![[AIESEC HCMC][iGIP] Intern Guidebook](https://static.fdocuments.in/doc/165x107/541da31f7bef0a5e528b684b/aiesec-hcmcigip-intern-guidebook.jpg)

Languages

Pages

Legal

CBRE VIETNAM, HCMC MARKET OVERVIEW Q1/2014

PRESENTED BY: GREG OHAN, DIRECTOR, VIETNAM

MARCH 11TH 2014

CONTENTS

2

1. Understand The Market Overview - Vietnam Office Market

2. How to “Beat The Cycle?” Tenant Profiling Planning & Strategies - Key Considerations

3. Outlook & Predictions – 2014+ Outlook CBRE Predictions

4. MB Sunny Tower Overview - MB Sunny Tower

HOW TO MAKE THE RIGHT DECISION ?

3

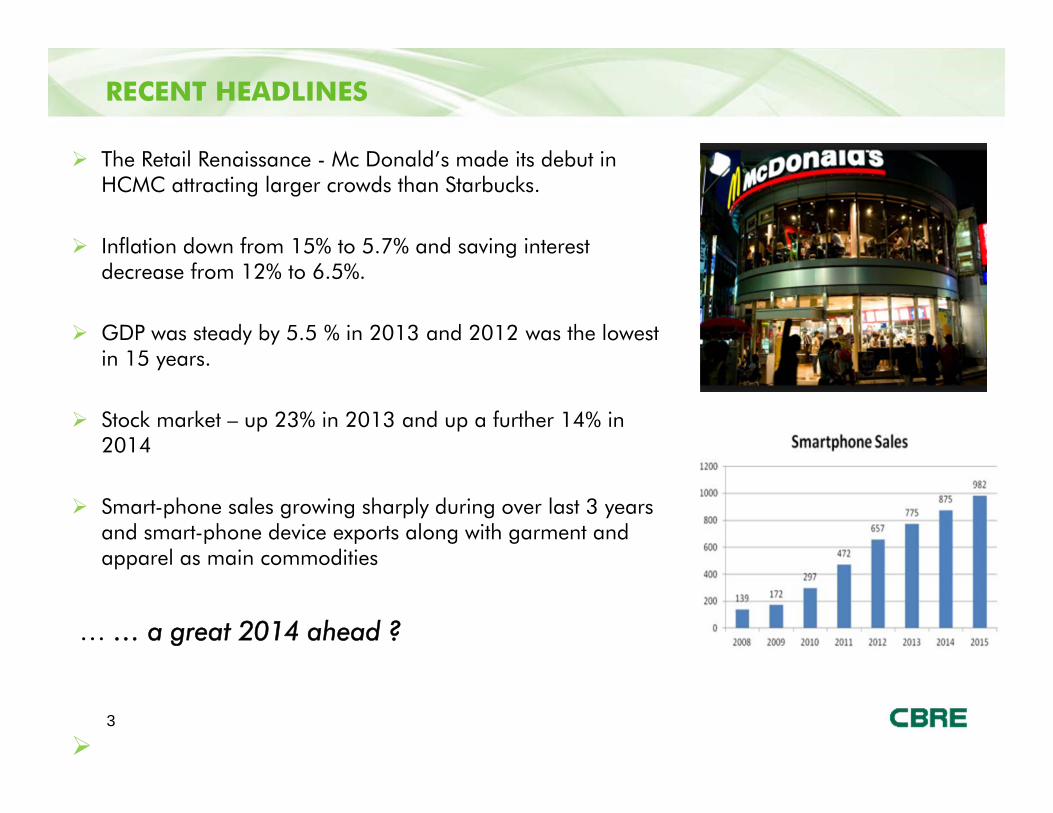

The Retail Renaissance - Mc Donald’s made its debut in HCMC attracting larger crowds than Starbucks.

Inflation down from 15% to 5.7% and saving interest decrease from 12% to 6.5%.

GDP was steady by 5.5 % in 2013 and 2012 was the lowest in 15 years.

Stock market – up 23% in 2013 and up a further 14% in 2014

Smart-phone sales growing sharply during over last 3 years and smart-phone device exports along with garment and apparel as main commodities

… … a great 2014 ahead ?

RECENT HEADLINES

UNDERSTAND THE MARKET

5

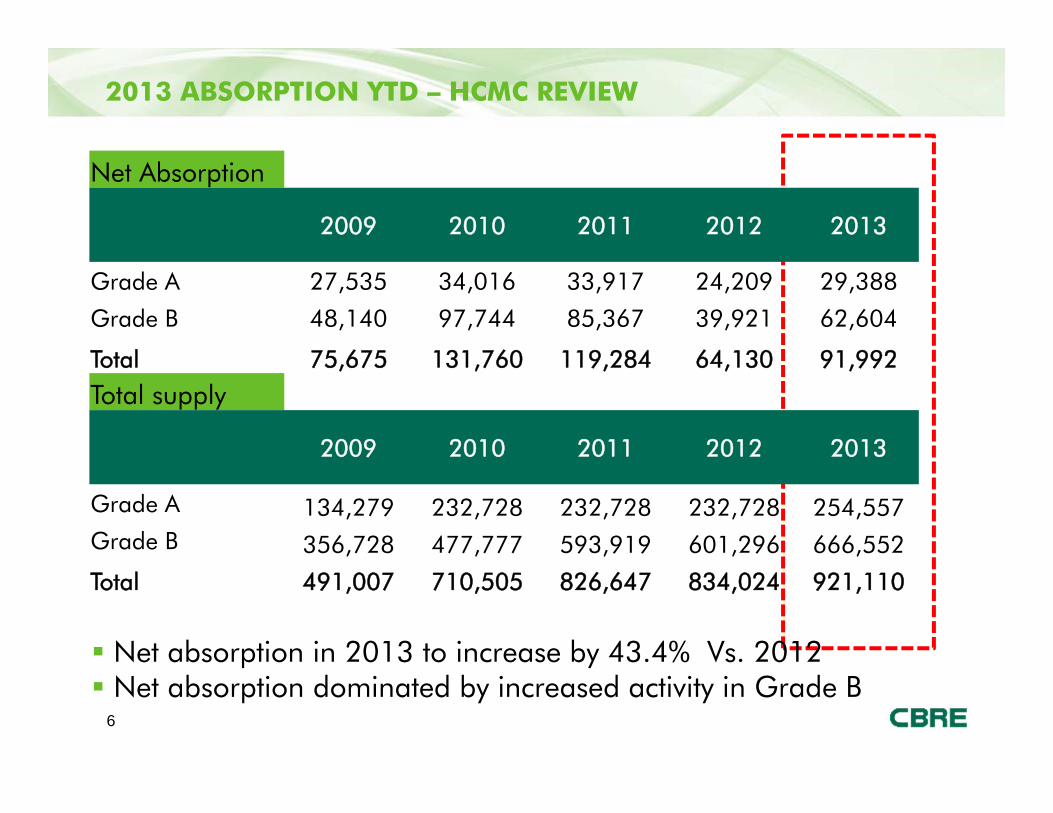

2013 ABSORPTION YTD – HCMC REVIEW

6

Net Absorption

2009 2010 2011 2012 2013

Grade A 27,535 34,016 33,917 24,209 29,388

Grade B 48,140 97,744 85,367 39,921 62,604

Total 75,675 131,760 119,284 64,130 91,992

Total supply

2009 2010 2011 2012 2013

Grade A 134,279 232,728 232,728 232,728 254,557Grade B 356,728 477,777 593,919 601,296 666,552

Total 491,007 710,505 826,647 834,024 921,110

Net absorption in 2013 to increase by 43.4% Vs. 2012 Net absorption dominated by increased activity in Grade B

7

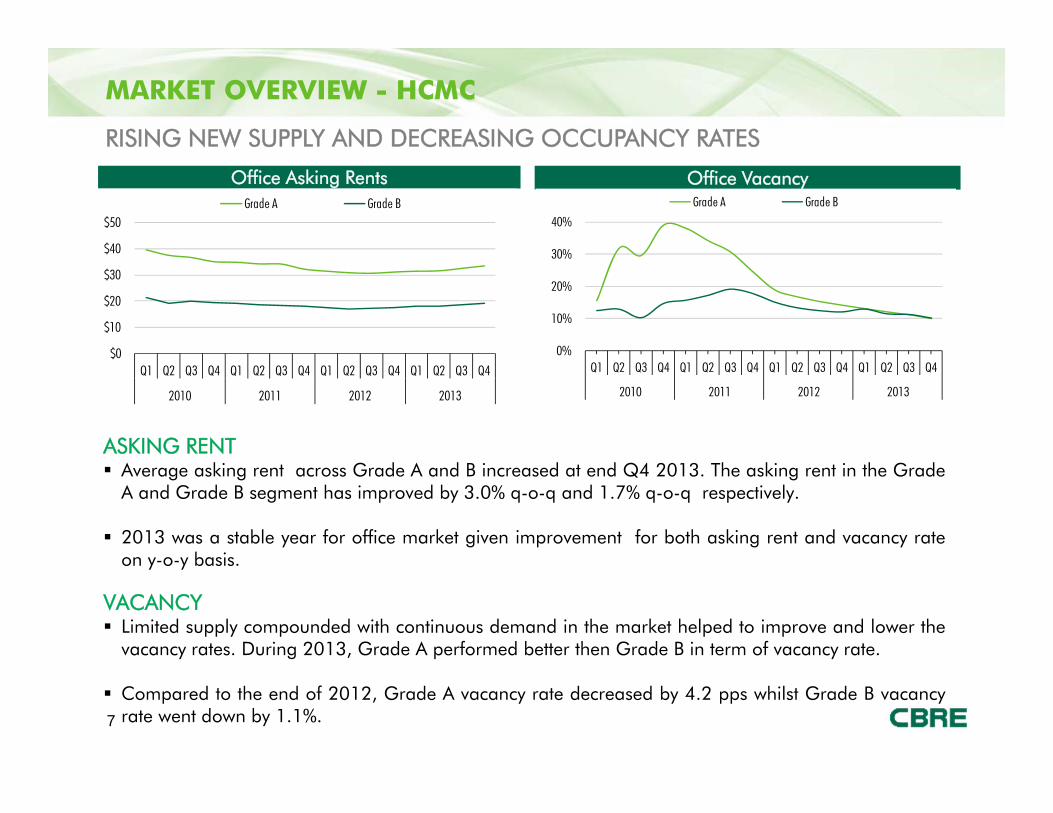

MARKET OVERVIEW - HCMC

RISING NEW SUPPLY AND DECREASING OCCUPANCY RATES

ASKING RENT Average asking rent across Grade A and B increased at end Q4 2013. The asking rent in the Grade

A and Grade B segment has improved by 3.0% q-o-q and 1.7% q-o-q respectively.

