Languages

Pages

Legal

CB Industrial Product Holding Berhad Equipping Palm Oil Industries Around The World

CBIP Financial Highlights

2Q 2012

Operational Highlights

• Leading engineering company specializing in construction and

engineering of palm oil mills Strong in engineering expertise and experience in construction of palm oil mill

• Leading manufacturer and supplier of Palm Oil Mill components

• Successfully invented and commercialized Modipalm mills with patented

continuous sterilization process Patented in Malaysia and Indonesia till 2021 Modipalm granted pioneer status for 10 years till 2015

• Sustaining longer term contribution from Plantation activities Steady earnings from plantation associates and JVs Building platform for future growth through plantation assets in Kalimantan,

Indonesia

2

Financial Highlights & Corporate Developments

• Strong growth in continuing operations FY11 revenue and PBT of RM322.6m and RM70.9m translate to y-o-y growth of

19.1% and 35.21% respectively Growth sustained with revenue +95.8% and PBT +71.3% in 2QFY12

• Balance sheet in net cash position

• Declared and paid total tax exempt dividend of 35sen per share for FY11 Comprising of interim dividend of 5sen* per share, and a second interim dividend

of 30sen per share paid in May 2012

• Declared tax exempt dividend for FY12

Declared interim dividend of 10sen per share payable in Sep 2012

• Latest corporate exercises Completed acquisition of 94% of PT Berkala Maju Bersama (BMB) and PT Jaya Jadi

Utama (JJU) in April 2012 for a total purchase price equivalent to RM14.2m Completed sale of Sachiew Plantations Sdn Bhd and Empresa (M) Sdn Bhd in May

2012 for total cash consideration of RM268m Proposed acquisition 94% of PT Gumas Alam Subur (GAS) in August 2012 for a total

purchase price equivalent to RM6.3m

3

* adjusted for 1 for 1 bonus issue completed in March 2012

CB Industrial Product Holding Berhad Equipping Palm Oil Industries Around The World

Review of 2QFY12 Results

Key Financial Highlights

FYE Dec (RMm) 2QFY12 2QFY11 % Chg FY11 FY10 % Chg

Revenue 264.89 135.28 +95.8 322.61 270.89 +19.1

Profit from Operations 45.72 16.15 +183.1 49.91 40.36 +23.7

Associates & Jointly-controlled 3.67 13.04 (71.7) 22.51 13.98 +61.0

PBT 48.90 28.54 +71.3 70.89 52.48 +35.1

Net Profit (after MI) * 42.39 25.52 +66.1 68.34 48.78 +40.1

Opt Margin (%) 17.3 11.9 15.5 14.9

* net profit from continuing operations

• Revenue growth underpinned by Increase in project billings Improvement in project completion for retrofitting special purpose vehicles

• Improved profitability for mill equipment & construction operations Higher better margin mechanical portion vs turnkey/civil works Ability to command premium pricing for Modipalm mills

• Lower CPO prices and production led to reduced profits from plantation

associates and JVs

5

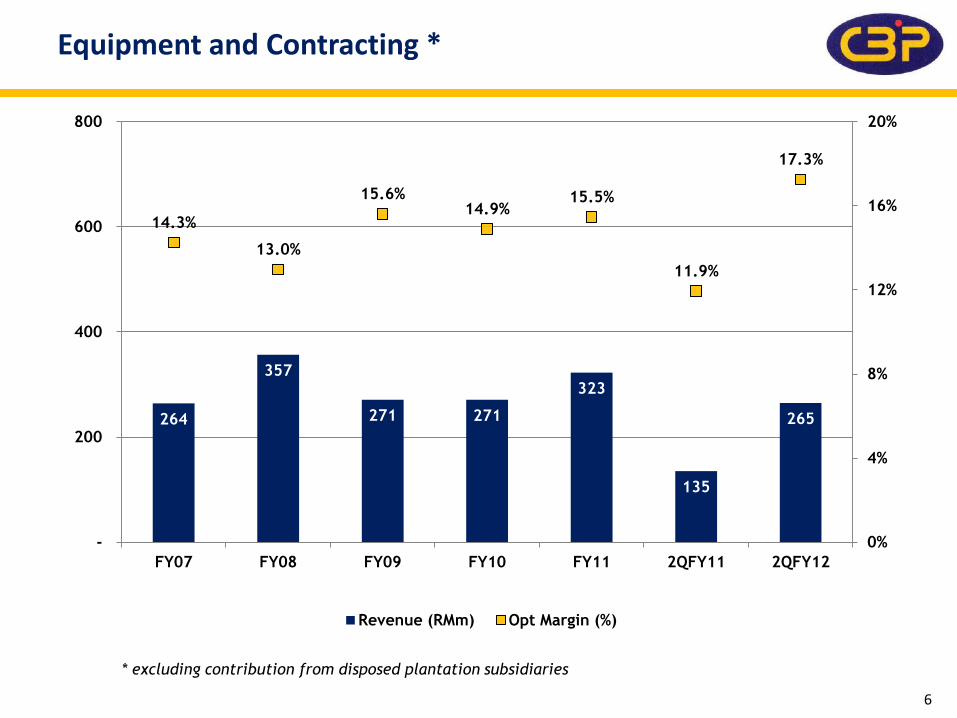

Equipment and Contracting *

264

357

271 271

323

135

265

14.3%

13.0%

15.6% 14.9%

15.5%

11.9%

17.3%

0%

4%

8%

12%

16%

20%

-

200

400

600

800

FY07 FY08 FY09 FY10 FY11 2QFY11 2QFY12

Revenue (RMm) Opt Margin (%)

