Languages

Pages

Legal

Union Budget 2017

Highlights

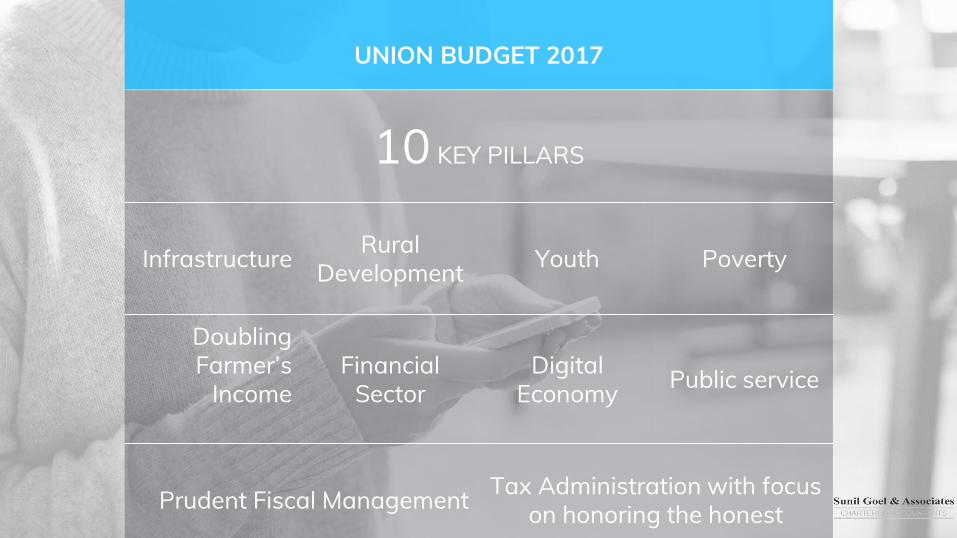

UNION BUDGET 2017

10 KEY PILLARS

Infrastructure Rural Development Youth Poverty

DoublingFarmer’s

IncomeFinancial

Sector Digital

Economy Public service

Prudent Fiscal Management Tax Administration with focus on honoring the honest

➜A new metro rail policy to be announced to enable easier financing and implementation.➜Focus on passenger safety, cleanliness and overhauling accounting practices.

➜Service Tax on E-tickets booked through IRCTC to be withdrawn

Union Budget 2017

Union Budget 2017Railways•Raksha coach with a corpus of Rs. 1 lakh cr for fiveyears (for passenger safety)•Unmanned level crossings to be eliminated by 2020•3,500 km of railway lines to be commissioned thisyear up•Coach mitra facility - to register all coach relatedcomplaints•2019 - bio toilets for all trains•500 stations to be made differently-abled friendly•Railways to partner with logistics players for frontend and back end solutions for selectedcommodities.•Shares of Railway PSE like IRCTC would be listed on

stock exchanges.

Foreign Investment Promotion Board to

be Abolished

Union Budget 2017

Union Budget 2017Financial Sector•Bill on resolution of financial firms to be introduced in

this session of parliament.

•Revised mechanism to ensure time bound listing of

CPSEs

•Computer emergency response team for financial

sector to be formed.

•Pradhan Mantri Mudra Yojana lending target at Rs

2.44 lakh crore for 2017-18

•Negotiable Instruments Act might be amended.

