Languages

Pages

Legal

AN

NU

AL R

EPO

RT 2

01

8

Hong Leong Bank Berhad (97141-X)

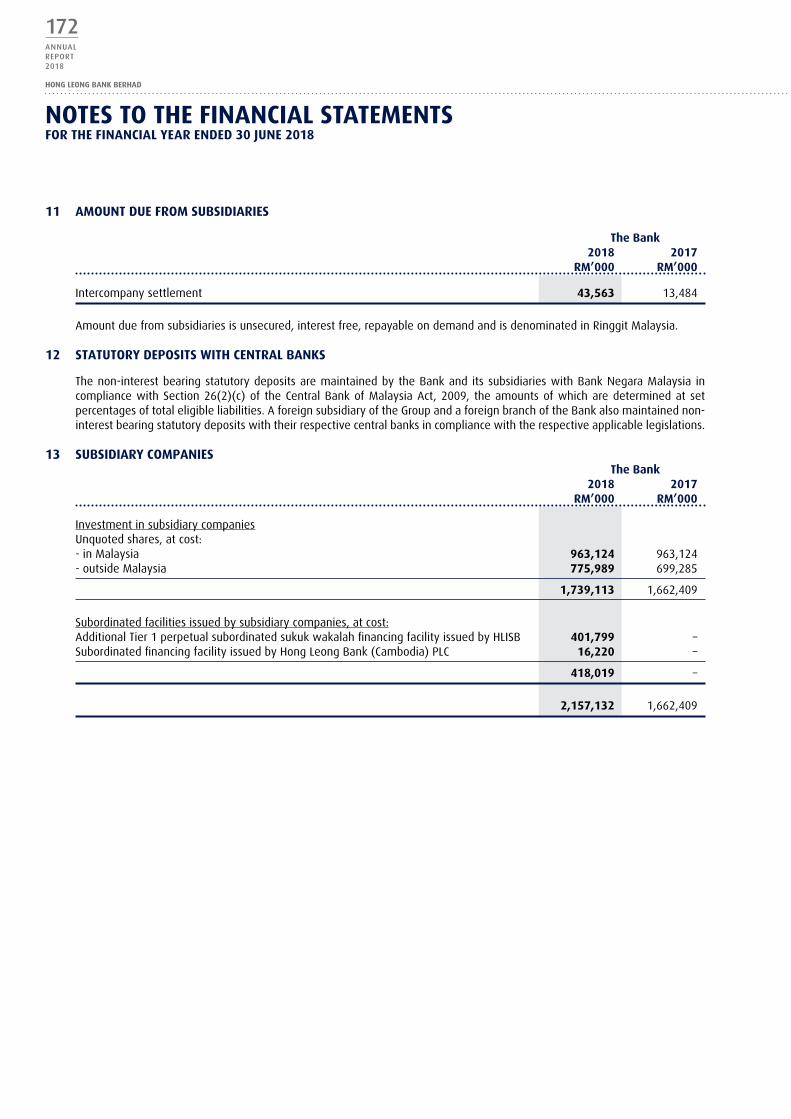

Level 19, Menara Hong Leong6, Jalan Damanlela, Bukit Damansara50490 Kuala LumpurTel : 03-2081 8888Fax : 03-2081 7801

w w w. h l b . c o m . m y

As part of Hong Leong Bank’s support for environmental sustainability, this Annual Report is printed on Forest Stewardship Council (FSC) certified paper and recycled paper.

Bank Berhad

Bank Berhad

ANNUAL REPORT 2018

corporate02 Vision

04 TheBusiness

06 Awards&Accolades

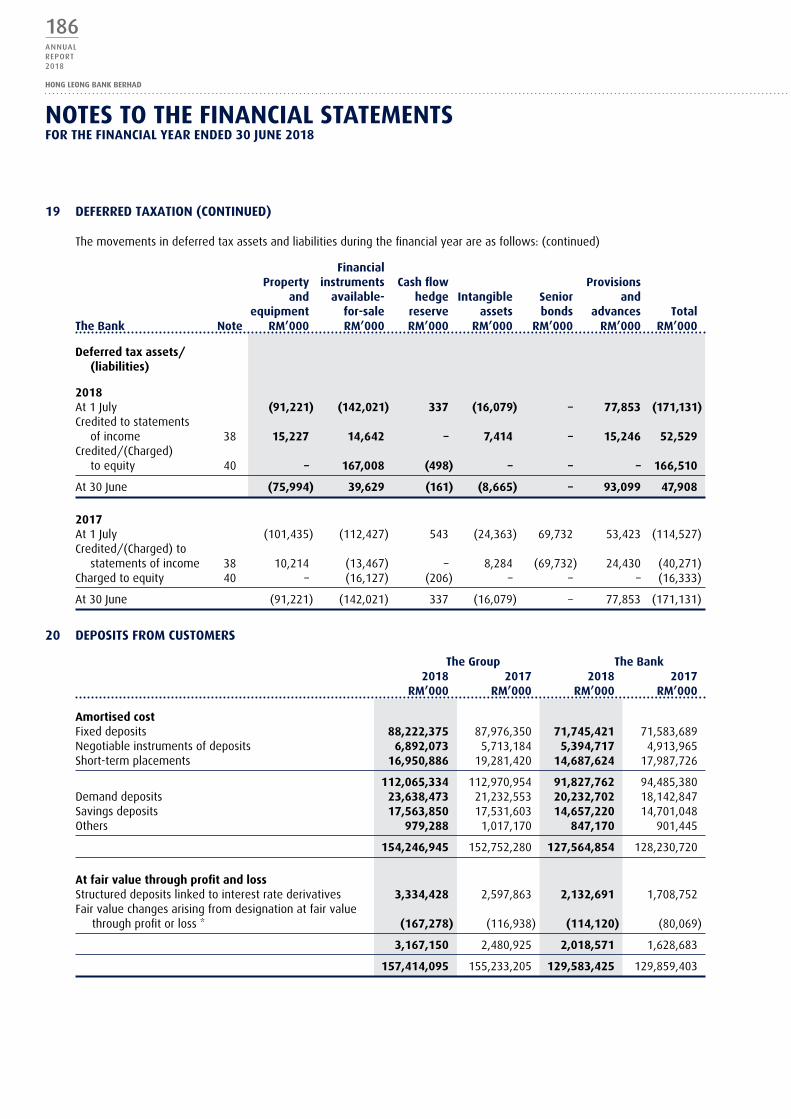

08 HongLeongBankStory

10 CorporateMilestones

12 Chairman’sStatement

18 FiveYearGroupFinancialHighlights

20 GroupManagingDirector/ChiefExecutiveOfficer’sReview

30 ManagementDiscussion&Analysis

67 SustainabilityStatement

83 CorporateInformation

84 NoticeofAnnualGeneralMeeting

87 StatementAccompanyingNoticeofAnnualGeneralMeeting

88 BoardofDirectors’Profile

92 KeySeniorManagement

96 BoardAuditCommitteeReport

99 BoardRiskManagementCommittee(BRMC)Report

102 CorporateGovernanceOverview,RiskManagement&InternalControlStatement

ScantheQRCodebyfollowingthesesimplesteps:

Get itDownloadthe“QRCodeReader”appfromGooglePlay(AndroidMarket),BlackBerryAppWorld,AppStore(iOS/iPhone)orWindowsPhoneStore

run itRuntheQRCodeReaderappandpointyourcameraattheQRCode

access itGetaccesstoHongLeongBankBerhad’swebsite

Scan the Qr code to visit our website.

FINaNcIaLS118 Directors’Report

128 StatementsofFinancialPosition

129 StatementsofIncome

130 StatementsofComprehensiveIncome

131 StatementsofChangesinEquity

135 StatementsofCashFlows

139 NotestotheFinancialStatements

275 StatementbyDirectors

275 StatutoryDeclaration

276 IndependentAuditors’Report

281 BaselIIPillar3Disclosures

aDDItIoNaL INForMatIoN

327 OtherInformation

338 Local&OverseasBranches

•FormofProxy

WHAT’S INSIDe

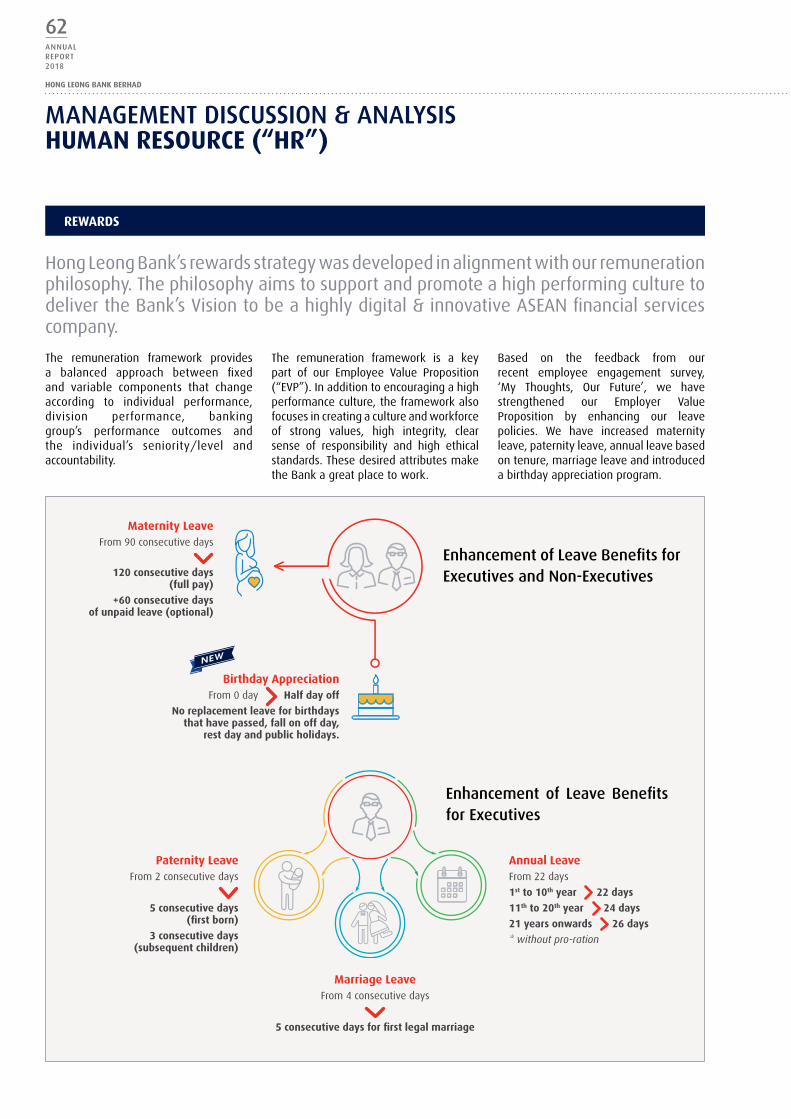

Highly digital and innovative aSeaN financial services company

VISION

THebuSINeSS

Digital and innovation is part of the Hong Leong bank culture, in line with our vision to be a highly digital and innovative financial service provider guided by its ethos of being digital-at-the-core, centred around customer experiences and the growing demand and expectation for digital based services, products and solutions.

HongLeongBank(“HLB”)standsproudlyasaleadingfinancial-servicesinstitutionbasedinMalaysia,providingregionalservicesof a wide range of comprehensive and innovative financialsolutions.Theseservicesaredeliveredthroughbothdigitalandtraditionalmeans,viaonlineandmobilebanking,aswellasitsdigital branch concept designed to provide customerswith anefficientandseamlessexperienceaidedbytechnology.

HLB’s extensive branch network extends beyond Malaysianborders with one branch each in Singapore and Hong Kongrespectively, four branches in Vietnam, five branches inCambodia,andarepresentativeofficeinNanjing,China,aswellas a full-service call centre and more than 1,100 self-serviceterminals. Wealth Management services are offered throughbranchesinMalaysia,SingaporeandHongKong,inadditiontovariousPriorityBankingcentreslocatedthroughoutMalaysiaandoneinSingapore.

Astheserviceandfinanciallandscapechangesrapidlywiththeever-increasinguseoftechnology,stayingattunedtocustomers’

needs and desires becomes even more critical to HLB’soperations.Tostayaheadofthesedynamicchanges,theBankhasadoptedtheapproachofreimaginingbankingbyembeddingdigitalconsiderationsandcustomercentricityineveryaspectofouroperations,fromproductsandservicesaswellascustomercareandengagement.

HLB’s ethos of being Digital-At-The-Core that is powered bycustomers-at-the-forefront has led and will continue to leadus to innovateofferings in linewithour aspirationofbeingahighly digital and innovative financial services organization.The Bank constantly looks at ways to leverage on technologyto increase efficiency and productivity towards improving theoverall customer experience, as well as to upskill employees’competencies and skill sets in this ever-changing financialindustry landscape, so that we have a “fit for the future”workforce.

ThedigitalambitionofHLBistoenablethecustomerstolivelifeuninterrupted,abletoperformtheirbankingandfinancialneeds–simpler,better,intuitivelyandtailoredtotheirpreferences.

HoNG LeoNG baNK’S KeY buSINeSS pILLarS are:

personal Financial Services

business and corporate banking

Global Markets Islamic Financial Services

Providingfinancialproducts,wealthmanagement,andprioritybankingservicestoindividualsincludingproperty,autoandpersonalloans,paymentproducts,sharefinancing,investmentandinsurance,aswellasdepositandremittanceservices.

Principalbusinessactivitiesincludetheprovisionofbankingsolutionssuchasdepositandloanservicescoveringbusinesscurrentaccount,interest-bearingauto-sweepaswellasfixeddeposit,andfinancingoptionsrangingfromassetacquisition,workingcapital,anddebtcapitalmarketstructures,forourcorporate,commercialandSMEclientbase.HLBalsospecializesintheprovisionoftransactionbankingsolutionsviacashmanagement,tradefinancingandservices.

Principalactivitiesincludeassistingcustomerstomeettheirinvestmentandhedgingneedsthroughvarioustreasuryproducts,rangingfromforeignexchange,moneymarket,derivativesincludinginterestrateswapsandinterestrateswapoptions,tostructuredinvestmentproducts.

