Languages

Pages

Legal

Do Board Contacts Matter? An analysis of the relationship between boards of directors’ ties and the performance of Australia’s largest companies.

Thesis submitted in partial fulfilment of the degree of Master of Business (Research)

Kevin J. Smith School of Accountancy

Faculty of Business Queensland University of Technology

2009

i

Keywords

corporate governance, boards of directors, directors, networks, social capital,

interlocks, resource dependence

ii

Abstract

Boards of directors are thought to provide access to a wealth of knowledge and

resources for the companies they serve, and are considered important to corporate

governance. Under the Resource Based View (RBV) of the firm (Wernerfelt, 1984)

boards are viewed as a strategic resource available to firms. As a consequence there has

been a significant research effort aimed at establishing a link between board attributes

and company performance. In this thesis I explore and extend the study of interlocking

directorships (Mizruchi, 1996; Scott 1991a) by examining the links between directors’

opportunity networks and firm performance. Specifically, I use resource dependence

theory (Pfeffer & Salancik, 1978) and social capital theory (Burt, 1980b; Coleman,

1988) as the basis for a new measure of a board’s opportunity network. I contend that

both directors’ formal company ties and their social ties determine a director’s

opportunity network through which they are able to access and mobilise resources for

their firms. This approach is based on recent studies that suggest the measurement of

interlocks at the director level, rather than at the firm level, may be a more reliable

indicator of this phenomenon.

This research uses publicly available data drawn from Australia’s top-105 listed

companies and their directors in 1999. I employ Social Network Analysis (SNA) (Scott,

1991b) using the UCINET software to analyse the individual director’s formal and

social networks. SNA is used to measure a the number of ties a director has to other

directors in the top-105 company director network at both one and two degrees of

separation, that is, direct ties and indirect (or ‘friend of a friend’) ties. These individual

measures of director connectedness are aggregated to produce a board-level network

metric for comparison with measures of a firm’s performance using multiple regression

analysis. Performance is measured with accounting-based and market-based measures.

Findings indicate that better-connected boards are associated with higher market-based

company performance (measured by Tobin’s q). However, weaker and mostly

unreliable associations were found for accounting-based performance measure ROA.

Furthermore, formal (or corporate) network ties are a stronger predictor of market

performance than total network ties (comprising social and corporate ties). Similarly,

iii

strong ties (connectedness at degree-1) are better predictors of performance than weak

ties (connectedness at degree-2).

My research makes four contributions to the literature on director interlocks. First, it

extends a new way of measuring a board’s opportunity network based on the director

rather than the company as the unit of interlock. Second, it establishes evidence of a

relationship between market-based measures of firm performance and the connectedness

of that firm’s board. Third, it establishes that director’s formal corporate ties matter

more to market-based firm performance than their social ties. Fourth, it establishes that

director’s strong direct ties are more important to market-based performance than weak

ties.

The thesis concludes with implications for research and practice, including a more

speculative interpretation of these results. In particular, I raise the possibility of reverse

causality – that is networked directors seek to join high-performing companies. Thus,

the relationship may be a result of symbolic action by companies seeking to increase the

legitimacy of their firms rather than a reflection of the social capital available to the

companies. This is an important consideration worthy of future investigation.

iv

Table of Contents KEYWORDS ......................................................................................................................................... I

ABSTRACT .......................................................................................................................................... II

LIST OF FIGURES ............................................................................................................................... VI

LIST OF TABLES ................................................................................................................................ VII

LIST OF APPENDICES ....................................................................................................................... VIII

STATEMENT OF ORIGINALITY............................................................................................................ IX

ACKNOWLEDGEMENTS ...................................................................................................................... X

CHAPTER 1 INTRODUCTION........................................................................................................... 1

1.1 BACKGROUND TO THE RESEARCH ..................................................................................................... 1 1.2 RESEARCH PROBLEM ..................................................................................................................... 2 1.3 JUSTIFICATION FOR THE RESEARCH ................................................................................................... 5 1.4 METHODOLOGY ........................................................................................................................... 6 1.5 OUTLINE OF THESIS ....................................................................................................................... 6 1.6 DEFINITIONS ................................................................................................................................ 7 1.7 DELIMITATIONS OF SCOPE AND KEY ASSUMPTIONS............................................................................... 9 1.8 CONCLUSION ............................................................................................................................. 10

CHAPTER 2 COMPANIES, BOARDS AND GOVERNANCE ................................................................ 12

2.1 INTRODUCTION .......................................................................................................................... 12 2.2 COMPANIES AND DIRECTORS’ LEGAL OBLIGATIONS ............................................................................ 12 2.3 CORPORATE GOVERNANCE AND THEORIES ....................................................................................... 15

2.3.1 Governance overview ................................................................................................... 15 2.3.2 Agency theory .............................................................................................................. 17 2.3.3 Stewardship theory ...................................................................................................... 20 2.3.4 Resource dependence theory ....................................................................................... 21 2.3.5 Resource based view of the firm .................................................................................. 22 2.3.6 Summary of key governance theories and their importance to this thesis .................. 23

2.4 BOARDS OF DIRECTORS - ROLES AND THEORIES ................................................................................. 24 2.4.1 Overview of board roles ............................................................................................... 24 2.4.2 Resource dependence role ........................................................................................... 26 2.4.3 Monitoring and control role ......................................................................................... 27 2.4.4 Service role ................................................................................................................... 28

2.5 THE STUDY OF BOARD STRUCTURE .................................................................................................. 28 2.5.1 Board size ..................................................................................................................... 29 2.5.2 Board independence .................................................................................................... 30 2.5.3 CEO duality ................................................................................................................... 32

2.6 CONCLUSION ............................................................................................................................. 33

CHAPTER 3 LITERATURE REVIEW & THEORETICAL DEVELOPMENT .............................................. 34

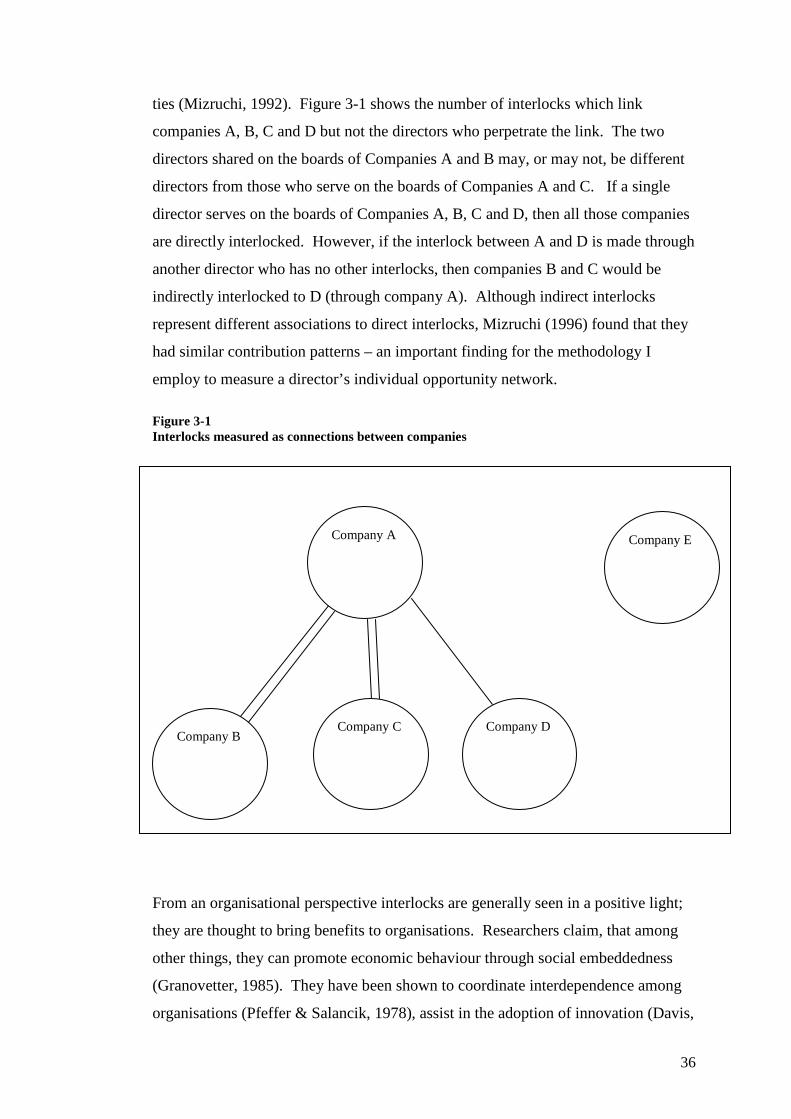

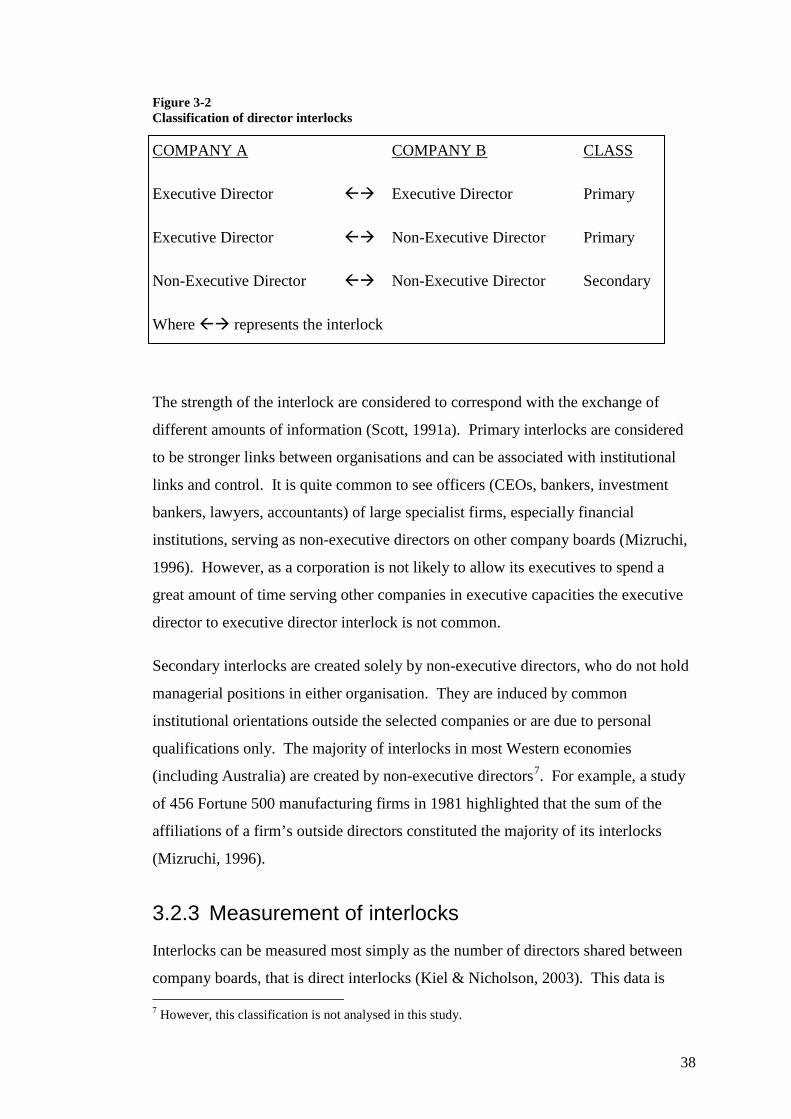

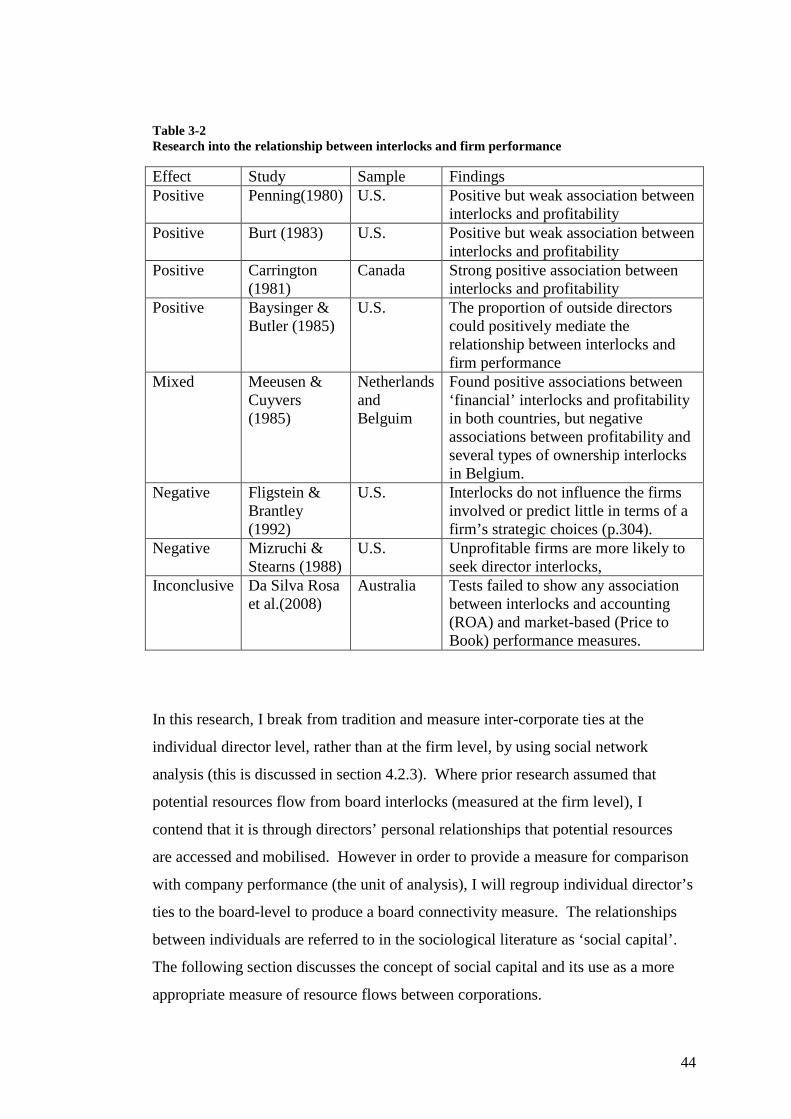

3.1 INTRODUCTION .......................................................................................................................... 34 3.2 DIRECTOR INTERLOCKS ................................................................................................................. 35

