Languages

Pages

Legal

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com

Harry Wang, Senior Director of Research

July 28, 2016

Digital Health Webcast:Disruption and Innovation in the Top-three Digital Health Markets

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 2

Parks Associates has invited you to view and listen to the webcast recording.

Click link to view recording: https://attendee.gotowebinar.com/recording/2653136227726965249

Audio Recording Playback

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 3

About Parks Associates

Expert Analysis and Forecasts

Competition

Consumers

• The company's expertise includes• Internet of Things (IoT) • Digital Media & Platforms• Entertainment Services • Streaming Media Devices • Augmented Reality/Virtual Reality• Home Networks• OTT & Pay TV services• Cloud Services• Privacy and Security • Big Data• Digital Health & Wellness• Mobile Applications and Services• Tech Support Services• Consumer Apps• Consumer Electronics • Home Control Systems and Security• Smart Home and Energy Management

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com

›Connected Health Summit: Engaging Consumersspotlights health technologies as part of the Internet of Things (IoT) phenomenon and the transformational impact of these connected solutions on the U.S. healthcare system.

›This focus provides strategic insights into consumer engagement, care accountability, service innovations, and platform design to determine successful approaches in the deployment of connected healthcare products and services.

›ConnectedHealthSummit.com

›Sample Confirmed Speakers From…

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com

Parks Associates Digital Health Research Service

•

•

••

