Languages

Pages

Legal

1

2

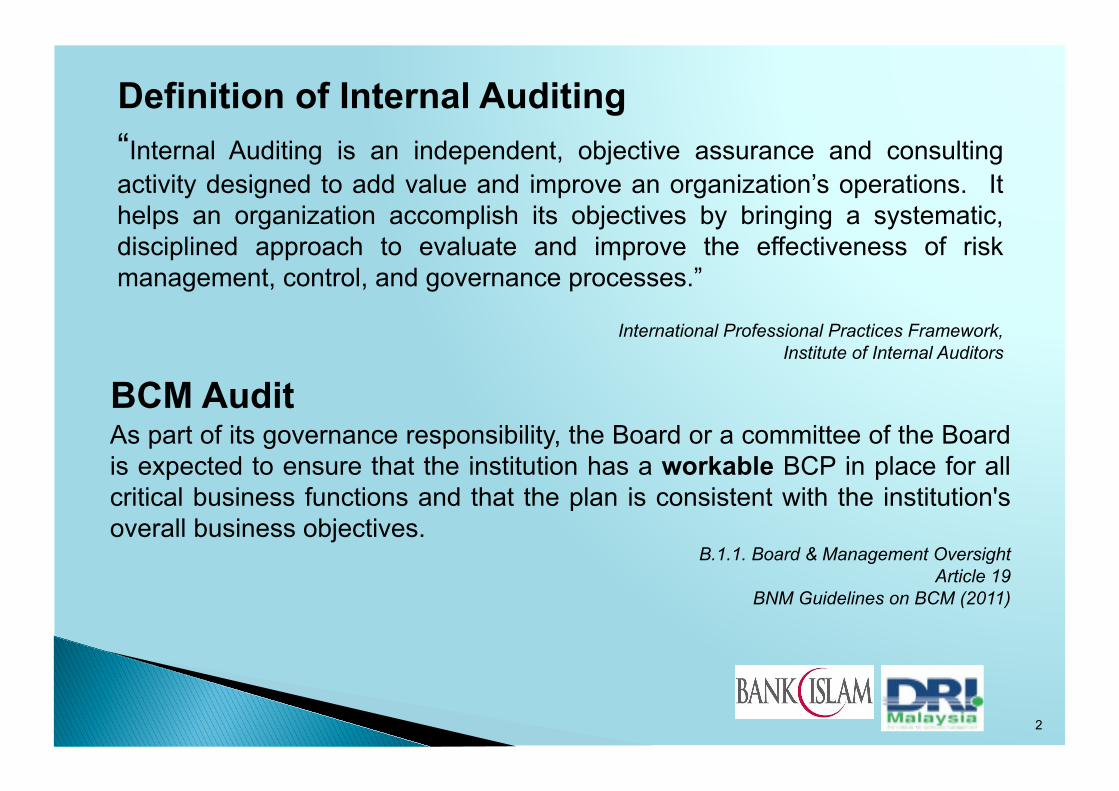

“Internal Auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization’s operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.”

International Professional Practices Framework, Institute of Internal Auditors

Definition of Internal Auditing

As part of its governance responsibility, the Board or a committee of the Board is expected to ensure that the institution has a workable BCP in place for all critical business functions and that the plan is consistent with the institution's overall business objectives.

B.1.1. Board & Management Oversight Article 19

BNM Guidelines on BCM (2011)

