Languages

Pages

Legal

Joseph L. Pagliari, Jr. Clinical Professor of Real Estate

May 2, 2013

Real Estate Research Institute

Discussion of: “Finding Cap Rates:

A Property Level Analysis of Commercial Real Estate Pricing”

1 An Outline of My Thoughts

OVERVIEW: – METHODOLOGY: My focus will not be on technique

– APPLICATIONS: My focus will be on theory & implementation: – income v. cash flow, – term structure of leases, – growth in income (&/or cash flow), – other fixed effects, – instrumental variables, and – investor sentiment.

– CONCLUSION: Less a criticism, more an emphasis on future research avenues

2 Better Intuition about Gordon’s Dividend Discount Model

SUBJECT PAPER: – RESTATEMENT OF GORDON MODEL:

DISCUSSANT COMMENT: – CORRECTION: However, Gordon’s model is based on cash flows:

NOIt ≠ Cash Flowt

– MODIFICATION : Would like to see the “cap ex” effects on yields

1 1Cap Ratet tt t t t

t t t

NOI NOIP r gr g P

+ += ⇒ = = −−

1 1 1 1Cash Flow Yieldt t t tt t t t

t t t

NOI CapEx NOI CapExP r gr g P

+ + + +− −= ⇒ = = −

−

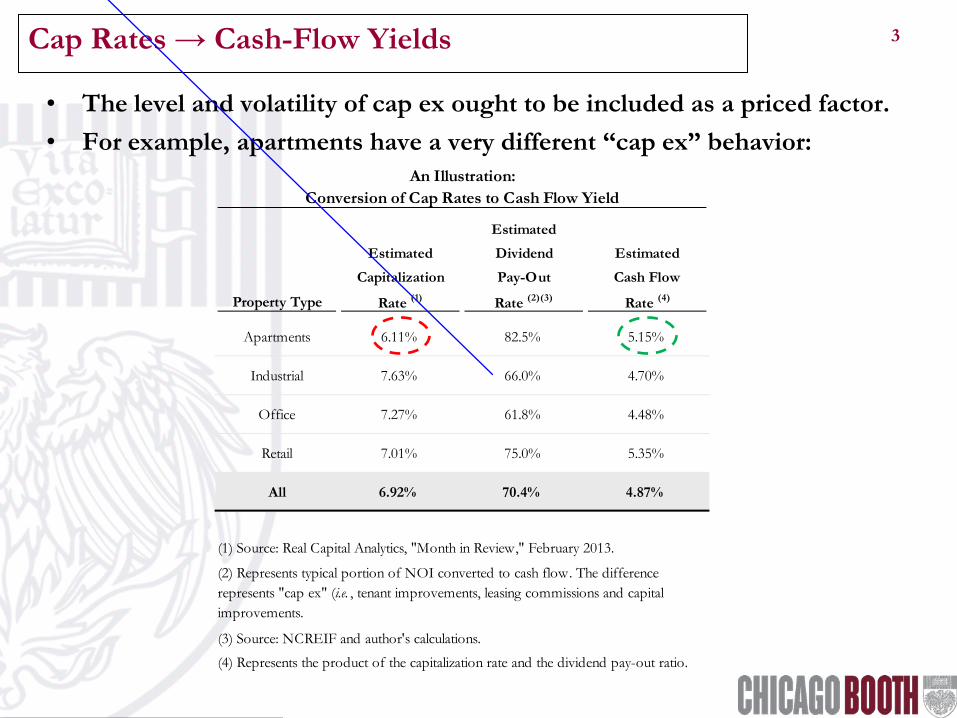

3 Cap Rates → Cash-Flow Yields

• The level and volatility of cap ex ought to be included as a priced factor. • For example, apartments have a very different “cap ex” behavior:

An Illustration:Conversion of Cap Rates to Cash Flow Yield

Estimated

Estimated Dividend Estimated

Capitalization Pay-Out Cash Flow

Property Type Rate (1) Rate (2)(3) Rate (4)

Apartments 6.11% 82.5% 5.15%

Industrial 7.63% 66.0% 4.70%

Office 7.27% 61.8% 4.48%

Retail 7.01% 75.0% 5.35%

All 6.92% 70.4% 4.87%

(1) Source: Real Capital Analytics, "Month in Review," February 2013.

(3) Source: NCREIF and author's calculations.