••

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 6

Background: Venture Funding

IPOed

Acquired

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 7

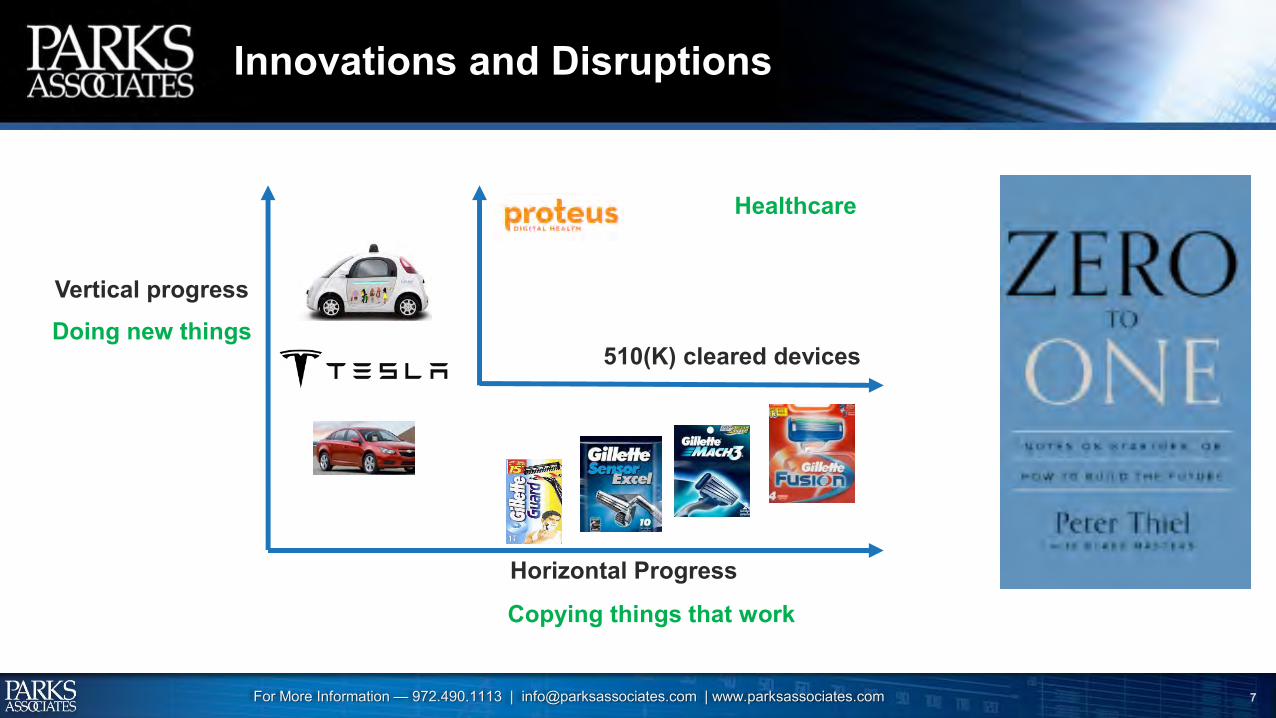

Innovations and Disruptions

Doing new things

Vertical progress

Horizontal Progress

Copying things that work

510(K) cleared devices

Healthcare

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 8

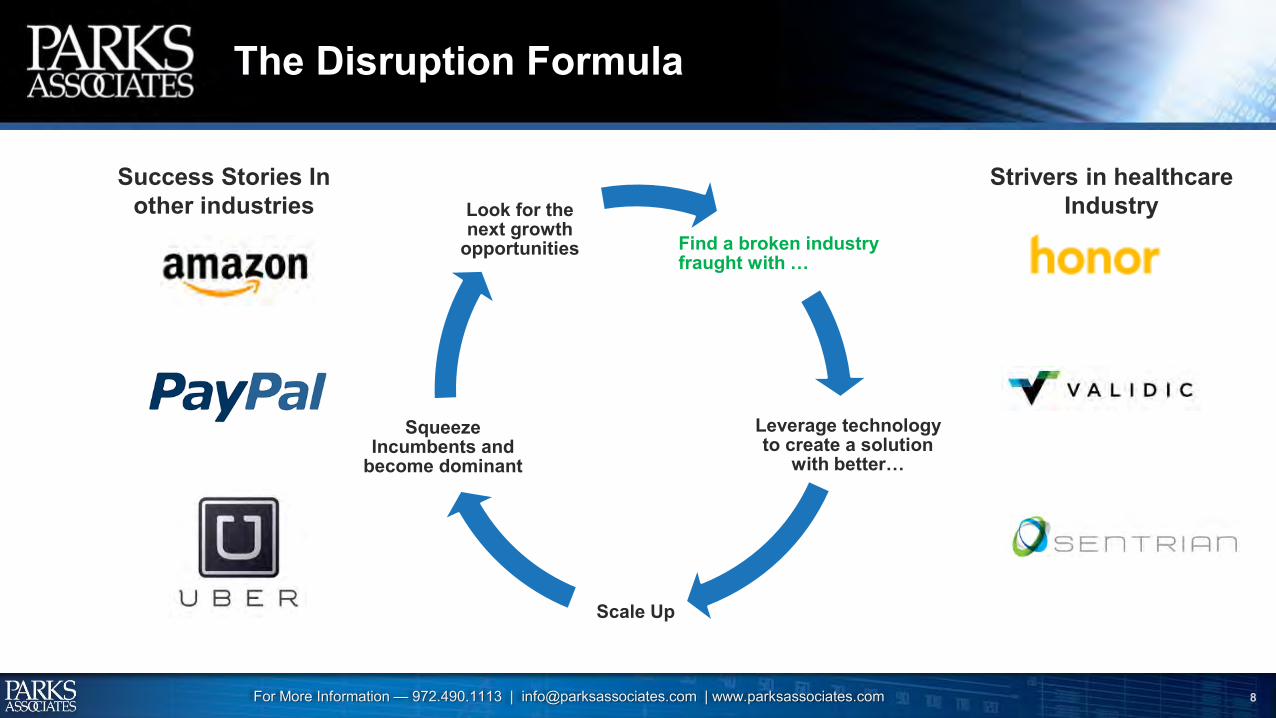

The Disruption Formula

Find a broken industry fraught with …

Leverage technology to create a solution

with better…

Scale Up

Squeeze Incumbents and

become dominant

Look for the next growth

opportunities

Success Stories In other industries

Strivers in healthcare Industry

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 9

What We Learned

Innovations may not be disruptions

Innovations may as well fail

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 10

Evaluate Innovators for Potential Sustainable Disruption

Innovator Leaderboard—Sustainable Disruption Matrix

Disruptiveness of Innovation

Gro

wth

Sus

tain

abilit

y

HighLow

Hig

hLo

w

Disruptive Front-Runners

Visionary Mavericks

Growth Masters

Differentiation Executors

Innovations don’t equal to disruptions

Technology breakthroughs can lead to disruptions only if the underlying business model is financially sustainable

Sustainability of revenue models should be considered along with innovation merits

Key Takeaways:

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 11

Three Leading Innovation Frontiers

Digital Health Solutions Definition Buyer Profiles

Consumer Fitness & Wellness

Digital products, software, and services that help consumers achieve fitness goals and improve overall wellbeing.

