![Welcome [res.cloudinary.com] · Definition – The number of persons for which the means of egress from a building or portion thereof is designed. Site Inspection (IFC 109.3, 111.4)](https://static.fdocuments.in/doc/165x107/5fa940439a472b490e4d1726/welcome-res-definition-a-the-number-of-persons-for-which-the-means-of-egress.jpg)

Languages

Pages

Legal

Facts and Figures

2010/2011 financial year

Issued September 2010

Contents Tax rates 3Tax offsets 6Capital gains tax 7Superannuation 9Termination payments 19Retirement income streams 21Social security 25Contact list 29

1_ Rates do not include 1.5% Medicare levy.2_ Non-residents are not required to pay Medicare levy.3_ Excluding distributions from property trusts.4_ Excludes dividends (franked or unfranked), interest, royalties, foreign sourced income and

capital gains or losses from assets that are not taxable Australian property. 5_ A list of countries with effective exchange of information agreements can be found in Taxation

Administration Regulations 1976, Regulation 44E.

Personal tax scales — 2010/2011 — residents and non-residents

Taxable income Tax payable(residents)1

Tax payable(non-residents)2

$0-$6,000 $0 29%$6,001–$37,000 $0 + 15% of excess

over $6,00029%

$37,001–$80,000 $4,650 + 30% of excess over $37,000

$10,730 + 30% of excess over $37,000

$80,001–$180,000 $17,550 + 37% of excess over $80,000

$23,630 + 37% of excess over $80,000

Over $180,000 $54,550 + 45% of excess over $180,000

$60,630 + 45% of excess over $180,000

Non-resident withholding tax

Income3 Double Tax Agreement (DTA)

No DTA

Franked dividends 0% 0%Unfranked dividends 15% 30%Interest 10% 10%Royalties 10% 30%

Note: The above rates are general rates of withholding only; the relevant DTA may specify a different rate.

Non-resident withholding tax for fund payments4 from managed investment trusts

Income year Residents of countries with effective exchange of information agreements5

Residents of countries with no effective exchange of information agreements

2010-2011 and onwards 7.5% 30%

Tax rates

3

Other tax rates

Type Entity Tax Rate

Super (accumulation) 15%Super (pension phase) 0%Companies 30%Insurance bonds(offered by life insurance companies)

30%

Taxable income of a trust distributed to benefi ciaries that are presently entitled are taxed in the hands of the benefi ciary. Generally, if no benefi ciary is presently entitled, the trustee is taxed at 46.5%.

Taxation of minors

Not excepted persons and not excepted income but are Australian residents.

Taxable income Tax

Up to $416 $0$417–$1,307 66% of excess over $416Over $1,307 45% on entire amount that is not excepted income

Note: $1,500 low income tax offset may be available; this increases the effective tax free threshold to $3,333.

Medicare levy — 2009/20101 and later income years

0% for taxable income/family income up to…

Phases in to 1.5% for taxable income/family income up to…

Senior Australians tax offset recipientsSingle $30,685 $36,100Couple (combined) no children $44,500 $52,352Pensioner tax offset recipientsSingle $27,697 $32,584Couple (combined) no children $31,196 $36,701Other AustraliansSingle $18,488 $21,750Married/defacto/sole parent $31,196 $36,701Add per dependant child/student $2,865 $3,370

Note: A 100% exemption from the Medicare levy exists for certain prescribed persons.

Tax rates (continued)

4

1_ Medicare levy thresholds are usually confi rmed at the end of each fi nancial year.

Medicare levy surcharge — 2010/2011

Additional 1% Medicare levy surcharge payable for ‘income’ over

Single $77,000Base Family threshold $154,000Families add for the second and subsequent dependant child

$1,500

The Medicare levy surcharge applies where individuals and families do not have private hospital cover and where their ‘income for surcharge purposes’ exceeds the relevant thresholds.Income for surcharge purposes include:> taxable income

> reportable fringe benefi ts > exempt foreign employment income (if your taxable income is $1 or more) > total net investment loss and> Reportable Superannuation Contributions (*RSC)> less the taxable component of a superannuation lump sum to which the low

rate cap amount ($160,000 for 2010/11) has been applied. The additional 1% rate is applied to the individual’s taxable income,

reportable fringe benefi ts and any amount on which family trust distribution tax has been paid.

*RSC include:> Reportable Employer Superannuation Contributions (RESC)1 – are those

contributions where the employee has infl uenced the rate or the amount of superannuation contributed for them and are additional to those contributions that are compulsory (such as SG, contributions made under an industrial agreement, the trust deed or governing rules of a superannuation fund, federal, state or territory law); plus

> Personal deductible contributions.Fringe Benefi ts Tax (FBT)

FBT is calculated by grossing up the taxable value of fringe benefi ts provided to the employee and multiplying this amount by 46.5%. The grossed up amount is calculated depending on the type of benefi t:Type 1 – where GST input tax credits are available to the provider of the

benefi t: Value of benefi ts x 2.0647.Type 2 – where GST input tax credits are not allowed, or GST was not paid by

the provider: Value of benefi ts x 1.8692.Reportable fringe benefi ts are the value of certain fringe benefi ts provided to you or your associates from your employer which exceeds $2,000 in an FBT year. Reportable fringe benefi ts are the grossed up taxable value of these benefi ts that appear on your payment summary for the corresponding fi nancial year.Note: FBT year 1 April 2010 – 31 March 2011.

51_ RESC is defi ned on page 15.

Low Income Tax Offset — 2010/2011

For taxable income under $30,000, a tax offset of $1,500 is available. For income above $30,000 the tax offset reduces by 4c per dollar above $30,000, phasing out at $67,500.