(4) Represents the product of the capitalization rate and the dividend pay-out ratio.

(2) Represents typical portion of NOI converted to cash flow. The difference represents "cap ex" (i.e. , tenant improvements, leasing commissions and capital improvements.

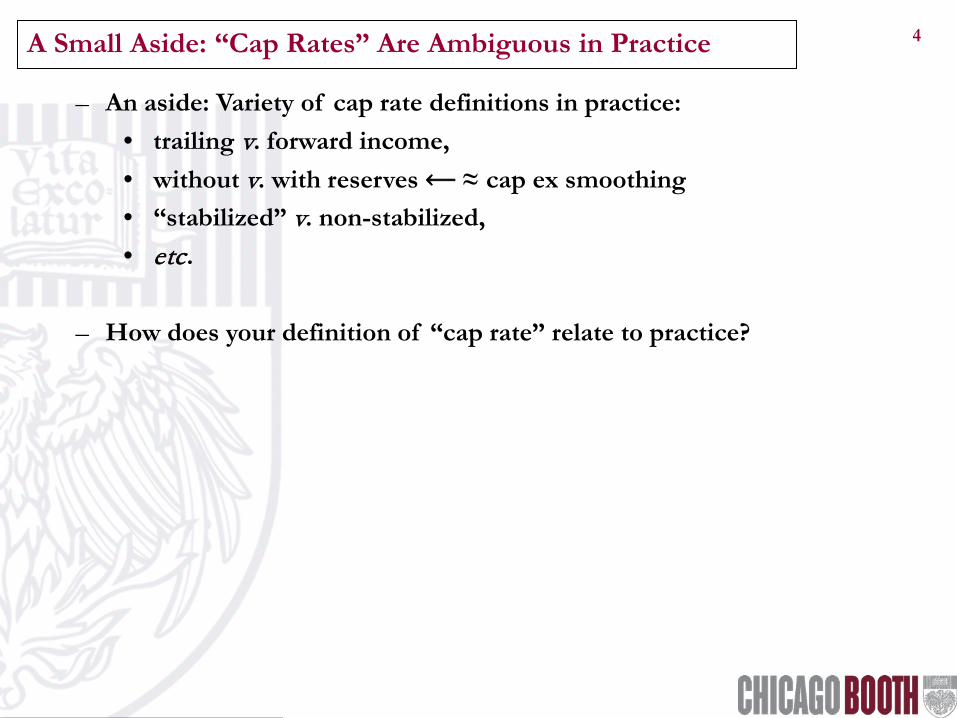

4 A Small Aside: “Cap Rates” Are Ambiguous in Practice

– An aside: Variety of cap rate definitions in practice: • trailing v. forward income, • without v. with reserves ⟵ ≈ cap ex smoothing • “stabilized” v. non-stabilized, • etc.

– How does your definition of “cap rate” relate to practice?

5 An Outline of My Thoughts

OVERVIEW: – METHODOLOGY: My focus will not be on technique

– APPLICATIONS: My focus will be on theory & implementation: – income v. cash flow, – term structure of leases, – growth in income (&/or cash flow), – other fixed effects, – instrumental variables, and – investor sentiment.

– CONCLUSION: Less a criticism, more an emphasis on future research avenues

6 Better Intuition about Gordon’s Dividend Discount Model

SUBJECT PAPER: – RESTATEMENT OF GORDON MODEL:

DISCUSSANT COMMENT: – WARNING: However, Gordon’s model is based on cash flows growing

at a constant rate. – This may be plausible for apartments, hotels and portfolios. – This may be implausible for individual industrial, office and

retail properties.

– MODIFICATION : What about lease maturity date(s)?