Health Optimizers & Savvy Engagers

Virtual Care SolutionsTechnology, solutions, and services that help care providers deliver care without requiring patients to meet in-person

Hospitals, health systems, and some payers

Patient Communications and Education Solutions

Technology and solutions helping care providers improve in-bound/out-bound communications with patients & their families and engage them for education purpose

Hospitals, health systems, particularly those with a high percentage of business tied to shared risk contracts or fully capitated contract

Consumer Fitness & Wellness

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 13

Demand Drivers:

Quantified-self benefits

Lowered product price

Growing integration of fitness/wellness tracking devices into wellness management solutions

Consumer Fitness & Wellness

Industry Trends:

Growing integration of other wellness tracking functions: e.g., sleep, stress, posture

Growing use of video to aid fitness training:

Wellness coaching as a premium service:

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 14

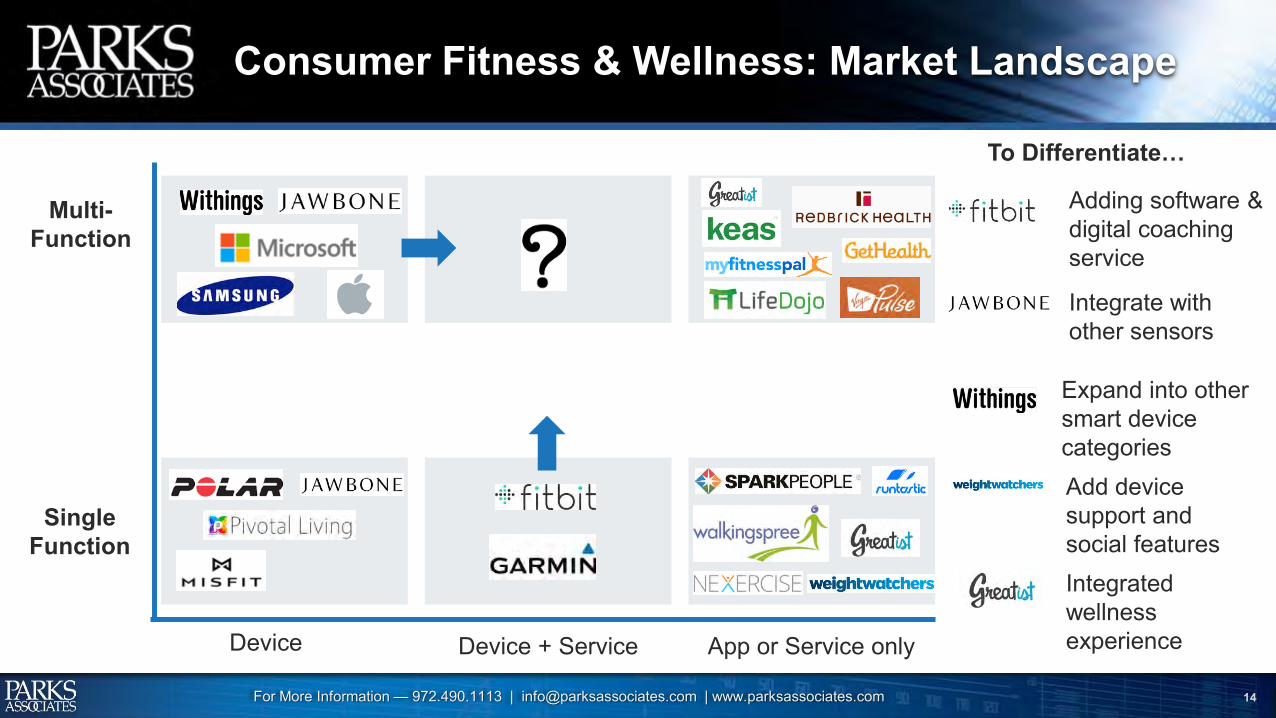

Consumer Fitness & Wellness: Market Landscape

Device App or Service only

Multi-Function

Single Function

Integrate with other sensors

Expand into other smart device categories

Adding software & digital coaching service

Add device support and social features

To Differentiate…

Device + Service

Integrated wellness experience

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 15

Fitness & Wellness Solution Adopters & Targets

49% 54%Current Heavy Users Next Good Targets

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 16

Usage, Usage, Usage

70%

83%

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 17

Positive Correlation between Fitness Device Ownership and Wellness Program Usage

±

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 18

Fitbit’s Software & Service Revenue

Corporate Wellness Program Users as %of Total Fitbit Active Users

Service Revenue

As % of Total2015 Fitbit Revenue

1% $9.3M 0.5%

3% $28M 1.5%

5% $46M 2.5%

10% $93M 5.0%

15% $139M 7.5%

20% $185M 10%

Virtual Care Solutions

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 20

Demand Drivers:

Convenience and cost savings for consumers

Care providers embrace it for patient acquisition, operation efficiency, and patient satisfaction

Payer acceptance: Reimbursement parity in most states

Good news on multistate licensure

Virtual Care Solutions

Industry Trends:

Expanding use cases: from primary urgent care and routine care to post-discharge follow-up and chronic care management & health coaching; from primary care physician, to pediatrician, behavioral therapist, and specialist

Growing # of Vendors target B2B: demand from not only care providers, but also EMR/PM/DM vendors that want to embed virtual care into their own software platform