IslamicFinancialServicesareofferedbyHongLeongIslamicBank,awholly-ownedsubsidiaryofHLBwhichisfocusedonprovidingShariah-compliantPersonalFinancialServices,BusinessandCorporateBanking,andGlobalMarketsproductsandservices.

04ANNUALRePORT2018

HoNG LeoNG baNK berHaD

THebuSINeSS

reGIoNaL FootprINt

Inlinewithourgrowthstrategy,HLBhasbeenexpandingitsfootprintintheAsianregion.

Singapore operations

HLBank,Singaporeisafullbankinglicensebranch offering wealth management,treasury services, deposit products andauto loan services. We have embarkedon a transformational journey towardsanintegratedbusinessmodel,expandinginto health banking, corporate bankingfor commercial clients and expandedconsumerlendingpropositions.

Hong Kong operations

The Bank’s branch in Hong Kong offersTreasury and Wealth Managementproducts and services. It is also thefirst

bank inHongKong to launchan Islamicbankingwindow.

Vietnam operations

Hong Leong Bank Vietnam Limited(“HLBVN”), a subsidiary of the Bank,commencedoperations inOctober2009.HLBVNisafull-fledgedcommercialbankin Vietnam whose principal activitiesinclude provision of retail loans, depositproducts, wealth management, andpriority banking services to individuals.Whereas business banking solutionsinclude working capital and term loans,deposit and liability managementproducts and trade finance services aswell as foreign exchange (“forex”) andmoney market services. To date HLBVNhas a branch and transaction officelocatedinHoChiMinhCity,andabrancheachinBinDuongandHanoi.

cambodia operations

InJuly2013,HongLeongBank(Cambodia)PLC (“HLBCAM”) commenced operationsas a 100% wholly owned subsidiaryproviding comprehensive financialservices covering consumer banking,business banking, global markets andtransaction banking services. With fivefull-fledged branches located in PhnomPenh,HLBCAM’sprimarycustomerfocusistowardsestablishedSMEandCommercialcorporate customers, high net worthindividuals, affluent and emergingaffluent as well as tech savvy youngprofessionals.

Investment in china

HLBwasthefirstMalaysianbanktoentertheChinesebankingsectorin2008withastrategicinvestmentinBankofChengduCo., Ltd (“Bank of Chengdu”) and hasan 18% stake in the company. Bank ofChengdu is a leading city commercialbank in Western and Central ChinabasedinChengdu,thecapitalofSichuanProvince.InMarch2010,thejointventurecompanybetweenHLBand theBankofChengduobtainedregulatoryapprovaltoestablishaconsumerfinancebusinessinChengdu. InNovember2013,HLBhadsetuparepresentativeofficeinNanjingwhichcommencedoperationsinFebruarythefollowingyear.

“Tostayaheadofthesedynamicchanges,theBankhasadoptedtheapproachofreimaginingbankingbyembeddingdigitalconsiderationsandcustomercentricityineveryaspectofour

operations,fromproductsandservicesaswellascustomercareandengagement.”

corporate

05ANNUALRePORT

2018

AWARdS &accoLaDeS

1. MaLaYSIa’S beSt baNK aWarDS For eXceLLeNce 2017 EuroMoney

2. beSt baNK IN MaLaYSIa caSH MaNaGeMeNt cuStoMer SatISFactIoN aWarD, 2017 AsiaMoney

3. beSt INNoVatIoN IN retaIL baNKING MaLaYSIa, 2017TheInternationalBanker

4. HIGHeSt returNS to SHareHoLDerS oVer 3 YearS – GoLD aWarD, 2017TheEdge–BillionRinggitClub

5. HIGHeSt returN oN eQuItY oVer 3 YearS – SILVer aWarD, 2017TheEdge–BillionRinggitClub

6. MoSt INNoVatIVe tecHNoLoGY aDoptIoN – GoLD aWarD MaLaYSIaN coNtact ceNtre aWarDS 2017 ContactCentreAssociationofMalaysia

7. beSt SocIaL MeDIa oF a coNtact ceNtre – GoLD aWarD MaLaYSIaN coNtact ceNtre aWarDS 2017 ContactCentreAssociationofMalaysia

8. beSt NeW coNtact ceNtre – GoLD aWarD MaLaYSIaN coNtact ceNtre aWarDS 2017 ContactCentreAssociationofMalaysia

9. beSt INbouND coNtact ceNtre aboVe 100 SeatS – MerIt aWarD MaLaYSIaN coNtact ceNtre aWarDS 2017 ContactCentreAssociationofMalaysia

10. beSt uSe oF ceM tecHNoLoGY – GoLD aWarD, 2017InternationalQualityandProductivityCentre

2

45

10

7

3

8

9

1

6

06ANNUALRePORT2018

HoNG LeoNG baNK berHaD

AWARdS &accoLaDeS

11. aSIa’S beSt FIrSt tIMe SuStaINabILItY report FINaLIStS 2017AsiaSustainabilityReportingAwards

12. aSIa’S beSt DIGItaL WorKForce FINaNcIaL INSIGHtS INNoVatIoN aWarDS 2018 IDCFinancialInsights

13. FINtecH perSoNaLItY oF tHe Year, 2018 MalaysiaFintechAwards

14. outStaNDING coNtrIbutIoN to MYDebIt MaLaYSIaN e-paYMeNtS eXceLLeNce aWarDS 2018 PayNet

15. beSt GraDuate recruItMeNt proGraMMe – broNze aWarD recruItMeNt aWarDS 2018 HumanResourceAsia

16. tHe beSt caSH MaNaGeMeNt proJect IN MaLaYSIa baNKer’S cHoIce aWarDS 2018 TheAsianBanker

17. tHe beSt FINaNcIaL SuppLY cHaIN MaNaGeMeNt IN MaLaYSIa baNKer’S cHoIce aWarDS 2018 TheAsianBanker

18. MaLaYSIa’S beSt braND, 2018CMOAsia

19. top baNK IN tHe SecoNDarY MarKet corporate boNDS MaLaYSIa – raNK 3 aSIaN LocaL curreNcY boND beNcHMarK reVIeW 2017 TheAsset

20. top baNK IN tHe SecoNDarY MarKet GoVerNMeNt boNDS MaLaYSIa – raNK 3 aSIaN LocaL curreNcY boND beNcHMarK reVIeW 2017 TheAsset

1112

13 14

15

16

17

201918

corporate

07ANNUALRePORT

2018

HONg LeONg bANk StorY

PERSONALFINANCIALSERVICES

BuSINESS&CORPORATEBANKING

GLOBAL MARKETS

ISLAMIC BANKING

HongLeongBankBerhad(“HLB”or“theBank”) islistedonBursaMalaysiaBerhadandformspartoftheHongLeongGroup.HeadquarteredinKualaLumpur,theBankhasa strongMalaysianentrepreneurshipheritage.

HLB was originally incorporated as Kwong LeeMortgage and Remittance Company in 1905 inKuching, Sarawak and later as Kwong Lee BankLimited in 1934, bearing heritage of the oldestlocal financial institution in Malaysia. Kwong LeeBankBerhadwasacquiredbytheMuIGroupinMay1982andrenamedMalayanunitedBankBerhadon2 February1983. In1989, itwas renamedasMuI

Bank.undertheMuIBankbanner,itgrewfrom11to35branchesnationwide.On3January1994,HongLeong Group acquired MuI Bank Berhad throughHong Leong Credit Berhad (now known as HongLeongFinancialGroupBerhad)andrenameditHongLeongBankBerhad.TheBankwaslistedontheKualaLumpurStockExchange(nowunderMainMarketofBursaMalaysia)on17October1994andsincethenhasgrownbyleapsandbounds,organicallyaswellasthroughmergersandacquisitions.ItsmergerwithEONBankGroup in 2011placedHLBasMalaysia’sfifthlargestbankinggroup;withoverRM200billioninassetsasat30June2018.

08ANNUALRePORT2018

HONG LEONG BANK BERHAD

BranchesInternetBanking

CallCentreMobileBanking

SelfServiceTerminals

STRONGENTREPRENEuRIALHERITAGE

EntrepreneurshipCommunityCustomersTalent

KEYFOCuSAREAS

CHANNELS

TECHNOLOGICALLYFOCuSED:DigitalattheCore,PeopleattheForefront

COREVALuES

Hereforthelongterm

Innovation Collaboratetowin

Decisiveness Havefun

INCORPORATEDIN1905:KwongLeeMortgageandRemittanceCompanyinKuching,Sarawak

LOCATIONS:• Malaysia(HQ) (Listed on Bursa Malaysia)

• Singapore• HongKong• Vietnam• Cambodia• China

CORPORATE

09ANNUALRePORT

2018

2013• HongLeong

BankCambodiacommenceditsoperations

• SetuprepresentativeofficeinNanjing,China

1905StartedinKuching,Sarawak,Malaysia,underthenameofKwongLeeMortgageandRemittanceCompany

1989RenamedasMuIBank,operatingwith35branches

2008EnteredChinaBankingSectorwitha20%strategicstakeinBankofChengduCo.,Ltd.

2011HongLeongBankcompletedmergerwithEONBankGroup

1934IncorporatedasKwongLeeBankLimited

1994• AcquiredMuIBank

throughHongLeongCreditBerhad(NowknownasHongLeongFinancialGroupBerhad)

• RenamedasHongLeongBankBerhad

2012LaunchedMachbyHongLeongBank,anextgenerationBankingsub-brand

2009HongLeongBankVietnamopeneditsdoorsinHoChiMinhCity

2014LaunchednewInternetBankingplatform,PExpayment,tabletappandcardlesswithdrawal

Intensified digitization of Hong Leong Bank’s products and services

cORPORATeMILeStoNeS

10ANNUALRePORT2018

HONG LEONG BANK BERHAD

2015• Launchednew

platformforbusinessinternetbankingtoreplaceHLOB(HongLeongOnlineBusiness),Applewatchapp,e-FD&e-TDI,e-Will/WasiatandBiometricauthentication

• IntroducedphysicalPEx+MerchantPayment

2017•Pilotedin-branch

mobileservicingsolutionfeaturingiPad-equippedserviceambassadorstogreetandservicecustomers

•LaunchedHLBLaunchPadtonurtureMalaysiantechnologyandFinTechstart-ups

•IntroducedeFDviaFPX

2016•FirstdomesticbanktoenableFPXpayment

allowingcustomerstoconducttransactions24/7viaHongLeongConnectBIZ

•LaunchedArtificialIntelligenceChatServiceusingIBMWatson,E-TTandonlinestatement

•SuperchargedinnovationthroughthesettingupofaCustomerExperienceandInnovationLab

•Movedtoonlineplatformsforautoandpersonalloans,creditcard&CASA(CurrentAccount&SavingsAccount)openingapplications

•PEx+MerchantPaymentwentonline

2018• RolledoutRoboticProcess

Automationprojects.

• Launchedcomprehensiveonlinebankingplatformsforcorporate,commercialandSMEbanking(HongLeongConnectFirst).

• Introduced,forthebenefitofeLearningforallemployees,apeer-to-peer,knowledgesharingmobileplatformapplicationwhichincorporatesfunelementsofgamificationinthelearningjourney(Smartup).

• EstablishedthefirstHongLeongBankDigitalConceptflagshipbranchinDamansaraCity,featuringPersonalizedTellertablets,TellerAssistedunitsandaDiscoveryZoneinteractivedigitalplatform.

• PilotedMulti-lingualRobotConciergeservicesatDamansaraCityPriorityBankingBranch

• IntroducedavirtualassistantArtificialIntelligencechatboxonouremployees’digitaldevices(HALI)toprovideanswersonHumanResourcesandBranchOperationsSupportpoliciesandprocedurequeries.

• RolledoutDigitalBusinessSolutionsandSMEliteFinancingfacilitiesforSMEs.

cORPORATeMILeStoNeS

CORPORATE

11ANNUALRePORT

2018

cHAIRmAN’SStateMeNt

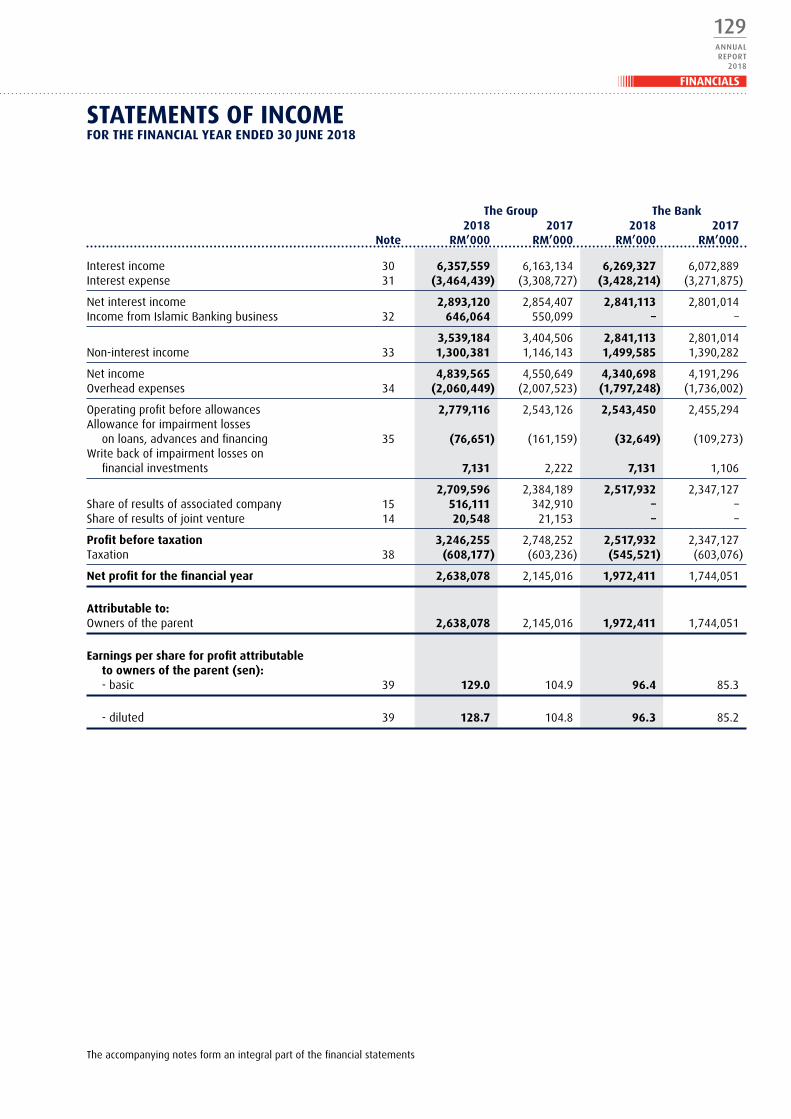

Hong Leong bank (“HLb” or “bank”) made important strides both financially and digitally in the 2018 Financial Year (“FY2018”). During the year, we achieved new milestones in profits and total assets. the bank made rM2,638 million in net profit in FY2018, our highest ever and 23% better than the previous year.