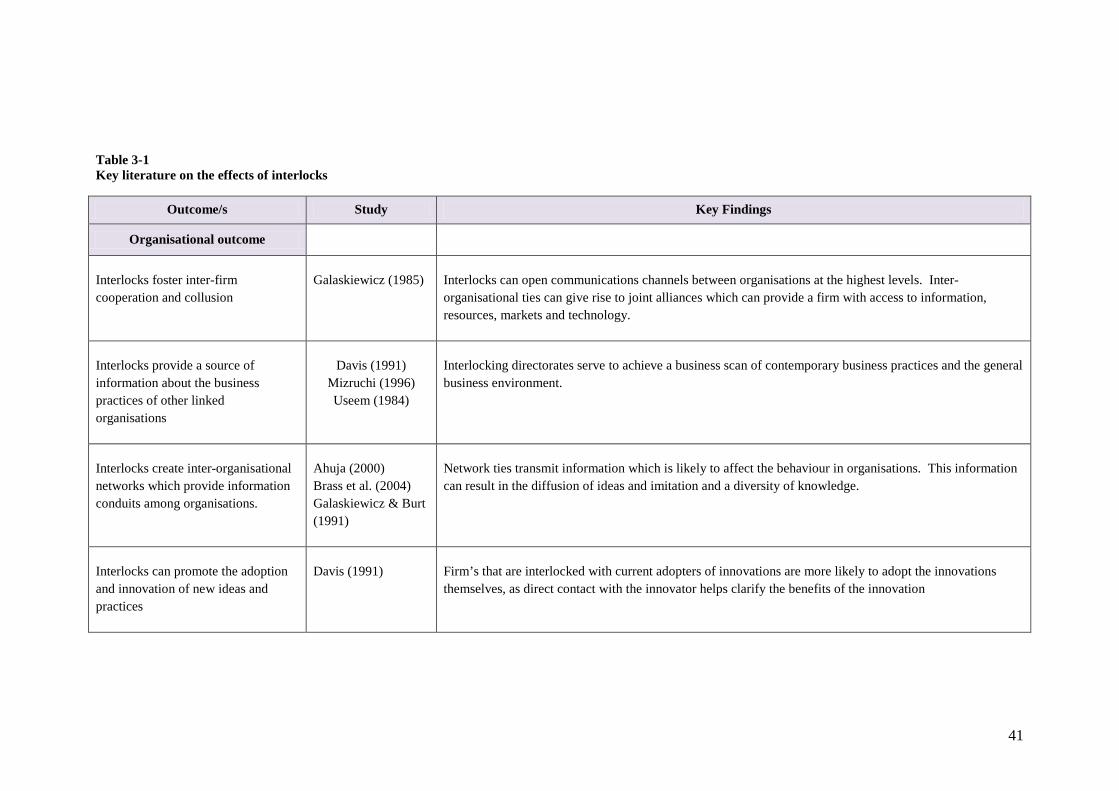

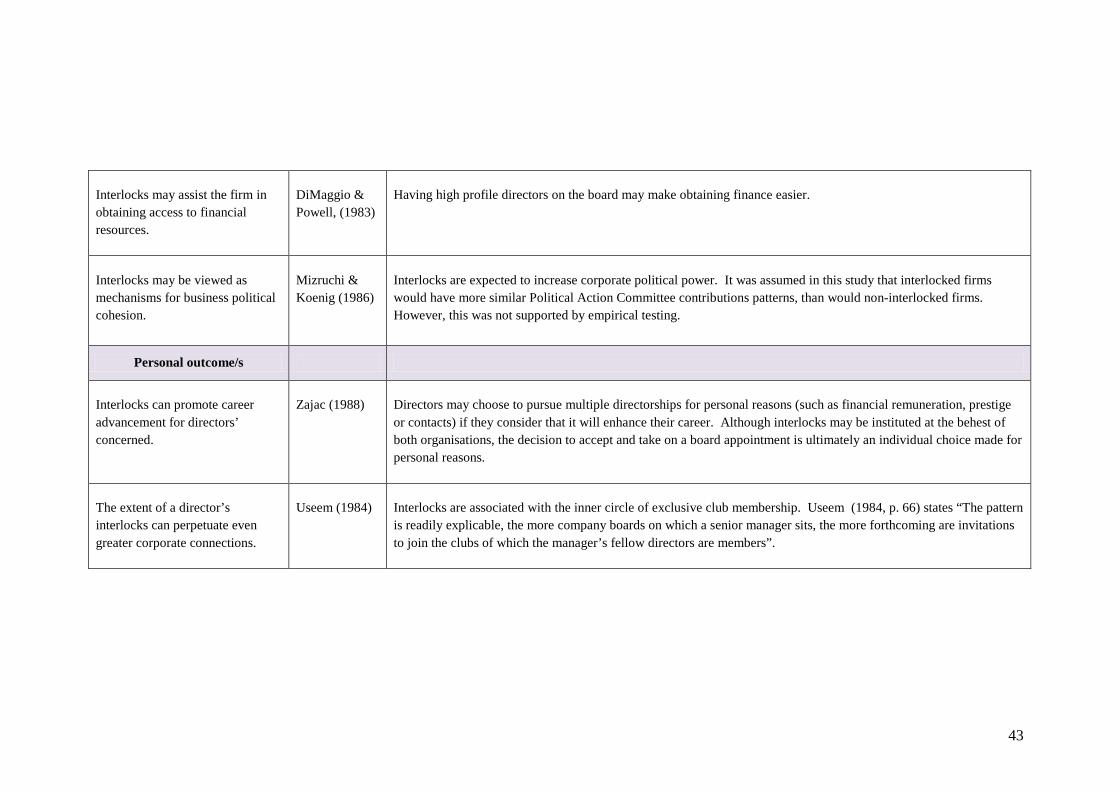

3.2.1 Definitions and overview .............................................................................................. 35 3.2.2 Classification of interlocks ............................................................................................ 37 3.2.3 Measurement of interlocks .......................................................................................... 38 3.2.4 Effects and consequences of interlocks ........................................................................ 39 3.2.5 Relationships of interlocks to firm performance .......................................................... 40

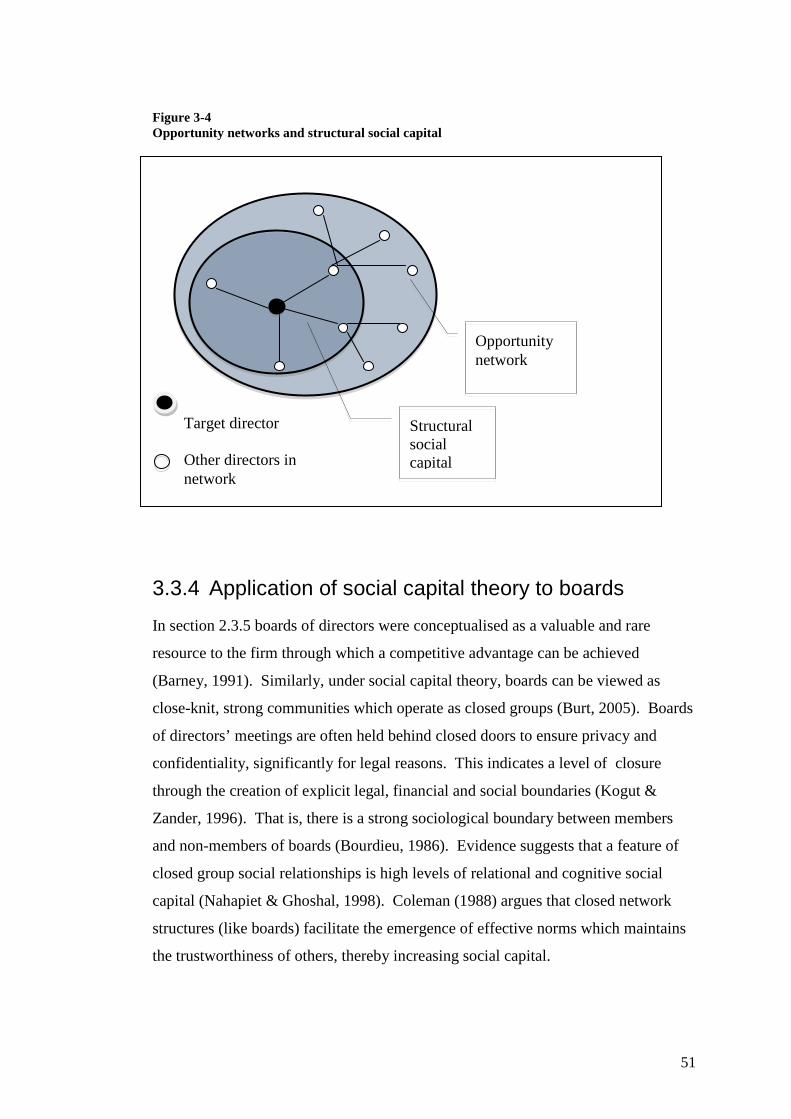

3.3 SOCIAL CAPITAL AND OPPORTUNITY NETWORKS ................................................................................ 45 3.3.1 Introduction to social capital ....................................................................................... 45 3.3.2 Defining social capital .................................................................................................. 45 3.3.3 Dimensions and measurement of social capital........................................................... 47 3.3.4 Application of social capital theory to boards.............................................................. 51

v

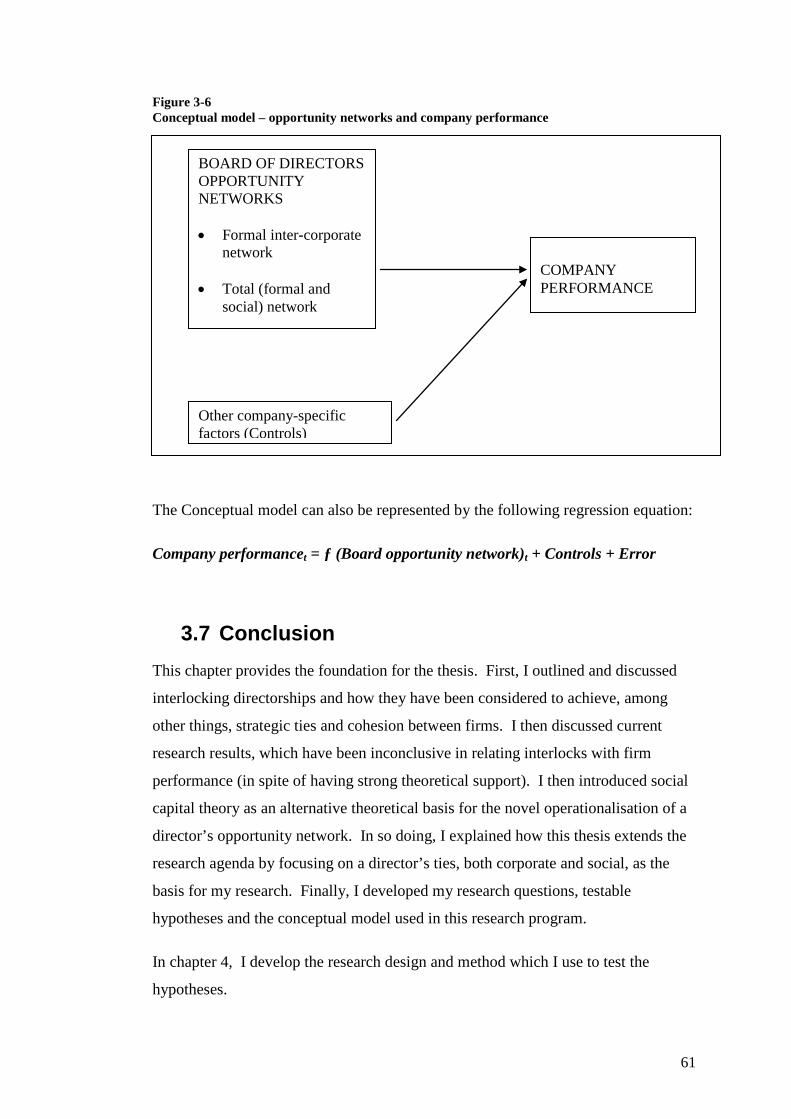

3.4 DEVELOPMENT OF RESEARCH QUESTIONS ........................................................................................ 55 3.5 HYPOTHESES DEVELOPMENT ......................................................................................................... 57 3.6 CONCEPTUAL MODEL .................................................................................................................. 60 3.7 CONCLUSION ............................................................................................................................. 61

CHAPTER 4 PHILOSOPHY, DESIGN AND METHOD ........................................................................ 62

4.1 INTRODUCTION .......................................................................................................................... 62 4.2 JUSTIFICATION FOR THE PARADIGM AND METHODOLOGY .................................................................... 62

4.2.1 Research philosophy .................................................................................................... 62 4.2.2 Approach to this research. ........................................................................................... 65

