Languages

Pages

Legal

Crocs, Inc (CROX)- LONG

MCINTIRE INVESTMENT INSTITUTE

Summary

• Overview• Financials• Thesis points• Misperceptions• VAR• Risks• Recommendation

Overview

• Footwear, apparel, accessories designer, manufacturerand distributor.

• Men, Women and Children.

• Styles- Casual, Athletic, Professional, Health needs

• Proprietary material- closed cell-resin Croslite.

• 35% USA, 65% International

• 158 kiosks, 180 retail stores, 92 outlet stores, 42 web stores

Some Financials

• Current Price- 20.00• Market cap- 1.80 bn• 52 week- 14.20-32.47• P/E ratio- 16.13• EV/EBITDA- 9.22• Beta- 1.64• Cash- 250 Mn• Debt- 1 Mn

5 Year Stock Chart

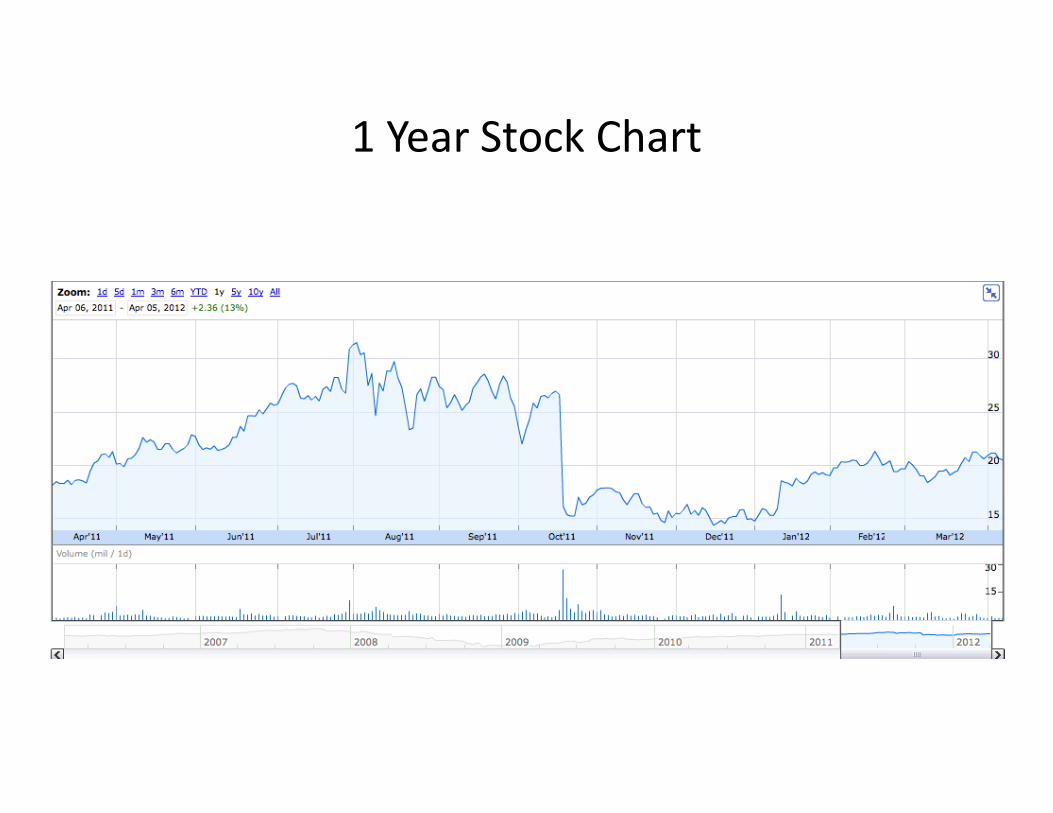

1 Year Stock Chart

Thesis Points

• Excellent CEO and mission clarity

• Insider buying

• Reversal in misperception-friendly conditions

• Positive business fundamentals

Excellent CEO, Mission

• Named CEO in Feb, 2010• Share Price has almost tripled since then.• Some very smart decisions-

– Closed down non-cost effective factories in Brazil, Canada.– Ended 10M marketing contract with AVP– Set the focus on Asia- rapid expansion plans– Moved a lot of production from China to Vietnam.

