Languages

Pages

Legal

Banco do BrasilThe Company

First Half 2003

Total AssetsR$ million

1999 2000 2001 2002 Jun/03

126,454138,363

165,120

204,595 205,762

CustomersTotal Current AccountsIn thousands

1999 2000 2001 2002 Jun/03

11,10612,697 13,844

15,39116,717

Net IncomeR$ million

1999 2000 2001 2002 1H03

843974 1,082

2,028

1,079

1999 2000 2001 2002 1H02 1H03

R$ million

Net Income 843 974 1,082 2,028 823 1,079

Dividends/Interests onShareholders’ Equity 236 258 265 579 307 322

Net Income per 1,000 shares (R$) 1.18 1.37 1.52 2.77 1.16 1.47

Book Value per 1,000 shares (R$) 10.21 11.19 12.29 12.40 11.21 14.85

R$ million

Shareholders’ Equity 7,271 7,965 8,747 9,197 7,984 10,872

Total Assets 126,454 138,363 165,120 204,595 169,910 205,762

Credit Operations (1) 29,006 36,013 40,298 51,470 46,543 56,686

Deposits (2) 75,807 69,070 73,436 97,253 79,710 99,881

Asset Management 33,527 47,967 61,438 66,153 64,492 83,172

In thousands

Customers 11,106 12,697 13,844 15,391 14,541 16,717

Service Outlets 7.2* 7.5* 11.0 12.3 11.6 12.8

Automated Teller Machines 24.5 30.1 32.3 33.6 32.9 34.1

Credit Cards 1,862 3,252 3,829 4,731 4,281 4,853

Employees 69.4 78.2 78.1 78.6 77.9 79.7

R$ million

Gross Result from Financial Brokerage 1,164 4,681 4,869 8,071 3,250 3,974

Service Fees 2,785 3,189 3,760 4,454 2,167 2,561

Personnel Expenses (5,036) (5,623) (5,575) (5,548) (2,620) (2,990)

Other Administrative Expenses (2,573) (2,882) (3,586) (4,097) (1,823) (2,125)

(%)

Capital Adequacy (BIS Ratio) 9.2 8.8 12.7 12.2 11.6 13.8

ROE 11.6 12.2 12.9 22.6 20.6 22.7

Effi ciency Ratio 87.3 80.9 69.2 59.0 60.1 55.4

Coverage Ratio (3) 55.7 56.7 67.4 80.3 82.7 85.7

Personnel Expenses per Employee (R$) 61,655 62,127 61,940 62,766 29,721 33,128

(1) Net of provision, includes leasing operations(2) Demand deposits, time deposits, savings accounts, interbank deposits(3) Service Revenues/Personnel Expenses* Points of service provided by ATMs only not included

Figures at a Glance

33.5

48.0

61.466.2

1999 2000 2001 2002

64.5

83.2

Jun/02 Jun/03

13.4% 13.2%

16.2%

17.4% 17.2%

18.7%

Market Share

Total Assets

Asset ManagementR$ billion

1Banco do Brasi l F i rst Hal f 2003

Leadership Position

Largest network in Brazil with 12,755 points of service

Export exchange leader 29.6% market share

Largest ATM network in Latin America with 34,125 machines

Largest customer base with 16.7 million customers

Internet leader with5.3 million registered customers

Leadership in Credit Operations R$68.7 billion

1st in Deposits R$99.8 billion

1st in Assets R$205.8 billion

1st in Asset Management R$82.3 billion, 18.7% market share

Global Rating Classifi cation

FitchRatingsShort-Term Foreign Currency BLong-Term Foreign Currency BShort-Term Local Currency BLong-Term Local Currency BIndividual DSupport 4

Standard & Poor’sLong-Term - Local Currency BBLong-Term - Foreign Currency B+

Moody´sLong-Term Debt - Foreign Currency Ba3Long-Term Deposits - Foreign Currency B3Short-Term - Foreign Currency NPLong-Term Deposits - Local Currency A3Short-Term - Local Currency P-2Financial Strength E+

Domestic Rating Classifi cation

FitchRatingsShort-Term F1+(bra)Long-Term AA(bra)

Moody´sShort-Term BR-1Long-Term Aaa.br

2 Banco do Brasi l F i rst Hal f 2003

Bank of the Year in Brazil – The Banker Award

World’s Best Internet Banks Award 2003 – Global Finance Magazine

Best Corporate Institutional site in Brazil - bb.com.br

Best Online Consumer Credit in Latin America

Best Online Cash Management in Latin America

Best Banking Technology in Brazil – The e-fi nance Award

2003 Awards

3Banco do Brasi l F i rst Hal f 2003

Company Profi le 5Economic Environment 6Industry Outlook 8Financial Performance 10Shareholders 13Customers 14Retail 15Micro and Small Businesses 16Wholesale 17Public Sector 18Asset Management 19Agribusiness 20Family Agriculture 21Trade Finance 22Funding 23Securities 24Credit 25Distribution Network 28Automated Channels 30Human Resources 32Social Responsibility 33Banco do Brasil Figures 34Organizational Structure 38Group Structure 39Distribution Network Abroad 40Contact List 41

Table of Contents

4 Banco do Brasi l F i rst Hal f 2003

5Banco do Brasi l F i rst Hal f 2003

Company Profi le

Banco do Brasil (BB) is a government controlled corporation listed in the São Paulo Stock Exchange – Bovespa, with its shares being publicly traded since 1906. The company’s largest shareholder is the National Treasury, which owns 71.8% of BB’s shares, followed by Previ, Banco do Brasil employees’ pension fund, with 13.8%.

Founded on October 12, 1808, Banco do Brasil was the fi rst bank operating in Brazil and the fourth currency issuer in the world. From its foundation up to 1964, it performed the role of a Central Bank. During these almost two centuries, it has participated in the main events of Brazil’s economic fi nancial history.

Banco do Brasil operates in all segments of fi nancial and capital markets. Major investments in technology and personnel training as well as the adopted segmentation strategy were fundamental for the position of Banco do Brasil as an agile, modern and competitive company, committed with Brazilian society. In 2001, it became a multiple bank, and in 2002, it presented its best results in the recent history.

Throughout the year of 2003, the Bank has rearranged its organizational structure in order to enhance its strategies by acting even more focused on its customers needs and banking market opportunities.

Also, in consonance with Brazilian Federal Government policy, BB focused on promoting micro-credit. A Provisional Measure was signed by the federal government authorizing BB to create two new subsidiaries - one to offer micro-credit and another to fi nance the purchase of consumer durables. These companies will be operating independently and, in a near future, they will be helping BB to increase its customer base.

6 Banco do Brasi l F i rst Hal f 2003

Brazilian economy has been outstanding by the good performance of its external accounts, infl uenced by successive surplus on trade balance and by the reduction of net income sent abroad. Even in an unfavorable international context, foreign investments were enough to cover the needs of external fi nancing.

In order to guarantee the stabilization of the Brazilian economy, the Brazilian Central Bank has maintained the basic interest rate in a level compatible to the needs of taking off prices’ pressure.

