Languages

Pages

Legal

Disability Income InsuranceHELP PROTECT YOUR INCOME, FAMILY AND LIFESTYLE

10008

Disability Income Protection – Protecting Your Life

If something happens that keeps you from working,

what is your greatest concern?

• Assuring you can continue to provide for your family?

• Staying in your home as long as possible?

• Protecting your savings and retirement?

The majority of us need to work to provide for our loved ones and

to maintain our standard of living.

Injury or Illness – The Impact

The loss of income for an extended

period of time has the potential to

disrupt your plans and create a

gap between you and the things

that matter most:

• Your family

• Your home

• Your savings and retirement

Being injured or sick may

have an impact on your

loved ones and may put a

strain on your family,

especially other wage

earners and dependents

in your home.

Protecting Your Family

Protecting Your Home

For the majority of

people, their mortgage or

rent is their largest

monthly bill. A long-term

loss of income can put

your ability to pay in

jeopardy and opens the

possibility of losing your

home.

Protecting Your Savings and Retirement

The loss of income may

create a gap in your

savings and retirement

plan as funds are

depleted just to make

ends meet.

Planning the Course

Major life events often represent a milestone that causes people to take an inventory of their financial plan.

• Marriage

• Birth of child

• Home purchase

• Promotion

Milestones provide the opportunity to make sure coverage supports a new life situation.

Bridging Life’s Milestones

Imagine a long, narrow suspension bridge with guardrails along the sides and a slight dip in the middle.

How comfortable are you crossing from one side to the next?

• What about in bad weather?

• What about if we remove the guardrails?

Disability Income Insurance is the guardrail that keeps you and your loved ones moving safely from one part of your life to the next during stormy times.

Truth in NumbersMost people don’t believe they will need Disability Insurance.

However, consider these facts:• One in three Americans will experience a long-term disability prior to retirement

with the average disability claim being 2 ½ years* • Most disabilities don’t happen at work and therefore, Workers Compensation

won’t provide benefits **• More than 90% of disability issues are caused by illness – not injury. ***• And. . . more alarming, 65% of people admitted they couldn’t survive an income

loss for more than a year and didn’t know how they would survive.***

Disabilities happen more than we think and the majority of us are not adequately prepared to lose income for an extended period.

* America’s Health Insurance Plans (AHIP), Baby Boomer Awareness of Disability Risk Study (2008); most recent available** National Safety Council, Injury Facts (2011); most recent available*** CDA Consumer Disability Awareness Survey, Long-Term Disability Claims Review, Council for Disability Awareness (2010); most recent available

Sources of Income

If you suffer a disability that keeps you from working for an extended period, can you count on these resources?

• Vacation time

• Spouse’s income

• Savings

• Borrowing money

Question: How long would these resources reasonably cover your expenses?

Other Disability Income Sources

What about…

• Social Security disability insurance: The average payment is less than $1,130 a month*

• Workers’ compensation: Only 10 percent of disability cases are caused by eligible on-the-job injuries**

• Disability coverage from work: Do you know how it pays

In many cases, there is a gap between these income sources and basic expenses. Disability

Income Insurance is designed specifically to help cover those basic expenses while you recover

from illness or injury and protect the things that are most important to you.* Medicare and You Handbook (2012); most recent available** CDA Consumer Disability Awareness Survey, Long-Term Disability Claims Review, Council for Disability Awareness (2010); most recent available

Disability Insurance in Your Day

What is Disability Income Insurance?

An income protection policy that provides monthly benefits to supplement the loss of wages during injury or illness.

Mutual of Omaha Insurance Company (Mutual of Omaha) offers multiple products

• Accident Only Disability

• Short-Term Disability

• Long-Term Disability

Who Needs it?

