Languages

Pages

Legal

Corporate Presentation

August, 2014

History and Business Model

3

More Than 30 Years of History

48%

Controlling Shareholders ¹ Others

52%

155,298,749 ordinary shares

1. Participation held directly and indirectly by the Controlling Shareholder

2. Data: 05/29/2014

Industrial projects acting

as contractor to third

parties

Important geographic

expansion: Brasília, Rio de

Janeiro and Campinas

Development of projects

focused on the low-income

segment

Beginning of large scale

projects for the low-income

segment

Consolidation of a leading

position in Manaus and

Brasilia

Operations expansion to

PA, RO and ES

IPO 36% annual growth

in PSV launched

(CAGR)

69% annual growth

in net revenue

(CAGR)

Follow-on

MCMV 2

Establishment of

own sales team

1981 - 2005 2006-2007 2008 2009 2010-2011 2012

Record net

revenue of R$ 1.4

Billion, a 28% YoY

growth

More than R$

1 billion on

projects delivered

during 2012

Increasing stock

liquidity

The most relevant

player in the MCMV

2nd phase Level 1

Focus on Cash

Generation and

Construction

Service business

2013

1%

3%

13%

16%

22%

45%

South American

Europe

Brazil

North American

Others

Asian

Free Floating (others 52%)²

Unique Footprint Strong footprint in markets with high growth potential, low

competition and high barriers to entry Low competition in

profitable markets

Track Record in

Operating in the low-

Income segment

Over 30 years of experience

Solid track record in MCMV Level 1 projects

Low equity commitment,

solid margins and high

ROIC

Focus on Large

Scale Projects

Verticalized

Business Model

Strong expertise in large scale ventures

Own work force

Performance-based compensation

Standardized and industrialized production on-site

Large scale operations in

the low-income segments,

with strict cost control and

high margins

4

Direcional: A Unique Business Model

The most profitable

and efficient player in

the low-income sector

‘’’’

High efficiency and profitability

ROE¹ among the highest in the sector LTM ROE¹: 14%

1. LTM ROE: Net Income in the Last Twelve Months / Average Shareholders’ Equity in the Last Twelve Months (net of non-controlling interest in silent partnerships and SPEs)

The best low-income player in Brazil

Industrialization Aluminum panels and concrete walls technology

45 days to develop a five floors building

1

2

3

5

4

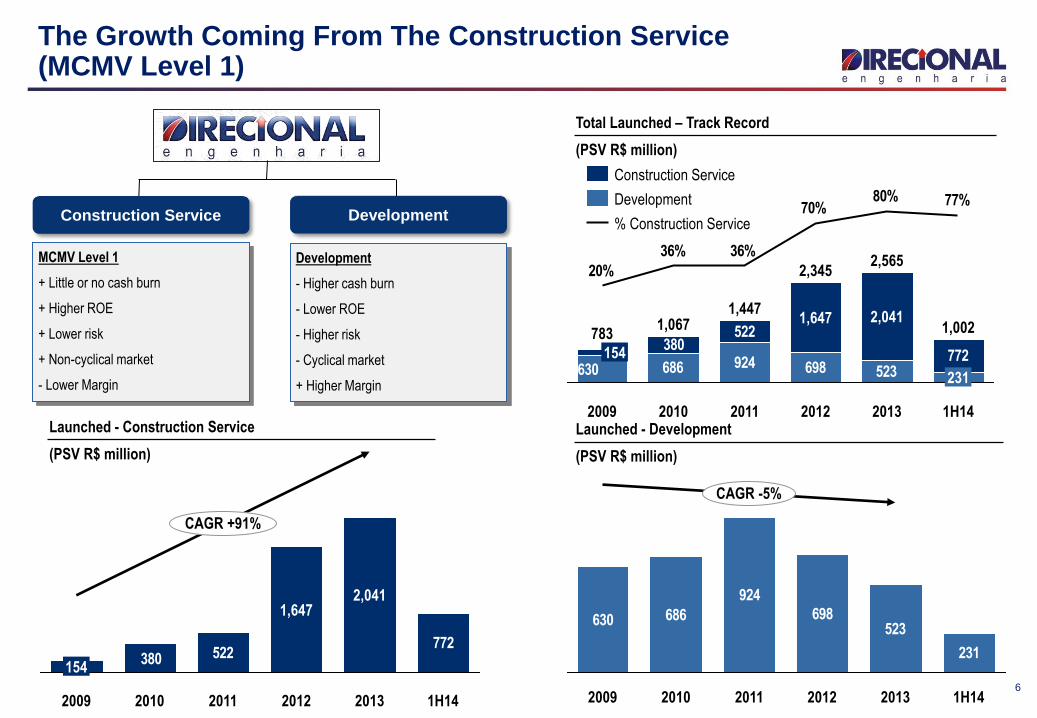

Focus on the Low-Income Segment

Launched - Construction Service

(PSV R$ million)

