Languages

Pages

Legal

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi

DOHA SIMPLIFIED COP18 SUMMARY & ANALYSISPublished by: Climate Connect Limited, 11 December 2012California | London | Melbourne | New DelhiUNFCCC Accredited Online Media for Doha COP 18, Qatar

INDIA PAT Scheme

477 industrial units coveredINDIA

REC Scheme45,600 MW

(expected by 2020)

NEW ZEALAND Emissions Trading

$351 million in 2011

VOLUNTARY CARBON MARKET

Emissions Trading$569 million in 2011

SOUTH KOREA Emissions Trading(498 companies)

SOUTH AFRICA Carbon Tax

KAZAKHSTAN Emissions Trading(178 companies)

VIETNAM Emissions Trading

THAILANDEmissions Trading

CHINAPilot Emissions Trading

$7 billion per year(estimated)

JAPANJoint Credit Mechanism

CALIFORNIAEmissions Trading

$1.8 billion(estimated) CERTAINTY

CDM(For projects

registered up to 31 Dec’12 & from LDCs)

AUSTRALIACarbon Tax

$9.25 billion per year(estimated)

NAMAs

CERTAINTY METER FOR GLOBAL CLIMATE MARKETS

USAFederal Climate Policy

GREEN CLIMATE FUNDClimate Finance

INTERIM FINANCE

AVIATION TRADINGEmissions Trading

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com | @Climate_Connect

Dear friends,

Another round of climate talks were concluded in Doha, Qatar last Friday, and the team from Climate Connect covered all 14 days of the action. The fundamental question for stakeholders remains – what are the opportunities in which we should invest our time and capital, and when? Despite the short-term uncertainty, I would like to make three points regarding the long-term future of the market, based on the outcomes from Doha and on my experience of a trader and then an entrepreneur in these markets.

New markets, new geographies, new skills

Europe is no longer the fulcrum of the global marketplace. New markets are developing across the world – in China, India, South Africa, Australia, etc. Participation in these new markets requires new skills, and a local presence in new geographies. I define climate markets as markets created by policy initiatives that aim to tackle climate change, as stated publicly, even if the actual drivers of change may be different.

Strong push to link/recognize regional markets between 2015-2020

What was surprising at Doha was that the countries were able to inch towards a long-term deal despite there not being much money on the table! This shows a strong desire, ostensibly driven by domestic priorities, to solve the climate problem. It is hence highly likely that – subject to the recovery of the global economy – a global market will emerge under a UN legal framework, which will consist of interlinked and bilaterally-recognised schemes.

It’s no longer just about “Carbon”

Loss and damage insurance, green infrastructure, sustainable development, amongst others, are the new buzzwords in the climate market. The market’s understanding and definition of mitigation and adaptation activities has certainly broadened. Carbon is emerging as a common tool of measurement across various new schemes driven by developmental and energy security factors. Happy reading!

Nitin Tanwar*[email protected]

*The author is the Founder & CEO of Climate Connect, an alumnus of University of Cambridge