Senior Australians Tax Offset — 2010/2011

Available to taxpayers who, as at 30 June 2011, are of Age Pension or Service Pension age, are eligible for (but may not necessarily receive) an Australian Government Age Pension, or a pension, allowance or benefi t from Veterans’ Affairs, were not in jail and their rebate income1 is within the following thresholds.

Maximum offset2

Shade-out threshold

Cut-out threshold

Single $2,230 $30,685 $48,525Couple (each) $1,602 $26,680 $39,496Couple separated by illness (each)3 $2,040 $28,600 $44,920

Mature Age Worker Tax Offset

Available to individuals aged 55 years and over at the end of the income year, are residents for tax purposes and have received net income from working.

If net income from working is… Tax offset is…

Less than $10,000 5% of net income from workingbetween $10,000 and $53,000 $500more than $53,000 but less than $63,000 $500 is reduced by 5c per $1

over $53,000$63,000 and above Nil

Note: Net income from working is defi ned as the total assessable income that is mainly a reward for personal effort or skills less any relevant deductions plus RESC (defi ned on page 15) plus reportable fringe benefi ts.

Tax offsets

1_ Rebate Income = taxable income + RSC (defi ned on page 5) + total net investment loss + adjusted fringe benefi ts total. Adjusted fringe benefi ts total is determined using the formula: Taxpayer’s reportable fringe benefi ts total x (1 – FBT rate).

2_ Offset reduces by 12.5c for every $1 above shade-out threshold. 3_ Figures are for 2009/2010.

6

Capital Gains Tax (CGT)

Entity Acquisition date CGT method

Individuals, trusts and non-complying superannuation funds

Before 20/09/1985 No CGT20/09/1985–11.45am EST 21/09/1999

Choice of indexed cost base to September 1999 quarter, or 50% discount on capital gain

After 11.45am EST 21/09/1999

50% discount on capital gain

Complying superannuationfunds

30/06/19881 –11.45am EST 21/09/1999

Choice of indexed cost base to September 1999 quarter, or 1/3 discount on capital gain

After 11.45am EST 21/09/1999

1/3 discount on capital gain

Companies Before 20/09/1985 No CGT 20/09/1985–11.45am EST 21/09/1999

Indexed cost base to September 1999 quarter

After 11.45am EST 21/09/1999

Gain fully assessed (no discount)

Notes:> for assets held less than 12 months, the full gain is taxable.> the above table outlines the basic methods for calculating capital gains.

Capital gains assessments can be complex and advisers should recommend clients seek professional tax advice on such matters.

Capital gains

1_ Deemed acquisition date for assets held by complying super funds.

7

1_ This is the last indexation factor applicable for CGT purposes.2_ The ABS has revised their historical AWOTE fi gures from September 1996 to June 2008

to exclude all salary sacrifi ced amounts. This revision will not affect superannuation thresholds prior to 1 July 2009. For more information on the revised AWOTE fi gures, please refer to www.abs.gov.au.

CPI and AWOTE tables

Year CPI factors AWOTE2

Mar Jun Sep Dec Mar Jun Sep Dec1985 — — 71.3 72.71986 74.4 75.6 77.6 79.81987 81.4 82.6 84.0 85.51988 87.0 88.5 90.2 92.01989 92.9 95.2 97.4 99.2 493.4 501.4 509.7 516.81990 100.9 102.5 103.3 106.0 524.8 534.5 541.7 554.41991 105.8 106.0 106.6 107.6 564.3 560.2 567.5 580.11992 107.6 107.3 107.4 107.9 588.8 587.3 585.7 586.91993 108.9 109.3 109.8 110.0 595.5 598.0 600.8 603.51994 110.4 111.2 111.9 112.8 612.3 616.9 620.0 629.91995 114.7 116.2 117.6 118.5 639.9 647.2 653.1 661.01996 119.0 119.8 120.1 120.3 665.8 671.2 674.6 685.51997 120.5 120.2 119.7 120.0 696.1 697.6 704.3 710.91998 120.3 121.0 121.3 121.9 721.3 725.2 735.4 742.71999 121.8 122.3 123.41 124.1 743.8 747.3 753.0 764.22000 125.2 126.2 130.9 131.3 774.8 784.2 796.1 800.42001 132.7 133.8 134.2 135.4 810.6 824.1 838.5 848.72002 136.6 137.6 138.5 139.5 860.5 866.8 879.4 889.62003 141.3 141.3 142.1 142.8 900.4 921.0 929.6 938.42004 144.1 144.8 145.4 146.5 947.8 949.5 962.9 976.42005 147.5 148.4 149.8 150.6 992.9 1006.7 1023.2 1025.72006 151.9 154.3 155.7 155.5 1037.5 1041.6 1053.0 1058.62007 155.6 157.5 158.6 160.1 1073.8 1090.0 1105.1 1108.52008 162.2 164.6 166.5 166.0 1124.8 1131.1 1151.4 1165.32009 166.2 167.0 168.6 169.5 1183.4 1195.6 1204.2 1226.82010 171.0 1243.9

Capital gains (continued)

Capital gainsSuperannuation

9

Contributions – who is eligible to contribute to superannuation?

Age of member Eligibility to contribute

Under 65 years Contributions can be made by the member or made on a member’s behalf at any time.

Aged 65 to 69 years

The member must have been gainfully employed on at least a part-time basis (ie for at least 40 hours in a period of not more than 30 consecutive days) in the fi nancial year in which they wish to make or have contributions made on their behalf — personal contribution, employer contribution or spouse contribution.

Alternatively, the contributions are mandated (award, certifi ed agreement or Superannuation Guarantee (SG)).