686

924

698523

231

630

2012 2011 2010 2009

CAGR -5%

1H14 2013

Launched - Development

(PSV R$ million)

522772

380

CAGR +91%

1H14 2013

2,041

2012

1,647

2011 2010 2009

154

Construction Service Development

MCMV Level 1

+ Little or no cash burn

+ Higher ROE

+ Lower risk

+ Non-cyclical market

- Lower Margin

Development

- Higher cash burn

- Lower ROE

- Higher risk

- Cyclical market

+ Higher Margin

Total Launched – Track Record

(PSV R$ million)

698924523686630

522380

772

77%80%70%

36%36%

20%

2013 1H14

2,565

2,041

2012

2,345

1,647

2011

1,447

2010

1,067

2009

783

154

1,002

231

% Construction Service

Development

Construction Service

The Growth Coming From The Construction Service (MCMV Level 1)

6

Total Hired % Balance Delivered % %(A) (B) (C) (C/A) (C/B)

Level 1 2.000.000 1.619.400 81% 380.600 552.644 28% 34%

Level 2 1.200.000 1.441.404 100% - 1.040.570 87% 72%

Level 3 400.000 438.836 100% - 142.391 36% 32%

Total 3.600.000 3.499.640 380.600 1.735.605

Results MCMV (Phase 1 & 2) - Up - to Date

MCMV Focus Moving Towards Level 1

Program Challenges ("Ministério das Cidades")

• Hire 381k units in 2H14; (ii) Quality assurance and delivery; (iii) Investments on projects sustainability; (iv) Improvements in the

construction process

Source : Ministério do Planejamento, Orçamento e Gestão 07/2014

Lauch Date Jul/2011 Aug/2012

Level 1 R$48 k - R$65 k R$57 k - R$76 k 17%

Level 2 and 3 R$65 k - R$170 k R$76 k - R$190 k 12%

MCMV 2MCMV 2

(after review)Unit Price D%

+300%

MCMV2

1,600,000

800,000

200,000

MCMV1

1,000,000

400,000

400,000

200,000

2,600,000

Level 1

Level 2

Level 3 The Government increased the price cap of 17% for the units within

the first level of the MCMV Program.

4x

2x

1x

• Brazil’s Federal Government has already shown that its focusing the Level 1 of MCMV, where the BZ housing deficit is heavily

concentrated.

• Such focus is clear when looking the breakdown of the Level 1 from MCMV 1 compared to MCVM 2 and its subsequent update.

7

8

MCMV Level 1 vs Development: Net FCF with no Sales Cancellations

Cash flow (traditional project vs MCMV Level 1 project)

-20%

-10%

0%

10%

20%

0Q -1Q 10Q 9Q 8Q 7Q 6Q 5Q 4Q 3Q 2Q 1Q -2Q -3Q -4Q

Traditional Development

MCMV Level 1 MCMV Level 1 Project Construction

• 100% of units sold to the Federal Government: No delinquency and sales cancelations from this segment, benefiting consolidated figures

• The Fist range of MCMV implies almost no working capital needs.

Land

acquisition Comercial

launch End of

construction

Hired to

Traditional Project Construction

Cash Exposure

MCMV Level 1

Development

9

MCMV: Risk of Discontinuation?

Even considering a potential reduction in the MCMV Level 1 program with a change in political parties, there should be little effect on Direcional.

There are few companies that can deliver high volumes of construction in MCMV Level 1:

MCMV Level 1: 34% of units launched in MCMV Level 1 were delivered

100% 81%

100%

100%

72%

34%

Contracted

100%

100%

Delivered

32%

Program

MCMV Program Phase 1 & 2: Status

(% of Units)

Low Share: Direcional represents 5% of MCMV Level 1 as a whole

Opportunity to increase its share

+500 bps

Source : Ministério do Planejamento, Orçamento e Gestão 07/2014

Level 3

Level 2

Level 1

Level 1 Contracted Units Direcional Share %

MCMV 1 & 2 1.619.400 84.065 5%

MCMV 1 482.741 7.391 2%

MCMV 2 1.136.659 76.674 7%

Very Low Income Projects:

# of projects: 34

# of Units: 84,065

Total PSV: R$ 5,363.2 MM

Average PSV: R$ 157.7 MM

Average Units: 2,472

Direcional’s Contracted MCMV Level 1

1st Phase MCMV 2nd Phase MCMV

# of projects: 3

# of Units: 7,391

Total PSV: R$ 380.3 million

# of projects: 31

# of Units: 76,674

Total PSV: R$ 4,983.2MM

+

Direcional`s Contracted MCMV – Level 1

(PSV million)

Direcional`s Contracted MCMV – Level 1

(Units)

772522380

2,041

2010 2012 2011

1,647

+437%

1H14 2013 2012 2010

7,391

+365% 34,372

10,196

2011 1H14

8,872

23,234

2013 10

Focus on Industrialization

Focus on Performance

49% 50% 56% 60% 70% 75% 78% 84% 85% 88%

43% 41% 36% 31%23% 18%

88%

16%5%5% 10%

3Q13 3Q12 2Q12

9% 7%

4Q12 4Q13

7%

1Q13

11% 6%

2Q13

9%

1Q12

8% 4%

2Q14 1Q14

8% 4% 8%

4Q11

7%

Units Under Construction by Construction Method

(% of Units)

1 Aluminum mold and concrete walls method

Industrial Construction¹ Conventional Structure (Concrete Pillars) Concrete Blocks

12

2Q14 2Q13 D %

Units Under Construction 76.211 62.515 22%

% of Industrialization (# of units) 88% 78% 10 p.p.

Construction Sites 58 55 5%

Average # of Units by Construction Sites 1.314 1.137 16%

# of Cities 19 14 36%

Construction Technology

45 days to develop 2 buildings with 5 floors and 4 apartments per floor

Video: http://www.direcional.com.br/ri

Aluminum Panels and Concrete Walls

13

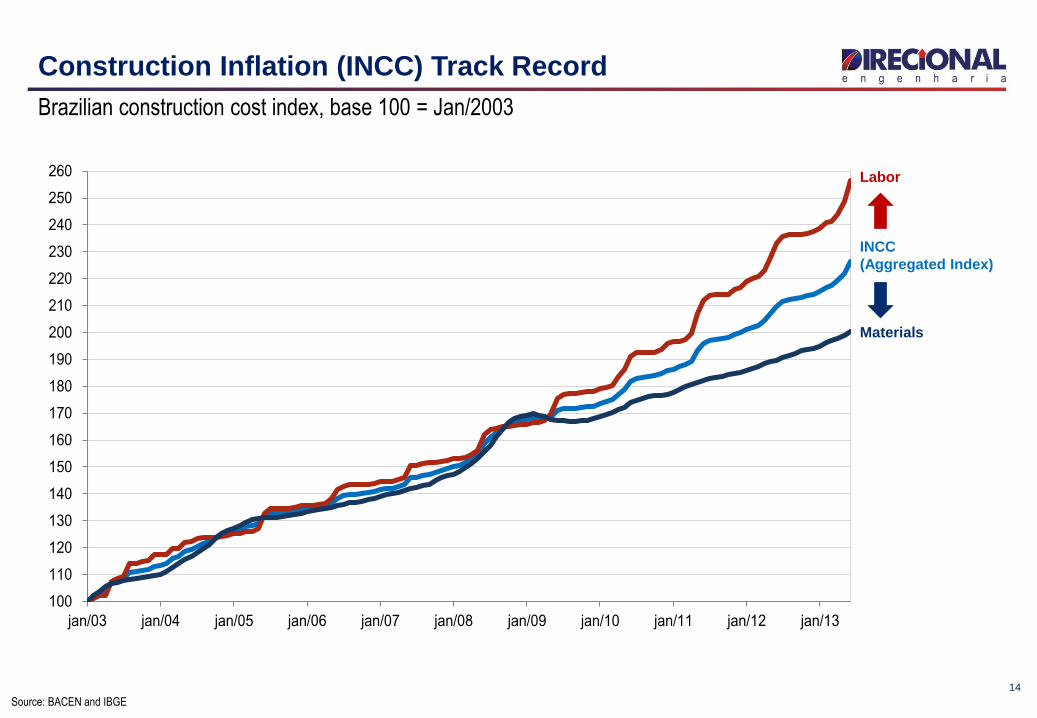

Construction Inflation (INCC) Track Record

Brazilian construction cost index, base 100 = Jan/2003

100

110

120

130

140

150

160

170

180

190

200

210

220

230

240

250

260

jan/03 jan/04 jan/05 jan/06 jan/07 jan/08 jan/09 jan/10 jan/11 jan/12 jan/13

Labor

INCC

(Aggregated Index)

