Languages

Pages

Legal

1

Eduardo Levy Yeyati

The World Bank & Universidad Torcuato Di Tella

December, 2006

Fear of Floating or Fear of Flying:

Exchange Rate Policy in the New Millenium

Storyboard

The basics: The debate post-Bretton Woods

The tradeoff: Exchange rate regimes and the real economy

The evidence: Regimes in the 2000s

The FIT (float + inflation targeting) paradigm: natural evolution or fad?

Fear of flying: building a case for a proactive exchange rate policy

The basics

The real view (‘70s) Trade (and welfare) gains vis à vis users of the peg

currency vs. loss of the exchange rate as a shock absorber in the presence of nominal rigidities.

Pro peg Openness, propensity to trade, trade concentration

Pro float Incidence of real shocks

The basics

The political view (‘80s) Bands, “tablitas” & other soft species: Exchange rate

anchors as a “policy crutch” to compensate for the lack of monetary credibility or political power

Pro peg high inflation, weak governments

The basics

The financial view (‘90s) The trilemma: as the world integrates, countries have

to choose between monetary autonomy & a stable ER

The bipolar view: Exchange rate policy in emerging economies become more vulnerable to the limits imposed by the trilemma: hard peg or float

The unipolar view: Balance sheet effects due to currency mismatches limit the scope for expansionary devaluations Hard pegs

The tradeoff

Oversimplifying: Fix vs. flex Enhanced monetary & fiscal discipline

(lower inflation) at the cost of greater sensitivity to real

shocks & output volatility…

…except under FD (contractionary devaluations)

Is this theoretical tradeoff validated by the evidence?

Yes

The tradeoff

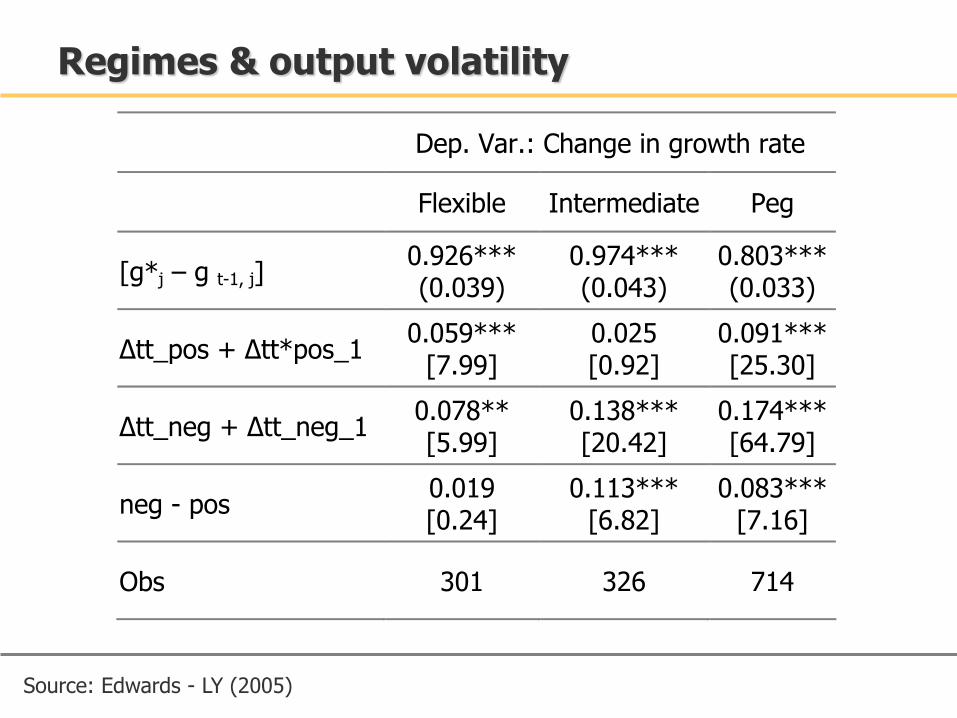

Preliminary evaluation:

Pegs contribute to lower inflation expectations…

…at the cost of greater output volatility…

Dep. Var.: Change in growth rate

Flexible Intermediate Peg

[g*j – g t-1, j] 0.926*** (0.039)

0.974*** (0.043)

0.803*** (0.033)

Δtt_pos + Δtt*pos_1 0.059***

[7.99] 0.025 [0.92]

0.091*** [25.30]

Δtt_neg + Δtt_neg_1 0.078** [5.99]

0.138*** [20.42]

0.174*** [64.79]

neg - pos 0.019 [0.24]

0.113*** [6.82]

0.083*** [7.16]

Obs 301 326 714

Regimes & output volatility

Source: Edwards - LY (2005)

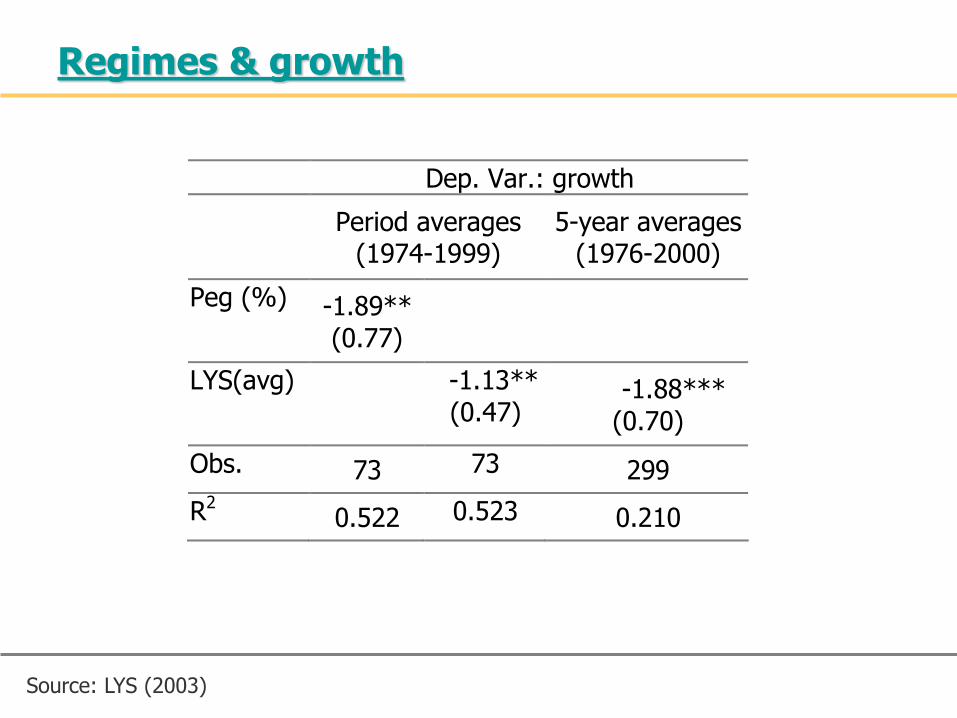

The tradeoff

Preliminary evaluation:

Pegs contribute to lower inflation expectations…

…at the cost of greater output volatility…

…and slower growth

Dep. Var.: growth

Period averages

(1974-1999) 5-year averages

(1976-2000)

Peg (%) -1.89**

(0.77)

LYS(avg)

-1.13**

(0.47) -1.88***

(0.70)

Obs. 73 73 299

R2 0.522 0.523 0.210

Regimes & growth

Source: LYS (2003)

The tradeoff

Preliminary evaluation:

Pegs contribute to lower inflation expectations…

…at the cost of greater output volatility…

…and lower growth

Balance sheet effects

Subdued inflation fears Volatility concerns dominate Float

Under FD Threshold floats

The bipolar view after Argentina

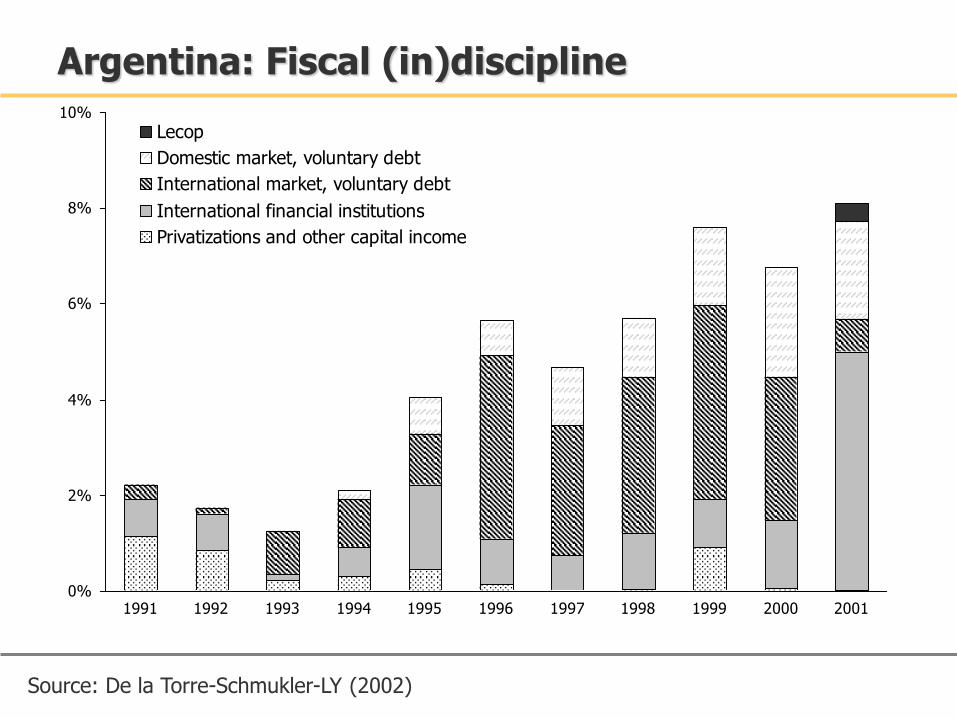

Argentina: Fiscal (in)discipline

0%

2%

4%

6%

8%

10%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Lecop

Domestic market, voluntary debt

International market, voluntary debt

International financial institutions

Privatizations and other capital income

Source: De la Torre-Schmukler-LY (2002)

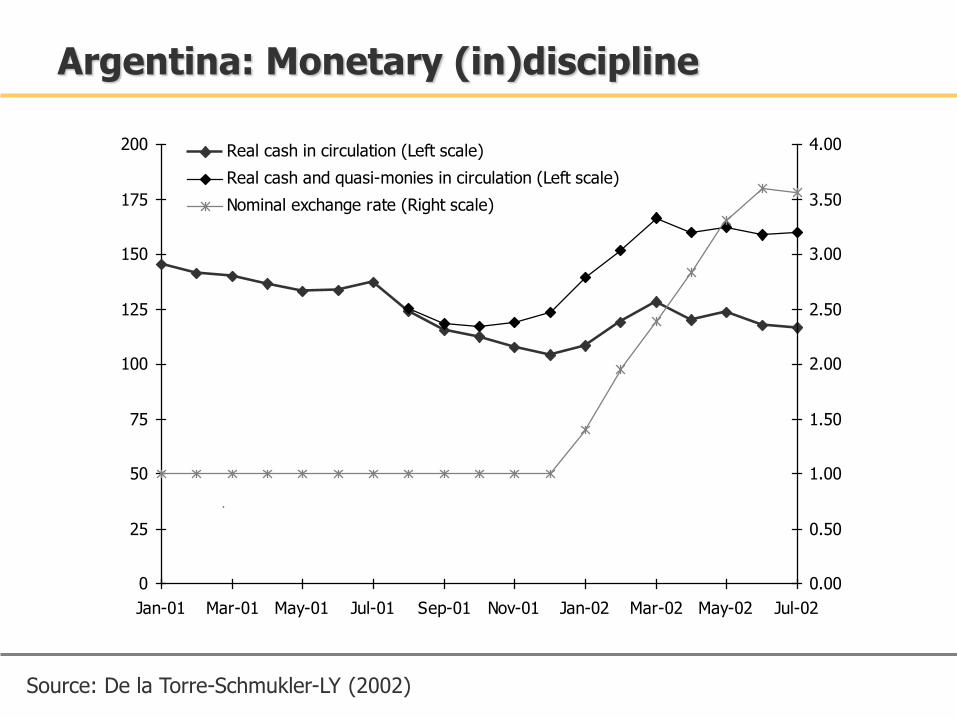

Argentina: Monetary (in)discipline

0

25

50

75

100

125

150

175

200

Jan-01 Mar-01 May-01 Jul-01 Sep-01 Nov-01 Jan-02 Mar-02 May-02 Jul-02

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00Real cash in circulation (Left scale)

Real cash and quasi-monies in circulation (Left scale)

Nominal exchange rate (Right scale)

Source: De la Torre-Schmukler-LY (2002)

The bipolar view after Argentina

Lack of external discipline by private markets

Hard pegs do not lead to fiscal discipline

Fiscal dominance Hard pegs do not lead to

monetary discipline

Is de jure dollarization hard enough?

Where do we stand?

Pegs are passé In most cases, inefficient short-term substitute for credibility

Hard pegs failed the test in Argentina

Learning to live with BS effects The (dynamic)

scope for countercyclical exchange rate policy

The double D: Domestication and de-dollarization of

sovereign debt

A unipolar view in reverse?

• Key criterion: ER variability relative to forex intervention

• The intervention dimension is key to characterized exchange rate policy (as opposed to the evolution of exchange rates) and its consequences

Exchange rate regimes in the 2000s: Classification

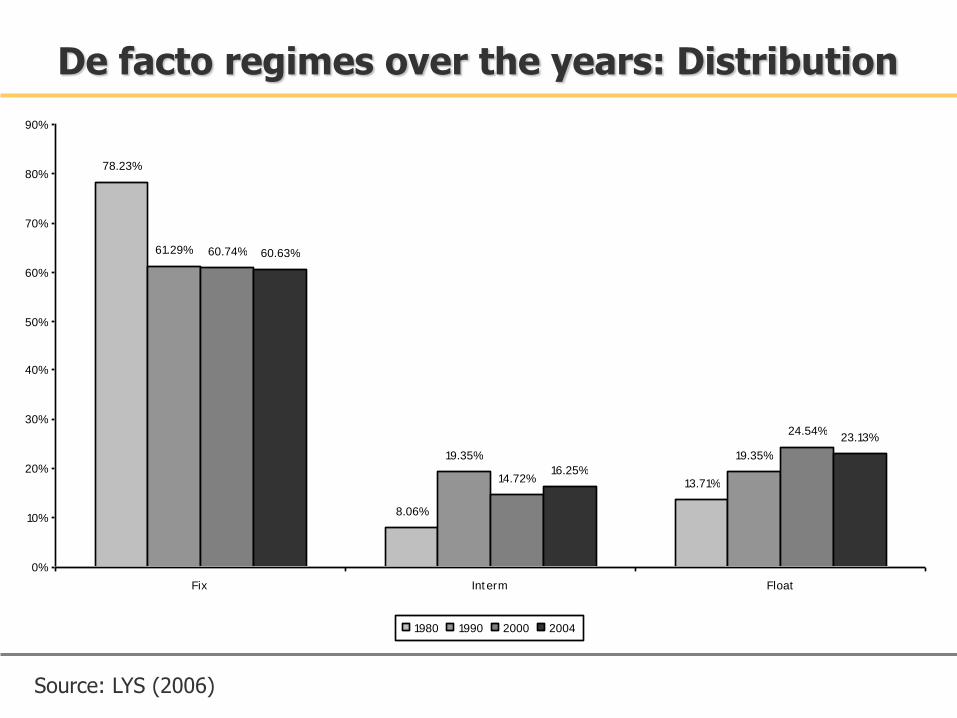

78.23%

8.06%

13.71%

61.29%

19.35% 19.35%

60.74%

14.72%

24.54%

60.63%

16.25%

23.13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Fix Int erm Float

1980 1990 2000 2004

De facto regimes over the years: Distribution

Source: LYS (2006)