Economic Environment

Trade Balance (FOB)US$ billion

-1.2 -0.7

2.6

1999 2000 2001 2002

13.1

10.4

2.6

1H02 1H03

Source: IBGE (Brazilian Institute of Geography and Statistics)

7Banco do Brasi l F i rst Hal f 2003

IPCA Price Index*Annual Change (%)

1999 2000 2001 2002

6.64

2.94

8.94

5.97

7.67

12.53

1H02 1H03

4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03

3.89

2.32 2.322.87

Exchange Rate*R$/US$

3.353.53

2.84

Source: IBGE (Brazilian Institute of Geography and Statistics)

Source: IBGE (Brazilian Institute of Geography and Statistics)*IPCA (Ample Consumer Price Index)

Source: Brazilian Central Bank*Price for dollar sale at the last working day of each quarter

1999 2000 2001 2002

GDPR$ billion

9641,087

1,1851,321

0.81

4.36

1.51 0.94

GDP Real Annual Chg. %

GDP

8 Banco do Brasi l F i rst Hal f 2003

Industry Outlook

Mergers and acquisitions made by private banks after the Real Plan increased competitiveness in the Brazilian Banking Industry. According to the Brazilian Central Bank, in the fi rst half of 2003, the Industry comprised 171 banks with Banco do Brasil leading the mainly fi nancial items.

Until March 2003, the whole banking industry reported total assets of R$1,254 billion, market funding (demand deposits, savings, interbank deposits, term depositsand open market funds) of R$612.3 billion and credit (loan operations, leasing operations and other credits, according to the National Monetary Council Resolution 2,682), of R$360.1 billion.

Banks in the Country

194 192 182

1999 12000 12001 12002 Mar/03

171 171

Source: Brazilian Central Bank

Total AssetsR$ billion

840

1999 2000 2001 2002 Mar/03

126

939

138

1,062

165

1,231

205

1,254

209

15.1% 14.7% 15.5% 16.5% 16.7%

Total Banking Industry

BB´s Market Share

BB

9Banco do Brasi l F i rst Hal f 2003

Demand DepositsR$ billion

42.0

1999 12000 12001 2002 Mar/03

11.0

50.8

15.4

57.4

18.8

76.5

24.3

64.0

20.3

Source: Brazilian Central Bank

26.2%30.4% 32.7% 31.8% 31.8%

Total Banking Industry

BB´s Market Share

BB

Credit*R$ billion

270.1

1999 12000 12001 2002 Mar/03

29.0

298.9

38.7

314.8

42.5

362.7

54.7

360.1

56.8

Source: Brazilian Central Bank*Loan and Leasing Operations

10.7%13.0% 13.5% 15.1% 15.8%

Total Banking Industry

BB´s Market Share

BB

The wide-ranging network and the largest banking industry customers base give BB the leadership in total assets (16.7% market share), in market funding (24.1% market share) and in credit (15.8% market share). Only in demand deposits, BB has 31.8% market share.

10 Banco do Brasi l F i rst Hal f 2003

Financial Performance

The Bank’s performance refl ects the goals established in the 2003 Corporate Strategy, as follows:

Create value to stockholders

Because of the Federal Financial Institutions Enhancement Program of June 2001, BB reached a higher profi tability level. In the fi rst half of 2003, Banco do Brasil reported net income of R$1,079 million, which was 31.1% higher than the same period in the prior year. This result is equivalent to a return on average shareholders’ equity of 22.7% and earnings per 1,000 shares of R$1.47.

Adequate relation between earnings and cost structure

Sustained growth in revenues and control of administrative expenses improved the coverage ratio, which measures how much of Personnel Expenses are covered by Service Revenues. In the fi rst semester of 2003, the Bank achieved a ratio of 85.7% compared to 82.7% in the same period of 2002.

Effi ciency ratio reached 55.4% in the fi rst semester of 2003, against 60.1% in the fi rst half of 2002.

Mitigate the Group’s risk exposure

In the fi rst half of 2003, BB improved its risk management by concentrating the Market/Liquidity Risk, Credit Risk and Operational Risk areas into one. The measure is aligned with guidelines set by the Brazilian Central Bank and by the New Basel Capital Accord recommendations.

11Banco do Brasi l F i rst Hal f 2003

Strengthen Customer Relationship

Banco do Brasil has the largest customer base in the Brazilian market. The strategy to increase its amount of customers is related to the synergy between Wholesale, Government and Retail Pillars, specially through pay roll agreements.

Service Revenues amounted R$2,561 million, a positive change of 18.2% over the same period of 2002. The customer base increased 15.0%, against a 27.9% increase in Customer relationship fees.

Public policy agent

Banco do Brasil is a nationwide and modern company. These attributes qualifi es BB as one of the main agents of the Federal Government. The Bank combines very well its commitment to society and its role as a profi table and competitive company.

BB is duly paid for the obligations assumed to implement Government economic growth programs. The Federal Government budget foresees the equalization of interest rates on loans in which the spread is incompatible with the profi tability expected by shareholders.

Socially Responsible

BB is concerned about being a socially responsible company. It has not only programs serving the society but also specifi c programs to serve its work force. The Bank understands that to guarantee a sustainable growth it is necessary to invest in society’s needs and in its employees satisfaction.

12 Banco do Brasi l F i rst Hal f 2003

Net IncomeR$ million

843974

1,082

1999 2000 2001 2002

2,028

8231,079

1H02 1H03

138,363

Total AssetsR$ million

126,454

165,120

1999 2000 2001 2002

204,595

169,910

205,762

Jun/02 Jun/03

Dividends/Interests on Shareholders’ EquityR$ million

236 258 265

1999 2000 2001 2002

579

307 322

1H02 1H03

Shareholders’ EquityR$ million

7,2717,965

8,747

1999 2000 2001 2002

9,1977,984

10,872

Jun/02 Jun/03

13Banco do Brasi l F i rst Hal f 2003

Shareholders

National Treasury 71.8Previ 13.8BNDESPar 5.8Treasury Stocks 1.5 Foreign Capital 1.1 Individuals 4.3Other Companies 1.2Other Pension Funds 0.5Total Shareholders 100.0

Multiples 1H02 1H03 Price/Earnings (12 months) 3.7 4.2 Price/Book Value 0.7 0.9 Market Capitalization - R$ million 5,866 9,582Book Value per 1,000 shares - R$ 11.21 14.85

Ibovespa (São Paulo Stock Exchange Index) increased 19.1% from June 2002 to June 2003, while BB shares (ticker symbol BBAS3) fi nished the period at a 66.4% increase.

Jul/0

2

BB Shares x Ibovespa - Index Jun/02 = 100

230

210

190

170

150

130

110

90

70

50

Jun/

03

Ibovespa

BBAS3

Dec

/02

14 Banco do Brasi l F i rst Hal f 2003

Customers

Banco do Brasil maintains its leadership in customer base in the Brazilian banking market, with 15.6 million individual customers and 1.1 million business customers.

Individuals In millions

1999 2000 2001 2002

10,35111,824

12,93514,398

Jun/02 Jun/03

15,644

13,592

BusinessesIn thousands

1,072949

755872 908

992

Jun/02 Jun/031999 2000 2001 2002

15Banco do Brasi l F i rst Hal f 2003

Retail

The Retail Pillar is responsible for operations with individuals and companies with annual turnover below R$10 million. Individuals are segmented in three levels of relationship with the Bank: Exclusivo (monthly income above R$4,000), Preferencial (monthly income between R$ 1,000 and R$4,000) and Pessoa Física (monthly income below R$1,000).