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi

UNCE

RTAI

NTY

TABLE OF CONTENTS

SEGMENT PAGE

Future Dates & Milestones 1

Summary of Major Decisions & their Potential Impacts

• Kyoto Protocol• CDM• NAMAs• New Market Mechanisms• REDD• Finance

2

Significant Developments 6

Climate Connect Exclusive Analytics

6

Country Statements & Positions 8

Climate Connect Exclusive Interviews

9

Doha COP18 Summary & Analysis

© Climate Connect Limited, 2012 London | New Delhi

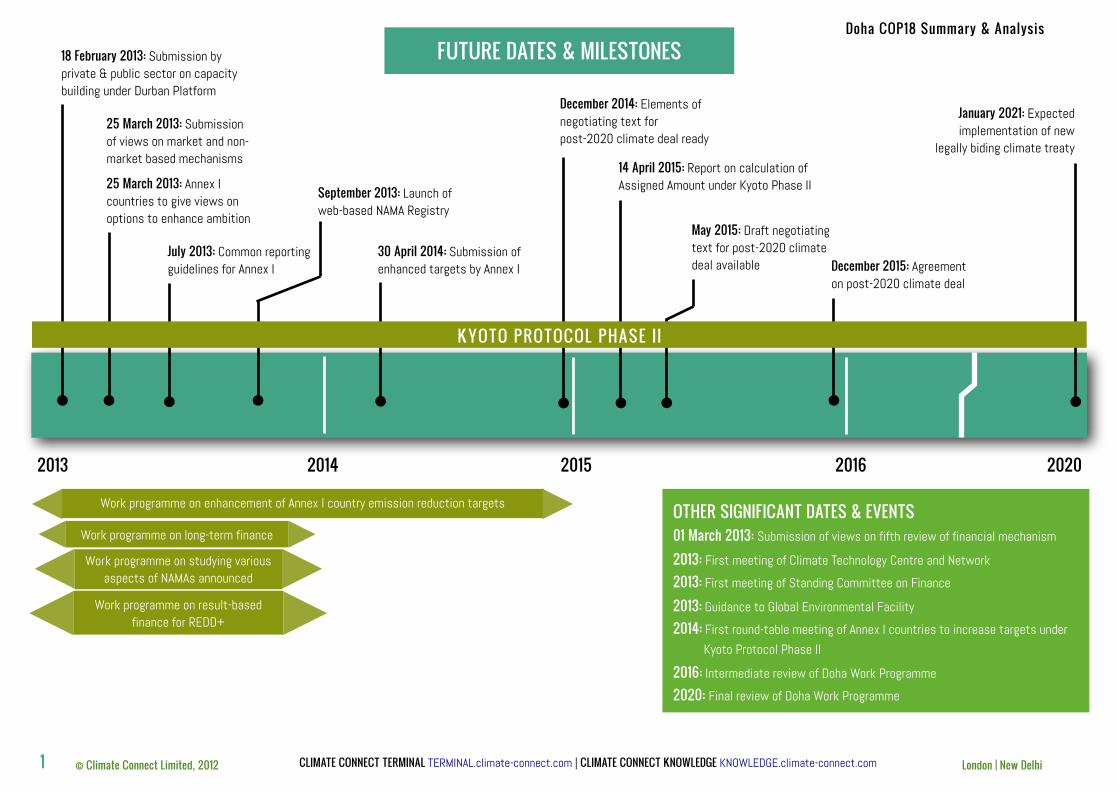

2013 2014 2015 2016 2020

25 March 2013: Annex I countries to give views on options to enhance ambition

December 2014: Elements of negotiating text for post-2020 climate deal ready

May 2015: Draft negotiating text for post-2020 climate deal available December 2015: Agreement

on post-2020 climate deal

25 March 2013: Submission of views on market and non-market based mechanisms

18 February 2013: Submission by private & public sector on capacity building under Durban Platform

OTHER SIGNIFICANT DATES & EVENTS01 March 2013: Submission of views on fifth review of financial mechanism

2013: First meeting of Climate Technology Centre and Network

2013: First meeting of Standing Committee on Finance

2013: Guidance to Global Environmental Facility

2014: First round-table meeting of Annex I countries to increase targets under Kyoto Protocol Phase II

2016: Intermediate review of Doha Work Programme

2020: Final review of Doha Work Programme

September 2013: Launch of web-based NAMA Registry

July 2013: Common reporting guidelines for Annex I

30 April 2014: Submission of enhanced targets by Annex I

14 April 2015: Report on calculation of Assigned Amount under Kyoto Phase II

January 2021: Expected implementation of new

legally biding climate treaty

KYOTO PROTOCOL PHASE II

FUTURE DATES & MILESTONES

1

Work programme on enhancement of Annex I country emission reduction targets

Work programme on long-term finance

Work programme on studying various aspects of NAMAs announced

Work programme on result-based finance for REDD+

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

2

SUMMARY OF MAJOR DECISIONS & THEIR POTENTIAL IMPACTS

KYOTO PROTOCOL

Only Annex I parties (mainly Australia, EU) with targets under KPII allowed to use CERs, AAUs, ERUs after 31 December 2012

Phase II agreed & duration to be between 01 January 2013 to 31 December 2020

Australia, EU, Japan, Liechtenstein, Monaco, Norway & Switzerland will not use Phase I AAUs to meet Phase II emission reduction

targets

• Annex I countries to maintain surplus reserve for unused Phase I AAUs in their national registries

• Phase I AAUs can only be used in case the Phase II emissions exceed the assigned amount of Phase II

