Languages

Pages

Legal

Chapter - VI

Profitability Analysis of Indian General Insurance Industry

As a result of the various reforms introduced by the Government of

India in the insurance sector, private companies have made their entry into the

field. It has thrown a new challenge before the public sector companies. Now it

has become quite tough for the companies to work in a competitive

environment. It has resulted in reduction of product prices, increases in

distribution cost and better service quality. There is uncertainty regarding the

effect of these reforms on the profitability of these companies which is

important for the safety and soundness of insurance industry.

6.1 Concept of Profitability

The term „profit‟ is an accounting concept which shows the excess of

income over expenditure viewed during a specified period of time. Profit is the

main reason for the continued existence of every commercial organization. On

the other hand, the term 'profitability' is a relative measure where profit is

expressed as a ratio, generally as a percentage. Profitability depicts the

relationship of the absolute amount of profit with various other factors.

Profitability is the most important and reliable indicator as it gives a broad

indicator of the ability of a insurance company to raise its income level. In

practice, executives define profits as the difference between total earnings from

all earning assets and total expenditure on managing entire asset-liabilities

portfolio (Kaur and Kapoor, 2007).

6.2 Drivers of Profitability

To analyze the drivers of profitability, it is useful to decompose ROE

into its main components. Profits are determined first by underwriting

performance (losses and expenses, which are affected by product pricing, risk

selection, claims management, and marketing and administrative expenses);

and second, by investment performance, which is a function of asset allocation

and asset management as well as asset leverage. The first fork of the

decomposition shows that an insurer‟s ROE is determined by earnings after

155

taxes realized for each unit of net premiums (or profit margin) and by the

amount of capital funds used to finance and secure the risk exposure of each

premium unit (solvency). The after-tax profit margin equals the pre-tax profit

margin times one minus the corporate tax rate. The tax rate depends upon

individual tax strategies and is otherwise an exogenous parameter of the

industry. The pre-tax profit margin is the sum of the underwriting result (or

underwriting margin) and the investment result. The investment result is

determined by total investment yield (relative performance including realized

capital gains) multiplied by invested assets (asset leverage).The underwriting

result - in per cent of net premiums - is determined by the loss ratio, the

expense ratio (Rudolf, 2001). The benefit of this type of decomposition is to

separate the various factors affecting profitability, isolating them for further

analysis. Though they will be analyzed separately, they are interrelated through

the decision-making processes of insurers.

6.3 Comparative Profitability Analysis of the Public and Private Sector

General Insurance Companies in the Post-reform Period

Claim Ratio

Claims incurred ratio may be defined as total net incurred claims divided

by net written premium (NWP). This indicator is a good complement to the

picture of economics, client value and service quality of the various insurance

schemes. The acceptable level for this indicator cannot be determined, but

generally, the higher it is, the better it would be.

156

Table 6.1

Claim Ratio of General Insurance Companies during the Post-reform

Period

(Percentage)

Name of the

Company 2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

Mean

Med

ian

S.D

.

National 76.01 84.10 79.92 105.49 83.85 89.05 86.40 83.98 10.33

New India 82.46 74.65 74.58 83.64 76.68 85.01 79.50 79.57 4.73

Oriental 77.23 78.09 86.04 82.57 81.91 90.40 82.71 82.24 4.94

United India 91.06 85.63 91.99 91.77 84.68 87.00 88.69 89.03 3.30

Mean 81.69 80.62 83.13 90.87 81.78 87.86 84.33 83.98 6.97

Median 79.84 81.095 82.98 87.705 82.88 88.025 83.975

S.D. 6.84 5.13 7.53 10.57 3.59 2.36 6.96

Royal

Sundaram 53.68 57.33 56.40 54.45 52.30 55.93 55.02 55.19 1.88

Reliance 99.48 68.73 61.91 62.01 34.34 56.13 63.77 61.96 21.12

IFFCO-Tokio 40.70 54.63 50.79 51.03 68.65 68.42 55.70 52.83 10.97

TATA AIG 47.41 44.84 48.31 47.55 49.81 46.77 47.45 47.48 1.65

Bajaj Allianz 59.01 52.59 47.22 58.68 53.44 53.96 54.15 53.70 4.36

ICICI Lombard 39.89 53.96 48.23 53.04 56.10 69.02 53.37 53.50 9.60

CHOLAMAN

DALAM 13.78 43.23 61.16 69.94 44.44 48.47 46.84 46.46 19.25

HDFC CHUBB 13.34 34.99 58.94 55.50 60.12 68.49 48.57 57.22 20.55

Mean 45.91 51.29 54.12 56.53 52.40 58.40 53.11 53.82 13.60

Median 44.055 53.275 53.595 54.975 52.87 56.03 53.82

S.D. 27.41351 10.23206 6.16237 6.99937 10.24469 9.10119 13.59524

Source: IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-tailed)

Mann- Whitney Test Claim Ratio -6.61 0.00

Table 6.1 exhibits the ratio of claim incurred as a percentage of net

written premium of the public and private sector general insurance companies

on a year to year basis during the period 2002-03 to 2007-08. The table also

reveals the mean, median and standard deviation for each general insurance

company over the study period and also for each year across the 12 companies.

The sector-wise analysis shows that the claim incurred ratio of the public sector

157

general insurance companies is higher than that of the private sector general

insurance companies throughout the study period. Among the public sector

companies, United India Insurance Co. Ltd. showed a maximum average claim

ratio of 88.69 per cent followed by National Insurance Co. Ltd. and Oriental

Insurance Co. Ltd. with respective percentages of 86.40 per cent and 82.71 per

cent respectively. However, among the private insurers, Reliance General

Insurance Co. showed a maximum average claim ratio of 63.77 per cent

followed by IFFCO-Tokio and Royal Sundaram with the respective

percentages of 55.70 per cent and 55.02 per cent. Cholamandalam General

Insurance Co., the private insurer showed the least average claim ratio of 46.84

per cent followed by TATA-AIG with the ratio of 47.45 per cent. The average

claim ratio of all the public sector insurers is 84.33 per cent and that of private

insurers is 53.11 per cent, which clearly indicates a huge difference between

the public and private insurers' claim ratio. The standard deviation values of the

public and private sector general insurance companies are 6.97 and 13.60

which exhibit that public insurers are more consistent than the private insurers

in paying claim to the customers. Year-wise analysis indicates that the average

claim ratio of the public sector is the highest, i.e., 90.87 per cent in the year

2005-06 followed by 87.86 per cent in the year 2007-08. The private insurers'

average claim ratio is also the highest in the year 2005-06 followed by the year

2007-08. A closer investigation of the product portfolio, reveals that it is

mainly due to the fact that the private companies are concentrating more on the

creamy business. In respect of loss making portfolio, such as motor business,

they have avoided to enter these businesses to reduce their claim incurred ratio.

Further investigation reveals that public sector insurance companies do not get

much of their business reinsured in contrast to the private sector players, who

get most of the business reinsured to reduce their claim incurred ratio. Mann-

Whitney test further shows that there is significant difference between the

claim ratio of the public and the private sector general insurance companies.

158

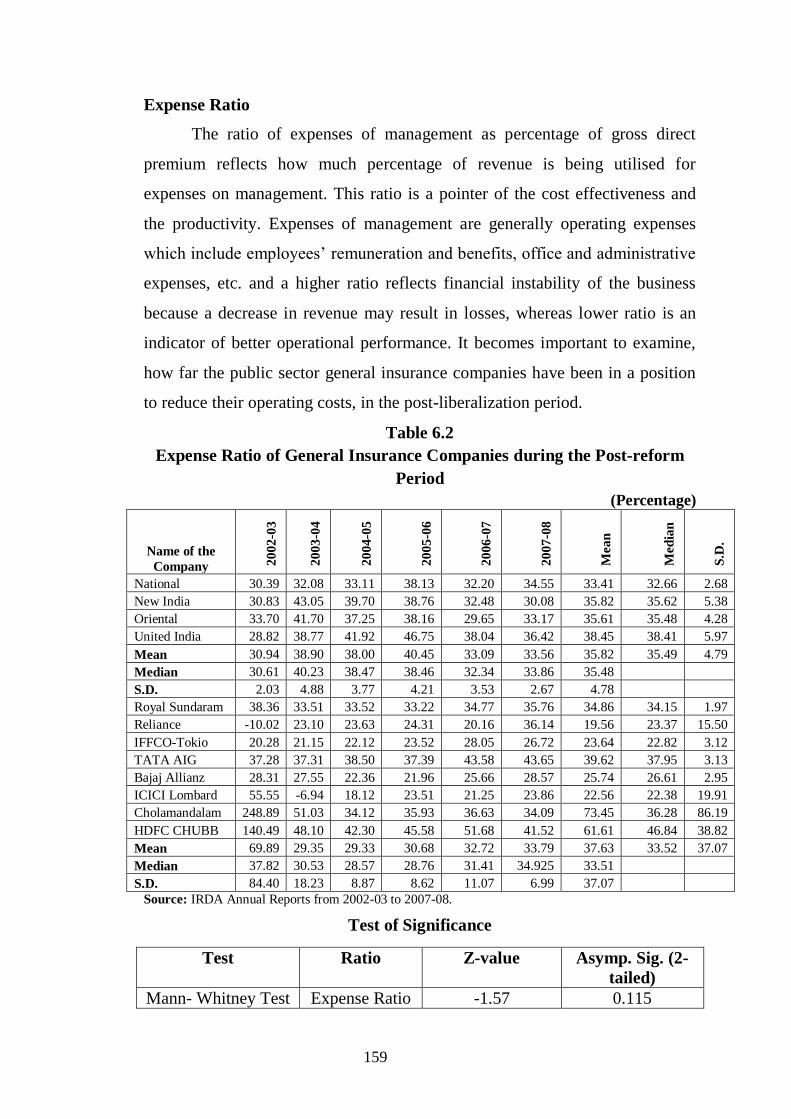

Expense Ratio

The ratio of expenses of management as percentage of gross direct

premium reflects how much percentage of revenue is being utilised for

expenses on management. This ratio is a pointer of the cost effectiveness and

the productivity. Expenses of management are generally operating expenses

which include employees‟ remuneration and benefits, office and administrative

expenses, etc. and a higher ratio reflects financial instability of the business

because a decrease in revenue may result in losses, whereas lower ratio is an

indicator of better operational performance. It becomes important to examine,

how far the public sector general insurance companies have been in a position

to reduce their operating costs, in the post-liberalization period.

Table 6.2

Expense Ratio of General Insurance Companies during the Post-reform

Period

(Percentage)

Name of the

Company 20

02-0

3

20

03-0

4

20

04-0

5

20

05-0

6

20

06-0

7

20

07-0

8

Mea

n

Med

ian

S.D

.

National 30.39 32.08 33.11 38.13 32.20 34.55 33.41 32.66 2.68

New India 30.83 43.05 39.70 38.76 32.48 30.08 35.82 35.62 5.38

Oriental 33.70 41.70 37.25 38.16 29.65 33.17 35.61 35.48 4.28

United India 28.82 38.77 41.92 46.75 38.04 36.42 38.45 38.41 5.97

Mean 30.94 38.90 38.00 40.45 33.09 33.56 35.82 35.49 4.79

Median 30.61 40.23 38.47 38.46 32.34 33.86 35.48

S.D. 2.03 4.88 3.77 4.21 3.53 2.67 4.78

Royal Sundaram 38.36 33.51 33.52 33.22 34.77 35.76 34.86 34.15 1.97

Reliance -10.02 23.10 23.63 24.31 20.16 36.14 19.56 23.37 15.50

IFFCO-Tokio 20.28 21.15 22.12 23.52 28.05 26.72 23.64 22.82 3.12

TATA AIG 37.28 37.31 38.50 37.39 43.58 43.65 39.62 37.95 3.13

Bajaj Allianz 28.31 27.55 22.36 21.96 25.66 28.57 25.74 26.61 2.95

ICICI Lombard 55.55 -6.94 18.12 23.51 21.25 23.86 22.56 22.38 19.91

Cholamandalam 248.89 51.03 34.12 35.93 36.63 34.09 73.45 36.28 86.19

HDFC CHUBB 140.49 48.10 42.30 45.58 51.68 41.52 61.61 46.84 38.82

Mean 69.89 29.35 29.33 30.68 32.72 33.79 37.63 33.52 37.07

Median 37.82 30.53 28.57 28.76 31.41 34.925 33.51

S.D. 84.40 18.23 8.87 8.62 11.07 6.99 37.07

Source: IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney Test Expense Ratio -1.57 0.115

159

Table 6.2 reports the results of insurer-wise expense of management

ratio from the year 2002-03 to 2007-08. The table also reveals mean, median

and standard deviation for each general insurance company over the study

period and also for each year across the 12 companies. The results show that

average expense of management ratio of the public sector general insurance

companies is 35.82 per cent, whereas that of the private sector companies is

37.63 per cent which is higher by 1.81 per cent in the case of private sector

general insurance companies during the period 2002-03 to 2007-08. However,

the Mann-Whitney test results indicate that the gap in expense of management

ratio of both the public and private sector companies is insignificant. Among

the public sector insurers, United India has registered the highest expense of

management ratio (38.45 per cent) followed by New India (35.82 per cent),

Oriental (35.61 per cent) and National (33.41 per cent). Among the private

sector insurers, Cholamandalam has exhibited the highest average expense ratio

of 73.45 per cent followed by HDFC CHUBB (61.61 per cent) and Tata-AIG

39.62 per cent. However, Reliance has registered the least average expense of

management ratio of 19.56 per cent followed by ICICI Lombard with 22.56 per

cent. Year-wise results explain that the average expense ratio of the public

sector companies during the year 2002-03 was 30.94 per cent which increased

to 40.45 per cent in the year 2005-06. However, it came down to 33.56 per cent

during the year 2007-08. Among the private sector insurers, the average

expense ratio in the year 2002-03 was 69.89 per cent which reduced to 33.79

per cent in the year 2007-08. So, it is evident from the table that in the initial

years of reforms the private sector had to spend more on advertisements,

commission and other expenses. But with the passage of time, these private

sector general insurance companies took various cost effective measures which

led to improve their operational performance. The standard deviation of

expense of management ratio in the case of public sector companies is 4.79 per

cent, whereas it is 37.07 per cent in private sector companies. It is clear that

there was wide variation in the expense ratio of the private sector general

insurance companies during the period 2002-03 to 2007-08.

