Languages

Pages

Legal

Competition from hubs in the Gulf and Turkey

Overview of academic and applied research Dr Guillaume Burghouwt [email protected] Director Airneth Head of section aviation economics, SEO www.airneth.nl 17 October 2012

Outline

• The Gulf and Turkish hub models • Gulf carrier competition & pricing • Answers from incumbent carriers • Some further points for discussion

The vertically integrated strategy of “Dubai Inc.”

• Dubai has prepared master plan to prepare for the post-oil era to establish Dubai as leading tourism, IT and financial destination

• Emirates Airlines essential instrument to achieve this goal

• Emirates part of Emirates Group: state-owned, globally active travel and tourism conglomerate, providing all kinds of aviation related services

• Emirates Group itself is part of a larger bundle of aviation-related activities, under responsibility of Sjeikh Ahmed bin Saeed Al Maktoum, including: – Dubai World Central Consortium (building of Jebel Ali airport city) – Dubai’s Department of Civil Aviation: regulator, operator of DXB,Dubai Duty

Free and Dubai Cargo Village

The vertically integrated strategy of “Dubai Inc.” (cont.)

• Sjeikh acts as an entrepreneur • Royal family involved in all parts of economy and public

administration: Difficult to distinguish between private and public property, between political leadership and commercial management. Result: – signicant financial resources and the ability of the state to

allocate and control developments that would be impossible in market-led economies

– Allignment of all stakeholders on the same goal: to increase the wealth of the emirate, its population and its rulers

– Quick decision making

Comparing cost structure Emirates to BA Eurocents/ATK Emirates British Airways EK vs BA (%)

Fuel/ATK 8.12 11.40 -29 Young fleet, proximity to oil production+facilities

Labour/ATK 4.36 12.01 -64 Two-tier tax free salary system; cheap labour

Landing and Nav/ATK 1.45 2.93 -51 Joint airline-airport ownership; cross subsidation charges from duty-free

Handling/ATK 1.69 5.42 -69 Low labour costs; scale advantages in monopoly

Maintenance/ATK 0.50 2.50 -80 New generation aircraft

Depreciation/ATK 1.34 3.84 -65 New generation aircraft

Distribution and sales/ATK

2.80 1.99 +41 Travel commissions, sales in countries with low Internet penetration rate; aggressive branding

Operating leases/ATK 2.83 0.38 +645 80% aircraft financed through operating leases

Total cost/ATK 26.56 43.69 -39

Total revenu/ATK 28.78 48.55 -41

Source: O’Connell (2011). The rise of the Arabian carriers. JATM 17(6), 339-346

0

50

100

150

200

250

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Num

ber o

f des

tinat

ions

Shar

e of

long

-hau

l des

tinat

ions

>2500km

<2500km

% long-haul

The network model of Gulf carriers: long-haul to long-haul. Turkish exception

Source: OAG, 3rd week 2012

Long-haul specialization partly driven by geography

Facebook network within a 2500km range

Focus on primary and secondary cities

• Gulf carriers do not only serve primary, but also secondary cities

Important feeder markets for European network carriers Newcomers from the Gulf do not have to compete against non-stop direct

travel options (=better quality) Entry easier for Gulf carriers than for European network carriers in relation

to slot times and charges Creates substantial competitive advantage in terms of travel time in certain

markets • E.g. HAM-DXB-SYD with Emirates instead of HAM-FRA-BKK-SYD with

Star

• Because Turkish can operate to Europe with a narrow-body fleet, it also feeders its hub from tertiary European cities

