Languages

Pages

Legal

Climate Finance at

scale: emerging

opportunities

Helena McLeod, KPMG

Thomas E Downing, Global Climate Adaptation Partnership

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 1

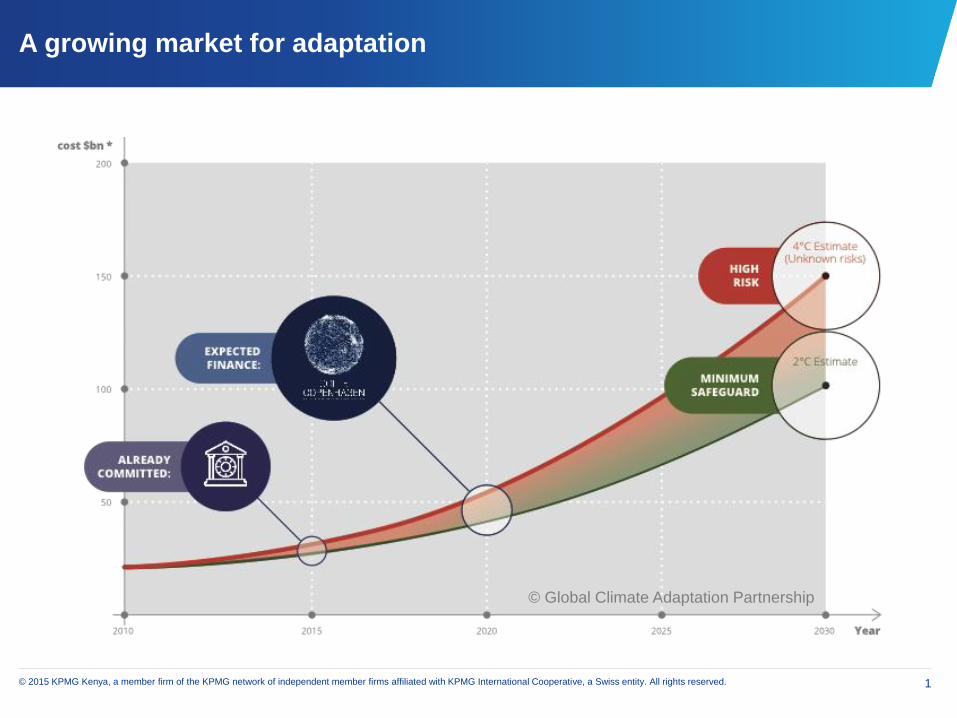

A growing market for adaptation

© Global Climate Adaptation Partnership

2015

Change

Readiness

Index

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 3

Change

readiness: a country’s capacity to

anticipate, prepare for,

manage, respond to

change & cultivate

resulting opportunity

No government, business or society is immune to change

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 4

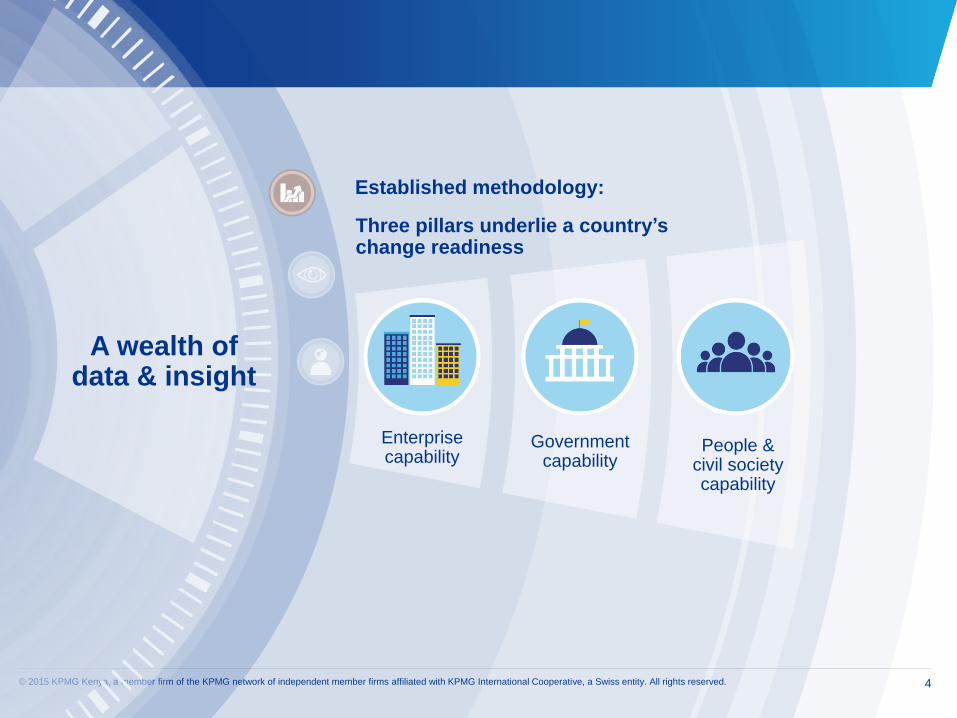

Established methodology:

Three pillars underlie a country’s change readiness

Enterprise capability

Government capability

People & civil society capability

A wealth of data & insight

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 5

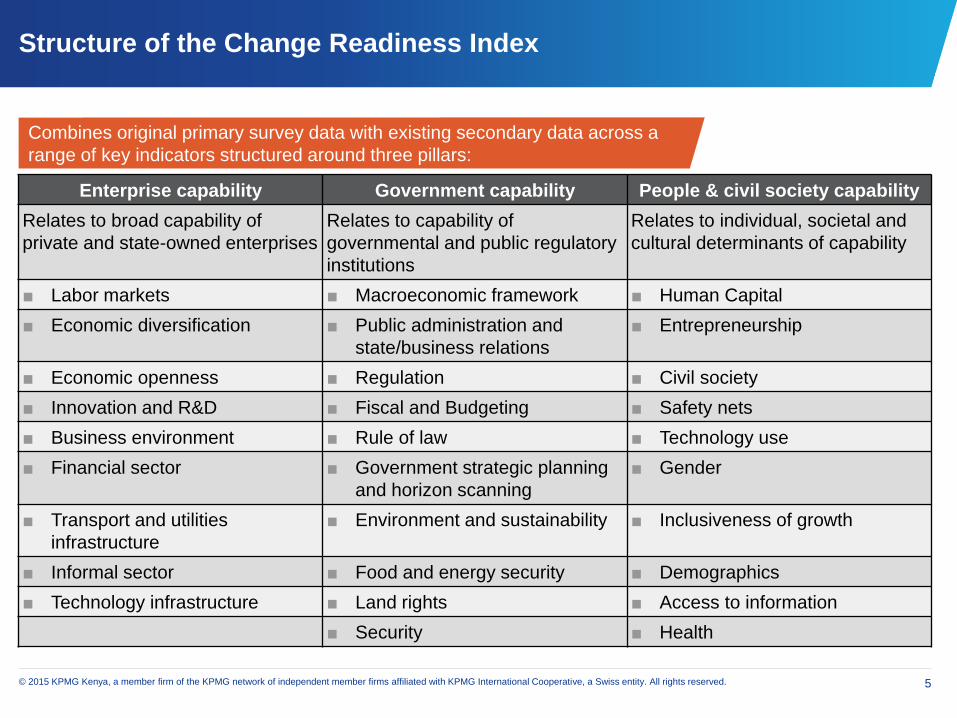

Structure of the Change Readiness Index

Enterprise capability Government capability People & civil society capability

Relates to broad capability of

private and state-owned enterprises

Relates to capability of

governmental and public regulatory

institutions

Relates to individual, societal and

cultural determinants of capability

■ Labor markets ■ Macroeconomic framework ■ Human Capital

■ Economic diversification ■ Public administration and

state/business relations

■ Entrepreneurship

■ Economic openness ■ Regulation ■ Civil society

■ Innovation and R&D ■ Fiscal and Budgeting ■ Safety nets

■ Business environment ■ Rule of law ■ Technology use

■ Financial sector ■ Government strategic planning

and horizon scanning

■ Gender

■ Transport and utilities

infrastructure

■ Environment and sustainability ■ Inclusiveness of growth

■ Informal sector ■ Food and energy security ■ Demographics

■ Technology infrastructure ■ Land rights ■ Access to information

■ Security ■ Health

Combines original primary survey data with existing secondary data across a

range of key indicators structured around three pillars:

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 6

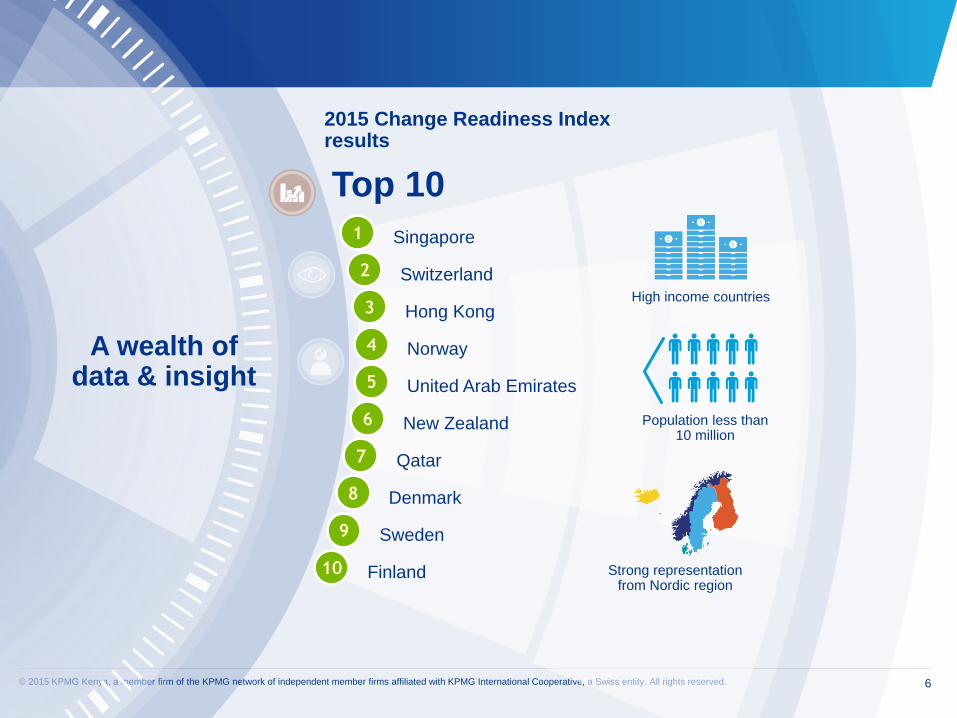

2015 Change Readiness Index results

Top 10

High income countries

Population less than 10 million

Strong representation from Nordic region

1 Singapore

2 Switzerland

3 Hong Kong

4 Norway

5 United Arab Emirates

6 New Zealand

7 Qatar

8 Denmark

9 Sweden

10 Finland

A wealth of data & insight

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 7

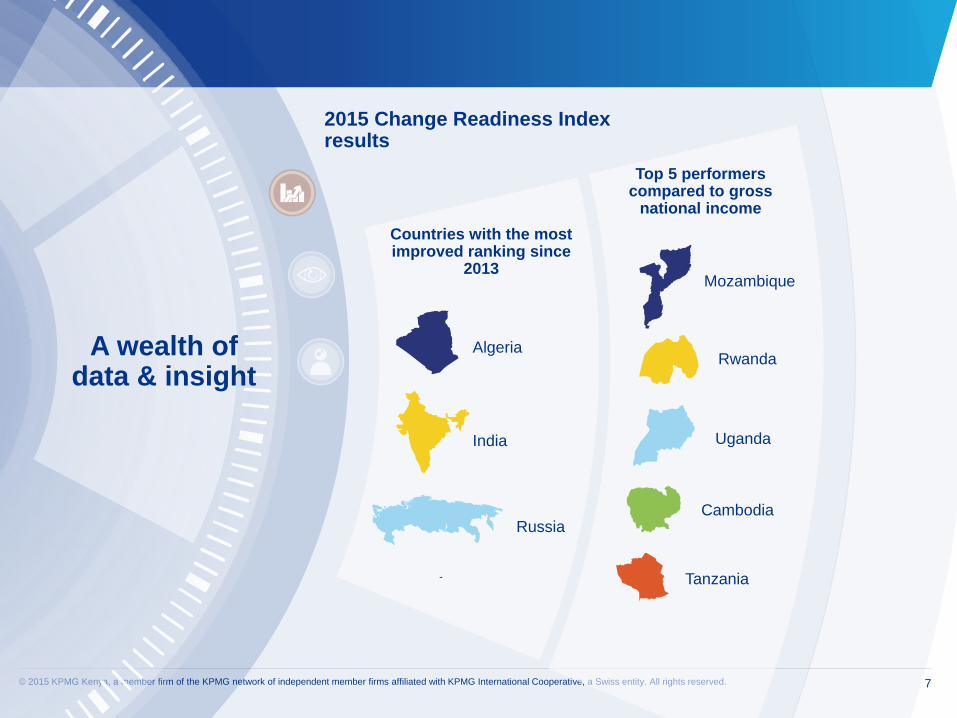

2015 Change Readiness Index results

Countries with the most improved ranking since

2013

Top 5 performers compared to gross

national income

Mozambique

Rwanda

Uganda

Cambodia

Tanzania

Algeria

India

Russia

A wealth of data & insight

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 8

Lovelock: Out of the building site……

…….comes something beautiful

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 9

We are creating the future

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 10

What differentiates humans is the ability to innovate

‘Never doubt that a small group of thoughtful, committed citizens can change

the world. Indeed, it is the only thing that ever has.’