This was largely due to our robust growth in non-interestincome and prudent loan pricing coupled with improved costmanagement. Total assets stood at RM202.9 billion, crossingthe RM200 billion mark for the first time. The Bank’s carefuland responsible stewardship continues to deliver sustainablegrowth with steady top-line performance and effective costcontrol. This includes intensifying our income diversificationandimplementingoursustainabilityanddigitizationinitiatives,whichimprovedourcost-to-incomeratio.

We expect that the group’s performance during FY2019 willbenefit from steady growth in both the global and Malaysianeconomies. The Malaysian economy remained healthy andexpanded at a good pace of 5% in the first half of 2018,underpinned by continued expansion in private consumptionand exports. The global economy is expected to continue togrow in 2018 and support demand for Malaysian exports.This export demand should have spill-over benefits to otherdomesticsectors.

The Malaysian economy is expected to continue its growthmomentum,albeitatamoremoderatelevelinthesecondhalfof2018despitepotentially challengingdomesticandexternalconditions. However we expect policy reforms and prudentfiscalmanagementtostrengthentheMalaysianeconomywhichaugurswell for thefuture.Wearealsomindfulofgeopoliticalandotherrisks,chieflythedevelopmentofnewuStradepolicieswhichcouldpossiblyprecipitateatradewarbetweentheuSandChinaand/orothereconomiesaroundtheworld.

ecoNoMIc coNDItIoNS

TheglobalandMalaysianeconomyremainedingoodshapeinFY2018.TheMalaysianeconomyremainedfundamentallysound,supported by domestic demand and continuous expansion inexports. Inflation also stayed benign and the nation’s currentaccount surplus and ample foreign reserves should help thenation weather any unforeseen external shocks. The country’sfinancial markets also demonstrated resilience in the faceof volatilities such as the sell-down that rocked global equitymarkets in March. The Malaysian banking sector remainedhealthy and well capitalized. This allowed the banking sectortoplayavitalroleinsupportingnationaleconomicgrowthoverthepastyear.

There were however also significant political and economicdevelopments in Malaysia and across the world in FY2018.MalaysiaexperiencedanunprecedentedchangeingovernmentinMay2018,itsfirstsincegainingindependencein1957.Somemajor European countries such as France also experienced achangeofguard.Globallyinfluentialcentralbanks–namelytheuSFederalReserveandBankofEngland–opted tonormalizetheirverylowinterestrates,impactingcapitalflowstoemergingmarkets.During theyear,Malaysiaalsoadjusted itsOvernightPolicyRate(“OPR”)upwardsby25bpsto3.25%inJanuary2018.

FBMKLCIIndexby

40.1%

rM18.20forFY2018

FBMKLFinIndexby

36.9%

OuTPERFORMED

SHare prIce

35.5%over

5 years

12ANNUALRePORT2018

HONG LEONG BANK BERHAD

buILDING LoNG-terM VaLue

Theyearwasnotwithout its challengesas an array of regulatory and economicfactorscameintoplay.Asabank,wewereready to meet higher capital adequacyrequirements on top of increasinglystringent compliance standards. Ourcompetitive landscape too has shifted.No longer are we competing only withconventional financial institutions, butnowhavetoincreasinglyrespondtothedisruptionposedbyFinTechstart-ups.

TheGroupishoweverwellpositionedtonotonlyovercome thesechallengesbutgrowstrongerfromit.Forexample,ratherthanviewingFinTechasathreat,wearelearning,andinsomecases,collaboratingwith FinTech, becoming even moreentrepreneurial and competitivein the process. Our underlying keyoperatingmetrics remainsolid.Theyareunderpinnedbyacombinationofprudentloan pricing and judicious funding costmanagement.Ourresultsalsoshowedahealthynon-interest incomecontributionandbenefitedstronglyfromourcarefullyembedded culture of uncompromisingdiscipline with regards to operatingefficiencies.

For the year, the Group’s total assetsexpandedby3.8%fromRM195.6billionasat30June2017toRM202.9billionasat 30 June 2018. The Bank’s total grossloans and financing meanwhile rose3.1%year-on-year (“y-o-y”) toRM129.1billion as compared to RM125.1 billionthe previous year. The growth, despitecautious business sentiments, reflectsthe strength of our domestic retail andSME business. Total customer depositsexpanded1.4%y-o-ytoRM157.4billionwithgrowthcomingfromcorecustomerdeposits.

I am delighted to announce that ourearnings per share (“EPS”) was 129.0sen, while our return on equity (“ROE”)stood at 11.3% for FY2018. The valuerepresented by the Bank has beenrecognizedbythemarketwithourstockdoingappreciablybetterthankeyindices.Our share price closed at RM18.20 forFY2018representinga35.5%appreciationoverfiveyearsandout-performingboththeFBMKLCIindexandFBMKLFinindexby40.1%and36.9%respectively.

NeT PROfIT

rM2,638million

+23%

TOTAL gROSS LOANS ANd fINANcINg

rM129.1billion

+3.1%

gROUP TOTAL ASSeTS

rM202.9billion

+3.8%

cHAIRmAN’SStateMeNt

CORPORATE

13ANNUALRePORT

2018

ForFY2018,theBoardhasproposedafinaldividendof32.0senper share subject to the approval of shareholders during theforthcomingAnnualGeneralMeetingon29October2018.ThisbringsthetotaldividendforFY18to48.0senpershare,3.0senpersharehigherthanlastyear.

In another noteworthy development during the year, RAMRatings upgraded the long-term financial institution ratings ofHongLeongBankBerhadfromAA1toAAAinrecognitionofoursuperiorassetquality.ItalsoreflectedtheBank’ssustainedtrackrecordofhavingrobustfundingandliquiditypositions,aswellasourrespectabledomesticretailandSMEfranchises.

ISLaMIc baNKING

MalaysiaranksasagloballeaderinIslamicBankingandIslamicFinance is a keyelementof its economicgrowth. Thegrowthof Islamic banking in Malaysia continues to be encouraging,registering a steady 10% growth in financing assets in 2017.ThemarketshareofIslamicbankingassetsofthetotalbankingassetsaccountedfor26%ofthetotalbankingassetsinMalaysiaasat30June2018.

As one of the country’s Islamic Financing institutions, HongLeong Islamic Bank Berhad (“HLISB”) is committed to deliversustainablegrowthofitsbusinessandparticipatewiththeotherIslamicfinanceprovidersintheindustrytohelpMalaysiaremainattheforefrontofIslamicFinance.

HLISBperformedwell in FY2018. Theexpansion inProfitafterTaxandZakatwasmore than commendable,growing27% toRM282 million over the previous year. Gross Islamic financingassetsalsoexpandedby10%toRM22.9billion,makingup18%ofHongLeongBankGroup’stotalfinancing.

AstheIslamicbankingarmoftheHongLeongGroup,HLISBwillcontinuetocontributesignificantlybyprovidingholisticIslamicfinancial solutions to theGroup’s customer base.HLISB is alsoundergoingadigitaltransformationofitsbusinessandShariahgovernancetodrivegrowthwhilstatthesametimeaddressingcompetitivethreatsfromFinTechplayers.

HLISBwillcontinuetoadoptValueBasedIntermediation(“VBI”)principles in our business. This is to realize the full potentialofVBIand theway it can strengthen thebeneficial impactofIslamicBankinginthenation’seconomyandsociety.

“Inanothernoteworthydevelopmentduringtheyear,RAMRatings

upgradedthelong-termfinancialinstitutionratingsofHongLeongBankBerhadfromAA1toAAAinrecognition

ofoursuperiorassetquality.”

cHAIRmAN’SStateMeNt

14ANNUALRePORT2018

HONG LEONG BANK BERHAD

proGreSS acroSS tHe reGIoN

The Group views our regional footprintas integral to our expansion strategy.Our regional presence will also supportour commitment to deliver long-termgrowth and returns to our shareholdersinasustainablemanner.Tothisend,ourefforts have shown itself in our resultsas the total profit contribution frominternational operations accounted for18.2% of the Group’s pre-tax profit inFY2018, up from 14.6% in the previousfinancialyear.

Our Singapore operation, through HLBank Singapore (“HLBS”) represents animportant franchise for the Group as itis located in a leading global financialhub. The branch has transformed froma pure Private Banking proposition to amore comprehensive business. It nowencompassesothernichesegmentssuch

as Health Banking, Auto Financing andSME Banking. In the coming year, HLBSwill look to progress its business evenfurther to stay relevant to the youngergeneration of wealth builders and SMEbusinesses. This includes using digitaltechnology and leveraging on the HeadOffice’s (“HO”) digital transformationroadmap.

For the fifth year in a row, Hong LeongBank (Cambodia) PLC (“HLBCAM”) hadanother outstanding performance inFY2018. Our Cambodian operation’snet profit grew an impressive 130%y-o-y to RM14.2 million. Its total assets

meanwhile grew by 37% y-o-y toRM1.7billion.Tomeettheminimumnetworth requirement set by the NationalBankofCambodiaaswellas to supportour own growth agenda, Hong LeongBankBerhadinjectedRM16millioninsubdebtintoHLBCAMinJune2018.

Ourassociate inChina,BankofChengdu(“BOCD”)becamethefirstcitycommercialbank in Sichuan Province to be listedon the Shanghai Stock Exchange on 31January2018.WelookforwardtoBOCD’scontinued growth despite the uncertainimplications of trade tensions betweenuSandChina.

“OurassociateinChina,BankofChengdu(“BOCD”)becamethefirstcitycommercialbankinSichuanProvincetobelistedonthe

ShanghaiStockExchangeon31January2018.”

PROfIT AfTeR TAx ANd zAkAT

rM282million

HLb gROUP gROSS ISLAmIc fINANcINg ASSeTS

+27%

18%

cHAIRmAN’SStateMeNt

CORPORATE

15ANNUALRePORT

2018

coMMItteD to SuStaINabLe perForMaNce

The Group has crafted a vision of going beyond the balancesheet to play a role to help our stakeholders, customersand the communities we operate in to benefit economically,environmentallyandsociallyfromourinvestments.Weareheretobearesponsiblebankerandhelpourcustomerssucceedinasustainableway.

Toachievethis,weoperateourbusinesssoastobemorethana banker but to actually be a valued partner to our clients.This means that we help our customers adopt practices thatstrengthentheirbusinesswhileatthesametimeachievetwoothersustainabilitygoals:enhancingthedevelopmentalimpactofinvestmentsandinfluencingnationbuildingforthebetter.

HLBGroupundertookabroadspectrumof initiativesdesignedtocatalyzeandbringaboutthedesiredsustainabilityoutcomes.

Werampedupthetechnicalassistanceandadvisoryresourceswe make available to clients. We provided tailored guidancetocompaniesthroughourcorporategovernanceprograms.Ourdigitizationstrategyhelpedtoreimaginethebankingexperiencewhilereducingenvironmentalimpact.Wepromotedsustainablebusinessdevelopmentthroughinnovationsinourproductsandservicesprovided toSMEs.We launched initiatives toenhanceenergy efficiency in our operations. We also implementedprudentandstringentpoliciestoensurecleanandresponsiblefinancingofferingstocustomers.

We publish a sustainability report to better communicateour strategies and progress. This report details our effortsand initiatives across the group to promote environmentallysustainableandinclusivegrowthaswellastoreduceourcarbonfootprint.Inthisregard,wearepleasedtohavemetthegloballyrecognized standards for inclusion in the FTSE4Good BursaMalaysiaIndex.

cHAIRmAN’SStateMeNt

16ANNUALRePORT2018

HONG LEONG BANK BERHAD

LooKING aHeaD

We expect major centralbanks to maintain theirgradual monetary policynormalization in thecoming year. This is dueto sustained growth inthe global economy,underpinnedbycontinuousexpansion in bothadvanced and emergingmarketeconomies.

IntheuS,weseeanyfiscalboostsarisingfrom theuS taxplansas likely towanemoving forward.Ongoing trade tensionsbetweentheuSandChinameanwhileisexpectedtocastashadowonthegrowthoutlookoftheworld’slargesteconomy.

Withthisinmind,wewillcontinuetostayvigilantandexercisecautioninexecuting

our strategy of prudent and responsiblegrowth.

WeexpectMalaysiatostayonamoderategrowthpaththankstoitsdiverseeconomicstructure,soundmacrofundamentalsandpolicy flexibility. These features suggestthecountryiswell-positionedtoweatheranyundesirableshocks.