BCM Audit

3

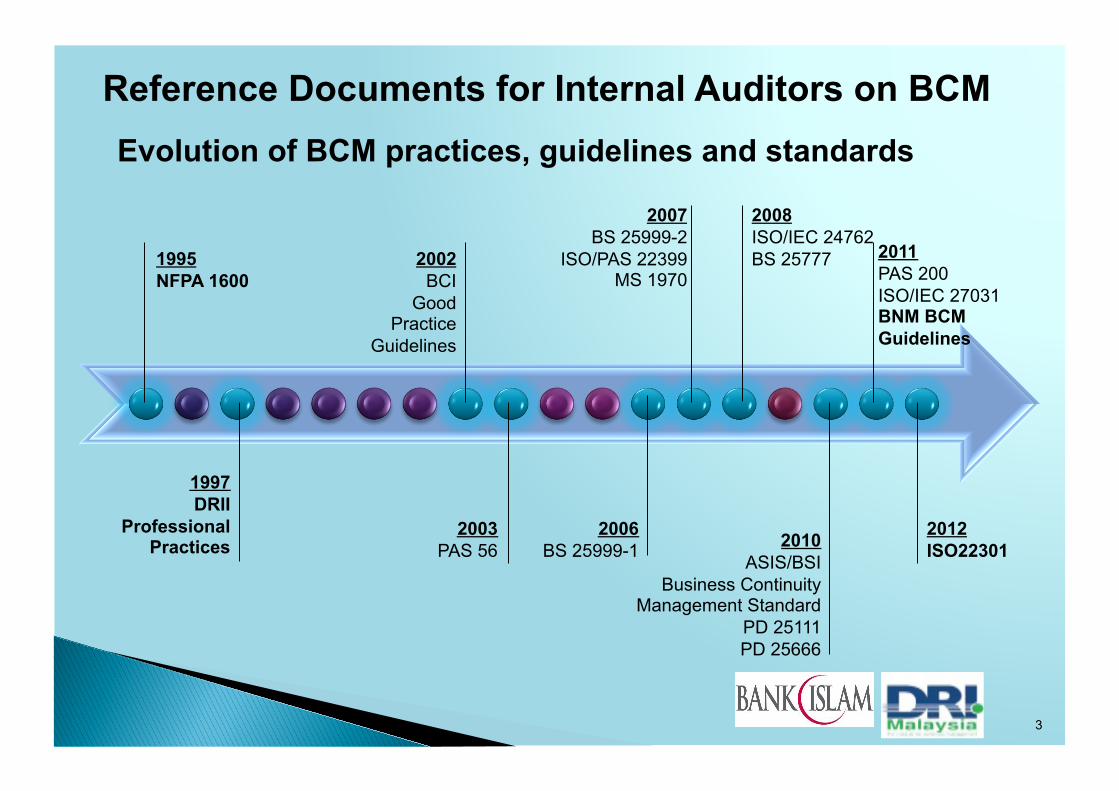

Evolution of BCM practices, guidelines and standards

Reference Documents for Internal Auditors on BCM

1995 NFPA 1600

1997 DRII

Professional Practices

2003 PAS 56

2002 BCI

Good Practice

Guidelines

2008 ISO/IEC 24762 BS 25777

2006 BS 25999-1 2010

ASIS/BSI Business Continuity

Management Standard PD 25111 PD 25666

2012 ISO22301

2007 BS 25999-2

ISO/PAS 22399 MS 1970

2011 PAS 200 ISO/IEC 27031 BNM BCM Guidelines

4

DRI International Professional Practices (PP)

Program Initiation & Management

Risk Evaluation & Control

Business Impact Analysis

Develop BC Strategies

Emergency Preparedness &

Response

Develop & Implement BC Plans

Crisis Communications & External Agencies

Awareness & Training

Test & Exercise

Audit & Maintenance

The Plan

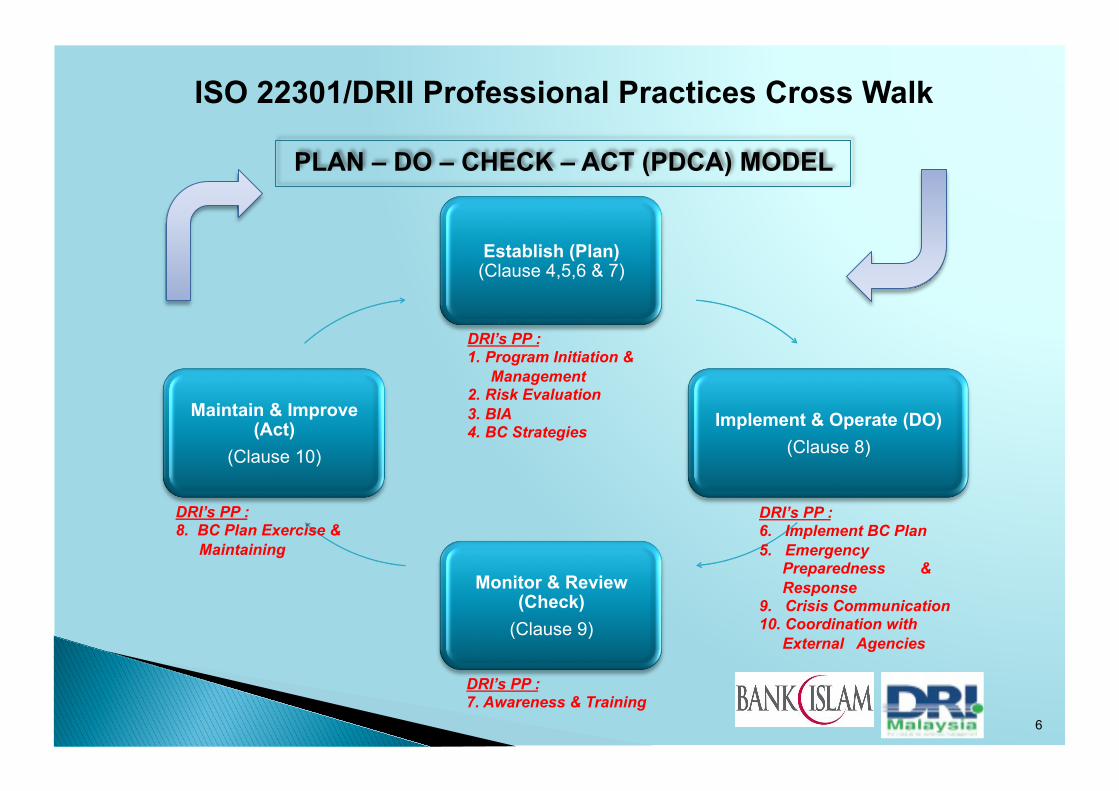

5

Establish (Plan) (Clause 4,5,6 & 7)