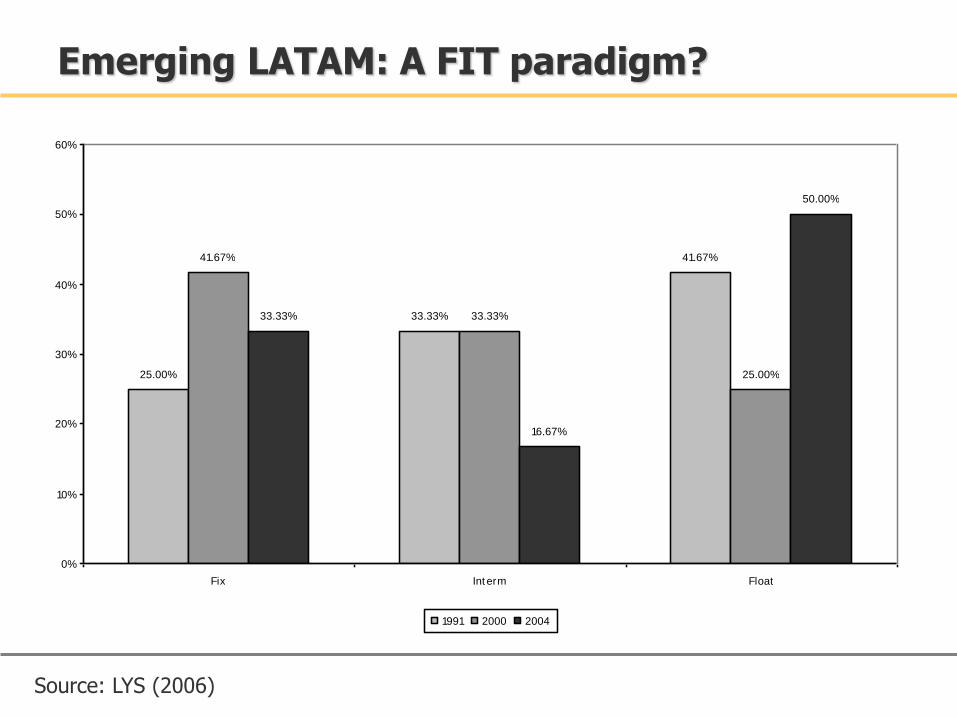

25.00%

33.33%

41.67%41.67%

33.33%

25.00%

33.33%

16.67%

50.00%

0%

10%

20%

30%

40%

50%

60%

Fix Int erm Float

1991 2000 2004

Emerging LATAM: A FIT paradigm?

Source: LYS (2006)

The FIT paradigm

Natural evolution or this year’s model?

Less than a paradigm, more than a fad

Negative experience with alternative options

Inflation awareness CB autonomy, fiscal restraint

Decline in inflation –and dollar indexation– tilts the balance towards more flexibility

Inflation targets substitute for ER anchors

Still far from the benign neglect

The comeback of exchange rate policy?

Mercantilist interventions as a substitute for protection

Less specific than subsidies

Less prone to mismanagement & corruption

Fear of floating or fear of flying?

Invertion of the ER anchor problem: sustaining an undervalued currency

Instead of amplified recessions due to price rigidities…

…inflationary expansions fueled by positive real shocks.

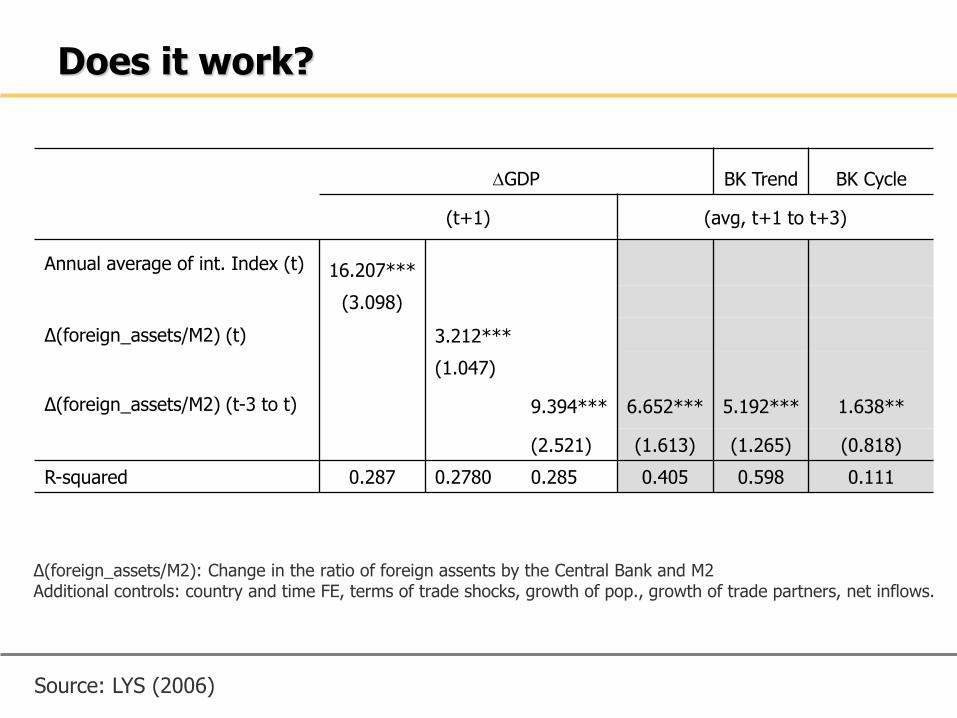

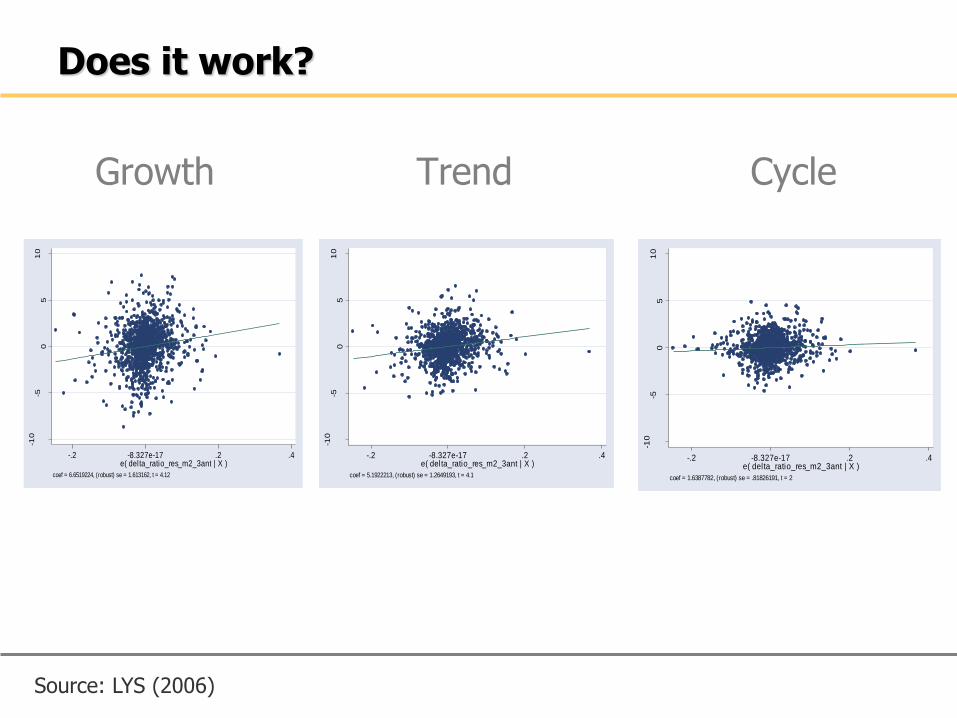

Does it work? How?

