Languages

Pages

Legal

CHAPTER 7Cashand Receivables……..…………………………………………………………...

Cash

readily available

free from contractual restrictions

restricted cash: current or long-term

Would a bank accept it for deposit?

Petty cash accountCas

hSep

arat

e Disc

losur

e

Other

Ass

ets

Liabil

ities

Bank overdraft

Advances to subsidiaries

Certificates of deposit

Minimum cash balanceCas

hSep

arat

e Disc

losur

e

Other

Ass

ets

Liabil

ities

Money market funds

RECEIVABLES

Current Receivables

trade receivables

accounts receivable

notes receivable

nontrade receivables

tax refunds, advances, etc.

Noncurrent Receivables

classified as long-term assets

Reported atnet

realizable value

Estimate:- uncollectible- sales returns

Trade Discounts

a reduction in catalog price

usually stated as a percentage

record the sale at the discounted amount

no one pays full price!

Sales Discounts

a discount for prompt payment

Gross Method vs. Net Method

(cf. Illustration 7-4)

2/10, n/30

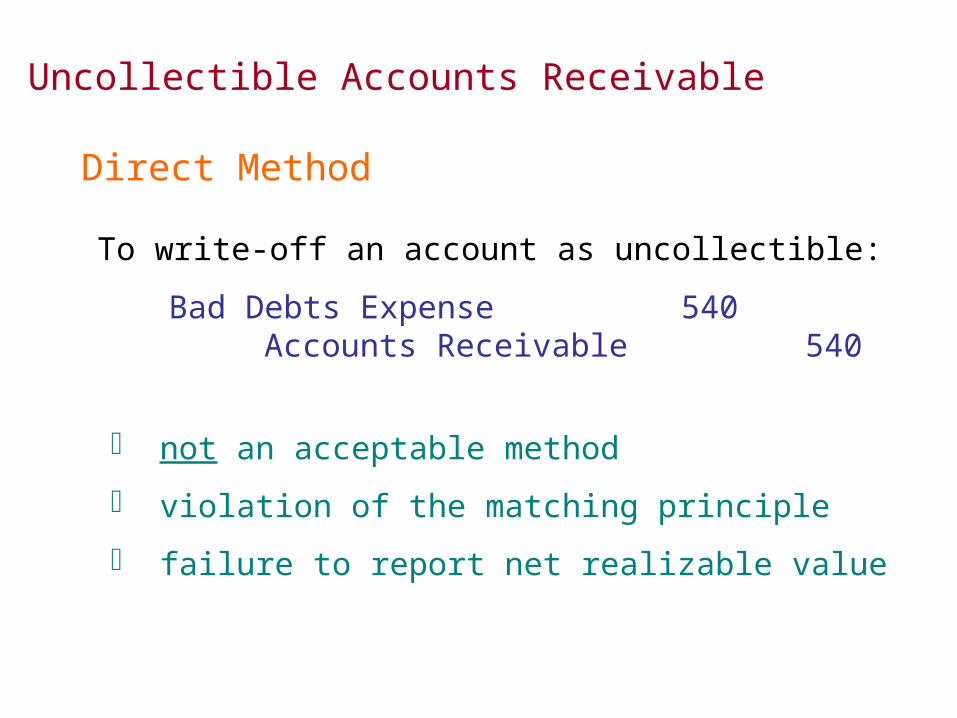

Uncollectible Accounts Receivable

not an acceptable method

violation of the matching principle

failure to report net realizable value

Direct Method

To write-off an account as uncollectible:

Bad Debts Expense 540Accounts Receivable 540

Allowance Method

To write-off accounts as uncollectible:

Sales

090,000

A/R

7,70090,000 87,000

Allow for DA

500

Bad Debt Exp

0

To record bad debts expense for the year:

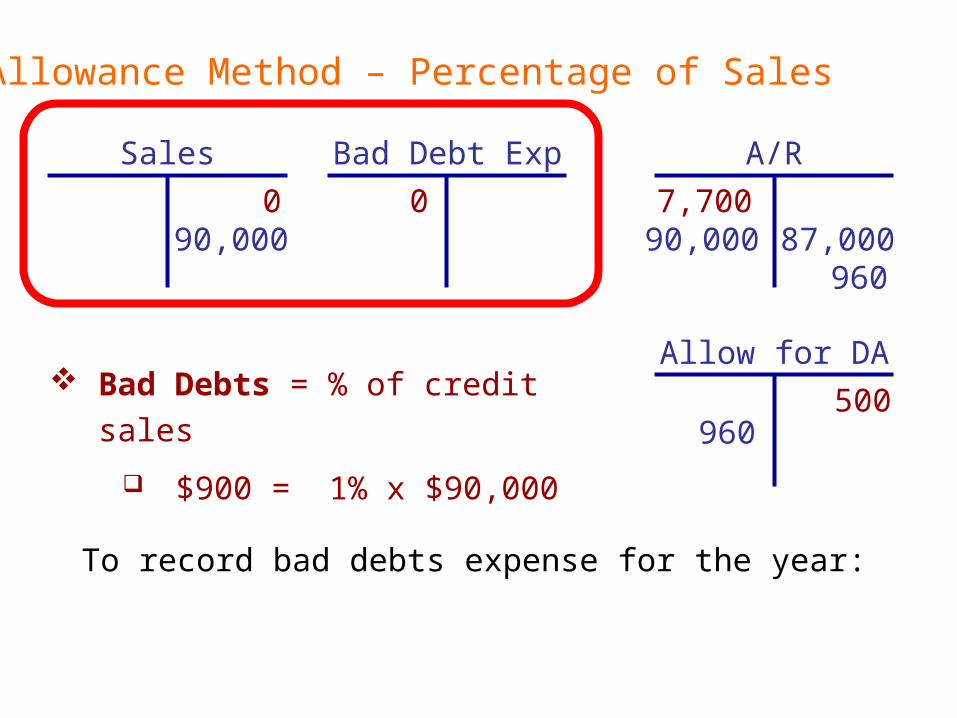

Allowance Method – Percentage of Sales

Sales

090,000

A/R

7,70090,000 87,000

960

Bad Debt Exp

0

To record bad debts expense for the year:

Allow for DA

500960

Bad Debts = % of credit sales

$900 = 1% x $90,000

Allowance Method – Percentage of Receivables

Sales

090,000

A/R

7,70090,000 87,000

960

Bad Debt Exp

0

To record bad debts expense for the year:

Allow for DA

500960

Allowance for DA = % of A/R

9,740

$487 = 5% x $9,740

NOTES RECEIVABLE

Notes Issued at Face Value

Bigelow Corp sells merchandise to customer for a

3-year, $5,000 note bearing interest at 10%

annually. Market rate for a similar note is 10%.

Periods Rate PV Annuity FV AD?

To record receipt of the note:

To record the interest received:

Noninterest-bearing Notes

Bigelow Corp sells merchandise to customer for a

3-year, $5,000 noninterest-bearing note. Market

rate for a similar note is 10%.

Periods Rate PV Annuity FV AD?

To record receipt of the note:

To record the interest earned:

DateCash

ReceivedInt Rev.(10%)

DiscountAmortize

d

CarryingAmount

7/1/03 3,757

7/1/04

7/1/05

Interest-bearing Notes

Bigelow Corp sells merchandise to customer for a

3-year, $5,000, 6% note. Interest on the note will

be paid semiannually. The market rate for a similar

note is 10%.

Periods Rate PV Annuity FV AD?

To record receipt of the note:

To record the first interest payment received:

DateCash

ReceivedInt Rev.