• Slightly lower production cost.• Ship to other countries, duty-free.

– ‘Be local’

Revenue

0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

2007 2008 2009 2010 2011

Net Income

(250.0)

(200.0)

(150.0)

(100.0)

(50.0)

0

50.0

100.0

150.0

200.0

2007 2008 2009 2010 2011

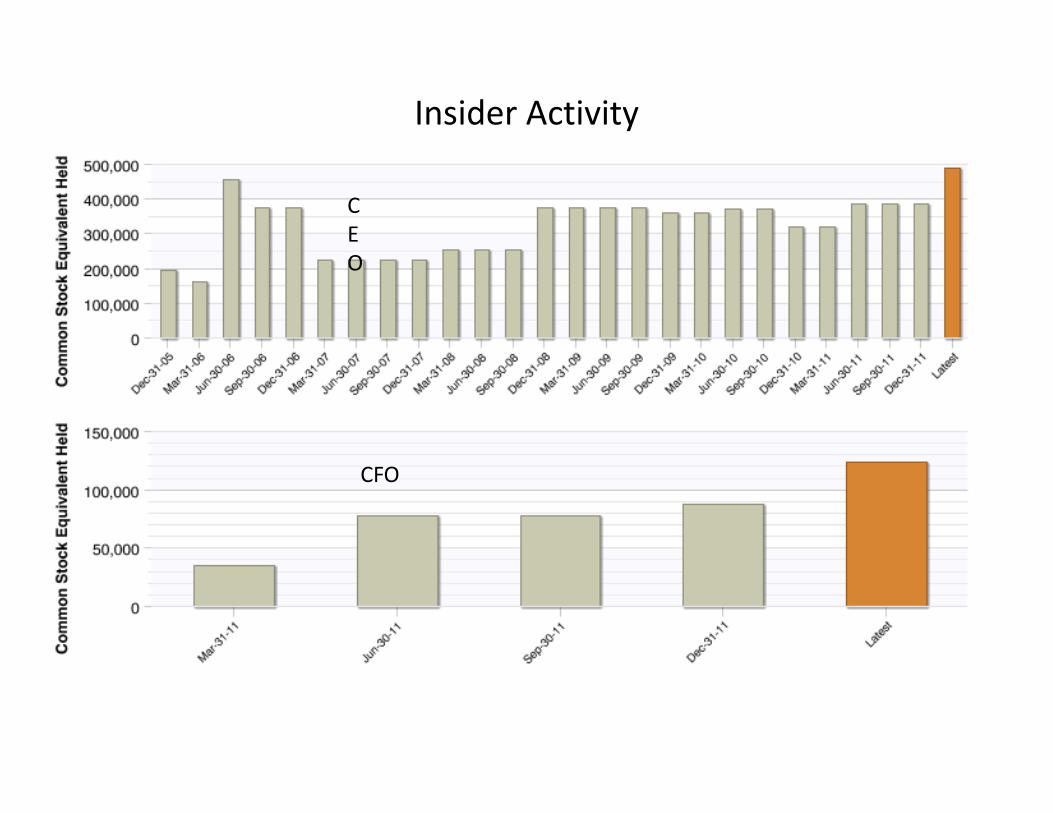

Insider Activity

CEO

CFO

More Insider Activity…

Chief Legal and Administrative Officer

Reversal in Misperceptions

• Misperceptions-– 1) Crocs makes one product.– 2) Crocs don’t sell anymore since they’re ugly.