Aged 70 to 74 years

The member must have been gainfully employed on at least a part-time basis (ie for at least 40 hours in a period of not more than 30 consecutive days) in the fi nancial year in which they wish to make or have contributions made on their behalf – personal contribution or employer contribution.

Alternatively, the contributions are mandated (award or certifi ed agreement but not SG).

Aged 75 years and over

Generally, only mandated employer contributions (award or certifi ed agreement but not SG) are allowed.

Member and employer contributions received on or before 28 days after the end of the month in which the member turns 75 can be accepted where the member meets the work test described above.

Spouse contributions

The contributing spouse can be of any age, the receiving spouse must be under age 65, or if 65 to 69, gainfully employed for at least 40 hours within a consecutive 30 day period in the fi nancial year in which the contribution is made.

Income1 Offset2 is calculated at 18% of lesser of:

$10,800 or less $3,000 or Spouse Contribution $10,801 to $13,799 $3,000 – (Income – $10,800) or Spouse Contribution $13,800 or more Nil

1_ Income = assessable income + reportable fringe benefi ts + RESC (defi ned on page 15).2_ Maximum offset is $540.

Contributing and receiving spouse must be resident taxpayers.

Superannuation (continued)

10

1_ Indexed to AWOTE in $5,000 increments (rounded down).2_ Not subject to indexation. 3_ 6 times CC cap (currently $25,000).4_ 3 times NCC cap (currently $150,000).5_ This includes capital proceeds from the disposal of small business assets that would have

been CGT exempt except: — if they were pre-CGT assets, or — if there was no capital gain, or — where the 15 year holding period was not met because of the permanent incapacity of

the person (or a signifi cant individual of a company or trust).6_ Generally constitutionally protected funds are run by state governments for employees, or

for members of the judiciary.7_ Individuals with defi ned benefi t funds will need to request details from their fund on the

amount of notional taxed contributions that will be included as concessional contributions.

Contributions caps — 2010/2011

Concessional contributions (CC) cap

Non-concessional contributions (NCC) cap

Capital gains tax (CGT) cap

$25,0001 per person, per fi nancial year or

$50,0002 per person, per fi nancial year if aged 50 or over at any time in the fi nancial year.The transitional period ends on30 June 2012.

$150,0003 per person, per fi nancial year or

$450,0004 over 3 years if under 65 on 1 July of the fi nancial year.

$1.155 million1 lifetime limit

The following contributions are allowed under this cap:> up to $500,000 of capital gains

where the small business retirement exemption has been claimed (lifetime limit and not indexed)

> capital proceeds from the disposal of small business assets that are exempt from CGT under the small business 15 year exemption5.

There are no caps on amounts contributed from certain payments for personal injury.

Concessional contributions

The following contribution types will be included in an individual’s concessional contributions cap: > Employer contributions (including SG and salary sacrifi ce) except for those

contributions made to a constitutionally protected fund6; > After-tax contributions for which a personal tax deduction has

been claimed;> Untaxed elements of the taxable component of directed termination

payments over $1 million contributed under the transitional rules for employment termination payments;

> Notional taxed contributions (defi ned benefi t funds)7; and> Certain allocations from reserve accounts in a super fund.

11

Non-concessional contributions

The following contribution types will be included in an individual’s non-concessional contributions cap: > after-tax contributions for which no tax deduction is claimed;> spouse contributions; > amounts transferred from overseas super funds1 (excluding the taxable

amount of such transfers); > contributions made from the proceeds from the sale of qualifying small

business assets unless they count towards the CGT cap (which is $1.155 million in 2010/11); and

> amounts of concessional contributions in excess of the concessional contributions cap.

Excess contributions> Amounts in excess of an individual’s concessional contributions cap will be

subject to an additional tax of 31.5%. This tax may be paid by withdrawing amounts from superannuation or by the individual personally.

> Amounts in excess of an individual’s non-concessional contributions cap will be subject to an additional tax of 46.5%. This tax must be paid by withdrawing amounts from superannuation.

> Excess concessional contributions also count towards an individual’s non-concessional contributions cap. Contributions in excess of both caps may be liable for excess contributions tax at a total rate of 93%.

Preservation age

Date of birth Preservation age

Before 1/07/60 551/07/60 – 30/06/61 561/07/61 – 30/06/62 571/07/62 – 30/06/63 581/07/63 – 30/06/64 59On or after 1 July 1964 60

Departing Australia superannuation payment rates

Component Withholding tax rate

Tax free 0%Taxable (taxed element) 35%Taxable (untaxed element) 45%

1_ A super fund is generally unable to accept an overseas transfer exceeding $450,000 (or $150,000 if the individual is 65 or over on 1 July of the fi nancial year in which the transfer is made) unless APRA has granted an exemption. You should check with your super provider.

12

Superannuation (continued)

Benefi ts – Superannuation conditions of release

Release condition Cashing restriction

Retirement1 Nil Attaining age 65 Nil Death2 Nil Terminal medical condition2 Nil Permanent incapacity2 Nil Attaining preservation age Only as a non-commutable income

stream and no lump sumsSevere fi nancial hardship

a) In receipt of a qualifying income support payment for 26 weeks

b) Age 55+39 weeks and be in receipt of a qualifying income support payment for 39 weeks

a) Single lump sum between $1,0003 and $10,000

b) Nil

Compassionate grounds Only as a single lump sum not exceeding the amount determined by the Regulator

Termination of employment with an employer who had contributed to the fund

a) Preserved benefi ts – as a non-commutable life pension/annuity

b) Restricted non-preserved benefi ts – Nil

Temporary incapacity2 Received as a non-commutable income stream4 for a period not exceeding the period of incapacity

Former temporary resident (Departing Australia Superannuation Payment)2

Entire benefi t paid as a single lump sum

Termination of employment with standard employer sponsor where the preserved benefi t is under $200

Nil

Being a lost member who is found where the balance is under $200

Nil

Provision of a release authority for excess contributions tax

The amount5 of excess concessional or non-concessional contributions tax

13

Notes:

1_ Where a member has reached preservation age, retirement occurs when an arrangement under which the member was gainfully employed has come to an end and the trustee is reasonably satisfi ed that the member intends never again to become gainfully employed either part time or full time (ie for 10 or more hours per week). Where aged at least 60 but less than 65, retirement occurs when an arrangement under which the member was gainfully employed has ceased on or after the member reached age 60.