2013 was a stable year for office market given improvement for both asking rent and vacancy rateon y-o-y basis.

VACANCY Limited supply compounded with continuous demand in the market helped to improve and lower the

vacancy rates. During 2013, Grade A performed better then Grade B in term of vacancy rate.

Compared to the end of 2012, Grade A vacancy rate decreased by 4.2 pps whilst Grade B vacancyrate went down by 1.1%.

Office Asking Rents Office Vacancy

$0

$10

$20

$30

$40

$50

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2010 2011 2012 2013

Grade A Grade B

0%

10%

20%

30%

40%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2010 2011 2012 2013

Grade A Grade B

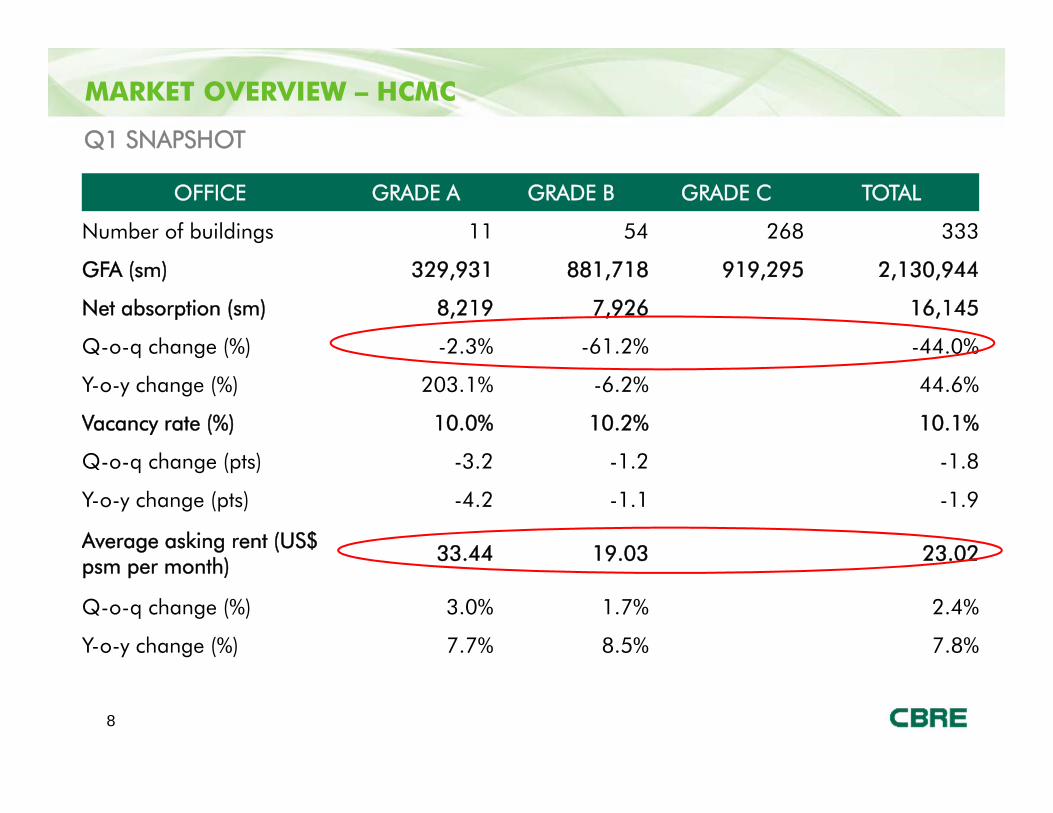

OFFICE GRADE A GRADE B GRADE C TOTAL

Number of buildings 11 54 268 333

GFA (sm) 329,931 881,718 919,295 2,130,944

Net absorption (sm) 8,219 7,926 16,145

Q-o-q change (%) -2.3% -61.2% -44.0%

Y-o-y change (%) 203.1% -6.2% 44.6%

Vacancy rate (%) 10.0% 10.2% 10.1%

Q-o-q change (pts) -3.2 -1.2 -1.8

Y-o-y change (pts) -4.2 -1.1 -1.9

Average asking rent (US$ psm per month) 33.44 19.03 23.02

Q-o-q change (%) 3.0% 1.7% 2.4%

Y-o-y change (%) 7.7% 8.5% 7.8%

MARKET OVERVIEW – HCMC

8

Q1 SNAPSHOT

9

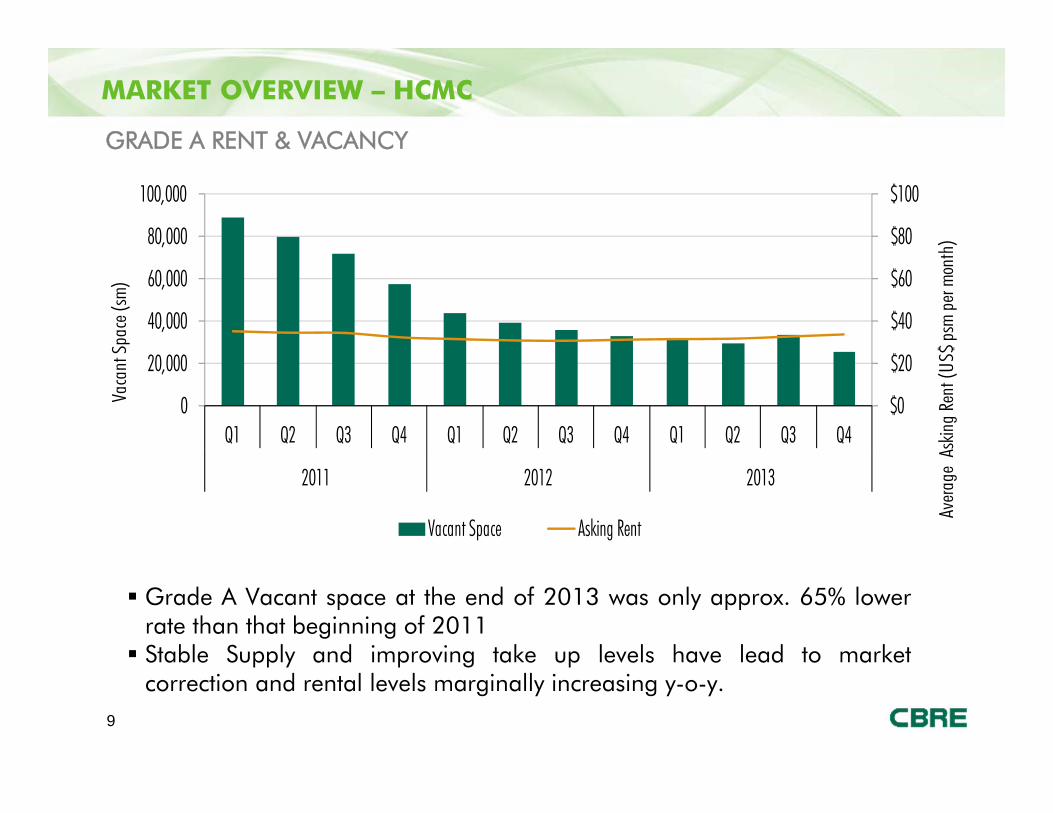

GRADE A RENT & VACANCY

MARKET OVERVIEW – HCMC

$0

$20

$40

$60

$80

$100

0

20,000

40,000

60,000

80,000

100,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012 2013

Aver

age

Askin

g Re

nt (U

S$ p

sm p

er m

onth

)

Vaca

nt S

pace

(sm

)

Vacant Space Asking Rent

Grade A Vacant space at the end of 2013 was only approx. 65% lowerrate than that beginning of 2011 Stable Supply and improving take up levels have lead to market

correction and rental levels marginally increasing y-o-y.