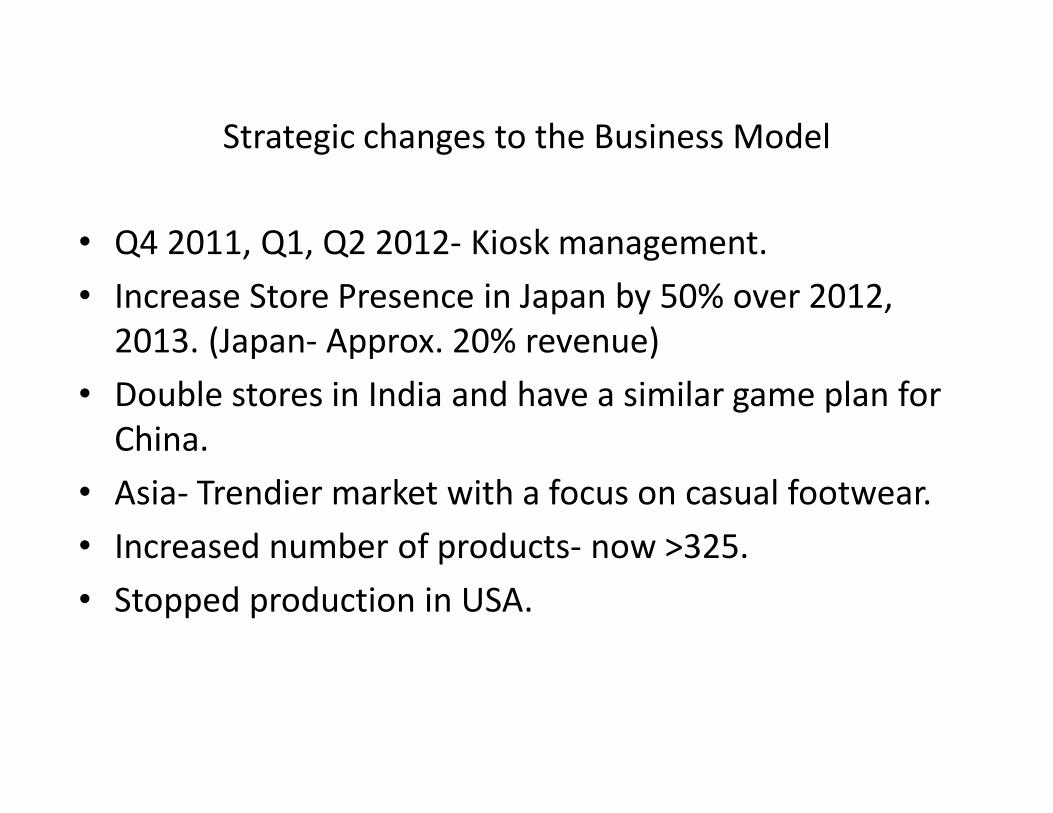

Strategic changes to the Business Model

• Q4 2011, Q1, Q2 2012- Kiosk management.• Increase Store Presence in Japan by 50% over 2012,

2013. (Japan- Approx. 20% revenue)• Double stores in India and have a similar game plan for

China.• Asia- Trendier market with a focus on casual footwear.• Increased number of products- now >325.• Stopped production in USA.

