposits. Treasury bills… etc., which are called money market

instruments.

vii. Tax Saving Schemes

This schemes offer tax rebates to the investors under specific

provisions of the Indian Income Tax laws as the Government. Offerstax incentives for investment in specified avenues. Investment

made in Equity Linked Saving Schemes (ELSS) and Pension Schemes

are allowed as deduction u/s 88 of the Income Tax Act 1961.

55

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 56/82

LIMITATIONS OF THE STUDY

1. A descriptive research was undertaken for the purpose of project.

But descriptive research has its own limitations regarding the

selection of sample size of sample unit.

2. Some of the data gathered from the mutual fund holders may not

be reliable.

3. Time limit was also a constraint while conducting the study. So,

the study does not give a picture of the whole market.

4. Time factor, as a period of two month, for gathering data is

inadequate as the gamut of information needs to be synchronized

to give much more comprehensive view of the problems and

prospects.

5. Detailed and depth research was not conducted due to financial

factors.

56

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 57/82

6. The study curtails comparison as it was done only in one city i.e.

Ludhiana.

7. The information provided by the organizations was limited to a far

extent due to drawbacks like competition.

OBJECTIVES OF THE STUDY

1. To track investor’s attitude, performance and behavior with respect to

financial institutions and financial products.

2. To find new and more effective ways of ensuring investor satisfaction

and to find efficient ways of communicating it.

3. To conduct the study with references to Kotak Mahindra products and

the competitive scenario in which Kotak Mahindra operates.

4. To study the structure of investment opportunities.

57

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 58/82

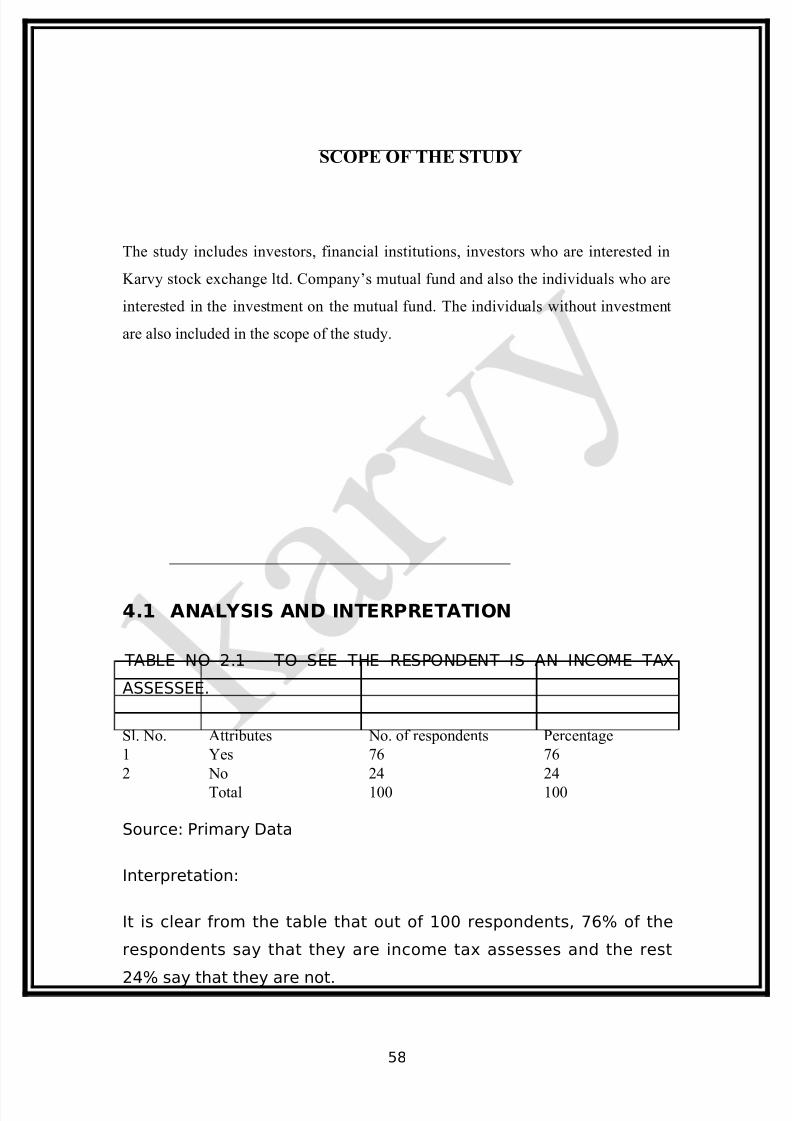

SCOPE OF THE STUDY

The study includes investors, financial institutions, investors who are interested in

Karvy stock exchange ltd. Company’s mutual fund and also the individuals who are

interested in the investment on the mutual fund. The individuals without investment

are also included in the scope of the study.