1 1Cap Ratet tt t t t

t t t

NOI NOIP r gr g P

+ += ⇒ = = −−

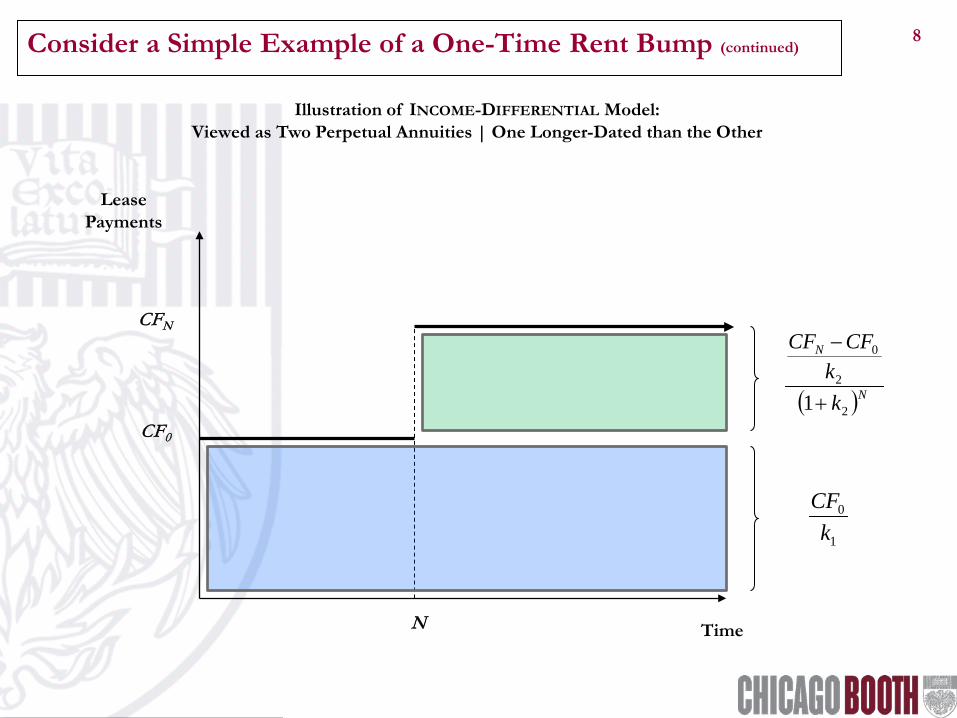

7 Consider a Simple Example of a One-Time Rent Bump

Lease Payments

CFN

CF0

N Time

8 Consider a Simple Example of a One-Time Rent Bump (continued)

Lease Payments

CFN

CF0

N Time

( )N

N

kk

CFCF

2

2

0

1+

−

1

0

kCF

Illustration of INCOME-DIFFERENTIAL Model: Viewed as Two Perpetual Annuities | One Longer-Dated than the Other

9 As Lease Maturity Dates Vary, “Cap Rates” Vary

– Consider: 10 < N ≤ 60 • Must solve for cap rate, given 10 < N ≤ 60 • where: P0 (= $100), rt (= 10%) and gt (= 2%) are constant across all

combinations

– Consider the two limiting cases: – 1) Constant rent growth:

• Cap rate = rt – gt = .10 - .02 = .08

– 2) No rent growth (N → ∞ ) • Cap rate = rt – gt = .10 - 0 = .10

10 As Lease Maturity Dates Vary, “Cap Rates” Vary (continued)

– Cap Rates vary purely as a function of N ; all other factors are held constant

11 An Outline of My Thoughts

OVERVIEW: – METHODOLOGY: My focus will not be on technique

– APPLICATIONS: My focus will be on theory & implementation: – income v. cash flow, – term structure of leases, – growth in income (&/or cash flow), – other fixed effects, – instrumental variables, and – investor sentiment.

– CONCLUSION: Less a criticism, more an emphasis on future research avenues

1 1 1 1Cash Flow Yieldt t t tt t t t

t t t

NOI CapEx NOI CapExP r gr g P

+ + + +− −= ⇒ = = −

−

12 What About Growth?!?!

– Clearly, cap rates can be greatly influenced by expected growth in future cash flows:

– Cap rates (or cash-flow yields) are positively correlated with returns – Longstanding story in mainstream finance:

Higgledy-piggledy growth (Little, 1962) Value v. growth (Lakonishok, Shleifer & Vishny, 1994)

• Real estate work in this area as well: • e.g., Plazzi, Torous & Valkanov (2011 RERI paper)

– Like cap ex, my concern is that a richer story can be produced by

empirically examining the pricing of the growth factor.