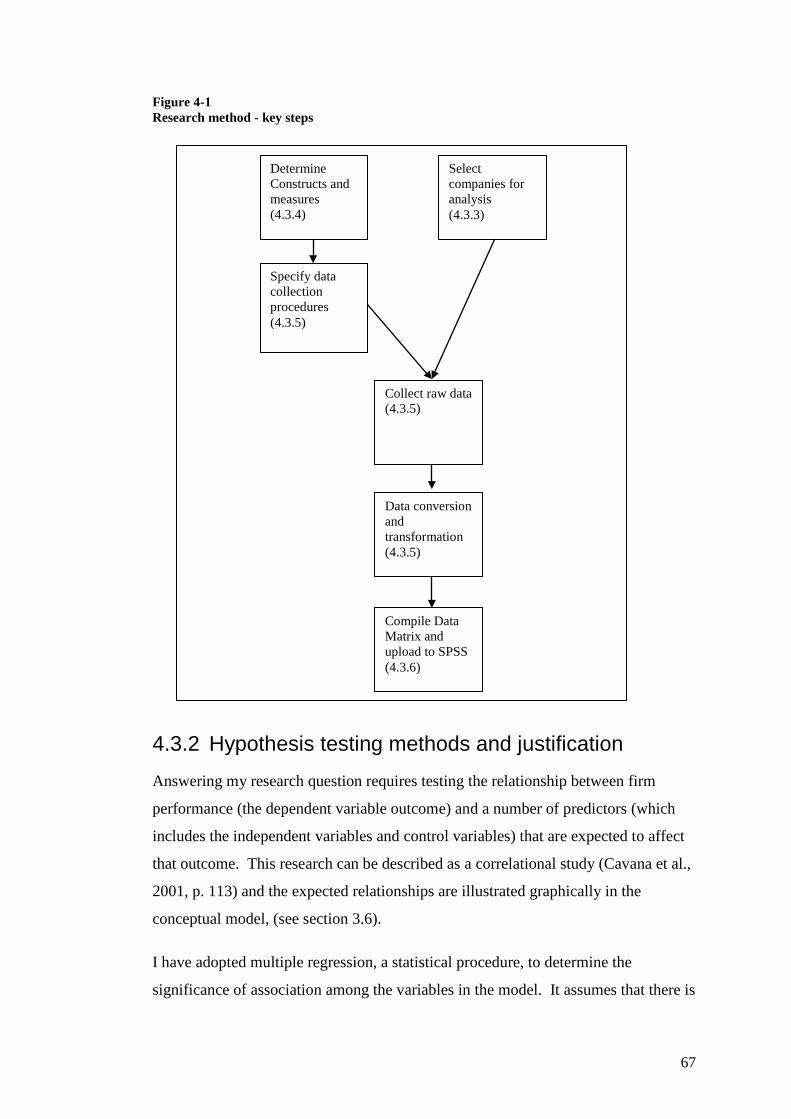

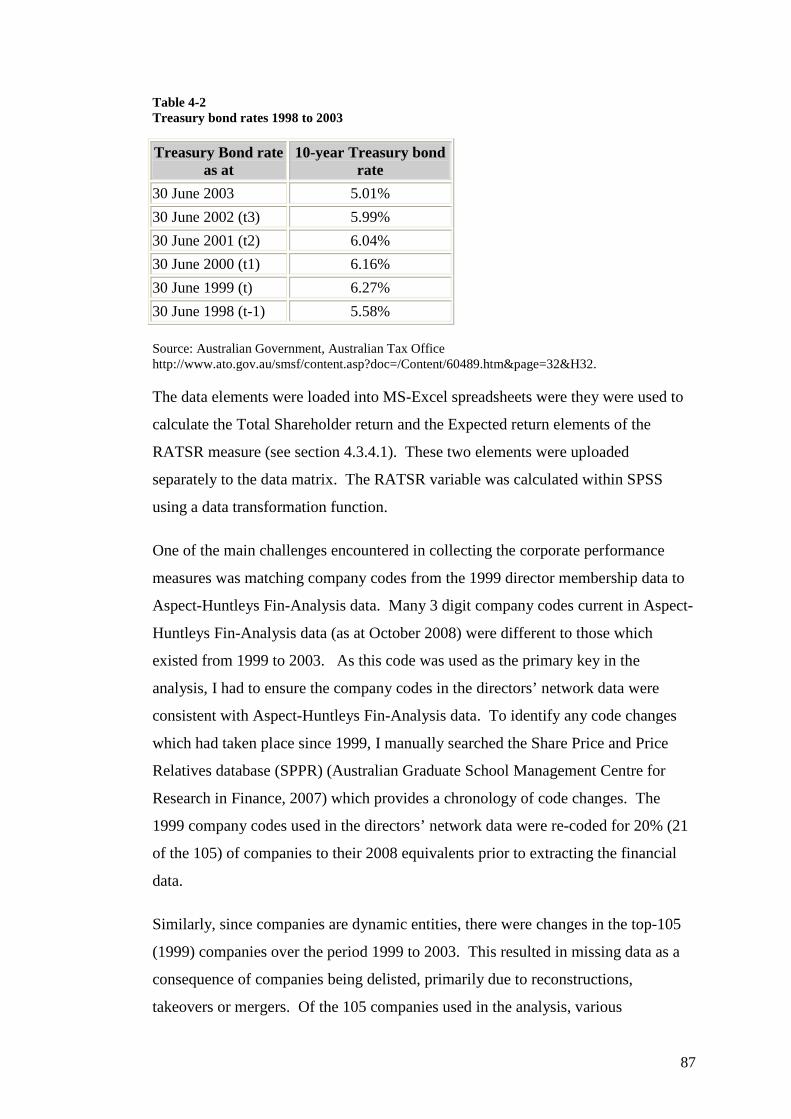

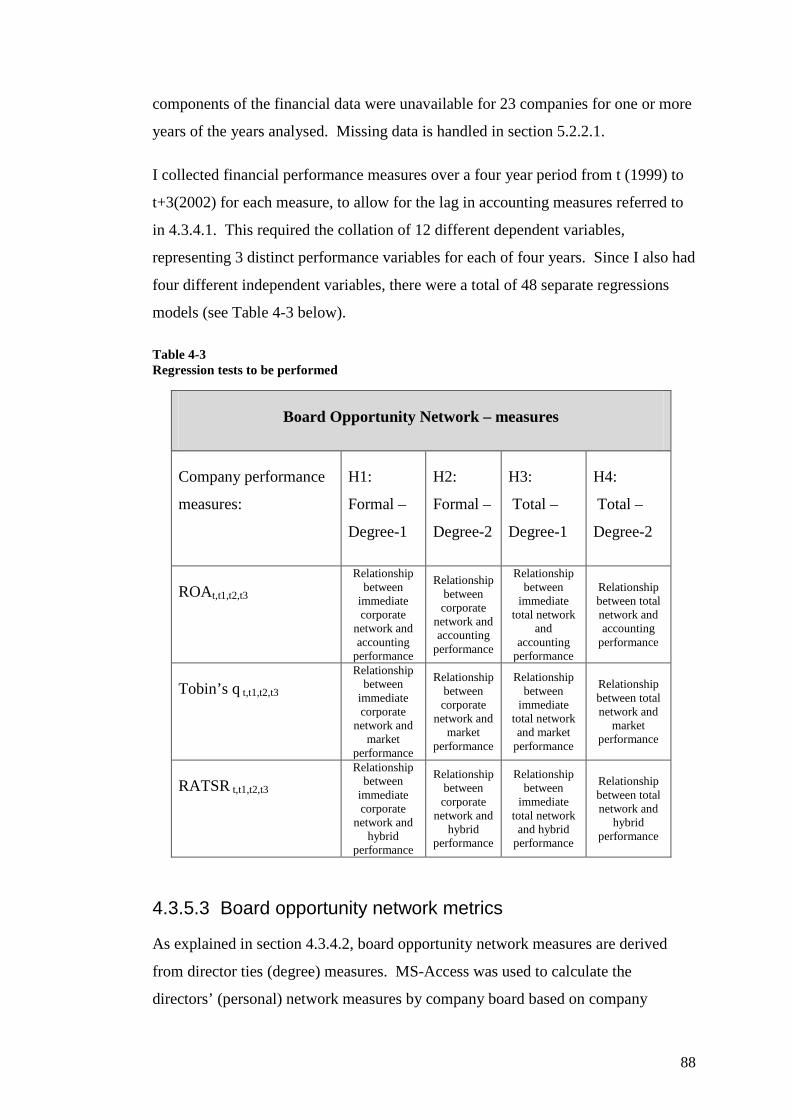

4.3 RESEARCH DESIGN AND METHOD ................................................................................................... 66 4.3.1 Overview ...................................................................................................................... 66 4.3.2 Hypothesis testing methods and justification .............................................................. 67 4.3.3 Study period and sample selection .............................................................................. 69 4.3.4 Constructs and measures ............................................................................................. 70 4.3.5 Data sources and data collection ................................................................................. 81 4.3.6 Data matrix preparation and upload ........................................................................... 99

4.4 CONCLUSION ............................................................................................................................. 99

CHAPTER 5 ANALYSIS AND FINDINGS ........................................................................................ 101

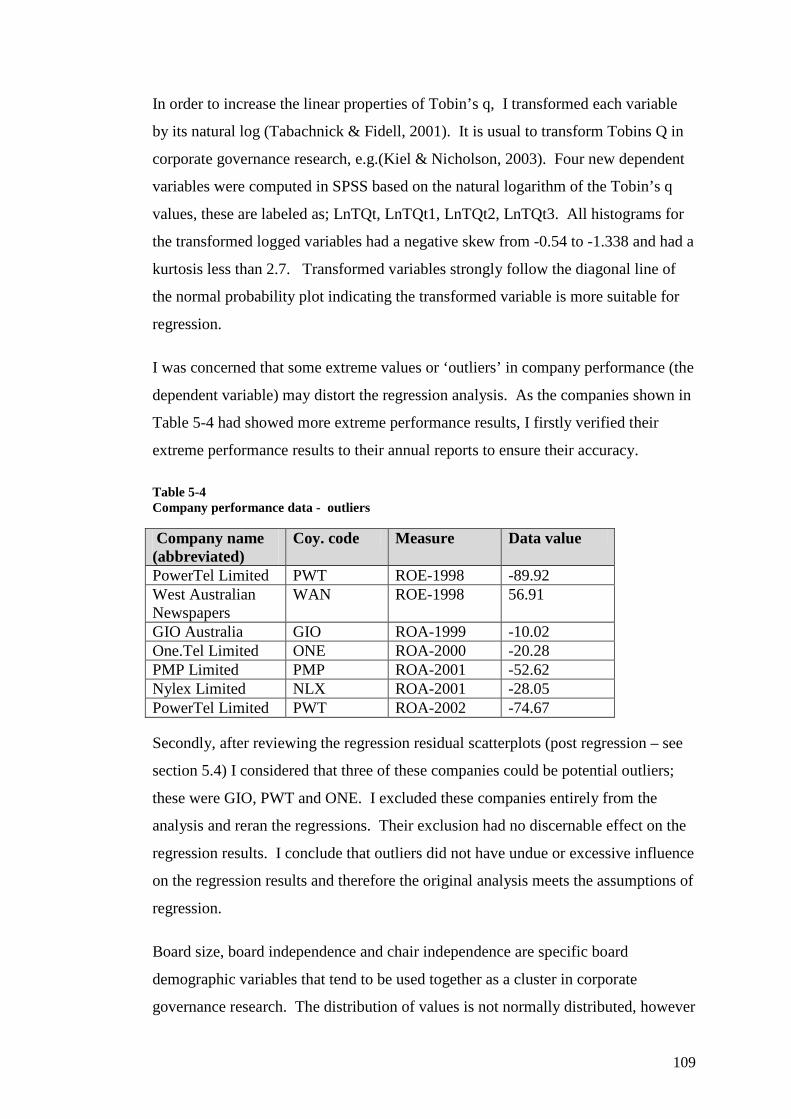

5.1 INTRODUCTION ........................................................................................................................ 101 5.2 DATA SCREENING AND DESCRIPTIVE STATISTICS ............................................................................... 101

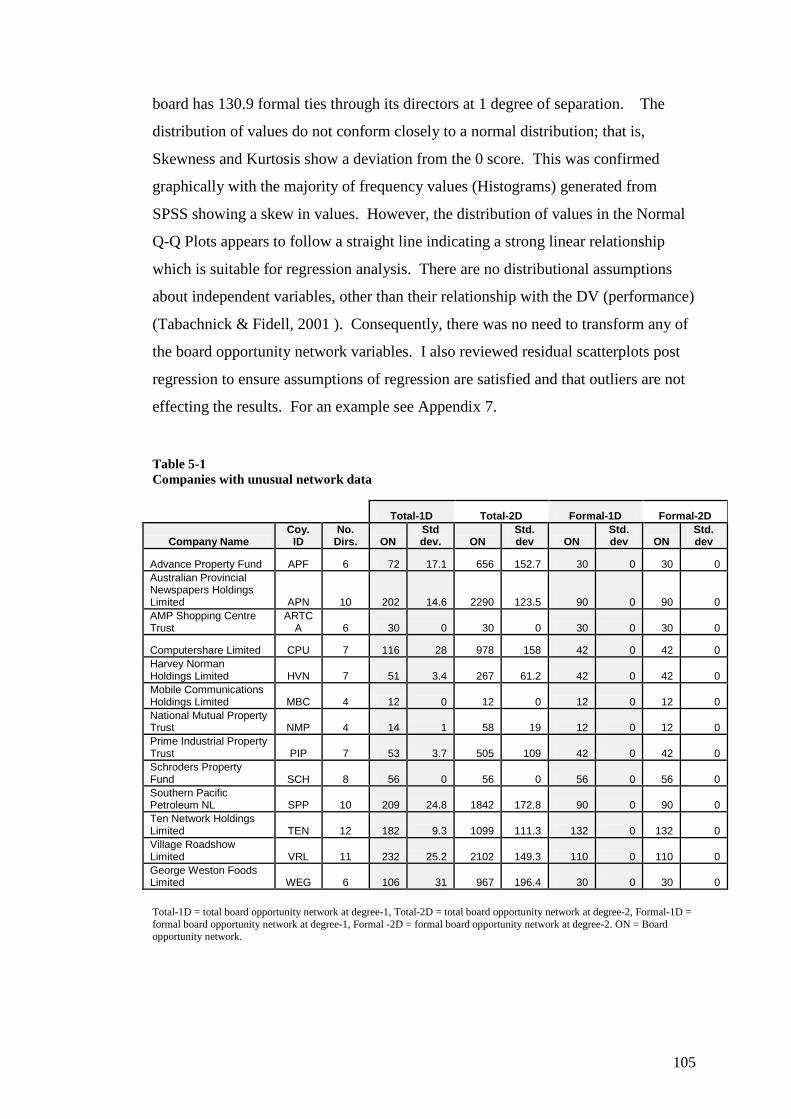

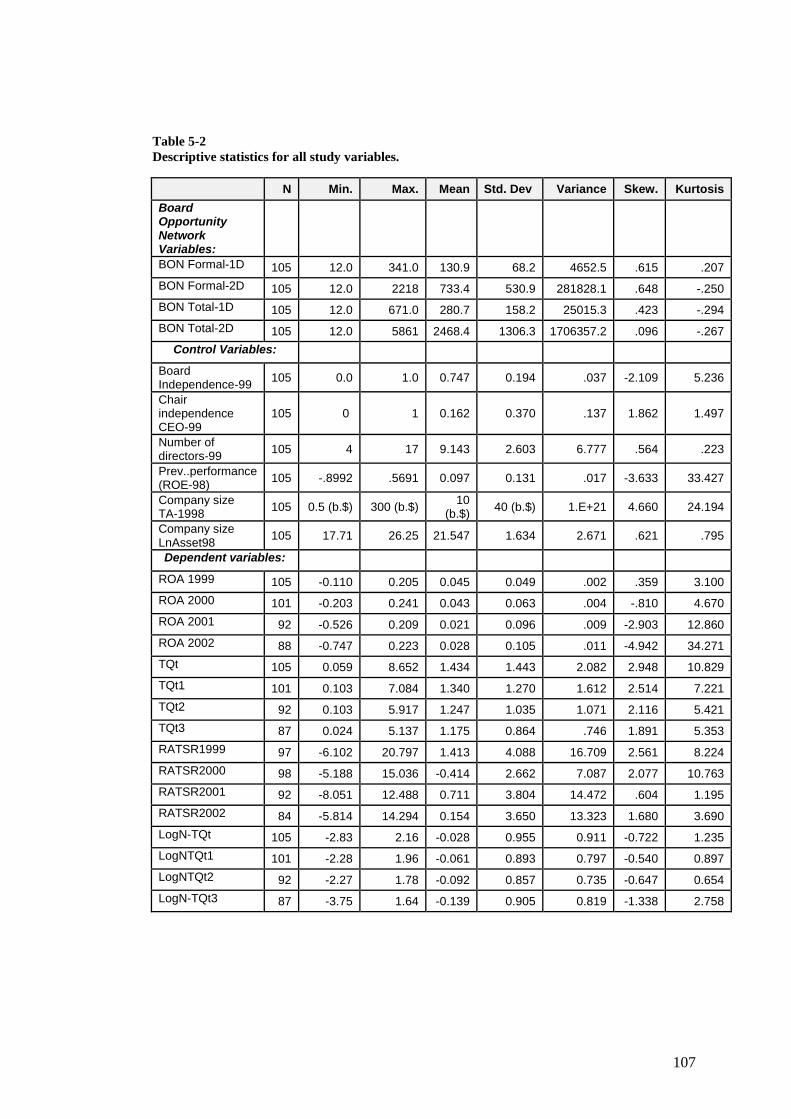

5.2.1 Pre-analysis screening ................................................................................................ 102 5.2.2 Screening board network (IV) data ............................................................................ 104 5.2.3 Screening performance and control data .................................................................. 106