•For big-time offences - including economic offenders

fleeing India, the govt. will introduce a legislative

change or new law to confiscate the assets of these

people within the country

Rebate of Rs 12,500

Available to those in personal income tax slabs over Rs 5 lakh per annum

Union Budget 2017

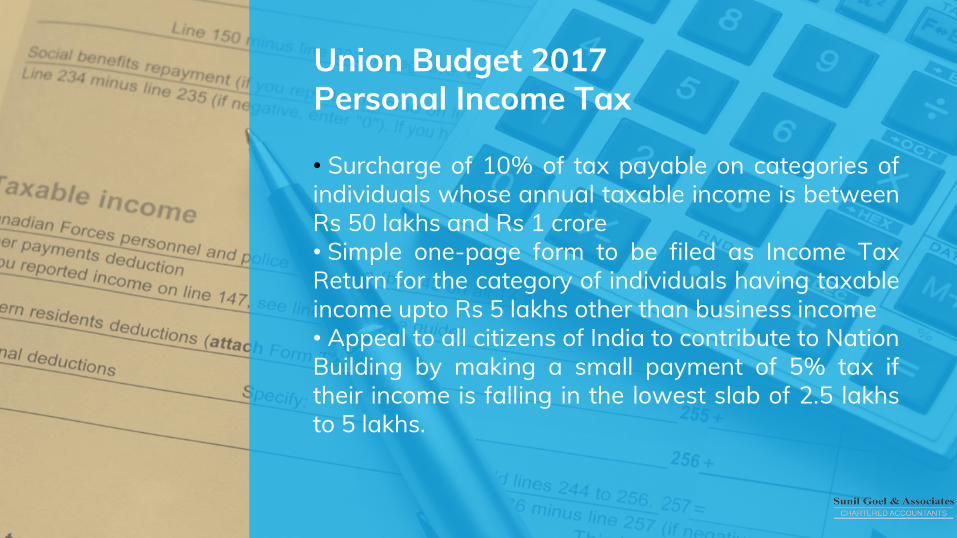

Union Budget 2017Personal Income Tax

• Surcharge of 10% of tax payable on categories ofindividuals whose annual taxable income is betweenRs 50 lakhs and Rs 1 crore• Simple one-page form to be filed as Income TaxReturn for the category of individuals having taxableincome upto Rs 5 lakhs other than business income• Appeal to all citizens of India to contribute to NationBuilding by making a small payment of 5% tax iftheir income is falling in the lowest slab of 2.5 lakhsto 5 lakhs.

INCOME TAX RATE FOR THOSE IN RS 2.5 LAKH-RS 5

LAKH CUT FROM 10 PERCENT TO 5 PERCENT

Union Budget 2017

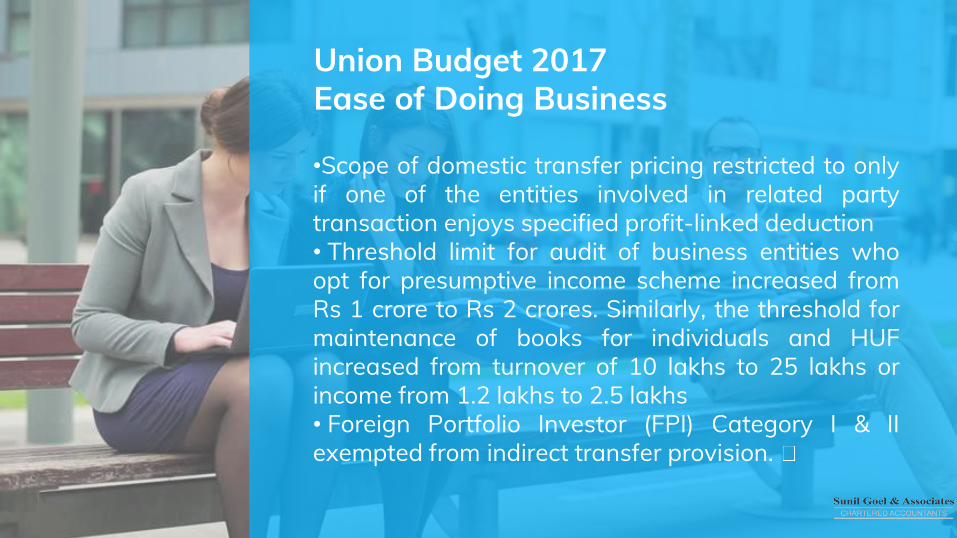

Union Budget 2017Ease of Doing Business

•Scope of domestic transfer pricing restricted to onlyif one of the entities involved in related partytransaction enjoys specified profit-linked deduction• Threshold limit for audit of business entities whoopt for presumptive income scheme increased fromRs 1 crore to Rs 2 crores. Similarly, the threshold formaintenance of books for individuals and HUFincreased from turnover of 10 lakhs to 25 lakhs orincome from 1.2 lakhs to 2.5 lakhs• Foreign Portfolio Investor (FPI) Category I & IIexempted from indirect transfer provision.