Margaret Mead (cultural anthropologist)

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 11

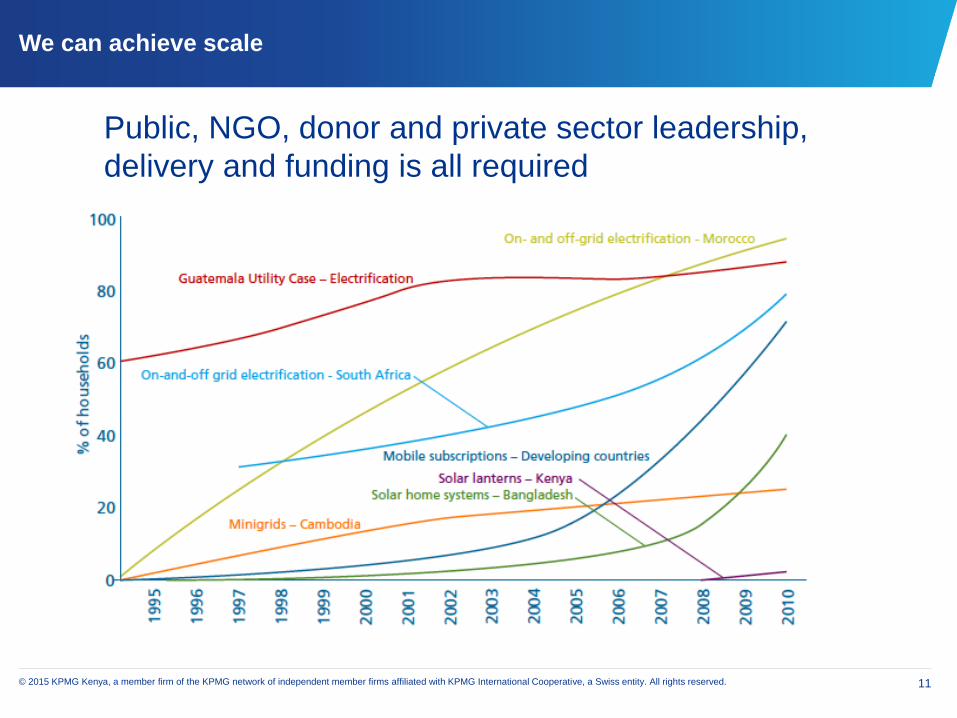

We can achieve scale

Public, NGO, donor and private sector leadership,

delivery and funding is all required

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 12

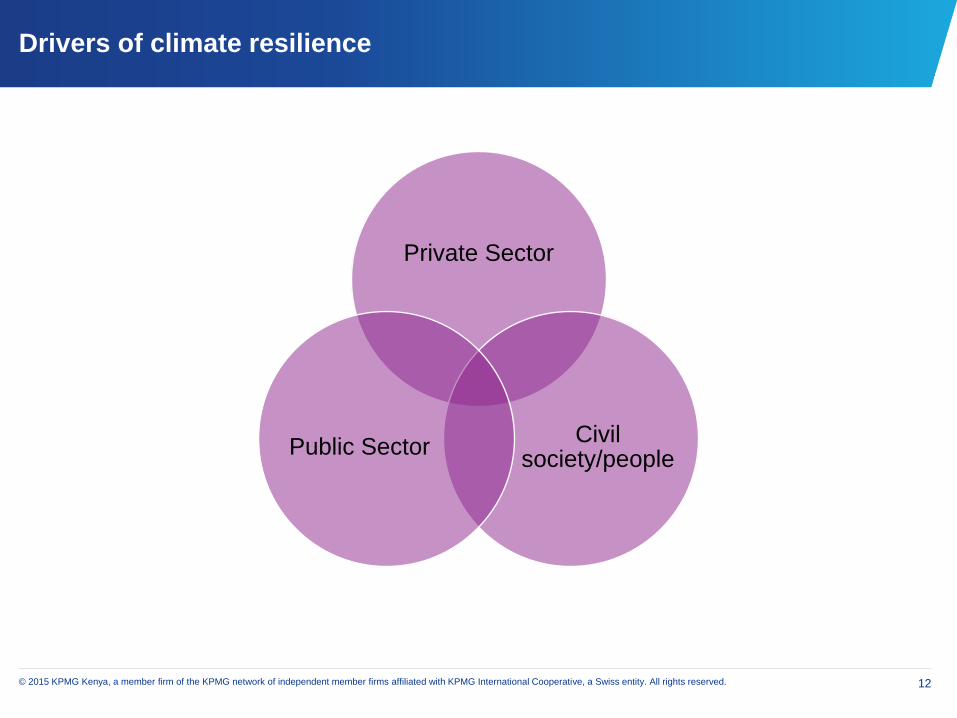

Drivers of climate resilience

Private Sector

Civil society/people

Public Sector

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 13

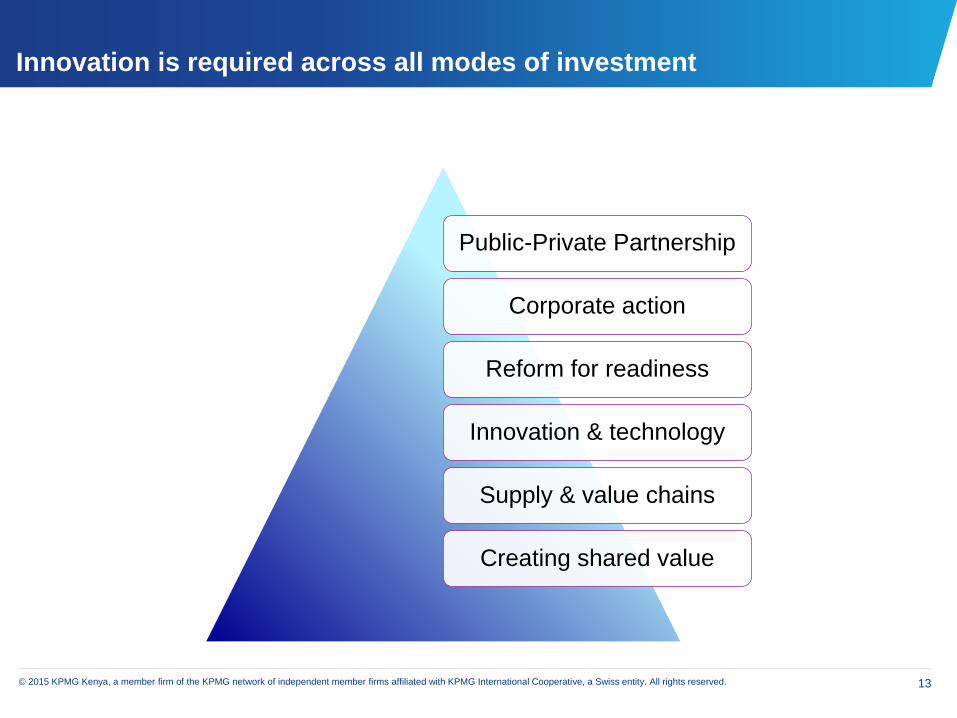

Innovation is required across all modes of investment

Public-Private Partnership

Corporate action

Reform for readiness

Innovation & technology

Supply & value chains