• Parties can traded maximum of 2% of unused Phase I AAUs amongst themselves

• Positive difference between assigned amount and average annual emissions of first three years of Phase II shall be transferred into cancellation account of the Party

• Parties to submit views by 15 April 2015 on how their assigned amounts be calculated

• About 13 billion surplus AAUs from Phase I may remain unused, which could potentially drive demand for other Kyoto instruments

• EU, Australia, Norway & Switzerland pledge to reduce at least 785 million tonnes between 2013 and 2020

• Can raise emission reduction targets to pledge reduction of up to 1,422 million tonnes by 2020

ENHANCING TARGETS UNDER KYOTO PHASE II

• Annex I countries to review emission reduction targets up to 2020 in 2014

• Revision of targets with an aim to reducing Annex I countries’ emissions by 25-40% by 2020 from 1990 levels

• Annex I countries to report any increase in target by 30 April 2014

• Long-term fungibility between emerging markets like China, South Korea, Chile, Vietnam and CDM possible

• Review of validation procedure could impact small-scale projects including several renewable energy projects

• About 480 million CERs from industrial gas projects may remain unused as they have been banned by EU, Australia, New Zealand

• About 7 million non-banned CERs likely to be carried over into Phase II

CLEAN DEVELOPMENT MECHANISM

EB asked to explore possibility of reviewing validation of CDM projects automatically deemed additional

• Parties with no Kyoto Phase II target will not be allowed to use CERs from 01 January 2013

• Only 2.5% of Phase I CERs allowed to be carried over into Phase II of Kyoto Protocol

EB to work closely with countries developing domestic carbon markets specifically with

regard to MRV activities

Parties encouraged to set up stabilisation funds

CDM projects recognised under Kyoto Protocol Phase II;Annex I countries can continue to invest in CDM projects

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi3

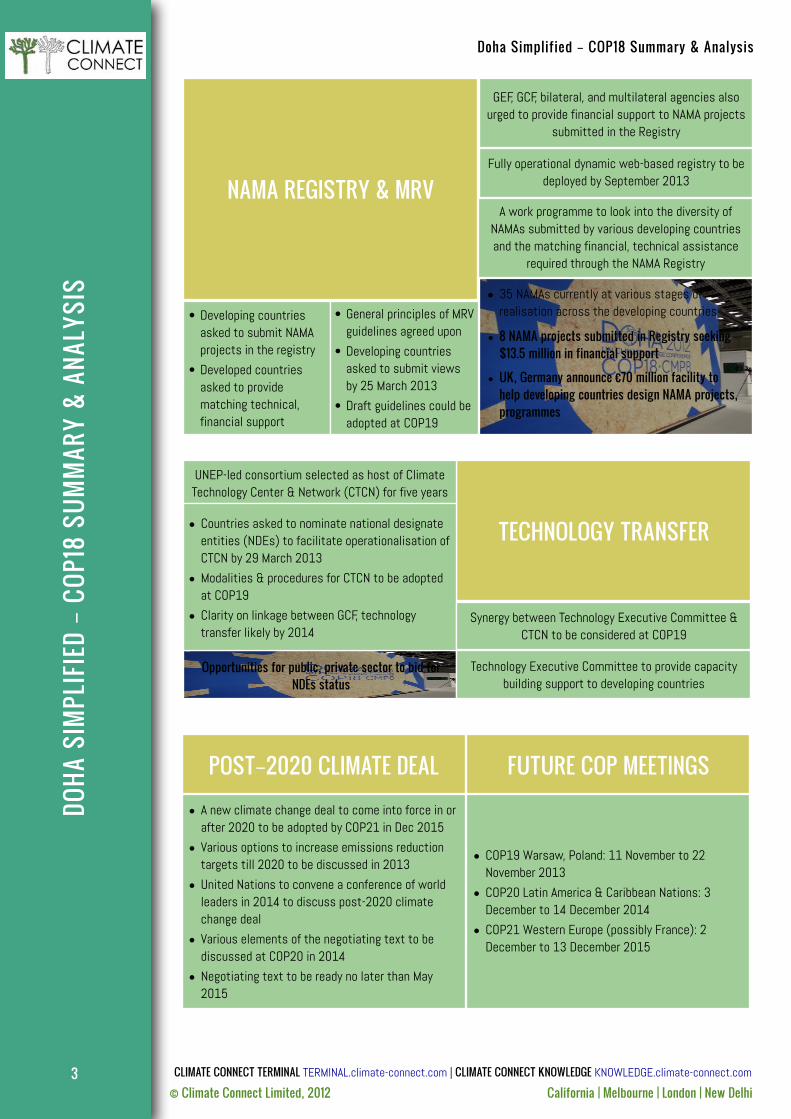

TECHNOLOGY TRANSFER

UNEP-led consortium selected as host of Climate Technology Center & Network (CTCN) for five years