• Fear of floating’s underlying fears:

– Contractionary devaluations (due to BS effects) and currency and debt crisis propensity

– Dollar pricing, pass-through and inflation

• Fear of flying: Leaning against the appreciation wind

– Intervention to strenthen the demand for the foreign currency, to avoid/mitigate appreciation pressures

Fear of flying: A characterization

Fear of flying over time (intermediates)

Source: LYS (2006)

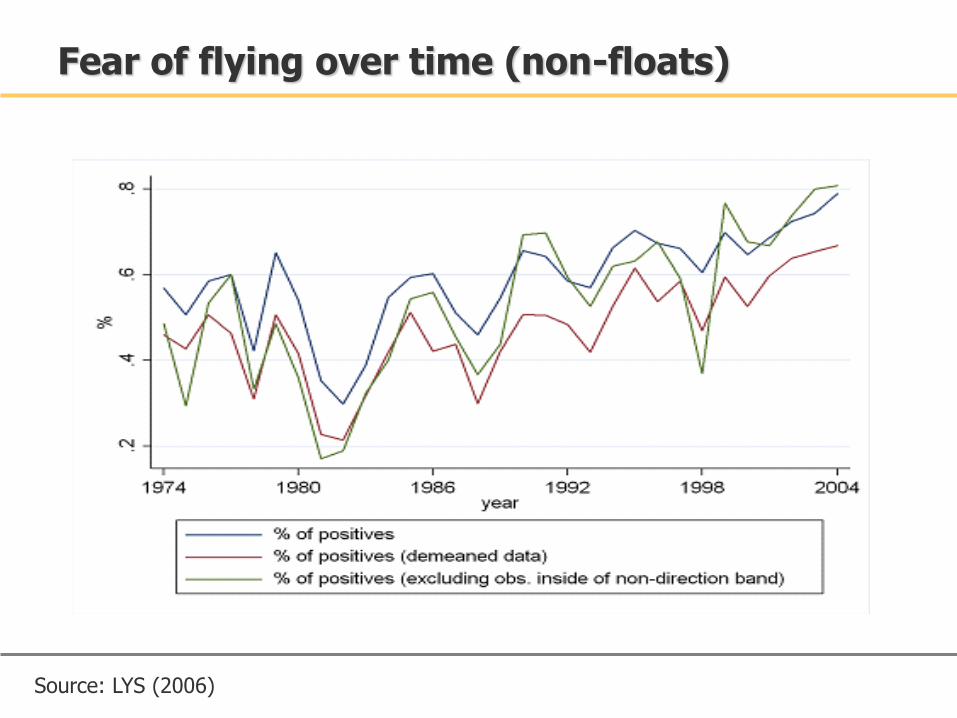

Fear of flying over time (non-floats)

Source: LYS (2006)

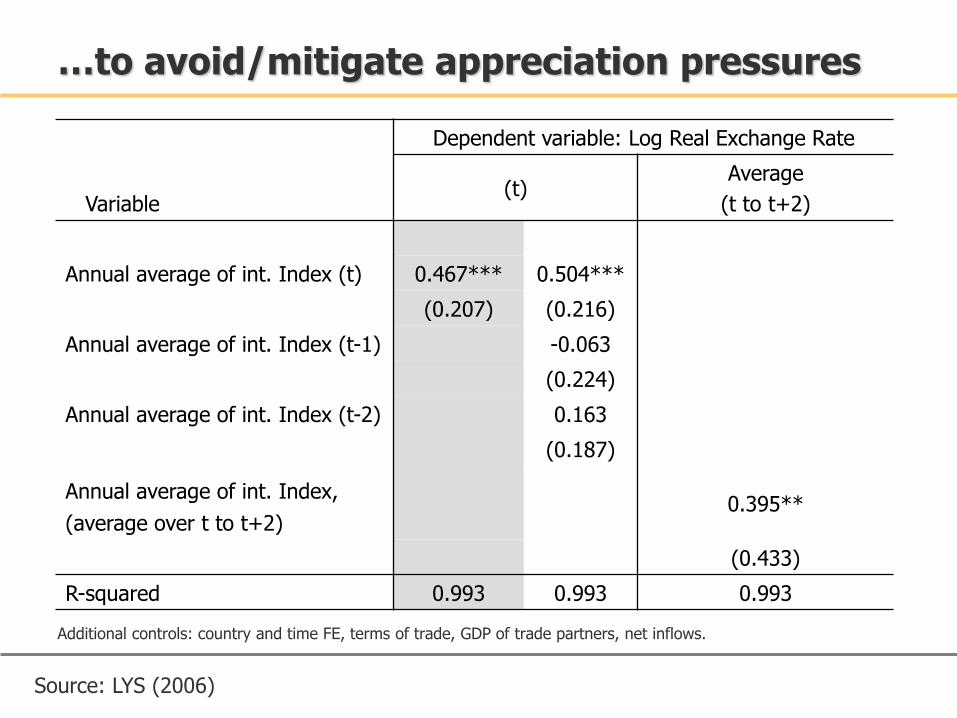

…to avoid/mitigate appreciation pressures

Additional controls: country and time FE, terms of trade, GDP of trade partners, net inflows.

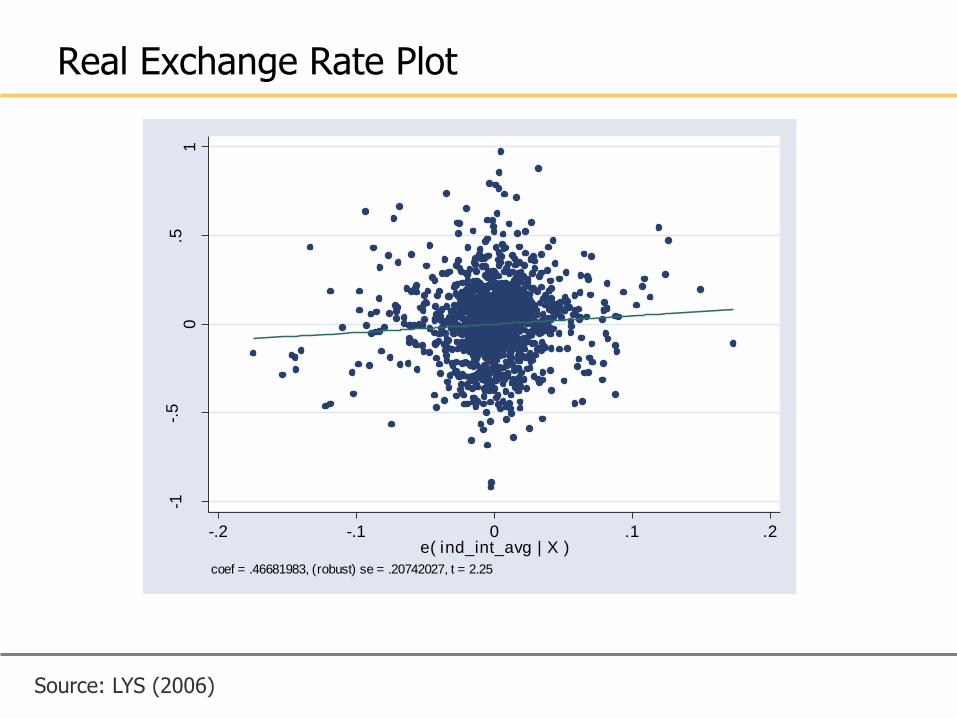

Variable

Dependent variable: Log Real Exchange Rate

(t) Average

(t to t+2)

Annual average of int. Index (t) 0.467*** 0.504***

(0.207) (0.216)

Annual average of int. Index (t-1) -0.063

(0.224)