Implement & Operate (DO) (Clause 8)

Monitor & Review (Check)

(Clause 9)

Maintain & Improve (Act)

(Clause 10)

6

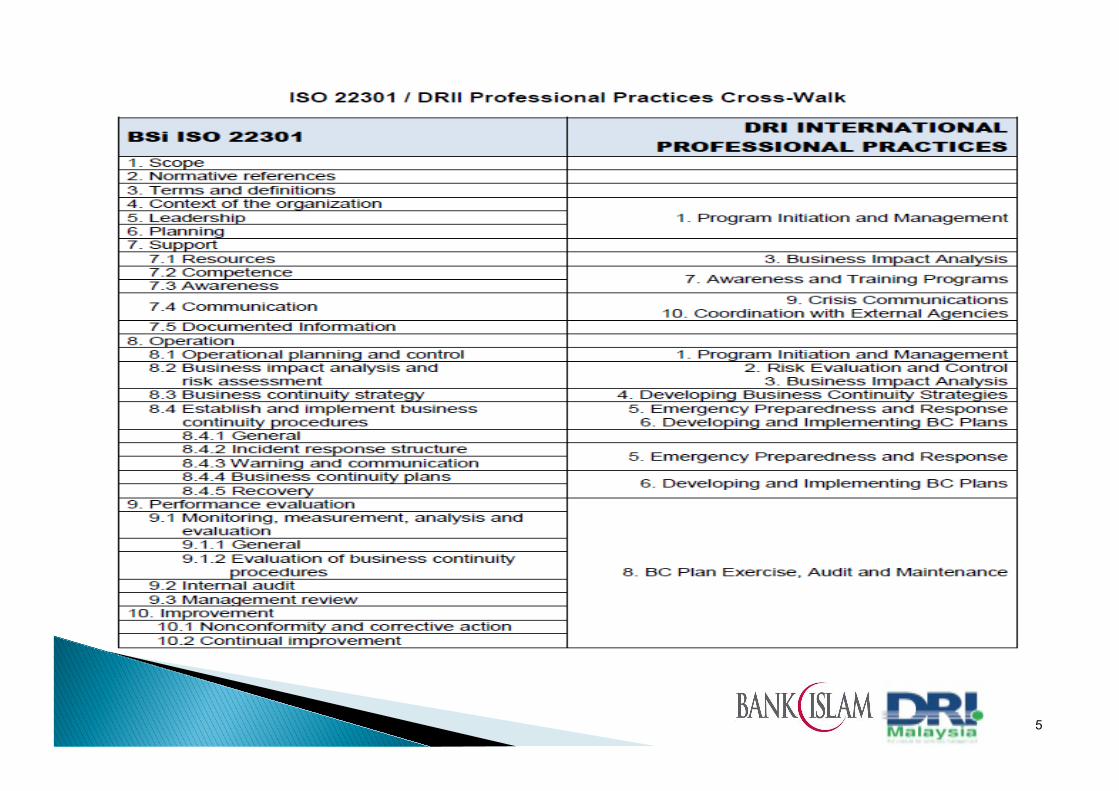

ISO 22301/DRII Professional Practices Cross Walk

DRI’s PP : 1. Program Initiation &

Management 2. Risk Evaluation 3. BIA 4. BC Strategies

DRI’s PP : 6. Implement BC Plan 5. Emergency

Preparedness & Response

9. Crisis Communication 10. Coordination with

External Agencies

DRI’s PP : 7. Awareness & Training

DRI’s PP : 8. BC Plan Exercise &

Maintaining

PLAN – DO – CHECK – ACT (PDCA) MODEL

7

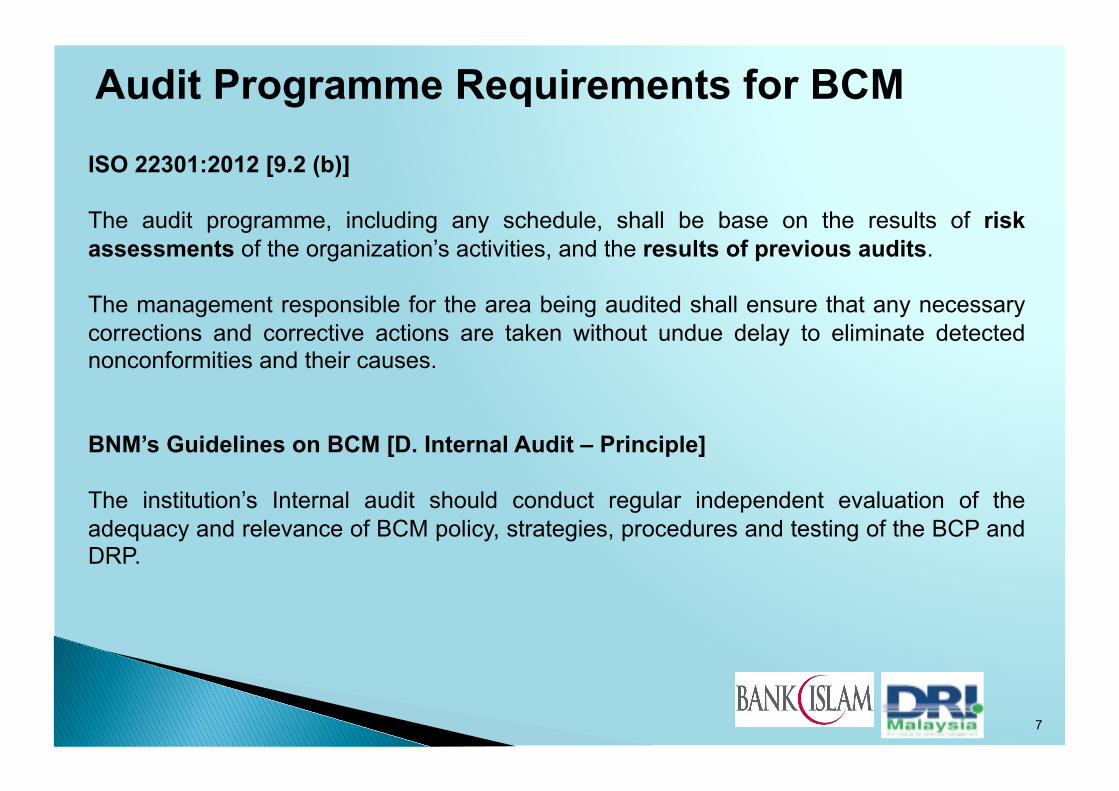

Audit Programme Requirements for BCM

ISO 22301:2012 [9.2 (b)]

The audit programme, including any schedule, shall be base on the results of risk assessments of the organization’s activities, and the results of previous audits.

The management responsible for the area being audited shall ensure that any necessary corrections and corrective actions are taken without undue delay to eliminate detected nonconformities and their causes.

BNM’s Guidelines on BCM [D. Internal Audit – Principle]

The institution’s Internal audit should conduct regular independent evaluation of the adequacy and relevance of BCM policy, strategies, procedures and testing of the BCP and DRP.