160

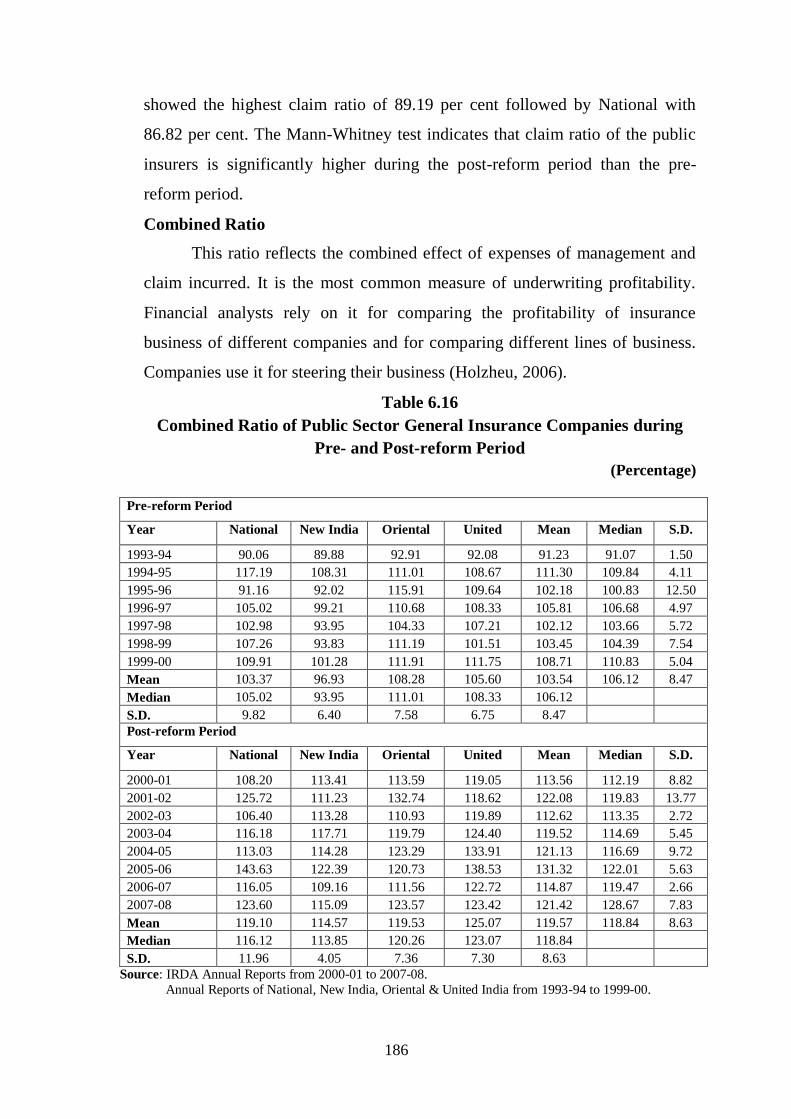

Combined Ratio

This ratio reflects the combined effect of expenses of management and

claim incurred. It is the most common measure of underwriting profitability.

Financial analysts rely on it for comparing the profitability of insurance

business of different companies and for comparing different lines of business.

The companies use it for steering their business (Holzheu, 2006).

Table 6.3

Combined Ratio of General Insurance Companies during the Post-reform

Period

(Percentage) Name of the

Company 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 Mean Median S.D.

National 106.40 116.18 113.03 143.63 116.05 123.60 119.82 116.12 12.92

New India 113.28 117.71 114.28 122.39 109.16 115.09 115.32 114.69 4.45

Oriental 110.93 119.79 123.29 120.73 111.56 123.57 118.31 120.26 5.67

United India 119.89 124.40 133.91 138.53 122.72 123.42 127.14 123.91 7.33

Mean 112.62 119.52 121.13 131.32 114.87 121.42 120.15 119.84 8.89

Median 112.10 118.75 118.78 130.46 113.80 123.49 119.84

S.D. 5.62 3.57 9.67 11.48 5.960 4.22 8.89

Royal

Sundaram 92.04 90.84 89.92 87.67 87.07 91.69 89.87 90.38 2.08

Reliance 89.47 91.84 85.54 86.32 54.50 92.27 83.32 87.90 14.39

IFFCO-Tokio 60.97 75.78 72.91 74.55 96.71 95.13 79.34 75.17 13.90

TATA AIG 84.69 82.15 86.80 84.95 93.39 90.42 87.07 85.88 4.14

Bajaj Allianz 87.33 80.14 69.58 80.64 79.09 82.53 79.89 80.39 5.83

ICICI Lombard 95.44 47.02 66.35 76.55 77.35 92.87 75.93 76.95 17.87

Cholaman

Dalam 262.67 94.27 95.28 105.86 81.07 82.56 120.28 94.78 70.35

HDFC CHUBB 153.83 83.09 101.24 101.08 111.80 110.01 110.18 105.63 23.68

Mean 115.81 80.64 83.45 87.20 85.12 92.18 90.74 87.20 29.95

Median 90.75 82.62 86.17 85.63 84.07 91.98 87.2

S.D. 64.88 15.01 12.59 11.10 16.77 8.58 29.94

Source: Compiled from IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney

Test

Combined Ratio -6.236 0.00

The insurer-wise combined ratio results for the period 2002-03 to 2007-

08 have been exhibited in table 6.3. The table also reflects the mean, median

and standard deviation for each general insurance company over the study

period. The results reveal that the average combined ratio in the case of public

sector general insurance companies during the period 2002-03 to 2007-08 is

161

120.15 per cent, whereas it is 90.74 per cent in private sector insurance

companies. It is evident that combined ratio of the public sector is higher by

29.41 per cent than the private sector. This has been due to higher claim ratio

of the public sector. Among the public insurers, United India exhibits the

highest average combined ratio of 127.14 per cent followed by National 119.82

per cent, Oriental 118.31 per cent and New India 115.32 per cent. However,

among the private insurers, Cholamandalam has exhibited the highest average

combined ratio of 120.28 per cent followed by HDFC CHUBB 110.18 per cent,

Royal Sundaram 89.87 per cent, Tata AIG 87.07 per cent, Reliance 83.32 per

cent, Bajaj Allianz 79.89 per cent, IFFCO-Tokio 79.34 per cent and ICICI

Lombard 75.93 per cent. Year-wise, the average combined ratio of the public

sector in the year 2002-03 was 112.62 per cent which increased to 131.32 per

cent in the year 2005-06. Again, it showed a decreasing trend and reached at

121.42 per cent in the year 2007-08. The average combined ratio of the private

sector general insurance companies in the year 2002-03 was 115.81 per cent

which reduced to 92.18 per cent in the year 2007-08. Both the public and

private sector general insurance companies showed a standard deviation of 8.89

per cent and 29.95 per cent respectively. It indicates that the variation in the

combined ratio of the private sector general insurance companies is higher. The

results of Mann-Whitney test also indicate that the combined ratio of the public

sector is significantly higher than that of the private sector general insurance

companies.

Underwriting Results Ratio

The underwriting results ratio of a general insurance company is

depicted by taking net written premium minus increase in the unexpired risk

reserve minus expense of management minus claim incurred minus

commission. The underwriting results indicate the performance of an insurance

company from core insurance business. The underwriting results ratio is

calculated by dividing underwriting results to net written premium.

162

Table 6.4

Underwriting Results Ratio of General Insurance Companies during the

Post-reform Period

(Percentage)

Name of the

Company

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

Mean

Med

ian

S.D

.

National -14.14 -21.00 -18.96 -40.64 -19.13 -28.92 -23.80 -20.07 9.55

New India -13.82 -18.96 -17.57 -27.50 -13.72 -17.18 -18.12 -17.38 5.05

Oriental -13.21 -22.77 -27.56 -26.52 -18.12 -23.65 -21.97 -23.21 5.42

United India -19.08 -25.09 -34.37 -39.94 -28.90 -29.62 -29.50 -29.26 7.23

Mean -15.06 -21.95 -24.62 -33.65 -19.97 -24.84 -23.35 -21.89 7.79

Median -13.98 -21.88 -23.26 -33.72 -18.62 -26.28 -21.88

S.D. 2.70 2.60 7.86 7.68 6.40 5.76 7.78

Royal Sundaram -21.59 -6.24 -3.98 -3.65 -1.43 -8.05 -7.49 -5.11 7.27

Reliance -41.10 -15.63 -8.02 10.86 -6.07 -20.49 -13.41 -11.83 17.28

IFFCO-Tokio -4.57 -0.61 1.79 -2.21 -2.39 -8.43 -2.74 -2.30 3.50

TATA AIG -19.27 -6.02 0.79 -0.15 -1.61 -4.46 -5.12 -3.04 7.39

Bajaj Allianz -2.07 0.39 7.81 3.29 1.55 -1.77 1.53 0.97 3.68

ICICI Lombard -34.05 13.90 0.84 -4.65 -3.82 -4.82 -5.43 -4.24 15.72

Cholamandalam -237.78 -44.95 -15.88 -16.17 -1.15 -5.06 -53.50 -16.03 91.57

HDFC CHUBB -147.39 -38.15 -12.42 -4.77 -6.41 -20.47 -38.27 -16.45 54.83

Mean -63.48 -12.17 -3.63 -2.18 -2.67 -9.19 -15.55 -4.71 40.35

Median -27.82 -6.13 -1.595 -2.93 -2 -6.55 -4.71

S.D. 84.29 20.01 7.98 7.69 2.66 7.27 40.34

Source: Compiled from IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-tailed)

Mann- Whitney Test Underwriting

Results Ratio

-4.539 0.00

The underwriting results to net written premium ratio of both the public

and private sector general insurance companies from 2002-03 to 2007-08 have

been presented in table 6.4. It is clear that the average underwriting results ratio

of the public sector general insurance companies is -23.35 per cent and that of

private sector companies is -15.55 per cent. Thus, the underwriting losses of

public sector companies are higher as compared to the private sector

companies. Among the public sector companies, United India has registered the

highest average underwriting losses of -29.50 per cent followed by National -

23.80 per cent, Oriental -21.97 per cent and New India -18.12 per cent which

means that all the public sector general insurance companies have shown huge

163

underwriting losses. However, among the private insurers, Cholamandalam has

shown the highest average underwriting loss of -53.50 per cent followed by

HDFC CHUBB -38.27 per cent, Reliance -13.41 per cent, Royal Sundaram -

7.49 per cent, ICICI Lombard -5.43 per cent, Tata AIG -5.12 per cent and

IFFCO-Tokio -2.74 per cent of all the private insurers, only Bajaj Allianz

earned average underwriting profits of 1.53 per cent. Year-wise, the public

insurers showed an increasing trend during the period 2002-03 to 2005-06,

when average underwriting losses increased from -15.06 per cent to -33.65 per

cent and again reduced to -24.84 per cent in the year 2007-08. However, the

private insurers showed decreasing trend except during the year 2007-08. The

average underwriting losses of the private sector companies during the year

2002-03 were -63.48 per cent which reduced to just -2.67 per cent in the year

2006-07 and again increased to -9.19 per cent in the year 2007-08. All the

private insurers except Cholamandalam and HDFC CHUBB, exhibited

underwriting losses lower than the public sector insurers. The standard

deviation of the underwriting results ratio of the public insurers is 7.79 per

cent, whereas that of the private insurers is 40.35 per cent which clearly

indicates that the variation in underwriting results of the private sector general

insurance companies is higher. The Mann-Whitney test also reveals that there

is a significant gap between underwriting losses of the public and private

insurers. The main reason for higher underwriting losses of the public insurers

is mainly ascribed to low reinsurance of their business and higher expenses of

management and incurred claim. Their excessive management expenses have

been higher due to massive strength of manpower. On the other hand, private

companies get most of their business reinsured to reduce their losses from

underwriting. Moreover, they have minimum staff strength and advanced

technology at their disposal. So, public sector general insurance companies

need to reduce the staff strength and use more advanced technology to compete

with the private sector. The general insurance business in India has been

detariffed with effect from 1st January, 2007; and even companies are allowed

to change the policy wordings with effect from 1st April, 2008. Now, it is the

164

right time for the public sector to revisit their loss making portfolios to improve

upon their underwriting results.