• Countries asked to nominate national designate entities (NDEs) to facilitate operationalisation of CTCN by 29 March 2013

• Modalities & procedures for CTCN to be adopted at COP19

• Clarity on linkage between GCF, technology transfer likely by 2014

Opportunities for public, private sector to bid for NDEs status

Synergy between Technology Executive Committee & CTCN to be considered at COP19

Technology Executive Committee to provide capacity building support to developing countries

NAMA REGISTRY & MRV

• Developing countries asked to submit NAMA projects in the registry

• Developed countries asked to provide matching technical, financial support

• 35 NAMAs currently at various stages of realisation across the developing countries

• 8 NAMA projects submitted in Registry seeking $13.5 million in financial support

• UK, Germany announce €70 million facility to help developing countries design NAMA projects, programmes

• General principles of MRV guidelines agreed upon

• Developing countries asked to submit views by 25 March 2013

• Draft guidelines could be adopted at COP19

Fully operational dynamic web-based registry to be deployed by September 2013

GEF, GCF, bilateral, and multilateral agencies also urged to provide financial support to NAMA projects

submitted in the Registry

A work programme to look into the diversity of NAMAs submitted by various developing countries and the matching financial, technical assistance

required through the NAMA Registry

POST–2020 CLIMATE DEAL

• A new climate change deal to come into force in or after 2020 to be adopted by COP21 in Dec 2015

• Various options to increase emissions reduction targets till 2020 to be discussed in 2013

• United Nations to convene a conference of world leaders in 2014 to discuss post-2020 climate change deal

• Various elements of the negotiating text to be discussed at COP20 in 2014

• Negotiating text to be ready no later than May 2015

FUTURE COP MEETINGS

• COP19 Warsaw, Poland: 11 November to 22 November 2013

• COP20 Latin America & Caribbean Nations: 3 December to 14 December 2014

• COP21 Western Europe (possibly France): 2 December to 13 December 2015

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi

NEW DOMESTIC MECHANISMS

• Work programme to consider following points: - NMM to work under COP- Participation will be voluntary- Permanent emission reduction with no

double-counting - Accurate MRV- Supplementarity

• Draft decision on this framework expected at COP19

• Parties to submit views by 25 March 2013

• Use of carbon instruments from NMMs in emerging markets for KP II compliance was discussed but not approved at COP18

• Linkage of NMMs with Kyoto compliance unlikely before 2014–2015

• New work programme to be implemented in 2013 to set up a framework for various domestic schemes (market-based and non-market-based)

• Draft decision on this framework addressing issues like environmental integrity and avoiding double-counting, and is expected at COP19

• Parties to submit views by 25 March 2013

REDD & FORESTRY SECTOR

• Work programme on results-based finance in 2013 • Aim to improve and increase finance for REDD

activities, and to incentivise non-carbon benefits

• Work programme may end by COP19

• Process to address issues such as the provision of financial and technical support for developing countries in the forestry sector

• Parties invited to submit views on the modalities of financial and technical support by 25 March 2013

• Possible increased scrutiny of progress of Annex I countries in achieving their mitigation targets with inter-country comparisons

• Increased scrutiny of NAMAs may enable fungibility in medium to long-term

• Analysis of financial, technical assistance required may expedite transfer of finance, technology

EMISSIONS REPORTING BY ANNEX I COUNTRIES

• Emissions to be reported in a common tabular format through Biennial Update Reports (BURs)

• BURs to include:

- Emissions from aviation, shipping sectors

- Progress made to achieve 2020 targets (voluntary and legally binding)

- Non-Kyoto instruments used

- Estimated emissions by 2030

- Details of climate finance contributions from public sources to developing countries