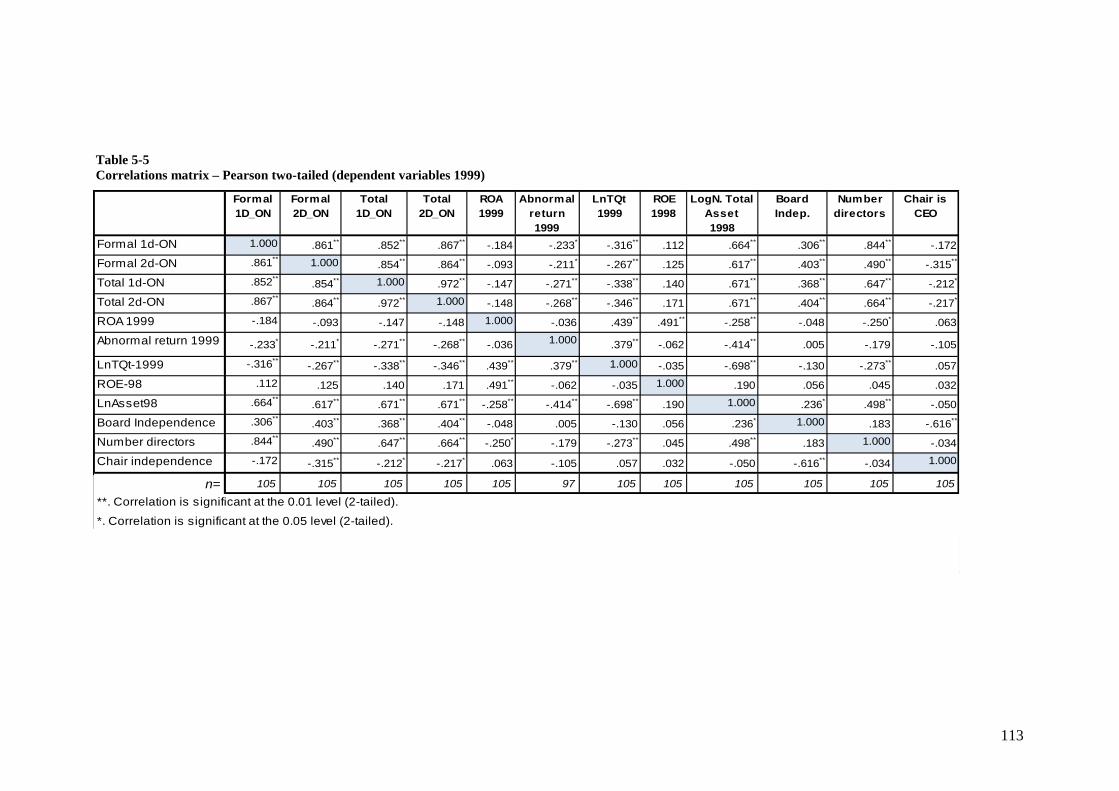

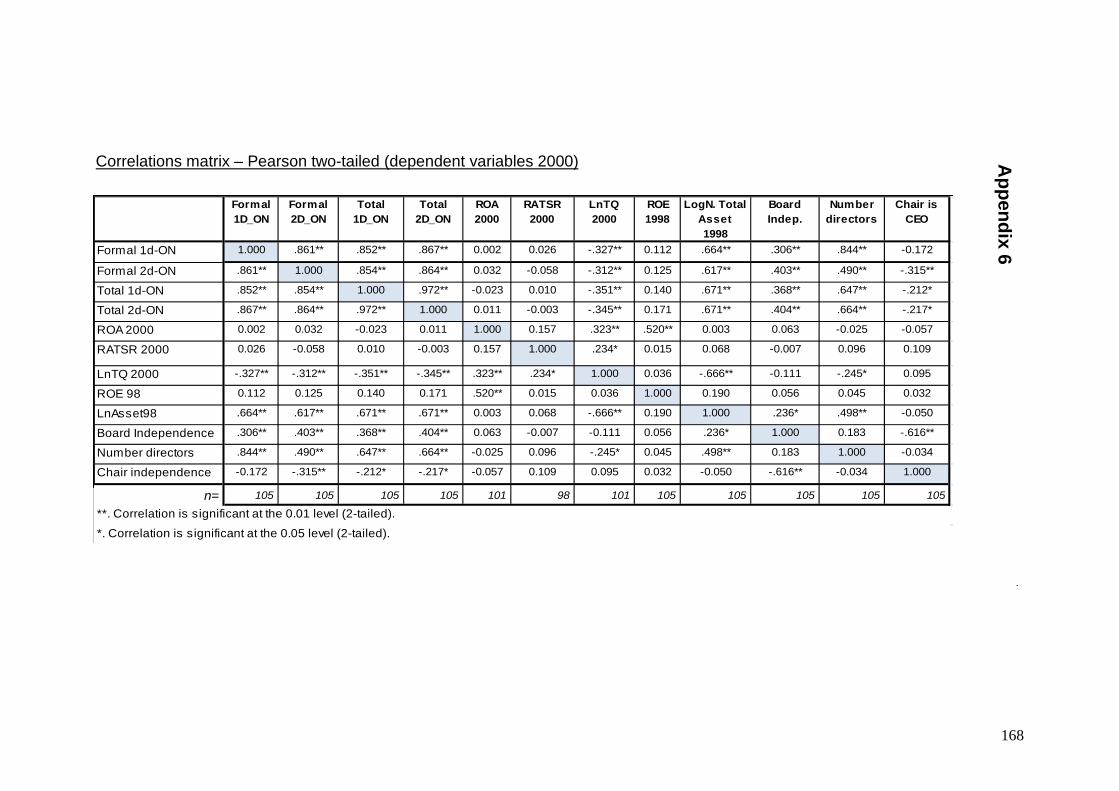

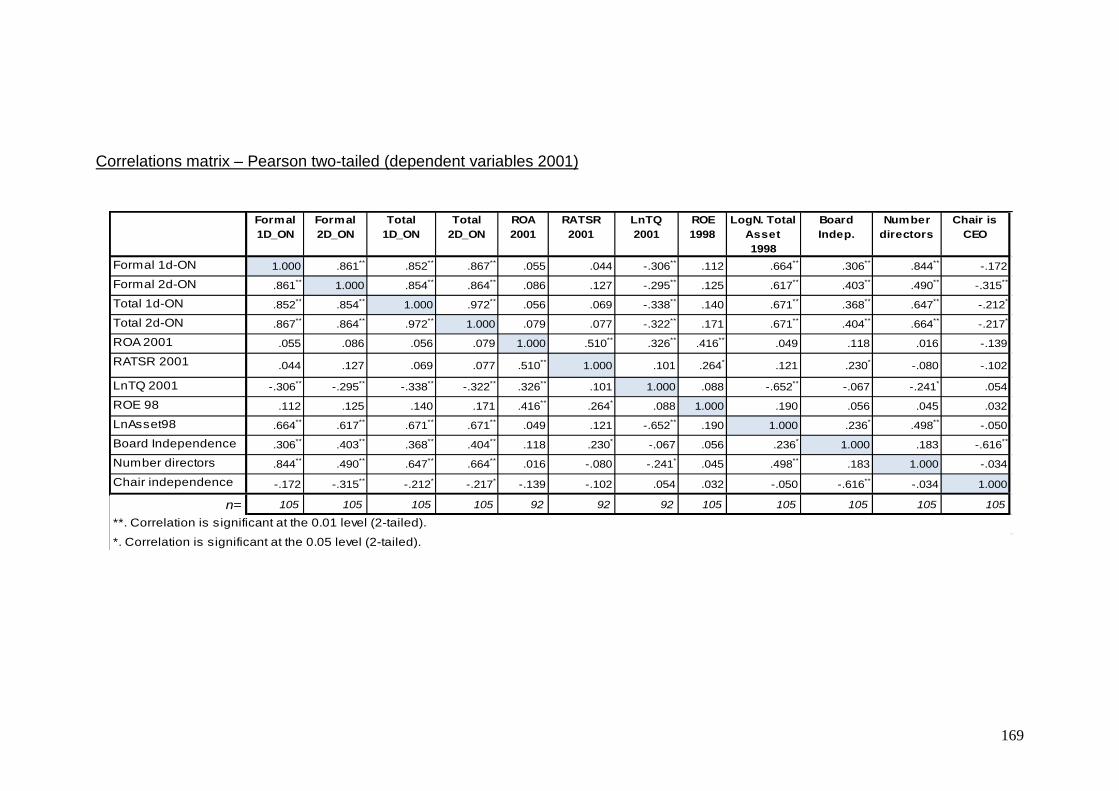

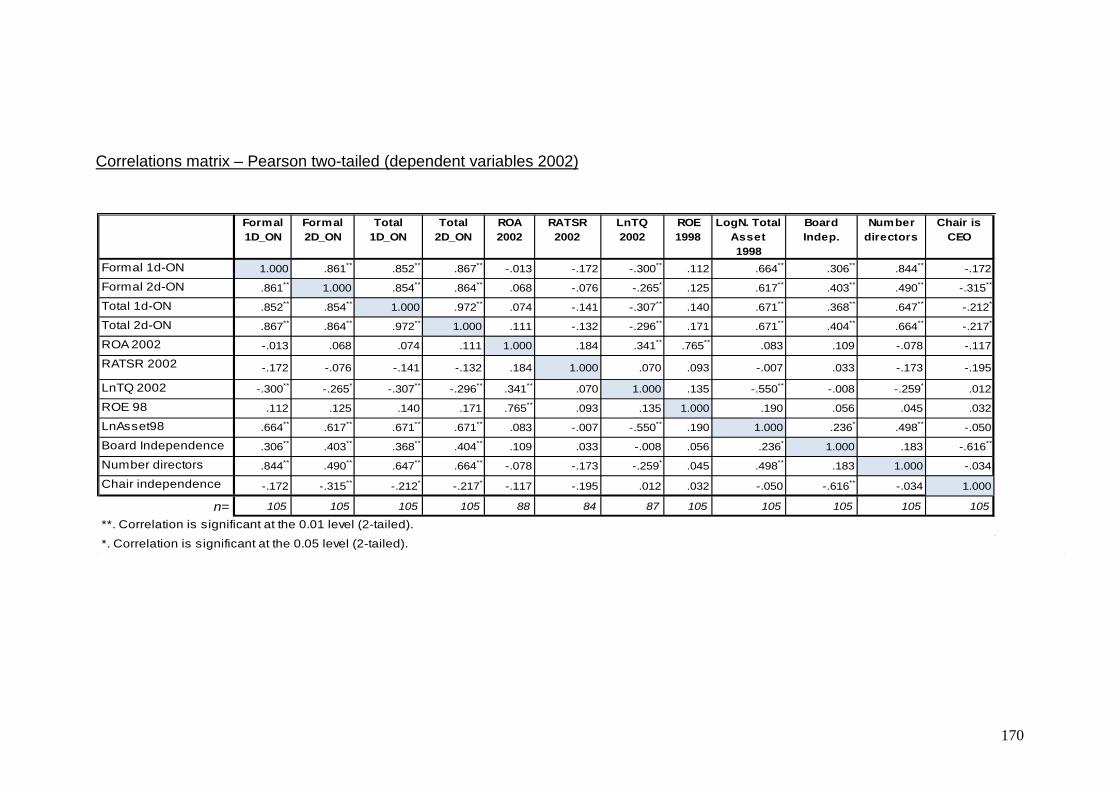

5.3 CORRELATIONS ........................................................................................................................ 111 5.3.1 Correlation matrix ...................................................................................................... 111

5.4 REGRESSION ANALYSIS ............................................................................................................... 115 5.5 FINDINGS ................................................................................................................................ 117

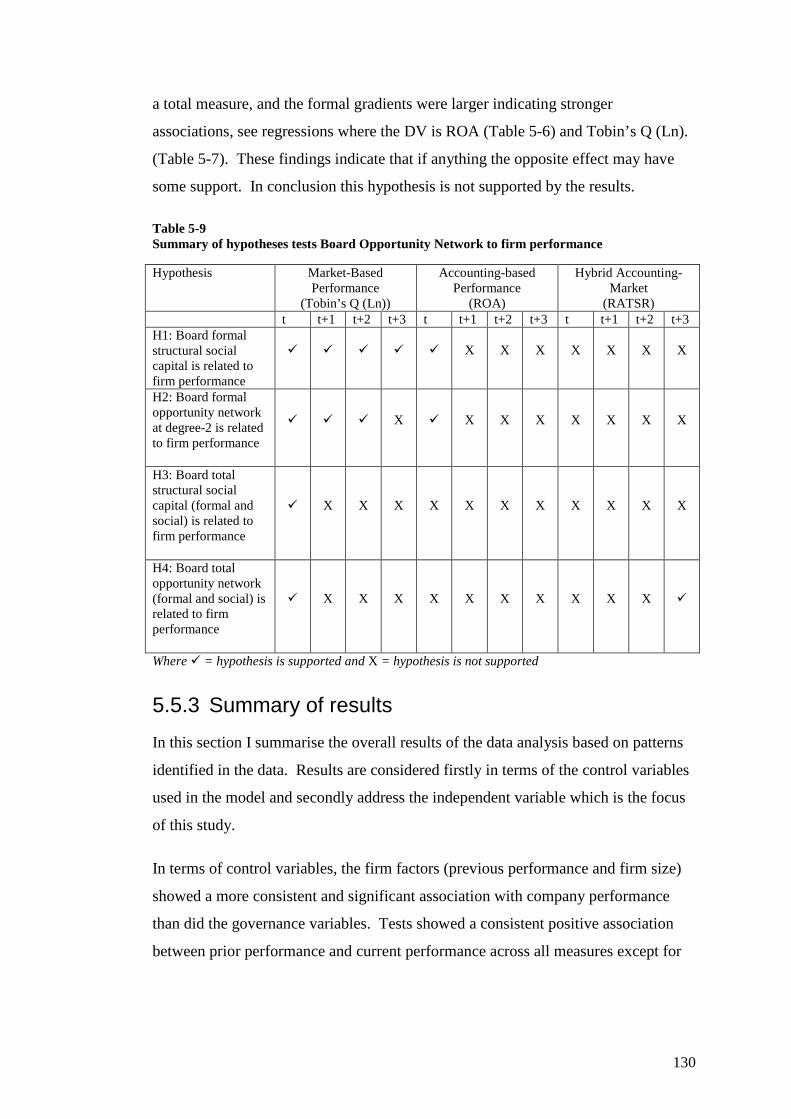

5.5.1 Results of regression tests .......................................................................................... 117 5.5.2 Results of hypotheses tests ........................................................................................ 123 5.5.3 Summary of results .................................................................................................... 130

5.6 CONCLUSION ........................................................................................................................... 131

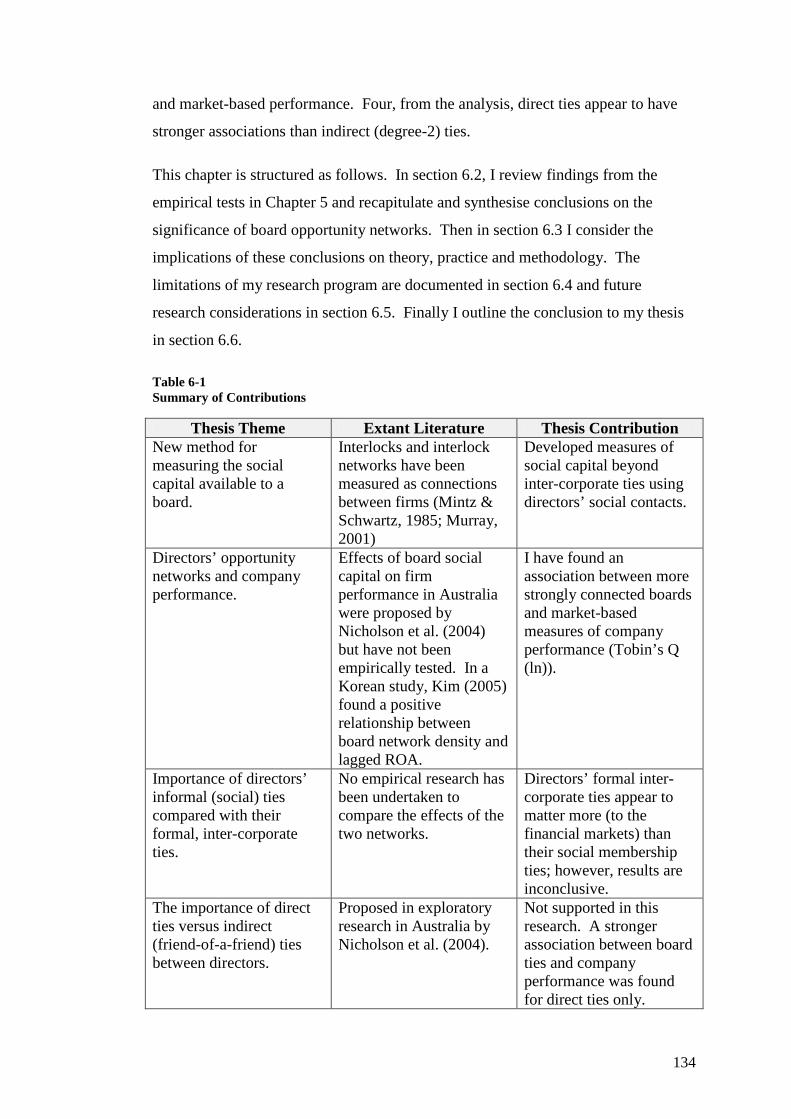

CHAPTER 6 DISCUSSION AND CONCLUSION .............................................................................. 133

6.1 INTRODUCTION ........................................................................................................................ 133 6.2 CONCLUSION ON RESEARCH QUESTIONS ........................................................................................ 135

6.2.1 Formal board ties and company performance ........................................................... 135 6.2.2 Inclusion of directors’ social ties in the analysis ......................................................... 139 6.2.3 Using the boards’ opportunity network in the analysis ............................................. 141

6.3 IMPLICATIONS OF THE THESIS ...................................................................................................... 142 6.3.1 Implications for theory ............................................................................................... 142 6.3.2 Implications for practice ............................................................................................ 143 6.3.3 Implications for methodology .................................................................................... 144

6.4 LIMITATIONS ........................................................................................................................... 146 6.4.1 Measurement error in formal networks at two degrees of separation. .................... 146 6.4.2 Limitations in the social connections data. ................................................................ 146 6.4.3 Datedness of the study period. .................................................................................. 147 6.4.4 Single year data and cross-sectional design. ............................................................. 148 6.4.5 Lagged accounting-based measures .......................................................................... 148

6.5 FURTHER RESEARCH .................................................................................................................. 148 6.6 CONCLUSION ........................................................................................................................... 150