13 Let’s Explore Growth: Too Much of a Good Thing?

Atlanta

Austin

Baltimore

Boston

Charlotte

Cincinnati

Dallas

Denver

Detroit

Houston

Kansas City

Miami

Minneapolis

Nashville

New York

Orlando

Phoenix

Portland, OR

Riverside

Salt Lake City

San Diego

San Francisco

Seattle

St. Louis

Tampa

Washington, D.C.

y = -0.1281x2 + 0.3918x + 0.1456R² = 0.2465

(0.40)

(0.20)

-

0.20

0.40

0.60

0.80

-0.5 0 0.5 1 1.5 2 2.5 3 3.5 4

Shar

pe R

atio

Annual Household Formation(%)

Illustration of Relationship between Metro-Area Growth & Risk-Adjusted Returns:Household Formation v. Apartment Risk-Adjusted Return for the Ten-Year Period Ended in 2011

14 An Outline of My Thoughts

OVERVIEW: – METHODOLOGY: My focus will not be on technique

– APPLICATIONS: My focus will be on theory & implementation: – income v. cash flow, – term structure of leases, – growth in income (&/or cash flow), – other fixed effects, – instrumental variables, and – investor sentiment.

– CONCLUSION: Less a criticism, more an emphasis on future research avenues

15 What About Major v. Non-Major Markets?

• Prices and cap rates can significantly differ by quality

60%

70%

80%

90%

100%

110%

120%

130%

140%

$50

$75

$100

$125

$150

$175

$200

$225

$250

2000 2002 2003 2005 2006 2007 2009 2010 2011

Rat

io o

f N

on-M

ajor

to M

ajor

-Mar

ket A

sset

Val

ues

(Unl

ever

ed) A

sset

Val

ues f

or C

ore

Prop

ertie

sAsset Appreciation in Major v. Non-Major Markets

From December 2000 through January 2013

Major Markets

Non-Major Markets

Ratio of Non-Major to Major Markets

Source: Real Capital Analytics and Instructor's calculations.

16 An Outline of My Thoughts

OVERVIEW: – METHODOLOGY: My focus will not be on technique

– APPLICATIONS: My focus will be on theory & implementation: – income v. cash flow, – term structure of leases, – growth in income (&/or cash flow), – other fixed effects, – instrumental variables, and – investor sentiment.

– CONCLUSION: Less a criticism, more an emphasis on future research avenues

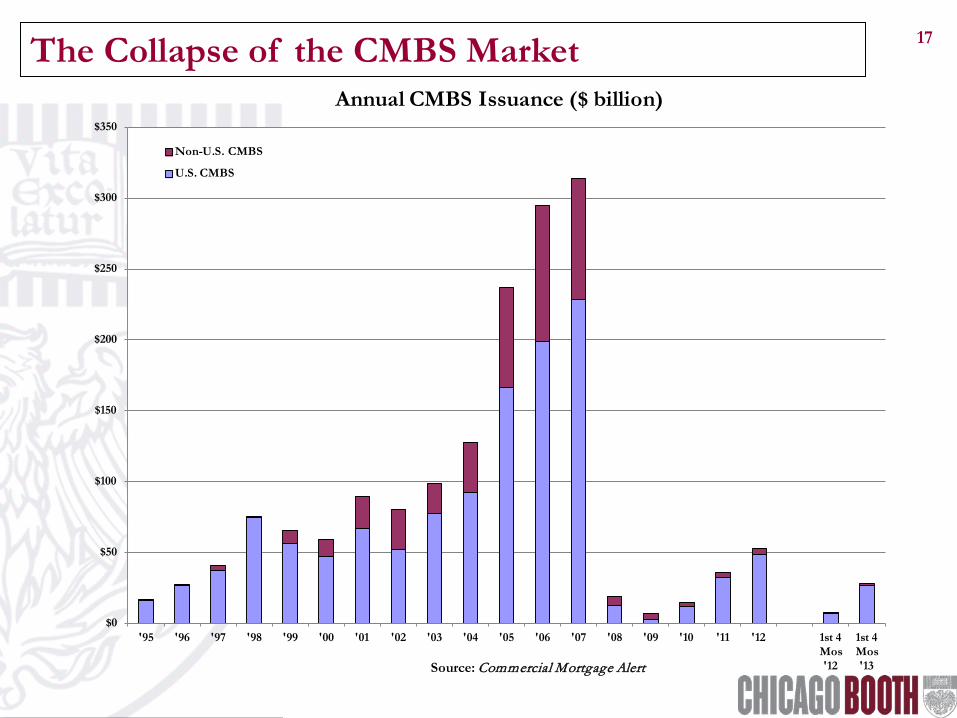

17 The Collapse of the CMBS Market

$0

$50

$100

$150

$200

$250

$300

$350

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 1st 4 Mos '12

1st 4 Mos '13

Annual CMBS Issuance ($ billion)

Non-U.S. CMBS

U.S. CMBS

Source: Commercial Mortgage Alert

18 How Can the CMBS Collapse Co-Exist with Falling Cap Rates?

Sources: NCREIF and instructor’s calculations.