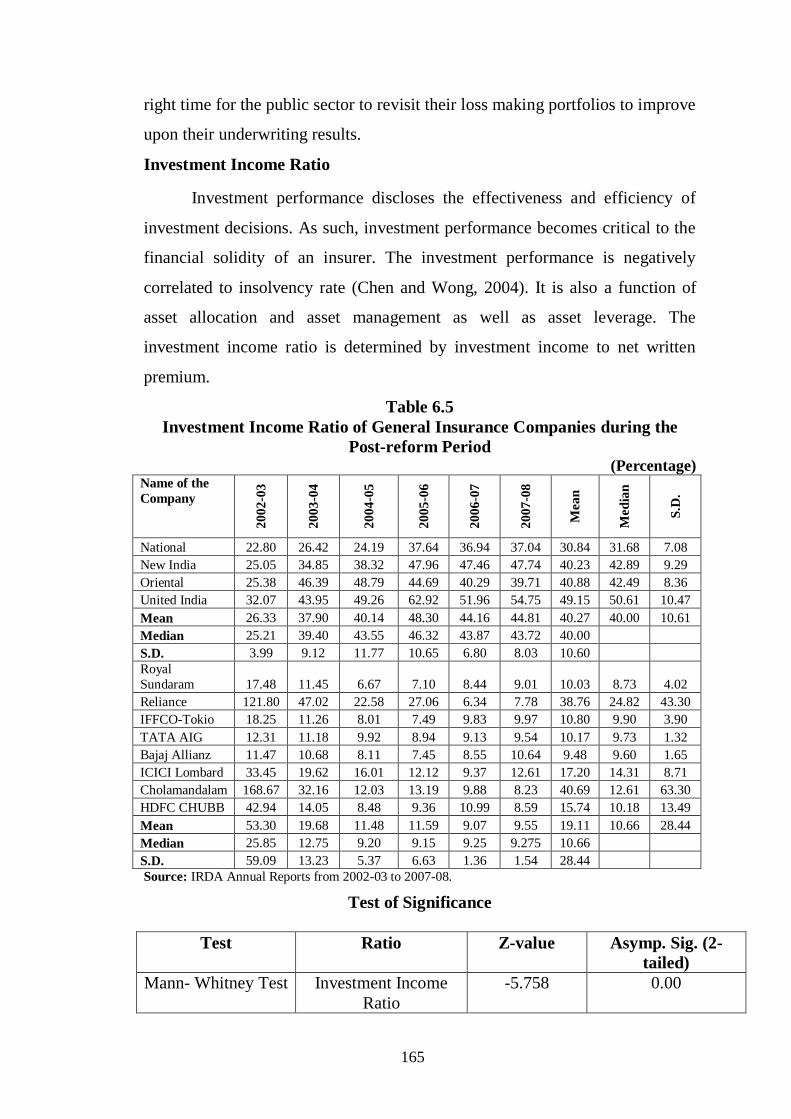

Investment Income Ratio

Investment performance discloses the effectiveness and efficiency of

investment decisions. As such, investment performance becomes critical to the

financial solidity of an insurer. The investment performance is negatively

correlated to insolvency rate (Chen and Wong, 2004). It is also a function of

asset allocation and asset management as well as asset leverage. The

investment income ratio is determined by investment income to net written

premium.

Table 6.5

Investment Income Ratio of General Insurance Companies during the

Post-reform Period (Percentage)

Name of the

Company

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

Mea

n

Med

ian

S.D

.

National 22.80 26.42 24.19 37.64 36.94 37.04 30.84 31.68 7.08

New India 25.05 34.85 38.32 47.96 47.46 47.74 40.23 42.89 9.29

Oriental 25.38 46.39 48.79 44.69 40.29 39.71 40.88 42.49 8.36

United India 32.07 43.95 49.26 62.92 51.96 54.75 49.15 50.61 10.47

Mean 26.33 37.90 40.14 48.30 44.16 44.81 40.27 40.00 10.61

Median 25.21 39.40 43.55 46.32 43.87 43.72 40.00

S.D. 3.99 9.12 11.77 10.65 6.80 8.03 10.60

Royal

Sundaram 17.48 11.45 6.67 7.10 8.44 9.01 10.03 8.73 4.02

Reliance 121.80 47.02 22.58 27.06 6.34 7.78 38.76 24.82 43.30

IFFCO-Tokio 18.25 11.26 8.01 7.49 9.83 9.97 10.80 9.90 3.90

TATA AIG 12.31 11.18 9.92 8.94 9.13 9.54 10.17 9.73 1.32

Bajaj Allianz 11.47 10.68 8.11 7.45 8.55 10.64 9.48 9.60 1.65

ICICI Lombard 33.45 19.62 16.01 12.12 9.37 12.61 17.20 14.31 8.71

Cholamandalam 168.67 32.16 12.03 13.19 9.88 8.23 40.69 12.61 63.30

HDFC CHUBB 42.94 14.05 8.48 9.36 10.99 8.59 15.74 10.18 13.49

Mean 53.30 19.68 11.48 11.59 9.07 9.55 19.11 10.66 28.44

Median 25.85 12.75 9.20 9.15 9.25 9.275 10.66

S.D. 59.09 13.23 5.37 6.63 1.36 1.54 28.44

Source: IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney Test Investment Income

Ratio

-5.758 0.00

165

Table 6.5 highlights the investment income to net written premium ratio

of the public and private insurers for the period 2002-03 to 2007-08. The

results indicate that the average investment income ratios of the public and

private insurers are 40.27 per cent and 19.11 per cent respectively. Thus, it is

21.16 per cent higher in the case of public sector insurers. Among the public

sector insurers, United India exhibits the highest average investment income

ratio of 49.15 per cent followed by Oriental 40.88 per cent, New India 40.23

per cent and National 30.84 per cent. However, among the private insurers,

Cholamandalam exhibits the highest average investment income ratio of 40.69

per cent followed by Reliance 38.76 per cent, ICICI Lombard 17.20 per cent,

HDFC CHUBB 15.74 per cent, IFFCO-Tokio 10.80 per cent, Tata AIG 10.17

per cent, and Royal Sundaram 10.03 per cent. Bajaj Allianz has shown the least

average investment income ratio. There is a wide gap in the investment income

ratio of Cholamandalam and Reliance with other private sector insurance

companies and this is mainly due to the investment income ratio during the first

two years.

Year-wise, the average investment income of all the public insurers in

the year 2002-03 was 26.33 per cent which showed an increasing trend up to

2005-06 when it rose to 48.30 per cent. Then it showed a downward trend and

became 44.81 per cent in the year 2007-08. However, the private insurers'

average investment income ratio continuously exhibited a downward trend and

during the period 2002-03 to 2007-08, it decreased from 53.30 per cent to 9.55

per cent. The standard deviation of investment income ratio of the public

insurers is 10.61 per cent, while it is 28.44 per cent in the case of private

insurers which explains more variation in the investment income of the private

insurers. It brings out that the private sector has accumulated fewer

underwriting losses and generated less investment income and having been in

business much longer, the public sector companies have considerable

investment portfolios and have benefited greatly from the strong performance

of the Indian economy. The substantial investment portfolios of the public

sector have compensated for their relatively weaker underwriting performance.

166

The Mann-Whitney test also indicates that the gap in the investment income of

public sector insurance companies is significantly greater than that of the

private sector.

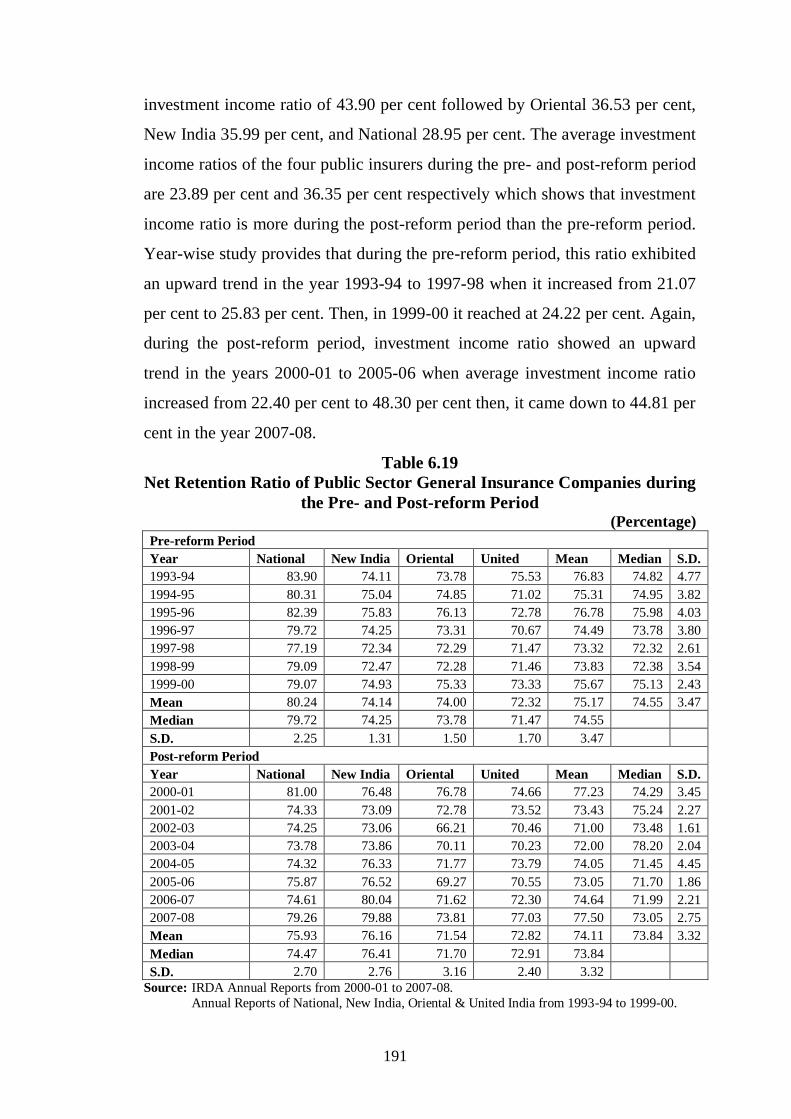

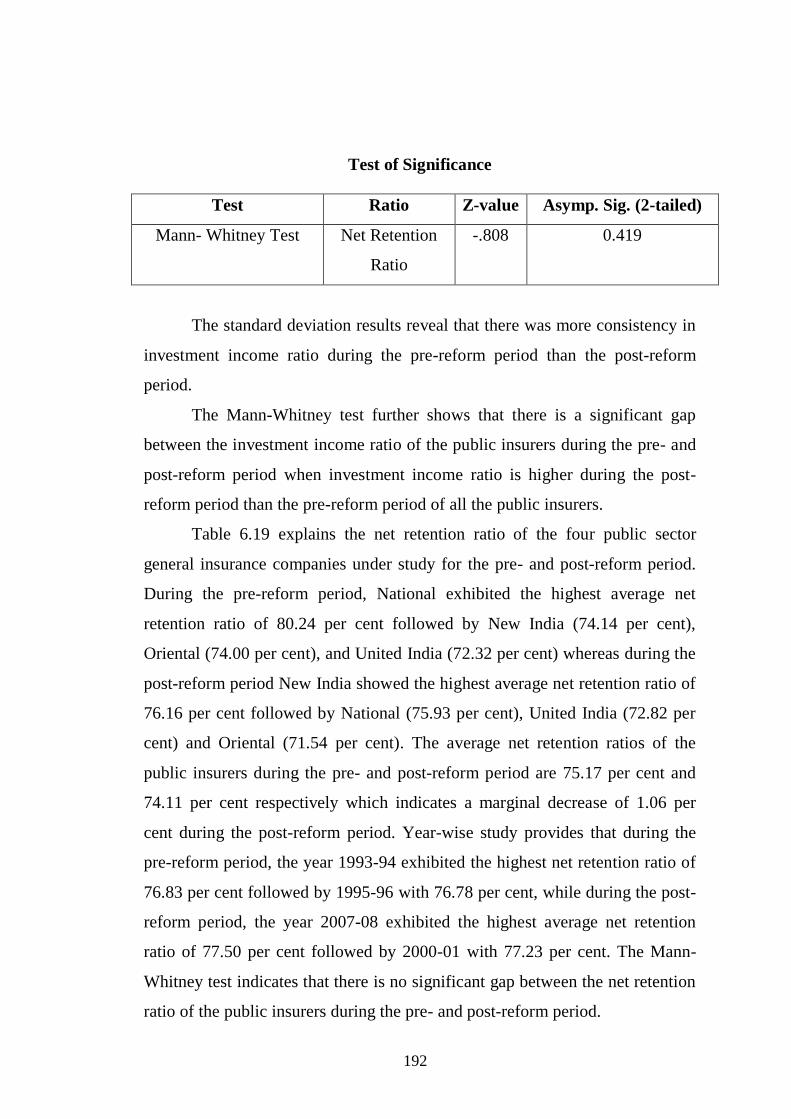

Net Retention Ratio

Net Retention ratio may be defined as net written premium divided by

gross-direct premium. It is a measure of the companies‟ ability to bear risks.

Direct insurance companies are required to cede a minimum of 15% (down

from 20% since April 2007) of their business to the national reinsurer, GIC.

(Moody's ICRA Global, 2008). In general, the companies having a stronger

capital base are able to retain more of their portfolios, whereas the companies,

with relatively lower capitalization (and hence lower capacity to retain risks)

have resorted to higher utilization of reinsurance.

Table 6.6

Net Retention Ratio of General Insurance Companies during the

Post-reform Period (Percentage)

Name of the

Company

20

02-0

3

20

03-0

4

20

04-0

5

20

05-0

6

20

06-0

7

20

07-0

8

Mea

n

Med

ian

S.D

.

National 74.25 73.78 74.32 75.87 74.61 79.26 75.35 74.47 2.04

New India 73.06 73.86 76.33 76.52 80.04 79.88 76.61 76.43 2.92

Oriental 66.21 70.11 71.77 69.27 71.62 73.81 70.46 70.87 2.60

United India 70.46 70.23 73.79 70.55 72.30 77.03 72.39 71.43 2.66

Mean 71.00 72.00 74.05 73.05 74.64 77.50 73.71 73.80 3.45

Median 71.76 72.00 74.05 73.21 73.45 78.14 73.80

S.D. 3.56 2.10 1.87 3.67 3.81 2.74 3.44

Royal

Sundaram 59.19 60.65 60.97 64.73 65.12 76.76 64.57 62.85 6.42

Reliance 10.38 21.45 38.32 34.21 55.28 68.71 38.06 36.27 21.41

IFFCO-

Tokio 32.83 41.38 47.27 53.58 50.73 65.39 48.53 49.00 11.08

TATA AIG 54.15 54.91 57.95 58.80 58.52 67.47 58.64 58.24 4.74

Bajaj Allianz 85.40 58.84 54.85 44.14 34.79 52.99 55.17 53.92 17.14

ICICI

Lombard 15.02 27.24 37.68 57.68 81.21 74.78 48.94 47.68 26.58

Cholamandal

am 30.43 49.79 52.86 44.76 51.09 61.48 48.40 50.44 10.36

HDFC

CHUBB 68.70 78.50 76.44 71.49 68.61 75.97 73.29 73.73 4.25

Mean 44.51 49.10 53.29 53.68 58.17 67.94 54.45 56.48 17.22

Median 43.49 52.35 53.85 55.63 56.90 68.09 56.48

S.D. 26.55 18.62 12.66 12.13 13.88 8.12 17.21

Source: IRDA Annual Reports from 2002-03 to 2007-08.