• Anyone who is looking to

complete their income

protection plan

• Homeowners, married couples,

wage earners, business

owners, single parents

• Most individuals between ages

18 - 61 who earn an income

Protection at a Glance

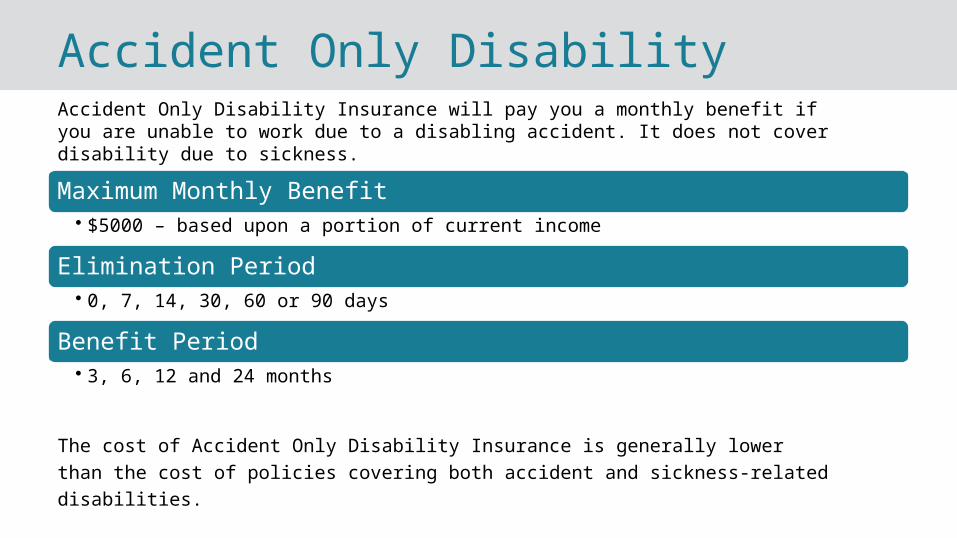

Accident Only DisabilityAccident Only Disability Insurance will pay you a monthly benefit if you are unable to work due to a disabling accident. It does not cover disability due to sickness.

The cost of Accident Only Disability Insurance is generally lower than the cost of policies

covering both accident and sickness-related disabilities.

Maximum Monthly Benefit• $5000 – based upon a portion of current income

Elimination Period• 0, 7, 14, 30, 60 or 90 days

Benefit Period• 3, 6, 12 and 24 months

Short-Term DisabilityShort-Term Disability Insurance provides coverage due to illness or injury and flexibility for those who are looking for immediate coverage that is portable.

Along with options to tailor your policy, there are a number of built-in benefits to this policy.

Maximum Monthly Benefit• $5000 – based upon a portion of current income

Elimination Period• 0/7, 7, 0/14, 14, 30, 60 or 90 days

Benefit Period• 3, 6, 12 and 24 months

Long-Term DisabilityLong-Term Disability Insurance is ideal for individuals who have resources that could cover living expenses for the first few months of a disability and want comprehensive, long-term benefits that would cover disability from an accident or sickness.

Additionally, Long-term Disability offers significantly more options to craft a policy tomeet unique needs.

Maximum Monthly Benefit• $12,000 – based upon a portion of current income

Elimination Period• 60, 90, 180 or 365 days

Benefit Period• 2, 5, 10 years and up to age 67

Next Steps

We have Protection that’s Right for YOU

Disability Income Insurance offers policies based upon your occupation and protection needs. Mutual of Omaha offers a number of solutions and optional benefits to meet your needs. I can help you:

• Assess your situation

• Understand your options

• Select a policy that’s right for you

Let’sTalk

Together we can tailor an income protection plan to meet your needs and keep you on track for your life and financial goals.

• [Agent/Producer Name]

• [Agent/Producer License Number]

• [Phone]

• [Email Address]

This is a solicitation of insurance and a licensed insurance agent/producer will contact you.

Disability Income Insurance is underwritten by Mutual of Omaha Insurance Company, 3300 Mutual of Omaha Plaza, Omaha, NE 68175.

Disability income policy form numbers D81, D82, D83, (In FL, D81-21283/21231 D82-21284/21232, D83-21285/21233; in ID, OR, and Texas, D81-20896/20897, D82-20898/20899, D83-20900/20901; In NY, D81-21098/21099, D82-21100/21101, D83-21102/21103; in NC, D81-21008/21009, D82-21010/21011, D83-21012/21013; in OK D81-21014/21015, D82-21016/21017, D83-21018/21019; in PA, D81-21080/2108, D82-21082/21083, D83-21084/21085; in WA, D81-21038/21039, D82-21040/21041, D83-21042/21043.) These policies have exclusions and limitations. Products may not be available in all states. For costs and complete details of coverage, contact your licensed insurance agent/producer. Mutual of Omaha Insurance Company is licensed nationwide.

In New York, these polices provide disability income insurance only. They do NOT provide basic hospital, basicmedical or major medical insurance as defined by the New York State Department of Financial Services. The expected benefitratio for policy form numbers D81-21098, D82-21100, and D83-21102 is 55% (D81-21099, D82-21101, D83-21103is 60%). The ratios are the portion of future premiums, which the Company expects to return as benefits whenaveraged over all people with these policies.

Top Related