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 21

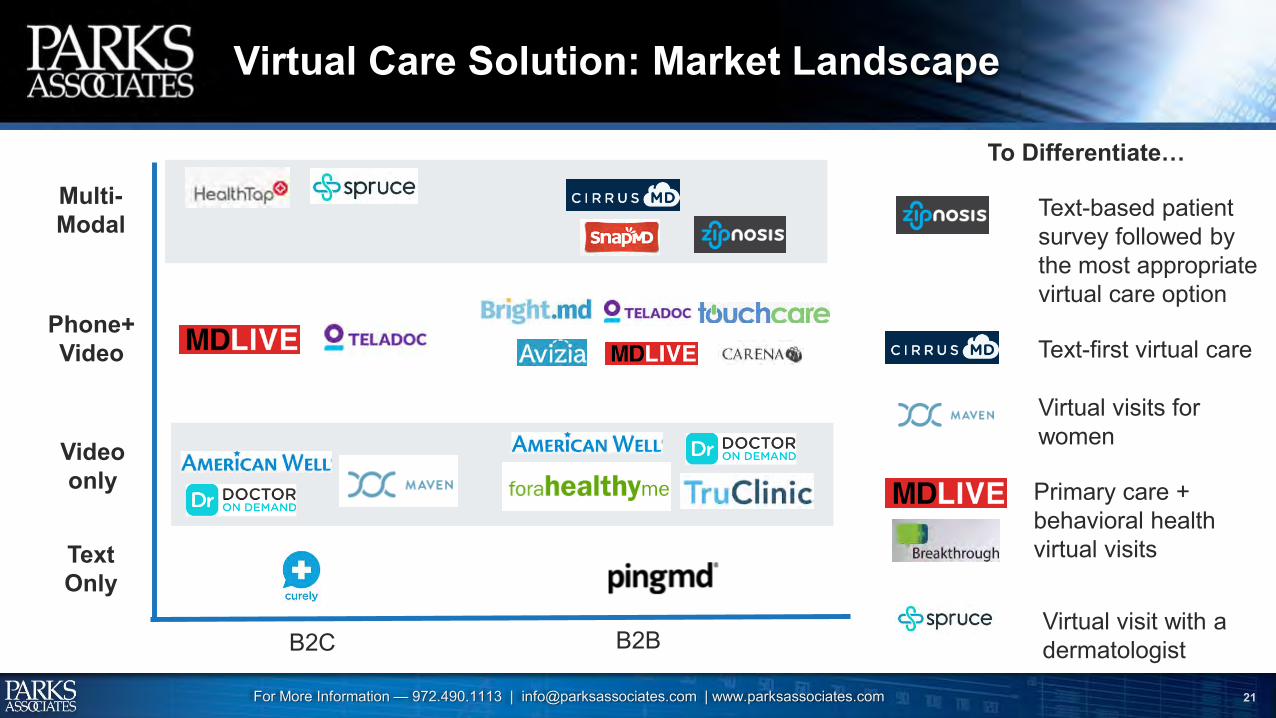

Virtual Care Solution: Market Landscape

B2C B2B

Phone+ Video

Video only

Multi-Modal

Text Only

Text-first virtual care

Virtual visits for women

Text-based patient survey followed by the most appropriate virtual care option