Creating shared value

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 14

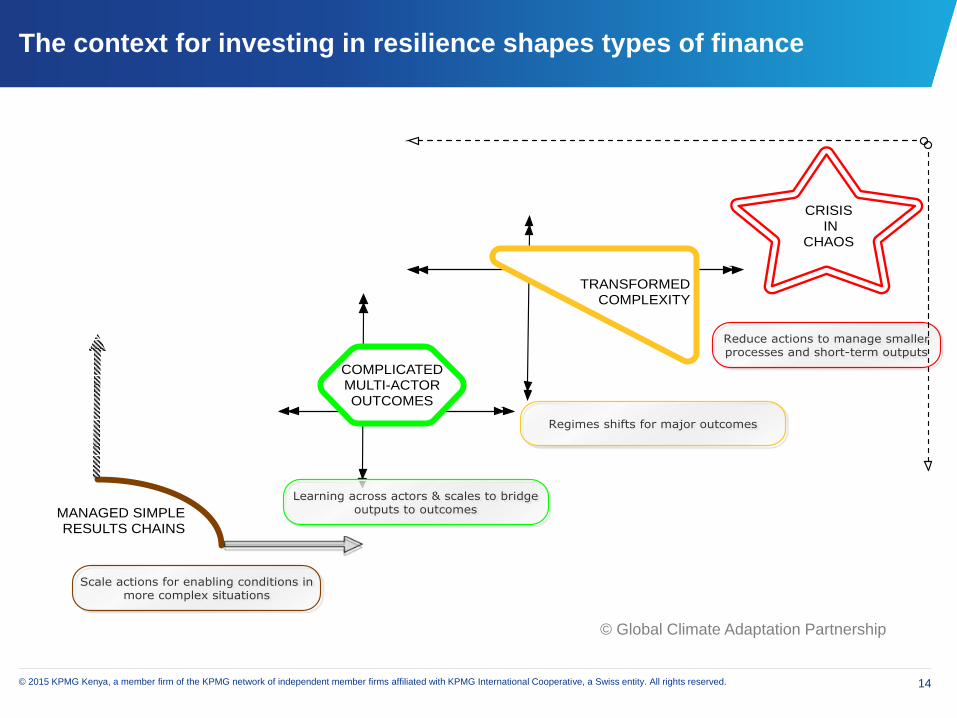

The context for investing in resilience shapes types of finance

Reduce actions to manage smaller processes and short-term outputs

MANAGED SIMPLE RESULTS CHAINS

TRANSFORMED COMPLEXITY

CRISIS IN

CHAOS

COMPLICATED MULTI-ACTOR OUTCOMES

Regimes shifts for major outcomes

Learning across actors & scales to bridge outputs to outcomes

Scale actions for enabling conditions in more complex situations

MLE ARCHETYPESFour situations guide project design and choice of instruments for monitoring, learning and evaluation (MLE).

© Global Climate Adaptation Partnership

Scaling up impact:

A fund manager’s

perspective

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 16

500m climate

portfolio within

IDAS Africa

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 17

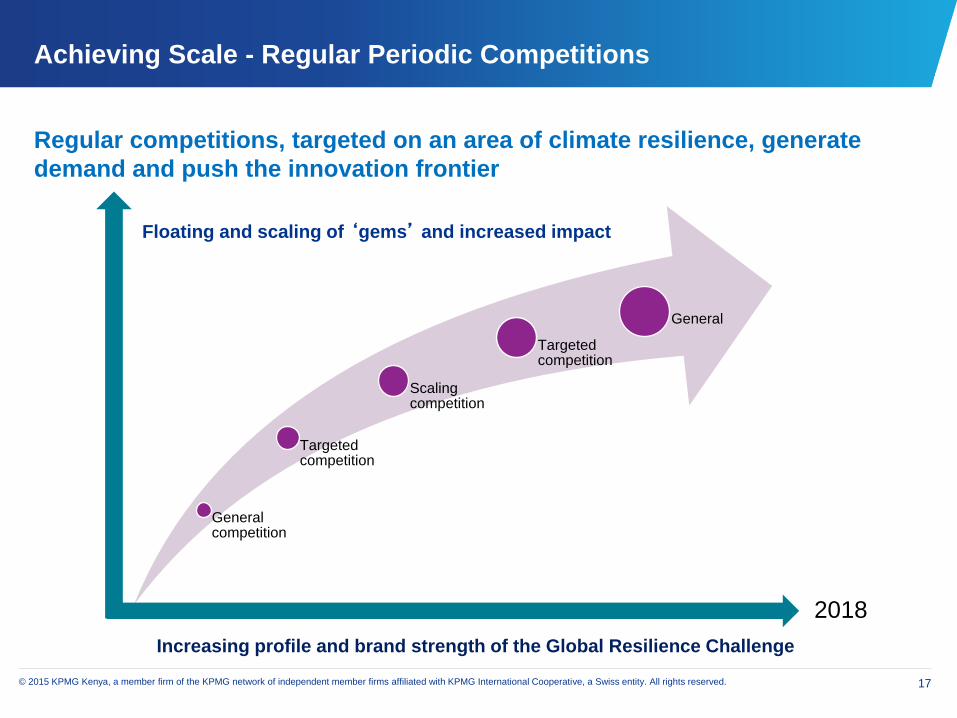

Achieving Scale - Regular Periodic Competitions

Floating and scaling of ‘gems’ and increased impact

General competition

Targeted competition

Scaling competition

Targeted competition

General

Increasing profile and brand strength of the Global Resilience Challenge

2018

Regular competitions, targeted on an area of climate resilience, generate

demand and push the innovation frontier

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 18

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

G

R

M

i

s

c

o

m

G

R

M

i

s

c

o

G

R

M

i

s

c

o

m

G

R

M

i

s

c

o

G

R

M

i

s

c

o

m

G

R

M

i

s

c

o

m

m

i

t

t

e

c

o

n

ti

n

ui

n

g

it

s

c

ol

la

is

c

o

m

m

it

te

d

t

o

c

o

n

ti

n

ui

G

R

M

i

s

c

o

m

G

R

M

i

s

c

o

m

m

i

s

c

o

m

m

i

t

t

e

i

s

c

o

m

m

i

t

t

i

s

c

o

m

m

i

t

t

e

i

s

c

o

m

m

i

t

t

i

s

c

o

m

m

i

t

t

i

s

c

o

m

m

i

t

t

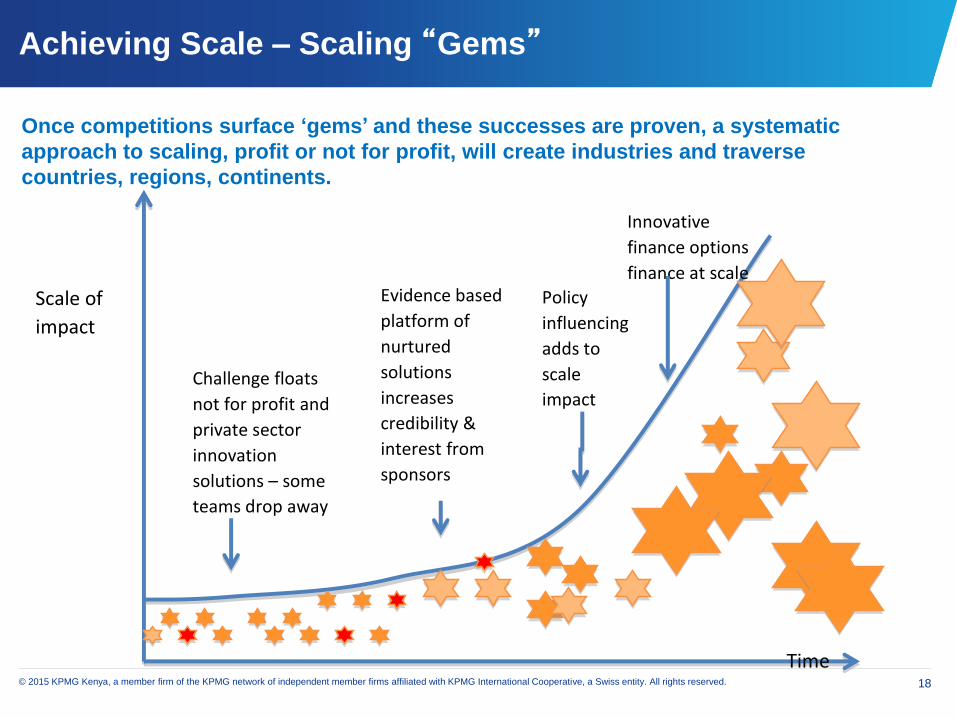

Time

Scale of

impact

Innovative

finance options

finance at scale

Challenge floats

not for profit and

private sector

innovation

solutions – some

teams drop away

Evidence based

platform of

nurtured

solutions

increases

credibility &

interest from

sponsors

Policy

influencing

adds to

scale

impact

Once competitions surface ‘gems’ and these successes are proven, a systematic

approach to scaling, profit or not for profit, will create industries and traverse

countries, regions, continents.

Achieving Scale – Scaling “Gems”