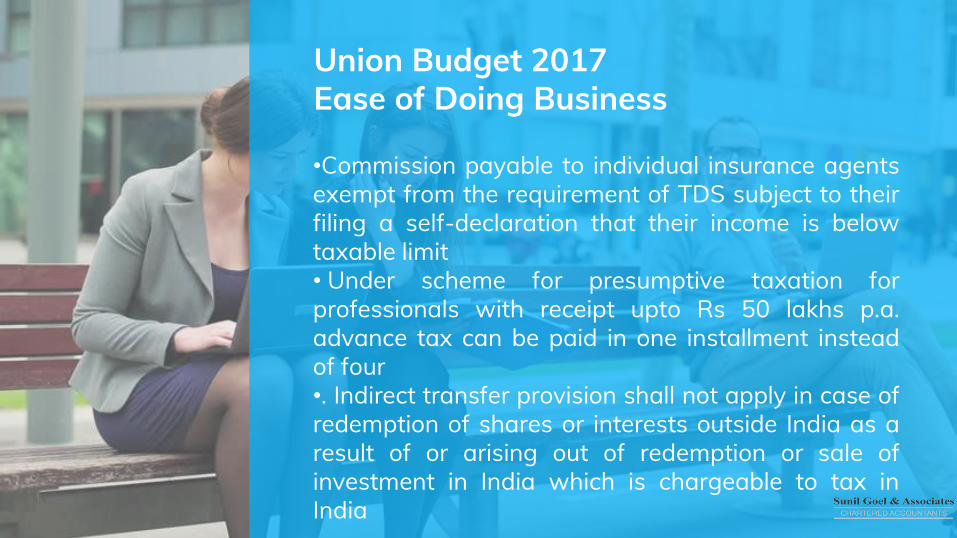

Union Budget 2017Ease of Doing Business

•Commission payable to individual insurance agentsexempt from the requirement of TDS subject to theirfiling a self-declaration that their income is belowtaxable limit• Under scheme for presumptive taxation forprofessionals with receipt upto Rs 50 lakhs p.a.advance tax can be paid in one installment insteadof four•. Indirect transfer provision shall not apply in case ofredemption of shares or interests outside India as aresult of or arising out of redemption or sale ofinvestment in India which is chargeable to tax inIndia

Reduction in Corporate Tax rate for MSMEs having

revenues less than 50 crores to 25%

Union Budget 2017Measures for stimulating growth•Concessional withholding rate of 5% charged oninterest earned by foreign entities in externalcommercial borrowings or in bonds and Governmentsecurities is extended to 30.6.2020. This benefit isalso extended to Rupee Denominated (Masala)Bonds•For the purpose of carry forward of losses in respectof start-ups, the condition of continuous holding of51% of voting rights has been relaxed subject to thecondition that the holding of the originalpromoter/promoters continues. Also the profit (linkeddeduction) exemption available to the start-upschanged to 3 years out of 7 years

Union Budget 2017Measures for stimulating growth

• MAT credit is allowed to be carried forward up to aperiod of 15 years instead of 10 years• Allowable provision for Non-Performing Asset ofBanks increased from 7.5% to 8.5%. Interest taxableon actual receipt instead of accrual basis in respectof NPA accounts of all non-scheduled cooperativebanks also to be treated at par with scheduled banks•Basic customs duty on LNG reduced from 5% to2.5%

Time period for revising a tax return is being reduced to 12 months from completion of financial year, at par with the time period for filing of return.

Also the time for completion of scrutiny assessments is being compressed further from 21 months to 18 months for Assessment Year 2018-19 and

further to 12 months for Assessment Year 2019-20 and thereafter.

UNION BUDGET 2017

Holding period for Long-term capital

gains tax on immovable property from three years to two

years

Union Budget 2017

Union Budget 2017Housing Sector

• Exemption from capital gain tax for persons holdingland on 2.6.2014, the date on which the State ofAndhra Pradesh was reorganized, and whose land isbeing pooled for creation of capital city of AndhraPradesh under the Government scheme•For Joint Development Agreement signed fordevelopment of property, the liability to pay capitalgain tax will arise in the year the project is completed•For builders for whom constructed buildings arestock-in-trade, tax on notional rental income will onlyapply after one year of the end of the year in whichcompletion certificate is received

Union Budget 2017

Promoting Digital Economy

Under scheme of presumptiveincome for small and medium taxpayers whose turnover is up to 2crores, the present, 8% of theirturnover which is counted aspresumptive income is reduced to6% in respect of turnover which isby non-cash meansNo transaction above Rs 3 lakhwould be permitted in cash subjectto certain exceptions

UNION BUDGET 2017GST

Preparation of IT System on Schedule

Extensive reach out efforts to start

from 1st April 2017

Recommendations Finalised based on

9 meetings held

Thanks!Any questions?Write to us

Disclaimer: Information presented in this document is considered private & proprietary information (unless otherwise noted)

and may not be distributed or copied. We strongly recommend that you seek professional guidance and opinion before acting

in any way on the proposals. While SGA makes every effort to provide accurate and complete information, various proposals

may change subsequently. SGA welcomes suggestions on how to improve our services and correct errors if any. SGA

provides no warranty, expressed or implied, as to the accuracy, reliability or completeness of furnished information

Top Related