Primary care + behavioral health virtual visits

Virtual visit with a dermatologist

To Differentiate…

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 22

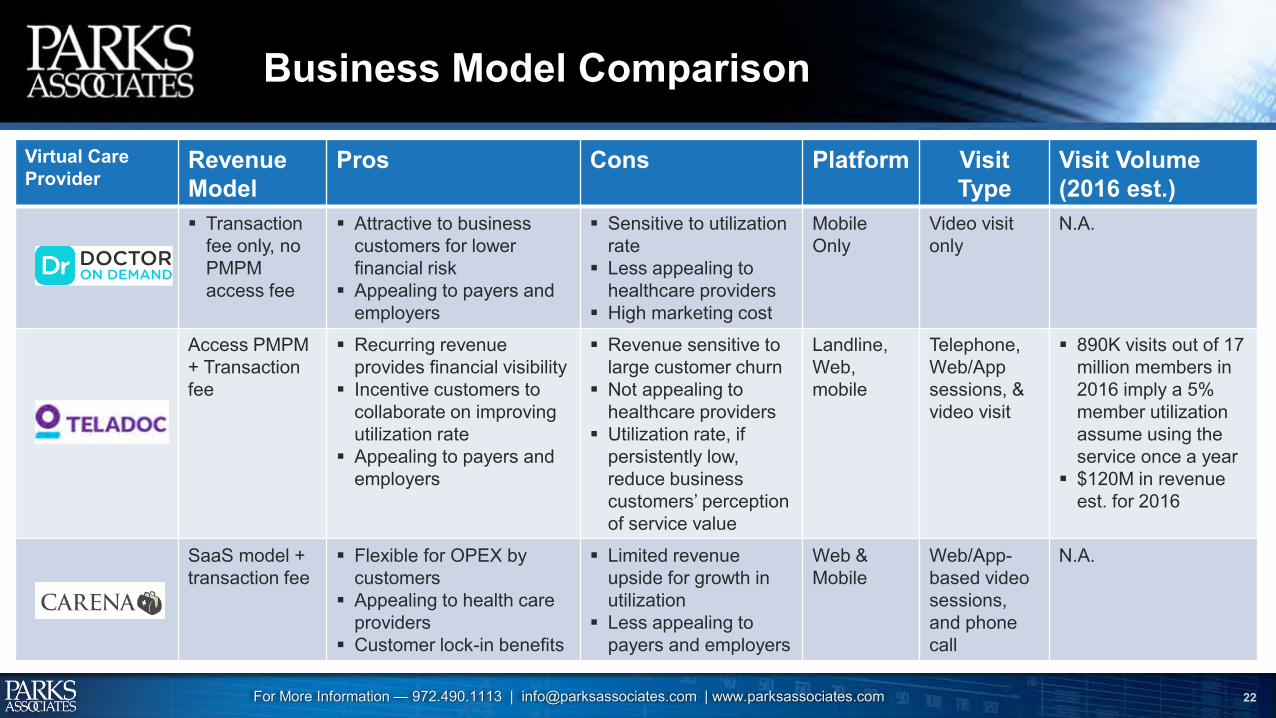

Business Model Comparison

Virtual Care Provider

RevenueModel

Pros Cons Platform Visit Type

Visit Volume (2016 est.)