APPENDICES .................................................................................................................................. 153

vi

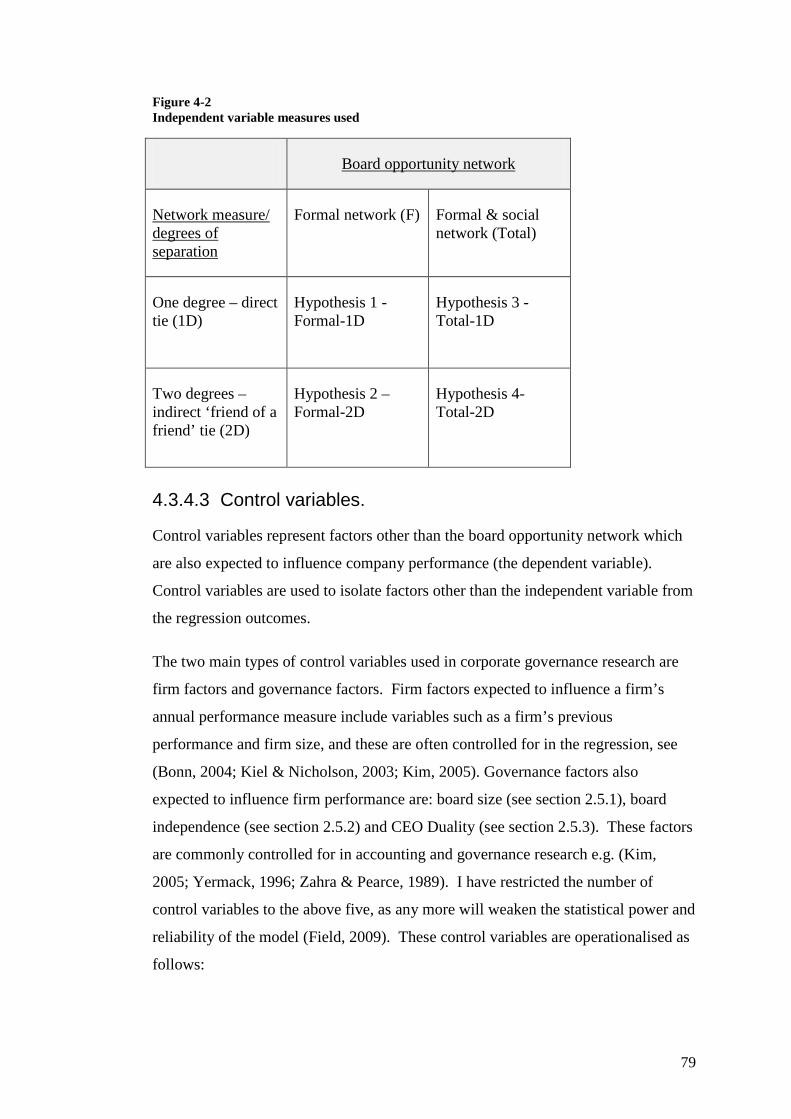

List of Figures Figure 2-1 Board attributes, roles and performance ........................................................................... 25Figure 3-1 Interlocks measured as connections between companies ................................................. 36Figure 3-2 Classification of director interlocks .................................................................................... 38Figure 3-3 Dimensions of social capital ............................................................................................... 48Figure 3-4 Opportunity networks and structural social capital ........................................................... 51Figure 3-5 Theory classification overview ............................................................................................ 54Figure 3-6 Conceptual model – opportunity networks and company performance ........................... 61Figure 4-1 Research method - key steps .............................................................................................. 67Figure 4-2 Independent variable measures used ................................................................................ 79Figure 4-3 Process to generate board opportunity network metrics .................................................. 91Figure 6-1 The dyad – a simple undirected network ......................................................................... 163

vii

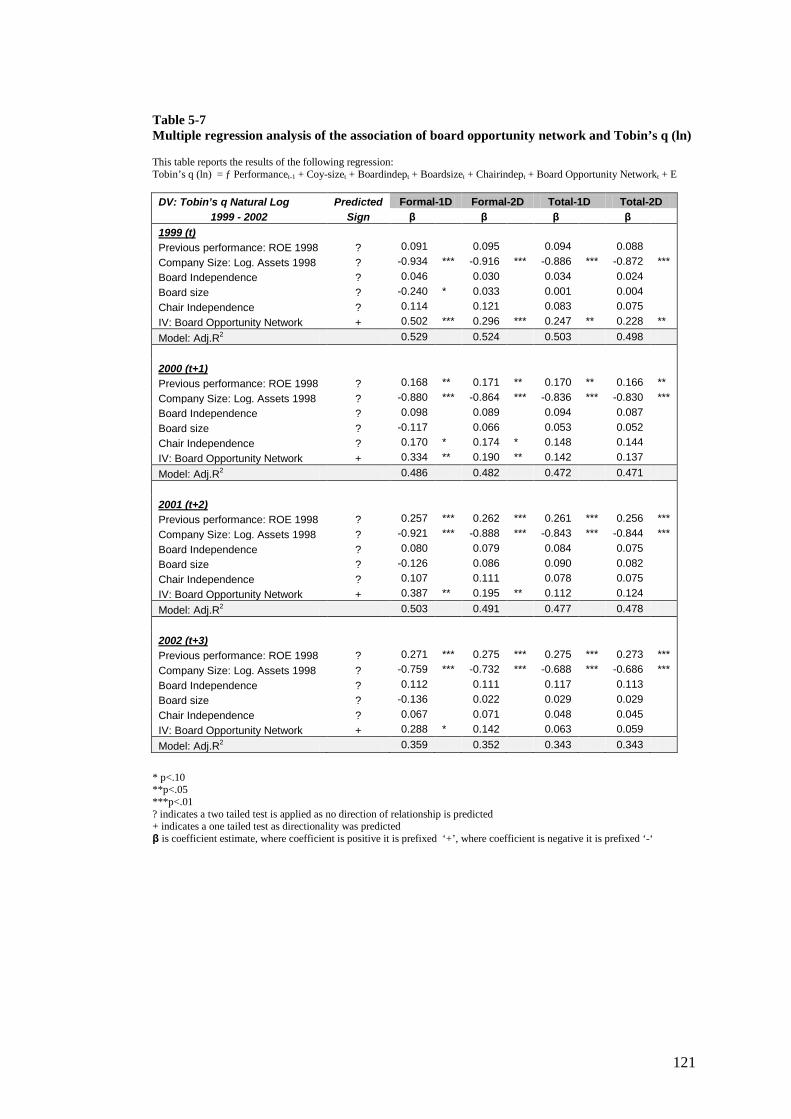

List of Tables Table 3-1 Key literature on the effects of interlocks ........................................................................... 41Table 3-2 Research into the relationship between interlocks and firm performance ......................... 44Table 4-1 Overview of data types, years, sources and processing requirements ............................... 84Table 4-2 Treasury bond rates 1998 to 2003 ....................................................................................... 87Table 4-3 Regression tests to be performed ....................................................................................... 88Table 4-4 Directors network relationship data - descriptive analysis .................................................. 93Table 4-5 Director memberships of professional organisations .......................................................... 95Table 5-1 Companies with unusual network data ............................................................................. 105Table 5-2 Descriptive statistics for all study variables. ...................................................................... 107Table 5-3 Missing data summary – company financial performance variables ................................. 108Table 5-4 Company performance data - outliers .............................................................................. 109Table 5-5 Correlations matrix – Pearson two-tailed (dependent variables 1999) ............................. 113Table 5-6 Multiple regression analysis of the association of board opportunity network and ROA . 119Table 5-7 Multiple regression analysis of the association of board opportunity network and Tobin’s q

(ln) ............................................................................................................................................ 121Table 5-8 Multiple regression analysis of the association of board opportunity network and RATSR

.................................................................................................................................................. 122Table 5-9 Summary of hypotheses tests Board Opportunity Network to firm performance ............ 130Table 6-1 Summary of Contributions ................................................................................................. 134Table 6-2 Implications of thesis conclusions for theory, practice and methodology ........................ 145

viii

List of Appendices APPENDIX 1 Director associations database tables ............................................................................................ 154

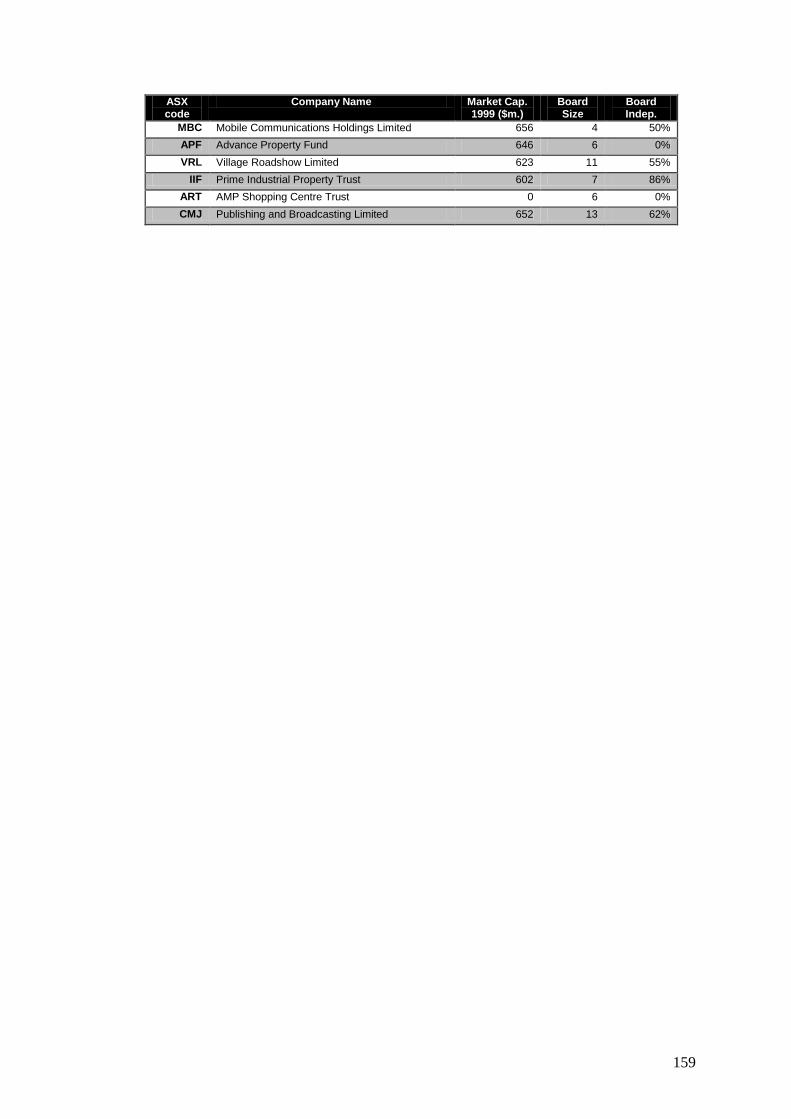

APPENDIX 2 Top-105 companies ....................................................................................................................... 157