10

GRADE B RENT & VACANCY

MARKET OVERVIEW – HCMC

$0

$20

$40

$60

$80

$100

0

20,000

40,000

60,000

80,000

100,000

120,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012 2013 Aver

age

Askin

g Re

nt (U

S$ p

sm p

er m

onth

)

Vaca

nt S

pace

(sm

)

Vacant Space Asking Rent

Grade B Vacant space at the end of 2013 was approx. 10% lower thanthat at the beginning of 2011 Stable Supply and improving take up levels have lead to stabilization and

rental levels remaining flat

11

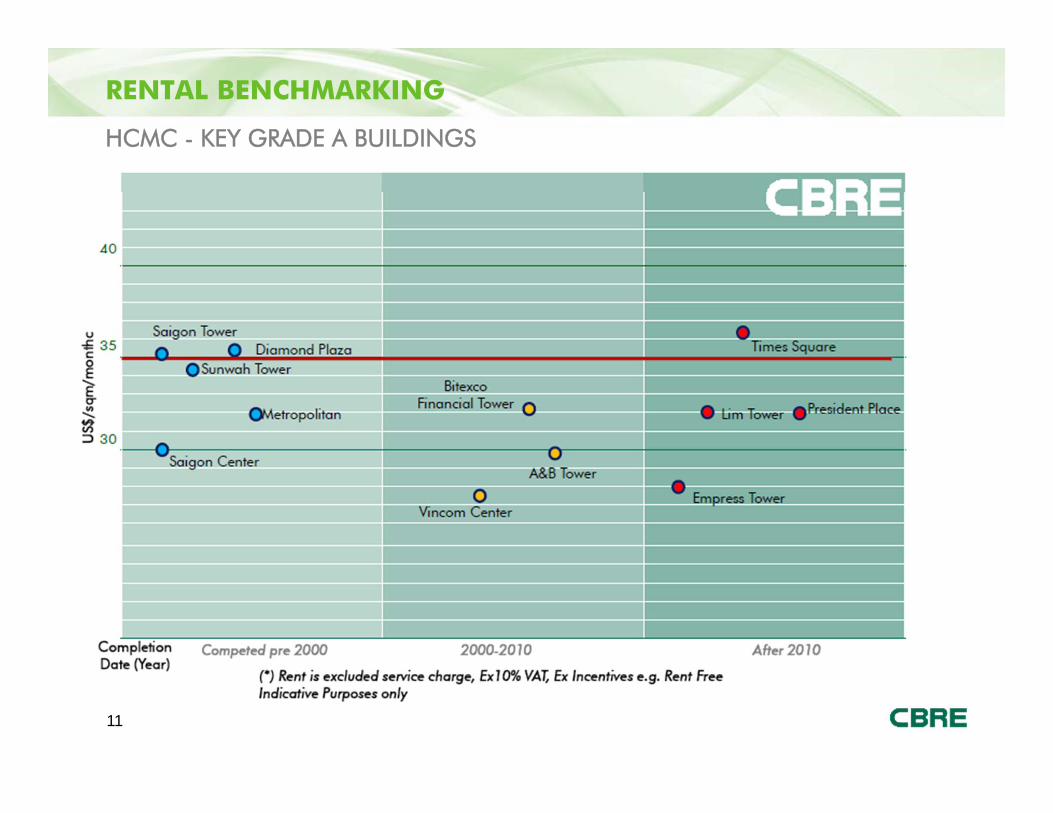

RENTAL BENCHMARKING

HCMC - KEY GRADE A BUILDINGS

12

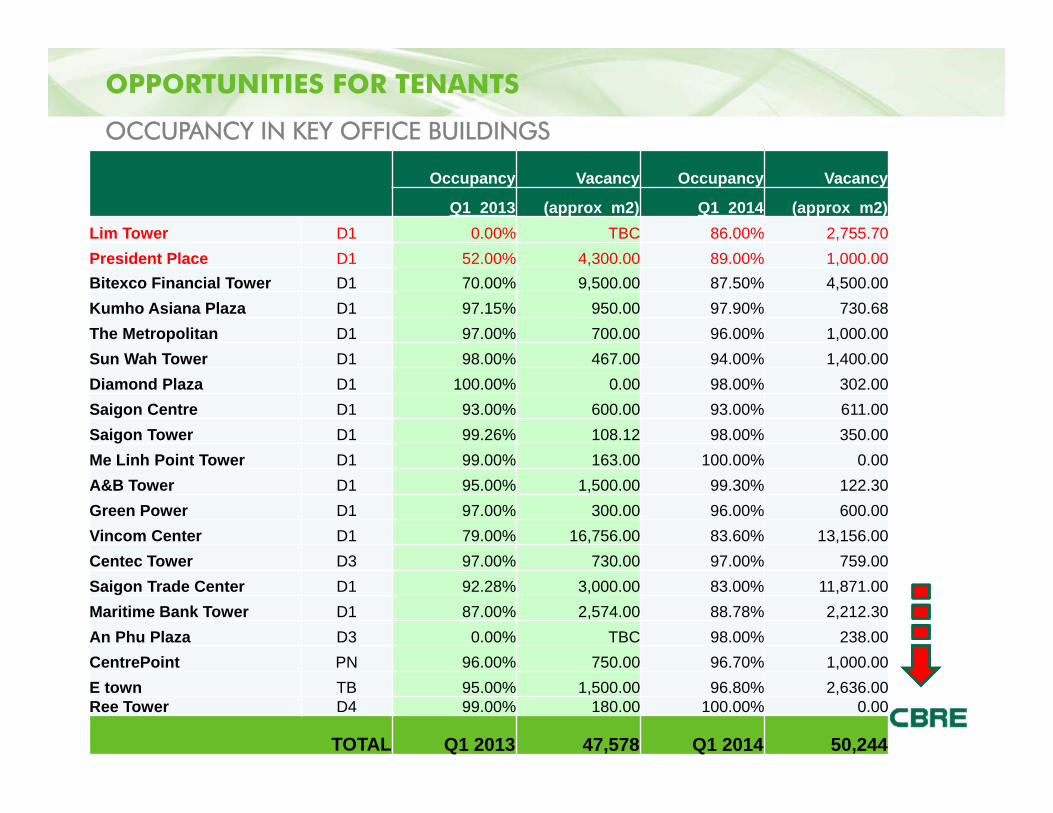

Occupancy Vacancy Occupancy Vacancy

Q1 2013 (approx m2) Q1 2014 (approx m2)Lim Tower D1 0.00% TBC 86.00% 2,755.70 President Place D1 52.00% 4,300.00 89.00% 1,000.00 Bitexco Financial Tower D1 70.00% 9,500.00 87.50% 4,500.00 Kumho Asiana Plaza D1 97.15% 950.00 97.90% 730.68 The Metropolitan D1 97.00% 700.00 96.00% 1,000.00 Sun Wah Tower D1 98.00% 467.00 94.00% 1,400.00 Diamond Plaza D1 100.00% 0.00 98.00% 302.00 Saigon Centre D1 93.00% 600.00 93.00% 611.00 Saigon Tower D1 99.26% 108.12 98.00% 350.00 Me Linh Point Tower D1 99.00% 163.00 100.00% 0.00 A&B Tower D1 95.00% 1,500.00 99.30% 122.30 Green Power D1 97.00% 300.00 96.00% 600.00 Vincom Center D1 79.00% 16,756.00 83.60% 13,156.00 Centec Tower D3 97.00% 730.00 97.00% 759.00 Saigon Trade Center D1 92.28% 3,000.00 83.00% 11,871.00 Maritime Bank Tower D1 87.00% 2,574.00 88.78% 2,212.30 An Phu Plaza D3 0.00% TBC 98.00% 238.00 CentrePoint PN 96.00% 750.00 96.70% 1,000.00 E town TB 95.00% 1,500.00 96.80% 2,636.00 Ree Tower D4 99.00% 180.00 100.00% 0.00

TOTAL Q1 2013 47,578 Q1 2014 50,244

OPPORTUNITIES FOR TENANTS

OCCUPANCY IN KEY OFFICE BUILDINGS

13

OPPORTUNITIES FOR TENANTSOCCUPANCY IN KEY OFFICE BUILDINGS

Occupancy%Q1 2013 vs Q1 2014

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Q1 2013

Q1 2014

14

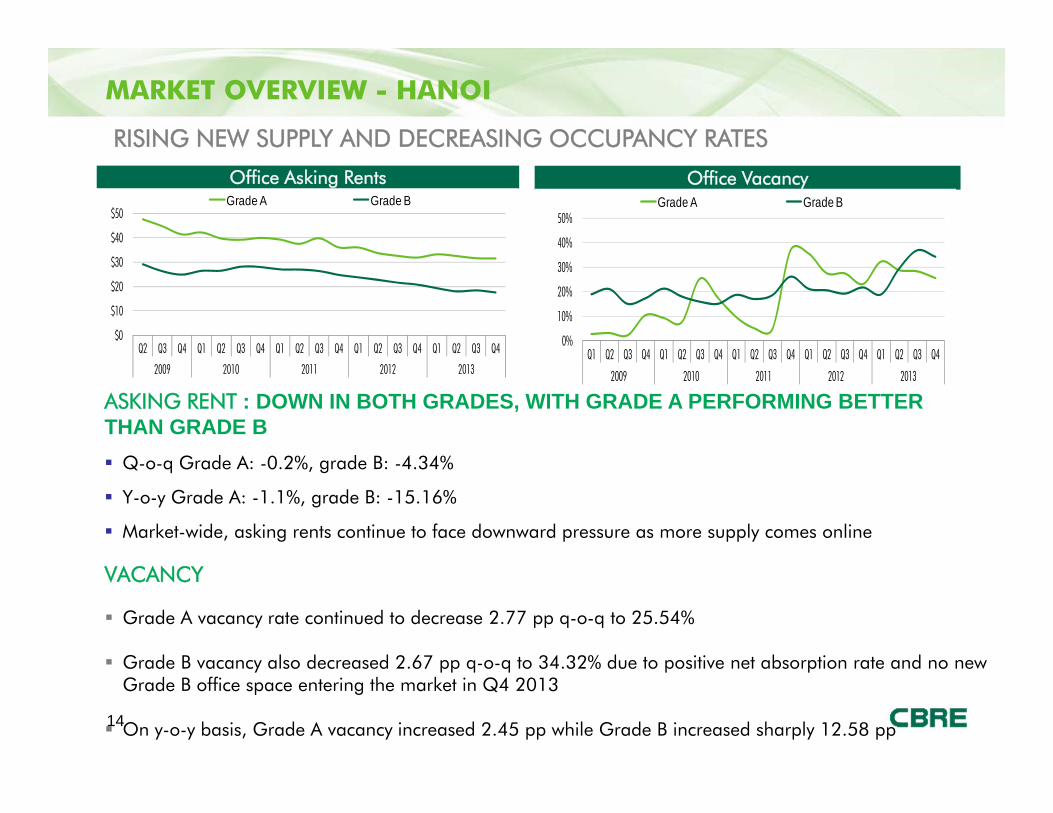

MARKET OVERVIEW - HANOI

RISING NEW SUPPLY AND DECREASING OCCUPANCY RATES

ASKING RENT : DOWN IN BOTH GRADES, WITH GRADE A PERFORMING BETTER THAN GRADE B Q-o-q Grade A: -0.2%, grade B: -4.34%

Y-o-y Grade A: -1.1%, grade B: -15.16%

Market-wide, asking rents continue to face downward pressure as more supply comes online