Goingforward,theGroupiscommittedtodeliverlong-termsustainablegrowthandshareholdervaluebycontinuingtoexecuteourbusinessanddigitalstrategies.Wearehowever,cognizantofthechallengesandpotential economic headwinds that lieahead.Toensuresustainablesuccess,wewill focus on improving our operationalefficiency with innovation and increaseour capacity through strategic costand portfolio management. We willalso strengthen our digital offerings totransform our customer engagementprocess and reimagine banking throughcustomer journeys. We will also growour customer base both through ourcommunity focusedbranchnetworkandthroughdigitalchannels.

acKNoWLeDGeMeNtS

Lastbutnotleast,Iwouldliketoexpressmy heartfelt appreciation to my fellowBoard members for their support,guidance andwisdom. Iwould also liketothankourcustomers,businesspartnersandshareholdersforplacingtheirtrustinusaswellasfortheirloyaltyandsupportovertheyears.WealsowouldnotbewherewearetodaywithoutthetirelesseffortsofourpeopleandIwouldliketoexpressmy appreciation to senior managementandallouremployeesforembodyingthetwin idealsof theBankofbeingethicalandentrepreneurial incarryingout theirduties. My deepest appreciation alsogoes out to Bank Negara Malaysia, theMinistryofFinance,governmentagenciesandotherregulatoryauthoritiesfortheirassistance,guidanceandsupport.

QueK LeNG cHaNChairman

19September2018

cHAIRmAN’SStateMeNt

CORPORATE

17ANNUALRePORT

2018

fIVe yeAR gROUPFINaNcIaL HIGHLIGHtS

FY14 FY15 FY16 FY17 FY18Group rM’Million rM’Million rM’Million rM’Million rM’Million

TotalAssets 170,351 184,020 189,828 195,553 202,891

GrossLoans 104,169 113,418 120,605 125,147 129,069

CustomerDeposits 130,252 140,276 148,524 155,233 157,414

Shareholders’Fund 14,530 16,790 21,117 22,685 23,892

ProfitBeforeTax 2,613 2,746 2,382 2,748 3,246

ProfitAfterTax 2,102 2,233 1,903 2,145 2,638

Earningspershare(sen) 119 126 100 105 129

Netdividendpershare(sen) 41.0 41.0 41.0 45.0 48.0

Dividendpayoutratio(%) 34.4% 32.4% 44.1% 42.9% 37.2%

FY14 FY15 FY16 FY17 FY18bank rM’Million rM’Million rM’Million rM’Million rM’Million

TotalAssets 148,822 160,681 162,238 164,817 169,111

GrossLoans 89,225 96,691 101,054 103,516 105,079

CustomerDeposits 114,099 122,337 126,241 129,859 129,583

Shareholders’Fund 12,330 13,428 17,431 18,442 19,263

ProfitBeforeTax 2,058 2,279 2,025 2,347 2,518

ProfitAfterTax 1,591 1,776 1,605 1,744 1,972

GroSS LoaNS, aDVaNceS aND FINaNcING GrowthledpredominantlybymortgagesandSME(RM’Million)

DepoSItS FroM cuStoMerS Healthygrowthwithindividualsdepositmixof56%

YoY +3.1% YoY +1.4%

£ Individuals Deposits Mix %£ Total Deposits (RM‘Million)

125,

147

155,

233

120,

605

148,

524

113,

418

140,

276

104,

169

130,

25212

9,06

9

157,

414

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

51.2

%

50.0

% 54.8

%

55.5

%

56.0

%

FY FY

18ANNUALRePORT2018

HONG LEONG BANK BERHAD

15.8%14.7%14.3%14.6%

16.3%

fIVe yeAR gROUPFINaNcIaL HIGHLIGHtS

totaL INcoMe underlyingrevenueremainedsolid(RM’Million)

aSSet QuaLItY Consistentlyout-performedtheindustryaverageof1.58%

proFItabILItY Record-breakingPBTandPAT(RM’Million)

roe % 15.3% 14.3% 10.0% 9.8% 11.3%

capItaL ratIoS Robustcapitalpositions,supportiveofgrowth

YoY +6.3%

2014 2015 2016 2017 2018 2014 2015 2016 2017 2018

£ GIL Ratio£ Industry GIL Ratio

£ PBT£ PAT

£ Total Capital %£ Tier 1 %£ CET 1 %

1.76%

1.18%

1.61%

0.84%

1.62%

0.79%

1.63%

0.96%

1.58%

0.87%

4,55

1

2,74

84,17

8

2,38

2

4,06

7

2,74

64,03

9

2,61

3

4,84

0

3,24

6

2014 2015 2016 2017 2018

2,14

5

1,90

32,23

3

2,10

2 2,63

8

2014 2015 2016 2017 2018

13.7%13.1%

11.9%

13.3%

13.3%12.7%10.5% 12.6%

FY

FY

FY

FY

11.9%

10.8%

CORPORATE

19ANNUALRePORT

2018

rM4,840million

rM1,344million

rM3,495million

totaL INcoMe

NoN-INtereSt INcoMe

Net INtereSt INcoMe

+6.3%

+12.5%

+4.2%

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

Our successextendedbeyonddomestic shoresasour regionalentitiesandassociateschalkedupimpressivegrowthnumbers.Wealsobrokenewgroundinourjourneytoreimagineourbankasadigitalenterprise.Wearethefirstbankincountrytoofferchat-basedbanking–utilizingtheubiquitousandpopularchattechnology to allow customers to now also perform bankingtransactions. We also embarked on artificial intelligence andautomationtorampupourproductivityandspeedofexecution.

The weaving of digital into our DNA has yielded valuableoutcomesrangingfrommonetarybenefitssuchascostsavingstomoreintangibleonessuchassuperiorcustomerexperiences.But while a superior customer experience may at first glancebeintangible,webelieveitcontributestocustomerloyaltyandgoodwill that in the long runwill translate to better businessoutcomes.

A deeper look at our numbers shows that the Bank hascontinuedtodowellthankstoitsprudentpoliciesanddiverseandstablefundingprofile.Apart fromourrecordnetprofitforthe year, total income also grew by 6.3% to RM4,840 millionfrom RM4,551 million the prior year. Our regional operationswereakeycontributorwith significantprofitgrowth fromourassociate company in China. Our sustainability initiatives alsohelpedimproveourbottomlinewithcostandefficiencygainsrealizedfromourongoingdigitaltransformation.

The overall macro environment remains favourable due tocontinuous moderate growth in the advanced economies andfasterexpansioninemergingmarket(“EM”)economies.TheuSeconomycontinuedtoholdupwell.Theothermajoreconomieshowever, notably the Eurozone and Japan are seeing softermomentum.

AsaresultoftheuSeconomy’sstrength,theFedremainsontheforefrontofmonetarypolicynormalization, triggering shifts inportfolioflowsoutoftheEMsbacktotheuS.ThispromptedsomeEMcentralbankstoraiseinterestratestoreducevolatilityandensurestability inthedomesticfinancialmarkets. InMalaysia,BankNegaramadethepre-emptivemovetoraisetheOvernightPolicyRate(“OPR”)by25bpsinJanuary2018.ThishikewasinanticipationoffurtherinterestrateincreasesintheuSamidthesteadygrowthandinflationoutlooklocally.

Onthelocalfront,weexpectgrowthprospectstoremainintact,albeitataslowerpace,on thebackofdomesticandexternaldemand.ThenewgovernmentinstalledinMay2018isreviewingspending on mega-projects that could cause some transitorysetback in investments. We expect however that the shortfallcouldbecushionedbyapotentialboostinprivateconsumptionandinvestments.

I am delighted with the Group’s performance and the manyachievements our people accomplished over the year. It ismy pleasure therefore, to present to you the Annual Reportand Financial Statements of Hong Leong Bank Berhad for thefinancialyearended30June2018.

Dear Shareholders, customers and business partners,

the bank turned in another strong performance across key fronts in FY2018. our profits were record breaking, our asset quality remained superior and our financial ratios were strong.

20ANNUALRePORT2018

HONG LEONG BANK BERHAD

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

operatING perForMaNce

Total income for theGroup for FY2018 stoodat a record RM4,840million, which is a 6.3%increasefromthepreviousyear. This achievementwas driven by prudentloan pricing, effectivefundingcostmanagementand good growth innon-interestincome.

Non-interestincomerosesignificantlyby12.5% to RM1,344 million as the Bankredoubledefforts todiversify its incomesources.Thekeycontributorstothehighernon-interest income were increases inwealthmanagement incomeandhighergains from treasury operations. This ledto an improvement in our non-interestincomeratioto27.8%.

Contributions from net interest incomealsoexpandedsteadilyby4.2%y-o-ytoRM3,495 million. For the financial year,ournetinterestmargin(“NIM”)increasedto2.10%comparedto2.09%thepreviousyear.

International operations were alsokey, contributing 18.2% of the Group’spre-tax profit in FY2018, versus 14.6%thepreviousyear.RegionalcontributionswereledbyBOCDwhichwerehigherby50.5% y-o-y at RM516 million. ProfitsfromBOCDmadeup15.9%oftheBank’spre-taxprofit.

Operating expenses improved over theyear, reflecting the gains realized fromourefficiencyandproductivitymeasures.Our cost-to-income ratio (“CIR”) dippedto a six-year low of 42.6%, betteringlastyear’smarkof44.1%.ThelowerCIRhelpedboostoperatingprofitforFY2018by 9.3% y-o-y to RM2,779 million fromRM2,543 million the previous year. Wealso saw positive JAWS (income growthrateexceedingexpensesgrowthrate)foreight consecutive quarters as costs andproductivityimprovedduetoefficienciesderivedfromourdigitizationandstrategiccostmanagementinitiatives.

In FY2018, gross loans and financinggrew 3.1% y-o-y to RM129.1 billiondespite a relatively cautious consumerand business environment. The increasewas predominantly due to contributionsfromourkeysegmentsofmortgagesandSmallandMediumEnterprises(“SMEs”).

Domesticloanstotheretailsegmentrosesteadilyby3.3%y-o-ytoRM91.0billion.Thefastestgrowthinloansandfinancingwasseeninresidentialmortgages,whichexpanded7.9%y-o-y to RM61.4 billion.The robust increasewas supportedby ahealthy home loan pipeline. Transportvehicle loans however, were lower atRM16.9 billion, reflecting softer industrygrowth.

“Oursuccessextendedbeyonddomesticshoresasourregionalentitiesandassociateschalkedupimpressivegrowthnumbers.Wealsobrokenewgroundinourjourneytoreimagineourbankasadigitalenterprise.Wearethefirstbankincountrytoofferchat-basedbanking–utilizingtheubiquitousandpopularchat

technologytoallowcustomerstonowalsoperformbankingtransactions.Wealsoembarkedonartificialintelligenceandautomationtorampupour

productivityandspeedofexecution.”

CORPORATE

21ANNUALRePORT

2018

SMEs are a key market for the Bank and loans and financingtoSMEswashigheratRM20.5billion,comprising15.9%oftheBank’sloanbase.Thiswasmainlydrivenbya22.4%growthintheBank’sGroupSMEBanking(“GSME”)portfolio.GSMEisanewcommunitybankinginitiativefocusingsolelyontheSMEmarketsegment.

The Bank maintained its strong position in terms of fundingandliquiditywhichremainedhealthyandprudentwithaloans-to-deposit ratio of 82.0%. Liquidity coverage ratio meanwhilecameinat126%,whichputsusaheadofscheduleaswellasfarexceedingregulatoryrequirementsof100%by2019.

TheBankcontinuedtoenjoyastablefundingbasebackedbyastrongindividualdepositbasewhichtopstheindustryat56.0%.

Customer deposits for FY2018 increased by 1.4% y-o-y toRM157.4 billion supported by strong CASA expansion of 6.3%y-o-y to RM41.2 billion. As a result, CASA ratio improved to26.2%ascomparedto25.0%lastyear.

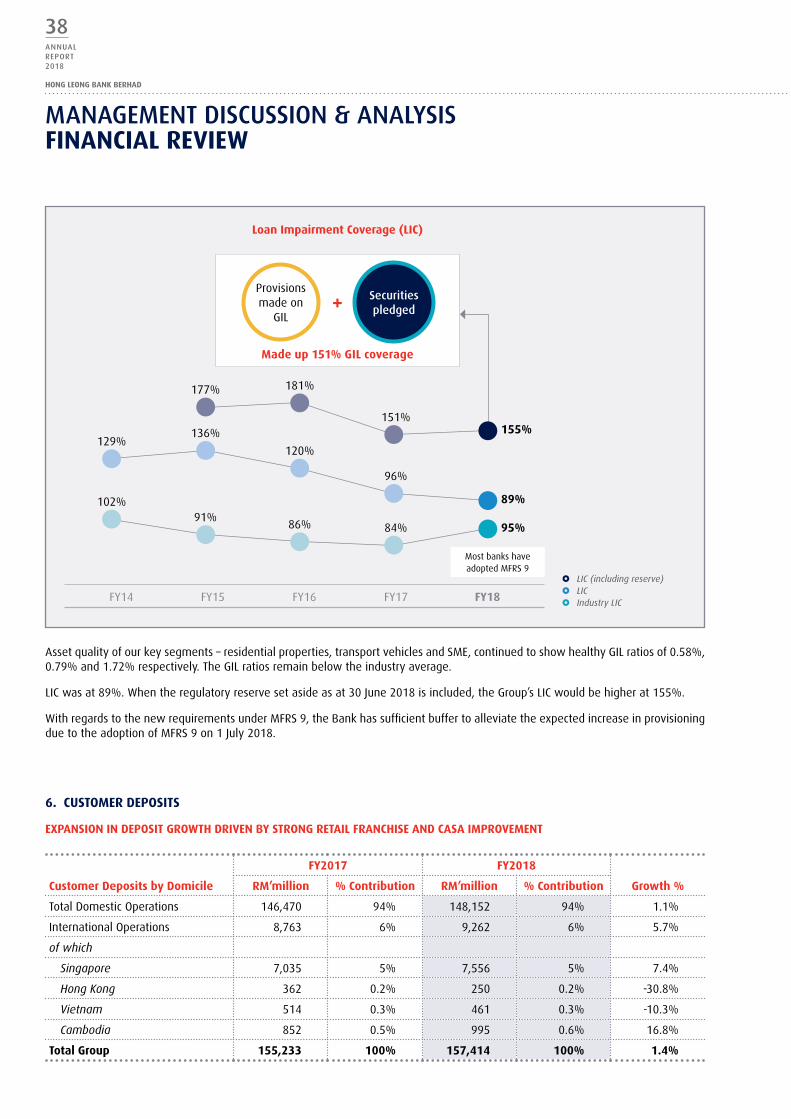

TheBankhasalwaysbeenuncompromisingaboutmaintainingstrong asset quality. FY2018 was no different as the grossimpaired loan ratio and the loan impairment coverage ratioremainedsolidat0.87%and89%respectively.Iftheregulatoryreserve set aside as at 30 June 2018 is included, the Bank’scoverageratiowouldbeevenhigherat155%.