SegmentationCurrent Accounts per Level

1999 2000 2001 2002

Private Pension, Insurance and CapitalizationIn thousands

63.3%

Pessoa Física

29.9%

Preferencial

6.8%

Exclusivo

340264

492

1,007

641

383425

820

1,050949

1,020

1,144

Private Pension PlansVehicle Insurance Capitalization Securities

Jun/02 Jun/03

194

565

221

651

444

529

1999 2000 2001 2002

3.8

1.9

3.3

4.7

Credit CardsIn thousands

4.94.3

Jun/02 Jun/03

16 Banco do Brasi l F i rst Hal f 2003

Micro and Small Businesses

Micro and small businesses (MPEs) make up 98% of all companies in Brazil. One of the goals of Banco do Brasil is to be the primary partner of small businesses. To accomplish this, the Bank has given special attention to this segment and offers specifi c services and products to serve them. MPEs are companies with turnover below R$10 million p.a. These companies are served by the Retail Pillar network.

BB leads credit concession to this segment in the Brazilian market. Among the lines of credit available to these companies, BB Giro Rápido – a working capital credit line – deserves special attention. As of the fi rst half of 2003, BB Giro Rápido contracts reached R$2,072 million.

As a result of the strategies aimed at MPEs, the average number of products per customer of this segment increased from 2.8 to 4.7 year on year.

Jun/02 Sept/02 Dec/02 Mar/03 Jun/03

1.51.4

2.1

1.5

1.8

BB Giro RápidoR$ billion

2.8

Jun/02 Dec/02 Jun/03

4.7

Products per MPE

3.1

17Banco do Brasi l F i rst Hal f 2003

Wholesale

Banco do Brasil has a network of 54 Empresarial branches specialized in middle market and large sized businesses (annual turnover between R$10 million and R$100 million) and 17 Corporate branches to serve customers with annual turnover above R$100 million.

Wholesale credit operations have signifi cant participation in BB’s credit portfolio, outstanding in BB Vendor and Conta Garantida credit lines, with shares of 95.3% and 63%, respectively.

95.3

4.7

63

37

NorthActive Corporate branches –Empresarial branches 2

SoutheastActive Corporate branches 11Empresarial branches 33

BB Vendor% of total balance

Conta Garantida% of total balance

Wholesale

Others

NortheastActive Corporate branches 1Empresarial branches 4

MidwestActive Corporate branches 1Empresarial branches 2

SouthActive Corporate branches 4Empresarial branches 13

Active Corporate branches 17Empresarial branches 54

18 Banco do Brasi l F i rst Hal f 2003

Public Sector

The Public Sector Pillar has 38 branches and 843 specialized employees that provide solutions to all levels of government.

BB uses its great experience and relationship with the Public Sector to create taylor made products to government customers needs, such as:

• BB Conta Única - a package of automated solutions to help government institutions manage their cash fl ow and centralize their business with the Bank - Over 1.5 thousand contracts, with 51,709 accounts.

• FCO - Constitutional fund utilized to support productive investments in the Brazilian Midwest Region - BB granted R$595.4 million in the fi rst half of 2003, 68% in the rural sector and 32% in commercial businesses.

19Banco do Brasi l F i rst Hal f 2003

Asset Management

BB DTVM is a BB’s wholly owned subsidiary, which manages retail investment funds and institutional investors portfolios.

Banco do Brasil has been the leader in asset management in Brazil for eight years in a row. Nowadays, it has 18.7% market share.

Investment FundsR$ billion

59.5

Jun/02 Jun/03

78.4

17.7%19.2%

Managed PortfoliosR$ billion

5.0

Jun/02 Jun/03

4.8

10.3%12.8%

Asset ManagementR$ billion

1999 2000 2001 2002

64.5

33.5

48.0

61.466.2

83.2

13.4% 13.2%

17.4% 17.2%

18.7%

Jun/02 Jun/03

16.2%

Market Share

Total Assets

Market Share

Total Assets

20 Banco do Brasi l F i rst Hal f 2003

Agribusiness

Agribusiness is one of the most effi cient and competitive sectors of the Brazilian economy, contributing signifi cantly to trade balance, playing strategic role in the Brazilian economy and making Brazil a key global player in this area.

BB is responsible for 65% of all rural and agribusiness fi nancing in Brazil. In the fi rst half of 2003 the amount of these fl ows reached R$7.6 billion, representing an increase of 94.9% from last year.

As the offi cial agent of the Federal Government’s rural credit policy BB receives proper compensation revenues, as shown in the graphs.

Funds ContractedR$ billion

1999 2000 2001 2002

6.27.7

9.8

13.5

1H02 1H03

3.9

7.6

Compensation for SubsidiesR$ million

412

508

261

2001 2002

336

1H02 1H03

21Banco do Brasi l F i rst Hal f 2003

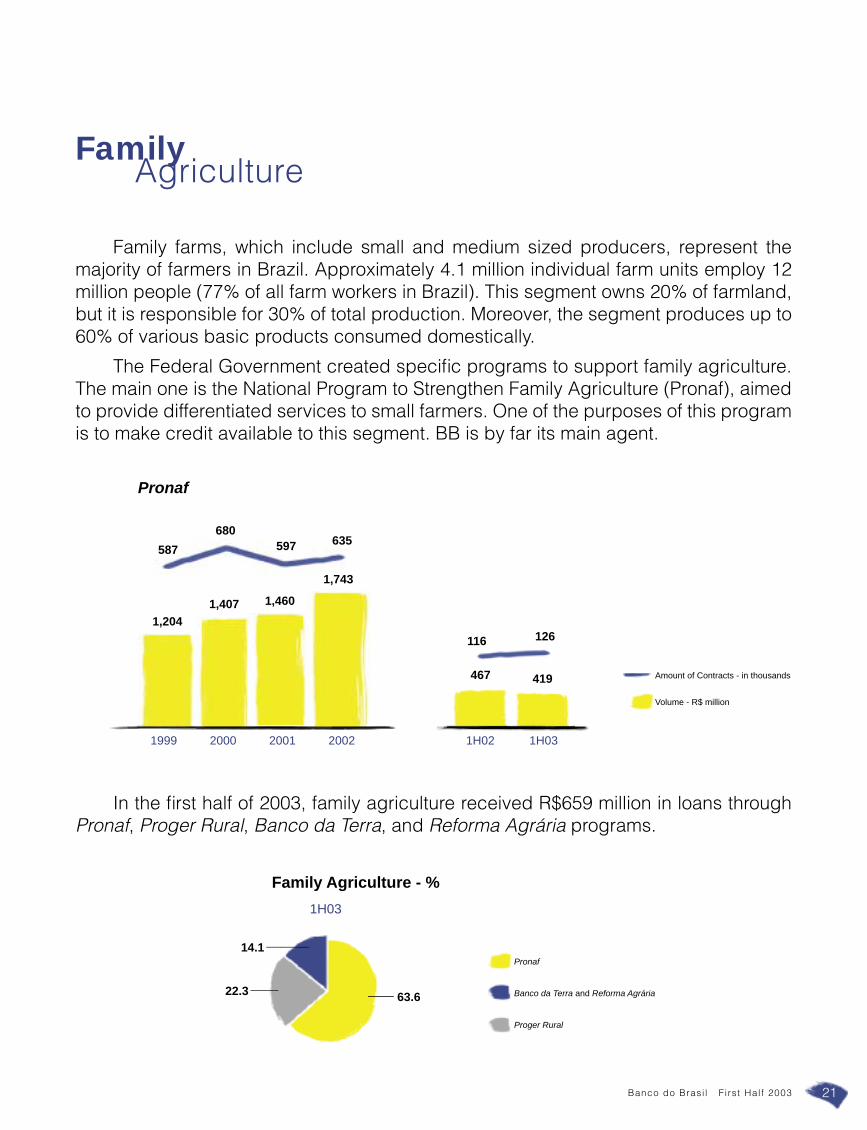

Family Agriculture

Family farms, which include small and medium sized producers, represent the majority of farmers in Brazil. Approximately 4.1 million individual farm units employ 12 million people (77% of all farm workers in Brazil). This segment owns 20% of farmland, but it is responsible for 30% of total production. Moreover, the segment produces up to 60% of various basic products consumed domestically.