4.1 ANALYSIS AND INTERPRETATION

TABLE NO 2.1 – TO SEE THE RESPONDENT IS AN INCOME TAX

ASSESSEE.

Sl. No. Attributes No. of respondents Percentage

1 Yes 76 76

2 No 24 24

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 76% of the

respondents say that they are income tax assesses and the rest

24% say that they are not.

58

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 59/82

This is illustrated in the following graph.

GRAPH NO.1 – TO SEE THE RESPONDENT IS AN INCOME TAX

ASSESSEE.

Source: - Table No: 2.1

TABLE NO 2.2. TO SEE WHETHER REPONDENTS INVEST FOR TAX

EXEMPTION OR TAX SAVINGS

Sl. No. Attributes No. of respondents Percentage

1 Yes 70 70

2 No 30 30

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 70% of the

respondents say that they invest for tax exemption and the rest

30% say that they do not.

This is illustrated in the following graph.

59

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 60/82

GRAPH NO 2. TO SEE WHETHER REPONDENTS INVEST FOR TAX

EXEMPTION OR TAX SAVINGS

Source: Table No: 2.2

TABLE NO 2.3. INVESTMENT PREFERENCE OF RESPONDENTS

Sl. No. Attributes No. of respondents Percentage

1 Fixed Deposits 33 33

2 Real Estate 27 27

3 Insurance 21 21

4 Mutual Fund 9 9

5 Gold 9 9

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 33% of the

respondents invest in fixed deposits, 27% invest in Real Estate, 21%

in Insurance, 9% in Mutual Fund and the rest 9% say that they

invest in gold.

60

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 61/82

This is illustrated in the following graph.

GRAPH NO 3. INVESTMENT PREFERENCE OF RESPONDENTS

Source: Table No: 2.3

TABLE NO 2.4 REASONS OF INVESTMENT PREFERENCE OF

RESPONDENTS

Sl. No. Attributes No. of respondents Percentage

1 Less Risk 28 28

2 Good Returns 21 21

3 Liquidity 12 12

4 Assured Returns 36 36

5 Other Reasons 3 3

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 28% of the

respondents prefer investment due to less risk, 21% due to good

returns, 12% due to liquidity, 36% due to assured returns and the

rest 3% do it due to other reasons.

61

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 62/82

This is illustrated in the following graph.

GRAPH NO 4. REASONS OF INVESTMENT PREFERENCE OF

RESPONDENTS

Source: Table No: 2.4

TABLE NO 2.5. CURRENT INVESTMENT PORTFOLIO OF

RESPONDENTS

Sl. No. Attributes No. of respondents Percentage

1 Govt securities and bonds 61 61

2 Mutual funds & company FD’s 18 18

3 Equity Shares 21 21

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 61% of the

respondents invest in Govt securities and bonds, 18% in Mutual

funds and company fixed deposits and the rest 21% in equity

shares.

62

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 63/82

This is illustrated in the following graph:

GRAPH NO 5. CURRENT INVESTMENT PORTFOLIO OF RESPONDENTS

Source: Table No: 2.5

TABLE NO 2.6. NATURE OF INVESTMENT THAT THE RESPONDENTS

LIKE

Sl. No. Attributes No. of respondents Percentage

1 Steadily 61 61

2 At average rate 27 27

3 Fast 12 12

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 61% of the

respondents like their investment to grow steadily, 27% in an

average rate and the rest 12% in a fast rate.

This is illustrated in the following graph.

63

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 64/82

GRAPH NO 6. NATURE OF INVESTMENT THAT THE RESPONDENTS

LIKE

Source: Table No: 2.6

TABLE NO 2.7 PERCENTAGE OF INCOME THAT THE RESPONDENTS

INVEST

Sl. No. Attributes No. of respondents Percentage

1 5 % 24 24

2 5% - 10% 37 37

3 More than 10% 39 39

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 24% of the

respondents invest 5% of their total income, 37% invests 5-10% and

the rest 39% invest more than 10%.

This is illustrated in the following graph.

64

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 65/82

GRAPH NO 7. PERCENTAGE OF INCOME THAT THE RESPONDENTS

INVEST

Source: Table No: 2.7

TABLE NO 2.8 TO SEE WHETHER THE RESPONDENT IS AN INVESTOR

OF MUTUAL FUND

Sl. No. Attributes No. of respondents Percentage

1 Yes 27 27

2 No 73 73

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, only 27% of

the respondents are investors of mutual funds and the rest 73% are

not.

This is illustrated in the following graph.

65

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 66/82

GRAPH NO 8. TO SEE WHETHER THE RESPONDENT IS AN INVESTOR

OF MUTUAL FUND

Source: Table: 2.8.