167

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-tailed)

Mann- Whitney Test Net Retention

Ratio

-5.05 0.00

Table 6.6 presents the trends of net retention ratio of all the public and

private sector general insurance companies from the years 2002-03 to 2007-08.

The average net retention ratio of the public insurers during the period of study

is 73.71 per cent, whereas it is 54.45 per cent in the case of private insurers. It

is evident that the average net retention ratio of the public insurers is 19.26 per

cent higher than that of the private insurers. Among the public insurers, New

India has exhibited the highest average net retention ratio of 76.61 per cent

followed by National with a percentage of 75.35 per cent, United India has

72.39 per cent and Oriental 70.46 per cent. Among the private insurers, HDFC

CHUBB has exhibited the highest average net retention ratio of 73.29 per cent

followed by Royal Sundaram with a percentage of 64.57 per cent, Tata AIG

58.64 per cent, Bajaj Allianz 55.17 per cent, ICICI Lombard 48.94 per cent,

IFFCO-Tokio 48.53 per cent, Cholamandalam 48.40 per cent and Reliance

38.06 per cent. The Year-wise trends indicate that, the public insurers have

reported on upward trend. Their average net retention ratio in the year 2002-03

was 71.00 per cent which increased to 77.50 per cent in the year 2007-08.

Similarly, the private insurers also reported an upward trend. Their average net

retention ratio in the year 2002-03 was 44.51 per cent which increased to 67.94

per cent in the year 2007-08. The standard deviation values of the net retention

ratio of both the public and private insurers are 3.45 per cent and 17.22 per cent

respectively, indicating higher consistency of the public insurers regarding net

retention. As is evident from the above analysis, the investment income offset

the effect of underwriting loss and contributing to the profitability of insurers.

The main reason for greater investment income of the public sector companies

is their high net retention which enables them to use more premiums in

investments. So, in order to increase their investment income and profitability,

the private sector companies need to enhance their net retention.

168

In general, the strong capital base of public sector companies has

enabled them to retain more of their portfolio, which the private insurers with a

weak capitalization (and hence lower capacity to retain risks) have resorted to

higher utilization of reinsurance resulting in lower net retention. The Mann-

Whitney test indicates that there is a significant gap between the net retention

ratio of public and private insurers.

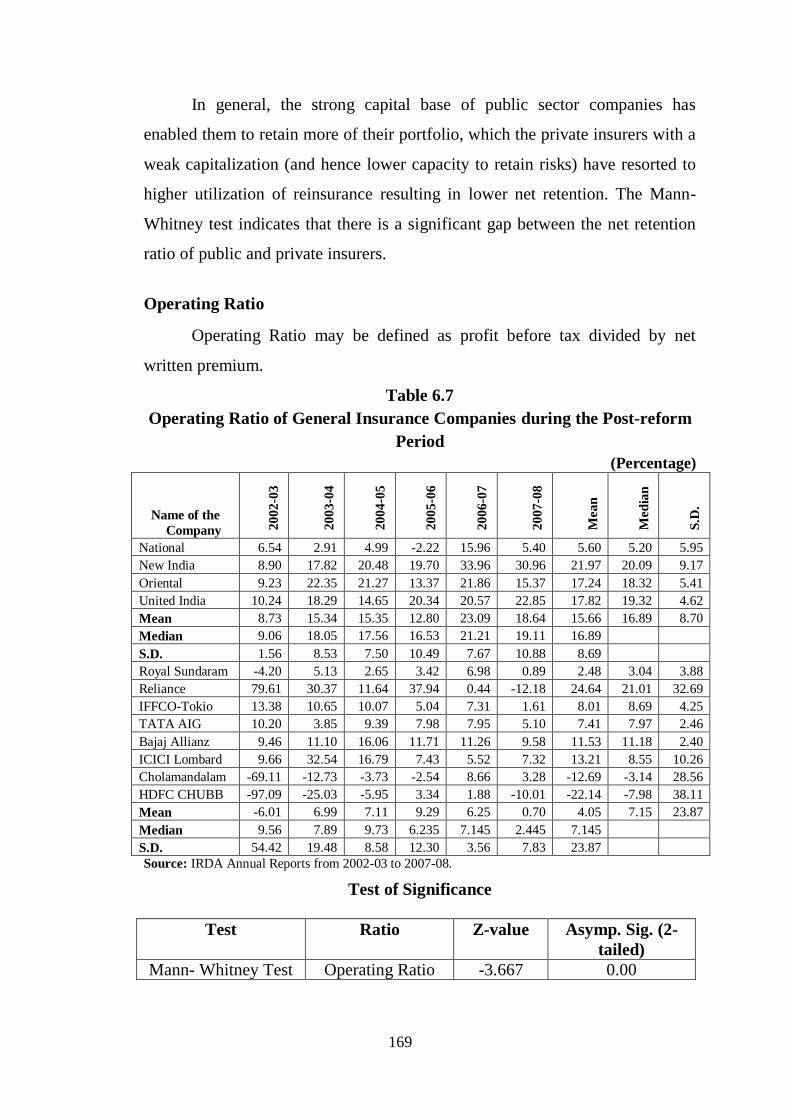

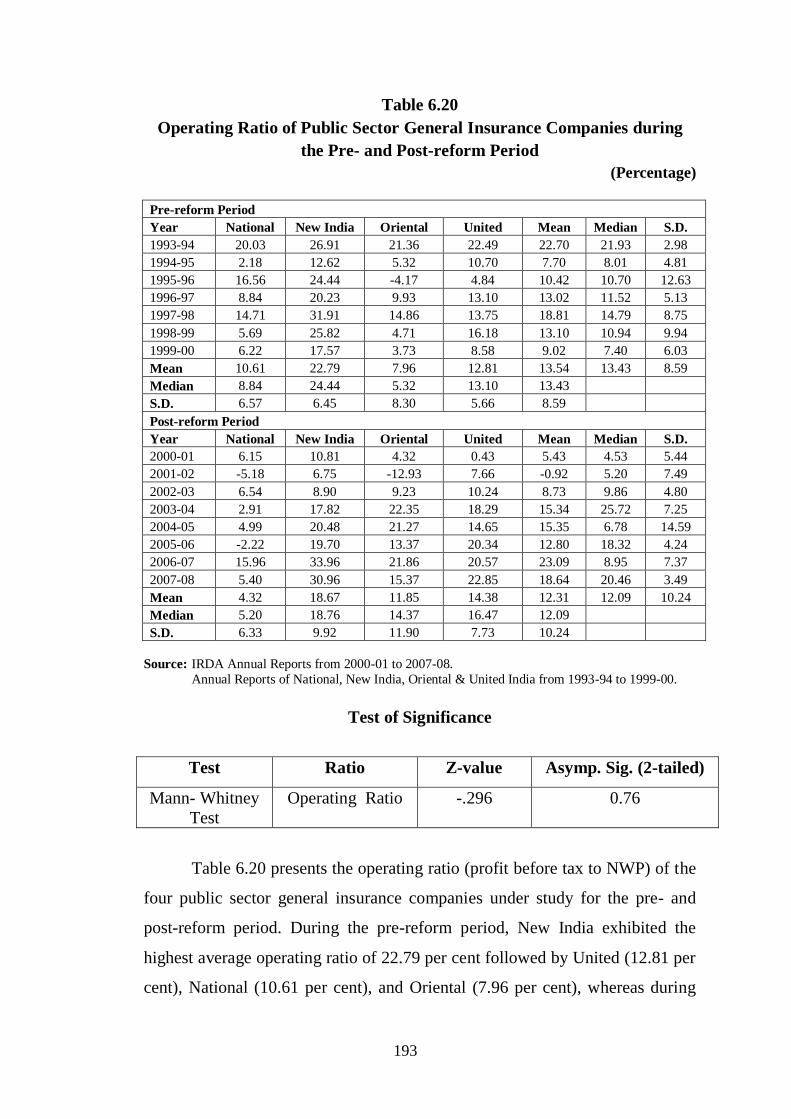

Operating Ratio

Operating Ratio may be defined as profit before tax divided by net

written premium.

Table 6.7

Operating Ratio of General Insurance Companies during the Post-reform

Period

(Percentage)

Name of the

Company 20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

Mea

n

Med

ian

S.D

.

National 6.54 2.91 4.99 -2.22 15.96 5.40 5.60 5.20 5.95

New India 8.90 17.82 20.48 19.70 33.96 30.96 21.97 20.09 9.17

Oriental 9.23 22.35 21.27 13.37 21.86 15.37 17.24 18.32 5.41

United India 10.24 18.29 14.65 20.34 20.57 22.85 17.82 19.32 4.62

Mean 8.73 15.34 15.35 12.80 23.09 18.64 15.66 16.89 8.70

Median 9.06 18.05 17.56 16.53 21.21 19.11 16.89

S.D. 1.56 8.53 7.50 10.49 7.67 10.88 8.69

Royal Sundaram -4.20 5.13 2.65 3.42 6.98 0.89 2.48 3.04 3.88

Reliance 79.61 30.37 11.64 37.94 0.44 -12.18 24.64 21.01 32.69

IFFCO-Tokio 13.38 10.65 10.07 5.04 7.31 1.61 8.01 8.69 4.25

TATA AIG 10.20 3.85 9.39 7.98 7.95 5.10 7.41 7.97 2.46

Bajaj Allianz 9.46 11.10 16.06 11.71 11.26 9.58 11.53 11.18 2.40

ICICI Lombard 9.66 32.54 16.79 7.43 5.52 7.32 13.21 8.55 10.26

Cholamandalam -69.11 -12.73 -3.73 -2.54 8.66 3.28 -12.69 -3.14 28.56

HDFC CHUBB -97.09 -25.03 -5.95 3.34 1.88 -10.01 -22.14 -7.98 38.11

Mean -6.01 6.99 7.11 9.29 6.25 0.70 4.05 7.15 23.87

Median 9.56 7.89 9.73 6.235 7.145 2.445 7.145

S.D. 54.42 19.48 8.58 12.30 3.56 7.83 23.87

Source: IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney Test Operating Ratio -3.667 0.00

169

Table 6.7 carried the data regarding operating ratio (profit before tax to

NWP) of both the public and private insurers for the period 2002-03 to 2007-

08. It is evident from the table that the average operating ratios of the public

and private sector general insurance companies for the period are 15.66 per

cent and 4.05 per cent respectively which indicates that the public sector

insurers average operating ratio is 11.61 per cent higher than that of the private

sector insurers. Among the public sector insurers, New India achieved the

highest average operating ratio of 21.97 per cent followed by United India,

Oriental and National with the respective percentages of 17.82 per cent, 17.24

per cent and 5.60 per cent. All the public insurers have earned operating profit

during all the years under study except National Insurance Company which

suffered operating loss of 2.22 per cent in the year 2005-06. Among the private

insurers, Reliance has exhibited the highest average operating ratio of 24.64 per

cent followed by ICICI Lombard, Bajaj Allianz, IFFCO-Tokio, Tata AIG and

Royal Sundaram with the respective percentages of 13.21 per cent, 11.53 per

cent, 8.01 per cent, 7.41 per cent and 2.48 per cent. The other private insurers

suffered average operating losses, whereas HDFC CHUBB showed the highest

negative average operating ratio of -22.14 per cent followed by

Cholamandalam with a percentage of -12.69 per cent. So, among the private

insurers, Reliance, ICICI Lombard and Bajaj Allianz have exhibited better

operating ratios as compared to other private insurers. Year-wise analysis

provides that the average operating ratio of the public insurers has shown an

upward trend during the period 2002-03 to 2004-05 when it increased from

8.73 per cent to 15.35 per cent, and again it came down to 12.80 per cent in the

year 2005-06, and further in 2007-08 it became 18.64 per cent. The private

insurers in the year 2002-03 showed a negative average operating ratio of -6.01

per cent. However, from the year 2003-04 onwards it registered a positive

operating ratio with no consistent trend, i.e., it showed an upward trend up to

2005-06 and again showed a downward trend from 2006-07 to 2007-08.

Overall, the public sector companies earned a higher average operating profit

as compared to their counter-parts. The Mann-Whitney test also indicates that

170

there is a significant gap between the operating ratios of the public and private

insurers.

Net Earning Ratio

The Net Earning Ratio shows how profitable the insurance business is.

This ratio reflects the summary of all activities during the period under review.

The Net Earning Ratio has been calculated by dividing profit after tax to net

written premium. Table 6.8 explains that the net earning ratios of the public

sector General Insurance Companies have improved during the period under

study.

Table 6.8

Net Earning Ratio of General Insurance Companies during the Post-

reform Period

(Percentage)

Name of the

Company

20

02

-03

20

03

-04

20

04

-05

20

05

-06

20

06

-07

20

07

-08

Mea

n

Med

ian

S.D

.