The Federal Government created specifi c programs to support family agriculture. The main one is the National Program to Strengthen Family Agriculture (Pronaf), aimed to provide differentiated services to small farmers. One of the purposes of this program is to make credit available to this segment. BB is by far its main agent.

Volume - R$ million

Amount of Contracts - in thousands

Pronaf

1999 2000 2001 2002

587

116

680597 635

1261,204

467

1,407 1,460

1,743

419

1H02 1H03

In the fi rst half of 2003, family agriculture received R$659 million in loans through Pronaf, Proger Rural, Banco da Terra, and Reforma Agrária programs.

63.6

14.1

Family Agriculture - %

Pronaf

Proger Rural

Banco da Terra and Reforma Agrária22.3

1H03

22 Banco do Brasi l F i rst Hal f 2003

Trade Finance

In the fi rst six months of 2003, the volume of export and import operations reached US$15.4 billion, 46% higher than in the same period of 2002. BB is leader in export exchange, presenting 29.6% market share.

In the fi rst half of 2003, Advancements on Exchange Agreements (ACCs), and Advancements on Delivered Exchange Securities (ACEs) contracts have totaled US$3.5 billion, 21.6% superior than the same period of the previous year.

Approximately US$1.6 billion in exports were made possible by the Program for Export Financing (PROEX). This program is the most important source of funding for small and medium sized Brazilian companies involved in trade fi nance.

ProexUS$ billion

1999 2000 2001 2002

1.60.8

6.5

8.28.7

5.5

1H02 1H03

ACC/ACEUS$ billion

2000 2001 2002

5.1 5.3

1H02 1H03

2.93.5

5.5

23Banco do Brasi l F i rst Hal f 2003

Funding

The Bank’s strong nationwide presence and large customer base contributed to the growth and maintenance of the Bank’s leadership in total funding.

Banco do Brasil has entered into long term trade credit line agreements amounting to approximately US$913.7 million at June 30, 2003 with foreign banks and export credit agencies covering Brazilian imports from countries such as: Germany, Canada, Denmark, Spain, United States, Finland, France, Italy, Japan, Norway, Sweden, Switzerland and Venezuela. These credit lines are used to fi nance the import into Brazil of capital goods, machinery, equipment and services.

Balance (R$ million) Change %

Jun/02 Jun/03

Demand Deposits 18,319 21,170 15.6Savings 22,639 26,427 16.7Interbank Accounts 5,165 5,437 5.3Time Deposit 33,588 46,847 39.5Open Market Funds 37,508 41,468 10.6Total 117,219 141,348 20.6

US$ 100 MMGlobal Medium

Term Notes6.25% p.a.

1 year

Jan/28

US$ 120 MM

MT-100

7.26% p.a.

7 years

Mar/17

US$ 75 MMGlobal Medium

Term Notes6.375% p.a.

2 years

Apr/25

US$ 223 MMVISANET

Securitizationof receivables

fl ows

Jul/02

€ 150 MMGlobal Medium

Term Notes4.5% p.a.

1 year

Jul/07

The Bank placed some US$690 million in international issues in the fi rst half of this year. The main operations have included plain vanilla Eurobonds, securities (zero bonds), innovative securitization operations on future remittance fl ows as well as some structured deals.

24 Banco do Brasi l F i rst Hal f 2003

Securities

Banco do Brasil’s securities portfolio is the largest among banks in Brazil. As can be seen in the graph below, the portfolio has shown considerable improvement in the level of risk due to the reduction in the length of maturity. In June 2002, the total share of securities with maturity of over 360 days, amounted to 80.7%. In June 2003 this participation decreased to 78.4%.

Analyzing the maturity of securities in years, it is to notice that the growth in the participation of securities with maturity of up to fi ve years has been constant while securities with maturity of over ten years has decreased.

Balance (R$ million)Jun/02 Share% Dec/02 Share% Jun/03 Share%

Available for Trading 3,325 4.8 3,585 5.1 2,104 2.9Available for Sale 40,377 58.9 41,303 58.2 42,515 58.4Held to Maturity 24,542 35.8 25,763 36.3 27,640 38.0Derivates 346 0.5 292 0.4 487 0.7Total 68,591 100.0 70,943 100.0 72,746 100.0

Securities Portfolio

Composition of the Securities Portfolio by Maturity (no. of days) - %

Jun/02

1.5

80.7

4.8

78.4

9.6

Jun/03

4.17.9

Until 30

31 to 180

181 to 360

Over than 360

13.0

25Banco do Brasi l F i rst Hal f 2003

Credit

Banco do Brasil continues to expand its credit portfolio, focusing on operations with diversifi ed risk and low operating costs.

CreditRisk

Banco do Brasil (R$ million) BankingIndustryVolume Required

Allowance %

AA 14,848 0 21.7 26.0A 29,578 148 43.1 33.2B 14,158 142 20.6 17.1C 4,592 138 6.7 10.2D 2,050 205 3.0 4.8E 588 176 0.9 1.9F 383 191 0.6 1.1G 306 214 0.4 1.6H 2,160 2,160 3.1 4.1