EMISSIONS REPORTING BY NON–ANNEX I COUNTRIES

• Consultative Group of Experts overlooking BURs to be expanded

• GEF asked to provide financial support to developing countries for preparing BURs

• Team of Technical Experts to provide analysis of BURs from non-Annex I countries estimated emissions by 2030

• Team of Technical Experts to provide analysis of BURs from non-Annex I countries

4

EDUCATION ON CLIMATE CHANGE

• An 8-year work programme, focused on education, training and skills development on climate change mitigation and adaptation, to be started by all countries

• Named Doha Work Programme, first review in 2016

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi

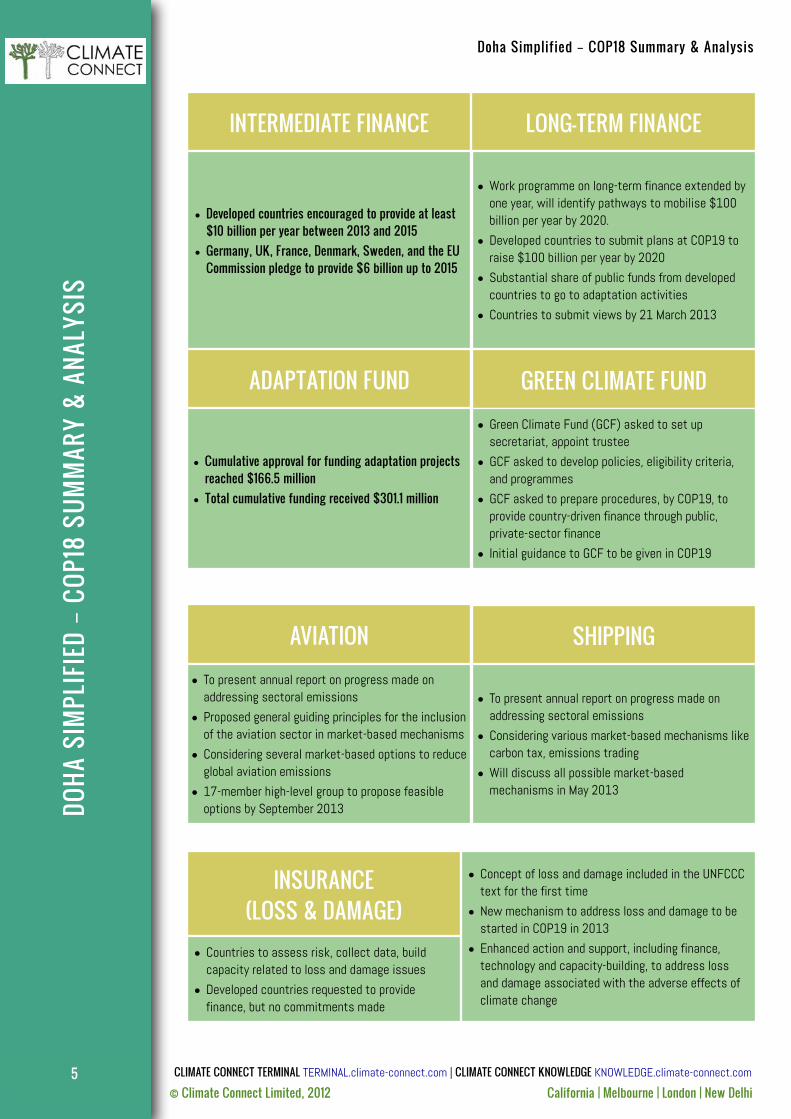

LONG-TERM FINANCE

• Developed countries encouraged to provide at least $10 billion per year between 2013 and 2015

• Germany, UK, France, Denmark, Sweden, and the EU Commission pledge to provide $6 billion up to 2015

• Work programme on long-term finance extended by one year, will identify pathways to mobilise $100 billion per year by 2020.