8

Emerging Risks More Frequent and Devastating

Natural Disasters

• Flood, Earthquake, Hurricane, Tsunami

Political Disaster

• Protest in the Gulf region, Thai red shirts…

Technological Disaster

• Computer Viruses, Cyber Attack, Cable Damage …

Manmade Disaster

• Oil spill, Dam release, Pollution

Pandemic

• H1N1, SARs

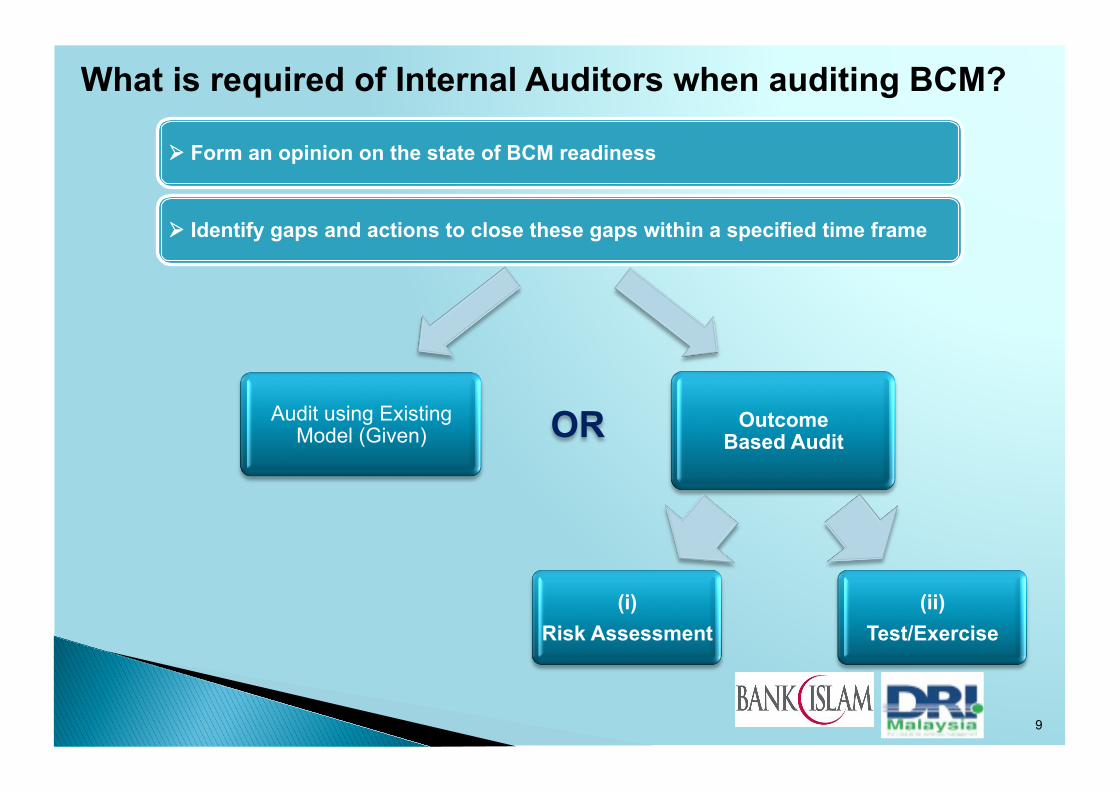

OR Audit using Existing Model (Given)

Outcome Based Audit

(i) Risk Assessment

(ii) Test/Exercise

9

What is required of Internal Auditors when auditing BCM?

Form an opinion on the state of BCM readiness

Identify gaps and actions to close these gaps within a specified time frame

10

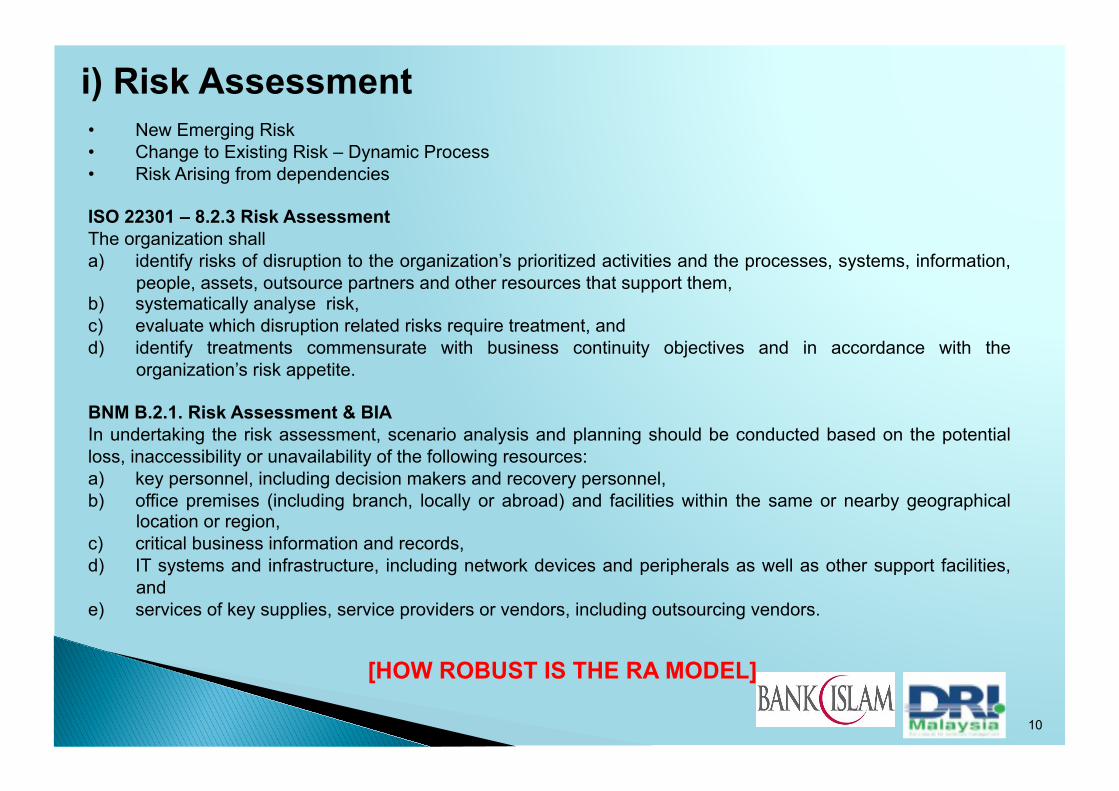

i) Risk Assessment • New Emerging Risk • Change to Existing Risk – Dynamic Process • Risk Arising from dependencies

ISO 22301 – 8.2.3 Risk Assessment The organization shall a) identify risks of disruption to the organization’s prioritized activities and the processes, systems, information,

people, assets, outsource partners and other resources that support them, b) systematically analyse risk, c) evaluate which disruption related risks require treatment, and d) identify treatments commensurate with business continuity objectives and in accordance with the

organization’s risk appetite.