TABLE NO 2.9 REASONS FOR NOT INVESTING IN MUTUAL FUNDS

Sl. No. Attributes No. of respondents Percentage

1 Awareness 15 15

2 Risky 58 58

3 Returns not assured 27 27

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 15% of the

respondents do not invest in mutual funds because of lack of

awareness, 58% as it is risky and the rest 27% as the returns are

not assured.

This is illustrated in the following graph.

66

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 67/82

GRAPH NO 9. REASONS FOR NOT INVESTING IN MUTUAL FUNDS

Source: Table No: 2.9

TABLE NO 2.10 REASONS FOR INVESTING IN MUTUAL FUNDS

Sl. No. Attributes No. of respondents Percentage

1 Less Risky 21 21

2 Liquidity 30 30

3 Professional Mgmt 24 24

4 Fast Appreciation 25 25

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 21% of the

respondents feel that investing in mutual funds are less risky and

hence they invest, 30% invest due to liquidity, 24% due to

Professional management and the rest 25% due to fast

appreciation.

This is illustrated in the following graph.

67

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 68/82

GRAPH NO 10. REASONS FOR INVESTING IN MUTUAL FUNDS

Source: Table No: 2.10

TABLE NO 2.11 KIND OF MUTUAL FUND THAT THE RESPONDENTS

PREFER

Sl. No. Attributes No. of respondents Percentage

1 Open-ended 57 57

2 Closed-ended 43 43

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 57% of the

respondents prefer open-ended mutual funds and the rest 43%

closed-ended ones.

This is illustrated in the following graph.

GRAPH NO 11. KIND OF MUTUAL FUND THAT THE RESPONDENTS

PREFER

68

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 69/82

Source: Table No: 2.11

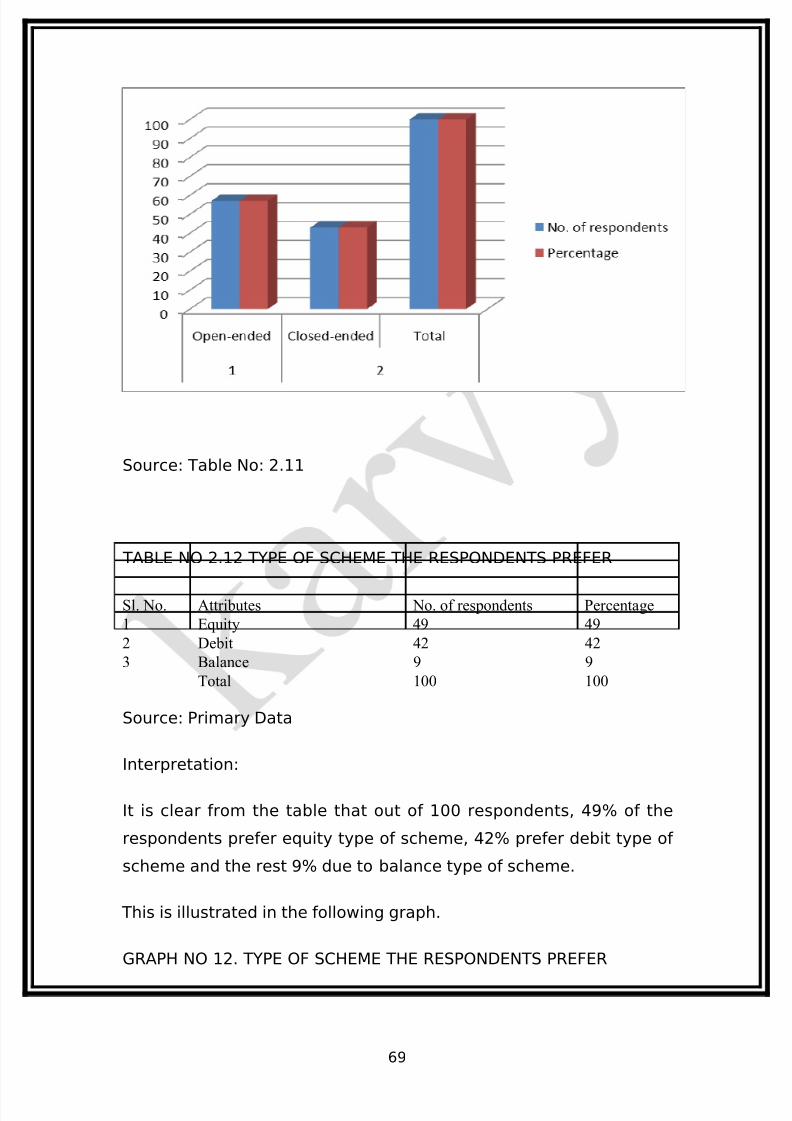

TABLE NO 2.12 TYPE OF SCHEME THE RESPONDENTS PREFER

Sl. No. Attributes No. of respondents Percentage

1 Equity 49 49

2 Debit 42 42

3 Balance 9 9

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 49% of the

respondents prefer equity type of scheme, 42% prefer debit type of

scheme and the rest 9% due to balance type of scheme.