Materials

Source: BACEN and IBGE

14

Operating and Financial Highlights

Launches

82%53%

29%

19%18%

1H14 1H13

Launches by Region - Development

(% PSV)

Launches by Region - MCMV Level 1

(% PSV)

807 772

231

+16%

1H14

1,002

1H13

866

59

Launched PSV

(R$ million)

MCMV Level 1

Development

Launches 1Q14

MG

RS

681,595PSV (R$'000)

Units

Granja Werneck

8,896

89,909PSV (R$'000)

Units

Irmãos Maristas

1,300

16

14%

1H14

12%

88%

1H13

22%

64%

Midwest North Southeast South Northeast

Net Sales and Inventory

Inventory by Region – 1H14

(% PSV)

Inventory

(PSV - R$ million)

807 772

266 237

-6%

1H14 1H13

1,073 1,008

Contracted Net Sales

(PSV - R$ million)

MCMV Level 1

Development

49.6%

2Q13

21.2%

55.1%

4Q13

14.0% 15.4%

3Q13

21.1%

46.9%

1Q14

55.3%

13.5%

2Q14

Without MCMV Level 1 project

With MCMV Level 1 project

Sales-over-supply ratio (VSO)¹

(% Total PSV)

1 - VSO ratio = Sales for the period / (Opening Inventory + Launches in the Period)

41%

40% Southeast

18%

North

Midweast

603

169

-4%

1H14

772

670

130

800

154

2012

571

2013

725

Under Construction

Finished Units

17

18

Deliveries

2Q14

LTM

1,806

1Q14

LTM

4Q13

LTM

1,676

3Q13

LTM

1,237

2Q13

LTM

1,020 1,029

Deliveries – Track Record

(Over the past 12 months: R$ million)

Residencial Macapaba

Parque Carioca

Deliveries by Region and Economic Segment

(Over the past 12 months: % PSV)

Northeast 4%

Midwest

19% North

44%

Southeast

32% 17%

Low-Income

14% Medium

11% Commercial

42%

MCMV Level 1

Upper-Middle 11%

6%

RET 1

Land Bank

72% are large scale projects (over 1,000 units)

56% are eligible for the MCMV Program

82% were acquired by physical or financial Swap

Average acquisition price of 12% over PSV

Land Bank by Segment

(% PSV)

Land Bank Track Record in 1H14

(R$ million in PSV)

Land Bank by Region

(% PSV)

Type of Payment

(% PSV)

Swap 81.8% Cash 18.2%

Low-Income 29%

Upper-Middle

9%

Medium

57%

Commercial

4%

19

ES1%

AM10%

MG44%

RO1%

SP5%

PA6%

DF17%

GO1%

RJ15%

R$ 8 Billion

51.540 units

221

1H14

7,952

Launches

231

Review of

Assumptions

/ Traded and

Cancellation

Acquired

Land Bank

1,021

2013

7,382

60%47%

31%24%

14%

1H14

524

2013

836

2012

457

2011

269

2010

117

% of Gross Revenue

Revenue from Services

(R$ million)

Cash Generation with Growth

1 - Cash Burn: measured by the change in net debt adjusted for dividend payments and shares buyback

2 – Numbers prior to 2012 are not adjusted in accordance with the new consolidation accounting practices (IFRS 11).

1H14

91

2013

76

2012

-183

2011

-176

2010

-283

2009

-95

Cash Burn¹,²

(R$ million)

Net Revenues - Track Record²

(R$ million)

CAGR +47%

1H14

822

2013

1,744

2012

1,449

2011

1,072

2010

782

2009

378

Financing Pass-through (“Repasses”)

(R$ million)

633

+39%

2013

273

360

2012

455

233

222

1H14

282

185

97

"Associativo"

SFH

Service 86%

Development 14%

Revenue to be Recognized

(% Total)

