Languages

Pages

Legal

PowerPoint Authors:Susan Coomer Galbreath, Ph.D., CPACharles W. Caldwell, D.B.A., CMAJon A. Booker, Ph.D., CPA, CIACynthia J. Rooney, Ph.D., CPA

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Chapter 4

COMPLETING THE ACCOUNTING CYCLE

4 - 2

BENEFITS OF A WORK SHEET

Aids the preparation of

financial statements.

Aids the preparation of

financial statements.

Reduces possibility of

errors.

Reduces possibility of

errors.

Links accounts and their

adjustments.

Links accounts and their

adjustments.

Assists in planning and organizing an

audit.

Assists in planning and organizing an

audit.

Helps in preparing

interim financial statements.

Helps in preparing

interim financial statements.

Shows the effects of proposed

transactions.

Shows the effects of proposed

transactions.

Not a required report.

Not a required report.

P 1

4 - 3FastForwardWorksheet

For the Month Ended December 31, 2011P 1

4 - 4

PREPARING THE FINANCIAL STATEMENTS

P 1

4 - 5

PREPARING THE FINANCIAL STATEMENTS

P 1

4 - 6

RECORDING CLOSING ENTRIES

1. Resets revenue, expense and withdrawal account balances to zero at the end of the period.

2. Helps summarize a period’s revenues and expenses in the Income Summary account.

Identify accountsfor closing.

Record and postclosing entries.

Prepare post-closingtrial balance.

C 1

4 - 7

Temporary Accounts

Revenues

Income Summary

Exp

ense

s

With

draw

als

Permanent Accounts

Assets

Lia

bili

ties

Ow

ner’s

Cap

italTEMPORARY AND

PERMANENT ACCOUNTS

The closing process The closing process applies only to applies only to

temporary accounts.temporary accounts.

The closing process The closing process applies only to applies only to

temporary accounts.temporary accounts.

C 1

4 - 8

Let’s see how the closing

process works!

RECORDING CLOSING ENTRIES

Close Credit Balances in Revenue Accounts to Income Summary.

Close Debit Balances in Expense accounts to Income Summary.

Close Income Summary account to Owner’s Capital.

Close Withdrawals to Owner’s Capital.

P 2

4 - 9

Close Credit Balances in

Revenue Accounts to

Income Summary.

FastForwardAdjusted Trial Balance

December 31, 2011Debit Credit

Cash 4,350$ Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-Equip. 375$ Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-Equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals 47,685$ 47,685$

P 2

4 - 10

CLOSE CREDIT BALANCES INREVENUE ACCOUNTS TO INCOME

SUMMARY

Now, let’s look at the ledger accounts after posting this closing entry.

Dr. Cr.

Dec. 31 Consulting revenue 7,850

Rental revenue 300

Income summary 8,150

P 2

4 - 11

Consulting Revenue7,850 7,850

-

Rental Revenue300 300

-

Income Summary8,150

P 2 CLOSE CREDIT BALANCES INREVENUE ACCOUNTS TO INCOME

SUMMARY

4 - 12

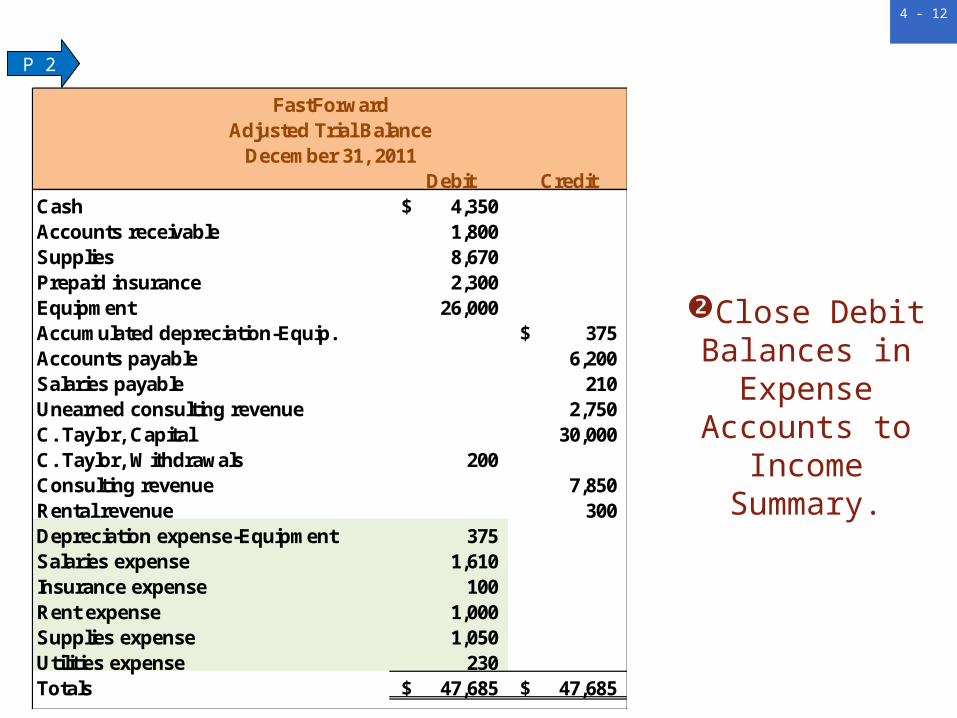

Close Debit Balances in

Expense Accounts to Income Summary.

P 2

FastForwardAdjusted Trial Balance

December 31, 2011Debit Credit

Cash 4,350$ Accounts receivable 1,800 Supplies 8,670 Prepaid insurance 2,300 Equipment 26,000 Accumulated depreciation-Equip. 375$ Accounts payable 6,200 Salaries payable 210 Unearned consulting revenue 2,750 C. Taylor, Capital 30,000 C. Taylor, Withdrawals 200 Consulting revenue 7,850 Rental revenue 300 Depreciation expense-Equipment 375 Salaries expense 1,610 Insurance expense 100 Rent expense 1,000 Supplies expense 1,050 Utilities expense 230 Totals 47,685$ 47,685$

4 - 13

Now, let’s look at the ledger accountsafter posting this closing entry.

CLOSE DEBIT BALANCES IN EXPENSE ACCOUNTS TO INCOME

SUMMARY Dr. Cr.

Dec. 31 Income summary 4,365Depreciation expense-Equipment 375Salaries expense 1,610Insurance expense 100Rent expense 1,000Supplies expense 1,050Utilities expense 230

P 2

4 - 14

Income Summary4,365 8,150

3,785

Utilities Expense230 230

-

Rent Expense1,000 1,000

-

Net Income

CLOSE DEBIT BALANCES IN EXPENSE ACCOUNTS TO INCOME

SUMMARY

Supplies Expense1,050 1,050

-

Depreciation Expense- Eq.

375 375 -

Salaries Expense1,610 1,610

-

Insurance Expense100 100

-

P 2

4 - 15

SUMMARY OF THE CLOSING PROCESS

1. Close Credit Balances in Revenue Accounts to Income Summary.

2. Close Debit Balances in Expense Accounts to Income Summary.

3. Close Income Summary to Owner’s Capital.4. Close Withdrawals Account to Owner’s

Capital.

4 - 16

END OF CHAPTER 4

Top Related