Transaction fee only, no PMPM access fee

Attractive to businesscustomers for lower financial risk

Appealing to payers and employers

Sensitive to utilization rate

Less appealing to healthcare providers

High marketing cost

Mobile Only

Video visit only

N.A.

Access PMPM + Transaction fee

Recurring revenue provides financial visibility

Incentive customers to collaborate on improving utilization rate

Appealing to payers and employers

Revenue sensitive to large customer churn

Not appealing to healthcare providers

Utilization rate, if persistently low, reduce business customers’ perception of service value

Landline, Web, mobile

Telephone,Web/Appsessions, & video visit

890K visits out of 17 million members in 2016 imply a 5% member utilization assume using the service once a year

$120M in revenueest. for 2016

SaaS model + transaction fee

Flexible for OPEX bycustomers

Appealing to health care providers

Customer lock-in benefits

Limited revenueupside for growth in utilization

Less appealing to payers and employers

Web & Mobile

Web/App-based video sessions,and phone call

N.A.

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 23

TelaDoc Revenue Model Sensitivity to Utilization

% Utilization Revenue Gain or Loss %

Total Revenue

1% -43% $68M

2% -31% $82M

3% -19% $97M

5% 0% $120M

8% 23% $147M

10% 44% $173M

12% 68% $201M

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 24

Doctor on Demand’s Revenue Model Tied to Utilization

% Utilization

Twiceper Year

Four per Year

Six per Year

1% 600 million

300 million

200 million

5% 120 million

60million

40 million

15% 40 million

20 million

13million

30% 20 million

10 million

7 million

600

200120

6040 30

2015

12

300

100

60

3020

1510

8 6

200

67

40

2013

107

54

1% 3% 5% 10% 15% 20% 30% 40% 50%

Utilization Rate: % of Users Who Use Virtual Visits

2 times PUPY4 times PUPY6 times PUPY

Doctor on Demand's Revenue Model Sensitivity: "At what user base size can Doctor On Demand achieve

TelaDoc's 2016 estimated revenues of $120 million, given different utilization rate assumptions?"

Doctor on Demand’s User Base Scenarios

Patient Communications & Education Solutions

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 26

Demand Drivers:

Health service providers have no CRM experience

ACO/Value-based care models: payment tied to patient care outcome

HCAHPS: patient satisfaction score

Patient Communications & Education Solutions

Industry Trends:

Bye-Bye, Patient Portal; Welcome, Patient Experience Platform

Desire both in-bound & outbound capability with multi-modal scalability

Priorities: transitional care, care coordination, & population health

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 27

Patient Education & Communications

EducationCommunications Engagement

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 28

Major Player Categories and product Strategies

Customer Service Center

Health IT Vendors

Telecom Services Startups

Patient Communications, Education, & Engagement

Repurpose Bundle

IntegratedValue-added

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 29

What do we like Emmi Solutions:

Focus on overall patient experience in and outside of care faculties

Solutions tailored for transitional care and care provider-supported care management tasks

High client retention rate

Robust product roadmap to support patient engagement across care continuum

Disrupter Highlight

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com 30

Recap: What is Sustainable Disruption?

Innovator Leaderboard—Sustainable Disruption Matrix

Disruptiveness of Innovation

Gro

wth

Sus

tain

abilit

y

HighLow

Hig

hLo

w

Disruptive Front-Runners

Visionary Mavericks

Growth Masters

Differentiation Executors

Innovations don’t equal to disruptions

Technology breakthroughs can lead to disruptions only if the underlying business model is financially sustainable

Sustainability of revenue models should be considered along with innovation merits

Key Takeaways:

For More Information — 972.490.1113 | [email protected] | www.parksassociates.com

Questions? Contact us today.

Harry WangSenior Director of Research

Leaders in Consumer Trends & Research

Top Related