6

* excluding contribution from disposed plantation subsidiaries

Dividend

1.5 1.8 2.5 2.5 2.5 2.5 5.0

10.0 2.5

30.0

1.5 1.8 2.5

8.1 32% 31% 29%

11% 17%

52%

90%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

5

10

15

20

25

FY05 FY06 FY07 FY08 FY09 FY10 * FY11 FY12

Interim 2nd Interim Final Dividend payout (LHS)

Gross dividend per share (sen) ^ Payout ratio (%)

35

* credited 3rd interim share dividend of 1 for 20 for FY10

^ adjusted for 1 for 1 bonus

• 2nd interim of 30 sen for FY11 paid out on 30 May 2012

• Interim of 10 sen for FY12 payable on 28 Sep 2012

• To maintain one-third of net profit as dividend payment

7

CB Industrial Product Holding Berhad Equipping Palm Oil Industries Around The World

Operations & Prospects

Production Capacity & Projects Award

• Capacity to produce 14 mills per annum with > 66,000 sq m floor space

9

Financial Year No of Projects Total Capacity

(TPH)

2007 9 325

2008 10 385

2009 9 370

2010 11 440

2011 12 502

* excluding retrofitting of special purpose vehicles and boilers

Financial Year No of New

Contracts Secured

Total Value

(RMm)

2007 10 191.0

2008 10 139.4

2009 14 173.7

2010 14 178.6

2011 18 313.2

Factory Output :

Projects Award :

Projects Orderbook

• Sizeable unbilled portion of about RM379m as at end 2QFY12 Equivalent to 1.8x FY11 turnover Expect to drive revenue and profit growth in FY12

• New contracts recently secured in 2QFY12 RM60m contract from Jaya Tiasa (RM40m for 120 tph) and PT Swakarsa Sawit

Raya (RM20m for 45 tph) RM16m boilers contract from Wilmar and Sime Darby

• Targeting to secure projects worth RM500m to sustain orderbook growth Core demand from Indonesia PNG emerging as potential new growth market

Projects in Hand Value (RMm) % Recognition Unbilled Sales

(RMm)

Palm oil mill construction

- Malaysia 248.1 30.3% 172.8

- Indonesia 389.9 69.2% 119.9

- Other countries 60.5 35.4% 39.1

Boilers 178.8 73.3% 47.7

Total 877.3 56.7% 379.5

* excluding retrofitting of special purpose vehicles

10

Plantation Division

• Disposal of Sachiew and Empresa completed in May 2012

Raised RM268.1m cash

• Consolidating plantation assets in Kalimantan, Indonesia

Acquired PT Berkala Maju Bersama and PT Jaya Jadi Utama in April 2012 Total plantation land in Kalimantan under subsidiaries raised to 37,273ha

o Total plantable area is now approximately 33,000ha Additional plantation land of 14,347 ha with proposed acquisition of PT GAS

11

Effective Interest

(%)

Landbank (ha) Estimated Planted

Areas (ha)

Subsidiaries

PT Sawit Lamandau Raya (SLR) 85% 8,000 5,000

PT Jaya Jadi Utama (JJU) 94% 13,645 13,000

PT Berkala Maju Bersama (BMB) 94% 15,628 15,000

Total 37,273 33,000

Associate & Jointly-controlled

Solar Green Sdn Bhd (50%) 50% 5,567

Kumpulan Kris Jati Sdn Bhd 30% 20,855

Bahtera Bahagia Sdn Bhd 30%

Planting Schedule for Indonesian Estates

• Target to complete planting for 5,000ha in SLR by FY13

• Currently preparing nurseries for JJU and BMB Expect to commence planting in FY13 Annual planting expected to be 5,000 – 8,000ha per annum

12

SLR JJU BMB

2011 1,300 ha - -

2012E 1,000 ha - -

2013E 2,700 ha - 4,000 ha

2014E 45MT mill - 4,000 ha

2015E - 4,000 ha 2,000 ha

& 45MT mill

2016E - 4,000 ha 3,000 ha

2017E - 3,000 ha 2,000 ha

& 45MT mill

2018E - 2,000 ha

& 45MT mill

-

Total 5,000 13,000 15,000

Outlook and Prospects

• Targeting consistent profit growth of 20% p.a. Unbilled orderbook of Modipalm mills of RM379m as at 30 June 2012 Steady contribution from plantation associates and JVs

• Equipment & Contracting Division Securing new projects to further grow orderbook in Modipalm mills

o Proven benefits of Modipalm mills and its continuous sterilization process o Core demand in Indonesia, with PNG offering new prospects

Growing recurring revenue from replacement and upgrading works o Accounts for 10% of Modipalm revenue currently o Pursuing new market segment in older and under-performing mills

• Plantation Division Positive impact in the longer term with new cultivation in Kalimantan,

Indonesia o Plantation hecterage rose from 8,000ha to 37,273ha with recent land

acquisitions o Potential additional land bank of 14,347ha via proposed acquisition of PT

GAS in August 12

13

Top Related