TheBank’scapitalpositionremainsrobustwithCommonEquityTier1,Tier1andTotalCapitalRatiosat12.6%,13.3%and16.3%respectively.

Strategic Workforce planning

Strong employee-employer proposition

Focus on employee potential

Leverage on technology

1

2

3

4

Cost-to-IncomeRatio

42.6%OperatingProfit

+9.3% yoy

Loans-to-DepositRatio

82.0%LiquidityCoverageRatio

126.0%

Four KeY pILLarS

HuMaN reSourceS

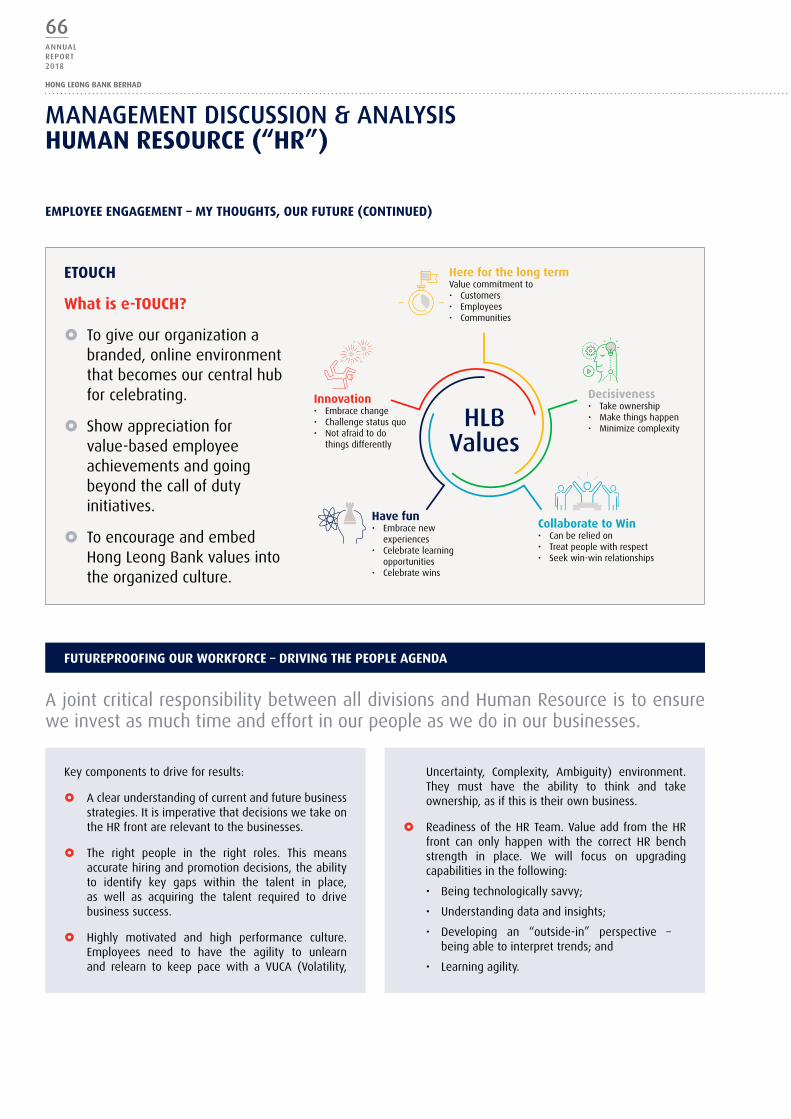

We at Hong Leong believe our people are our most valuableasset.OurambitiontobeahighlydigitalandinnovativeASEANfinancial services enterprise puts us in a unique position toattract, develop and retain a diverse pool of talented people.Tobuild thisfit for future talentpool,wehaveput inplaceastrategicroadmaptodrivethepeopleagenda.

GuidedbythefourkeypillarsofStrategicWorkforcePlanning,Strong Employee-Employer Proposition, Focus on EmployeePotentialandLeverageonTechnology,wehavemadesignificantprogressover thepast12months in advancingeachof thesefourpillars.

This year’s annual report present stories that reflect on theinitiatives we carried out based on the four guiding pillars.Thesestoriesillustrateourcommitmenttocreatingaconducivework environment, one that genuinely takes into account ouremployees’ needs and ambitions. We do this by giving ouremployees the best possible opportunities for learning andpersonal growth and equipping them to face the new andevolvingchallengesoftoday’sdynamicenvironment.

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

22ANNUALRePORT2018

HONG LEONG BANK BERHAD

SuStaINabILItY

We have a proud heritage of creatingvalue for our stakeholders, customersand communities in which we operate.Tomaintain thisover the longterm,wehave integrated sustainability practicesin our business to become stronger andmore resilient as well as to deliver onour social, economic and environmentalobligations.

In this report we will show how oursustainability practices have enhancedefficiency and supported SMEs – thebackbone of our economy. We will alsoshow how our compliance efforts andcorporate governance enhance andprotect stakeholder value. And last butnotleast,ourreportwillpresenthowour

Corporate Social Responsibility (“CSR”)efforts reach beyond our Group to helpourcustomerssucceed.

Digitalinnovationisakeycomponenttoour sustainability as an enterprise as ithelpsusremainrelevantandcompetitivein an era of increasing technologicalsophistication.Ourdigitalizationexercisehasreapedpositivereturnsandsignificantsavings for thegroupsince its launch in2016.Inthisreport,youwillseethatthelaunch of “Digital at the Core” in bothbusinessandhumanresourceoperationshasincreasedefficiencysignificantlyandenhanced effectiveness in our businessfacilities.

We also showcase how our corporatebankingproductsandservicesfacilitated

SME development by providing value-added services and programs that gobeyond financial services. SMEs accountfor over 98% of enterprises in Malaysiaandcontributesignificantly toMalaysia’sGDP. Similar to other emerging marketshowever, Malaysian SMEs commonlyfacebarriers tofinance.Or theymaybeheldbackbyabusinessenvironmentdueto the challenges that come with sizelimitations.

Supporting small business growthis essential for long term economicgrowth.Wewant to help small firms tothriveandbecome largerfirms.Thisnotonly increases market competition andinnovation but most importantly createssustainablejobopportunities.

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

CORPORATE

23ANNUALRePORT

2018

In line with this view and given thatSME development is a core componentof the Bank’s corporate strategy, wehavehelpedmanyofourSMEcustomersovercome their limitations with ourvaluepropositions.Thismeansthattheirlimitations in termsofHumanResource,Administrative,SupplyChainandLogisticswere all addressed with our innovativeproducts and services. This serves asmeans of operationalizing our end goaltopromotesustainableSMEdevelopmentlocallyandintheSouthEastAsianregion.

In this report, we also present in atransparentway, thestringentprocessesimplemented internally to ensure ourproducts and services are customers’needs focused and adhere to stringentethics and professional norms. Thisincludes our corporate governanceprocessesandthenecessaryduediligencereviews that ensure HLB is compliantto the codeand conduct of thebankingindustry and operates as a responsiblefinancialinstitution.

Webelieveverymuch inpromotingCSRin client companies as well as our ownorganization. Our CSR focuses on threeareas. The first is helping the Group’sclientsandcommunitiesbetterrecognizeand seize opportunities. The second ishelpingthemavoidanyrisksarisingfromenvironmental and social areas relevanttotheirbusiness.Andthethirdishelpingthem to engage more effectively withlocalstakeholders.

recognition of our digital efforts

Anumber of theBank’s initiativeswereselected for prestigious awards andaccoladesoverthepastyear.TheseawardsarearecognitionfortheBank’sresiliencyin a challenging operating environmentand also a spotlight on our ongoingdigital transformation and commitmenttowards the provisioning of innovativedigital financial services solutions. Wealso emerged winners in competitionsthathighlightourexcellenceinattractingandgroomingtop-flighttalent.

Theawardsarealsoatestamenttohowour investments have enhanced thecustomer experience. The benefits wereespeciallyapparentfromourinvestmentsinourmulti-platformbankingchannels,inparticularourpushtoincreaseourreachthrough digital and mobile banking, aswell as through our community focusedbranchnetwork.

One of the highlights of the year waswhen we were selected as one ofAsia’s best employers for graduatesby Human Resources Asia RecruitmentAwards 2018. The award was for BestGraduate Recruitment Programme andis a recognition of our commitmentto developing the next generation ofexceptional bankers for the Group. TheBankoutshonemanystrongcompetitorsfromacrossAsiatobeselected.Theawardis a clear recognition of our program’scomprehensive approach to recruitinggraduatetalentanddevelopingthemintofirst-classbankingprofessionals.

AnotherawardtheBankclinchedwasforBestInnovationinRetailBankingMalaysia2017 by International Banker 2017BankingAwards. Thiswas in recognitionofourconstantdrivetoimproveproductsand services and make them customerfocusedthroughstate-of-the-artbankingsolutions.

TheGroup’sintensiveeffortstotransformcustomer experience as a digital bankwas recognized by Asiamoney whenit gave us the Best Bank in Malaysia –CashManagementCustomerSatisfactionAward 2017. In winning the award,Asiamoney noted our unmatchedcustomercentricapproachwhichincludedseveral first-in-Malaysia innovationsfocused on improving overall customerexperience. These included the use ofArtificialIntelligencetosupportcustomerservicethroughchatsoftwareandarobotconcierge to help guide customers atbranches, and the launch of “Loan2Go”being a straight-through-processingmobileautoloanapplicationplatform.

“TheseawardsarearecognitionfortheBank’sresiliencyinachallengingoperatingenvironment

andalsoaspotlightonourongoingdigitaltransformationandcommitmenttowardsthe

provisioningofinnovativedigitalfinancialservicessolutions.Wealsoemergedwinnersincompetitions

thathighlightourexcellenceinattractingandgroomingtop-flighttalent.“

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

24ANNUALRePORT2018

HONG LEONG BANK BERHAD

TheBankalsoclinchedtheGoldAwardforHighest Returns to Shareholders Over 3YearsandSilverAwardforHighestReturnonEquityOver3YearsasawardedinTheEdge–BillionRinggitClub2017edition.Thesetwoawardsarearecognitionoftheoutstanding returns that we generatedfor our shareholders. Our shareholdersenjoyed commendable capital gainswhen our stock appreciated by 25.4%,from RM12.49 to RM15.66, betweenApril1,2014,and June30,2017,whichwas the period of review for The EdgeBillion Ringgit Club (“EBRC”). The returnwas the highest among all our bankingpeersintheEBRC.

StrateGIc prIorItIeS

We are transforming to be a highly digital andinnovative ASEAN financial services enterpriseand executing our digital strategy is a top priority.Whendiscussingourstrategicpriorities,itisimportanttokeepinmindthatweholdourwellembeddedvaluesastheguidingprinciplesthathaveledustowherewearetoday–standingtallasoneofMalaysia’sleadingbanks.We,therefore, remainsteadfast inourcommitmenttobuild momentum with carefully developed initiativesthatarebasedonourstrategicpriorities.

In formulating our strategic priorities, we will focus on: ever expanding digitalcapabilities,increasecustomerengagementandtransformationoftheentirecustomerexperiencewhenevertheyinteractwithus,capabilitiesenhancementinthesegmentsweserve;culturetransformationtoensureourworkenvironmentremainsconduciveto business growth in a highly evolving competitive landscape and finally, physicallocationsanddistributionnetworktransformationtoensurethatweareabletoengagecustomerswithvalueaddconversationsratherthansimpletransactionalinteractions.Iwillgointogreaterdetailabouteachofourstrategictenetsonthefollowingpage.

“Ourshareholdersenjoyedcommendablecapitalgainswhenourstockappreciatedby25.4%,whichwastheperiodofreviewforTheEdgeBillionRinggitClub.”

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

CORPORATE

25ANNUALRePORT

2018

Wehavealsolaunchedagame-changingnewmobilebankingapp with an enhanced interface and innovative ‘3-word-banking’functions.Thelatterisasmartfeaturewhichmakesbankingsimplerandevenmoreconvenientforourcustomers.Itallowsthemtotypeinjustthreewordstocompleteanentirebankingtransaction,anytimeandanywhere.ThethreewordsjustneedtostatethedesiredAction,NameandAmountandthetransactionwillbecompletedinstantlyanddigitally.Theappisalsobuilttogivecustomersamoresecureandseamlessmobilebankingexperience.

To improve the experience for our corporate, commercialandSMEcustomers,we launchedHongLeongConnectFirstinNovember2017.HongLeongConnectFirstoffersasinglesign-onaccesstoacomprehensivesuiteofadvancedcash,tradeandforeignexchangesolutions.Itisacomprehensiveplatformthatalsoprovidesforhighlevelsofcustomization.Thisallowsustoserveourcustomersbetterbycateringtoindividual needs across the entire range of our businessclients,eachofwhommayhavedifferentrequirements.

To strengthen our position as society goes increasinglycashless, we partnered with China’s mobile ecommercegiantTenCent.ThispartnershipinvolvesusingWeChatpaytoenableonlineandoffline(O2O)digitalpaymentsfromretailmerchantsinMalaysiawithaneasy-to-adopt,fullyintegratedcross-borderpayment solution. This is ourfirst forayas anacquirer of the very popular Chinese digital wallet-basedpaymentmethodology.BypartneringwithTenCent,wecanrideontheWeChatPayplatformwhichhasover600millionmonthlyactiveusersinChina.

Our goal to utilize technology to raise levels of customersatisfaction extends to the frontier of using Big Data.To deliver products and services that enhance customerexperience, we need meaningful insights to help usimprove our offerings. The Bank is increasingly leveragingon a combination of structured and unstructured data toderive the required insights. Our teams are at the sametimeimprovingourservicequalitybyconstantlymonitoringcustomer interactions through real-time analytics. We arealso enhancing our cross selling and customer acquisitioneffectiveness by the strategic use of data analytics togeneratetargetedleads.