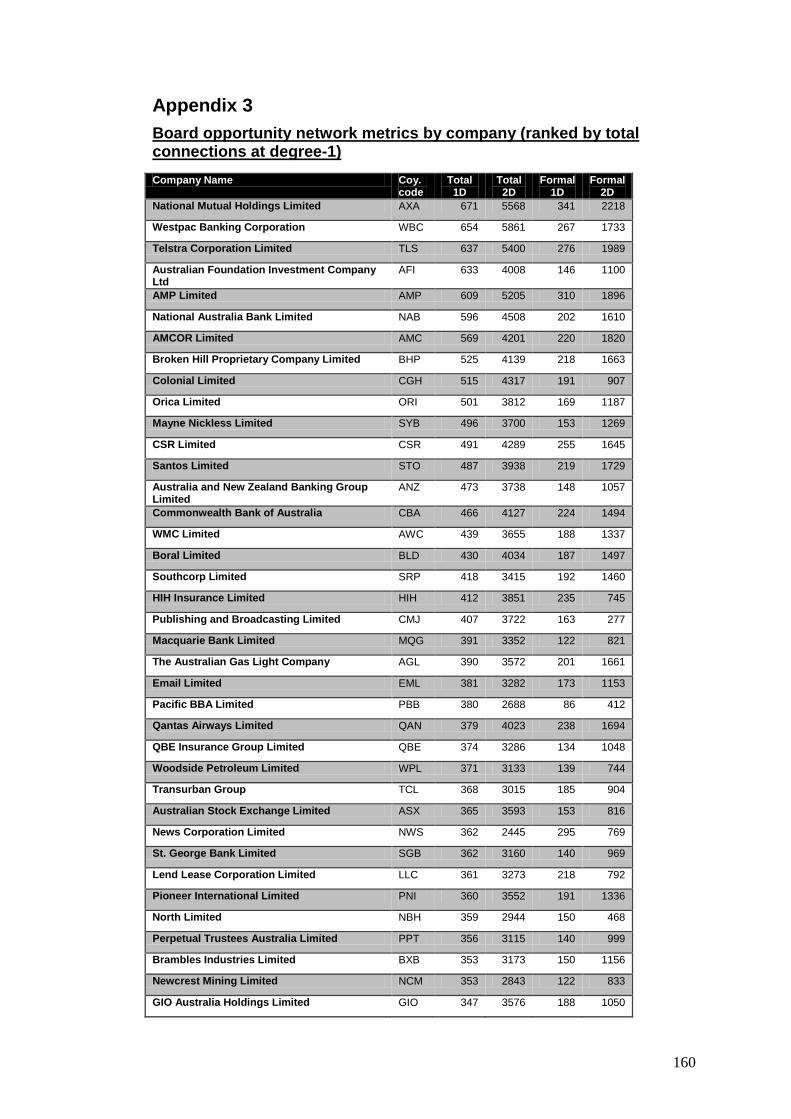

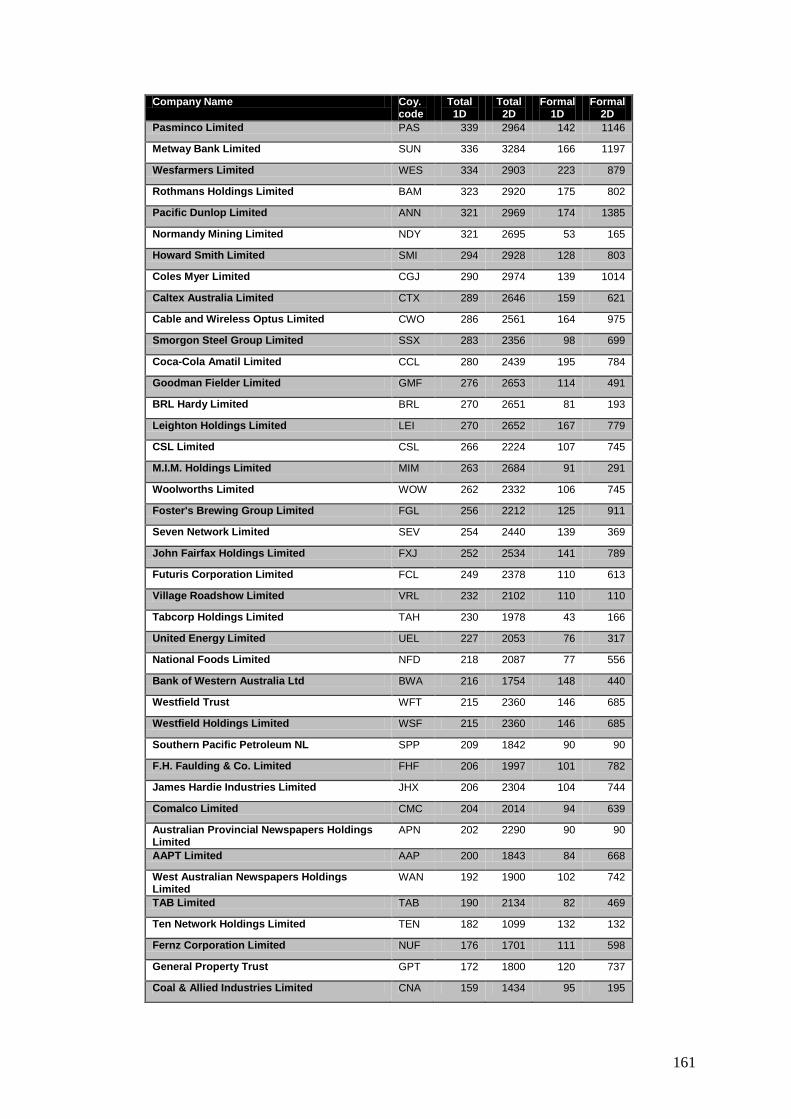

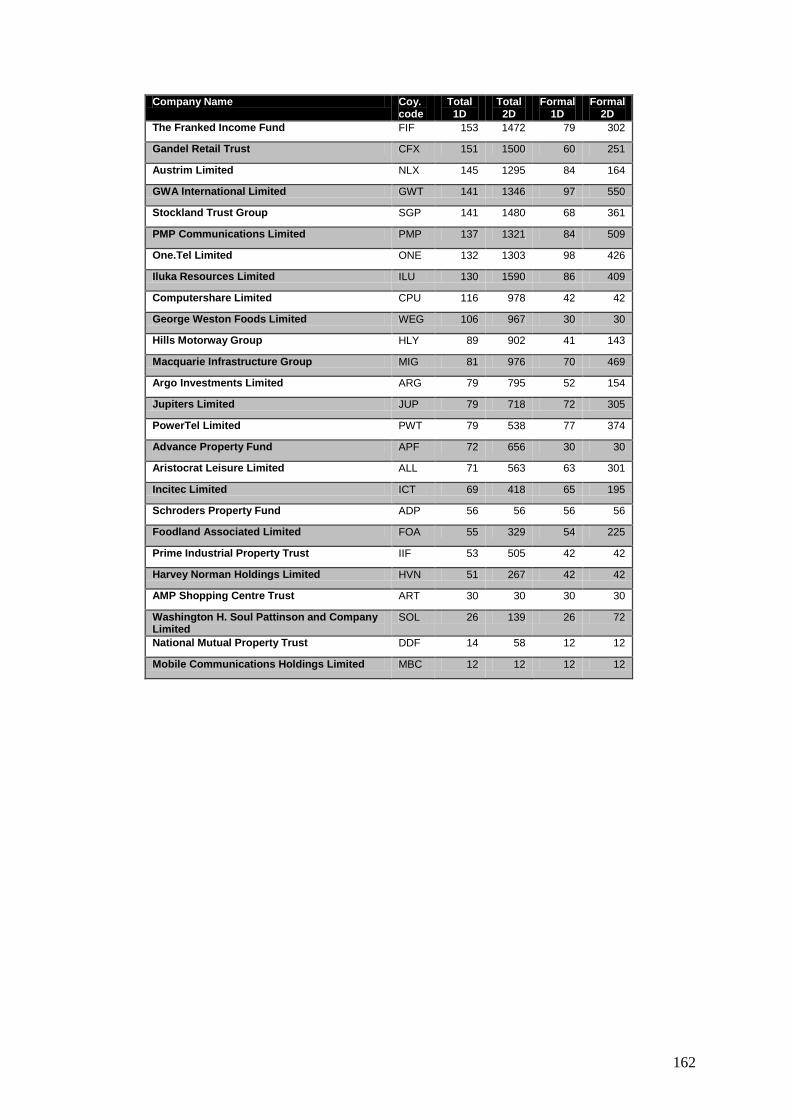

APPENDIX 3 Board opportunity network metrics by company .......................................................................... 160

APPENDIX 4 Social network analysis (SNA) ........................................................................................................ 163

APPENDIX 5 SNA network measures ................................................................................................................. 166

APPENDIX 6 Correlation matrices 2000-2002 ..................................................................................................... 168

APPENDIX 7 Statistical procedures employed .................................................................................................... 171

ix

Statement of Originality

The work presented in this thesis, is to the best of my knowledge and belief, original

and my own work, except as acknowledged in the text. It has not been submitted in

whole or in part, for a degree at this or any other university.

________________________________

Kevin J. Smith

Date_____________________________

x

Acknowledgements Firstly, I would like to express my thanks to Dr. Gavin Nicholson my principal supervisor, for the many hours I know he contributed to making this thesis happen for me. His thoughts and challenging ideas have added a new dimension to my learning. I would also like to thank other staff and colleagues at QUT for their help and support over the duration of this research; in particular Professor Natalie Gallery (my associate supervisor), Professor Gerry Gallery, Dr. Stephen Cox, Dr. Cameron Newton and Kerry Kruger. To Associate Professor, Malcolm Alexander at Griffith University your assistance with social network analysis is appreciated. Finally to my friends and family, thank-you for your support and encouragement over the period of this study, particularly those who assisted in reading the document.

1

Chapter 1 Introduction

1.1 Background to the research Do board contacts matter? In this thesis I seek to develop an understanding of this

question by investigating boards of directors’ formal inter-corporate connections as

well as their social connections, and any relationship between these connections and

the performance of the companies they govern.

Over the past decade corporate governance has received regular coverage in the

financial press, and various articles have targeted boards of directors’ and the roles

they play in governing companies. There have been calls for boards to be more

effective and add value to the corporations they oversight. This has generated

discussion and research into the roles boards play (Johnson, Daily, & Ellstrand,

1996; Zahra & Pearce, 1989). Although there is no universal board role set (Daily,

Dalton & Cannella, 2003), boards clearly play multiple roles in the corporations they

govern (Hillman & Dalziel, 2003). This research focuses on the strategic role of the

board of directors, and a board’s capability to assist their company in acquiring the

resources it needs for its survival. Under the Resource Based View (RBV) of the

firm (Barney, 1991; Wernerfelt, 1984) boards are seen as a strategic resource that

can add value to their firms and the Australian economy. For example, the quoted

market capitalisation of the ASX in 2008 was estimated to be $1.29 trillion.1

Specifically my research is concerned with better understanding how a firm’s access

to resources may vary with the social capital of the board of directors. Often

referred to as their resource dependence role (Pfeffer & Salancik, 1978), it is a

strategic role whereby board members provide their firms with access to critical

resources (Pfeffer, 1972) and a consequent advantage over competitors. I adopt

, if

boards could add an additional 1% greater value to companies they govern, the

impact on the value of the ASX market capitalisation alone would be $12.9 billion.

Therefore the impact of boards and their potential to add value to the corporations

they govern is significant.

1 Based on the ASX domestic market capitalisation as at 30 June 2008, from ASX website http://www.asx.com.au/about/asx/index.htm as at 2 August 2009.

2

social capital theory (Burt, 1980b; Nahapiet & Ghoshal, 1998) to understand how

resources are accessed through the network of directors’ personal connections. I do

this by examining how a firm’s financial performance varies with different measures

of a board’s opportunity network, or the potential social capital available to it

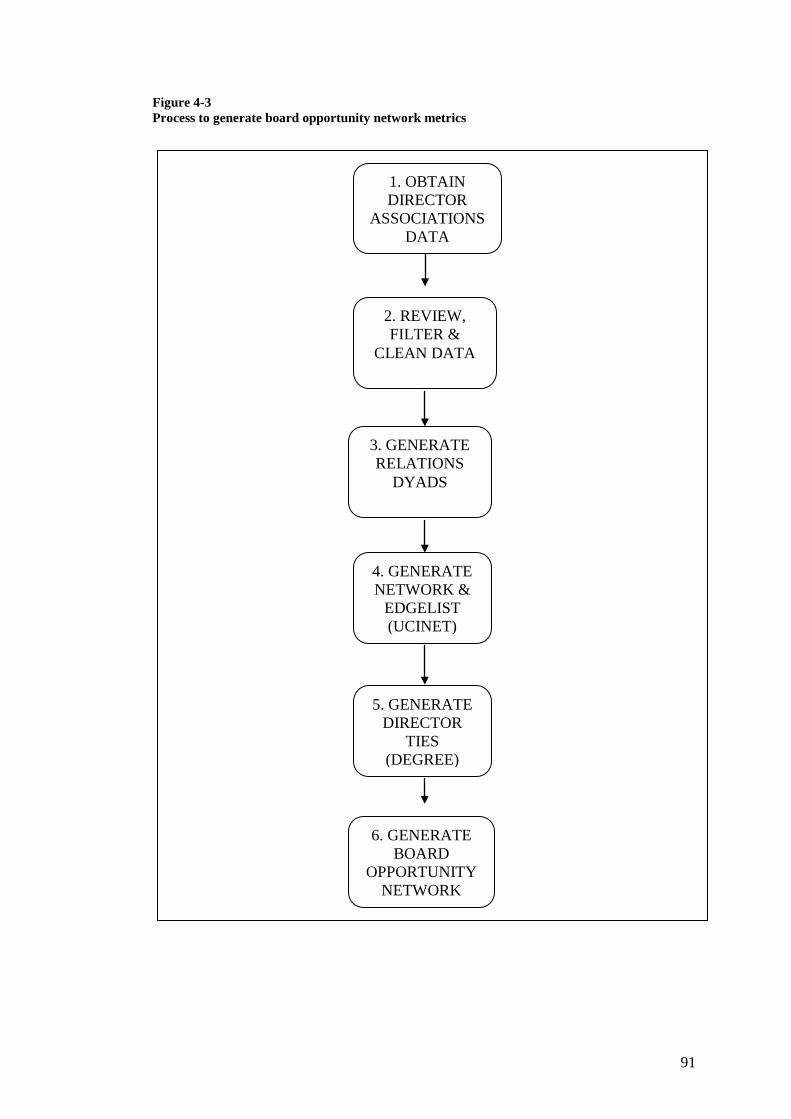

(Nicholson, Alexander, & Kiel, 2004).

The remainder of Chapter 1 provides an overview of this thesis. In section 1.2, I

identify the research problem and the specific hypotheses that are tested in this

research. The justification for the research is contained in section 1.3 and an

overview of the research methodology is discussed in section 1.4. The thesis

structure is discussed in section 1.5, and the definition of key terms used throughout

the thesis is contained in section 1.6. In the final section 1.7, I discuss the

delimitations or boundaries to this research program.

1.2 Research problem This research investigates the relationship between board of director opportunity

networks and company performance. Specifically, the central theme of this research

is the question:

Is there a relationship between the size of a corporate board’s opportunity

network and the performance of the company it governs?

This research is based on the Resource Based View (RBV) of the firm (Wernerfelt,

1984) where boards are viewed as a strategic resource available to firms, through

which firms can access scarce resources critical to their survival. This view of the

board is based on social capital theory (Burt, 1980b; Coleman, 1988) and resource

dependence theory (Pfeffer & Salancik, 1978). Social capital theory investigates

relationships between people, their interpersonal ties and the advantage that

interpersonal ties can generate. In Australia’s largest companies this social capital

(i.e. the ties between the individual directors of company boards) forms the basis for

possible competitive advantage. Since resource dependence theory links a firm’s

survival to its ability to acquire and control external resources, firms may engage

directors to improve their access to external resources (Pfeffer & Salancik, 1978). In

short, they can use interlocking directorships (Mizruchi, 1996) or interlocks (when a

3

director of one company also serves on the boards of one or more other companies

(Scott, 1991a) to control the flow of resources. As discussed in section 3.2,

interlocks are considered to be inter-corporate connections.

As interlocks are thought to be associated with a firm’s ability to access resources, it

can be reasonably expected that they will be associated with corporate performance.

However a considerable amount of research, including recent Australian research

into interlocks and firm performance, has failed to produce robust results in support

of this phenomenon (see section 3.2.5).

In this study I question the conceptual validity of measuring inter-corporate

connections at the firm level. Social capital theory argues that it is through

individual relationships and ties between people (in this case directors), and not firm

ties, that resources and advantage can be acquired. Every person has a unique social

capital footprint which comprises their network of connections (Nahapiet &

Ghoshal, 1998). Therefore I measure inter-corporate connections through directors

structural social capital which is a key component of, and used as a proxy for, their

individual social capital. I define the network of contacts available to directors

through their connections as their ‘opportunity network’, and propose that it is

through their opportunity network that directors access resources. The opportunity

network available through their formal inter-corporate ties is referred to as their

formal opportunity network. I extend the measure of the director’s opportunity

network in two directions, firstly to include directors’ social connections and

secondly to include their indirect as well as their direct ties (see section 3.3.4 for

more detail). Social ties are all other personal ties a director may have excluding

their formal inter-corporate ties. I refer to the combined opportunity network

comprising their formal ties and their social ties as their ‘total opportunity network’.

As social capital is regarded as cumulative and transferable across different types of

relations including business and social relations (Coleman, 1988; Nahapiet &

Ghoshal, 1998), the total opportunity network is, at least theoretically, a more

complete picture of potential resources that a director can access. As well as

examining the impact of social ties, this research extends the study of opportunity

networks to indirect ties. Indirect ties occur through a third person, for example a

‘friend of a friend’ and are considered weaker ties (Granovetter, 1973). Intuitively,

4

social capital is expected to pass to the second level of contact (Nicholson et al.,

2004) which I refer to throughout this thesis as two degrees of separation or degree-2

(see section 3.3). Therefore by measuring directors’ ties at two degrees of

separation, I propose that a more complete measure of directors’ social capital

(through which they can access resources for their companies) is obtained.

As a result of this investigation I test the following six hypotheses:

Hypothesis 1: The size of an Australian company board’s formal structural social

capital is positively correlated with firm performance.

Hypothesis 2: The size of an Australian company board’s formal opportunity

network at degree-2 is positively correlated with firm performance.

Hypothesis 3: The size of an Australian company board’s total structural social

capital (i.e. formal and social) is positively correlated with firm performance.

Hypothesis 4: The size of an Australian company board’s total opportunity

network (i.e. formal and social) at degree-2 is positively correlated with firm

performance.

Hypothesis 5: There is a stronger association and effect of a boards’ opportunity

network measured at degree-2 on firm performance than of a boards’ structural

social capital on firm performance.

Hypothesis 6: There is a stronger association and effect of a boards’ total (formal

and social) opportunity network on firm performance than of a boards’ formal

opportunity network on firm performance.

My results indicate that better connected boards are associated with higher market-

based measures of company performance (measured by Tobin’s q). However there

does not appear to be any consistent association between the size of board

opportunity networks and the accounting-based performance measure (ROA) or the

hybrid market-accounting measure (Risk Adjusted Total Shareholder Return). Also

there does not appear to be any support for extending the board opportunity network

measures beyond direct ties and including social connections in the analysis. More

5

significant results are found when the opportunity network is measured using the

boards’ formal structural social capital.

This thesis makes four contributions to the corporate governance literature (see

chapter 6, particularly section 6.1). These contributions (briefly) are (1) a new and

arguably better method than firm-focused interlocks for measuring inter-corporate

ties, (2) evidence of a positive association between board connections and market-

based measures of firm performance, (3) evidence that formal inter-corporate board

ties matter to financial markets more than social ties, and finally (4) evidence that

directors direct ties are more strongly associated with company performance than

indirect ties.

1.3 Justification for the research This research focuses on the boards of directors’ of Australia’s largest companies

and their performance. Companies make up a major contribution to Australia’s

economy, and boards of directors’ are the ultimate decision making body of listed

companies (see section 2.2). Ultimately this research may provide practical

direction to boards to enhance the performance of the companies they govern.

Director interlocks are regarded as a important mechanism by which boards can

access resources through their inter-corporate connections. However in spite of

strong theoretical support for the benefits of interlocks (see section 3.2.4), research

into links between interlocks and firm value (or performance) have produced mixed

results (Carrington, 1981; Fligstein & Brantley, 1992; Mizruchi & Stearns, 1988).

Some researchers have suggested that reverse causality may be a more probable

outcome, that is higher performing companies may lead to more interlocks. This

suggests that directors seek to join the boards of well performing companies to

advance their careers or reputation (Zajac, 1988). Regardless of the association, a

better understanding of interlocks and inter-corporate connections and how they

relate to corporate performance is required. This is expected to be of interest not

only to researchers, but to practitioners and regulators as well.

6

1.4 Methodology In this section I provide an introduction and overview of my approach to this

research. A detailed account is contained in Chapter 4, including my research

philosophy (section 4.2.1), the research approach (section 4.2.2), and research

method (section 4.3).

I adopt a positivist approach to this study (see section 4.2.2), as essentially I believe

there is an observable and measurable social reality waiting to be discovered

(Saunders, Lewis, & Thornhill, 2003). I employ regression analysis to test the

relationships between board connections (which represent the opportunity network

of connections available to the board) and company performance. Data are drawn

from publicly available archival sources. Full details of the sampling and data

collection methods are discussed in sections 4.3.3 and 4.3.5 respectively.

To operationalise board connectivity measures (i.e. the independent variable used in

the analysis) I have used Social Network Analysis (SNA). SNA is a technique

developed within the social sciences (see section 4.3.5.3) to analyse social relations

and inter-personal ties. In this study, I measure ties at the individual director level

and develop a board-level measure to determine the impact on corporate

performance. Since I have measured both direct and indirect ties as well as the

formal inter-corporate network and the combined formal and social network, I use

four different board connectivity measures to represent alternative measures of the

board opportunity networks. Details of other measures and variables used in the

analysis are discussed in section 4.3.4.