Annual average of int. Index (t-2) 0.163

(0.187)

Annual average of int. Index,

(average over t to t+2) 0.395**

(0.433)

R-squared 0.993 0.993 0.993

Source: LYS (2006)

Real Exchange Rate Plot

Source: LYS (2006)

GNB

BOL

URYMDGBRA

UGA

URY

ARG

MOZ

ECU

SVN

GAB

MDG

MEX

LSO

MDG

NGA

TUR

SLE

TTO

KWT

TZA

THA

MWILKA

UGA

BRA

ZMB

MNG

URY

SEN

ZMB

NGA

NGA

IDNSVNMDGMKDDMA

CRI

SLV

HND

BGRMYS

ZWE

CMR

MUSGABPHLBHR

BRA

ARG

BRA

VEN

PRYMDGGAB

ZMB

NGA

RWA

BDI

SEN

SAUZAF

ZAF

SLEMUS

BGRZWEMEX

IDN

ECU

GAB

URY

BOL

BFA

BEN

NGA

KEN

GAB

ARM

HNDZAF

BOLTTO

SVK

SDN

VEN

HND

MWILKA

CZEHTI

MDG

KNA

HND

BRB

MKD

MYSBENDMATGO

VEN

MYS

MEX

IDN

SWZ

BRA

ZAF

HNDCOL

PER

MWI

MUS

CRI

MWI

DOM

BRA

TGO

MLI

NER

MYS

POL

SLV

MOZ

RWA

COGCZE

MWI

ZAFVEN

VCT

MOZGAB

VENPRY

HND

BGR

MYS

CRISWZTUR

MYS

DOMMLI

SYR

BDITTO

TGO

SWZ

VEN

MRTCMR

TGOPRY

VEN

URY

LKA

HND

SWZ

MKD

SLV

TGOKNA

TCD

TTO

VEN

TUN

PAKCOG

ECU

HTI

GTM

ARG

MDG

TUNIDN

NER

ARG

IDNPHL

MYS

GAB

SVKTGO

ECU

ZAF

SYR

CMR

SLV

MEX

ARM

PER

IDN

KNA

HND

PHL

KENZAF

HND

SAU

DOM

ARG

SVN

ARG

MYSGABSWZCOL

PER

RWA

TCD

COL

GNB

DMASEN

MNGSWZ

KEN

ECU

CHL

UGA

NER

PER

SEN

PAKPRY

SLV

GNB

DOM

ECUTCD

NER

PER

GTM

BRB

TUR

CHL

ARG

BRA

DMA

SEN

CZEPHL

GTM

DOM

MYSBHRMUS

LTUSEN

SVN

COLTCD

SWZ

GRD

GTM

COG

NER

BFA

HUN

PRY

IDN

ETH

PAK

RWACOL

MEX

PAKSLV

BRA

GTMPRY

SWZ

CHL

SLVKNA

HND

CRIARM

CMR

EGY

GTM

VCT

TZADOM

VCTTUNLTU

VEN

VCTDMACOG

HRVMYSPOL

PAKVCT

SEN

VEN

BFA

CZEPOL

TCD

PERPER

MUS

COG

SYR

VCT

ARG

GRD

SLE

TTOTTO

IND

VCT

GRD

BOL

HND

DMA

SDN

THA

BEN

MLI

TUNKNADMAARM

PER

UGA

GRDVENSLECZESYC

SVK

BFA

IND

VCT

SWZ

HRV

BRA

KEN

DMA

MAR

BRASDN

RWAKNA

POL

IDN

EGY

MWIPOL

CHLTHAKEN

BFA

SVK

IND

MYS

PER

SEN

EGY

IND

NER

URY

MEX

MLI

LKA

MOZ

VCT

HRV

CHLBFA

THA

RWA

BDI

TUR

NAMSYC

SEN

GABTUR

LKA

BOLMWI

PERSYR

SYCGRDCHLCRI

TURLVA

TCDLKATHA

IND

DOM

TGOLKA

GNB

KNASLVFJIGTM

MLI

TTO

ETH

SDN

SYR

BOL

SLV

NER

THA

ETH

PAK

SYCTGO

SEN

HTIPAKDOM

GRD

SVN

GTM

LVAKNAGRD

PAK

CHLKNA

CHLTUR

COL

COG

NERBRA

NGA

TTOSLVVENECUZAF

HTI

ZAF

MUS

ETH

GTM

CRI

ETH

HUN

SYR

TONDMA

VEN

SYC

INDPRY

PHL

MYS

CPV

GTM

ZAF

CHL

MEX

ARG

PAK

EGY

UGA

EGY

GNBGTMPAK

BRB

CHL

ETH

PHL

NGA

TZA

TGO

BRB

DMA

PHL

HND

SLV

MAR

PER

MWI

NAMNGA

GRDMUSBOL

IND

PRY

COG

SLV

HUNPOL

RWASWZ

CHL

BEN

BRA

CHL

HRV

MAR

IDN

ETH

LTU

KNAUGA

ECU

BFA

CRI

BFA

MAR

VCT

LKA

TCD

BEN

ETH

PAK

CZEEGY

MUSSAUSLEPRY

SYR

IDN

PRY

CRI

UGA

TZA

THA

COGBFA

RWAGRDPAK

ARG

POL

MLI

CMREGY

ETH

ETH

RWA

ETH

IND

NERINDNER

CHLTUN

KEN

GRD

MLI

MEX

CHL

COL

TUN

CHL

GRDLKAMWICOL

ETH

SLV

PAK

TUN

ECU

GAB

SYCKNA

MARRWABRB

TGO

URY

SLV

BFASYR

SYR

TTO

SYR

TZA

POLGRD

PER

EGYMUS

HTI

CRI

CPV

ARG

TUN

SEN

EGYDOM

SDN

EGY

HTI

TGO

NGA

COL

IND

NGA

FJI

TTOBGRTUNMEX

GAB

MEX

TURGNB

KWT

SWZSYCCHL

HUN

NGA

PHL

CMR

GAB

NER

TTODOM

KENLTU

PAK

GNB

VCT

COGVCTDMAKEN

KNA

CRI

BGR

UGA

KEN

BENHTI

ARG

PHL

KNATTO

DOMLTUCHLBRA

THA

BEN

IND

ZAF

MEX

DMA

MARCOGTUN

ECU

LTU

NGA

TUNBGDLVAHRVEGY

COL

COG

CMR

HTI

BOL

MWI

EGY

THA

DOM

BRBGRD

GTM

BRBCRI

ARG

MLI

SYR

ETH

KENNERSYC

PAK

IND

BGRDMA

CZEPOLHRV

NERBDI

NGA

COL

MARHTI

DOMCRIGRDDMA

PER

FJI

BFA

SVK

ARG

RWA

THARWA

SENTGO

THA

IDN

VEN

LVAMNG

GTM

DOM

SYR

GAB

DOM

INDPOL

COL

LVAECUDMA

NGA

SYRBRACPV

SWZ

LVAMNG

URY

TUNCOLSDN

MOZ

PRY

URY

IDN

ETHSLVGTM

HTI

ETH

GAB

TUR

PER

BRB

SLV

IND

PRYHUNMOZ

MLI

TUR