BNM B.2.1. Risk Assessment & BIA In undertaking the risk assessment, scenario analysis and planning should be conducted based on the potential loss, inaccessibility or unavailability of the following resources: a) key personnel, including decision makers and recovery personnel, b) office premises (including branch, locally or abroad) and facilities within the same or nearby geographical

location or region, c) critical business information and records, d) IT systems and infrastructure, including network devices and peripherals as well as other support facilities,

and e) services of key supplies, service providers or vendors, including outsourcing vendors.

[HOW ROBUST IS THE RA MODEL]

11

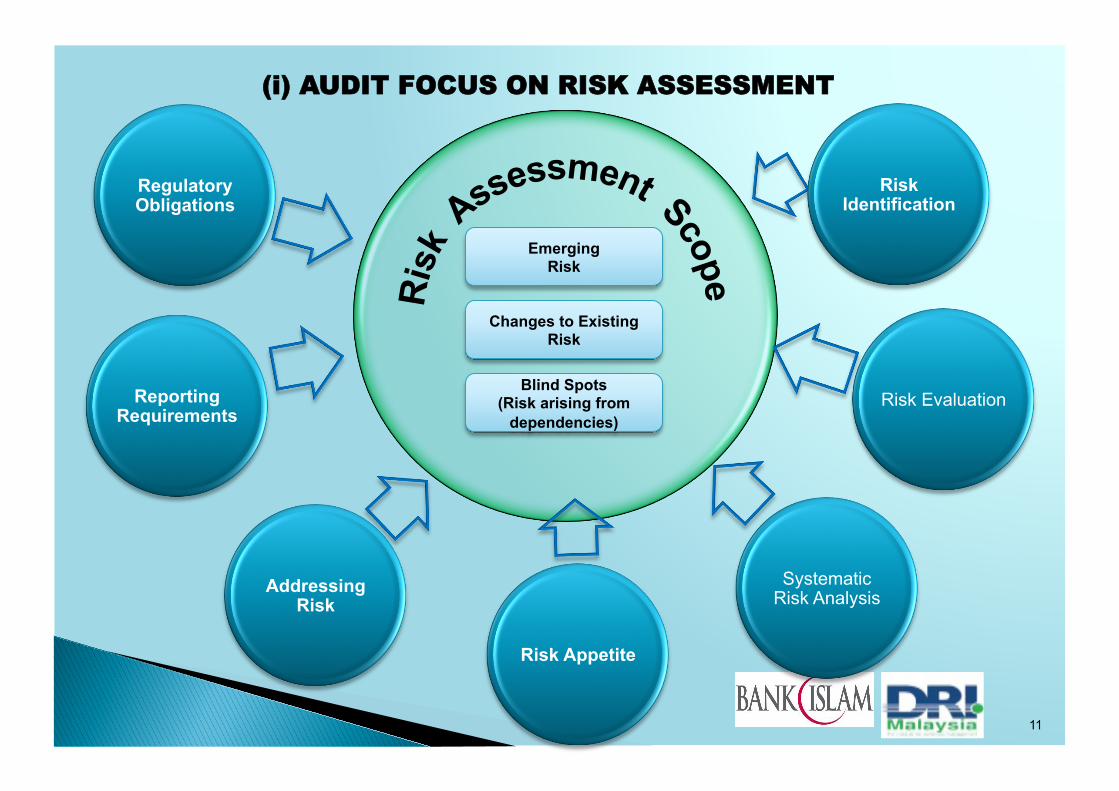

(i) AUDIT FOCUS ON RISK ASSESSMENT

Regulatory Obligations

Reporting Requirements

Addressing Risk

Risk Appetite

Systematic Risk Analysis

Risk Evaluation

Risk Identification

Emerging Risk

Changes to Existing Risk

Blind Spots (Risk arising from

dependencies)