Total 68,662 3,374 100.0 100.0

Risk Level of Credit Operations - June 2003

BB’s Credit Portfolio - %

22.9

21.4

Jun/02

23.9

16.8

Jun/03

31.3

2.8

20.8

21.8

12.3

Others

Abroad

International

Agribusiness11.0

Commercial

12.6

Retail

2.3

26 Banco do Brasi l F i rst Hal f 2003

25.4

43.3

31.3

Credit vs Total Assets - %

Mar/02 Jun/02 Sept/02 Dec/02 Mar/03 Jun/03

27.5

38.6

33.9

25.6

42.2

32.2

25.2

44.2

30.6

24.1

44.2

31.7

27.4

42.5

30.1

Other Assets

Credit Assets

Securities and Interbank Funds

Retail Credit PortfolioR$ billion

1999 2000 2001 2002

2.2

1.1

0.00.5

1.2

4.7

1.4

0.0

0.8

1.8

7.2

2.3 2.11.5

1.2

6.9

2.01.4

1.0 0.9

6.7

1.91.5 1.4

1.0

6.4

1.81.3

1.0 0.8

CDC Automated Consumer Credit

Overdraft Accounts

BB Automated Working Capital

Credit Cards

Others

Jun/02 Jun/03

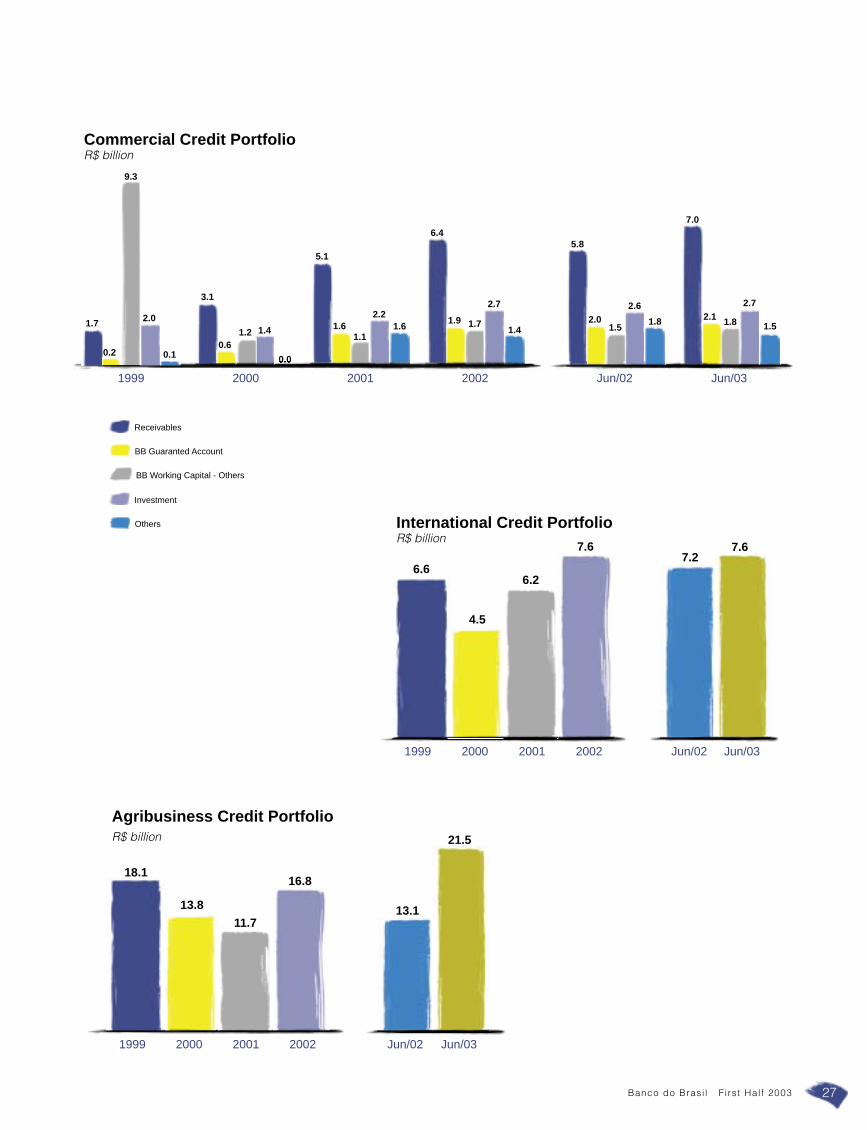

27Banco do Brasi l F i rst Hal f 2003

Agribusiness Credit Portfolio R$ billion

1999 2000 2001 2002

13.1

18.1

13.811.7

16.8

21.5

Commercial Credit PortfolioR$ billion

1999 2000 2001 2002

5.1

1.61.1

2.21.6

6.4

1.9 1.7

2.7

1.4

5.8

2.01.5

2.61.8

7.0

2.1 1.8

2.7

1.5

3.1

0.61.2 1.4

0 0

1.7

0.2

2.0

0.1

9.3

Receivables

BB Guaranted Account

BB Working Capital - Others

Investment

Others

Jun/02 Jun/03

International Credit PortfolioR$ billion

1999 2000 2001 2002

7.26.6

4.5

6.2

7.6 7.6

Jun/02 Jun/03

Jun/02 Jun/03

28 Banco do Brasi l F i rst Hal f 2003

2125 22 22 20 20

Distribution Network

Banco do Brasil has the largest distribution network in Brazil, with 12,755 points of service nationwide.

PAA - Advanced Service Post: these are service locations utilized in towns without a bank. It requires a small group of employees and provides ATM services;PAB - Banking Service Post: this type of unit is located inside the facilities of companies or government offi ces. This service on employee and provides ATM services;PAE - Electronic Service Point: Service are provided by ATMs;PAP - Payment and Collection Post: this type of service is mainly located in government offi ces (municipalities). Service is provided by employees and ATMs.

Points of Service

1Q02 2Q02 3Q02 4Q02 1Q03 2Q03

410

1,559

3,050

6,130

408

1,599

3,077

6,467

411

1,601

3,134

7,007

418

1,595

3,164

7,135

421

1,606

3,183

7,315

421

1,598

3,209

7,507

PAAPAP PAEBranchesPAB

Points of Service by Region

North

Points of Service 890

7%

Midwest

Points of Service 1,431

11.2%

South

Points of Service 2,585

20.3%

Northeast

Points of Service 3,080

24.1%

Southeast

Points of Service 4,769

37.4%

Points of Service 12,755 100%

29Banco do Brasi l F i rst Hal f 2003

BB extends its services through a network partnership with local businesses known as Banking Agents, such as supermarkets and drugstores, where BB’s customers are able to pay water, electricity, telephone and other bills. The Banking Agents network fi nished the fi rst half with 1,712 stores over Brazil. This network will be responsible to serve BB micro-credit subsidiary customers.

Still, Banco do Brasil counts on a network abroad distributed throughout 21 countries, and composed of 18 branches, 6 sub-branches, 9 business units, and 4 subsidiaries.

Also, in order to offer effi cient support to its businesses BB has 1,745 correspondent banks around the world.

Argentina • Bolivia • Cayman Islands • Chile • China • France • Germany • Hong Kong • Italy • Japan • Mexico

Netherlands • Panama • Paraguay • Peru • Portugal • Spain • United Kingdom • Uruguay • USA • Venezuela

Distribution Network Abroad

30 Banco do Brasi l F i rst Hal f 2003

Automated Channels

Besides its distribution network, BB extends its services through automated channels, such as Automated Teller Machines – ATM network, Internet, and Gerenciador Financeiro.

BB’s automated teller machine network is the largest in Latin America, with 34,125 machines.