National 6.33 2.84 4.63 -3.96 14.75 5.13 4.95 4.88 6.03

New India 7.28 16.24 10.33 16.50 30.72 28.51 18.26 16.37 9.50

Oriental 3.34 15.56 14.90 11.35 17.27 0.32 10.46 13.13 7.02

United India 8.17 17.68 14.16 19.10 20.91 21.93 16.99 18.39 5.11

Mean 6.28 13.08 11.01 10.75 20.91 13.97 12.67 14.46 8.59

Median 6.80 15.90 12.24 13.92 19.08 13.52 14.45

S.D. 2.10 6.88 4.69 10.32 7.01 13.40 8.58

Royal

Sundaram -4.20 5.13 2.48 2.91 5.44 0.88 2.11 2.70 3.53

Reliance 100.31 26.06 9.41 25.86 0.32 -12.38 24.93 17.63 39.81

IFFCO-Tokio 9.08 7.18 6.27 3.06 4.67 0.97 5.21 5.47 2.93

TATA AIG -10.20 8.11 4.71 4.04 5.19 3.06 2.49 4.38 6.44

Bajaj Allianz 5.31 7.58 9.82 7.38 7.25 6.03 7.23 7.31 1.55

ICICI Lombard 7.66 24.48 15.06 6.86 4.71 5.78 10.76 7.26 7.66

Cholamandalam -69.11 -12.73 -3.73 -3.17 7.84 2.25 -13.11 -3.45 28.28

HDFC CHUBB -97.09 -25.03 -5.95 3.07 1.50 -10.14 -22.27 -8.05 38.01

Mean -7.28 5.10 4.76 6.25 4.62 -0.44 2.17 4.71 24.63

Median 0.55 7.38 5.49 3.55 4.94 1.61 4.71

S.D. 17.15 7.04 8.54 2.57 6.97 24.62

Source: IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney Test Net Earning Ratio -3.548 0.00

171

Table 6.8 highlights the trends of net earning ratio (profit after tax to

NWP) of the public and private sector general insurance companies for the

period 2002-03 to 2007-08. The average net earning ratios of both the public

and the private insurers for the period are 12.67 per cent and 2.17 per cent

respectively which exhibits that the net earning ratio of public insurers is higher

by 10.50 per cent than that of the private insurers. Among the public sector

insurers, New India has earned the highest average net earning ratio of 18.26

per cent followed by United India, Oriental and National with the respective

percentages of 16.99 per cent, 10.46 per cent, and 4.95 per cent. All the public

insurers have shown operating profit during all the years under study except

National Insurance Company which suffered a loss of -3.96 per cent in the year

2005-06. Among the private insurers, Reliance has earned the highest average

net earning ratio of 24.93 per cent followed by ICICI Lombard, Bajaj Allianz,

IFFCO-Tokio, Tata AIG and Royal Sundaram with the respective percentages

of 10.76, 7.23, 5.21, 2.49 and 2.11. Among the other private insurers, HDFC

CHUBB suffered the highest average loss of -22.27 per cent followed by

Cholamandalam with a loss of -13.11 per cent. Year-wise analysis provides

that the public insurers have registered the highest average net earning ratios of

20.91 per cent and 13.97 per cent during the last two years, i.e., 2006-07 and

2007-08 respectively. However, no clear trend in the case of the public insurers

could be observed. In the case of private insurers, the average net earning ratio

is the highest, i.e., 6.25 per cent during the year 2005-06 followed by the ratios

both of 5.10 per cent, and 4.62 per cent during the years 2003-04 and 2006-07

respectively. The standard deviation values of both the public and private

sector insurers also indicate that there is greater consistency in the net earning

ratio of public insurers as compared to private insurers. The results of Mann-

Whitney test also indicate that there is a significant gap between the net earning

ratio of the public and private insurers.

172

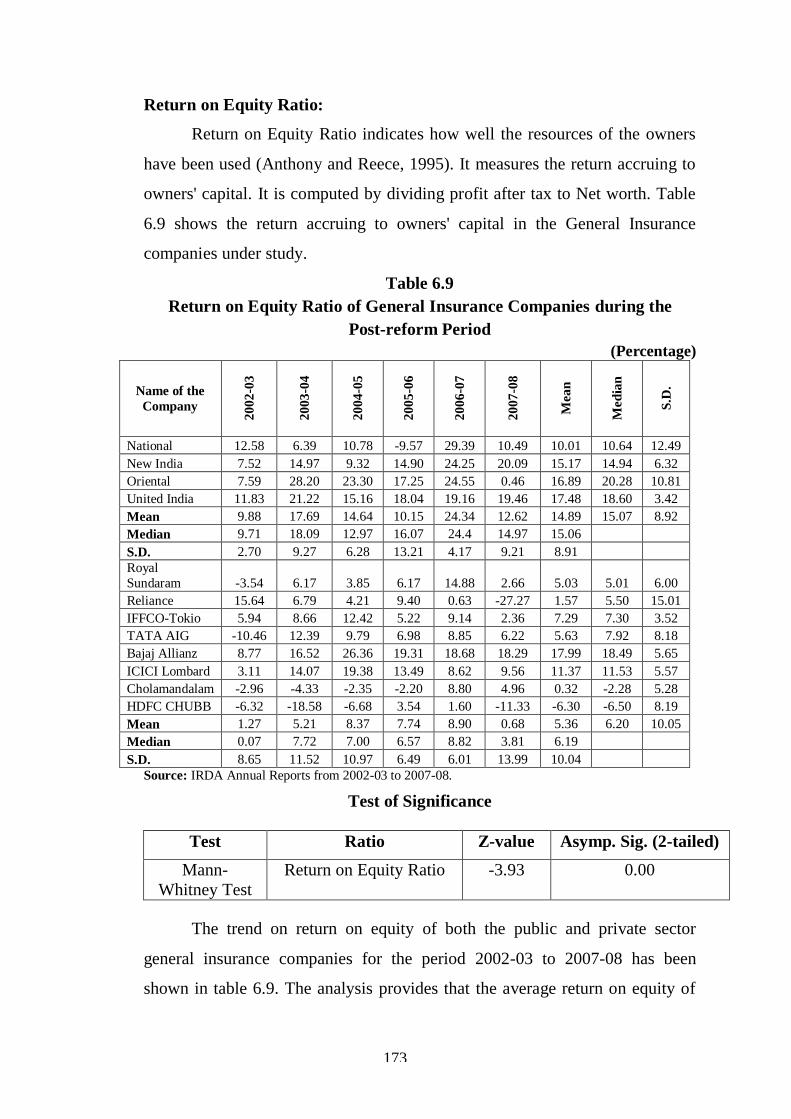

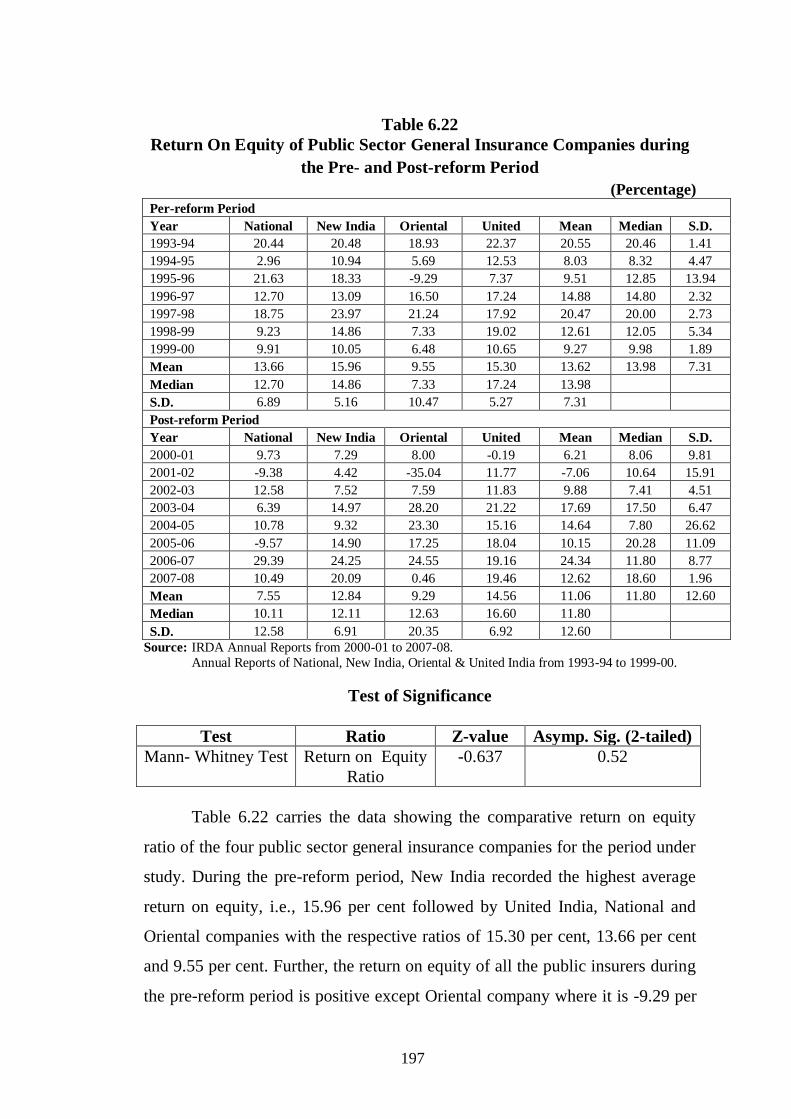

Return on Equity Ratio:

Return on Equity Ratio indicates how well the resources of the owners

have been used (Anthony and Reece, 1995). It measures the return accruing to

owners' capital. It is computed by dividing profit after tax to Net worth. Table

6.9 shows the return accruing to owners' capital in the General Insurance

companies under study.

Table 6.9

Return on Equity Ratio of General Insurance Companies during the

Post-reform Period

(Percentage)

Name of the

Company

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

20

07-0

8

Mean

Med

ian

S.D

.

National 12.58 6.39 10.78 -9.57 29.39 10.49 10.01 10.64 12.49

New India 7.52 14.97 9.32 14.90 24.25 20.09 15.17 14.94 6.32

Oriental 7.59 28.20 23.30 17.25 24.55 0.46 16.89 20.28 10.81

United India 11.83 21.22 15.16 18.04 19.16 19.46 17.48 18.60 3.42

Mean 9.88 17.69 14.64 10.15 24.34 12.62 14.89 15.07 8.92

Median 9.71 18.09 12.97 16.07 24.4 14.97 15.06

S.D. 2.70 9.27 6.28 13.21 4.17 9.21 8.91

Royal

Sundaram -3.54 6.17 3.85 6.17 14.88 2.66 5.03 5.01 6.00

Reliance 15.64 6.79 4.21 9.40 0.63 -27.27 1.57 5.50 15.01

IFFCO-Tokio 5.94 8.66 12.42 5.22 9.14 2.36 7.29 7.30 3.52

TATA AIG -10.46 12.39 9.79 6.98 8.85 6.22 5.63 7.92 8.18

Bajaj Allianz 8.77 16.52 26.36 19.31 18.68 18.29 17.99 18.49 5.65

ICICI Lombard 3.11 14.07 19.38 13.49 8.62 9.56 11.37 11.53 5.57

Cholamandalam -2.96 -4.33 -2.35 -2.20 8.80 4.96 0.32 -2.28 5.28

HDFC CHUBB -6.32 -18.58 -6.68 3.54 1.60 -11.33 -6.30 -6.50 8.19

Mean 1.27 5.21 8.37 7.74 8.90 0.68 5.36 6.20 10.05

Median 0.07 7.72 7.00 6.57 8.82 3.81 6.19

S.D. 8.65 11.52 10.97 6.49 6.01 13.99 10.04

Source: IRDA Annual Reports from 2002-03 to 2007-08.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-tailed)

Mann-

Whitney Test

Return on Equity Ratio -3.93 0.00

The trend on return on equity of both the public and private sector

general insurance companies for the period 2002-03 to 2007-08 has been

shown in table 6.9. The analysis provides that the average return on equity of

173

the public sector insurers is 14.89 per cent, and that of private sector insurers is

5.36 per cent which means the public sector insurers earn 9.53 per cent higher

average return on equity than the private insurers. Among the public sector

insurers, United India has earned the highest average return on equity of 17.48

per cent followed by Oriental, New India and National with the respective

percentage of 16.89, 15.17 and 10.01 per cent. All the public sector insurers

have shown a positive return on equity during all the years except National

Insurance Company which showed a negative return on equity in the year

2005-06 of -9.57 per cent. Among the private sector insurers, Bajaj Allianz

achieved the highest average return on equity of 17.99 per cent followed by

ICICI Lombard (11.37 per cent), IFFCO-Tokio (7.29 per cent), Tata AIG (5.63

per cent), Royal Sundaram (5.03 per cent), and Reliance (1.57 per cent). HDFC

CHUBB suffered a loss and showed a negative average return on equity of -

6.30 per cent. Year-wise analysis provides that public sector insurers' average

return on equity was the highest in the year 2006-07 which is 24.34 per cent

followed by the percentages of 17.69 per cent, 14.64 per cent and 12.62 per

cent which appeared during the years 2003-04, 2004-05 and 2007-08

respectively. In the case of the private insurers, the average return on equity is

the highest, i.e., 8.90 per cent in the year 2006-07 followed by 8.37 per cent,

7.74 per cent, 5.21 per cent which appeared during the years 2004-05, 2005-

06, and 2003-04 respectively. The Mann-Whitney test also indicates that there

is a significant gap between the return on equity of the public and private

insurers. The return on equity of the public insurers is significantly higher than

that of the private insurers. Therefore, the study rejected the hypothesis that the

profitability of the private insurers is significantly higher than that of the public

insurers.

On the basis of above analysis, it can be concluded that the private

sector General Insurance companies have shown better efficiency in terms of

claim incurred and combined ratio which resulted into lower underwriting

losses. A closer investigation of the product portfolio, through their annual

reports, reveals that it is mainly ascribed to the fact that the private companies

174

are concentrating more on the creamy business. In respect of loss making

portfolio, such as motor business, they have avoided to enter this business to

reduce their claim incurred ratio. Further investigation reveals that public

sector insurance companies do not get much of their business reinsured in

contrast to the private sector players, who get most of the business reinsured to

reduce their claim incurred ratio. But the higher investment return of the public

sector offsets their underwriting losses and resulted into their better operating,

net earning and returns on equity ratios. The main reason for higher investment

income of the public sector companies is their higher net retention which

enables these companies to use more premium in investment. So, in order to

increase the investment income and profitability, the private sector companies

need to increase their net retention. In general, the strong capital base of public

sector companies has enabled them to retain more of their portfolio, and private

insurers with lower capitalization (and hence lower capacity to retain risks)

have resorted to higher utilization of reinsurance resulted in lower net retention.

It has been found that the underwriting results and investment results are

negatively correlated. Good investment returns allow the public sector insurers

to post losses on underwriting without risking overall losses. But the prospects

for a rapid improvement in investment return are not certain. Equity markets

are currently weak, volatile and uncertain. So, due to uncertain prospects of

investment returns, the public sector general insurance companies must focus

on underwriting results to achieve greater profitability. On the other hand, the

private sector must bring more capital to improve net retention, increase risk

bearing capacity which resulted into their increase in business and investment

return.