12

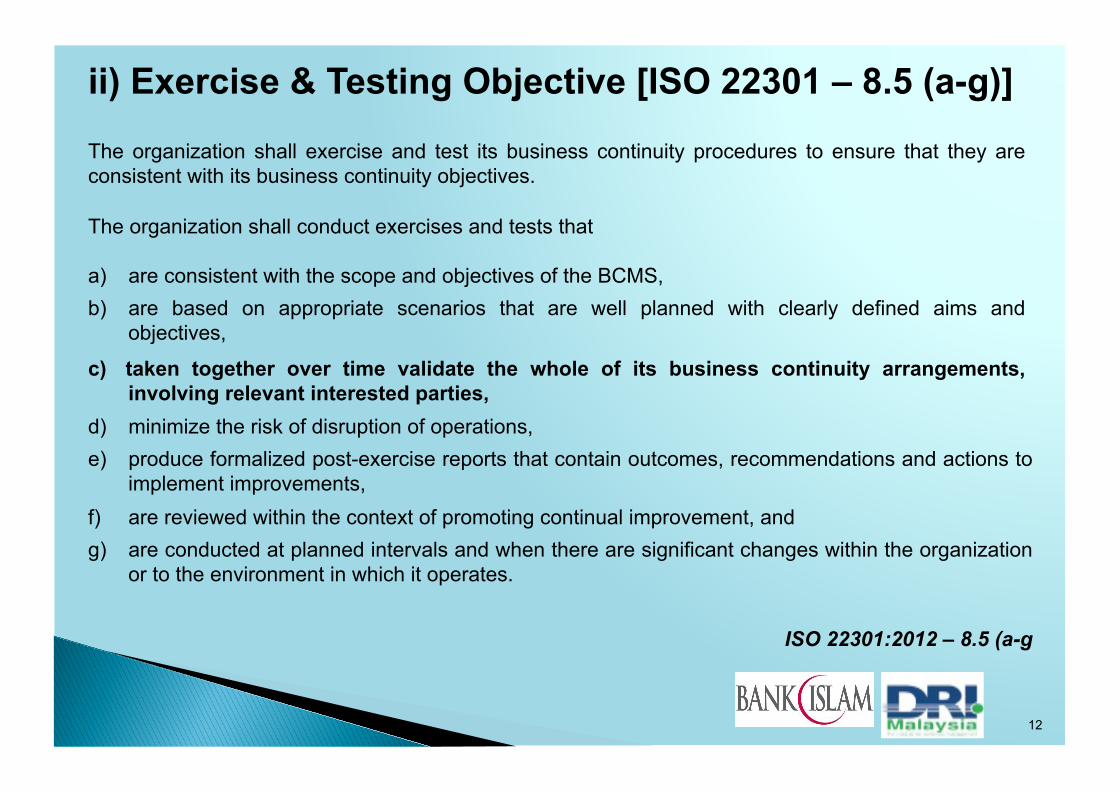

ii) Exercise & Testing Objective [ISO 22301 – 8.5 (a-g)]

The organization shall exercise and test its business continuity procedures to ensure that they are consistent with its business continuity objectives.

The organization shall conduct exercises and tests that

a) are consistent with the scope and objectives of the BCMS, b) are based on appropriate scenarios that are well planned with clearly defined aims and

objectives,

d) minimize the risk of disruption of operations, e) produce formalized post-exercise reports that contain outcomes, recommendations and actions to

implement improvements, f) are reviewed within the context of promoting continual improvement, and g) are conducted at planned intervals and when there are significant changes within the organization

or to the environment in which it operates.

ISO 22301:2012 – 8.5 (a-g

c) taken together over time validate the whole of its business continuity arrangements, involving relevant interested parties,