% transactions in ATMs

72.173.9 73.8

Jan Feb Mar Apr May Jun

74.7 76.273.7

84.2 84.6 84.4 84.9 85.084.1

80.6 81.4 80.5 81.5 82.580.7

1H01

1H02

1H03

Automated Teller Machines

1999 2000 2001 2002

34,12532,936

24,545

30,14932,287 33,645

Jun/02 Jun/03

31Banco do Brasi l F i rst Hal f 2003

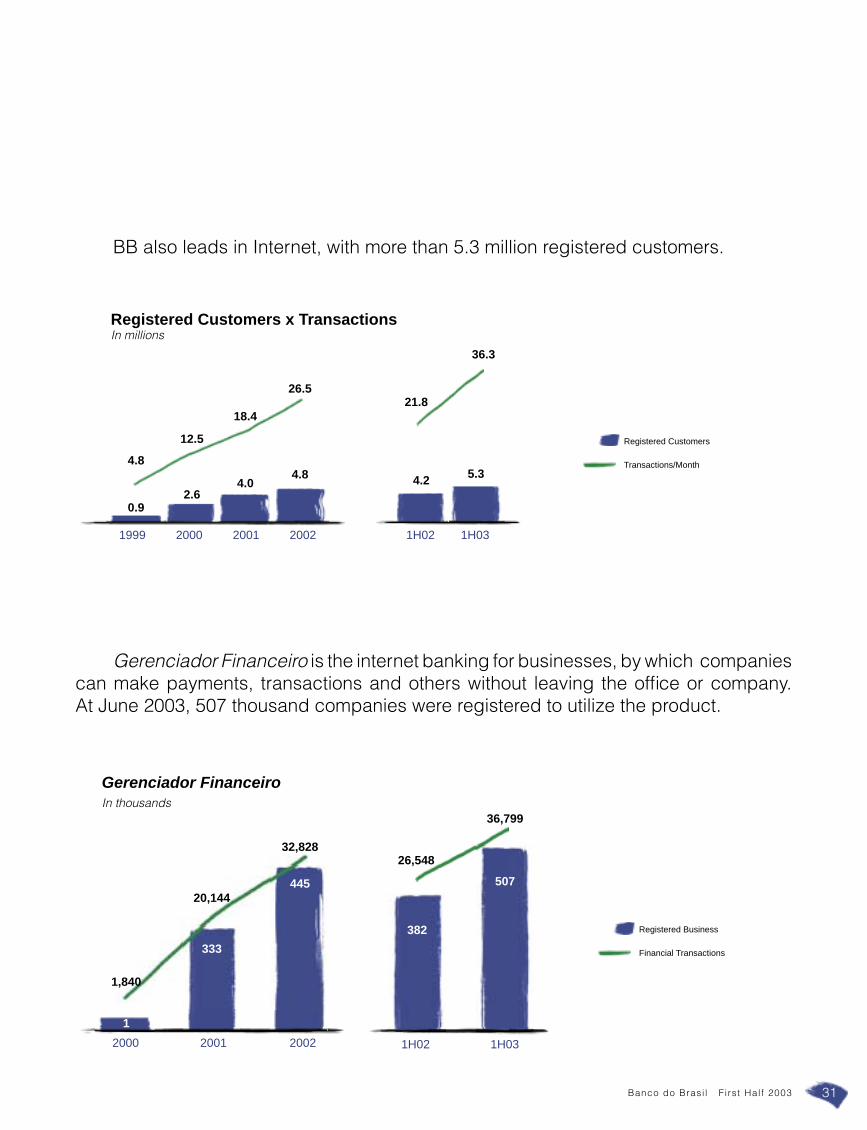

BB also leads in Internet, with more than 5.3 million registered customers.

Gerenciador Financeiro is the internet banking for businesses, by which companies can make payments, transactions and others without leaving the offi ce or company. At June 2003, 507 thousand companies were registered to utilize the product.

Registered Customers x TransactionsIn millions

1999 2000 2001 2002

5.34.2

0.92.6

4.04.8

4.8

12.5

18.4

26.5

36.3

21.8

Gerenciador FinanceiroIn thousands

1H02 1H02 1H0320012000 2002

333

445

1

382

50720,144

32,828

1,840

26,548

36,799

Registered Customers

Transactions/Month

Registered Business

Financial Transactions

1H02 1H03

32 Banco do Brasi l F i rst Hal f 2003

Human Resources

Banco do Brasil is committed with its work force by supporting professional development and quality of life.

Up to 30 years

31 to 40 years

41 to 50 years

Above 50 years

Age Bracket - %

Tenure - %

Level of Education - %

44.5

44.1

7.7 3.7

30.5

6.2

32.7

30.642.8

6.9

20.3 30.0

Up to 5 years

From 6 to 10 years

From 11 to 20 years

Above 20 years

Specialization, Master or Doctor's Degree

Holders of Bachelor's Degree

High School

Workforce

1999 2000 2001 2002

69,437

12,243

79,474

10,781

77,952

10,199

78,619

9,540

78,122

11,880

78,201

12,267

Employees

Interns

Jun/02 Jun/03

Elementary School

33Banco do Brasi l F i rst Hal f 2003

Social Responsibility

Banco do Brasil carries out special programs to serve its work force and Brazilian society.

The program Adolescente Trabalhador seeks to form ethical and professional values in low income adolescents. In June, 2003 the program had 3,305 teenagers.

The Voluntariado BB program supports the volunteering culture among employees and their relatives, contributing to improve communities quality of life. Over 10 thousand people are signed up for the Volunteer program.

As the primary partner of the Federal Government in the Fome Zero program against hunger, BB created a specifi c group to structure the Company’s role on it, and to develop the actions proposed, seeking to integrate them from a stand point of a few defi ned focuses: promoting jobs and revenues, nutritional assurance and empowerment of local resources. Also, in the fi rst half of 2003, BB collected and distributed over 1 thousand ton of food.

The Bank has also improved its relations with employees by incorporating new parameters for remuneration and professional growth, investing in training programs, benefi ts other than those provided by Social Security and healthcare system. BB also offers a special profi t-sharing program.

34 Banco do Brasi l F i rst Hal f 2003

Banco do Brasil Figures

Balance Sheet ItemsR$ million

Jun/02 Jun/03 Change - %

Assets 169,910 205,762 21.1Available funds 7,353 6,683 (9.1)Short-term interbank investments 4,875 12,348 153.3Marketable securities 68,591 72,746 6.1

Securities for trading 3,325 2,104 (36.7)Securities available for sale 40,377 42,515 5.3Securities held to maturity 24,542 27,640 12.6Financial derivatives 346 487 40.5

Interbank accounts 11,011 22,110 100.8Intrabank accounts 227 308 35.7Loans 46,473 56,654 21.9

Loans 27,350 32,422 18.5(Allowance for loan losses) (2,691) (3,498) 30.0

Leasing 70 32 (53.9)Leasing and sub-leasing receivables 480 349 (27.3)(Unearned lease income) (389) (303) (22.1)(Allowance for lease losses) (21) (14) (36.1)

Other receivables 26,578 30,600 15.1Other assets 244 234 (3.9)Permanent assets 4,489 4,048 (9.8)Liabilities and Shareholders’ Equity 169,910 205,762 21.1Deposits 79,710 99,881 25.3

Demand deposits 18,319 21,170 15.6Savings deposits 22,639 26,427 16.7Interbank deposits 5,165 5,437 5.3Time deposits 33,588 46,847 39.5

Money market borrowing 37,508 41,468 10.6Funds from acceptances and securities placed 831 1,071 28.9Interbank accounts 2,801 2,676 (4.5)Intrabank accounts 915 813 (11.2)Foreign borrowing 10,925 8,714 (20.2)Domestic onlending – offi cial institutions 4,705 6,134 30.4Foreign onlending 2 2 (10.6)Financial derivatives 704 702 (0.2)Other accounts payable 23,737 33,333 40.4Unearned income 87 97 11.6Shareholders’ equity 7,984 10,872 36.2

35Banco do Brasi l F i rst Hal f 2003

Income StatementR$ million

1H02 1H03 Change - %

Financial intermediation revenues 15,128 16,476 8.91Loans 6,413 7,654 19.4Leasing 54 44 (17.6)Securities 5,568 6,882 23.6Financial derivatives (615) (216) (64.9)