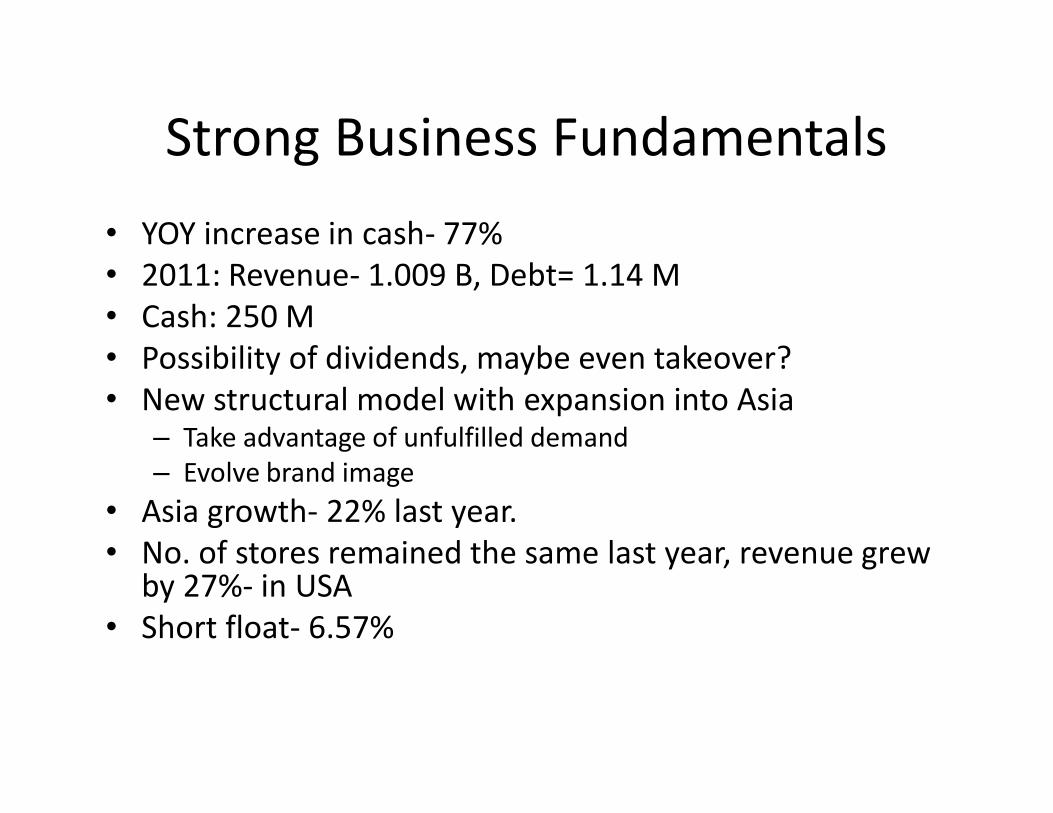

Strong Business Fundamentals• YOY increase in cash- 77%• 2011: Revenue- 1.009 B, Debt= 1.14 M• Cash: 250 M• Possibility of dividends, maybe even takeover?• New structural model with expansion into Asia

– Take advantage of unfulfilled demand– Evolve brand image

• Asia growth- 22% last year.• No. of stores remained the same last year, revenue grew