Services

R$ 4,2 Billion

Development

20

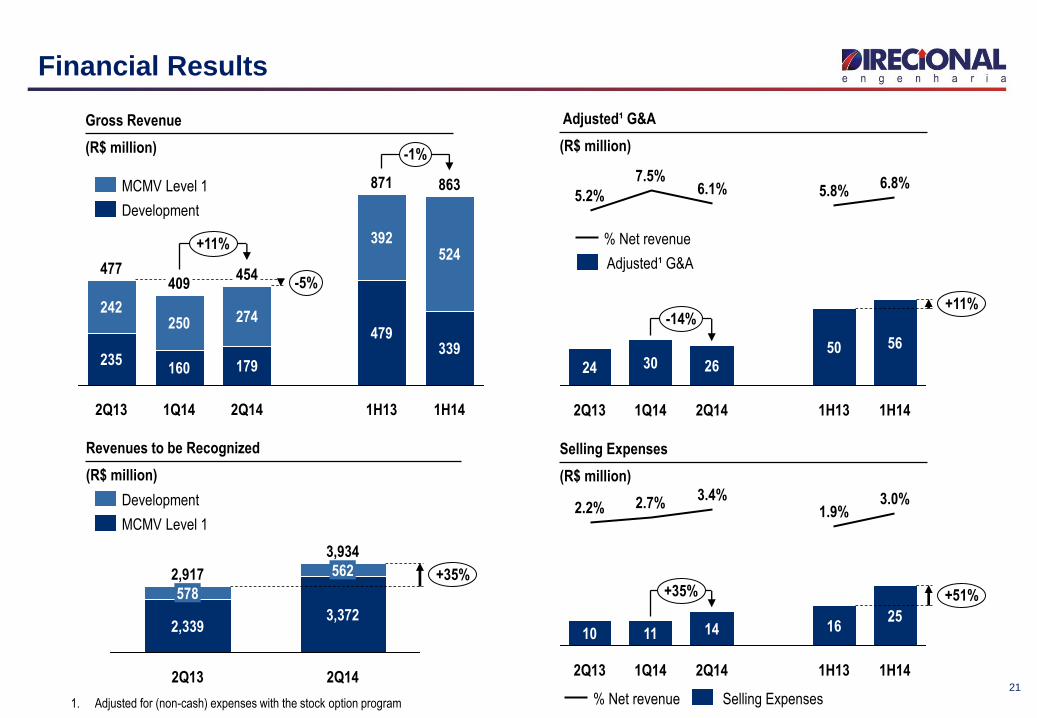

Financial Results

1. Adjusted for (non-cash) expenses with the stock option program

Adjusted¹ G&A

(R$ million)

+11% -14%

1H14

56

6.8%

1H13

50

5.8%

2Q14 1Q14

30

7.5%

2Q13

24

5.2% 6.1%

26

Adjusted¹ G&A

% Net revenue

Selling Expenses

(R$ million)

11

2.7%

2Q13

10

2.2%

14

+51% +35%

1H14

25

3.0%

1H13

16

1.9%

2Q14

3.4%

1Q14

Selling Expenses % Net revenue

3,934

+35%

2Q14

3,372

562

2Q13

2,917

2,339

578

MCMV Level 1

Development

Revenues to be Recognized

(R$ million)

Gross Revenue

(R$ million)

179

274

1Q14

409

160

-1%

2Q13

477

235

242

+11%

1H14

863

339

524

1H13

-5%

871

479

392

2Q14

454

250

Development

MCMV Level 1

21

22

Capital Structure

(R$ million)

Loans and Financing – 2Q14

(% of Debt)

642.801

956.347

1Q14

602.814

868.721

2Q13

499.962

944.834

2Q14

Cash

Gross Debt 374

Net Debt

25% 22% 16%

Net Debt / Shareholder's Equity

348 266

Capital Structure

Debt – 2Q14

(R$ million)

13%

CRI

Working Capital

1%

SFH

60%

FINAME and Leasing 5%

Debentures

21%

Net Debt

262

Cash and

Cash

Equivalent

Net Debt

Without SFH

643

Debt

956

SFH

576

381

314

Benchmarking 2013 – Outstanding Results

Direcional: Adjusted for non-cash expenses (Stock-Options Program)

BISA3; -10%

CYRE3; 13%

EVEN3; 15%

EZTC3; 30%

GFSA3; 1%

HBOR3; 26%

MRVE3; 11%

PDGR3; -6%

DIRR3 16%

RDNI3; 12%

RSID3; 2%

TCSA3; 16%

VIVR3; -63%

SETOR; 7%

TRIS3; 6%

22%

27%

32%

37%

42%

47%

52%

-55% -35% -15% 5% 25% 45%

Net

Rev

enu

e LT

M/T

ota

l Ass

ets

Net Margin¹

Slow turnover and margin above averageSlow turnover and margin below average

Fast turnover and margin below average Fast turnover and margin above average

Company; ROE LTMSize: Leverage (Assets/Equity)

Color: Average Prince - Launched Units Last 24 months

Low - up to R$ 200k per unit

Medium - between R$ 200k and R$ 400k per unit

High - above R$ 400k per unit

Setor

18%

24

Contacts

Carlos Wollenweber CFO | IR Officer

Paulo Sousa IR Coordinator

Luiz Felipe Almeida IR Analyst

www.direcional.com.br

(55 31) 3214-6200

(55 31) 3214-6450

Top Related