2_ Temporary residents may only use these conditions of release. Temporary residents exclude holders of retirement visas — subclass 405 and 410, Australian or New Zealand citizens or permanent residents of Australia. This rule does not apply to those who have met a condition of release in the table prior to 1 April 2009, even if the benefi t is paid after this date.

3_The entire amount may be cashed if less than $1,000.4_The benefi ts must not be paid from the member’s minimum benefi ts.5_Conditions apply.

Tax deductions for contributions

To claim a tax deduction for a contribution to superannuation, the fund must have received the contribution in that fi nancial year.

Individuals

For the purpose of claiming a personal tax deduction for personal contributions, eligible persons are: > self employed persons; > substantially self employed persons (if less than 10% of a person’s

assessable income, RESC1 and reportable fringe benefi ts2 are attributable to employment as an employee for the fi nancial year); and

> persons who are not deriving income from an employer. This continues to include anyone who is not employed and aged 18 to 64. Those under 18 at the end of the fi nancial year cannot claim a tax deduction unless they earned income as an employee or business operator in that fi nancial year.

Individuals must make personal contributions before 28 days after the end of the month in which they turn 753. The full amount of the contribution can be claimed as a deduction.

Restricted time period to give notice to super funds

Generally, the individual must provide a notice by 30 June in the fi nancial year following the fi nancial year in which the contribution was made. For the 2010/11 fi nancial year this will be 30 June 2012. However, some individuals will need to notify their super fund prior to this date as their ability to claim a deduction will cease on the date: > they lodge their tax return for the 2010/11 year (year in which the

contribution was made); > they cease to be a member of the fund; > the super fund trustee no longer holds all of the contributions (eg this will

generally occur after any partial withdrawal); > the super fund trustee begins to pay an income stream based in whole or

part on the contribution; or> the super fund trustee is provided with a request from the member to split

contributions with their spouse.

Employers

Employers are entitled to a full tax deduction for superannuation contributions made for employees.

14

Superannuation (continued)

1_ Reportable Employer Superannuation Contributions (RESC) is defi ned on page 15.2_ Reportable Fringe Benefi ts is defi ned on page 5.3_ Normal work test rules apply for contributions made on or after age 65 (refer to page 9 for further

information).

Co-contribution eligibility — 2010/2011

An individual must meet the following criteria to be eligible for the Government co-contribution: > They make a personal after-tax contribution to their superannuation fund. > ‘Total Income’ for the fi nancial year is less than $61,920.

Total Income1 = Assessable Income + Reportable Fringe Benefi ts2 + Reportable Employer Superannuation Contributions (RESC)

> At least 10%3 or more of the person’s ‘Total Income’ for the fi nancial year is attributable to either or both:

i_ the person engaging in activities where treated as an employee for the purposes of SG legislation.

ii_the person carrying on a business. > They are not a temporary resident. > They are under 71 at the end of the fi nancial year.> They have lodged a tax return for the fi nancial year.Co-contribution entitlement

Total income4 Reduction in co-contribution

Maximumco-contribution

$31,920 or less No reduction $1,000$31,920–$61,920 (Total Income – $31,920)

x 0.03333$1,000 – Reduction in co-contribution

$61,920 or more No entitlement Nil

The Government co-contribution entitlement is then worked out as the lesser of: > Maximum co-contribution (worked out above) and > Personal after-tax contribution made in fi nancial year x $15.

Reportable Employer Superannuation Contributions (RESC) are amounts contributed by an employer, or an associate of the employer, for the individual’s benefi t to the extent that the individual has or has had, or might reasonably be expected to have or have had, the capacity to infl uence either the size of the amount or the way the amount is contributed so that his or her assessable income is reduced (eg salary sacrifi ce). It excludes superannuation guarantee, mandated and after-tax contributions.

15

1_ Where self employed, ‘Total Income’ is reduced by allowable business deductions. Deductible contributions to super and work related employee deductions are not allowable business deductions and cannot reduce ‘total income’.

2_ Reportable Fringe Benefi ts is defi ned on page 5.3_ Business deductions do not reduce ‘total income’ for 10% test.4_ For the 2010/11 and 2011/12 fi nancial years, the lower and upper thresholds of $31,920 and

$61,920 (respectively) will be frozen.5_ The $1 for $1 matching rate remains indefi nitely resulting in a maximum co-contribution of $1,000.

Super Guarantee (SG)

9% of employees’ ‘ordinary time earnings’ (up to $42,220 per quarter for 2010/2011) is payable to a complying super fund. $42,220 per quarter equates to $168,880 per annum representing a maximum SG entitlement of $15,199.