MLI

FJI

PRYTHA

TGO

SYR

TTOCMR

SENEGY

URY

KNA

PRYMKD

ARG

GTM

INDETH

GRD

MUS

BDIBENCRITUN

DMA

GAB

DMAPOL

GRDTTO

CMR

ECU

HTI

VCTUGA

VEN

MYS

SLV

MNG

PER

HTIBDIPAKTZAGTM

COGLKA

BOLZMB

THAMAR

BOLBRB

GAB

MLI

LKA

SWZ

SVKSEN

MDGGTM

PHLLVA

HTI

VCT

IND

HND

KEN

ARG

SLV

ETH

MAR

ETH

FJIGRD

SYC

MLI

COL

ETH

NERLKA

GRD

MLI

THABRALVA

ARG

MYS

ETHCOG

BRB

SYR

CPVSAUZWEGRDRWARWA

KWT

TCDMLIBENVCTIDN

KNA

ARM

IDN

HTI

ECUTURKEN

TON

IND

SWZ

PHL

BGR

DOM

BOL

HRV

TGO

THATGO

GTMPER

PHL

ETH

CMR

LKA

TCDTTODOMMAR

SWZ

IND

PRY

SENBOL

TGO

EGY

BEN

MOZ

URY

KNA

MEX

MUSPHLBGR

CHLSDN

IND

GRD

ARG

VCT

IDNVEN

GTM

GNB

CHL

SYR

TGO

CRICZE

ZAFLTU

LKA

PHL

SYR

CHL

COLGNB

COLTUR

HTI

PRY

LKA

BRA

EGY

BRB

BOLSYCTHACRIKEN

CMR

BDIMWIMAR

HND

ECU

MDG

NERIND

PER

RWABDI

SYRMEXECUPAK

BFA

PER

RWA

LTU

ETH

DOMKNALKA

DOM

ZAF

ARG

VEN

SLV

BOL

VEN

IDN

MNGMWI

ZAFURY

HTIHNDBGR

GNB

THACHL

IND

VEN

TUNARM

CMRTUN

BFA

NGA

MKD

URY

LKABHR

SENMDG

NER

BOL

RWA

GABMLI

MYS

SENSENNERGRD

TZAARMTGO

SLV

URY

ZAF

NGA

KNA

MDG

THA

HTI

PRY

BEN

ARMGTM

IND

URY

KNATCDBDI

CMR

TCD

SYR

MDG

THAMNG

DMA

VCT

MDG

CHL

EGY

SWZURY

COL

LTU

DOM

HRV

LKA

ARG

CHL

VCT

MEX

UGA

GAB

TGO

MNG

CRI

PAK

SLV

HTI

ARMPERPHL

PRYSWZ

KEN

TGO

PAK

BOL

COL

NAM

URY

RWA

BHRDMA

PRY

PER

SENHRV

SEN

ZAF

MDG

SYR

MUS

TTOBHR

TGOTGOTGOHND

RWA

VEN

HND

SVNPER

TZA

PHL

SEN

MYS

PHL

CRIBRBCRI

HND

BOLGTMGAB

SEN

VCT

MEX

RWAPHL

MWI

CMR

RWA

BRAIDN

ZAF

BOLDOM

BFA

IDN

NGA

SYR

PHL

IDNARM

NER

ZAFBRB

NGA

TURCMRMEX

MYS

ECUECU

BRA

NGA

BEN

RWA

BHRCOL

MKDMUSBFAMYSTHAMEXVENSLV

BOL

BOL

PAK

SWZSWZ

SEN

MEX

TUR

MLI

GRDPOL

CMR

SVK

DMA

MRT

NGA

MYS

ETHCRI

LKA

GRD

ZAF

TUR

PRY

MLI

BFABFACRITUN

TCD

UGA

TZAPAK

LKA

BRA

ZAF

TTOBRA

IDNEGY

HUN

MYS

SWZTUNDOM

MEX

COL

SAU

BRA

PER

URYVCT

PRY

HND

SWZ

KEN

GTM

NGA

ECU

COG

MYS

NER

SVNSWZ

LSO

MEX

NGA

TCD

MWI

VEN

VCTCRITHA

MOZ

MYSMKDTUR

SAU

KEN

URY

MUS

DOM

BDISYC

MDGPRY

SVN

MNGDMA

PAK

IDN

GTMHND

MWI

ZWE

TURKNASLEUGA

NGA

DMANERURY

MEX

BENMOZMOZMOZBOL

ZAF

TTO

CZE

TZA

MDGGNBMDGMYS

BOL

LKAMWIMYS

HND

SVNMDGMKD

TGO

MDG

GABSVKZAFDMA

PER

HNDECUSLE

GABLSO

TTOKNA

ZWE

TTO

URY

CZE

GAB

ARG

BRA

POL

SDNGAB

ARGCHL

URY

SLV

SLE

UGA

URY

COG

ZMB

GABSVNSEN

MWI

HND

IDN

KWT

ECU

SLV

VENBRA

MDG

MDGMUS

UGAVEN

BGR

NGA

ARG

ZMB

GNB

BRA

-1-.

50

.51

e(

ltcr

| X

)

-.2 -.1 0 .1 .2e( ind_int_avg | X )

coef = .46681983, (robust) se = .20742027, t = 2.25

Does it work?

∆(foreign_assets/M2): Change in the ratio of foreign assents by the Central Bank and M2 Additional controls: country and time FE, terms of trade shocks, growth of pop., growth of trade partners, net inflows.

DGDP BK Trend BK Cycle

(t+1) (avg, t+1 to t+3)

Annual average of int. Index (t) 16.207***

(3.098)

∆(foreign_assets/M2) (t) 3.212***

(1.047)

∆(foreign_assets/M2) (t-3 to t) 9.394*** 6.652*** 5.192*** 1.638**

(2.521) (1.613) (1.265) (0.818)

R-squared 0.287 0.2780 0.285 0.405 0.598 0.111

Source: LYS (2006)

Growth Trend Cycle

Source: LYS (2006)

Does it work? -1

0-5

05

10

e(

pro

m_

de

lta

_g

dp

| X

)

-.2 -8.327e-17 .2 .4e( delta_ratio_res_m2_3ant | X )

coef = 6.6519224, (robust) se = 1.613162, t = 4.12

-10

-50

51

0

e(

pro

m_

d_

bktr

en

d_

lgd

p_

un

| X

)

-.2 -8.327e-17 .2 .4e( delta_ratio_res_m2_3ant | X )

coef = 5.1922213, (robust) se = 1.2649193, t = 4.1

-10

-50

51

0

e(

pro

m_

d_

bkcic

le_

lgd

p_

un

| X

)

-.2 -8.327e-17 .2 .4e( delta_ratio_res_m2_3ant | X )