Turkish also serves many tertiary European cities. Its service tends to be relatively better to

lower ranked airports

0

10.000

20.000

30.000

40.000

50.000

60.000

LON

PA

R FR

A M

AD

BCN

M

UC

FCO

AM

S M

OS

PMI

MIL

O

SL

CPH

VIE

DUS

TXL

ARN

ZR

H DU

B M

AN

BRU

HA

M

AGP

HEL

LIS

NCE

AT

H GV

A PR

G ST

R ED

I CG

N

VCE

ALC

BHX

LED

BUD

BGY

CTA

TLS

IBZ

AYT

WAW

LY

S LP

A M

RS

OTP

TL

V BG

O

VKO

FA

O

SXF

GLA

CRL

NAP

KB

P BL

Q

BRS

OPO

TF

S RI

X SV

G TR

D PS

A PM

O

HER

BIO

VL

C LP

L HA

J LC

A SK

G BO

D CI

A CA

G SV

Q

BFS

GOT

NCL

BS

L TF

N

TRN

AC

E EM

A BR

I

Num

ber o

f sea

ts p

er w

eek

airports ranked accordining to total scheduled seat capacity

Emirates Etihad Qatar Turkish

Top-10

Top-20

Top-30

Source: OAG

The network model: connecting at night

• Core of the wave-system is concentrated during night-time – Curfews and flight

restrictions at destination airports

– Meteorological conditions during daytime at the hub

Wave-system Emirates at Dubai

Europe to Asia/ Aus

Aus/Asia/ME to Europe/AFR/US

Source: O’Connell 2011

Asia/ME to Europe/ME/AFR

Remarkable similarity between the hubs. Turkish supplements night and early morning waves with intensive

hub system during the day

0%

20%

40%

60%

80%

100%

120%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

Num

ber o

f dep

artu

res

per w

eek

rela

tive

to h

ighe

st

peak

-hou

r

Departure time window (UAE local time)

EY AUH QR DOH EK DXB TK IST

Hub connections offered by Turkish via Istanbul more diversified than

DXB, DOH and AUH

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

DXB DOH AUH IST

Shar

e of

mar

ket i

n to

tal h

ub

conn

ectiv

ity other

AFR ZO-EUR

M-O ZO-Europa

M-O NW-EUR

M-O AZ/PAC

ZO-Europa AZ/PAC

NW-EUR AZ/PAC

Source: OAG; SEO Netscan

Building a Gulf route

• Typical build-up pattern of an Emirates destination (Lohmann et al. 2009): 1. Always enter a new destination with a daily flight 2. When demand increases, scale up aircraft capacity 3. Later, increase frequency, as this is important to attract

high-yield business passenger 4. Ultimate mid-term goal is double daily on almost every

destination

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

0

50

100

150

200

250

300

350

400

Aver

age

freq

uenc

y pe

r wee

k

Aver

age

seat

capa

city

/flig

ht

average frequency/week average seat capacity

Route build-up Emirates at Hamburg Scale up to B777

Introduction double daily

building seat capacity again

Daily operation with A340

Source: OAG

Route build-up pattern Emirates at Amsterdam

0

1

2

3

4

5

6

7

8

0

100

200

300

400

500

600

2008

01

2008

03

2008

05

2008

07

2008

09

2008

11

2009

01

2009

03

2009

05

2009

07

2009

09

2009

11

2010

01

2010

03

2010

05

2010

07

2010

09

2010

11

2011

01

2011

03

2011

05

2011

07

2011

09

2011

11

2012

01

2012

03

2012

05

2012

07

2012

09

Aver

age

freq

uenc

y pe

r wee

k

Aver

age

seat

cap

acity

/flig

ht

average frequency/week average seat capacity

Entry with daily flight B777-200LR, mixed with B777-300ER

Scale up to full B777-300ER operation

Scale up to A380

Source: OAG

Strengths and weaknesses Emirates and Dubai

Strengths • Geographical location of the hub • A380 allows for growth at slot

constrained airports • No legacy costs • Low unit costs • High labour productivity • High service-level • Strong brand (marketing) • Open Skies policy by UAE

government • Favourable political environment

(“Dubai Inc.”) – Strong vertical integration – Quick decision-making – Lack of NIMBY-culture

• Diversity of markets served

Weaknesses • Temperature and humidity constrain

middle-of-the-day operations at DXB • Limited short-haul feeder potential • No alliance membership • Related to destination

development/OD growth: • Sterility and homogeinity of the

destination (Henderson 2006) • Low level of repeat visits to Dubai • Tourism depends on large extent on

stop-over market. Average stay is short (2.5 days)

Opportunities and threats Emirates and Dubai

Opportunities • 3.5 billion people within

8 hrs flying time • Central to many

emerging, underserved economies – Clark: “Africa is ripe fruit

that only needs to be picked”

• Alliances?