This is illustrated in the following graph.

GRAPH NO 12. TYPE OF SCHEME THE RESPONDENTS PREFER

69

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 70/82

Source: Table No: 2.12

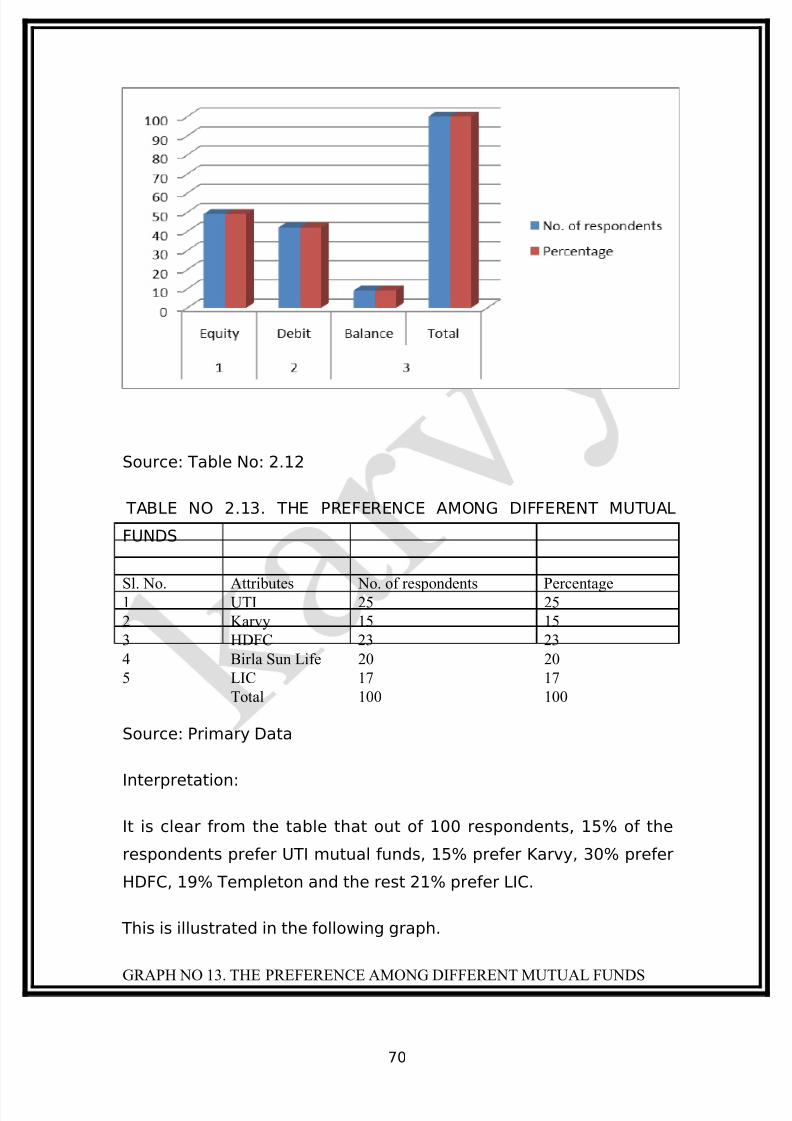

TABLE NO 2.13. THE PREFERENCE AMONG DIFFERENT MUTUAL

FUNDS

Sl. No. Attributes No. of respondents Percentage1 UTI 25 25

2 Karvy 15 15

3 HDFC 23 23

4 Birla Sun Life 20 20

5 LIC 17 17

Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 15% of the

respondents prefer UTI mutual funds, 15% prefer Karvy, 30% prefer

HDFC, 19% Templeton and the rest 21% prefer LIC.

This is illustrated in the following graph.

GRAPH NO 13. THE PREFERENCE AMONG DIFFERENT MUTUAL FUNDS

70

8/3/2019 Final 2nd Sam Project Report

http://slidepdf.com/reader/full/final-2nd-sam-project-report 71/82

Source: Table No: 2.13

TABLE NO 2.14 TO ANALYSE WHETHER THE RESPONDENT SEES THE

BRAND NAME WHILE INVESTING

Sl. No. Attributes No. of respondents Percentage

1 Yes 94 94

2 No 06 06Total 100 100

Source: Primary Data

Interpretation:

It is clear from the table that out of 100 respondents, 94% of the