Foreign exchange portfolio 2,937 - -Compulsory investments 771 2,112 174.1

Financial intermediation expenses (11,878) (12,502) 5.3Money market funds (5,776) (9,093) 57.5Borrowing, assignments, and onlending (4,786) (652) (86.4)Foreign exchange portfolio - (1,103) - Provision for doubtful loans (1,317) (1,654) 25.6

Gross income from fi nancial intermediation 3,250 3,974 22.3Other operating income (expenses) (1,860) (1,823) (2.0)

Service revenues 2,167 2,561 18.2Personnel expenses (2,620) (2,990) 14.1Other administrative expenses (1,823) (2,125) 16.5Taxes (374) (534) 42.8Equity interest in income (loss) of affi liates and subsidiaries 967 (1,036) (207.1)Other operating income 802 4,908 512.1Other operating expenses (979) (2,608) 166.3

Operating income 1,390 2,151 54.7Non-operating income 42 92 118.3Income before taxes 1,432 2,243 56.6

Income and social contribution taxes (532) (1,096) 105.9Statutory profi t sharing (77) (68) (10.9)

Net income 823 1,079 31.1

36 Banco do Brasi l F i rst Hal f 2003

Ratios (Income Statements with Reallocations)

1H02 1H03

Profi tabilityNet Income per 1,000 shares (R$) 1.16 1.47ROE - annualized 20.6 22.7ROA - annualized 0.99 1.05Gross Financial Margin / Assets (-) Permanent - % 7.13 7.61Gross Financial Margin / Profi table Assets* - % 8.99 9.50

ProductivityEffi ciency Ratio - % 60.1 55.4Service Fees / Personnel Expenses - % 82.7 85.7Service Fees / Administrative Expenses - % 48.2 49.5Personnel Expenses per Employee - R$ 29,721 33,128Employees per (Branches + PAA + PAB) 17.3 17.3

Credit Portfolio QualityCredit Risk Provision / Credit Portfolio - % 5.2 5.6Loans past due more than 60 days/total loan portfolio % 3.5 3.2

Capital StructureLeverage x 21.3 18.9BIS Ratio - % 11.6 13.8

Capital MarketPrice / Earnings (12 months) 3.66 4.20Price / Book Value 0.73 0.88Market Capitalization - R$ millions 5,866 9,582Book Value per 1,000 shares - R$ 11.21 14.85

37Banco do Brasi l F i rst Hal f 2003

Effi ciency Ratio - %

60.9 58.057.7

67.769.269.770.7

59.3

1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03

54.156.7

86.077.179.3

63.869.267.969.979.4

Coverage Ratio Service Revenues/Personnel Expenses - %

1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03

90.7

80.7

11.1

9.2 8.8

1998 1999 2000 2001 2002

12.7

Capital Adequacy BIS Ratio (%)

12.2 11.6

13.8

Jun/02 Jun/03

38 Banco do Brasi l F i rst Hal f 2003

Cássio Casseb LimaPresident

Organizational Structure Co

mm

erci

al

Board of Directors

General Shareholders Meeting

Fiscal Council

Rossano Maranhão PintoVice-presidentInternational

and CommercialBusinesses

Inte

rnat

iona

l

Dist

ribut

ion

Reta

il

Gov

ernm

ent

Agrib

usin

ess

Fina

nce

Capi

tal M

arke

tsan

d In

vest

men

ts

Infra

stru

ctur

e

Tech

nolo

gy

Cont

rolli

ng

Cred

it

Acco

untin

g

Ris

k M

anag

emen

t

Cred

it Re

cove

ry

Hum

an R

esou

rces

Empl

oyee

Rel

atio

ns

and

Soci

al-E

nviro

nmen

t R

espo

nsib

ility

Mar

ketin

g

Stra

tegy

and

Org

aniz

atio

n

Lega

l

Exec

utiv

e Se

cret

aria

t

Audi

t

Inte

rnal

Con

trols

SoftwareDevelopment

Investor RelationsMicro and Small

Businesses Management

Edson Machado Monteiro

Vice-presidentRetail,

Services andDistribution

Ricardo Alves da ConceiçãoVice-president

Rural and Agro-industrial Businesses and

Government Affairs

Luiz Eduardo Franco de AbreuVice-president

Finance, Capital Markets

and Investor Relations

José Luiz de Cerqueira César

Vice-president Technology andInfrastructure

Adézio de Almeida LimaVice-presidentCredit and Risk

Management

Luiz Oswaldo Sant’lago Moreira de Souza

Vice-president Human Resources

and Social-Enviroment Responsability Affairs

Inte

rnal

Aud

it

Directors

General Managers

Manager

InformationTechnology

Board of Directors

Bernard Appy Chairman Federal Government

Cássio Casseb Lima Vice-Chairman Federal Government

José Carlos Rocha Miranda Member Federal Government

Tarcísio José Massote de Godoy Member Federal Government

Carlos Augusto Vidotto Member Minority Shareholders

Francisco Augusto da Costa e Silva Member Minority Shareholders

João Carlos Ferraz Member Minority Shareholders

Fiscal Council

Marcus Pereira Aucélio President Federal Government

Vacant Member Federal Government

Satomi Iura Member Minority Shareholders

Vicente de Paulo Barros Pegoraro Member Minority Shareholders

João Batista Nogueira Member Minority Shareholders

39Banco do Brasi l F i rst Hal f 2003

BB SecuritiesBB Turism

BB Investment

Bank

BB AG.Viena

BBLeasing Co. Ltd.

BB Insurance

Broker

Brasilian American

Merchant BanksBB CardsCobra BB Leasing

Banco do Brasil(Multiple Bank)

Wholly Owned Subsidiaries

Group Structure

BB DTVM Asset

Management

Maxblue AliançaBrasil Brasilcap Brasilprev Brasilsaúde Brasilseg Cibrasec SBCE

Brasilveículos

Affi liated Companies

40 Banco do Brasi l F i rst Hal f 2003

Argentina - Buenos Aires Branch Address: Calle Sarmiento, 487 esquina San Martin C1041AAI - Federal Capital - Argentina Phone: 54 + 11 + 40002727 e-mail: [email protected]

Bolivia - La Paz Branch Address: Avenida 16 de julio, 1642 , Prado Central - La Paz - Bolivia Phone: 591 + 2 + 2310909 e-mail: [email protected]

Cayman Islands - Grand Cayman Branch Address: Elizabethan Square, Phase III Building-4th fl oor, Sheden Road George Town -Grand Cayman Islands Cayman Islands Phone: 1 + 345 + 9495907 e-mail: [email protected]

Chile - SantiagoBranchAddress: Avenida Apoquindo, 3001, Piso 1Las Condes - 6760342 - ChilePhone: 56 + 2 + 3363001e-mail: [email protected]

China - ShanghaiNot operational yet

France - ParisBranchAddress: 4, Avenue de La Grande Armée75017 - FrancePhone: 33 + 1 + 40535500e-mail: [email protected]

Germany - Frankfurt Branch Address: Eschersheimer Landstrasse 55 60322 - AM - GermanyPhone: 49 + 69 + 299090 e-mail: [email protected]

Hong Kong - Hong Kong Business Unit Address: Unit 3601, 36/F., Tower 2, Lippo Centre, 89 Queensway, Admiralty Hong Kong - Hong KongPhone: 852 + 25216411 e-mail: [email protected]