VACANCY

Grade A vacancy rate continued to decrease 2.77 pp q-o-q to 25.54%

Grade B vacancy also decreased 2.67 pp q-o-q to 34.32% due to positive net absorption rate and no newGrade B office space entering the market in Q4 2013

On y-o-y basis, Grade A vacancy increased 2.45 pp while Grade B increased sharply 12.58 pp

Office Asking Rents Office Vacancy

$0

$10

$20

$30

$40

$50

Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2009 2010 2011 2012 2013

Grade A Grade B

0%

10%

20%

30%

40%

50%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2009 2010 2011 2012 2013

Grade A Grade B

HOW TO “BEAT THE CYCLE?”

16

17

Asia Pacific, Office rental cycle, Grade A&B, Q4 2013

Shanghai New DelhiAdelaide

Guangzhou

Hanoi

Shenzhen

Tokyo

Melbourne

Singapore

Manila

Taipei

Auckland

Kuala Lumpur

Brisbane

Beijing

Seoul

Ho Chi Minh City

Jakarta

Hong Kong

Bangkok

Canberra

PerthSydney

Wellington

BangaloreAK

MS

HSGCW

ATM

T

JB

B

SN

PS

HS

B

H

M

B

Mumbai

HCMCLandlords TENANTs

Grade A and B vacancy rate: y-o-y Grade A and B asking rent: slightly –

but watch for Grade B supply

HANOITENANTs

Landlords

Grade A vacancy rate: Grade B vacancy rate: Grade A and B asking rent: y-o-y

OFFICE MARKET ANALYSIS

THE RENTAL CYCLE

18

OFFICE MARKET ANALYSIS

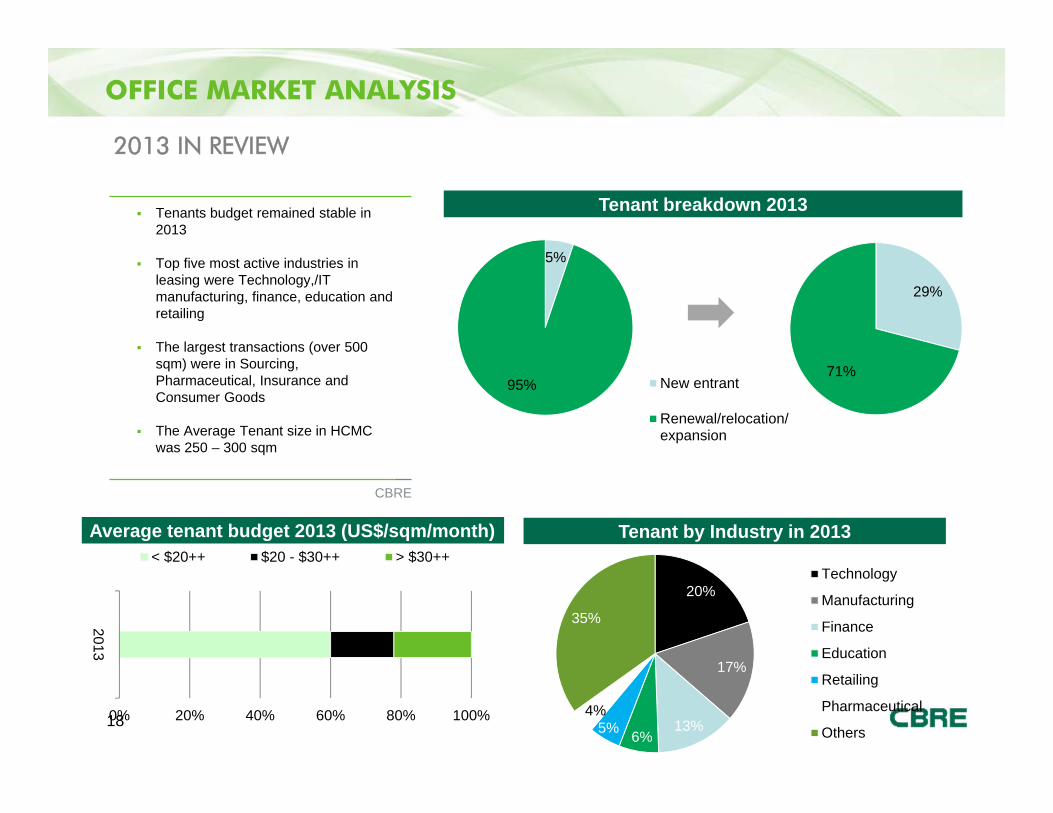

2013 IN REVIEW

5%

95%

Tenant breakdown 2013

Average tenant budget 2013 (US$/sqm/month) Tenant by Industry in 2013

29%

71%New entrant

Renewal/relocation/expansion

Tenants budget remained stable in 2013

Top five most active industries in leasing were Technology,/IT manufacturing, finance, education and retailing

The largest transactions (over 500 sqm) were in Sourcing, Pharmaceutical, Insurance and Consumer Goods

The Average Tenant size in HCMC was 250 – 300 sqm

CBRE

0% 20% 40% 60% 80% 100%

2013

< $20++ $20 - $30++ > $30++

20%

17%

13%6%5%

4%

35%

Technology

Manufacturing

Finance

Education

Retailing

Pharmaceutical

Others

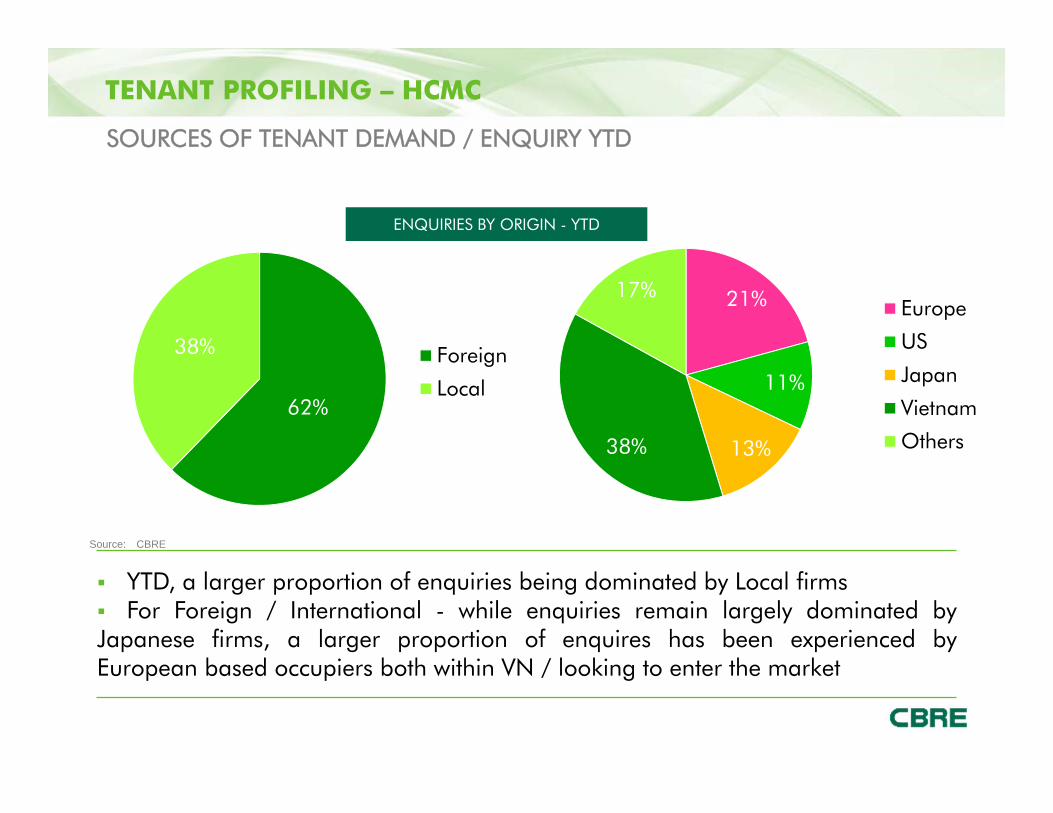

TENANT PROFILING – HCMC

YTD, a larger proportion of enquiries being dominated by Local firms For Foreign / International - while enquiries remain largely dominated byJapanese firms, a larger proportion of enquires has been experienced byEuropean based occupiers both within VN / looking to enter the market