SG quarter Cut off date for SG contribution

Due date for lodgement of a SG statement if not made by cut off date

1 July – 30 September 28 October 28 November1 October – 31 December 28 January 28 February 1 January – 31 March 28 April 28 May1 April – 30 June 28 July 28 August

Superannuation member benefi ts — taxed element in the fund

Age Superannuation lump sum1 Superannuation income stream1

Below preservation age

20% MTR no pension offset2

Preservation age to age 59

First $160,000 at 0%

Excess at 15%

MTR with 15% pension offset

Aged 60 and above Tax free Tax free

Superannuation member benefi ts — untaxed element in the fund

Age Superannuation lump sum1 Superannuation income stream1

Below preservation age

First $1.155 million at 30%

Excess at 45%

MTR no pension offset

Preservation ageto age 59

First $160,000 at 15%

$160,001–$1.155 million at 30%

Excess at 45%

MTR no pension offset

Aged 60 and above

First $1.155 million at 15%

Excess at 45%

MTR with 10% pension offset

Superannuation (continued)

16

1_ Describes taxable component only; tax free component is always tax free. Rates do not include Medicare levy.

2_ A disability superannuation income stream also receives a 15% tax offset.

Superannuation death benefi ts paid to dependant1 — taxed element in the fund

Age of deceased Type of benefi t Age of recipient Taxation2

Below age 60 Income stream3 Below age 60 MTR with 15% pension offset

Above age 60 Tax freeAge 60 and over Income stream3 Any age Tax freeAny age Lump sum Any age Tax free

Superannuation death benefi ts paid to dependant1 — untaxed element in the fund

Age of deceased Type of benefi t Age of recipient Taxation2

Below age 60 Income stream3 Below age 60 MTRno pension offset

Above age 60 MTRwith 10% offset

Age 60 and over Income stream3 Any age MTRwith 10% offset

Any age Lump sum Any age Tax free

Superannuation death benefi ts paid to non-dependant1

— taxed and untaxed elements in the fund

Age of deceased

Type of benefi t

Age of recipient

Taxation2

Any age Lump sum

Any age Taxable component (taxed element) at 15%Taxable component (untaxed element4) at 30%

Any age Income stream

Any age n/a3

Income streams commenced prior to 1 July 2007 will be taxed as if received by a dependant

1_ Dependant for tax purposes. 2_ Describes taxable component only; tax free component is always tax free. Rates do not include

Medicare levy. 3_ SIS Regs only allow a death benefi t income stream to be paid to dependent child; less than 18, or if

over 18, either fi nancially dependent and less than 25 or have a specifi ed disability. 4_ An untaxed element will only arise in a taxed fund where the lump sum death benefi t contains an

insurance payout, where the benefi t is paid to a non-dependant. The amount of the untaxed element is calculated by using a statutory formula.

17

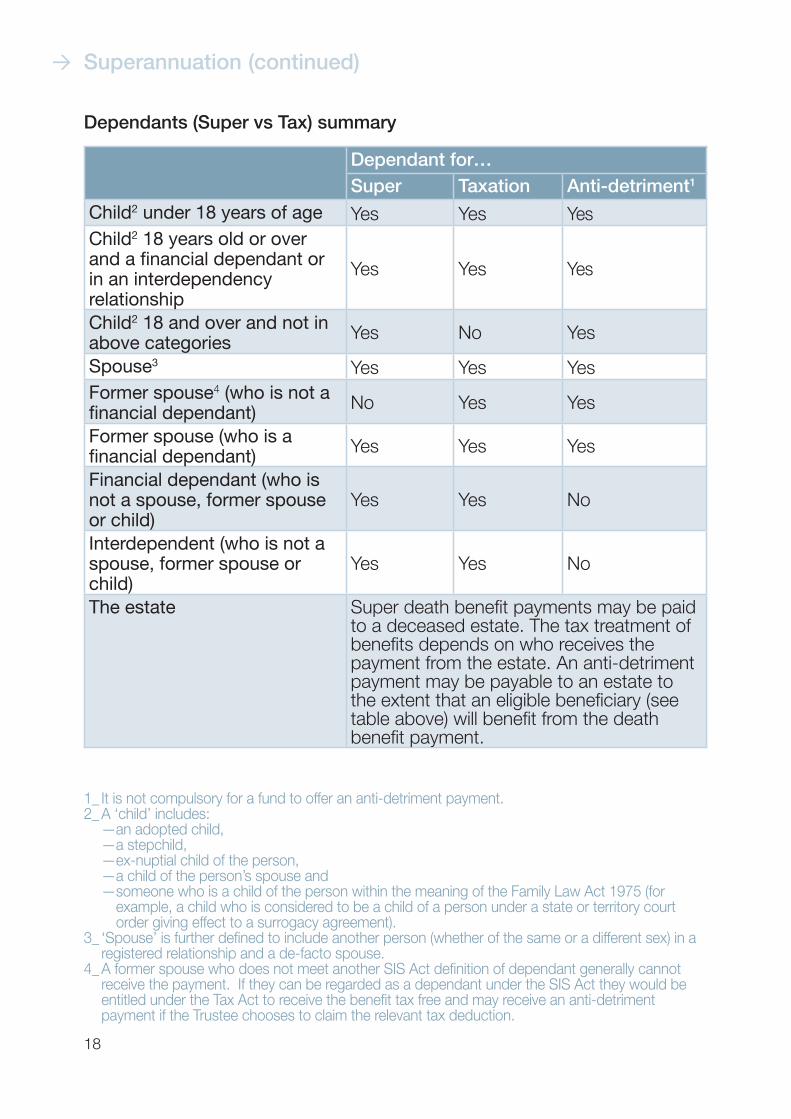

Dependants (Super vs Tax) summary

Dependant for…

Super Taxation Anti-detriment1

Child2 under 18 years of age Yes Yes YesChild2 18 years old or over and a fi nancial dependant or in an interdependency relationship

Yes Yes Yes

Child2 18 and over and not in above categories Yes No Yes

Spouse3 Yes Yes YesFormer spouse4 (who is not a fi nancial dependant) No Yes Yes

Former spouse (who is a fi nancial dependant) Yes Yes Yes

Financial dependant (who is not a spouse, former spouse or child)

Yes Yes No

Interdependent (who is not a spouse, former spouse or child)

Yes Yes No

The estate Super death benefi t payments may be paid to a deceased estate. The tax treatment of benefi ts depends on who receives the payment from the estate. An anti-detriment payment may be payable to an estate to the extent that an eligible benefi ciary (see table above) will benefi t from the death benefi t payment.