6.4 Multivariate Profitability Analysis of the General Insurance

Companies in the Post-reform Period

Correlation analysis involves measuring the magnitude and direction of

the relationship between two or more variables. Interdependence among

variables is a common characteristic of most multivariate techniques and

correlation matrix is a table used to display correlation coefficients between

175

these variables. Matrices form the basis for computation and understanding of

the nature of relationships in multiple regressions, discriminant analysis, factor

analysis, and many other similar techniques. One sample t-test is used as a

parametric tool for testing the significance of correlation coefficient. The study

aimed at identifying the most important independent variable (s) which have

higher significant association with the dependent variable.

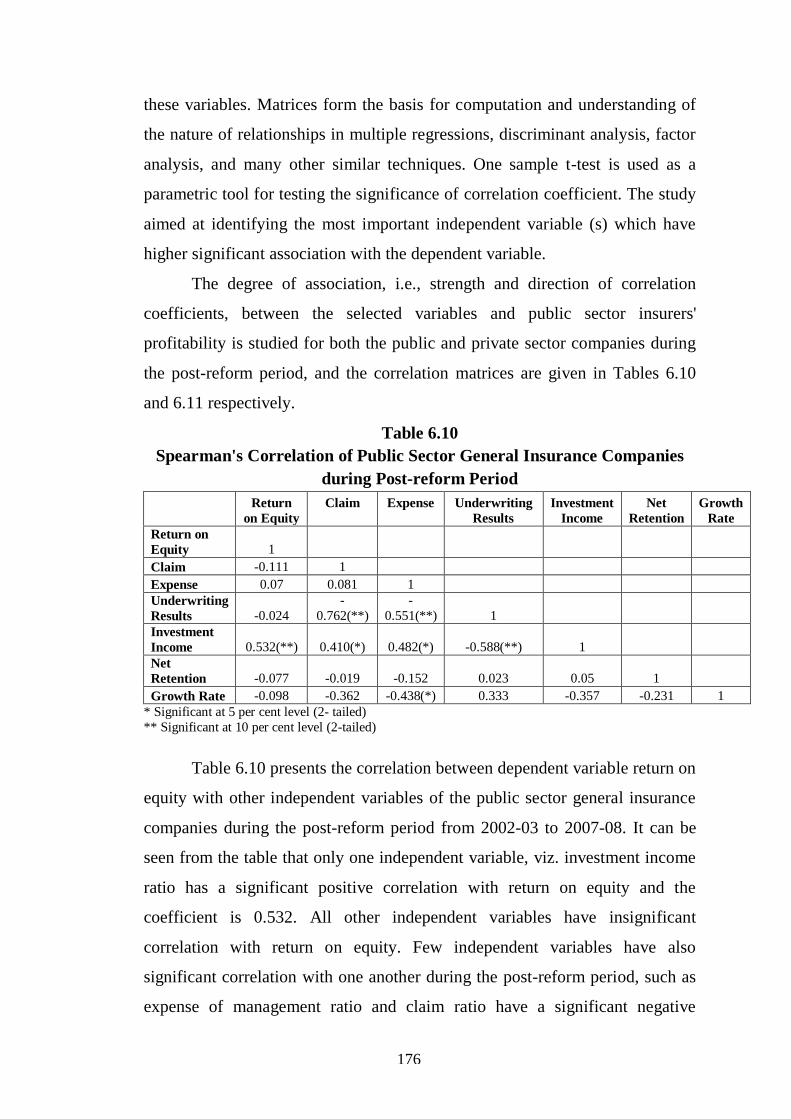

The degree of association, i.e., strength and direction of correlation

coefficients, between the selected variables and public sector insurers'

profitability is studied for both the public and private sector companies during

the post-reform period, and the correlation matrices are given in Tables 6.10

and 6.11 respectively.

Table 6.10

Spearman's Correlation of Public Sector General Insurance Companies

during Post-reform Period

Return

on Equity

Claim

Expense

Underwriting

Results

Investment

Income

Net

Retention

Growth

Rate

Return on

Equity 1

Claim -0.111 1

Expense 0.07 0.081 1

Underwriting

Results -0.024

-

0.762(**)

-

0.551(**) 1

Investment

Income 0.532(**) 0.410(*) 0.482(*) -0.588(**) 1

Net

Retention -0.077 -0.019 -0.152 0.023 0.05 1

Growth Rate -0.098 -0.362 -0.438(*) 0.333 -0.357 -0.231 1

* Significant at 5 per cent level (2- tailed)

** Significant at 10 per cent level (2-tailed)

Table 6.10 presents the correlation between dependent variable return on

equity with other independent variables of the public sector general insurance

companies during the post-reform period from 2002-03 to 2007-08. It can be

seen from the table that only one independent variable, viz. investment income

ratio has a significant positive correlation with return on equity and the

coefficient is 0.532. All other independent variables have insignificant

correlation with return on equity. Few independent variables have also

significant correlation with one another during the post-reform period, such as

expense of management ratio and claim ratio have a significant negative

176

correlation with underwriting results and their coefficients are -0.551 and -

0.762 respectively. Underwriting results have significant negative correlation

with investment income ratio due to this higher underwriting loss is offset by

higher investment income ratio of the public sector general insurance

companies resulted into higher profitability.

Table 6.11

Spearman's Correlations of Private Sector General Insurance Companies

during the Post-reform Period

Return

on

Equity Claim Expense

Underwriting

Results

Investment

Income

Net

Retention

Growt

h Rate

Return on

Equity 1

Claim 0.051 1

Expense

-

0.585(**) -0.294(*) 1

Underwriting

Results 0.793(**) -0.017 -0.497(**) 1

Investment

Income -0.101 -0.001 0.082 -0.408(**) 1

Net

Retention -0.352(*) 0.078 0.385(**) -0.168 -0.417(**) 1

Growth Rate -0.051

-

0.450(**) -0.157 -0.124 0.075 -0.134 1

* Significant at 5 per cent level (2- tailed)

** Significant at 10 per cent level (2-tailed)

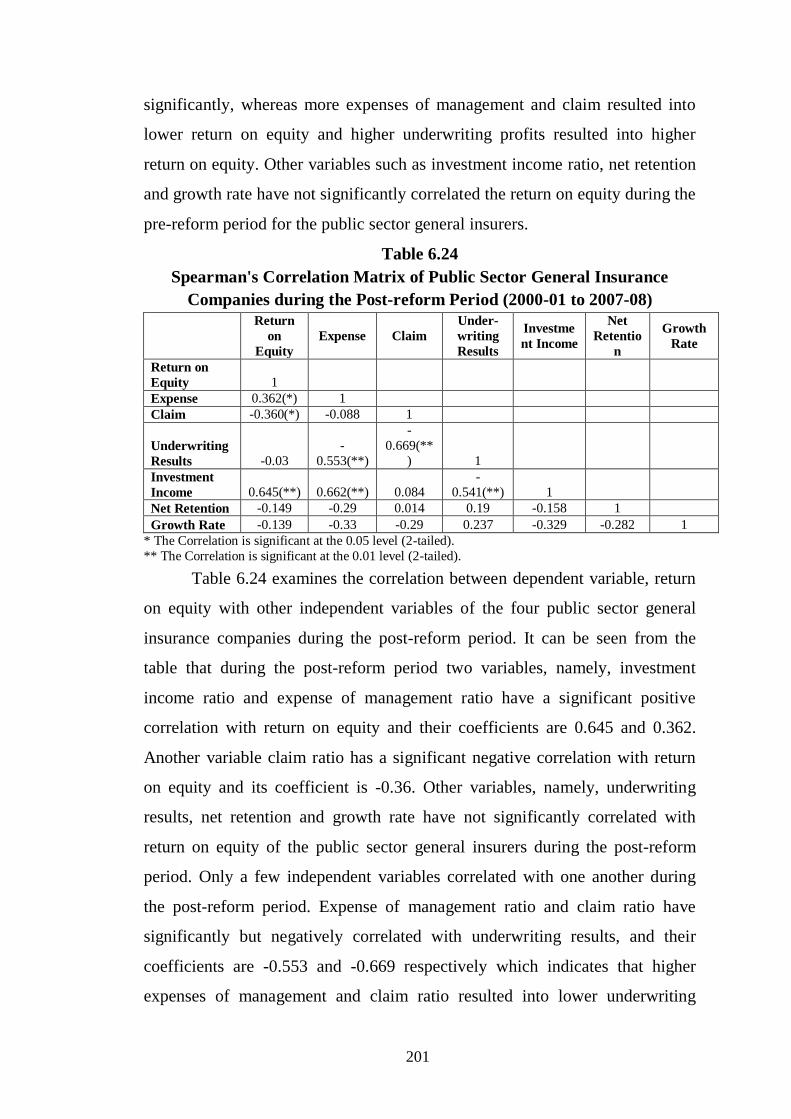

Table 6.11 highlights the correlation between the dependent variable,

viz. return on equity with other independent variables of the eight private sector

general insurance companies during the post-reform period from 2002-03 to

2007-08. It can be seen from the table that two independent variables, namely,

expense of management ratio and net retention ratio have significant negative

correlation with return on equity and the coefficients are -0.585 and -0.352

respectively. Underwriting results have significant positive correlation with

return on equity and the coefficient is 0.793. Other independent variables,

namely, claim ratio, investment income ratio & growth rate have not significant

correlation with return on equity. Few independent variables have also

significant correlation with one another, such as claim ratio has significant

negative correlation with expense of management ratio and the coefficient is -

0.294. Expense of management has a significant negative correlation with

177

underwriting results; and underwriting results has a significant negative

correlation with investment income ratio and the coefficient is -0.408.

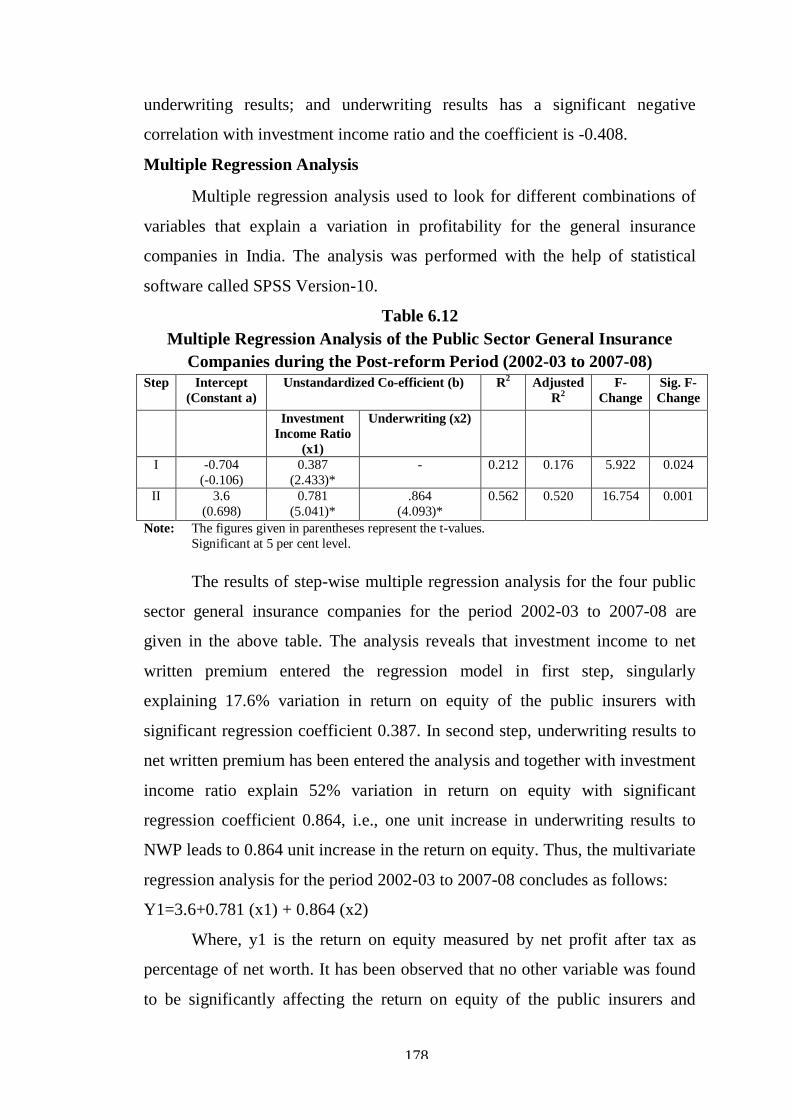

Multiple Regression Analysis

Multiple regression analysis used to look for different combinations of

variables that explain a variation in profitability for the general insurance

companies in India. The analysis was performed with the help of statistical

software called SPSS Version-10.

Table 6.12

Multiple Regression Analysis of the Public Sector General Insurance

Companies during the Post-reform Period (2002-03 to 2007-08)

Step Intercept

(Constant a)

Unstandardized Co-efficient (b) R2 Adjusted

R2

F-

Change

Sig. F-

Change

Investment

Income Ratio

(x1)

Underwriting (x2)

I -0.704

(-0.106)

0.387

(2.433)*

- 0.212 0.176 5.922 0.024

II 3.6

(0.698)

0.781

(5.041)*

.864

(4.093)*

0.562 0.520 16.754 0.001

Note: The figures given in parentheses represent the t-values.

Significant at 5 per cent level.

The results of step-wise multiple regression analysis for the four public

sector general insurance companies for the period 2002-03 to 2007-08 are

given in the above table. The analysis reveals that investment income to net

written premium entered the regression model in first step, singularly

explaining 17.6% variation in return on equity of the public insurers with

significant regression coefficient 0.387. In second step, underwriting results to

net written premium has been entered the analysis and together with investment

income ratio explain 52% variation in return on equity with significant

regression coefficient 0.864, i.e., one unit increase in underwriting results to

NWP leads to 0.864 unit increase in the return on equity. Thus, the multivariate

regression analysis for the period 2002-03 to 2007-08 concludes as follows:

Y1=3.6+0.781 (x1) + 0.864 (x2)

Where, y1 is the return on equity measured by net profit after tax as

percentage of net worth. It has been observed that no other variable was found

to be significantly affecting the return on equity of the public insurers and

178

investment income to NWP and underwriting results to NWP have been found

significantly affecting profitability of the public sector general insurance

companies during the period 2002-03 to 2007-08.