1.5 Outline of thesis The remainder of the thesis comprises six chapters. Chapter 2 discusses the

institutional and legal background in which listed companies operate in Australia. It

outlines the major theories of corporate governance and discusses boards of directors

and the important roles they play in governing companies. Chapter 3 details the

research framework for my study based on my review of key literatures in this area

and culminates in development of the research question and hypotheses. In Chapter

4, I discuss my research approach and the research design. I present the methods

7

used to answer the research questions and test the hypotheses. I then proceed to

collecting the data required to undertake the analysis. Chapter 5 presents the

analysis of data. In Chapter 6, I interpret and discuss the results and findings and

consider major conclusions that can be drawn from this research program in its

entirety. I further discuss the implications which can be drawn from these

conclusions and consider further research agendas which may be developed from,

and extend, the knowledge gained in this study.

1.6 Definitions As definitions adopted by researchers are often not uniform (Perry, 1998), the

following list defines terms I used throughout this thesis:

Board of Directors or Board A body of elected or appointed persons who jointly oversee the activities of a company.

Board Opportunity Network (BON) A measure of ties by a company board (through its directors) to all other (top-105) company directors, accessible within the directors’ inter-corporate network.

Director A person appointed under Australia’s Corporations Act (2001) to oversee the activities of a company.

Dyad From Social Network Analysis (SNA), the most simple network relation comprises ties between two actors.

Degree of separation, degree-1 or degree-2

The least number of ties required to connect two persons (directors) in a network. Where persons have a direct connection through serving on the same board, or membership of the same club, this is referred to as 1 degree of separation or degree-1. Where there is no direct connection between the persons, but they are connected through another (third) person, this is referred to as 2 degrees of separation or degree-2.

Director’s formal network

The network of direct inter-corporate ties created by a person holding a directorship on the boards of one or more companies.

8

Director social network

The network of direct inter-personal social ties that exist between directors (excluding their formal network ties) and include social, professional, government, community and other business ties.

External Director, Outside Director or non-executive director

A person who serves on the board of a company but who is not an employee of the company, referred to throughout this study as a non-executive director.

Formal opportunity network A measure of potential ties within the directors’ formal network through which social capital is accessible. This includes ties at degree-1 and degree-2. Note: ties at degree-1 only represent formal structural social capital (see below).

Formal structural social capital A measure of potential ties within the directors’ formal network through which social capital is accessible at degree-1.

Internal Director, Inside Director or Executive director

A person appointed to the company board and who is also an employee of the company, referred to throughout this study as an executive director.

Independent Director A director who is independent of the management of the company and free of any business or other relationship that could materially interfere (or be seen to interfere) with the exercise of their unfettered and independent judgment2.

Indirect tie A tie between two actors which occurs through other actors (third persons) and not directly.

Listed Public Company A company registered in Australia under Australia’s Corporations Act (2001).

Opportunity network Potential ties within a network through which social capital is accessible (can be either through a formal network or a total (formal and social) network).

Total opportunity network Refers to social capital which is accessible through the total (formal and social) network by both direct and indirect ties. This includes ties at degree-1 (structural social capital) and degree-2.

Total structural social capital Refers to social capital which is accessible through the total (formal and social) network by direct ties only.

2 Definition adopted from the ASX Corporate Governance Council (2003)

9

1.7 Delimitations of scope and key assumptions Delimitations define explicit boundaries around the research program and key

assumptions made which together may limit the application of this research and need

to be clearly expressed (Perry, 1998, p. 19).

First, this research is limited to corporate governance and is applicable to corporate

entities only. Other business structures (including partnerships, unincorporated

associations, not for profit associations, government authorities), although they may

play an important role in the modern business environment were not included in the

population of interest.

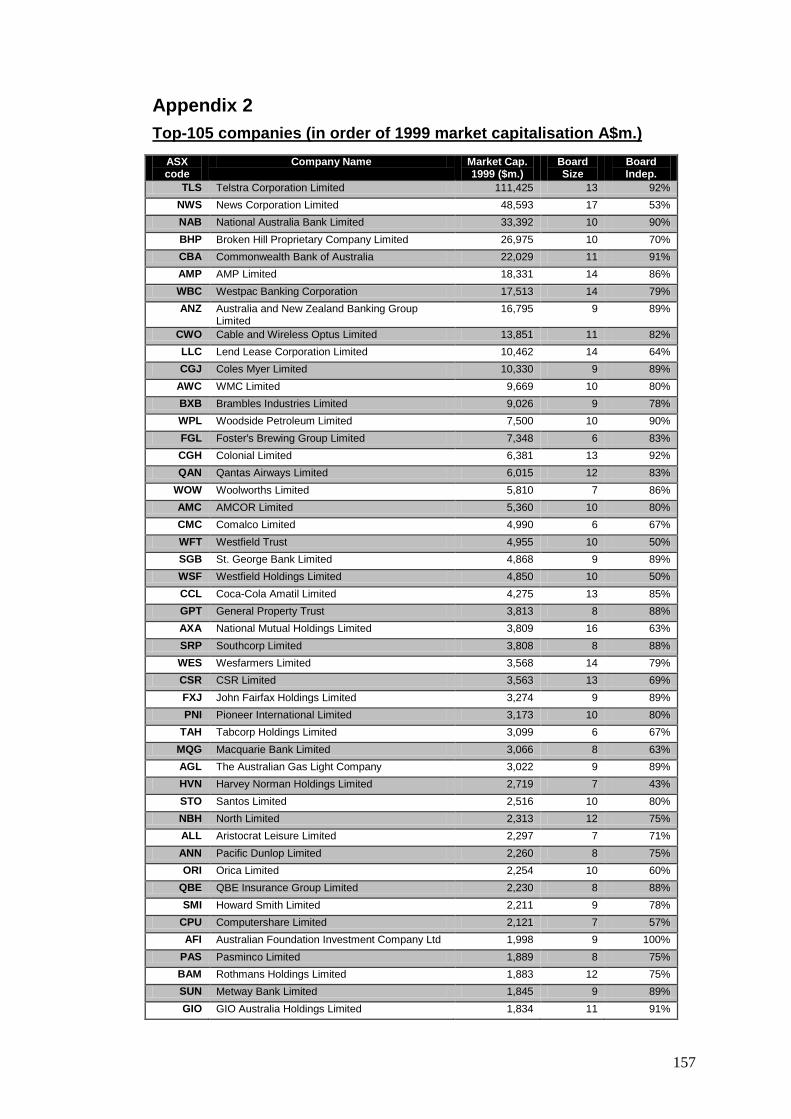

Second, the study relates to a specific population, which are the largest Australian

listed companies in 1999 (measured by their market capitalisation). I cover

companies in all industries, but have excluded companies that operate in Australia

but are not registered in Australia. The top-105 largest companies in Australia are

selected as an important network to study, due to their economic significance in

Australia and the apparent importance and regular reference to this particular group.

The ASX 100 companies represent Australia’s premier large capitalisation

companies3

Third, this study focuses on company boards made up of serving directors in 1999. I

do not consider past directors who are no longer serving on the board or other

company officers who are not serving in a director’s capacity. For example

company secretaries have been excluded.

.

Fourth, the inter-corporate director network comprises all directors serving on the

boards of the top-105 companies. While I have been able to accurately determine

who knows who through an analysis of the top-105 directors, I cannot be assured

that all other direct and indirect (‘friend of a friend’) connections will be collected.

This is because there may be many other organisations both corporate and social that

are not included in my analysis. For example, directors may know each other

through other formal business connections including companies other than those in

the top-105 listed. To capture all business and corporate memberships would be a

3 InvestSmart website http://www.investsmart.com.au/shares/indices_details.asp accessed 2 August 2009

10

considerable task and beyond the scope and resources (primarily time and

computing power) available for a master’s thesis. For instance in June 2008 there

were 2226 listed companies in Australia alone.

Fifth, I have captured directors’ social memberships data from public sources to

which they have declared their social memberships. I have assumed that directors

will declare social connections they consider important them, and this will be a good

proxy for their social opportunity network. However, I do not expect to have

collected all significant social connections through which the directors are able to

access social capital. For instance family ties, religious ties and school ties are

considered important social ties (Nahapiet & Ghoshal, 1998) but have not been

specifically addressed.

Finally, and perhaps the most significant limitation in this thesis lies in my measure

of directors’ social capital. I measure the size of directors’ opportunity networks for

my independent variable. Opportunity networks are used as a proxy for directors’

social capital. Opportunity networks are ties (either direct or indirect) between

directors and represent a network through which social capital is accessible.

Therefore, opportunity networks represent potential social capital and assume that

all the bonds between directors are positive and capable of generating social capital.

However, this may not always be the case. As discussed in section 3.3.3 opportunity

networks are derived from structural social capital (ties) which represent one of the

three dimensions to social capital (Nahapiet & Ghoshal, 1998). Measurement of the

nature and strength of the bonds between directors in the network is specifically

excluded from the scope of this thesis.

1.8 Conclusion In this Chapter, I laid down the foundations for this research. I provide a

background to the study in section 1.1 and introduce the research problem and

research issues (section 1.2). Section 1.3 explains the importance of the research

within the corporate governance context. A brief introduction to the methodology

used is discussed in section 1.4. Finally this chapter concludes with a road map for

the thesis, definitions, and discusses any key delimitations.

11

In Chapter 2, I provide an overview of companies, boards and governance within

which this thesis is centred.

12

Chapter 2 Companies, boards and governance

2.1 Introduction Any relationship between the opportunity networks of company boards and

performance needs to be understood in the context of the institutional environment

in which they operate. This chapter briefly describes the corporate legal and

institutional environment in Australia in four parts. First, I describe the legal

framework for companies, boards and directors in Australia and then discuss the

importance of corporate governance in general. Second, I introduce four main

governance theories and their application to both boards and companies. These

theories are important to this thesis and I draw on them during the study. This

Chapter does not provide an exhaustive treatment of these issues. Rather it provides

important context by describing the complex environment relevant to this study.

Thirdly, I discuss the importance of boards and the various roles that they play in

controlling and governing corporations. Finally, I discuss board structure and

demographics and their significance of to this research agenda. Board structure and

demographics is related to how boards perform in the roles they play and I draw on

this when selecting control variables for this study.

2.2 Companies and directors’ legal obligations Companies are important to the Australian economy and society in general, at June

2008 the market capitalisation of companies listed on the ASX is estimated at $1.29

trillion. One of the key reasons which have led to the success of the company

organisational form is that they can be registered with limited legal liability. That is,

the financial liability of the members (shareholders) can be capped. Legal liability

reduces the down-side risk of ownership in companies to the members. If the

company fails the members may only be liable up to the nominal value of their

shares.

Companies in Australia, like most nations, have a separate legal status and are

survivable independently of their owners. In Australia most companies are now

13

established under the provisions of the federal Corporations Act (2001). This

research is particularly concerned with company boards of directors. A company

director is broadly defined in s 9 of the Corporations Act 2001 as:

(a) A person who: (i) Is appointed to the position of director or (ii) Is appointed to the position of an alternate director and is acting in

that capacity; regardless of the name that is given to their position.

Under previous laws (i.e. state laws and UK colonial law) directors were charged

with a small number of legal obligations and their roles were viewed from a

legalistic perspective. However today, under the Corporations Act 2001, boards’

and directors’ powers are derived from the company’s constitution (which all

companies are required to have). The company constitution is an important

mechanism by which members can to safeguard their interests and exercise some

control over their investments. Companies can either write (and adopt) their own

constitution, or they can adopt the default constitution (referred to as the replaceable

rules (s.135)) within the Corporations Act 2001. Where the default constitution is

adopted, the board’s power is derived from a replaceable rule under s198A of

Corporations Act 2001 (Power of directors) which states:

(1) The business of a company is to be managed by or under the direction of the directors.

(2) The directors may exercise all the powers of the company except any powers that this Act or the company’s constitution (if any) requires the company to exercise in general meeting.

In addition to their obligations under the company’s constitution, directors’

obligations have continued to increase due to a range of specific legislation (taxation

laws, occupational health and safety laws, environmental laws, securities laws and

insolvency laws). The legal obligations of directors and officers are contained in

both case law (general law) and under statutory (state and federal) laws. These

obligations can be broadly categorized as four types of duties (1) Fiduciary duties,

(2) Due care and diligence (3) Contractual obligations and (4) other legal

obligations (Psaros, 2009). These duties are briefly discussed below:

14

Fiduciary duties:

1. a duty to act in good faith (s.181 Corporation Act 2001)

Directors have an obligation to act to the best of their ability in

serving the interests of the company. Fiduciary duties bring in four main themes,

which have been codified in legislation. These are:

2. a duty to use their powers for proper purpose (s.182 Corporation Act 2001)

3. a duty to avoid conflicts of interest, this might occur where a director

transacts with the company (ss. 180, 181 and 182 Corporation Act 2001)

4. a duty not to misuse information (ss182 and 183 Corporation Act 2001)

In addition to fiduciary duties to shareholders, directors also have an obligation not

to permit the company to trade when they believe the company is insolvent (or likely

to become insolvent), s.588G Corporation Act 2001.

Due care and diligence: Directors have a duty to act with care and diligence in the

performance of their duties, s.180 Corporation Act 2001. If they are proven to be

negligent in performing their duties they may be liable to the company for loss

suffered.

Contractual obligations. Directors have contractual obligations with the companies

under the company’s constitution. They must perform their duties in accordance

with obligations.

Other legal obligations.

While most companies adopt the replaceable rules contained in s.198 A to C of the

Corporations Act (i.e. that the business is under the direction of directors), the board

cannot make every decision necessary to run the company. Thus, s198D of the

Corporations Act empowers directors to delegate authority and powers to

committees, individual directors, employees and other individuals. Nevertheless, the

boards of directors are held ultimately responsible for the exercise of these powers

Specific legislated obligations, with some involving

criminal penalties, are contained on other state and federal legislative provisions,

e.g. occupational health and safety laws and environmental laws.

15

(subject to the constitution), and are therefore responsible to ensure any delegations

are appropriate and regularly monitored (s190 (1)).

Today, board roles are now seen from a wider corporate governance perspective

than simply their legal obligations, this is discussed in the following sections.

2.3 Corporate governance and theories

2.3.1 Governance overview

Definitions of corporate governance vary with the perspectives of the authors

(Gillan, 2006). Many follow Shleifer and Vishny (1997) who define corporate

governance from a financial perspective as the ways in which suppliers of finance to

corporations assure themselves of getting a return on their investment. In contrast,

Gillan and Starks (1998) take a legal perspective and define corporate governance as

the system of laws, rules and factors that control operations at a company. Daily,

Dalton and Cannella (2003, p. 371) adopt a broad perspective and define governance

as “the determination of the broad uses to which organizational resources will be

deployed and the resolution of conflicts among the myriad of participants in

organizations”. An authoritative definition, which I adopt in this study, is provided

by the ASX Corporate Governance Council (2007, p. 3) as:

The framework of rules, relationships, systems and processes within and by which authority is exercised and controlled in corporations. It encompasses the mechanisms by which companies , and those in control, are held to account. Corporate governance influences how the objectives of the company are set and achieved, how risk is monitored and assessed and how performance is optimised. Good corporate governance structures encourage companies to create value (through entrepreneurialism, innovation, development and exploration) and provide accountability and control systems commensurate with the risks involved.

Irrespective of the definition of corporate governance, researchers have generally

adopted either an internal or external perspective when studying corporate

governance mechanisms. Internal governance mechanisms concentrate on

management (who decide the assets in which the firm will invest and how they will

be financed) and the board of directors who are charged with overseeing and

advising management. External governance mechanisms introduce elements which

arise from a firm’s need to raise capital and highlights a separation between capital

16

providers and those who manage the firm. Gillan (2006) proposes an integrated

governance framework that synthesises these mechanisms. This framework sets out

five categories of internal governance: boards of directors, managerial incentives,

capital structure, by-laws and charter provisions, and internal control systems.

Similarly, Gillan (2006) provides five categories of external governance: law and

regulation, markets (capital/ corporate control/ labour/ product), capital information

markets, market for professional services, and other private sources of external

oversight.