© 2015 KPMG Kenya, a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved. 19

We seek to create industries

20

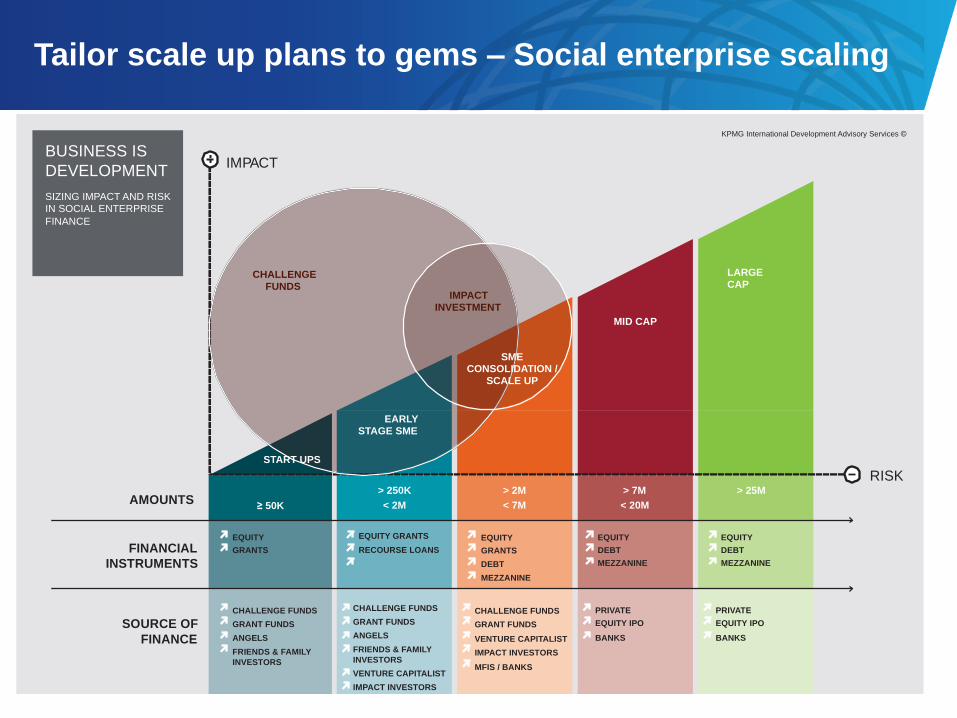

Tailor scale up plans to gems – Social enterprise scaling

BUSINESS IS

DEVELOPMENT

SIZING IMPACT AND RISK

IN SOCIAL ENTERPRISE

FINANCE

FINANCIAL

INSTRUMENTS

SOURCE OF

FINANCE

EQUITY

GRANTS

CHALLENGE FUNDS

GRANT FUNDS

ANGELS

FRIENDS & FAMILY

INVESTORS

CHALLENGE FUNDS

GRANT FUNDS

ANGELS

FRIENDS & FAMILY

INVESTORS

VENTURE CAPITALIST

IMPACT INVESTORS

CHALLENGE FUNDS

GRANT FUNDS

VENTURE CAPITALIST

IMPACT INVESTORS

MFIS / BANKS

PRIVATE

EQUITY IPO

BANKS

PRIVATE

EQUITY IPO

BANKS

EQUITY GRANTS

RECOURSE LOANS

EQUITY

GRANTS

DEBT

MEZZANINE

EQUITY

DEBT

MEZZANINE