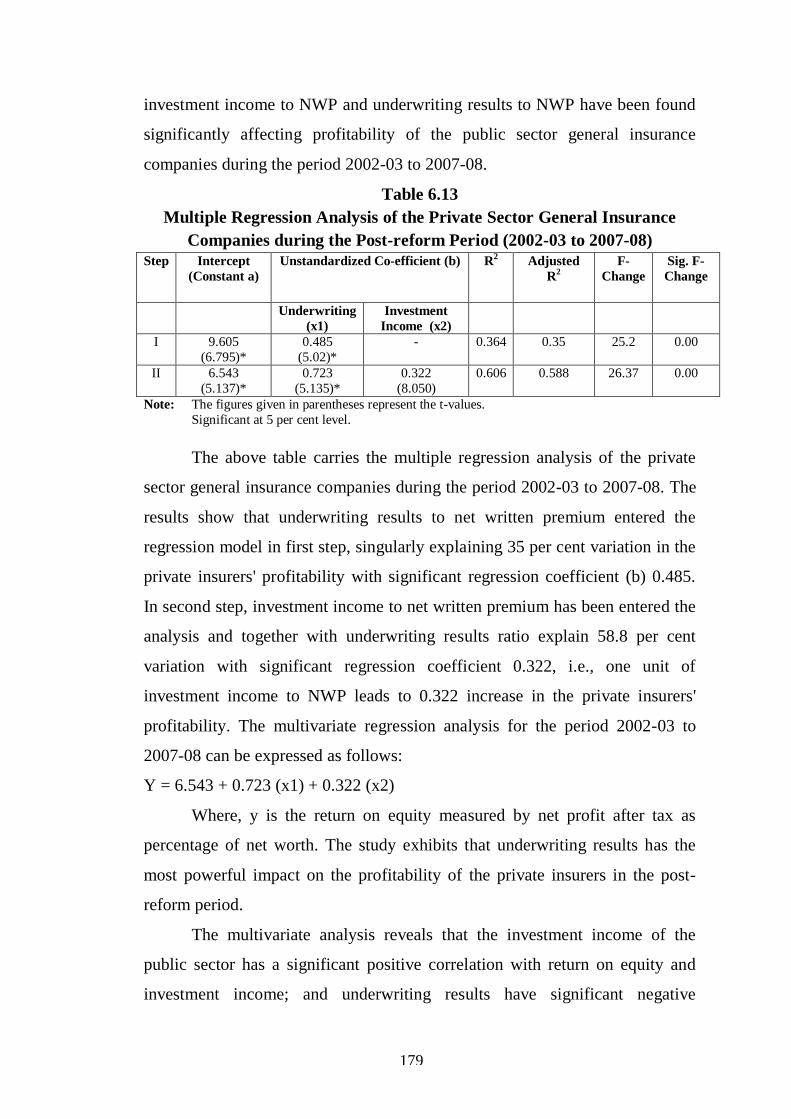

Table 6.13

Multiple Regression Analysis of the Private Sector General Insurance

Companies during the Post-reform Period (2002-03 to 2007-08)

Step Intercept

(Constant a)

Unstandardized Co-efficient (b) R2 Adjusted

R2

F-

Change

Sig. F-

Change

Underwriting

(x1)

Investment

Income (x2)

I 9.605

(6.795)*

0.485

(5.02)*

- 0.364 0.35 25.2 0.00

II 6.543

(5.137)*

0.723

(5.135)*

0.322

(8.050)

0.606 0.588 26.37 0.00

Note: The figures given in parentheses represent the t-values.

Significant at 5 per cent level.

The above table carries the multiple regression analysis of the private

sector general insurance companies during the period 2002-03 to 2007-08. The

results show that underwriting results to net written premium entered the

regression model in first step, singularly explaining 35 per cent variation in the

private insurers' profitability with significant regression coefficient (b) 0.485.

In second step, investment income to net written premium has been entered the

analysis and together with underwriting results ratio explain 58.8 per cent

variation with significant regression coefficient 0.322, i.e., one unit of

investment income to NWP leads to 0.322 increase in the private insurers'

profitability. The multivariate regression analysis for the period 2002-03 to

2007-08 can be expressed as follows:

Y = 6.543 + 0.723 (x1) + 0.322 (x2)

Where, y is the return on equity measured by net profit after tax as

percentage of net worth. The study exhibits that underwriting results has the

most powerful impact on the profitability of the private insurers in the post-

reform period.

The multivariate analysis reveals that the investment income of the

public sector has a significant positive correlation with return on equity and

investment income; and underwriting results have significant negative

179

correlation with each other. The regression results indicated that both

investment income and underwriting results have significant impact on the

profitability of public sector general insurance companies. The negative

correlation between underwriting results and investment income indicated the

trend that higher investment income resulted into lower underwriting profits

and vice-versa. The correlation analysis of the private sector indicated that

return on equity has a significant correlation with expenses of management and

net retention, and positive relation with underwriting results. The regression

analysis reported that both underwriting results and investment income have

significant impact on return on equity. As is evident from the analysis that the

significant variation in return on equity is due to both underwriting results and

investment income of both the public and private insurers. But all the insurers

have exhibited underwriting losses. So, in order to enhance their profitability,

these companies need to focus on their underwriting results.

6.5. Comparative Profitability Analysis of the Public Sector General

Insurance Companies in the Pre- and Post-reform Period

Market liberalization of insurance services involves removing

restrictions on foreign and domestic investment and allowing firms the freedom

to set rates. In the process of liberalization, the government generally sets

minimum capital requirements for insurers; introduces solvency margins; and

allows firms to engage in brokerage and perhaps reinsurance activities. The

liberalization of market may be partial, i.e., less than 100 per cent equity

ownership permitted or completely open, i.e.,100 per cent foreign equity

ownership allowed to foreign competition, although the WTO is pushing all

member countries towards complete openness over the long-term (WTO,

2004). Liberalization of insurance sector in India was initiated following the

report of R.N Malhotra Committee, which was set up in 1993 with an objective

of complementing the reforms in the Indian financial sector. The reforms are

aimed at creating more efficient and competitive financial system suitable for

the requirement of the economy. The year 1999 saw a revolution in the Indian

180

insurance sector, as major structural changes took place with the ending of

Government monopoly and the passage of the Insurance Regulatory and

Development Authority (IRDA) bill, lifting entry restrictions for private

players and allowing foreign players to enter the market with some limits on

direct foreign ownership. The insurance market has witnessed dynamic changes

due to liberalization and privatization of insurance sector, which has resulted in

increasing number of insurers. At present, in general insurance, there are six

public sector and fifteen private sector insurance companies.

The reforms in general insurance industry in India have far reaching

consequences in terms of market size, structure and operational practices. The

effect of reforms on the firm‟s performance has received bulk attention in the

national and international business research and has suggested that

liberalization has a positive long-term effect on economic growth and firm's

performance (Dollar, 1992; Sachs and Warner, 1997). The reforms brought an

overall increase in the awareness of the insuring public about the wider range

of choice of insurance products and the price offered by the competing insurers

in the market. The market share of public insurance companies has been

challenged in recent years by a variety of forces from internet disintermediation

to aggressive marketing by new entrants, financial services deregulation,

compliance pressure, competition from other investment vehicles and of course

customer empowerment (Capgemine and EFMA, 2007).

Since the onset of reforms, the public sector general insurance

companies have been compelled to review their philosophy and method of

working, in order to be ready for competition with the private sector

companies. The urgent response that is required from the existing public

insurers is clear that they must remain competitive by doing things better and

faster, and by ensuring cost effectiveness to improve profitability. Large

number of initiatives have been taken by these public sector companies to

compete with private sector companies to exist in the market. But still public

sector companies need to reassess their present status of profitability after

having modified their approach and philosophy. Now the time has come for

181

taking stock of the situation, how liberalization has affected the profitability of

public sector general insurance companies since profit is the main reason for

the continued existence of every commercial organisation. Sustainable

profitability is important for the safety and soundness of the industry and public

sector general insurance companies are no exception to this.

The study seeks to assess the comparative profitability of the public

sector general insurance companies in India in the pre-liberalization period and

the post-liberalization period with respect to the below mentioned drivers of

profitability.

Expense Ratio

The ratio of Expenses of Management as percentage of gross direct

premium reflects how much percentage of revenue is being utilised for

expenses on management. This ratio is a pointer of the cost effectiveness and

the productivity. Expenses of Management are generally operating expenses

which include employees‟ remuneration and benefits, office and administrative

expenses, etc. and a higher ratio reflects financial instability of the business

because a decrease in revenue may result in losses, whereas lower ratio is an

indicator of better operational performance. It becomes important to examine,

how far the public sector general insurance companies have been in a position

to reduce their operating cost during the post-liberalization period.

Table 6.14

Expense Ratio of Public Sector General Insurance Companies during Pre-

and Post-reform Period

(Percentage)

Pre-reform period

Year National New

India Oriental United Mean Median S.D.

1993-94 23.36 20.45 21.33 18.18 20.83 20.89 2.14

1994-95 25.62 18.70 22.19 18.69 21.30 20.44 3.31

1995-96 27.61 22.15 32.95 25.65 27.09 26.63 4.51

1996-97 31.10 29.31 27.12 25.91 28.36 28.21 2.30

1997-98 24.56 22.52 24.07 24.91 24.02 24.31 1.05

1998-99 28.75 22.42 24.58 23.36 24.78 23.97 2.79

1999-00 29.23 24.34 30.28 24.54 27.10 26.88 3.09

Mean 27.17 22.84 26.07 23.03 24.78 24.55 3.78

Median 27.61 22.42 24.58 24.54 24.55

S.D. 2.77 3.35 4.27 3.25 3.78

182

Post-reform Period

Year National New

India Oriental United Mean Median S.D.

2000-01 27.21 28.07 26.53 24.75 26.64 30.49 2.04

2001-02 30.59 27.95 32.22 31.56 30.58 33.83 2.60

2002-03 30.39 30.83 33.70 28.82 30.94 29.45 7.17

2003-04 32.08 43.05 41.70 38.77 38.90 35.62 4.70

2004-05 33.11 39.70 37.25 41.92 38.00 32.96 6.25

2005-06 38.13 38.76 38.16 46.75 40.45 35.21 3.92

2006-07 32.20 32.48 29.65 38.04 33.09 30.19 5.90

2007-08 34.55 30.08 33.17 36.42 33.56 39.98 4.59

Mean 32.28 33.87 34.05 35.88 34.02 32.79 5.34

Median 32.14 31.65 33.43 37.23 32.79

S.D. 3.21 5.81 4.86 7.17 5.34

Source: IRDA Annual Reports from 2000-01 to 2007-08.

Annual reports of National, New India, Oriental & United India from 1993-94 to 1999-00.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney Test Expense Ratio -5.73 0.00

Table 6.14 presents the comparative expense of management ratio of the

four public sector general insurance companies during the pre- and post-reform

period. The study shows that during the pre-reform period, the average expense

of management ratio of National, New India, Oriental and United India was

27.17 per cent, 22.84 per cent, 26.07 per cent and 23.03 per cent respectively.

Similarly, during the post-reform period, the average expense ratio of National,

New India, Oriental and United India was 32.28 per cent, 33.87 per cent, 34.05

per cent and 35.88 per cent respectively. The results indicate that the expenses

of management of all the public insurers have increased during the post-reform

period as compared to the pre-reform period. However, the increase in expense

is not the same for all the four public insurers. The highest average increase of

expense of management ratio during the post-reform period as compared to the

pre-reform period of United India was 12.85 per cent followed by New India

(11.03 per cent), Oriental (7.98 per cent), and National (5.11 per cent). During

the pre-reform period, among the public sector insurers, National Insurance

Company registered the highest average expense ratio, whereas during the

post-reform period, it registered the lowest average expense ratio. Overall, the

183

average expense ratio of all the public insurers during the pre- and post-reform

period is 24.78 per cent and 34.02 per cent respectively which shows an

increase of 9.24 per cent in average expense ratio during the post-reform

period. A glance at the year-wise results during the post-reform period provides

that the average expense ratio showed an increasing trend during the period

2000-01 to 2005-06 when it increased from 26.64 per cent to 40.45 per cent.

Later on, it decreased to 33.56 per cent in the year 2007-08. The results of

Mann-Whitney test also exhibit a significant increase in expense of

management ratio during the post-reform period which is higher than the pre-

reform period. The increase of expense ratio in the post-reform period is

mainly due to higher spending of the public insurers on advertisements,

commission and other expenses to compete with the private insurers.