In short,over the long term,wewant customers toenjoysimplicity, speed and control by offering a digital journeylikenoother.Onethatiscompletelyon-line,paperlessandhassle-freewithreal-timeapprovals.Andthiswillbedoneby effectively harnessing the power of digital capabilitiesandbigdataanalytics.

As part of our bank-wide strategic initiative ofembracingamindsetofbeingDigitalattheCore,wehave committed todo the following. Firstly,wewilldigitizetheBanksothatwecanacquirenew customers seamlessly. Secondly, we willtransform our customer engagement process toensure that we get to know customers better,anticipating their needs and providing solutionsthatcorrespondtothoseneeds.Wearespendingtimeandresourcestoreimagininghowbankingcanbethroughoutcustomerjourneysandhencedriving new experiences centred on making itsimple for customers when they deal with us.We are streamlining customer interactions overmultiple channels to provide a seamless andpersonalized customer experience across all thevarioustouch-points.

Tomaketheabovehappen,itiscrucialthatwesharpenourfocuson thedigitalbusinessmodelbyenhancingfivekeycapabilities:

ü Leverage on digital technologies to broaden our reachandacquirenewcustomers.

ü Enable customers to transact anytime and anywhereinstantlyanddigitally.

ü Engagewithourcustomersthroughcontextualmarketing.

ü Re-platform our technology stack and build inhousedigitalexpertise.

ü Step up utilization of data to create insights and driveaction.

Our people are exploring impactful new ideas aroundcustomerinteractionandengagement.Oneoftheoutcomesofthisistheimprovementoftheoverallcustomerexperiencethroughtheuseofinnovativeandcutting-edgetechnologies.For example, we introduced online application capabilitiesfora rangeofproducts. These include currentand savingsaccounts, personal loans, credit cards and mortgages. Byofferingthisonlineapplicationfunctionality,wemakethingseasierandsimplerforourcustomersastheycannowsubmitapplicationsattheirconvenience.

1. eXpaNDING DIGItaL capabILItIeS, INcreaSe cuStoMer eNGaGeMeNt aND traNSForMatIoN oF tHe eNtIre cuStoMer eXperIeNce

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

26ANNUALRePORT2018

HONG LEONG BANK BERHAD

We are cognizant of the evolving digital trendsthat shape consumer behaviour and businessmodels that are transforming the financialservices industry. Rather than trying to resistthe tide, we are utilizing these latest digitaltechnologies and emerging business models tobemorecompetitivebydesigningproductsandservicesthatcancatertotheneedsofevenourmostdiscerningcustomers.

Tobuildtherequisitecapabilities,wehavestrengthenedourtechnologicalreadinessandinvestedinin-houseproprietarydigital capabilities. Our technology team reconfigured oursystemstooptimizeourtechnologyinfrastructure.Wemadethestrategicdecisiontomovefromproprietarytechnologytoopensourceplatforms.TheBankalsoadoptedtheagiledevelopment cycle. These last two initiatives paved theway for us to build internal digital capabilities that candevelop solutions in significantly shorter time frames andat lower cost levels than was previously possible throughthe outsource model. As a result, we have become morecompetitiveagainstaggressiveandinnovativenon-financialserviceplayerssuchasFinTechstart-ups.

Now that we are armed with better in-house technicalcapabilities,enhancedfront-enddigitaltoolsandimprovedspeedtomarket,wecancollaboratebetterwithourbusinesspartners.Ourcollaborations, intheformofsharedbankingservices capabilities, help us build an edge against futurecompetition.

Our belief in the power of collaboration also led us toinitiate a mentorship and developmental program namedHLBLaunchPad.ThisstrategicprogramisaimedatnurturingyoungMalaysianentrepreneursand fosteringcollaborationwith theemerginggenerationof FinTechpractitioners andothertech-savvystart-ups.Theprogramhasbeenasuccessandisatestamenttoourbeliefthatworkingwithstart-upsisthewayforward.WorkingwithFinTechplayerstaughtustobemoreagile,nimbleandadaptivetocurrentmarketneeds.

Italsoinspiredustoacceleratethepaceofimprovementinourproductsandservices.

In order to remain relevant for the future and achievelong term sustainability, we continue to invest and buildcapabilities that take advantage of new and emergingtechnologies such as digitization and software robotics oralsoknownasroboticsprocessautomation(“RPA”).Throughdigitization of our products and services we are able toachieve operational excellence and transform the cost ofacquiringandservicingcustomers.Thisinturnallowsustodirect savings from the existing cost base into investmentin digital initiatives. A key example of this would be theintroduction of RPA. Development work on this excitinginnovation is currently underway at our processing centerandoperationsunit.WeforeseethattheuseofroboticswilldriveproductivityandefficiencyintheRetailandWholesaleBank Operations divisions. It is also expected to improvecycletimesandlowererrorrates.

We also worked on making banking a more pleasurableexperienceforbothourcustomersandemployees.Wedidthisby seamlessly integratingour services intoonlineandmobileplatforms.Weinspireouremployeestobeagileandadopt a start-upmentality byempoweringour employeeswiththefollowingdigitaltools:

ü Smartup:Ourknowledgesharingplatformthatprovidesbite sized learning programs to our employees tofacilitatecontinuousacquisitionofnewknowledgeanddevelopmentoftheirskillsbase.

ü HaLI:OurAIchatbotthatanswersquestionsrelatingtoHumanResources(“HR”)andbranchoperationssupport.ThechatbotisalsoaccessiblethroughthemobilephoneforquestionspertainingtoHRpolicies.

ü big Data dashboard: Our platform that provides realtime information to channel owners and otherstakeholders. It is a single data source for us to viewoperational performance, service levels and customersatisfactionlevels.

2. cuLture traNSForMatIoN to eNSure our WorK eNVIroNMeNt reMaINS coNDucIVe to buSINeSS GroWtH IN a HIGHLY eVoLVING coMpetItIVe LaNDScape

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

CORPORATE

27ANNUALRePORT

2018

We believe mobile and Internet banking willaccount for more than 75% of the Bank’s totaltransactions over the next couple of years. Thisis in line with evolving customer preferencesand hence our initiatives to transfer bankingtransactionstoonlineplatforms.

Infact,wesawtremendousgrowthininternetandmobilebankingcustomersovertheyear.Wearethereforeactivelyre-platforming our branches to ensure relevancy andefficiencyaswe continue toembedourbranches into thecommunitiestheyserve.

We are confident that robust digital capabilities will helpusacceleratebranch transformationbymovingaway fromlow-valuetransactionstomorecomplexproductssalesthatrequire human assistance. Our branches will complementtheir service offerings with our digital platforms. Towardsthisend,wearereconfiguringbankinghallsandequippingbrancheswithdigitaldevicesforbettercustomercentricity.

Themostexcitingdevelopmentinourjourneytorecastandreshapeourpremisesforthedigitalerawastheopeningofour flagship branch inDamansara City inNovember 2017.StrategicallylocatedinthedynamicandupscaleDamansaraHeightsbusinessdistrict, theflagshipbranch ispartofournewgreencertifiedcorporateheadquarters–MenaraHongLeong,whichweofficiallymovedintoinOctober2017.

As befitting a flagship experience that will serve as atemplateforourotherbranches,theDamansaraCitylocationfeaturesoptimaldeploymentofdigitaltechnologiesthatwillshift our customer experience to make it more rewardingandengaging.Tominimizequeuelines,weinstalledwirelessterminalsandapplications.Thesefacilitiesallowcustomerstheflexibilityofperformingspeedyandpersonalizedbankingtransactionsanywherewithinthepremises.AnewDiscoveryZone was also introduced in Damansara City. In the zone,visitorscaninteractwithourdigitalplatformstocustomizesolutionsfortheirfinancialplanningneeds.DamansaraCityisalsothefirstbranchtoofferadozenmeetingroomsforusebyourentrepreneurandbusinessassociates.OurPriorityBankingcustomerswillalsoenjoyanupgradedexperiencewithcomplimentaryvaletparking,state-of-the-artfacilitiesaswellasexclusiveartandfurnishings.Dodrop-intohaveacoffeeonus!

TheBankhasallocatedRM30millionofourcapextoconvert50outof250existingbranches to thenewdigital formatover the next couple of years. This initiative will lead tooperationalcostsavings.Forinstance,inourBurmahHousebranchinPenang,thenewdigitalformatreducedspacethat

waspreviouslydedicated forbackroomoperations suchasdepositmachinesto25%oftheoriginalarea.ThisopenedupadditionalspaceforcustomerservicingaswellasattheDiscoveryZone,whichisaimedatenhancingthecustomerexperience; whilst reducing overall space, hence, reducingrunningcosts.

Ourin-branchsalesandservicetabletdeviceswillalsoassistourbranchrelationshipofficersinservicingtheircustomersmore effectively. The devices have enabled our officers tooffercustomerspersonalizedsales,after-salesandcustomerservice. Ithelps themperformdigitalbanking transactionsand at the same time offer new products that meetcustomers’specificneeds.

Thisenhancedproductivitymeansthatwecanrepositionourbranchestoperformmorehighervalueactivities.WecannowdeployfocusedresourcesforWealthManagement,Insuranceandhighvaluesecuredlendingandofferadvisoryservicesto our customers. The branch will also focus on buildingdeeper relationships with the business community aroundthe catchmentareaof thebranch. This communitybasedapproachwillanchorourSMEofferinggoingforward.WearealsoinstallingTellerAssistunitstofacilitatethehandlingofcashanywhereinthebranch.Theunitssignificantlyincreasethesecurityofholdingcashinbranches,aswellas,enhancetheemployeeexperienceastheycomewithauditabletrailstoshortenreconciliationtimes.

We are building a best-in-class SME business to moreeffectively engage and serve SMEs. We are doing this byleveraging dedicated SME coverage teams. These teamsincludespeciallytrainedseniorexecutivesandarestationedatourtopbranchesandbusinesscentres.Thisallowsustogrow our presence in the SME segment and increase ourmarketsharebyembeddingourselvesinthecommunitytoimprove engagement and service delivery, as mentionedabove.

ThankstoourunderstandingofthesmallbusinesscommunityandthechallengesthatSMEsfaceoperatinginacompetitivemarket, the Bank is playing a role to help them be moreagileandnimble.TocatertotheneedsoftheSMEmarket,we launched an innovative and comprehensive suite ofdigitalbusinessandfinancingsolutions tailoredspecificallyto serve the needs of SMEs. The suite encompasseseverything from cash management to advertising andpromotion(A&P)solutionsaswellaspropertyfinancingandworking capital schemes to support day-to-day businessoperations;employeeandtaxmanagementdigitaltoolsandan innovative invoice financing offering through a FinTechpartner.

3. pHYSIcaL LocatIoNS aND DIStrIbutIoN NetWorK traNSForMatIoN to eNSure tHat We are abLe to eNGaGe cuStoMerS WItH VaLue aDD coNVerSatIoNS ratHer tHaN SIMpLe traNSactIoNaL INteractIoNS

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

28ANNUALRePORT2018

HONG LEONG BANK BERHAD

outLooK

The global economy isexpected togrowsteadilyin 2019, underpinned bycontinuous but slowergrowth in advancedeconomies and fastergrowth in the emergingmarketeconomies.While global demand is expected toremain healthy, there are potentiallydisruptive risks in the coming year thatwewillkeepaclosewatchon.ThefirstisanyescalationintradetensionsbetweentheuSanditsmajortradingpartners.Thesecondismonetarypolicyshiftsbyglobalcentral banks. The third are geopoliticalrisks, especially in Europe with Brexitexpected tohappen inMarch2019,andlastbutnotleast,thelatestTurkishcrisisthat raised fearofaspill-over toEuropeand other emerging markets. Each ofthese developments could have majorrepercussionsontheglobaleconomyandfinancialmarkets.

Major central bankers, including theuS Federal Reserve and the Bank ofEngland,havewarnedofdownsiderisksto global growth prospects should tradeprotectionism and geopolitical riskscontinue to manifest. This is in additionto policy normalization that is moreaggressive than expected, which couldstymiegrowthandliquidity.

In the local context, the Malaysianeconomy is expected to track theoutlook of the global economy. Growth

will continuetobesupportedbyprivateconsumptionandexternaldemand.Thesetwoeconomicdriversmighthavetopickuptheslack fromanytransitorysetbackin investmentdue to thepostponementandreviewofnumerousmegadomesticprojects as the new governmentreprioritizes and streamlines its fiscalagenda. That said, overall growth isexpectedtoremainonasteadytrajectory,barringoutbreakofanyglobalcrisis.

acKNoWLeDGeMeNtS

Many parties have played a part in oursuccess. I want to thank our customersfirstandforemostfortheirtrustinusandfor their loyal patronage. I also want tothank our shareholders for their strongsupport and belief in us and what wearedoing.Mydeepestappreciationalsogoes to the Board of Directors for theirinvaluablewisdomandguidance.

The Hong Leong Group family – all theemployeesandmymanagementteam–havegivenselflesslyoftheirenergyandtalentstoensuretheBank’sprogressandsustainability. I want to thank them fortheir dedication, commitment and hardworkintheexecutionoftheirduties.

IalsowanttoextendmyappreciationtoBank Negara Malaysia, the Ministry ofFinance, related government agenciesandotherregulatoryauthoritiesfortheirguidanceandassistanceduringtheyear.

For a deeper look at the Bank’sperformance in FY2018, please refer totheManagementDiscussionandAnalysis(“MD&A”)section.