Strong governance mechanisms are thought to ensure that corporate activity is

effectively scrutinized, and that companies behave as good public citizens (Huse,

2007). Corporate governance mechanisms therefore can have a significant impact

on the economic performance of countries. Where governance mechanisms are

weak this can lead to substantial economic problems. It is in the public interest to

ensure that effective corporate governance mechanisms exist as this will enable

firms to raise external capital at the lowest cost. For example, in Italy where

corporate governance is weak, flows of external capital to firms are retarded and

similarly in Russia (where weakness of corporate governance has lead to a

substantial diversion of assets by managers of many privatized firms) external

capital supply to firms is virtually non-existent (Huse, 2007).

Public pressure on governments by their constituents can force changes to be made

to the Corporations Law, and other specific corporate related legislation in such

areas as environment and health and safety. External governance mechanisms

comprising economic and legal institutions are altered through the political process,

particularly when there is sufficient public outcry. The recent global financial crisis

of 2007 has already lead to number of corporate causalities (or near causalities) in

Australia including ABC Learning Centres, Rams Home Loans and Centro

Properties which the Australian regulators will monitor. Similarly, after major

corporate collapses in the early 2000’s including HIH, One-Tel, Harris-Scarfe and

Ansett, the Clerp 9 changes were introduced to the Corporations Act 2001.

Boards of directors are regarded by many as the lynchpin of internal corporate

governance (Gillan, 2006). This is understandable given that directors have the

17

ultimate corporate decision making power, the responsibility to oversight corporate

operations, and the fiduciary duty to act in the best interests of the corporation.

Several governance theories have developed to provide a theoretical perspective for

application in governance studies of corporate organisations. Many modern

corporations, particularly companies listed on the stock exchange are characterised

by factors like: their large size and complexity, significant assets or access to assets

and wealth, separation of ownership and management, a large number (6 and more)

of directors on their boards, independent directors on their boards, significant

economic power and many thousands on small shareholders. I concentrate on four

of the predominant governance theories most relevant to large (listed) corporations

and to this research of the top-105 listed companies in Australia, these are discussed

in the following sections together with their relevance to this research. These

theories are agency and contracting theory, stewardship theory, resource dependence

theory and the resource based view of the firm.

2.3.2 Agency theory The agency problem occurred following a separation of ownership and control in

companies (Berle & Means, 1932), and is arguably the most dominant governance

theory having its roots back to the ‘Wealth of Nations’ (Smith, 1776). In simple

terms, Agency theory involves one person (i.e. the principal) delegating work and

authority to another person (i.e. the agent) so that the principal is reliant on the agent

for their future well being (Eisenhardt, 1989). Agency costs arise from this

relationship and represent the costs that occur when the interests of the principal and

the agent are misaligned and the bonding costs for establishing relationship

(discussed below). For example, the agent may not perform in a way that the

principal had intended. Agency theory has been applied to corporate governance to

help understand the relationships between managers of the firm and the shareholders

whose interests are arguably represented by the board of directors.4

4 Under the theory of the firm (Coase, 1937) the firm is viewed as a set of contracts with agents to secure its factors of production. In large corporations where responsibility for managing the companies is delegated by the board to the professional managers, contracts are established for management labour.

With respect to

corporate governance, the challenge for agency theorists is to reduce agency costs by

aligning the interests of managers with those of the owners (Fama, 1980; Fama &

18

Jensen, 1983; Jensen & Meckling, 1976). Ideally, this will encourage managers to

produce the best returns for themselves and shareholders.

Agency costs (in the typical corporate form) are thought to be created in three main

ways, these are through (1) moral hazard, (2) risk taking preferences and (3)

principal centred problems. Firstly, moral hazard is considered the most common

conceptualisation of the agency problem (Hendry, 2002) that argues that managers

can be self interested entrepreneurs and opportunists who may make decisions that

benefit themselves rather than in the interests of shareholders (Fama & Jensen,

1983). This behaviour may manifest itself in several ways including using the

owner’s funds to acquire perquisites, paying excessive remuneration or otherwise

make operating decisions which may not be in the best interests of shareholders

(Jensen & Meckling, 1976). Agency theory also recognises that managers will

generally possess greater knowledge and expertise of the firm, and are thus in an

advantaged position to the owners. This is referred to as information asymmetry,

and may enable managers to pursue self interested action at the expense of

shareholders (Healy. & Palepu, 2001). Second, risk taking preferences centre on the

different risk profiles of the principal and agent (Jensen & Meckling, 1976). This

depends on the general risk sharing approach between principals and managers, that

is the sharing of residual claims and how this effects risk bearing by residual

claimants (Fama & Jensen, 1983). Shareholders generally want to encourage and

motivate managers to take risk and produce higher returns for their investments

rather than produce normal returns. This includes the take on of high risk capital

projects that have the potential to yield super-normal returns, but are also associated

with higher risk and the potential for disaster. Residual claims (including super-

normal profits or losses) would flow to the shareholders. Modern capital markets

allow shareholders to spread (minimize) their risk to acceptable levels through

diversified share portfolios (Fama, 1980; Jensen & Meckling, 1976). However,

managers may have little to gain from undertaking high risk projects, as these

projects can involve significant career risks and potential reputation loss.

Consequently managers are considered to be more risk averse in their decision

making than diversified shareholders (Fama, 1980). Finally, principal centred

problems arise where the agent, selected by the principal, cannot perform the role

required of them (Eisenhardt, 1989). This can arise from adverse selection by the

19

principal (Eisenhardt, 1989) and honest incompetence of the agent (Hendry, 2002)

and are errors made by the principal in agent selection.

Economic inefficiencies in the principal and agent relationship are referred to as

agency costs. Three of the predominant methods used to reduce or control agency

costs in the manager and owner (shareholder) relationship are: (1) contracts, (2)

disclosure, (3) monitoring of management. These are briefly discussed below.

Contracts, which are compensation agreements between management and the

shareholders, are used to motivate the agent by focussing on desired behaviours and

outcomes (Jensen & Meckling, 1976). In essence, financial incentives are offered to

the agent to encourage them to meet the shareholders’ goals. However, contracts

themselves can give rise to other type of agency costs, because these contracts are

not costlessly written and enforced (Fama & Jensen, 1983). These agency costs

include the costs of structuring, monitoring and bonding a set of contracts among

agents with conflicting interests and also include the value of output lost where the

costs of full enforcement of contracts exceed the benefits (Jensen & Meckling,

1976).

Disclosure requires management to provide relevant information to shareholders

through either voluntary or through mandatory requirements. This mechanism is

designed to reduce information asymmetry. Since managers have access to more

information than the shareholders they have a clear power advantage over

shareholders (Healy. & Palepu, 2001). Disclosing relevant information is thought to

facilitate shareholder monitoring of firm performance.

Monitoring of management by the board of directors (on behalf of the shareholders)

is regarded as a key mechanism to reduce agency costs (Fama, 1980). However,

legally shareholders do not have any direct influence over the managers and they do

not have a claim to the position of principal under an agency relationship (Aglietta,

2008). Shareholders effectively have no legal rights to exercise control over the

corporation (Bainbridge, 2003) as that is the directors’ legal duty (see section 2.2).

Management are hired by the board and answerable to the board for their

performance, and the board has a fiduciary duty to the company to monitor their

performance.

20

In summary, Agency theory (a subset of contracting theory) has been applied to

understand and predict management motivations (following the separation of the

ownership and management in many large companies). Various mechanisms have

been developed to control and mitigate agency problems. Some researchers consider

that agency problems are primarily based on the assumption of management

exploiting their advantaged position, however this is not generally accepted.

Stewardship theory, which I discuss in the next section, is based on different

assumptions which some researchers claim is almost diametrically opposed to

Agency theory.

2.3.3 Stewardship theory

Stewardship theory is regarded as an alternative to agency theory that developed in

the 1990’s as a response to the dominance of agency theory’s influence on corporate

governance research (Donaldson, 1990; Huse, 2007). Whereas agency theory has

primarily developed on the assumption of managerial opportunism, the core concept

in stewardship theory is that managers are trustworthy stewards, whom boards

should support and mentor. Stewardship theory assumes that managers are

collectivistic and motivated by intrinsic rewards such as achievement and

satisfaction in their work rather than extrinsic rewards such as financial incentives.

Donaldson (1990, p. 377) stated that ‘there is no conflict of interest between

managers and owners and the desideratum of governance structure is to find an

organisational structure that allows coordination to be achieved more effectively’.

The challenge for stewardship theorists is to develop organisational structures that

facilitate and empower managers. Stewardship theory is consistent with the classic

motivational theory, Theory ‘Y’, developed by McGregor (1960) whereby managers

are characterised as hard working, selfless and honest. In contrast McGregor’s

theory ‘X’ views workers as lazy, disloyal and opportunistic and self interested, a

situation analogous to the assumptions underlying agency theory. In contrast with

proponents of agency theory, stewardship theorists argue that agency costs would be

minimized as a matter of course, as senior managers keen to protect their reputations

would not jeopardize them by abusing their power to the detriment of shareholders

(Donaldson & Davis, 1994).

21

2.3.4 Resource dependence theory In contrast to both stewardship and agency theories and their management

motivation focus, resource dependence theory attempts to explain how firms acquire

and manage their dependence on resources available through the external

environment (Hillman & Dalziel, 2003; Pfeffer & Salancik, 1978). A firm’s

survival is regarded as contingent on how effectively the firm performs in its ability

to acquire and control external resources (Aldrich, 1979; Aldrich & Pfeffer, 1976).

Resource dependence theory is premised on three key assumptions or concepts

(Pfeffer & Salancik, 2003) these are (1) resource interdependence, (2) external social

constraint, and (3) organisational adaptation. Resource dependence theory is based

on the idea that in social systems and social interactions, interdependence exists

whenever an actor does not entirely control all of the conditions necessary for

achieving an action, or for obtaining the desired outcome desired from the action

(Pfeffer & Salancik, 1978). Thus, a firm is linked to its external environment

whereby organizations are embedded in a network of interdependences and social

relationships (Granovetter, 1985). These interdependencies with other organizations

and the environment are affected by social power (Blau, 1964) and with economic

efficiency and rationality (Williamson, 1995). Organisations are constrained by

their situations and affected by their environments. Thus, firm performance (or

effectiveness) can be viewed as a derivative of how well a firm manages the

demands placed upon it. In particular, effectiveness depends on a firm’s ability to

manage the interest groups on whom it depends for its resources and support

(Pfeffer, 1972). The key to organisational survival is acquiring and maintaining

adequate resources, include financial, physical, and information resources (Pfeffer &

Salancik, 2003).

Consequently, organisations develop and use various strategies to cope with external

constraints (i.e. to avoid, reduce or manage resource dependence or interdependence

(Pfeffer & Salancik, 1978)). These strategies are thought to provide at least

temporary autonomy. Pfeffer and Salancik (2003) categorise these strategies into

four main groups, namely:

22

1. Adapting to or avoiding external demands such as implementing new electronic

commerce business systems. This strategy exclusively concentrates on

improving the efficiency of the internal transformation processes (Pfeffer,

1972).

2. Altering the patterns of interdependence through growth, merger or acquisition.

Business mergers and takeovers are common practice among Australia’s listed

public companies.

3. Establishing alliances and collective structures such as interlocking directorships

(Mizruchi, 1996), co-option (Selznick, 1949; Zald, 1967), joint ventures, trade

associations or similar means of association and influence (Guetzkow, 1966).

For instance Selznick found that co-option onto the governing board was used

successfully by the Tennessee Valley Authority to partially neutralize strong

opposition from hostile groups. In this way, the board can be viewed as an

administrative body linking the firm with its environment. As a ‘boundary

spanner’, the board can assist the firm to acquire important resources from its

environment and thereby enable the firm to either reduce its dependence on

external stakeholders or protect it from external threats.

4. Intervention in public policy and political process. This strategy can result in

altering the definitions of legitimacy and public opinion. For instance, Schuler

et. al. (2002) found that companies which were heavily reliant on government

contracts lobbied and contributed to campaigns which maintained close ties to

the policymakers responsible for their livelihoods. A notable example of

political lobbying in Australia over the past 10 years has been by Telstra in an

attempt to retain its monopoly position in key areas of the Australian telephony

and communications infrastructure.

2.3.5 Resource based view of the firm

Closely allied to resource dependence theory is the resource based view (RBV) of

the firm. Whereas resource dependence concentrates on how firms rely on the

external environment, the RBV posits that the firm is a bundle of resources,

knowledge, competencies and capabilities which can be used to create value

(Barney, 1991). By developing these unique and inimitable resources a firm can

develop and sustain a competitive advantage (Wernerfelt, 1984). The basic

23

assumptions made in resource based theory are that resources are distributed

heterogeneously across firms and that resources which are productive cannot be

transferred across firms without cost.

In order to produce a sustainable competitive advantage a firm should seek ownership of

firm-specific resources that are valuable, rare, inimitable and non-substitutable (Barney,

1991). Resources with these properties are valuable and can be used to exploit

opportunities and/or neutralize threats in a firm’s environment.

From the resource based perspective, the board of directors is a potentially valuable

resource for the firm and its management. A board of directors could meet these

required attributes and so be considered a strategic resource when governance choices

affect the creation of economic rents. In particular, where boards can provide a firm

access to scarce, valuable and non-replicable resources, it can become a valuable

resource, particularly when compared to a board that focuses mainly on monitoring and

minimizing agency costs (Huse, 2007). Thus, a board’s capabilities may be a valuable

resource that cannot be easily duplicated or substituted and so may provide the firm with

a distinct competitive advantage.

2.3.6 Summary of key governance theories and their importance to this thesis

In this section, I outlined four key theories of relevance to this study. First, I outlined

agency theory, then stewardship theory and resource dependence theory and then finally

the resource based view of the firm. These theories can be used to justify the perceived

roles of the directors and the board. For instance agency theorists who emphasise the

importance of the board’s role in monitoring and oversighting management would argue

for greater board independence, as this will strengthen this role. In contrast, stewardship

theorists would focus on structures that facilitate and empower would perceive the

board’s role as one of providing service and guidance to management. Consequently

stewardship theorists would take the view that a majority of executive directors will

yield superior firm performance, as executive directors will understand the business

better than outside directors and can offer more informed counsel (Donaldson, 1990;

Donaldson & Davis, 1994), collaborative strategy formulation and mentorship.

Resource dependence theorists view the role of boards as one of providing access to

24

resources, and would to support greater board connections. These roles are further

discussed in section 2.4.

2.4 Boards of directors - roles and theories

2.4.1 Overview of board roles Boards of directors, as the ultimate corporate decision makers in the firm, have been

the subject of a significant research effort the past two decades (Nicholson & Kiel,

2007; Pettigrew, 1992; Zahra & Pearce, 1989). However attempts to link boards to

the performance of the companies they govern have met with mixed results

(Hillman & Dalziel, 2003; Johnson et al., 1996).

Much of the corporate governance research agenda has focused on defining and

reviewing how board attributes are related to company effectiveness. Reviews of the

literature are near unanimous that there is no uniform relationship between boards

and firm performance (Daily et al., 2003; Johnson et al., 1996). Instead, individual

projects have tended to focus on single mechanisms by which a board can affect firm

performance (i.e. they concentrate on a single board role). As a result, there is no

clearly agreed role set that a board follows (e.g. see Nicholson and Kiel, 2007 for a

summary and exception to single theory focus).

Most studies assume a board role (i.e. they do not directly measure the mechanism

by which boards are thought to affect corporate performance (Daily et al, 2003).

Rather, they use an input-output approach (Pfeffer, 1972) that seeks to link board

attributes (e.g. board composition, director characteristics, and governance process)

with firm performance. They assume that these will affect how well the board

functions in performing its three key roles of service, strategy (which includes

resource dependence) and control (Zahra & Pearce, 1989). Earlier research by Zahra

& Pearce (1989) has led to a framework which has generally been used by

researchers in their studies of boards and company performance. Zahra & Pearce

(1989) in their summary paper presented an integrated model of the links between

boards and company performance, including board attributes and roles. Their

integrated model combined four separate models based on different perceived

perspectives of the board, viz. legalistic, resource dependence, class hegemony and

25

agency theory. This model indicates that a relationship exists between board