(5% semi)

DiscountAmortize

d

CarryingAmount

7/1/03 4,492

1/1/04

7/1/04

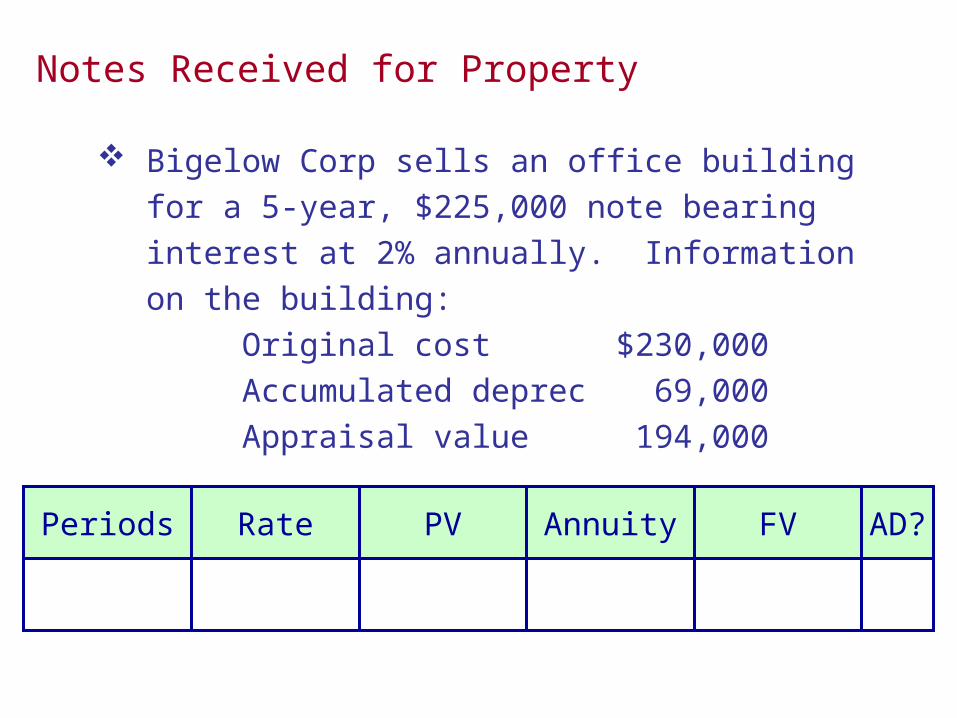

Notes Received for Property

Bigelow Corp sells an office building for a 5-year,

$225,000 note bearing interest at 2% annually.

Information on the building:

Original cost $230,000

Accumulated deprec 69,000

Appraisal value 194,000

Periods Rate PV Annuity FV AD?

To record sale of building:

Cost 230,000Accum depr69,000

PV 194,000FV 225,000

DISPOSITION OF ACCOUNTS RECEIVABLE

Secured Borrowing

A/R are used as collateral when borrowing money

Notes or loans payable are recorded as usual

A/R remain on the books of the company

no special entry when they become collateral

collection of A/R recorded as usual

collections are remitted to the lender

Sale of Receivables

Factoring: sale of receivables to a bank

Securitization: sales of a share in a pool of assets

that include receivables

Sale without Recourse

Cash 460,000Due from Factor 25,000Loss on Sale of Receiv 15,000

A/R 500,000

Sale with Recourse

Cash 460,000Due from Factor 25,000Loss on Sale of Receiv 21,000

A/R 500,000Recourse Liability 6,000

Proceeds retained by the factor for possible

discounts, returns, and allowances.

The estimated value of the recourse

obligation.

PRESENTATION AND ANALYSIS - RECEIVABLES

Presentation

Separate current from noncurrent

Report net realizable value

Disclose receivables pledged as collateral

Analysis

A/RTurnover

Net Sales

Average Net Trade Receivables=

PETTY CASH SYSTEM

Receipt

Petty Cash 500Cash 500

Fund EstablishedExpenses Paid

No entry

Office Exp 130Auto Exp 215Misc Exp 130

Cash 475

ReceiptReceiptReceiptReceiptReceipt

Fund Reimbursed

BANK RECONCILIATIONS

Balance per bank $13,417.20Add: Deposits in Transit

Oct. 31, 2006 2,013.00Less: Checks Outstanding

#5164 $ 220.00#5170 35.50#5171 756.67 1,012.17

Adjusted balance per bank $14,418.03

Balance per books $14,425.53Less: Bank service charge 7.50

Adjusted balance per books $14,418.03

Top Related