• Developed countries to submit plans at COP19 to raise $100 billion per year by 2020

• Substantial share of public funds from developed countries to go to adaptation activities

• Countries to submit views by 21 March 2013

INTERMEDIATE FINANCE

GREEN CLIMATE FUND

• Green Climate Fund (GCF) asked to set up secretariat, appoint trustee

• GCF asked to develop policies, eligibility criteria, and programmes

• GCF asked to prepare procedures, by COP19, to provide country-driven finance through public, private-sector finance

• Initial guidance to GCF to be given in COP19

ADAPTATION FUND

• Cumulative approval for funding adaptation projects reached $166.5 million

• Total cumulative funding received $301.1 million

INSURANCE(LOSS & DAMAGE)

• Concept of loss and damage included in the UNFCCC text for the first time

• New mechanism to address loss and damage to be started in COP19 in 2013

• Enhanced action and support, including finance, technology and capacity-building, to address loss and damage associated with the adverse effects of climate change

• Countries to assess risk, collect data, build capacity related to loss and damage issues

• Developed countries requested to provide finance, but no commitments made

5

SHIPPING

• To present annual report on progress made on addressing sectoral emissions

• Considering various market-based mechanisms like carbon tax, emissions trading

• Will discuss all possible market-based mechanisms in May 2013

AVIATION

• To present annual report on progress made on addressing sectoral emissions

• Proposed general guiding principles for the inclusion of the aviation sector in market-based mechanisms

• Considering several market-based options to reduce global aviation emissions

• 17-member high-level group to propose feasible options by September 2013DO

HA S

IMPL

IFIE

D –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi6

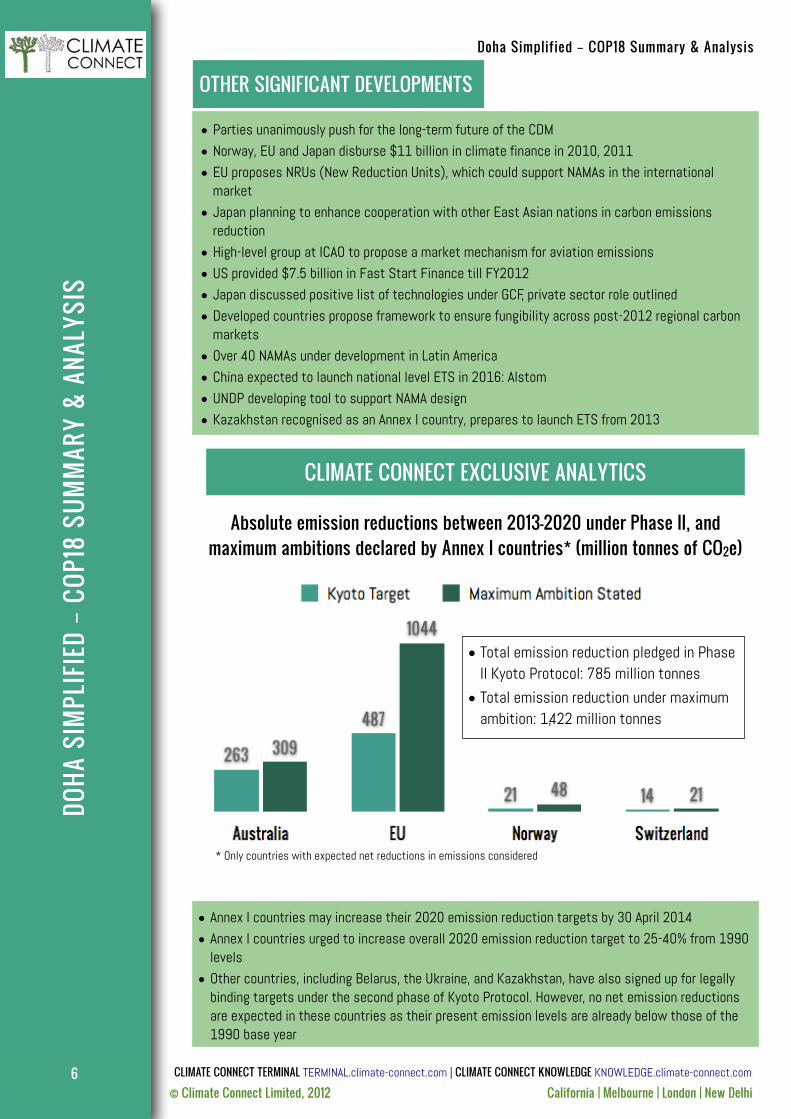

OTHER SIGNIFICANT DEVELOPMENTS

• Parties unanimously push for the long-term future of the CDM• Norway, EU and Japan disburse $11 billion in climate finance in 2010, 2011• EU proposes NRUs (New Reduction Units), which could support NAMAs in the international