18

1_ It is not compulsory for a fund to offer an anti-detriment payment.2_ A ‘child’ includes:

—an adopted child, —a stepchild, —ex-nuptial child of the person, —a child of the person’s spouse and — someone who is a child of the person within the meaning of the Family Law Act 1975 (for

example, a child who is considered to be a child of a person under a state or territory court order giving effect to a surrogacy agreement).

3_ ‘Spouse’ is further defi ned to include another person (whether of the same or a different sex) in a registered relationship and a de-facto spouse.

4_ A former spouse who does not meet another SIS Act defi nition of dependant generally cannot receive the payment. If they can be regarded as a dependant under the SIS Act they would be entitled under the Tax Act to receive the benefi t tax free and may receive an anti-detriment payment if the Trustee chooses to claim the relevant tax deduction.

Superannuation (continued)

1_ This rate does not include Medicare levy. 2_ Otherwise known as a ‘directed termination payment’, this applies if (as at 9 May 2006) a

termination payment was specifi ed under a written contract, Australian or foreign law or workplace agreement under Workplace Relations Act 1996.

3_ Dependant for tax purposes.

Termination payments

Genuine redundancy and approved early retirement scheme payments

The fi rst $8,126 plus $4,064 for each full year of service is tax free.The remainder is taxed as an employment termination payment.

Employment termination payments

Tax payer Taxablecomponent

Maximum rate1

ETPs Below preservation age

First $160,000 30%

Excess 45%Preservation age and over

First $160,000 15%

Excess 45%Transitional rules2 — ETP cashed prior to 1 July 2012

Below preservation age

First $1 million 30%

Excess 45%Preservation age and over

First $160,000 15%

Between $160,000 – $1 million

30%

Excess 45%Transitional rules2 — ETP contributed to super prior to1 July 2012

Subject to individual meeting contribution rules

Taxable amount 15% taxed within fund

Death benefi t employment termination payments

Recipient Taxable component

Maximum rate1

Paid to dependant3 Any age First $160,000 0% Excess 45%

Paid to non-dependant3

Any age First $160,000 30%

Excess 45%

19

Unused long service leave

Amount assessed Maximum rate1

Standard paymentBefore 16 August 1978 5% MTR16 August 1978– 17 August 1993

100% 30%

After 17 August 1993 100% MTRGenuine redundancy and approved early retirement scheme paymentsBefore 16 August 1978 5% MTRAfter 15 August 1978 100% 30%

Unused annual leave2

Amount assessed Maximum rate1

Standard paymentBefore 18 August 1993 100% 30%After 17 August 1993 100% MTRGenuine redundancy and approved early retirement scheme paymentsWhole period 100% 30%

20

1_ This rate does not include Medicare levy. 2_ Including annual leave loading.

Termination payments (continued)

Retirement income streams

Pension payments

A pension commenced on or after 1 July 2007 will have a tax free and taxable amount based on the fi xed percentage of the tax free and taxable components at commencement.

See tables: Superannuation member benefi ts — taxed element in the fund (page 16).Superannuation member benefi ts — untaxed element in the fund (page 16).

A pension commenced before 1 July 2007 will still have a deductible amount (see below) based on the existing formula until a trigger event occurs.Trigger events are those aged 60 and over at 1 July 2007, turning 60, commutation (either partial or full) and death.

Pension/Annuity deductible amounts (Pre 1 July 2007)

For most pensions and annuities, the deductible amounts are calculated differently for tax and for FaCHSIA (Centrelink)/DVA purposes as follows:

Deductible amount for tax

= (Undeducted purchase price – Residual capital value)

Relevant number

Income stream started… Undeducted purchase price includes…

Before 1 July 1994 Undeducted, concessional, pre ‘831 July 1994 – 30 June 1997 Undeducted1 July 1997 – 3 June 1998 Undeducted, CGT exemptAfter 3 June 1998 Undeducted, post June 1994

invalidity, CGT exempt

Deduction amount

FaCHSIA (Centrelink)/DVA =

On commutation:

FaCHSIA (Centrelink)/DVA =

21

(Original purchase price – Residual capital value) - Commutation(s)

Original relevant number

(Purchase price – Residual capital value)