ENQUIRIES BY ORIGIN - YTD

Source: CBRE

62%

38% Foreign

Local

21%

11%

13%38%

17%Europe

US

Japan

Vietnam

Others

SOURCES OF TENANT DEMAND / ENQUIRY YTD

20

BUDGET & LOCATION TRENDS YTD

51.2%$1k-2k

BUDGET

LOCATION

TENANT PROFILING – HCMC

< $20 ++ • 77%

< $20 - $30 ++ • 23%

CBD • 73%

Source: CBRE

77%

23%

<$20

$20 - < $30

NON CBD • 27%73%

27%CBD

Non CBDNON CBD • 27%

21

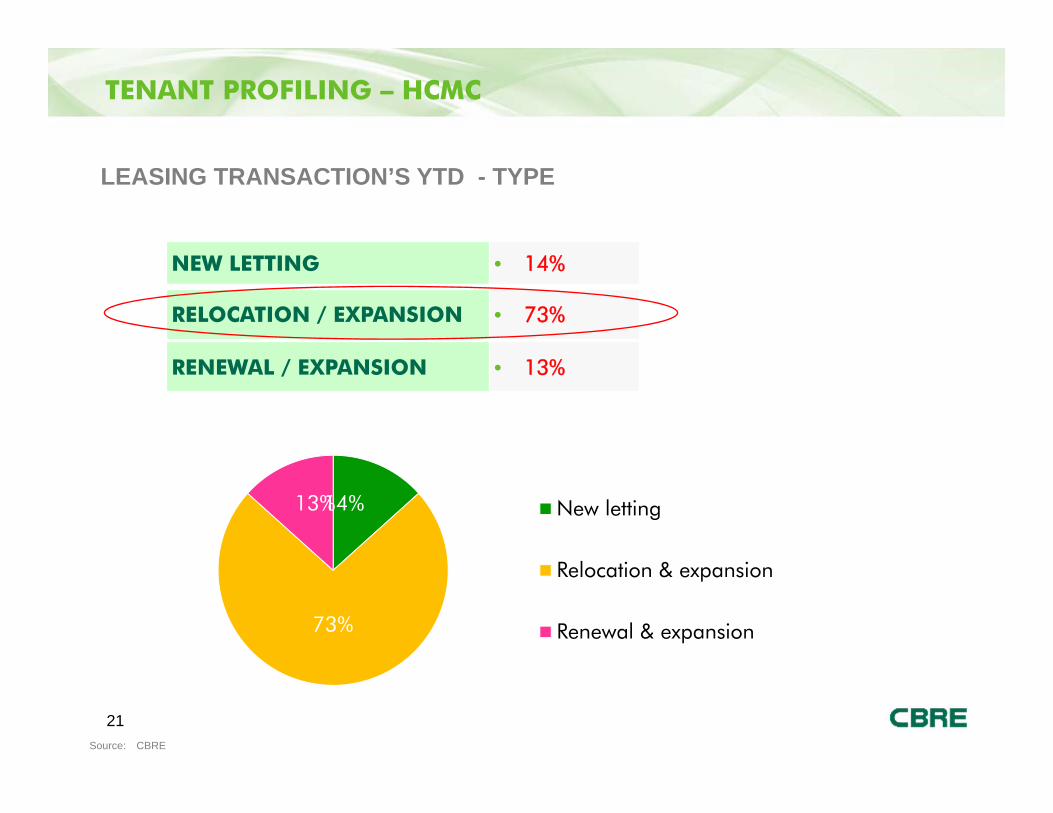

51.2%$1k-2k

LEASING TRANSACTION’S YTD - TYPE

NEW LETTING • 14%

RELOCATION / EXPANSION • 73%

RENEWAL / EXPANSION • 13%

TENANT PROFILING – HCMC

Source: CBRE

14%

73%

13% New letting

Relocation & expansion

Renewal & expansion

22

STANDARD INCENTIVES REQUIRED TO ENCOURAGE TENANTS TO LEASE

1. Rent free period2. Parking 3. Fit out period4. Rental Cap and Collar 5. Reinstatement Provisions 6. Cleaning services – Discounted / offering of internal unit cleaning as part

of Service Charge7. Out of out-of-hours air-conditioning8. Upfront Rental Payment

ADDITIONAL INCENTIVES & EXPECTATIONS FROM TENANTS TO “SEAL THE DEAL”

1. Option to Renew 2. Early termination right 3. Bank guarantees Vs deposit 4. First Right of Refusal

POTENTIAL TENANT INCENTIVES – OTHER THAN RENT

TENANT PROFILING

23

1. TYPE OF BUSINESS • Industry type can define location• E.g. Banking / Finance D1. Call centre non CBD

2. LENGTH OF TENANCY • Current lease term length

3. REASON FOR MOVING • Expansion? Consolidation? Cost

4. CURRENT REQUIREMENTS• Understanding current needs and whether

existing size / accommodation suitable.• Current location, space, head count, expiry etc

5. FUTURE REQUIREMENTS• Headcount, location, space sqm, building grade

desired, operational date, operational hours, IT provider etc

6. PARKING • No. of car and motorbike

7. BUDGET • Monthly / p/sqm

8. OTHER OPERATIONAL FACTORS • Security, Back Up Power, IT. Fire & Safety, Signage

KEY FACTORS TO UNDERSTAND BEFORE MOVING

TENANT PROFILING

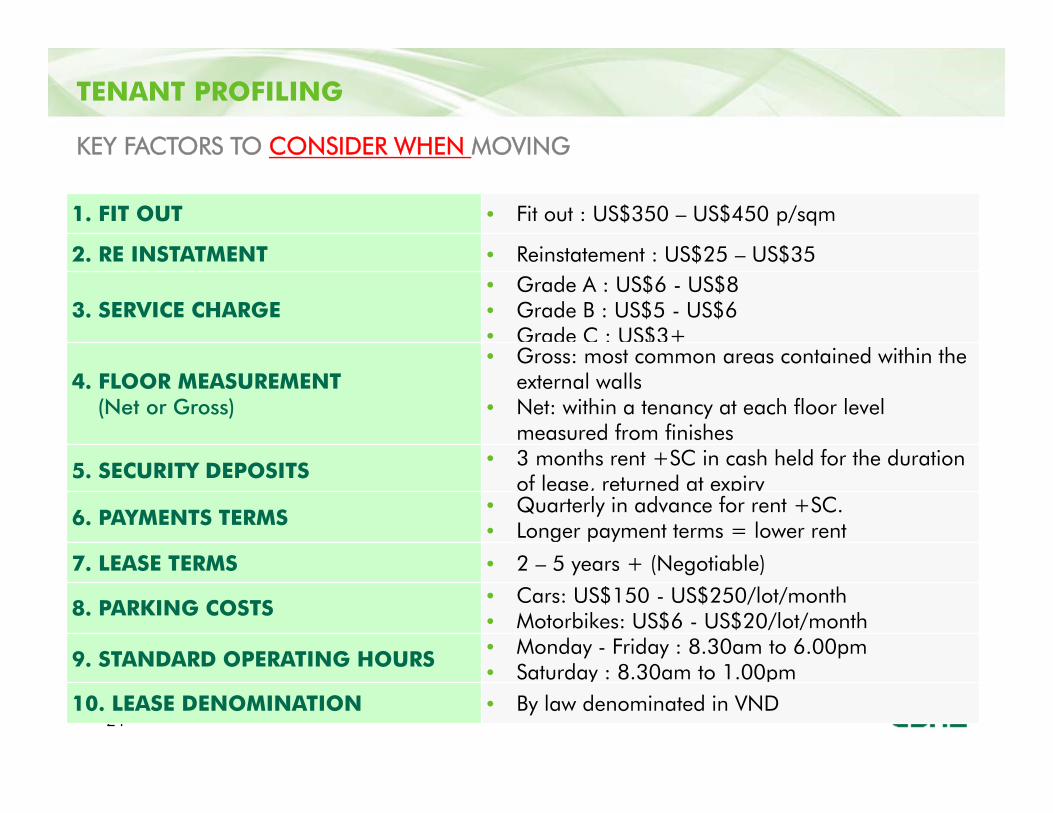

24

1. FIT OUT • Fit out : US$350 – US$450 p/sqm

KEY FACTORS TO CONSIDER WHEN MOVING

2. RE INSTATMENT • Reinstatement : US$25 – US$35

3. SERVICE CHARGE• Grade A : US$6 - US$8• Grade B : US$5 - US$6• Grade C : US$3+

4. FLOOR MEASUREMENT(Net or Gross)

• Gross: most common areas contained within the external walls

• Net: within a tenancy at each floor level measured from finishes

5. SECURITY DEPOSITS • 3 months rent +SC in cash held for the duration of lease, returned at expiry

6. PAYMENTS TERMS • Quarterly in advance for rent +SC. • Longer payment terms = lower rent

7. LEASE TERMS • 2 – 5 years + (Negotiable)

8. PARKING COSTS • Cars: US$150 - US$250/lot/month• Motorbikes: US$6 - US$20/lot/month

9. STANDARD OPERATING HOURS • Monday - Friday : 8.30am to 6.00pm• Saturday : 8.30am to 1.00pm

10. LEASE DENOMINATION • By law denominated in VND

TENANT PROFILING - OPTIMIZING YOUR OFFICE SPACE

Its not about the amount of space you leasebut how you need to use the space. Meeting your headcount and growthprojections are important but there will beincreased amenity space and support spaceneeded as well …. Workstyle and workplace should always gohand in hand …. The correct use of new technologies canreduce your space needs… Floor plate efficiencies vary widely and canaccount for up to 20% in lost useable space… Do an full site assessment beforehand….

