Languages

Pages

Legal

Equity Relationships and the Balance Sheet

What do we know?

• We know what an expanded ledger is!

• We know how to show balances of new accounts on income statements.

• We know the income statement is the second major statement in accounting.WHAT IS THE FIRST?

• We have to understand equity accounts and how they relate to each other mathematically. Let’s look again at Eve Boa, LLB.

• Everything is in balance.

• New equity accounts are there.

• To make a balance sheet agree, theamounts in the trial balance could bemoved to a balance sheet, but largecompanies would have trouble withthis. SO WHAT DO WE DO?

• We have to come up with some equity calculations. Debits and credits will help us understand the calculations needed.

• Eve’s beginning capital was $21,878. This is a credit balance.

• If revenues are greater than expenses, what do we have?

Equity Calculations.

Beginning Capital + Net Income

Beginning Capital + Net Income – Drawings =

Ending Capital$21,878 + 8209 = 26,137

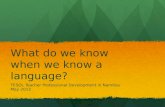

Equity Calculations

• What if the Net Income is a Net Loss?

• Capital can also be a debit balance. How? Then what would we do?

• What if there are investments?

Beginning Capital - Net Income – Drawings =

Ending Capital

Top Related