2.5%

3.5%

4.5%

5.5%

6.5%

7.5%

8.5%

9.5%

$0

$50

$100

$150

$200

$250

$300

$350

$40019

78

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Cap

italiz

atio

n R

ate

Mar

ket V

alue

and

Res

cale

d N

OI

NCREIF Property Index: Market Values, Rescaled NOI and Capitalization Rates Based on a $100 Investment for the Period 1978 through 2012

Capitalization Rates (Right Axis) Market Values Rescaled NOI Average Capitalization Rate (Right Axis)

19 Pro-cyclical CMBS Underwriting Standards?

Source: Moody’s, “U.S. CMBS Review,” 3rd Quarter 2012.

• Another case of “here we go again”?

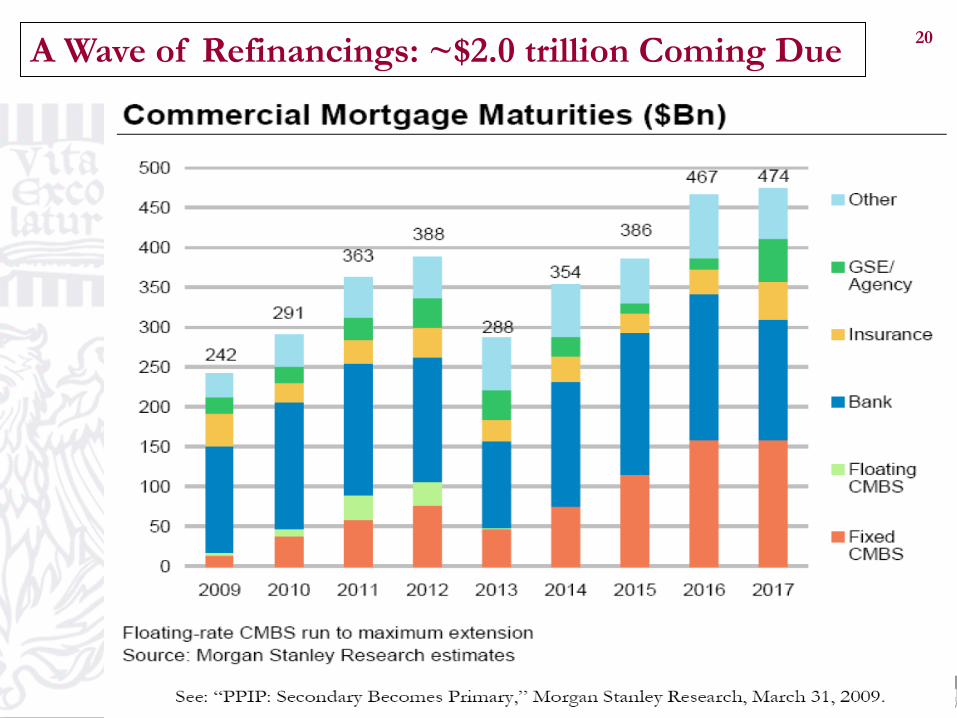

20 A Wave of Refinancings: ~$2.0 trillion Coming Due

21 An Outline of My Thoughts

OVERVIEW: – METHODOLOGY: My focus will not be on technique

– APPLICATIONS: My focus will be on theory & implementation: – income v. cash flow, – term structure of leases, – growth in income (&/or cash flow), – other fixed effects, – instrumental variables, and – investor sentiment.

– CONCLUSION: Less a criticism, more an emphasis on future research avenues

22 Better Intuition about Gordon’s Dividend Discount Model

SUBJECT PAPER: – EXPANSION OF GORDON MODEL:

where: st = investor sentiment and mt = mortgage supply DISCUSSANT COMMENT: – QUESTIONS:

• Isn’t “sentiment” subsumed in rt ? • Is it “sentiment” or is it:

• “return-chasing” (Jensen’s ex post α) behavior? • “momentum-chasing (ala Jegadeesh & Titman)?

( ) ( )1 1Cap Rate+ += ⇒ = = − + +−

t tt t t t t t

t t t

NOI NOIP r g f s g mr g P

Top Related