Before committing to a new lease…….….a few thoughts about your office layout

26

Get a professional interior designer, engineer and Project Manager on board.

Doing it yourself will cost you money in the long run…

Points to consider: A thorough Programming Session Technical Site Assessment Determining your space

requirements Test Fits Preliminary budgets and

schedules

TENANT PROFILING - OPTIMIZING YOUR OFFICE SPACE

OUTLOOK & PREDICTIONS2014 +

28

29

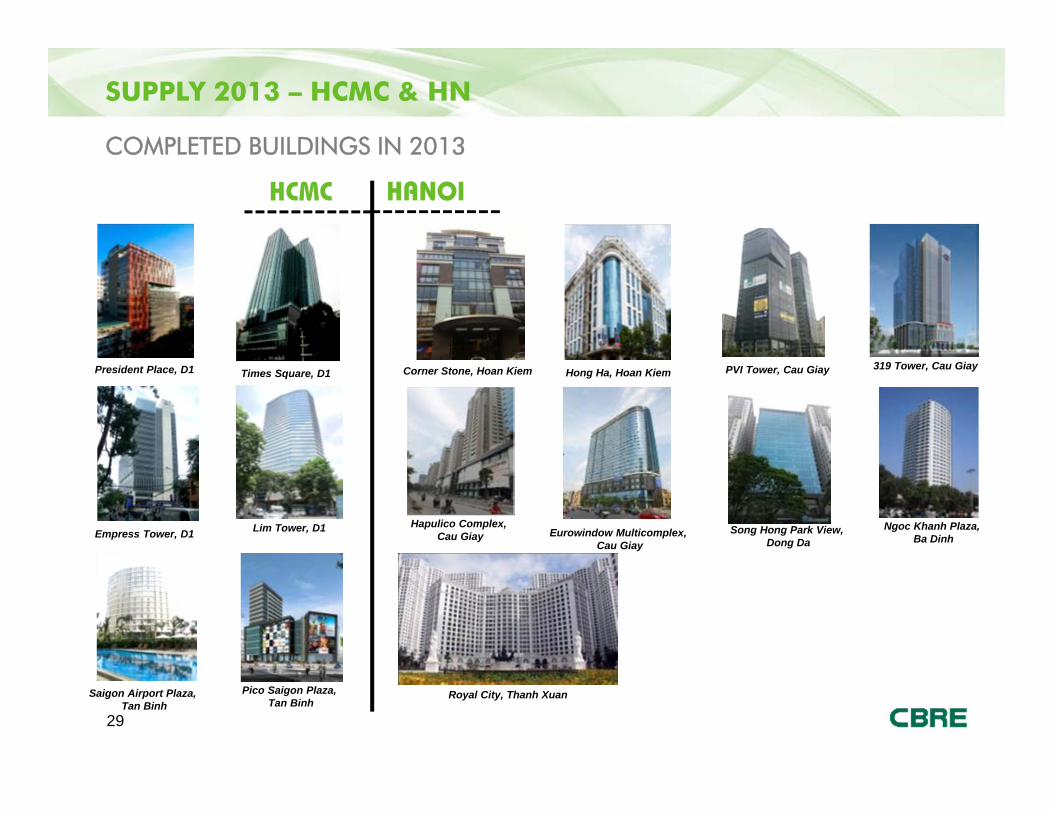

SUPPLY 2013 – HCMC & HN

COMPLETED BUILDINGS IN 2013

President Place, D1

HCMC HANOI

Lim Tower, D1

Saigon Airport Plaza, Tan Binh

Corner Stone, Hoan Kiem PVI Tower, Cau Giay

Eurowindow Multicomplex, Cau Giay

Empress Tower, D1

Times Square, D1

Pico Saigon Plaza, Tan Binh

Song Hong Park View, Dong Da

Hong Ha, Hoan Kiem 319 Tower, Cau Giay

Hapulico Complex, Cau Giay

Ngoc Khanh Plaza, Ba Dinh

Royal City, Thanh Xuan

30

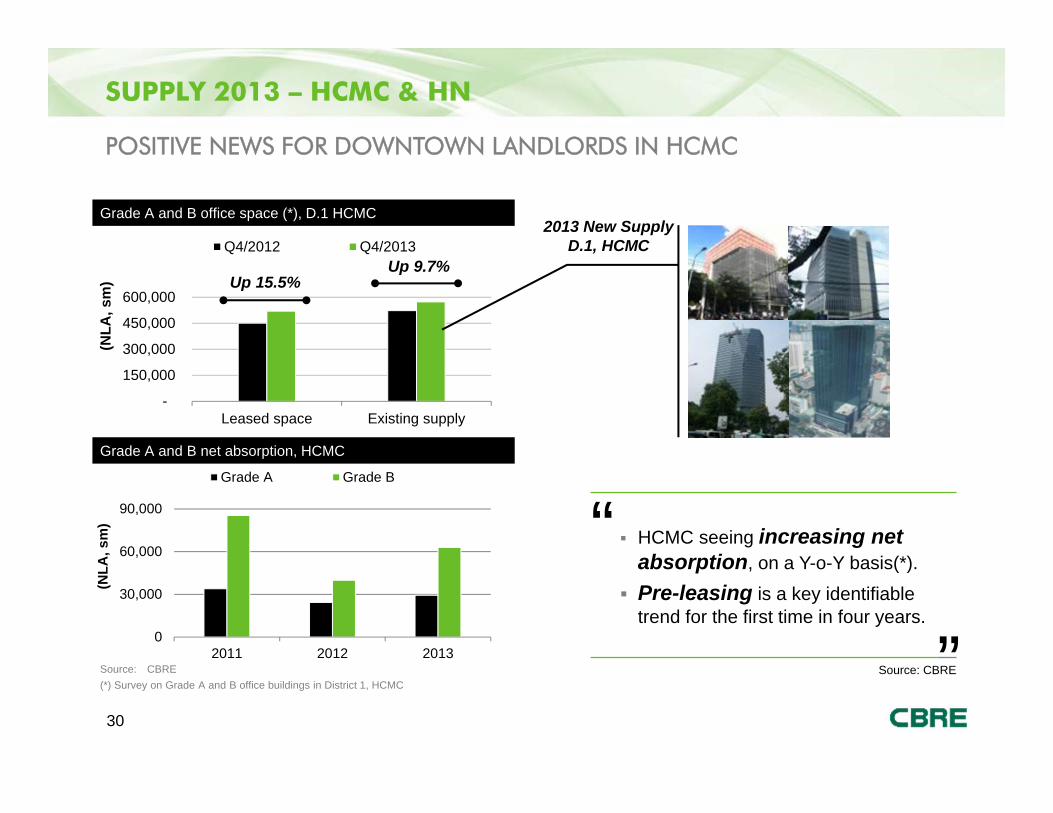

SUPPLY 2013 – HCMC & HN

POSITIVE NEWS FOR DOWNTOWN LANDLORDS IN HCMC

Source: CBRE

Grade A and B office space (*), D.1 HCMC

(*) Survey on Grade A and B office buildings in District 1, HCMC

-

150,000

300,000

450,000

600,000

Leased space Existing supply

(NLA

, sm

)

Q4/2012 Q4/2013Up 9.7%

Up 15.5%

2013 New Supply D.1, HCMC

Grade A and B net absorption, HCMC

0

30,000

60,000

90,000

2011 2012 2013

(NLA

, sm

)

Grade A Grade B

“ HCMC seeing increasing net absorption, on a Y-o-Y basis(*).

Pre-leasing is a key identifiable trend for the first time in four years.

”Source: CBRE

31

SUPPLY YTD – HCMC 2014 PIPELINE

CURRENT & FUTURE SUPPLY

0

100,000

200,000

300,000

400,000

500,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2010 2011 2012 2013 2014

Gross Flo

or Area

(sm)

Exisitng supply Future supply Total GFA

0

200,000

400,000

600,000

800,000

1,000,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2010 2011 2012 2013 2014

Gross F

loor Are

a (sm)