Relevant number

Life Expectancies

2000-2002 2005-2007

Age Male Female Male Female

55 25.92 29.91 26.95 30.5356 25.05 29.00 26.08 29.6157 24.19 28.10 25.20 28.7058 23.34 27.21 24.34 27.7959 22.49 26.32 23.48 26.8960 21.66 25.44 22.63 26.0061 20.84 24.57 21.79 25.1162 20.04 23.71 20.96 24.2363 19.24 22.85 20.14 23.3564 18.46 22.00 19.34 22.4865 17.70 21.15 18.54 21.6266 16.95 20.32 17.76 20.7667 16.21 19.49 16.99 19.9268 15.48 18.67 16.24 19.0869 14.78 17.87 15.49 18.2470 14.08 17.08 14.76 17.4271 13.41 16.29 14.04 16.6172 12.75 15.53 13.33 15.8273 12.11 14.78 12.64 15.0374 11.50 14.05 11.96 14.2775 10.90 13.33 11.31 13.5176 10.32 12.63 10.68 12.7877 9.77 11.94 10.07 12.0578 9.24 11.27 9.48 11.3579 8.73 10.61 8.92 10.6780 8.24 9.98 8.38 10.0181 7.77 9.38 7.86 9.3782 7.32 8.81 7.36 8.7583 6.89 8.27 6.89 8.1784 6.48 7.76 6.45 7.6185 6.11 7.28 6.03 7.0886 5.77 6.83 5.64 6.5887 5.47 6.41 5.27 6.1188 5.20 6.02 4.94 5.6889 4.95 5.66 4.63 5.2890 4.74 5.33 4.36 4.91

RetirementRetirement income streams (continued)

22

1_ The minimum payment rule is not required to be met until the following fi nancial year for account based income streams that commence on or after 1 June in a fi nancial year.

2_ The relief from the standard minimum payment requirements for 2010/2011 applies to account based annuities and pensions, allocated annuities and pensions and market linked annuities and pensions.

Minimum annual pension percentage

The minimum1 payment for an account based income stream is determined by multiplying the account balance by the age based percentage.

Age (at commencement or each 1 July)

Percentage of account balance

Percentage of account balance for 2010/20112

Under 65 4% 2%65 to 74 5% 2.5%75 to 79 6% 3%80 to 84 7% 3.5%85 to 89 9% 4.5%90 to 94 11% 5.5%95 and over 14% 7%

No maximum annual payment unless pension is a Transition to Retirement (TTR) pension. For TTR pensions, the maximum annual payment is 10% of the account balance at commencement or each 1 July.

23

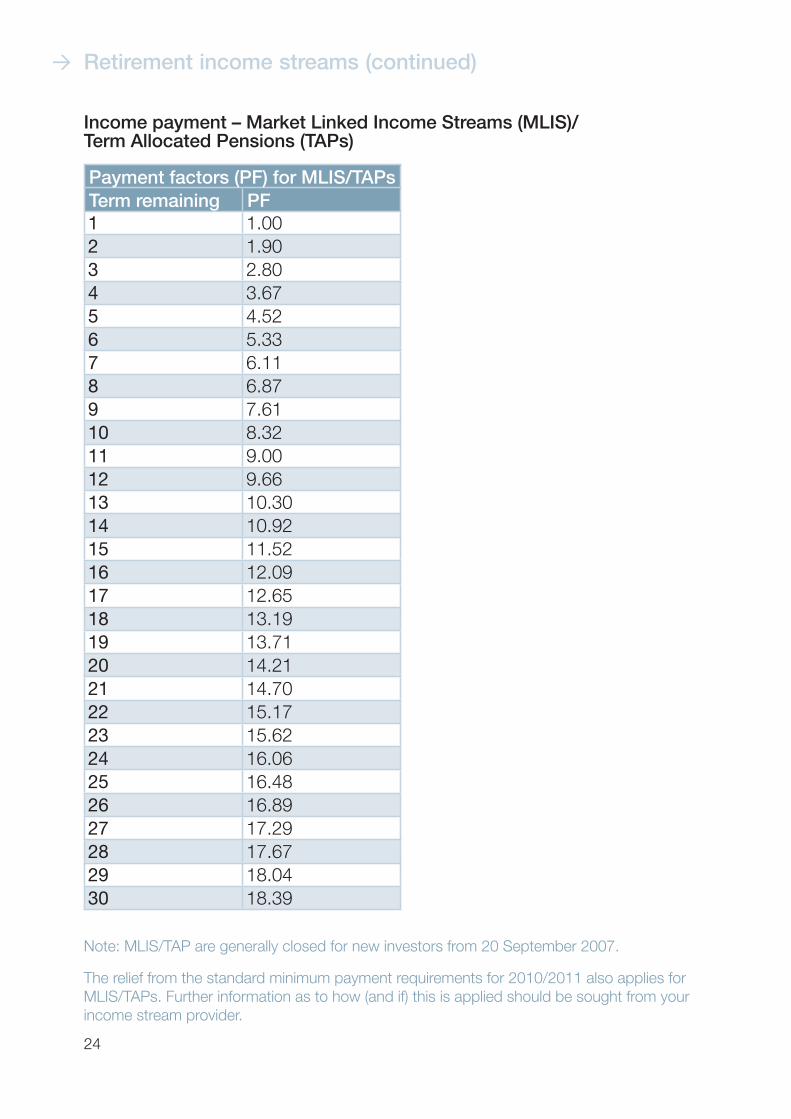

Income payment – Market Linked Income Streams (MLIS)/Term Allocated Pensions (TAPs)

Payment factors (PF) for MLIS/TAPs

Term remaining PF

1 1.002 1.903 2.804 3.675 4.526 5.337 6.118 6.879 7.6110 8.3211 9.0012 9.6613 10.3014 10.9215 11.5216 12.0917 12.6518 13.1919 13.7120 14.2121 14.7022 15.1723 15.6224 16.0625 16.4826 16.8927 17.2928 17.6729 18.0430 18.39

Retirement (continued)

24

RetirementRetirement income streams (continued)

Note: MLIS/TAP are generally closed for new investors from 20 September 2007.

The relief from the standard minimum payment requirements for 2010/2011 also applies for MLIS/TAPs. Further information as to how (and if) this is applied should be sought from your income stream provider.