Threats • World economy • Political and economic instability

in the region* • Terrorism • Lobbying by competitors, calling

for legal protection against unfair competition

• Aggressive competition from the neighbours; overcapacity?

• Dependency on expatriate professionals *Source: M. Levine (2013). Is the Gulf airline boom a

bubble? Airneth column 12 June 2013. www.airneth.nl

Turkish Airlines and Istanbul compose a somewhat different story

• Turkish Airlines partly privatized in 2004-2006 49% of shares still held by Republic of Turkey • Liberalization domestic market in 1996

Opportunities: • Benefits from domestic market of 70 million people, with a rapidly increasing propensity to fly • Geographical location in some ways better than that of Gulf hubs:

– Domestic market with over 70 million people, with a rapidly increasing propensity to fly – Short-haul fleet can cover large part of population centres in Europe, North-Africa, Middle

East and Russia • Strong Turkish diaspora in Western-Europe • Part of STAR alliance

Major bottlenecks: – fierce congestion at the Istanbul hub – But third Istanbul Airport planned for 90-150 million passengers, scheduled to be opened in

2015 – Fairly restrictive bilaterals – Landside accessibility

Outline

• The Gulf and Turkish hub models • Gulf carrier competition & pricing • Answers from incumbent carriers • Some further points for discussion

Competition for European hubs in transfer market has increased during last decade

Number of alternatives for transfer passengers to best connection where European hubs offer at least one connection, 2002-2011

Source: Copenhagen Economics/SEO 2012

Turkish larger competitor to SkyTeam at AMS than Emirates in terms of

market overlaps

0%

10%

20%

30%

40%

50%

60%

Parijs Charles de Gaulle

(CDG)

Dubai (DXB) Frankfurt (FRA) Istanbul (IST) Londen Heathrow

(LHR)

München (MUC)

% o

f mar

kets

on

whi

ch h

ub o

verla

ps w

ith

Amst

erda

m

2009

2010

2011

New Emirates services to secondary cities stimulate demand to Dubai and beyond destinations, without only limited cannibalization of demand of incumbent airlines

Source: Grimme (2011). The growth of Arabian airlines from a German perspective-A study of the impacts of new air services to Asia. Journal of Air Transport Management

EK traffic growing quickly…

..but traffic via FRA and MUC…

..and other hubs as well

Demand generation

Market between Düsseldorf and Asia

Via DXB

Via FRA/MUC

Via AMS/LON/PAR

Emirates on average 22-28% market share on directly served overlap destinations in Asia; share increases with

frequency to Dubai

Emirates has on average 28% market share on overlapping STAR destinations in Asia out of secondary city Hamburg

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Market Share FRA/MUC Market Share DXB

Source: Grimme (2011) From Dusseldorf From Hamburg

via FRA/MUC via DXB via FRA/MUC via DXB

Top 10 overlap 20% 32% 43% 27%

Top 28 overlap 20% 34% 42% 28% Total Asia destinations 21% 28% 35% 22%

Market share Emirates of twice-daily services to Dubai on overlapping destinations in Asia 6% higher than for single daily Emirates service

EK DUS-DXB: 14x/week

EK HAM-DXB: 7x/week

Source: Grimme (2011)