market • Japan planning to enhance cooperation with other East Asian nations in carbon emissions

reduction• High-level group at ICAO to propose a market mechanism for aviation emissions• US provided $7.5 billion in Fast Start Finance till FY2012• Japan discussed positive list of technologies under GCF, private sector role outlined • Developed countries propose framework to ensure fungibility across post-2012 regional carbon

markets• Over 40 NAMAs under development in Latin America• China expected to launch national level ETS in 2016: Alstom• UNDP developing tool to support NAMA design• Kazakhstan recognised as an Annex I country, prepares to launch ETS from 2013

Absolute emission reductions between 2013-2020 under Phase II, and maximum ambitions declared by Annex I countries* (million tonnes of CO2e)

* Only countries with expected net reductions in emissions considered

• Total emission reduction pledged in Phase II Kyoto Protocol: 785 million tonnes

• Total emission reduction under maximum ambition: 1,422 million tonnes

• Annex I countries may increase their 2020 emission reduction targets by 30 April 2014• Annex I countries urged to increase overall 2020 emission reduction target to 25-40% from 1990

levels • Other countries, including Belarus, the Ukraine, and Kazakhstan, have also signed up for legally

binding targets under the second phase of Kyoto Protocol. However, no net emission reductions are expected in these countries as their present emission levels are already below those of the 1990 base year

CLIMATE CONNECT EXCLUSIVE ANALYTICS

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi7

Emission reduction potential by 2020, under NAMAs announced by developing countries* (million tonnes of CO2e)

TARGETS BY DEVELOPING COUNTRIES• Brazil: Up to 38.9% emission reduction from BAU through forestry,

clean energy, energy efficiency• Indonesia: 26% emission reduction from BAU through forestry

• South Africa: 34% emission reduction from BAU through carbon tax, clean energy

• South Korea: 30% emission reduction from BAU through emissions trading

• India: 20-25% carbon intensity reduction from 2005 levels through clean energy, energy efficiency

• China: 40-45% carbon intensity reduction from 2005 levels through emissions trading, clean energy, energy, energy efficiency

Total mitigation pledged: over 2.64 billion tonnes

* Only countries with quantified emission reduction targets under NAMAs considered

New climate funding announced at Doha COP18

• REDD: Norway, UN-REDD Programme to help Vietnam implement the second phase of UN-REDD National Programme

• NAMAs: Germany, UK to assist developing countries design and implement NAMA projects

• Interim Finance till 2015: No details of activities shared, Annex I countries likely to continue along the lines of Fast Start Finance

• National Communications: Increased support by Global Environmental Facility (GEF) to help developing countries prepare national communications, biennial update reports

• Africa, Uganda: UK to assist in clean energy projects in African countries

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi8

CLIMATE CHANGE NEGOTIATIONS• Intermediate finance is critical until Green

Climate Fund becomes operational is critical

• Against the increasing of voluntary target to reduce emission intensity

• Wants focus to shift to Durban Platform

DOMESTIC CARBON MARKET• Has launched trading of credits generated from

Bamboo Afforestation

• Expects some provinces to hit emissions peak by 2020

• Announced 29 new low-carbon pilot areas

• Carbon intensity expected to fall 5% in 2012, above annual average target of 3.5%

CHINA

CLIMATE CHANGE NEGOTIATIONS• Among the first countries to submit target under

Kyoto Phase II

• Target under Kyoto Phase II matches national target

• Possibility of increasing the target remains subject to certain conditions

• Announced that it will not use Phase I AAUs to meet Kyoto Phase II targets

DOMESTIC CARBON MARKET• Showcased Savanna Burning Methodology

recently approved under the Carbon Farming Initiative

AUSTRALIA

COUNTRY STATEMENTS & POSITIONS

CLIMATE CHANGE NEGOTIATIONS• Reiterated opposition to accept targets under

Phase II of Kyoto Protocol

• Announced that it will not use Phase I AAUs

DOMESTIC CARBON MARKET• Renamed the Bilateral Offset Credit Mechanism

(BOCM) as Joint Credit Mechanism (JCM)

• Announced bilateral deals with Mongolia, Vietnam under JCM

• Not looking to consume credits generated from projects under JCM; to focus on MRV, mitigation