Exisitng supply New supply Total GFA

GRADE A

GRADE B

32

Union Square20,000 sm GFA

CBD

Union Square20,000 sm GFA

CBD

Vietcombank Tower55,000 sm GFA

CBD

Vietcombank Tower55,000 sm GFA

CBD

MB Sunny Tower16,000 sm GFA

CBD

MB Sunny Tower16,000 sm GFA

CBD

HCMC UPCOMING COMPLETED 2014 SUPPLY

Viettel Tower65,971 sm GFA

CMT8, D3

Viettel Tower65,971 sm GFA

CMT8, D3

OPPORTUNITIES FOR TENANTS – 2014 PIPELINE

V-Tower 12,500 sm GFA

DBP, Binh Thanh

V-Tower 12,500 sm GFA

DBP, Binh Thanh

33

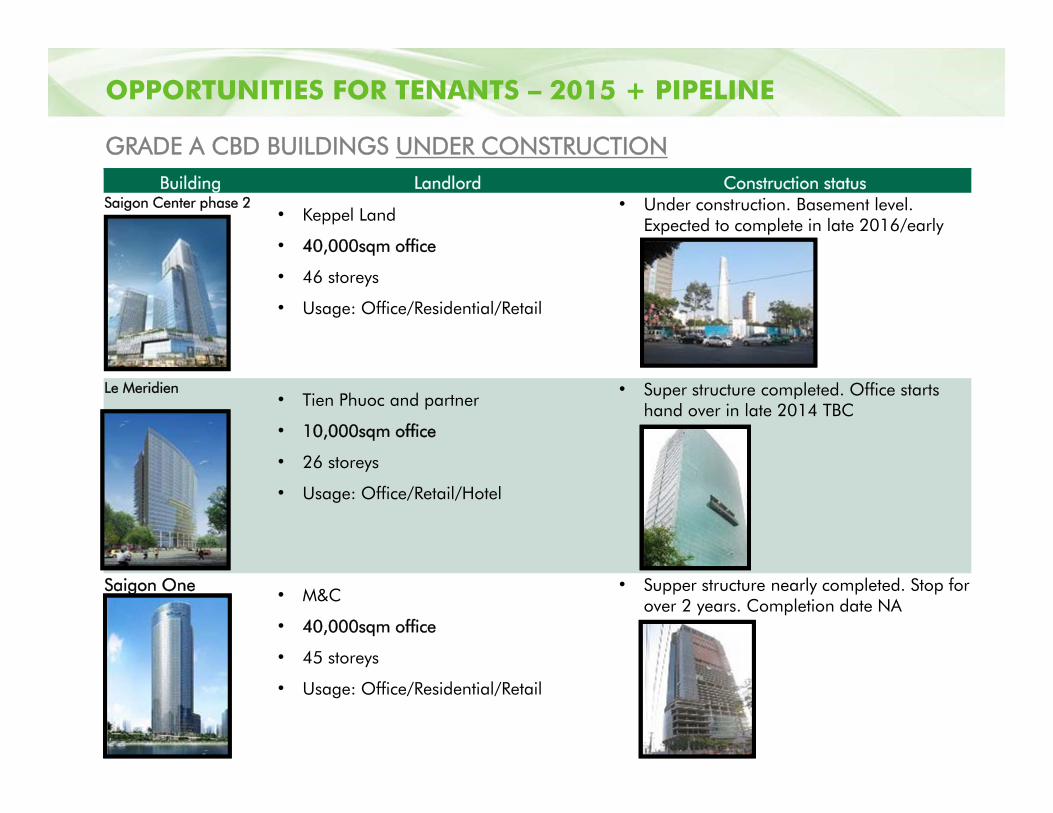

Building Landlord Construction statusSaigon Center phase 2

• Keppel Land

• 40,000sqm office

• 46 storeys

• Usage: Office/Residential/Retail

• Under construction. Basement level. Expected to complete in late 2016/early 2017

Le Meridien• Tien Phuoc and partner

• 10,000sqm office

• 26 storeys

• Usage: Office/Retail/Hotel

• Super structure completed. Office startshand over in late 2014 TBC

Saigon One • M&C

• 40,000sqm office

• 45 storeys

• Usage: Office/Residential/Retail

• Supper structure nearly completed. Stop for over 2 years. Completion date NA

OPPORTUNITIES FOR TENANTS – 2015 + PIPELINE

GRADE A CBD BUILDINGS UNDER CONSTRUCTION

34

Building Landlord Construction updateViettel

• Viettel Corporation

• 45,000sqm office

• 33 storeys

• Usage: Office/ Retails

• Under construction up to 20th

floor, aim to complete Q1 2015. Q4 2014 handover

SSG Tower• SSG Group

• 35,000sqm office

• Block 1: 27 storeys. Block 2: 19 storeys. 5

commercial storeys

• Usage: Office/ Apartment/ Retails

• Under construction up to 10th

floor. Expected to complete in Q1 2015 for handover

Lim Tower 2 • Hoa Lam

• 20,000sqm office

• 22 storeys

• Usage: Office/ Retails

• Under construction up to 3rd

level. Expected to complete in Q1 2015 for handover

OPPORTUNITIES FOR TENANTS – 2014 / 2015 + PIPELINE

MAJOR DECENTRALISED BUILDINGS UNDER CONSTRUCTION

Source: CBRE

WHAT DOES THE FUTURE HOLD? OUTLOOK ...

36

Pre-commitments in 2014. Only 4 buildings (A and B Grade)combined in the HCMC CBD have a floor plate over 1,000 sqm

In District 1, 10 buildings (A and B Grade) can provide over 1,000sqm of available space today

7 are Grade A buildings and only 3 Grade B buildings. MB SunnyTower is one of those Grade B buildings

Of the 7, only 3 buildings in District 1 can provide contiguous spaceover 1,000 sqm (in one line)

This means, VERY few options for MNCs seeking internationalstandard, quality buildings with large availability un til the end of2014

50% of the 175+ NEW Small-Medium sized buildings are beingbuilt by SOEs and 50% are for owner occupation

For large Tenants planning an occupancy solution, the market willremain tight until the end of 2014 as a result Rent levels will remainstable at least until Q1 2015 when the next wave of supply comesonline

WHAT DOES THE FUTURE HOLD? OUTLOOK ...

MB SUNNY TOWER

38

MB SUNNY TOWER

39

Prime location, positioned one of the main arterial roads of HCMC,connecting the CBD - D.1 and D.3 ,D.4, D5 with easy access from all districts Within a 1.5 km radius positioned opposite the newly completed 5 starPullman Hotel.

MB SUNNY TOWER – PRIME LOCATION

Panoramic city view

40

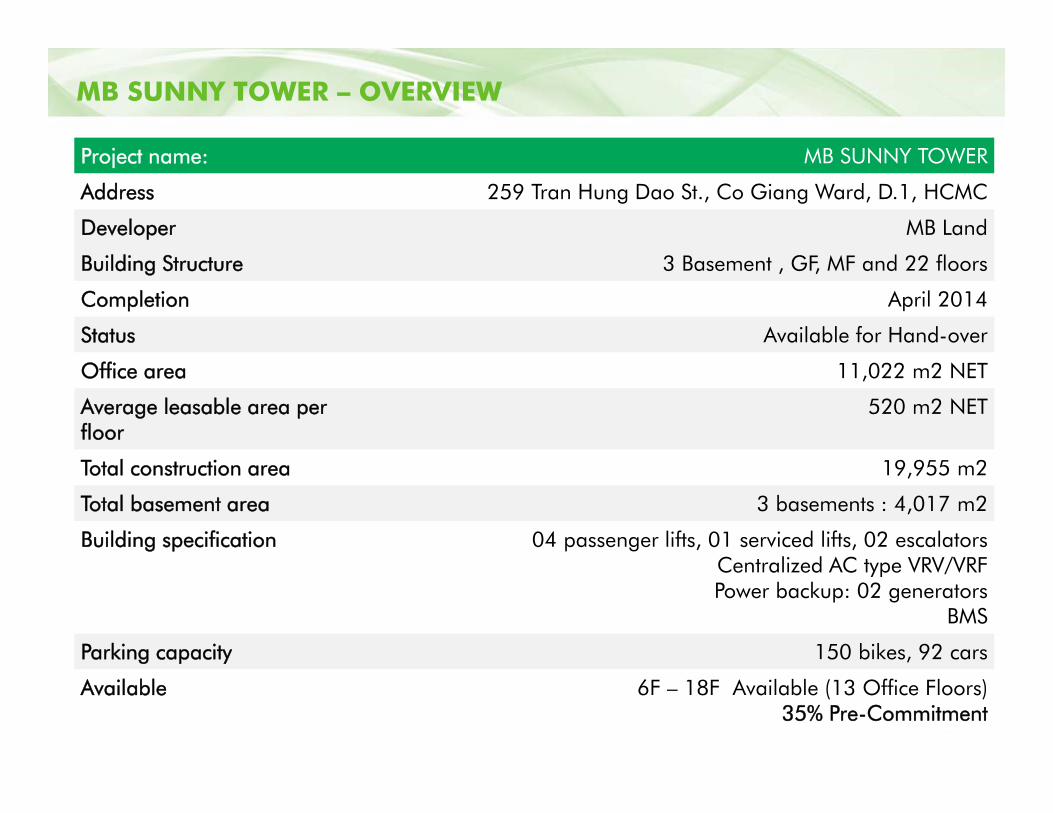

MB SUNNY TOWER – OVERVIEW

Project name: MB SUNNY TOWER

Address 259 Tran Hung Dao St., Co Giang Ward, D.1, HCMC

Developer MB Land

Building Structure 3 Basement , GF, MF and 22 floors

Completion April 2014

Status Available for Hand-over

Office area 11,022 m2 NET

Average leasable area per floor

520 m2 NET

Total construction area 19,955 m2

Total basement area 3 basements : 4,017 m2

Building specification 04 passenger lifts, 01 serviced lifts, 02 escalatorsCentralized AC type VRV/VRF Power backup: 02 generators