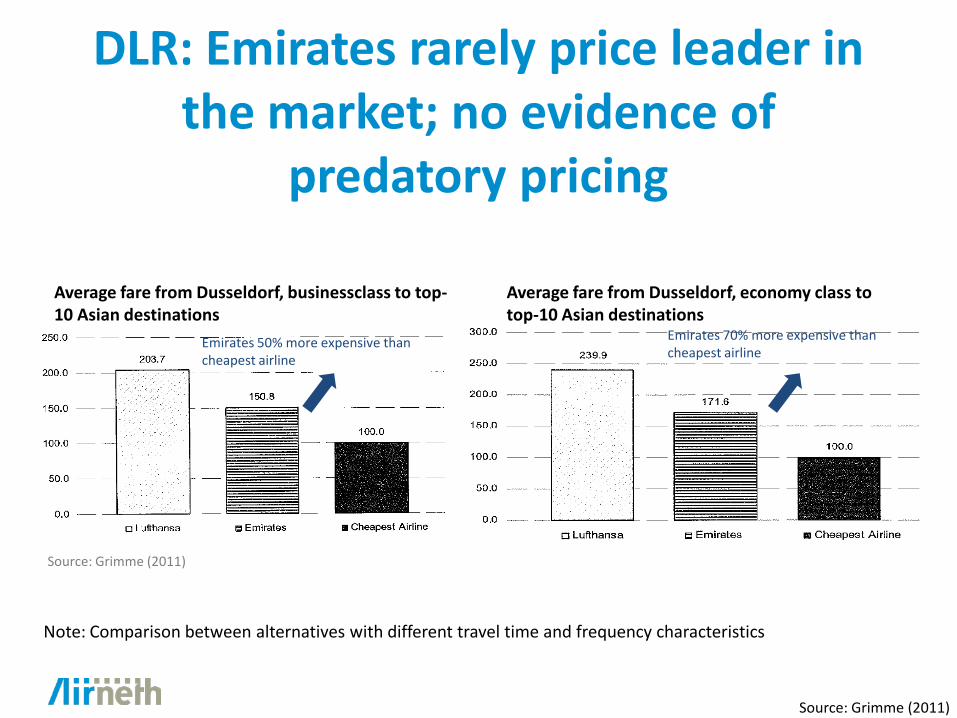

DLR: Emirates rarely price leader in the market; no evidence of

predatory pricing

Average fare from Dusseldorf, businessclass to top-10 Asian destinations

Average fare from Dusseldorf, economy class to top-10 Asian destinations

Emirates 50% more expensive than cheapest airline

Source: Grimme (2011)

Emirates 70% more expensive than cheapest airline

Note: Comparison between alternatives with different travel time and frequency characteristics

Source: Grimme (2011)

Outline

• The Gulf and Turkish hub models • Gulf carrier competition & pricing • Answers from incumbent carriers • Conclusions & research agenda

The answers from European network carriers

• Cost restructuring • Focus on markets outside reach of Gulf carriers

– Markets on which travel times via Gulf are substantially longer than via European hubs, (e.g. UK to China) or where Gulf is not an option (Transatlantic)

– Market size: move towards increasingly smaller markets • Searching for alliances and joint ventures “ If you can’t beat

them, join them” • Lobbying, limitation of traffic rights, fair competition clauses

in EC external aviation policy

Gulf carriers have entered the alliance game

• Turkish Airlines part of STAR-alliance since 2008 • Qatar Airways joining Oneworld • Participation Etihad in Air Berlin • Cooperation/codesharing Etihad with Air France-KLM • Cooperation Etihad and Garuda (changing AMS operation from DXB to AUH) • Cooperation Emirates and Qantas • But: already many codeshare agreements and interlining, EK showing U2 beyond

cnx’ • Impact of alliances and joint ventures:

– Larger indirect network for European consumers into India, Asia and Australia – More efficient schedules, larger FFP – In case of joint ventures:

• Price-coordination • Reduction of overcapacity on the Europe-Middle East market • Less competition • Better yields

Outline

• The Gulf and Turkish hub models • Gulf carrier competition & pricing • Answers from incumbent carriers • Some further points for discussion

Outline

• The Gulf and Turkish hub models • Gulf carrier competition & pricing • Answers from incumbent carriers • Further points for discussion

Remaining questions and further points for discussion

• To what extent do Gulf carriers compete with EU network carriers?

• How do Gulf carriers price their flights in comparison to EU network carriers. Predatory pricing?

• What is the impact of Gulf carrier entry on ticket prices in the market?

• What will be the impact of aircraft deliveries on market shares and profitability?

• How will Gulf carrier competition impact networks of European carriers in longer-run? What role will alliances play? Will these impact outweigh the economic benefits associated with Gulf carrier service?

Top Related