EQUITY

DEBT

MEZZANINE

> 25M > 7M

< 20M

> 2M

< 7M

> 250K

< 2M ≥ 50K AMOUNTS

IMPACT

START UPS

RISK

CHALLENGE

FUNDS

MID CAP

EARLY STAGE SME

LARGE

CAP IMPACT

INVESTMENT

SME CONSOLIDATION /

SCALE UP

KPMG International Development Advisory Services ©

fGAIA

21

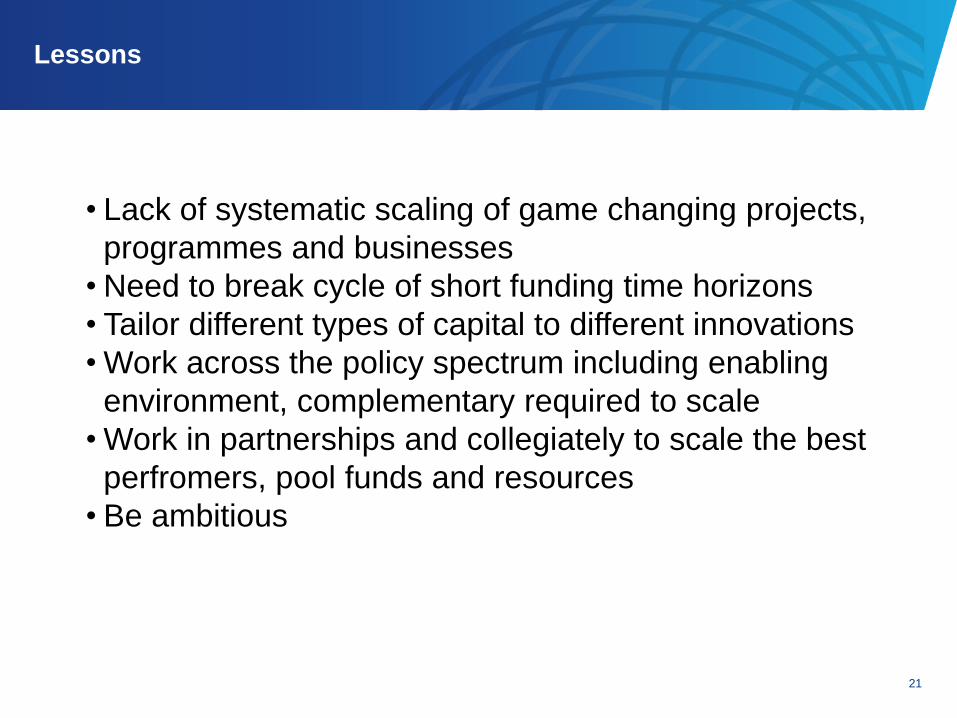

Lessons

• Lack of systematic scaling of game changing projects,

programmes and businesses

• Need to break cycle of short funding time horizons

• Tailor different types of capital to different innovations

• Work across the policy spectrum including enabling

environment, complementary required to scale

• Work in partnerships and collegiately to scale the best

perfromers, pool funds and resources

• Be ambitious

Top Related