• Other countries free to purchase credits from projects under JCM

UNITED STATES OF AMERICAJAPAN

CLIMATE CHANGE NEGOTIATIONS• Wants consistent approach towards next legally

binding treaty through Durban Platform

• Pledged to continue to provide climate finance but refused to give any commitment

• Stated that many developed countries were not in position to commit to emission reduction targets due to several reasons that include economic slowdown

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi9

Representatives from Tianjin Climate Exchange (TCX)

• Major sectors covered: Metals, Chemicals, Power & Heat Supply, Oil & Gas Exploration, Petrochemicals

• Emissions trading training for companies, with the scheme to be launched in 2013

• Integration with national carbon market by 2015

TIANJIN (CHINA) PILOT ETS Click here to watch video

Mr Alex Gosman, CEO of Australian Industry Greenhouse Network (AIGN)

Major priorities for Australian industries

• Effective implementation of carbon tax

• Removal of programmes that are not market-based

• Effective and sufficient financial assistance to the industry, particularly the manufacturing sector

AUSTRALIA CARBON MARKET Click here to watch video

Yoon-Gih Ahn, PhD, Group Leader, Steel Strategy Research Center, POSCO Research

Institute, Seoul, South Korea• South Korea ETS to be launched in 2015

• Companies given 6-7% emissions reduction targets, which will be increased in the future

• Compliance fine to be 3 times the market price of carbon with a maximum penalty of $100

SOUTH KOREA ETS Click here to watch video

CLIMATE CONNECT EXCLUSIVE INTERVIEWS

Nitin Tanwar, Director, Climate Connect LimitedJeff Swartz, International Policy Director, IETA

• Climate Connect, IETA launched a survey to gauge expectations of stakeholders

• 55% of respondents expect new climate deal to be agreed upon by 2015

• Stakeholders are eyeing new markets, with over 50% looking to invest in Africa, China, and India

CLIMATE CONNECT, IETA DOHA SURVEY Click here to watch video

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Doha Simplified – COP18 Summary & Analysis

© Climate Connect Limited, 2012 California | Melbourne | London | New Delhi10

Connie Hedegaard, EU Commissioner for Climate Action

• Doha outcome not revolutionary but a way forward; expect progress on increasing ambition in future

• Countries like Russia dissatisfied with decision on surplus AAUs, but carry-over would have cast doubts on environmental integrity

• Hard work ahead for securing 2015 climate deal

DOHA COP18 OUTCOME Click here to watch video

Dirk Forrester, President & CEO, IETA

• Markets were the focus during Doha COP; inclusion of NMMs in final text signals upcoming opportunities

• Doha outcome a good starting point for New Market Mechanisms (NMMs)

• UN Secretary General likely to push for increased ambitions and a 2015 climate deal

DOHA COP18 OUTCOME Click here to watch video

DOHA

SIM

PLIF

IED –

COP1

8 SU

MM

ARY

& AN

ALYS

IS

About Us: Climate Connect, founded in May 2010, is a news, data and Knowledge Process Outsourcing (KPO) company specialising in new age environmental markets. Email: [email protected]

Team Background @ Climate Connect

Disclaimer:Climate Connect Ltd has taken due care and caution in compilation and reporting of data as has been obtained from various sources including which it considers reliable and first hand. However, Climate Connect Ltd does not guarantee the accuracy, adequacy or completeness of any information and it not responsible for errors or omissions or for the results obtained from the use of such information and especially states that it has no financial liability whatsoever to the users of this report. This research and information does not constitute recommendation or advice for trading or investment purposes and therefore Climate Connect Ltd will not be liable for any loss accrued as a result of a trading/investment activity that is undertaken on the basis of information contained in this report. Climate Connect Ltd does not consider itself to undertake Regulated Activities as defined in Section 22 of the Financial Services and Markets Act 2000 and it is not registered with the Financial Services Authority of the UK.

EU Commissioner for Climate Action acknowledges Climate Connect’s Doha coverage!

Website: 1000s visits per day

Over 50 article published on Doha COP

Tweets: 20 per day

Daily Summary of Major Developments

CLIMATE CONNECT TERMINAL TERMINAL.climate-connect.com | CLIMATE CONNECT KNOWLEDGE KNOWLEDGE.climate-connect.com

Top Related