DoMeNIc FuDaGroupManagingDirector/ChiefExecutiveOfficer

19September2018

Whiledigitizationisourprincipalpriority,weremaincognizantofthecyber-securityrisksinvolved.Toaddressthis,wehavestrengthenedourcyber-securitycapabilitiestocreateahighlysecured digital environment. We did this through activemonitoringandethicalhackingtoidentifyanyweaknessinourtechnologycapabilitiesandorganizationset-up.Wealsocreatedawareness through threat intelligenceand internal

training. We made sure that our robust and automatedprocesses are backed by comprehensive security controlsthatenablereal-timeservicedeliverywhilemanagingfuturethreats.Wecontinuetoruneducationalcampaignstoensurethatcustomersareawareofcybersecurityrisksandplayapartinsafeguardingdigitalofferingsandcapabilities.

gROUP mANAgINg dIRecTOR/cHIeF eXecutIVe oFFIcer’S reVIeW

CORPORATE

29ANNUALRePORT

2018

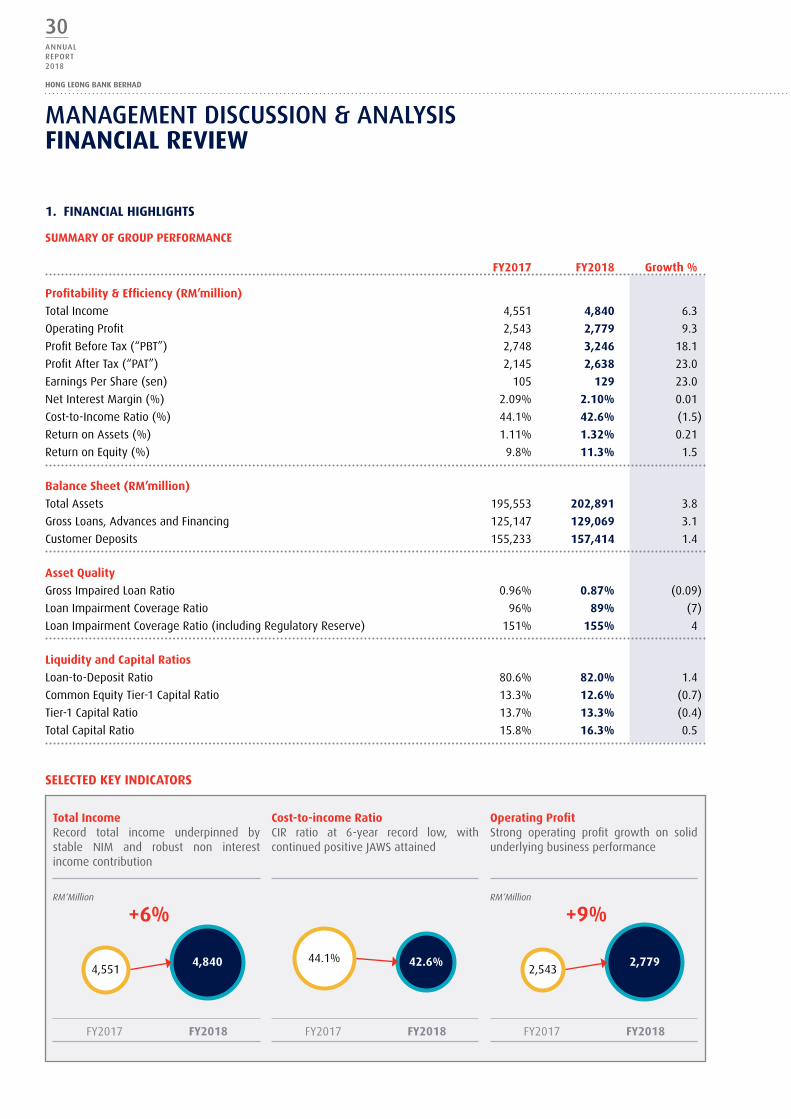

mANAgemeNT dIScUSSION & ANALySISFINaNcIaL reVIeW

FY2017 FY2018 Growth %

profitability & efficiency (rM’million)

TotalIncome 4,551 4,840 6.3

OperatingProfit 2,543 2,779 9.3

ProfitBeforeTax(“PBT”) 2,748 3,246 18.1

ProfitAfterTax(“PAT”) 2,145 2,638 23.0

EarningsPerShare(sen) 105 129 23.0

NetInterestMargin(%) 2.09% 2.10% 0.01

Cost-to-IncomeRatio(%) 44.1% 42.6% (1.5)

ReturnonAssets(%) 1.11% 1.32% 0.21

ReturnonEquity(%) 9.8% 11.3% 1.5

balance Sheet (rM’million)

TotalAssets 195,553 202,891 3.8

GrossLoans,AdvancesandFinancing 125,147 129,069 3.1

CustomerDeposits 155,233 157,414 1.4

asset Quality

GrossImpairedLoanRatio 0.96% 0.87% (0.09)

LoanImpairmentCoverageRatio 96% 89% (7)

LoanImpairmentCoverageRatio(includingRegulatoryReserve) 151% 155% 4

Liquidity and capital ratios

Loan-to-DepositRatio 80.6% 82.0% 1.4

CommonEquityTier-1CapitalRatio 13.3% 12.6% (0.7)

Tier-1CapitalRatio 13.7% 13.3% (0.4)

TotalCapitalRatio 15.8% 16.3% 0.5

SeLecteD KeY INDIcatorS

1. FINaNcIaL HIGHLIGHtS

SuMMarY oF Group perForMaNce

total Income Record total income underpinned bystable NIM and robust non interestincomecontribution

operating profit Strong operating profit growth on solidunderlyingbusinessperformance

cost-to-income ratio CIR ratio at 6-year record low, withcontinuedpositiveJAWSattained

FY2017 FY2018 FY2017 FY2018FY2017 FY2018

RM‘Million RM‘Million

+6% +9%

4,840 2,77942.6%4,551 2,543

44.1%

30ANNUALRePORT2018

HONG LEONG BANK BERHAD

mANAgemeNT dIScUSSION & ANALySISFINaNcIaL reVIeW

outStaNDING operatING MetrIcS & proFItabILItY

Allofourkeyfinancialindicatorshaveshownimprovementsfromthepreviousyeardespitea challengingbusinessenvironmentthathasaffectedthebankingindustry.

Total income for FY2018 sustained its growth momentum,improvingby6.3%y-o-y toRM4,840million.Thegrowthwassupportedbyacombinationofprudentloanpricingandfundingcost management coupled with strong growth in non-interestincomecontribution.

Operating expenses for FY2018 remained well managed, atRM2,060million.ThissetsanewmilestonefortheBankascost-to-incomeratio(“CIR”)dippedto42.6%,thelowestinsixyears,withpositiveJAWsaffirmedforeightconsecutivequarters.Thisisaresultofourcontinuingdrivetorealizeefficienciesfromourdigitizationandstrategiccostmanagementinitiatives.

Operating profit for FY2018 expanded 9.3% y-o-y to RM2,779million versus RM2,543 million in the same period last yearon the back of solid top-line growth coupled with improvedefficiencies. Correspondingly, PBT and PAT accelerated 18.1%and 23.0% to a record RM3,246 million and RM2,638 millionrespectively.

Earningspershare(“EPS”)hasimprovedto129sencomparedto105senthelastfinancialyear.Returnonequity(“ROE”)wasalsofurtherenhancedto11.3%forFY2018ascomparedto9.8%thepreviousyear.

StroNG baLaNce SHeet

Althoughoperatinginarelativelycautiousconsumerandbusinessenvironment, our gross loans, advances and financing grewcommendablyby3.1%y-o-ytoRM129.1billion,predominantlyledbygrowthinourkeysegmentsofmortgagesandSME.Atthesametime,ourcustomerdepositsforFY2018increasedby1.4%y-o-ytoRM157.4billion.Ourcustomerdepositshadanindustryhighest individual deposit mix of 56.0% - a testament to ourstrongretaildepositfranchise.Asaresult,theBank’sloans-to-depositsratio(“LDratio”)wasaprudent82.0%andsupportiveofgrowthgoingforward.Asat30June2018,theBank’sLiquidityCoverage Ratio (“LCR”) position was at 126%, surpassing theminimumregulatoryrequirementof90%foryear2018.

INDuStrY LeaDING aSSet QuaLItY MetrIcS

The Bank’s asset quality metrics has remained solid with anindustryleadinggrossimpairedloan(“GIL”)ratioof0.87%whileloanimpairmentcoverage(“LIC”)stoodat89%.Whenincludingtheregulatoryreservesetasideasat30June2018,theBank’sloanimpairmentcoverageratiostandsataveryrobustlevelof155%. TheadoptionofMFRS9on1 July2018 is expected toincreaseprovisioningrequirements.Nevertheless,theBankhassufficientbuffertoalleviateanyincreaseinprovisioningduetoMFRS9.

HeaLtHY capItaL poSItIoN

TheBank’scapitalpositionremainsrobustwithCommonEquityTier1,Tier1andTotalCapitalRatiosat12.6%,13.3%and16.3%respectively.

Gross Loans Growth was led by key segments ofmortgagesandSME

Deposits Deposit growth driven by healthy CASAexpansion

Gross Impaired Loan ratio Solidassetqualitywithnomajorstressonanyportfolio

FY2017 FY2018 FY2017 FY2018FY2017 FY2018

RM‘Billion RM‘Billion

+3% +1%

129.1 157.40.87%125.1 155.2

0.96%

CORPORATE

31ANNUALRePORT

2018

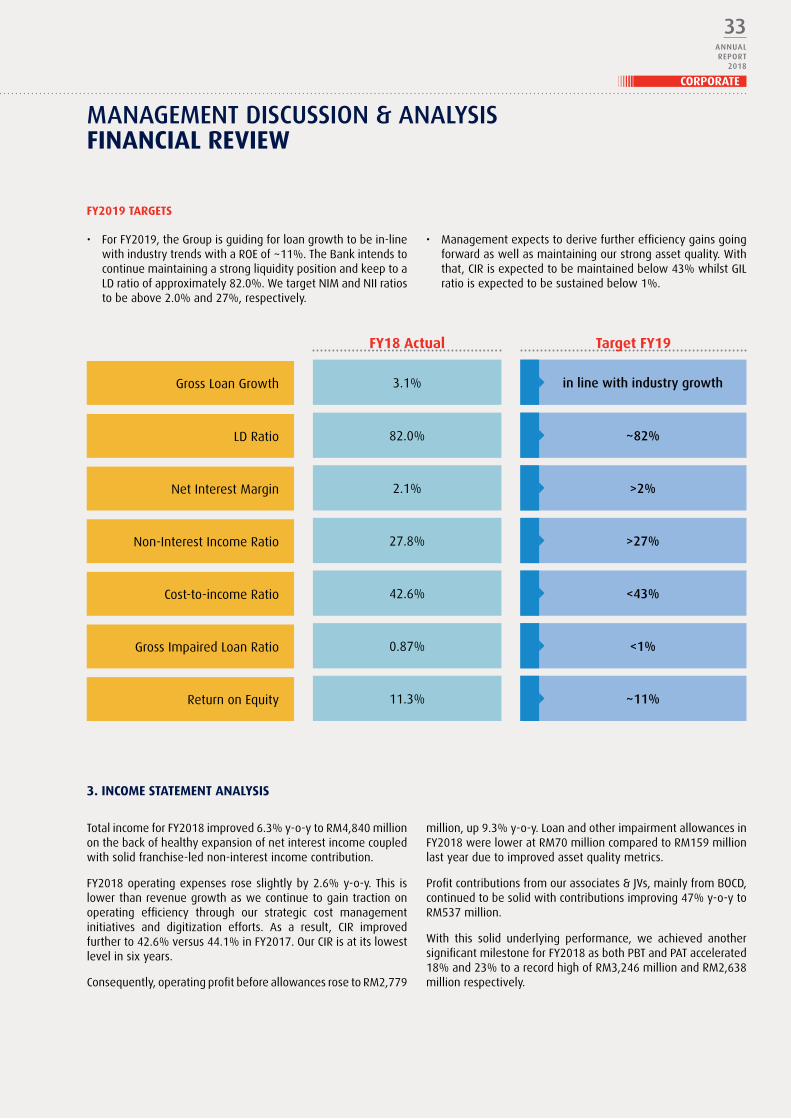

2. KeY perForMaNce INDIcatorS (KpIs)

FY2018 KpI acHIeVeMeNt

TheBank’sachievementsfortheyearisatestamentofitsstrongunderlyingoperatingperformanceasalltargetssetforFY2018were met. We are encouraged by these solid achievementsand expect that this will set the pace for a continued strongperformanceinthenewfinancialyear.

• Loansgrowthof3.1%was ledpredominantlybygrowth inkeysegmentsofmortgagesandSME,albeitstilloperatinginarelativelycautiousconsumerandbusinessenvironment.

• LiquidityremainshealthywithaLDratioof82.0%andLCRof126%,inlinewithourviewthatmaintainingampleliquidityremains a top priority, especially in a dynamic operatingenvironmentinfluencedbymacroglobaluncertainties.

• Netinterestmargin(“NIM”)forFY2018improvedto2.1%onprudentfundingcostsmanagementandloanpricing.

• Non-interest income (“NII”) expanded 12.5% y-o-y whichwascomplementedmainlybystrongerwealthmanagementincomeandhighergains fromtreasuryoperations.ThishasledtoastrongNIIratioof27.8%forFY2018.

• For FY2018,CIR improved further toa6-year record lowof42.6%,aswecontinuetoplaceemphasisonefficiencyandproductivitygains.

• AssetqualityindicatorsremainssolidwithGIL<1%asperourguidance.

• Our continued strong performance further underlines thestrengthoftheBankandreinforcesourcommitmenttowardsdelivering consistent results and sustainable profits as weachievedaROEof11.3%forFY2018.

GrossLoanGrowth

LDRatio

NetInterestMargin

Non-InterestIncomeRatio

Cost-to-incomeRatio

GrossImpairedLoanRatio

ReturnonEquity

3.1%

82.0%

2.1%

27.8%

42.6%

0.87%

11.3%

3%–4%(revised)

~82%

>2.1%

~26%

<44%

<1%

10%–11%

target FY18 achieved FY18

mANAgemeNT dIScUSSION & ANALySISFINaNcIaL reVIeW

32ANNUALRePORT2018

HONG LEONG BANK BERHAD

3. INcoMe StateMeNt aNaLYSIS

FY2019 tarGetS

TotalincomeforFY2018improved6.3%y-o-ytoRM4,840milliononthebackofhealthyexpansionofnetinterestincomecoupledwithsolidfranchise-lednon-interestincomecontribution.