1_ Men born before 1 July 1952 are eligible at age 65.2_ DVA Service pension age for veterans with qualifying service is generally 5 years younger than the

ages specifi ed above.3_ Applying from 20 September 2009.4_ These amounts include the maximum fortnightly Pension Supplement available for singles and

couples respectively.5_ Residing in Australia or temporarily absent from Australia for a continuous period not

exceeding 13 weeks.

Social security

Age qualifi cation – Pension age for woman born on or before 30 June 1952

Date of birth Eligible at age1

Born on or before 31 December 1945 Eligible now1 January 1946 to 30 June 1947 64.01 July 1947 to 31 December 1948 64.51 January 1949 to 30 June 1952 65.0

Age qualifi cation – Pension age for women and men1 born on or after 1 July 1952

Date of birth Eligible at age2

1 July 1952 to 31 December 1953 65.51 January 1954 to 30 June 1955 66.01 July 1955 to 31 December 1956 66.5On or after 1 January 1957 67.0

Current vs transitional rules

The following table depicts the changes that apply under the current and transitional rules. If the transitional rules apply, a transitional rate will be paid to the pensioner.

Item Current rules3 Transitional rules

Maximum payment as at 1 July 2010

$701.104 per f/n (singles)

$528.504 per f/n (each couple)

$634.305 per f/n (singles)

$512.305 per f/n (each couple)

Work bonus Yes No Income test taper rate

50c (singles), 25c (each couple)

40c (singles), 20c (each couple)

Additional income test ‘free area’ for dependent children

No Yes, $24.60 per f/n per child

25

Age and DVA Service Pension assets test – 1 July 2010

Homeowners For full pension / allowance(up to)

For part pension

Current rules1

(less than)Transitional rules (less than)

Single $181,750 $649,250 $604,750

Couple (combined) $258,000 $963,000 $941,500

Illness separated couple (combined)

$258,000 $1,193,000 $1,104,000

Non-homeowner For full pension / allowance(up to)

For part pension

Current rules1

(less than)Transitional rules (less than)

Single $313,250 $780,750 $736,250

Couple (combined) $389,500 $1,094,500 $1,073,000

Illness separated couple (combined)

$389,500 $1,324,500 $1,235,500

Fortnightly pension reduces by $1.50 per $1,000 (single and couple combined) of assets over full pension threshold.Age and DVA Service Pension income test – 1 July 2010

Family Situation For full pension(up to)

For part pension

Current rules1

(less than)Transitional rules (less than)

Single $146 $1,548.20 $1,731.75

Couple (combined) $256 $2,370.00 $2,817.50

Illness separated couple (combined)

$256 $3,060.40 $3,427.50

For income test taper rates, refer to Current vs transitional rules table on page 25.

26

Social security (continued)

1_ Applying from 20 September 2009.

Newstart Allowance — 1 July 2010

Single, no children $462.80 per f/nPartnered (each) $417.70 per f/n

Note: Pharmaceutical Allowance may be payable in addition; at $6 per f/n (eligible single) and $3 per f/n (each eligible member of couple).

Allowance assets test

No allowance is payable if assessable assets of the person exceed the following thresholds.

Homeowner Non-homeowner

Single $181,750 $313,250Couple (combined) $258,000 $389,500

Allowance income test

No reduction in the allowance will occur where fortnightly income is less than $62. The allowance reduces by 50c for every dollar of fortnightly income between $62 and $250. Thereafter the allowance reduces at 60c for every dollar above $250. Partner income may reduce allowance paid.

Deeming rates — 1 July 2010

Financial investments

Deemed income Maximum fi nancial investments before pension impact

Single Below $43,200 3% n/aAbove $43,200 $1,296 + 4.5%

above $43,200$98,756

Pensioner couple (combined)

Below $72,000 3% n/aAbove $72,000 $2,160 + 4.5%

above $72,000$171,911

27

Deprivation of income and assets

Deprived assets will be assets tested and deemed for 5 years from the date of gifting where:> the gift exceeds $10,000 in a single fi nancial year or> total gifting exceeds $30,000 over the current and previous 4 fi nancial

years if not assessed under the fi rst test.The disposal limits apply to both singles and couples.

Commonwealth Seniors Health Card (CSHC)

Maximum Adjusted Taxable Income (ATI)1

Single $50,000Couple $80,000 (combined) Couple (separated by illness) $100,000 (combined)

The limit is increased by $639.60 for each dependent child.

28

Social security (continued)

1_ ATI for the tax year is the sum of taxable income, employer provided fringe benefi ts for the applicable tax year, target foreign income, reportable superannuation contributions and total net investment losses.

Contact list

29

ATO

Superannuation info line 131 020Personal tax info line 132 861Website www.ato.gov.au

Centrelink

Disability, Sickness & Carers help line 132 717Retirement help line 132 300Website www.centrelink.gov.au

FaHCSIA

Website www.fahcsia.gov.au

DVA

Info line 133 254Website www.dva.gov.au

APRA

Phone 1300 131 060Website www.apra.gov.au

ASIC

Phone 1300 300 630Website www.asic.gov.auInvestor website www.fido.gov.au

For general information only

This information has been prepared by BT Funds Management Ltd ABN 63 002916 458. It is provided solely for the general information of external fi nancial advisers and must not be relied on as a substitute for legal, tax or other professional advice. Further, it must not be copied, used, reproduced or otherwise distributed or circulated to any retail client or other party. The information is given in good faith and has been derived from sources believed to be accurate at its issue date. However, it should not be considered a comprehensive statement on any matter nor relied upon as such. BT Funds management Ltd (including its related entities, employees and directors) does not give any warranty of reliability or accuracy or accept any responsibility arising in any way including by reason of negligence for errors or omissions in the information. BT8767-0710rr

Top Related