coef = 1.6387782, (robust) se = .81826191, t = 2

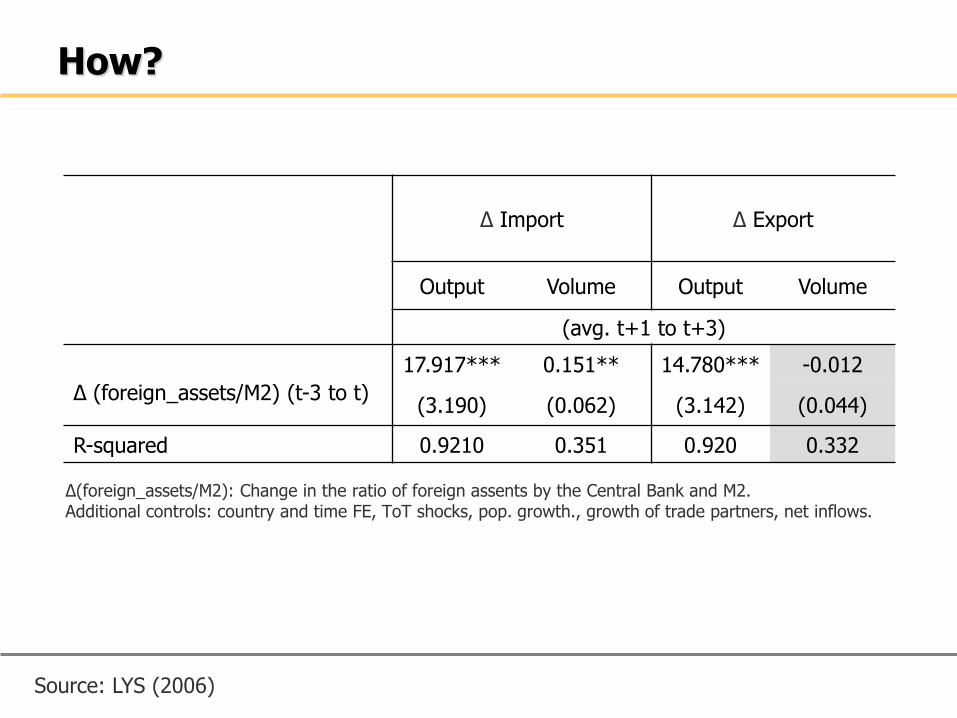

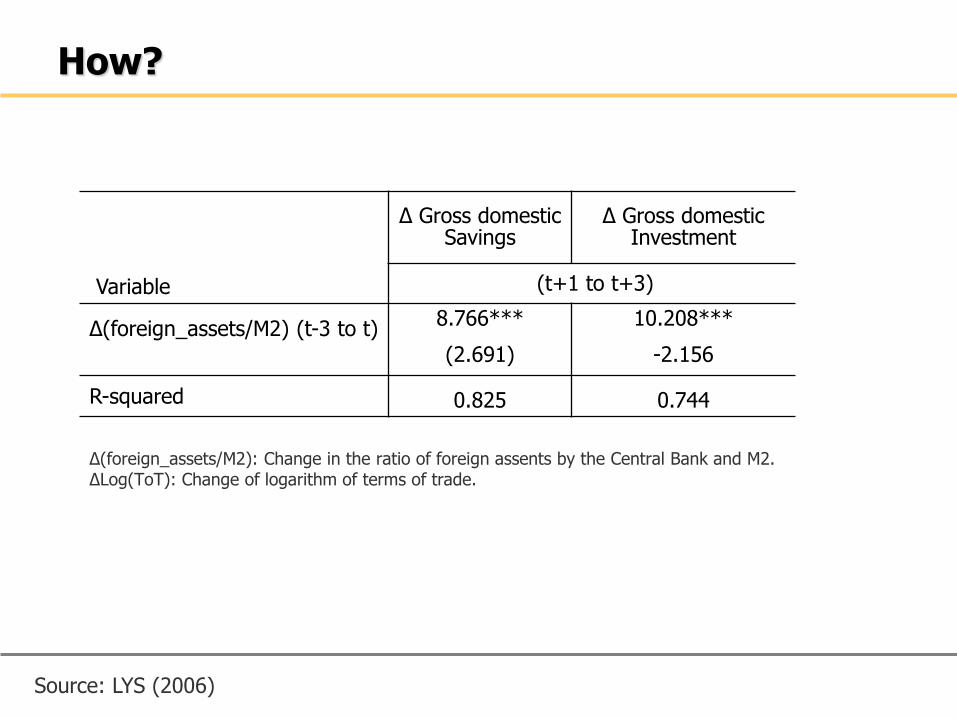

How?

∆(foreign_assets/M2): Change in the ratio of foreign assents by the Central Bank and M2. Additional controls: country and time FE, ToT shocks, pop. growth., growth of trade partners, net inflows.

∆ Import ∆ Export

Output Volume Output Volume

(avg. t+1 to t+3)

∆ (foreign_assets/M2) (t-3 to t)

17.917*** 0.151** 14.780*** -0.012

(3.190) (0.062) (3.142) (0.044)

R-squared 0.9210 0.351 0.920 0.332

Source: LYS (2006)

How?

∆(foreign_assets/M2): Change in the ratio of foreign assents by the Central Bank and M2. ∆Log(ToT): Change of logarithm of terms of trade.

∆ Gross domestic Savings

∆ Gross domestic Investment

Variable (t+1 to t+3)

∆(foreign_assets/M2) (t-3 to t)

8.766*** 10.208***

(2.691) -2.156

R-squared 0.825 0.744

Source: LYS (2006)

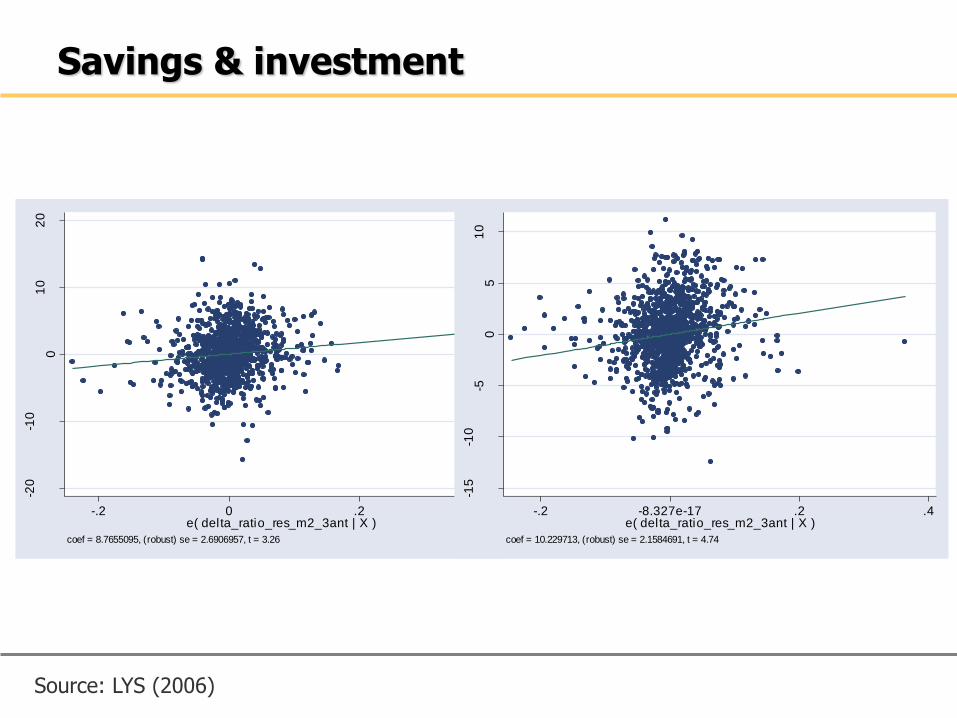

Savings & investment

Source: LYS (2006)

-20

-10

01

02

0

e(

pro

m3

_p

_g

ds |

X )

-.2 0 .2 .4e( delta_ratio_res_m2_3ant | X )

coef = 8.7655095, (robust) se = 2.6906957, t = 3.26

-15

-10

-50

51

0

e(

pro

m3

_p

_g

kf

| X

)

-.2 -8.327e-17 .2 .4e( delta_ratio_res_m2_3ant | X )

coef = 10.229713, (robust) se = 2.1584691, t = 4.74

Taking stock

Dedollarization and debt reduction reduce the incidence of capital reversals

Soft FIT paradigm replaces the ER as nominal anchor

Fear of flying is an increasingly popular contender to drive domestic saving & investment (but not so much exports)

The exchange rate debate appears to have gone full circle to the issues of the 1970s

Thank you

33

Eduardo Levy Yeyati

The World Bank & Universidad Di Tella

December, 2006

Fear of Floating or Fear of Flying:

Exchange Rate Policy in the New Millenium

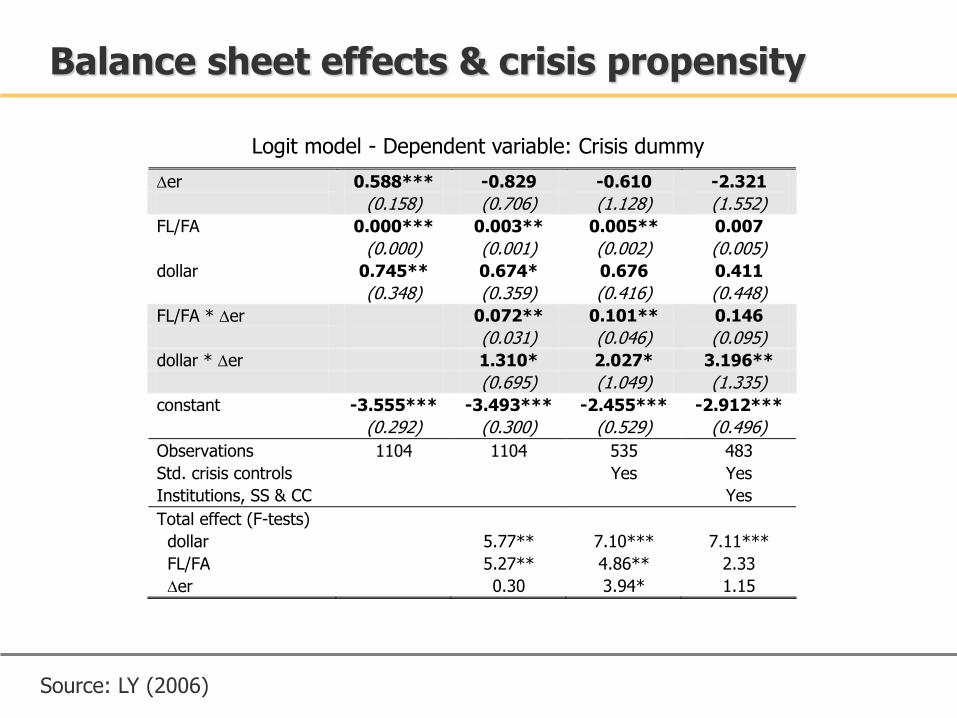

Balance sheet effects & crisis propensity

Logit model - Dependent variable: Crisis dummy

Der 0.588*** -0.829 -0.610 -2.321

(0.158) (0.706) (1.128) (1.552)

FL/FA 0.000*** 0.003** 0.005** 0.007

(0.000) (0.001) (0.002) (0.005)

dollar 0.745** 0.674* 0.676 0.411

(0.348) (0.359) (0.416) (0.448)

FL/FA * Der 0.072** 0.101** 0.146

(0.031) (0.046) (0.095)

dollar * Der 1.310* 2.027* 3.196**

(0.695) (1.049) (1.335)

constant -3.555*** -3.493*** -2.455*** -2.912***

(0.292) (0.300) (0.529) (0.496)

Observations 1104 1104 535 483

Std. crisis controls Yes Yes

Institutions, SS & CC Yes

Total effect (F-tests)

dollar 5.77** 7.10*** 7.11***

FL/FA 5.27** 4.86** 2.33

Der 0.30 3.94* 1.15

Source: LY (2006)

Controlling for deposit dollarization ratios

0%

20%

40%

60%

80%

100%

-2.1

-1.8

-1.4

-1.1

-0.7

-0.3 0.

00.

40.

81.

11.

51.

92.

22.

63.

03.

33.

74.

14.

44.

85.

2

Exchange rate depreciation

Pro

bab

ilit

y o

f a

ban

kin

g c

risi

s

Low dollarization

High dollarization

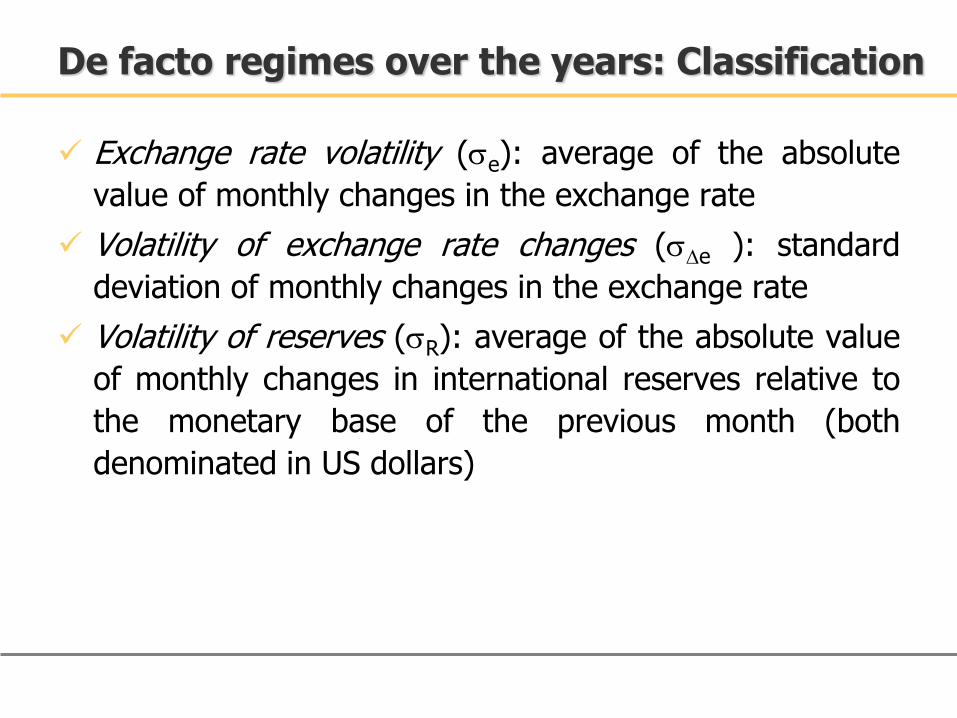

Balance sheet effects & crisis propensity

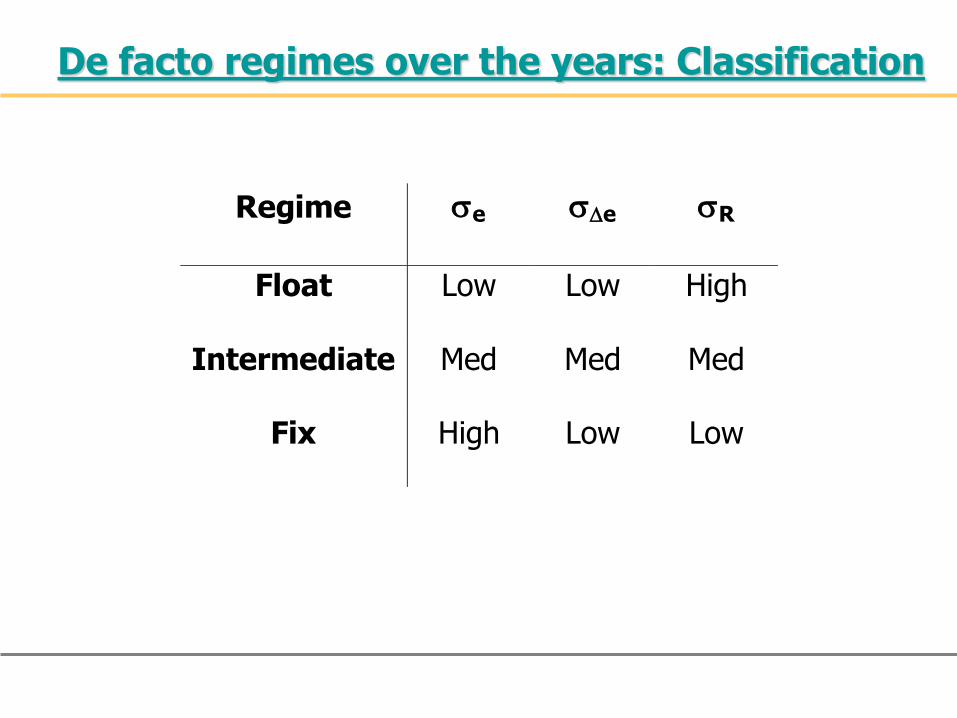

Exchange rate volatility (e): average of the absolute

value of monthly changes in the exchange rate

Volatility of exchange rate changes (De ): standard

deviation of monthly changes in the exchange rate

Volatility of reserves (R): average of the absolute value

of monthly changes in international reserves relative to

the monetary base of the previous month (both

denominated in US dollars)

De facto regimes over the years: Classification

De facto regimes over the years: Classification

Regime e De R

Float Low Low High

Intermediate Med Med Med

Fix High Low Low

Top Related