FY2018operatingexpensesroseslightlyby2.6%y-o-y.This islowerthanrevenuegrowthaswecontinuetogaintractiononoperating efficiency through our strategic cost managementinitiatives and digitization efforts. As a result, CIR improvedfurtherto42.6%versus44.1%inFY2017.OurCIRisatitslowestlevelinsixyears.

Consequently,operatingprofitbeforeallowancesrosetoRM2,779

• ForFY2019,theGroupisguidingforloangrowthtobein-linewithindustrytrendswithaROEof~11%.TheBankintendstocontinuemaintainingastrongliquiditypositionandkeeptoaLDratioofapproximately82.0%.WetargetNIMandNIIratiostobeabove2.0%and27%,respectively.

million,up9.3%y-o-y.LoanandotherimpairmentallowancesinFY2018wereloweratRM70millioncomparedtoRM159millionlastyearduetoimprovedassetqualitymetrics.

Profitcontributionsfromourassociates&JVs,mainlyfromBOCD,continuedtobesolidwithcontributionsimproving47%y-o-ytoRM537million.

With this solid underlying performance, we achieved anothersignificantmilestoneforFY2018asbothPBTandPATaccelerated18%and23%toarecordhighofRM3,246millionandRM2,638millionrespectively.

• Managementexpectstoderivefurtherefficiencygainsgoingforwardaswellasmaintainingourstrongassetquality.Withthat,CIRisexpectedtobemaintainedbelow43%whilstGILratioisexpectedtobesustainedbelow1%.

GrossLoanGrowth

LDRatio

NetInterestMargin

Non-InterestIncomeRatio

Cost-to-incomeRatio

GrossImpairedLoanRatio

ReturnonEquity

3.1%

82.0%

2.1%

27.8%

42.6%

0.87%

11.3%

in line with industry growth

~82%

>2%

>27%

<43%

<1%

~11%

FY18 actual target FY19

mANAgemeNT dIScUSSION & ANALySISFINaNcIaL reVIeW

CORPORATE

33ANNUALRePORT

2018

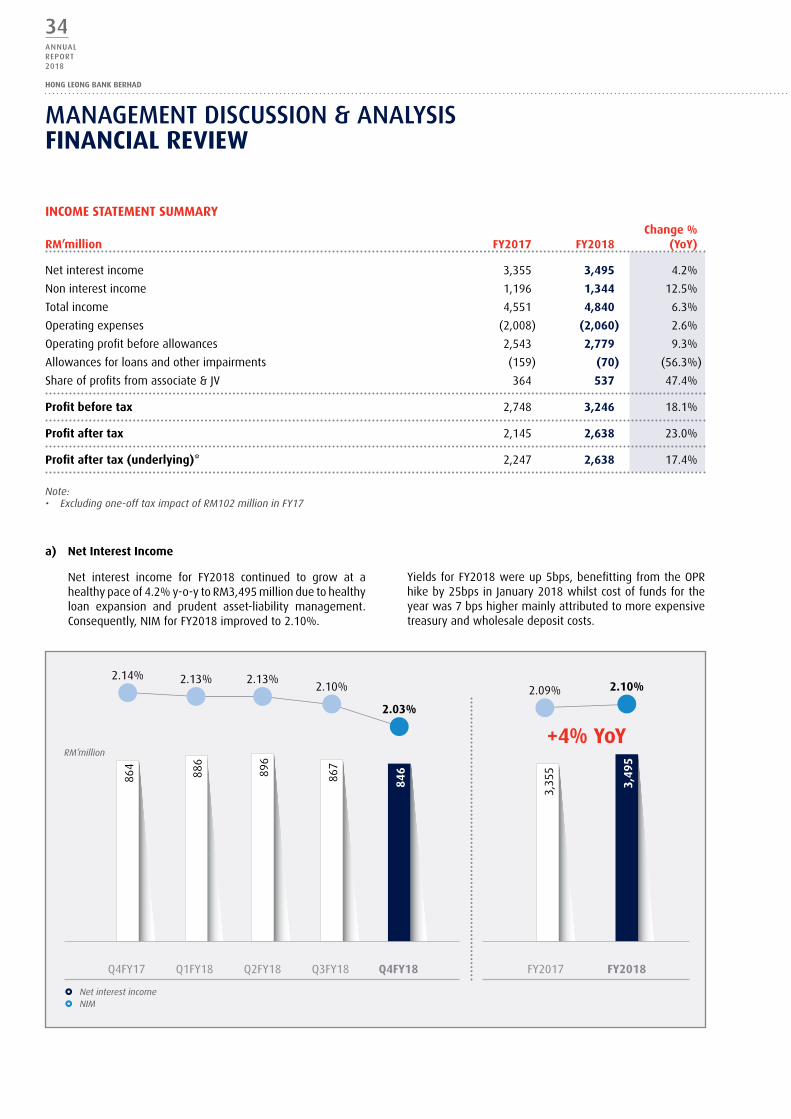

change % rM’million FY2017 FY2018 (YoY)

Netinterestincome 3,355 3,495 4.2%

Noninterestincome 1,196 1,344 12.5%

Totalincome 4,551 4,840 6.3%

Operatingexpenses (2,008) (2,060) 2.6%

Operatingprofitbeforeallowances 2,543 2,779 9.3%

Allowancesforloansandotherimpairments (159) (70) (56.3%)

Shareofprofitsfromassociate&JV 364 537 47.4%

profit before tax 2,748 3,246 18.1%

profit after tax 2,145 2,638 23.0%

profit after tax (underlying)* 2,247 2,638 17.4%

Note:• Excluding one-off tax impact of RM102 million in FY17

a) Net Interest Income

Net interest income for FY2018 continued to grow at ahealthypaceof4.2%y-o-ytoRM3,495millionduetohealthyloan expansion and prudent asset-liability management.Consequently,NIMforFY2018improvedto2.10%.

YieldsforFY2018wereup5bps,benefittingfromtheOPRhikeby25bpsinJanuary2018whilstcostoffundsfortheyearwas7bpshighermainlyattributedtomoreexpensivetreasuryandwholesaledepositcosts.

+4% YoY

2.14% 2.13% 2.13%2.10% 2.09%

2.03%

2.10%

867

3,35

5896

886

864

846

3,49

5

Q4FY17 Q1FY18 Q2FY18 Q3FY18 Q4FY18 FY2017 FY2018

£ Net interest income£ NIM

RM’million

INcoMe StateMeNt SuMMarY

mANAgemeNT dIScUSSION & ANALySISFINaNcIaL reVIeW

34ANNUALRePORT2018

HONG LEONG BANK BERHAD

b) Non-interest Income

Non-interest income for FY2018 saw a 12.5% y-o-yimprovementtoRM1,344million.Thisgaveusahighernon-interest income ratio of 27.8%. The growth in non-interestincome follows stronger wealth management income,dividend income from investments as well as robust gainsfromtreasuryoperations.

Wealth management income for Malaysia grew 24% y-o-ydriven mainly by growth in unit Trust and Banca whilststructured product contribution remained relatively stable.Fee incomecame in loweratRM574millionmainlyduetolowercreditcardfeesandloansyndicationfees.

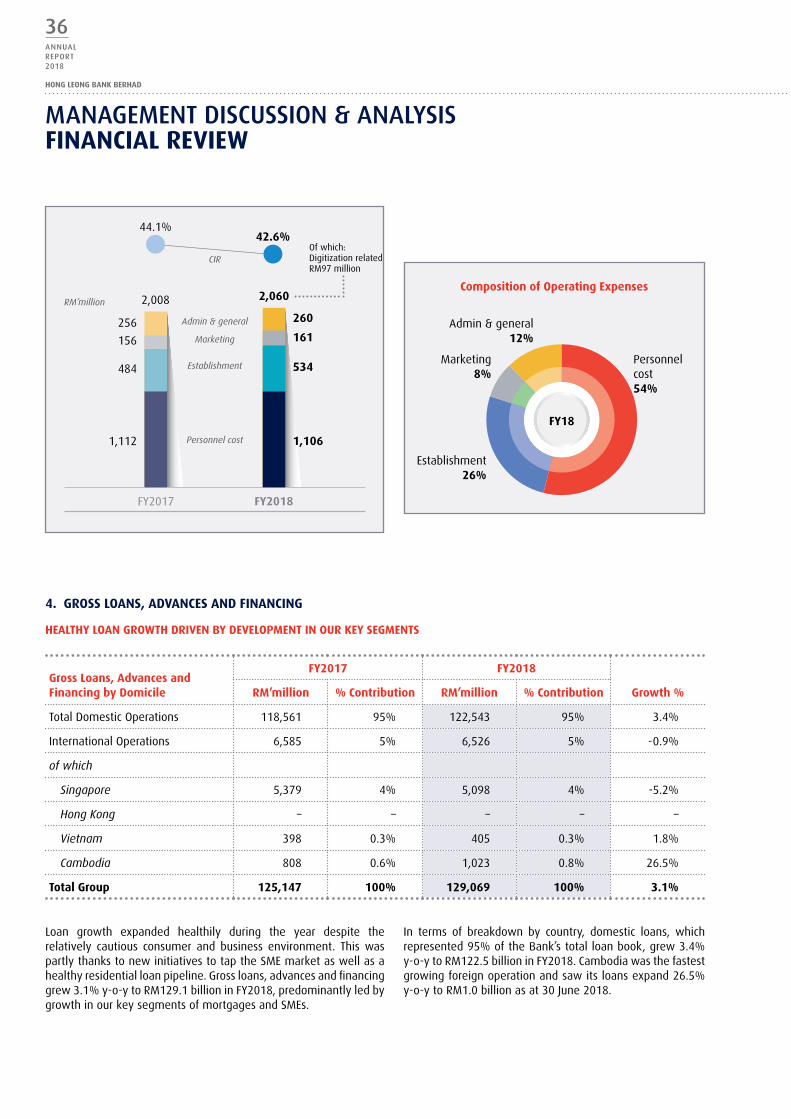

c) operating expenses

Operating expenses for FY2018 remained well managed.Operatingexpenses rose2.6%y-o-y toRM2,060millionasrevenuecontinued tooutpaceexpensesgrowth for the8thconsecutivequarter.Thefavorabledifferential ingrowthledtoanimprovedCIRof42.6%asourdigitalizationeffortsandstrategic cost management initiatives continue to improveefficiencyandproductivity.

Personnelcostsaccountedfor54%oftotaloperatingexpensesandwasmarginally loweratRM1,106millioninFY2018. Inlinewithourcommitmenttotalentmanagement,personnelexpenditurecontinuedtobefocusedoninvestmentintalentacquisition.

Establishment costs rose 10.3% y-o-y to RM534 million,representing26%oftotaloperatingexpenses.The increasewas primarily due to higher investment in informationtechnologytosupporttheBank’sdigitizationtransformationinitiatives. More specifically, expenses for digitization

Trading and Investment income grew 45.9% to RM623million. This growth was driven mainly by higher dividendincome received from our investments in wholesale fundscoupledwithhighergainsfromsaleofsecurities.

Foreignexchange(“FX”)incomewashigheratRM105millioncompared to the previous financial year due mainly to thereduction in FX swapactivities that resulted in lower swapcosts. FX income also benefited from higher FX franchiseincomefromincreasedclienthedgingvolumesarisingfromtheincreaseinRM/uSDFXvolatilitymoretowardsthesecondhalfofthefinancialyear.

initiativesaccounted forRM97millionorapproximately5%of the total cost base. The on-going digitization exercisehowever,isexpectedtoyieldnumerousmedium-to-longtermbenefits.Theseincludeincostsavingsduetobetterefficiencyand productivity. The benefits of the digitization initiativesrangefromprocesssimplification,redundancyreductionandturn-aroundtime(“TAT”)reduction,allofwhichwillincreaseefficiencylevelsacrosstheGroup.Digitizationwillalsoallowustoreachcustomersegments,bothinMalaysiaandintheother markets we operate, that the usual physical branchpresence would not, increasing the prospects for futurebusinessgrowth.

Marketing expenses in FY2018 rose 3.2% y-o-y toRM161million,makingup8%oftotaloperatingexpenses.Administration and general expenses for FY2018 wererelatively stable at RM260 million and accounted for theremaining12%oftheBank’stotaloperatingexpenses.

Feeincome:ofwhich

Wealth Management Income (Malaysia)

FY2017 FY2018

+24%

rM105millionRM85

million

26.3%27.8%

FY2017 FY2018

RM’million

69

1,196

1,344

91

427

609

10542

623

574

£ Non-interest income ratio£ Islamic and others£ Forex

£ Trading & investment£ Fee income

mANAgemeNT dIScUSSION & ANALySISFINaNcIaL reVIeW

CORPORATE

35ANNUALRePORT

2018

4. GroSS LoaNS, aDVaNceS aND FINaNcING

HeaLtHY LoaN GroWtH DrIVeN bY DeVeLopMeNt IN our KeY SeGMeNtS

Loan growth expanded healthily during the year despite therelatively cautious consumer and business environment. This waspartlythankstonewinitiativestotaptheSMEmarketaswellasahealthyresidentialloanpipeline.Grossloans,advancesandfinancinggrew3.1%y-o-ytoRM129.1billioninFY2018,predominantlyledbygrowthinourkeysegmentsofmortgagesandSMEs.

In terms of breakdown by country, domestic loans, whichrepresented95%oftheBank’stotalloanbook,grew3.4%y-o-ytoRM122.5billioninFY2018.Cambodiawasthefastestgrowingforeignoperationandsawitsloansexpand26.5%y-o-ytoRM1.0billionasat30June2018.

Gross Loans, advances and Financing by Domicile

FY2017 FY2018

Growth %rM’million % contribution rM’million % contribution

TotalDomesticOperations 118,561 95% 122,543 95% 3.4%

InternationalOperations 6,585 5% 6,526 5% -0.9%

of which

Singapore 5,379 4% 5,098 4% -5.2%