13

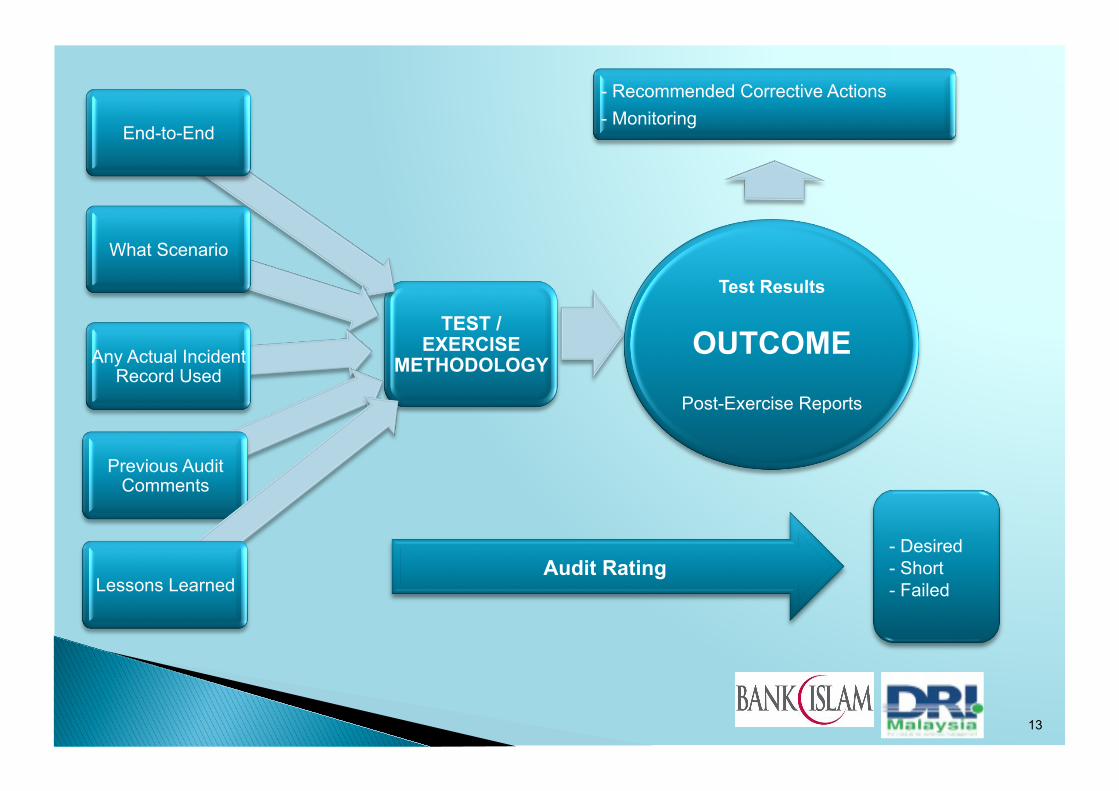

TEST / EXERCISE

METHODOLOGY

End-to-End

What Scenario

Any Actual Incident Record Used

Previous Audit Comments

Lessons Learned

Test Results

OUTCOME

Post-Exercise Reports

- Recommended Corrective Actions - Monitoring

- Desired - Short - Failed

Audit Rating

14

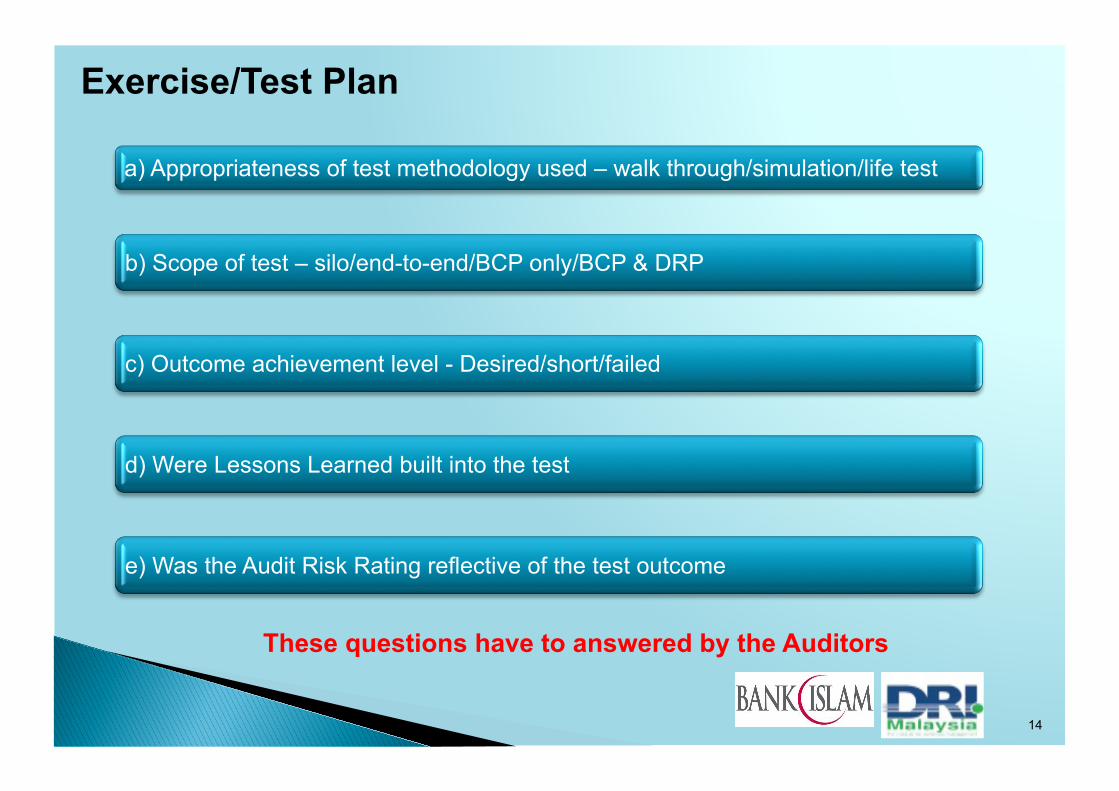

Exercise/Test Plan

a) Appropriateness of test methodology used – walk through/simulation/life test

b) Scope of test – silo/end-to-end/BCP only/BCP & DRP

c) Outcome achievement level - Desired/short/failed

d) Were Lessons Learned built into the test

e) Was the Audit Risk Rating reflective of the test outcome

These questions have to answered by the Auditors

15

Conclusion

Auditing BCM is fairly straight forward, but stating an opinion on the state of BCM readiness and whether the organization has a workable BCP/DRP in place is the challenge.

Evaluating Risk Assessment and Testing Process via the OUTCOME approach within the overall audit of the BCM System is where Auditors can make a difference.

16

Top Related