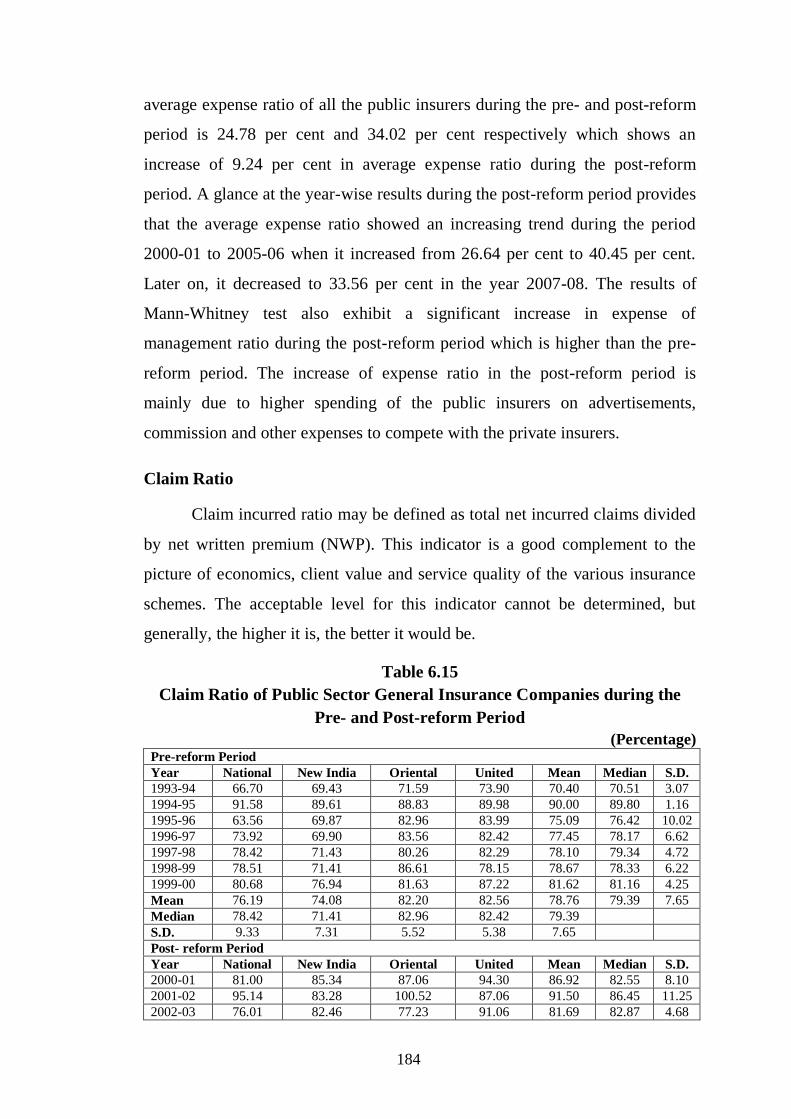

Claim Ratio

Claim incurred ratio may be defined as total net incurred claims divided

by net written premium (NWP). This indicator is a good complement to the

picture of economics, client value and service quality of the various insurance

schemes. The acceptable level for this indicator cannot be determined, but

generally, the higher it is, the better it would be.

Table 6.15

Claim Ratio of Public Sector General Insurance Companies during the

Pre- and Post-reform Period

(Percentage) Pre-reform Period

Year National New India Oriental United Mean Median S.D.

1993-94 66.70 69.43 71.59 73.90 70.40 70.51 3.07

1994-95 91.58 89.61 88.83 89.98 90.00 89.80 1.16

1995-96 63.56 69.87 82.96 83.99 75.09 76.42 10.02

1996-97 73.92 69.90 83.56 82.42 77.45 78.17 6.62

1997-98 78.42 71.43 80.26 82.29 78.10 79.34 4.72

1998-99 78.51 71.41 86.61 78.15 78.67 78.33 6.22

1999-00 80.68 76.94 81.63 87.22 81.62 81.16 4.25

Mean 76.19 74.08 82.20 82.56 78.76 79.39 7.65

Median 78.42 71.41 82.96 82.42 79.39

S.D. 9.33 7.31 5.52 5.38 7.65

Post- reform Period

Year National New India Oriental United Mean Median S.D.

2000-01 81.00 85.34 87.06 94.30 86.92 82.55 8.10

2001-02 95.14 83.28 100.52 87.06 91.50 86.45 11.25

2002-03 76.01 82.46 77.23 91.06 81.69 82.87 4.68

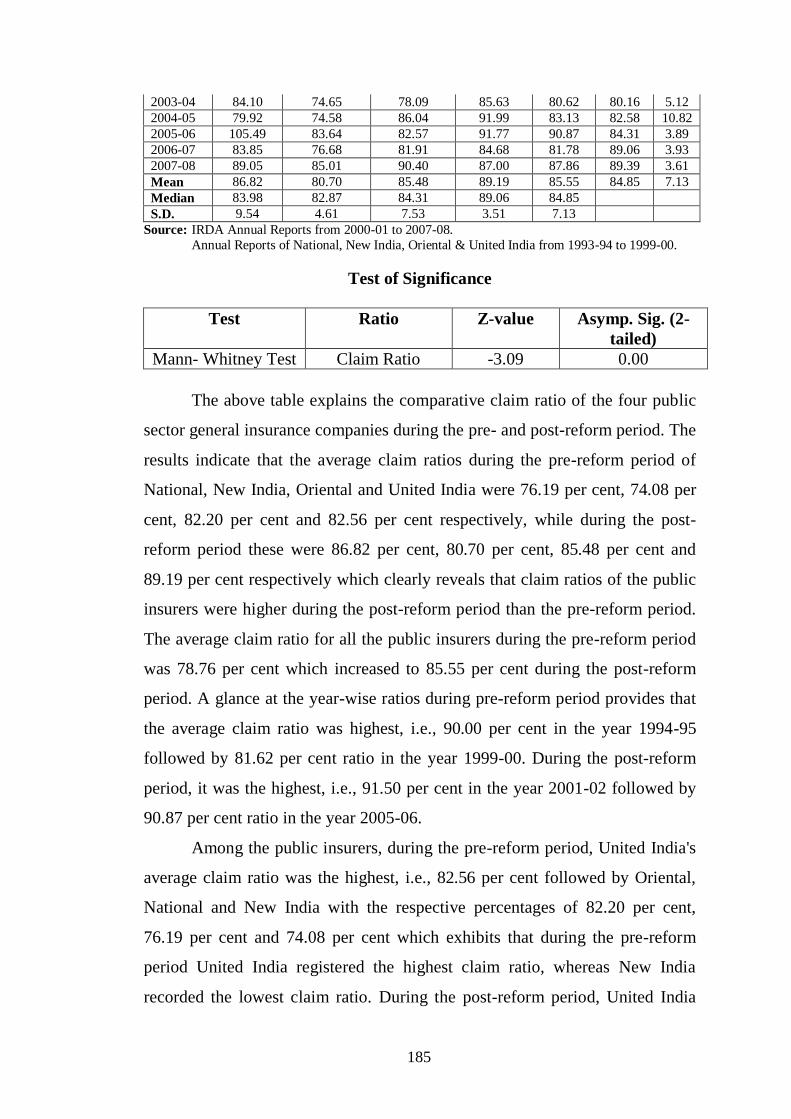

184

2003-04 84.10 74.65 78.09 85.63 80.62 80.16 5.12

2004-05 79.92 74.58 86.04 91.99 83.13 82.58 10.82

2005-06 105.49 83.64 82.57 91.77 90.87 84.31 3.89

2006-07 83.85 76.68 81.91 84.68 81.78 89.06 3.93

2007-08 89.05 85.01 90.40 87.00 87.86 89.39 3.61

Mean 86.82 80.70 85.48 89.19 85.55 84.85 7.13

Median 83.98 82.87 84.31 89.06 84.85

S.D. 9.54 4.61 7.53 3.51 7.13

Source: IRDA Annual Reports from 2000-01 to 2007-08.

Annual Reports of National, New India, Oriental & United India from 1993-94 to 1999-00.

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-

tailed)

Mann- Whitney Test Claim Ratio -3.09 0.00

The above table explains the comparative claim ratio of the four public

sector general insurance companies during the pre- and post-reform period. The

results indicate that the average claim ratios during the pre-reform period of

National, New India, Oriental and United India were 76.19 per cent, 74.08 per

cent, 82.20 per cent and 82.56 per cent respectively, while during the post-

reform period these were 86.82 per cent, 80.70 per cent, 85.48 per cent and

89.19 per cent respectively which clearly reveals that claim ratios of the public

insurers were higher during the post-reform period than the pre-reform period.

The average claim ratio for all the public insurers during the pre-reform period

was 78.76 per cent which increased to 85.55 per cent during the post-reform

period. A glance at the year-wise ratios during pre-reform period provides that

the average claim ratio was highest, i.e., 90.00 per cent in the year 1994-95

followed by 81.62 per cent ratio in the year 1999-00. During the post-reform

period, it was the highest, i.e., 91.50 per cent in the year 2001-02 followed by

90.87 per cent ratio in the year 2005-06.

Among the public insurers, during the pre-reform period, United India's

average claim ratio was the highest, i.e., 82.56 per cent followed by Oriental,

National and New India with the respective percentages of 82.20 per cent,

76.19 per cent and 74.08 per cent which exhibits that during the pre-reform

period United India registered the highest claim ratio, whereas New India

recorded the lowest claim ratio. During the post-reform period, United India

185

showed the highest claim ratio of 89.19 per cent followed by National with

86.82 per cent. The Mann-Whitney test indicates that claim ratio of the public

insurers is significantly higher during the post-reform period than the pre-

reform period.

Combined Ratio

This ratio reflects the combined effect of expenses of management and

claim incurred. It is the most common measure of underwriting profitability.

Financial analysts rely on it for comparing the profitability of insurance

business of different companies and for comparing different lines of business.

Companies use it for steering their business (Holzheu, 2006).

Table 6.16

Combined Ratio of Public Sector General Insurance Companies during

Pre- and Post-reform Period

(Percentage)

Pre-reform Period

Year National New India Oriental United Mean Median S.D.

1993-94 90.06 89.88 92.91 92.08 91.23 91.07 1.50

1994-95 117.19 108.31 111.01 108.67 111.30 109.84 4.11

1995-96 91.16 92.02 115.91 109.64 102.18 100.83 12.50

1996-97 105.02 99.21 110.68 108.33 105.81 106.68 4.97

1997-98 102.98 93.95 104.33 107.21 102.12 103.66 5.72

1998-99 107.26 93.83 111.19 101.51 103.45 104.39 7.54

1999-00 109.91 101.28 111.91 111.75 108.71 110.83 5.04

Mean 103.37 96.93 108.28 105.60 103.54 106.12 8.47

Median 105.02 93.95 111.01 108.33 106.12

S.D. 9.82 6.40 7.58 6.75 8.47

Post-reform Period

Year National New India Oriental United Mean Median S.D.

2000-01 108.20 113.41 113.59 119.05 113.56 112.19 8.82

2001-02 125.72 111.23 132.74 118.62 122.08 119.83 13.77

2002-03 106.40 113.28 110.93 119.89 112.62 113.35 2.72

2003-04 116.18 117.71 119.79 124.40 119.52 114.69 5.45

2004-05 113.03 114.28 123.29 133.91 121.13 116.69 9.72

2005-06 143.63 122.39 120.73 138.53 131.32 122.01 5.63

2006-07 116.05 109.16 111.56 122.72 114.87 119.47 2.66

2007-08 123.60 115.09 123.57 123.42 121.42 128.67 7.83

Mean 119.10 114.57 119.53 125.07 119.57 118.84 8.63

Median 116.12 113.85 120.26 123.07 118.84

S.D. 11.96 4.05 7.36 7.30 8.63

Source: IRDA Annual Reports from 2000-01 to 2007-08.

Annual Reports of National, New India, Oriental & United India from 1993-94 to 1999-00.

186

Test of Significance

Test Ratio Z-value Asymp. Sig. (2-tailed)

Mann- Whitney Test Combined Ratio -5.70 0.00

Table 6.16 presents the comparative combined ratio of the four public

sector general insurance companies during the pre- and the post-reform period.

The table reflects that the combined ratio of Oriental is the highest, i.e., 108.28

per cent during the pre-reform period followed by United India, National and

New India with the respective ratios of 105.60 per cent, 103.37 per cent and

96.93 per cent. During the post-reform period the average combined ratio of

United India is the highest, i.e., 125.07 per cent followed by Oriental (119.53

per cent), National (119.10 per cent), and New India (114.57 per cent). It is

evident from the table that the combined ratio of all the public insurers is

higher during the post-reform period than the pre-reform period. The average

combined ratio of all the public insurers during the pre- and post-reform period

is 103.54 per cent and 119.57 per cent respectively which clearly indicates that

there is an increase of 16.03 per cent in this ratio during the post-reform period.

A glance at the year-wise ratios during the pre-reform period provides that the

average combined ratio was the lowest, i.e., 91.23 per cent in the year 1993-94

and the highest, i.e., 111.30 per cent in the year 1994-95. During the post-

reform period, the combined ratio was the highest, i.e., 131.32 per cent in the

year 2005-06, and the lowest, i.e., 122.08 in the year 2001-02. The Mann-

Whitney test also shows that the increase in the combined ratio of the public

insurers was significantly higher during the post-reform period than the pre-

reform period.

Underwriting Results Ratio

The underwriting results ratio of a general insurance company is

depicted by taking net written premium minus increase in the unexpired risk

reserve minus expense of management minus claim incurred minus

187

commission. The underwriting results indicate the performance of an insurance

company from core insurance business. The underwriting results ratio is

calculated by dividing underwriting results to net written premium.

Table 6.17

Underwriting Results Ratio of Public Sector General Insurance

Companies during the Pre- and Post-reform Period

(Percentage)

Pre-reform Period

Year National New India Oriental United Mean Median S.D.

1993-94 0.71 3.08 1.59 1.80 1.79 1.70 0.98

1994-95 -20.14 -13.31 -15.91 -11.84 -15.30 -14.61 3.64

1995-96 -3.53 -1.70 -26.55 -19.57 -12.84 -11.55 12.17

1996-97 -11.94 -4.37 -14.79 -12.90 -11.00 -12.42 4.58

1997-98 -7.35 2.94 -9.12 -12.29 -6.45 -8.24 6.59

1998-99 -14.52 0.60 -18.07 -7.92 -9.98 -11.22 8.21

1999-00 -14.36 -7.18 -1.83 -15.78 -9.79 -10.77 6.50

Mean -10.16 -2.85 -12.10 -11.21 -9.08 -10.48 8.03

Median -11.94 -1.70 -14.79 -12.29 -10.48

S.D. 7.18 5.95 9.73 6.77 8.03

Post-reform Period

Year National New India Oriental United Mean Median S.D.

2000-01 -13.74 -16.97 -16.00 -22.35 -17.26 -17.57 5.69

2001-02 -25.51 -18.05 -32.62 -22.15 -24.58 -24.03 10.27