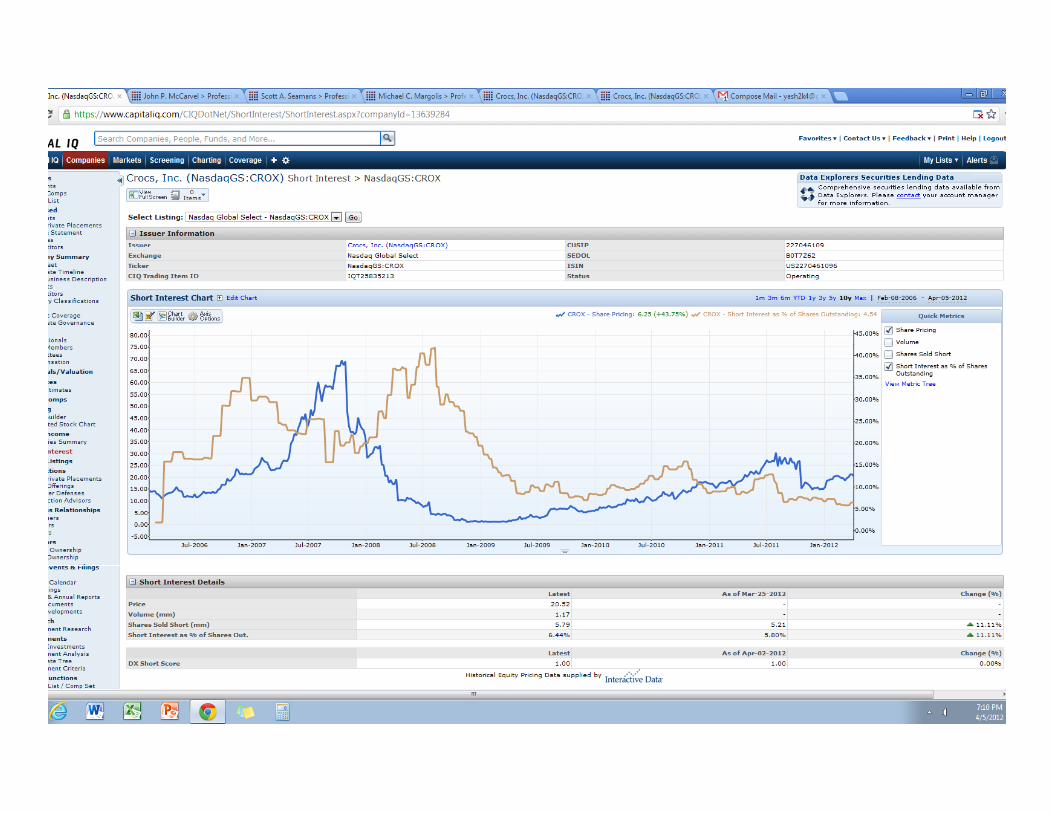

by 27%- in USA• Short float- 6.57%

Undervalued

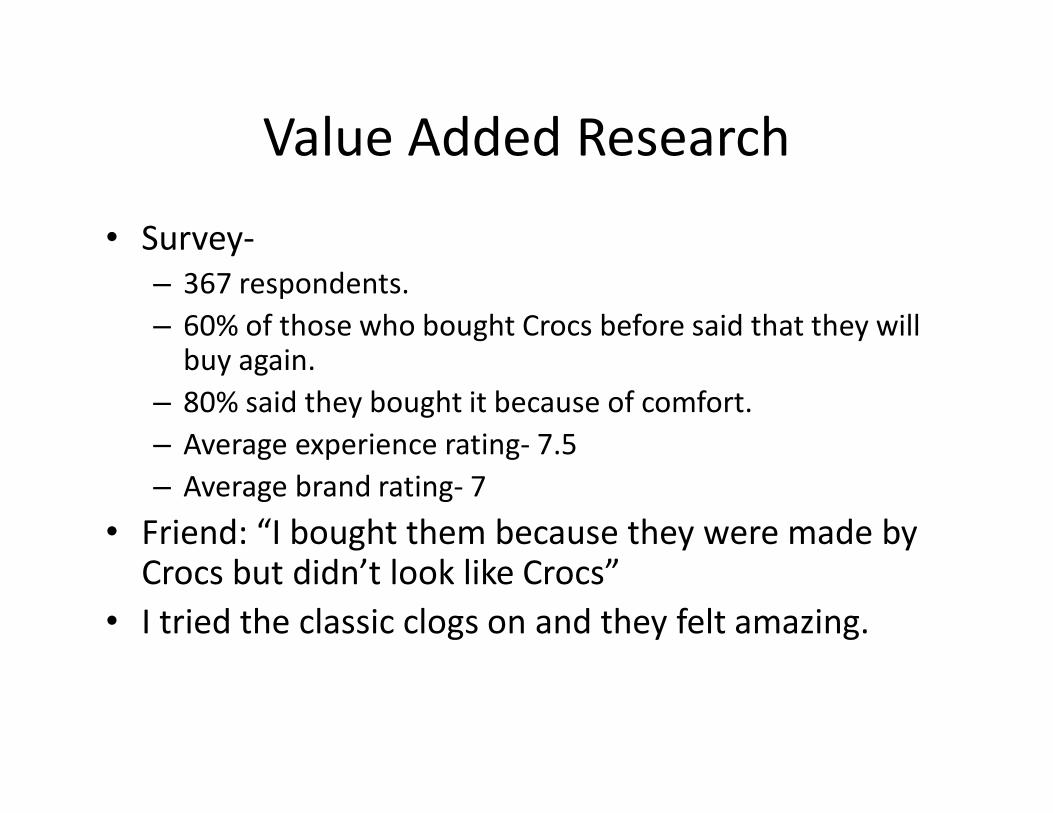

Value Added Research

• Survey-– 367 respondents.– 60% of those who bought Crocs before said that they will

buy again.– 80% said they bought it because of comfort.– Average experience rating- 7.5– Average brand rating- 7

• Friend: “I bought them because they were made by Crocs but didn’t look like Crocs”

• I tried the classic clogs on and they felt amazing.

Risks

• Expansion always poses risks through costs, R&D and legal issues.

• The Asian Counterfeit problem is reality and will definitely challenge expansion.

• Inventory forecasting issues.

On a Lighter Note…

Recommendations

• Buy now.• Hold for 2-3 years.• Monitor trends in earnings (upcoming- April 26),

company announcements (I expect these mainly to pertain to kiosk management and expansion status), any special situations (M&A rumours, change in management etc.) and most importantly, product design- check if it continues to evolve because if it stops, we can see this as a red flag and exit.

Q-A?

Top Related