Italy - Milan Branch Address: Piazza Castello, 1 , 3º PianoCAP: 20121 - Centro20123 - Milan - MI - ItalyPhone: 39 + 02 + 8825201e-mail: [email protected]

Italy - RomeBusiness UnitAddress: Via Barberini, 29 , 4° Piano00187 - RM - ItalyPhone: 39 + 06 + 4880707e-mail: [email protected]

Distribution Network AbroadBranches, Sub-Branches and Business Units

Japan - GifuSub-Branch Address: Asahi Plaza Minokamo Station Core Offi ce 101, Minokamo-shi, Ota-cho 2591-1 Gifu-Ken - Japan Phone: 81 + 574 + 245568 e-mail: [email protected]

Japan - Gunma Sub-Branch Address: Bandou Building , 1319-1, Iida-cho Ota-shi - Gunma-ken - Japan Phone: 81 + 276 + 466511 e-mail: [email protected]

Japan - Hamamatsu Sub-Branch 430-7701 Shizuoka-ken, Hamamatsu-shi, Itaya-machi 111-2 Hamamatsu Act Tower 1FPhone: 81 + 53 + 4526511 e-mail: [email protected]

Japan - Ibaraki Sub-Branch Address: Shirai Buiding 2909-1, Mitsukaido-shi, Fuchigashira-Machi Ibaraki-Ken - Japan Phone: 81 + 297 + 306511 e-mail: [email protected]

Japan - NaganoSub-BranchAddress: Atago Mansion 101 , Ueda-shi, Chuo Higashi 1-5Nagano-Ken - JapanPhone: 81 + 268 + 286512 e-mail: [email protected]

Japan - NagoiaSub-BranchAddress: Chuo Fushini BDG 3-2 , Nishiki 1- Chome, NAKA-KUAichi-Ken - 460-0003 - JapanPhone: 81 + 52 + 2024611e-mail: [email protected]

Japan - TokyoBranchAddress: New Kokusai Building 3-4-1 , MarunouchiChiyoda ku - 100-0005 - Japan - TokyoPhone: 81 + 3 + 32136511e-mail: [email protected]

Mexico - Mexico City Business Unit Address: Calle Campos Elíseos, 345, piso 6o., Colônia Chapultepec Polanco11560 - Ciudad del Mexico D.F. - Mexico Phone: 52 + 55 + 52817245e-mail: [email protected]

Netherlands - Amsterdam Branch Address: Stadhouderskade 2 , 2o. fl oor Downtown 1054 ES - Netherlands Phone: 31 + 20 + 5241111 e-mail: [email protected]

Panama - Panama CityBranchAddress: Calle Elvira Mendez, Edifício Interseco Nr. 10, Planta BajaCampo Alegre - Zona 7 - PanamaPhone: 507 + 2636566e-mail: [email protected]

Paraguay - Asunción Branch Address: Calle Oliva Y Nuestra Senora de La Asunción Asunción - Paraguay Phone: 595 + 21 + 490121 e-mail: [email protected]

Paraguay - Ciudad del Este Branch Address: Calle Nanawa, 107, Esquina Monsenhor Rodrigues - CentroCiudad del Este - Alto Paraná - Paraguay Phone: 595 + 61 + 500319 e-mail: [email protected]

Peru - Lima Business Unit Address: Av. Camino Real 348 - Piso 9 , Torre El Pilar San Isidro 27 - Peru Phone: 51 + 1 + 2124230 e-mail: [email protected]

Portugal - LisbonBranch Address: Praça Marquês de Pombal, 16 1269-134 - Portugal Phone: 351 + 21 + 3585000 e-mail: [email protected]

Spain - Madrid Branch Address: Calle José Ortega y Gasset, 29 - 1ª Planta, Edifi cio Beatriz - Madri 28006 - Spain Phone: 34 + 91 + 4232500 e-mail: [email protected]

United Kingdom - London Branch Address: 34 King Street, London EC2V 8ES - United Kingdom Phone: 44 + 20 + 76067101 e-mail: [email protected]

Uruguay - Montevideo Branch - In liquidation process Address: 25 de Mayo, 506 - Esquina Treinta y Tres11.000 - UruguayPhone: 598 + 2 + 9170318 Fax: 598 + 2 + 9170299

USA - ChicagoBusiness Unit Address: 2 North La Salle Street-Suite 2005 - IL - USA Phone: 1 + 312 + 2369766 e-mail: [email protected]

USA - Los Angeles Business Unit Address: 811, Wilshire Boulevard 90017 - CA - USA Phone: 1 + 213 + 688 2996 e-mail: [email protected]

USA - Miami Branch Address: 2 S. Biscayne Boulevard , Suite 3870 33131 - FL - USA Phone: 1 + 786 + 4374444 e-mail: [email protected]

USA - New YorkBranchAddress: 600 Fifth Avenue, Third Floor , Rockfeller CenterNew York - 10020 - NY - USAPhone: 1 + 212 + 6267000e-mail: [email protected]

USA - WashingtonBusiness UnitAddress: 1801, K Street - N.W.- Suite 71020006 - Washington - DC - USAPhone: 1 + 202 + 8570320e-mail: [email protected]

Investor Relations Division

Address: SBS – Ed.Sede III – 17th fl oor70073-901 – Brasília (DF) – BrazilPhone: 55 (61) 310.5920Fax: 55 (61) 310.3735e-mail: [email protected]

Venezuela - Caracas Business Unit Address: Av. Francisco de Miranda , Centro Lido - Piso 09, Ofi cina 93A - Torre A El Rosal 1067-A - Miranda - Venezuela Phone: 58 + 212 + 9522674 e-mail: [email protected]

SUBSIDIARIES

BAMB - Brazilian American Merchant BankAddress: C/O - International DivisionGerin/DIOPB - SBS Qd.1 Bl.C Lote 32 Ed.Sede III - 12° andar70073-901 - DF - Brasilia - BrazilPhone: 1 + 61 + 3104504e-mail: [email protected]

BB - A.G. VienaAddress: Tegetthoffstrasse 4A-1010 - AustriaPhone: 43 + 1 + 51266630e-mail: [email protected]

BB-Leasing Company LtdAddress: C/O - International DivisionGerin/DIOPB - SBS Qd.1 Bl.C Lote 32 Ed.Sede III - 12° andar70073-901 - DF - Brasilia - BrazilPhone: 1 + 61 + 3104504e-mail: [email protected]

BB-SecuritiesAddress: 7th Floor, 16 St. Martins Le Grand LondonEC1A 4NA - United KingdomPhone: 44 + 207 + 3675800Fax: 44 + 207 + 7960859e-mail: [email protected]

CONTACT LIST

Banco do BrasilSBS – Ed.Sede III – 24th fl oor70073-901 – Brasília (DF) – Brazilwww.bb.com.br

PresidencyPhone: 55 (61) 310.3400Fax.: 55 (61) 310.2563

Finance, Capital Markets and Investor Relations VPPhone: 55 (61) 310.3406Fax.: 55 (61) 310.2561

International and Commercial Business VPPhone: 55 (61) 310.3406Fax.: 55 (61) 310.2561

International Division Phone: 55 (61) 310.4500Fax: 55 (61) 310.2444

International Division - Financial Institutions Department Phone: 55 (11) 3066.9081Fax: 55 (11) 3066.9089

Top Related