BMS

Parking capacity 150 bikes, 92 cars

Available 6F – 18F Available (13 Office Floors)35% Pre-Commitment

41

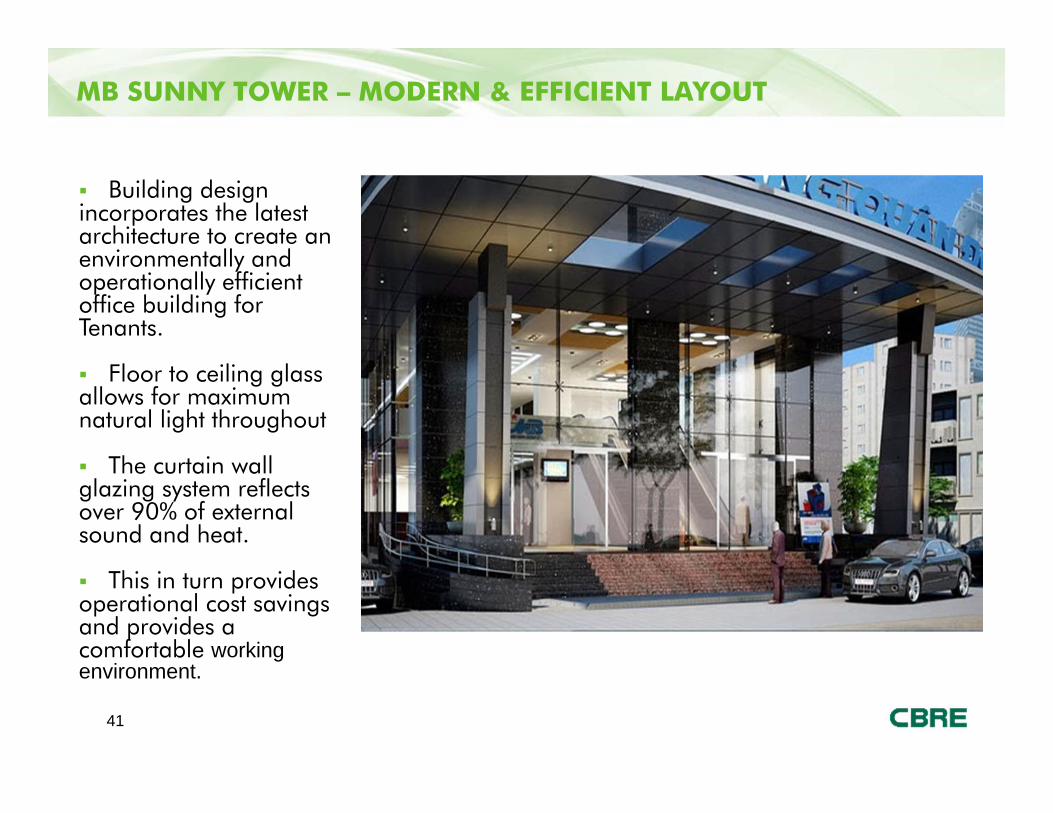

Building design incorporates the latest architecture to create an environmentally and operationally efficient office building for Tenants.

Floor to ceiling glass allows for maximum natural light throughout

The curtain wall glazing system reflects over 90% of external sound and heat.

This in turn provides operational cost savings and provides a comfortable working environment.

MB SUNNY TOWER – MODERN & EFFICIENT LAYOUT

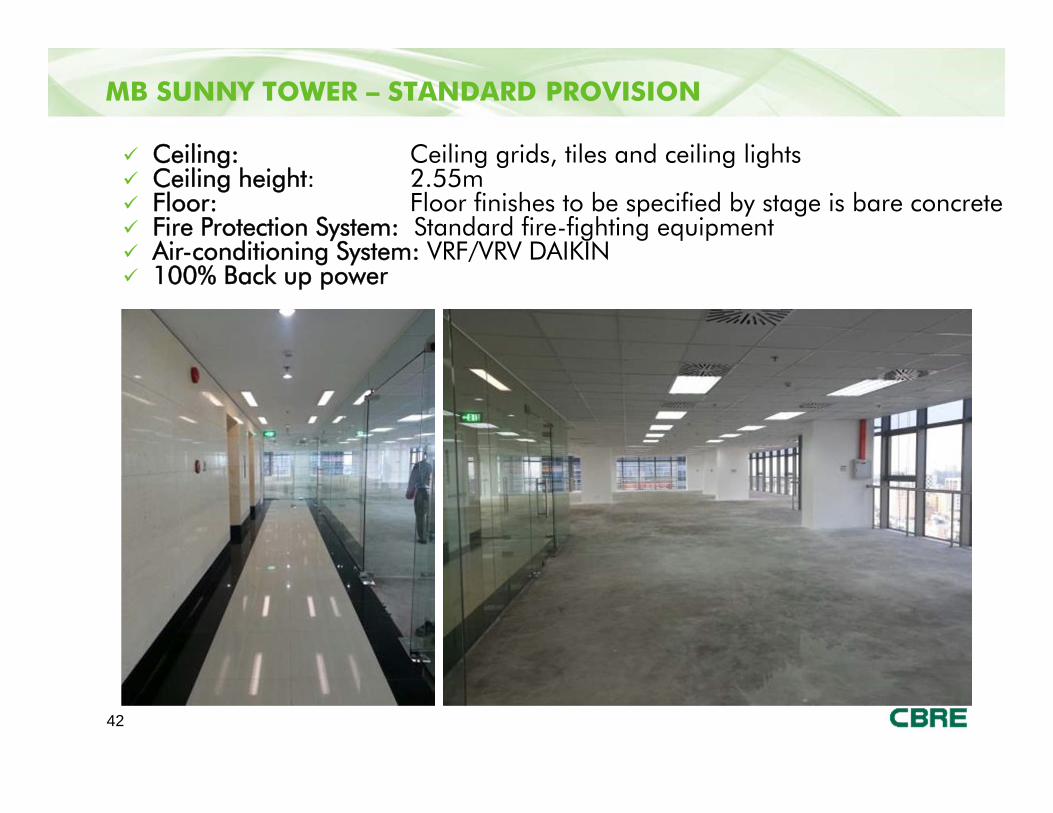

MB SUNNY TOWER – STANDARD PROVISION

42

Ceiling: Ceiling grids, tiles and ceiling lights Ceiling height: 2.55m Floor: Floor finishes to be specified by stage is bare concrete. Fire Protection System: Standard fire-fighting equipment Air-conditioning System: VRF/VRV DAIKIN 100% Back up power

43

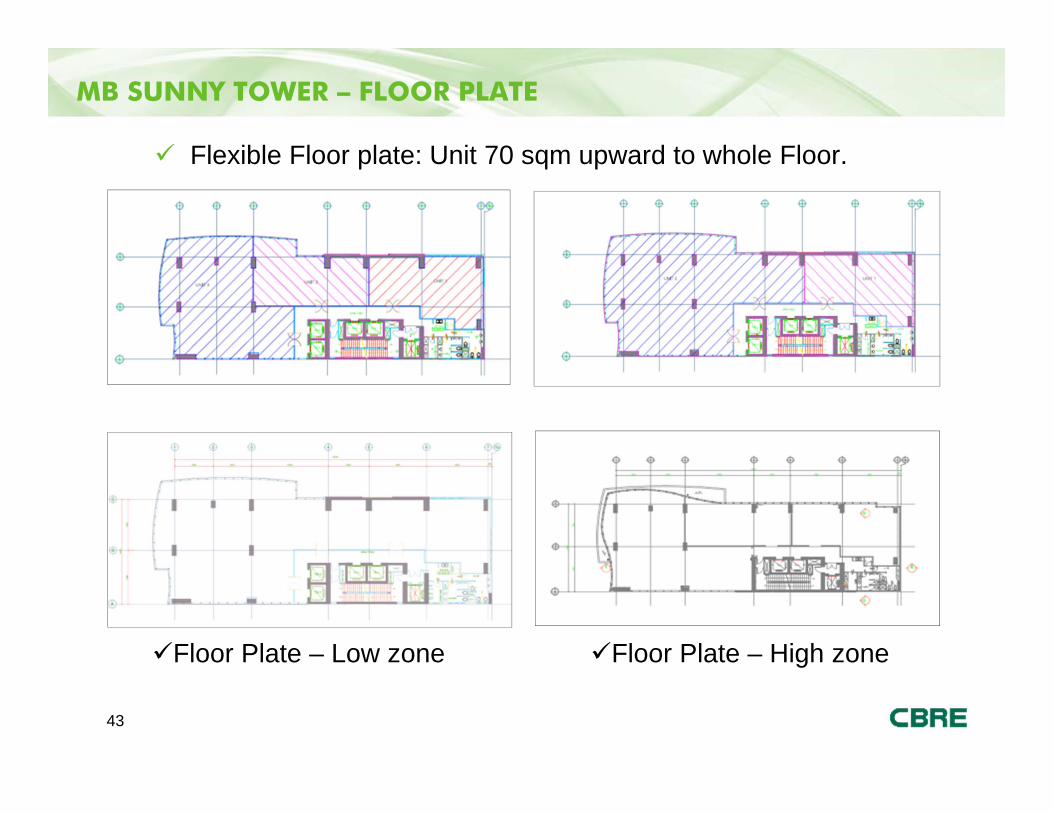

MB SUNNY TOWER – FLOOR PLATE

Flexible Floor plate: Unit 70 sqm upward to whole Floor.

Floor Plate – Low zone Floor Plate – High zone

44

© 2014, CBRE, Group Inc. CBRE Limited confirms that information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt their accuracy, we have not verified them and make no guarantee, warranty or representation about them. It is your responsibility to confirm independently their accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be reproduced without prior written permission of CBRE.

About CBRE Group, Inc.CBRE Group, Inc. (NYSE:CBG), a Fortune 500 and S&P 500 company headquartered in Los Angeles, is the world’s largest commercial real estate services firm (in terms of 2011 revenue). The Company has approximately 34,000 employees (excluding affiliates), and serves real estate owners, investors and occupiers through more than 300 offices (excluding affiliates) worldwide. CBRE offers strategic advice and execution for property sales and leasing; corporate services; property, facilities and project management; mortgage banking; appraisal and valuation; development services; investment management; and research and consulting. Please visit our Web site at www.cbre.com.

OFFICE ENQUIRY HOTLINE 0936 299 899

Thank you