Languages

Pages

Legal

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 1/15

FINANCIAL ANALYSIS

of THE COMMERCIAL BANK

“Banca Sociala”

Period 2008-2010

Made by:

Chisinau 2011

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 2/15

In this year,2011,”Banca sociala” accomplishes 20 years of activity. In all this time,

the bank passed through different periods- good ones ,not very good ones, even difficult

ones. But all this periods served for the future development.

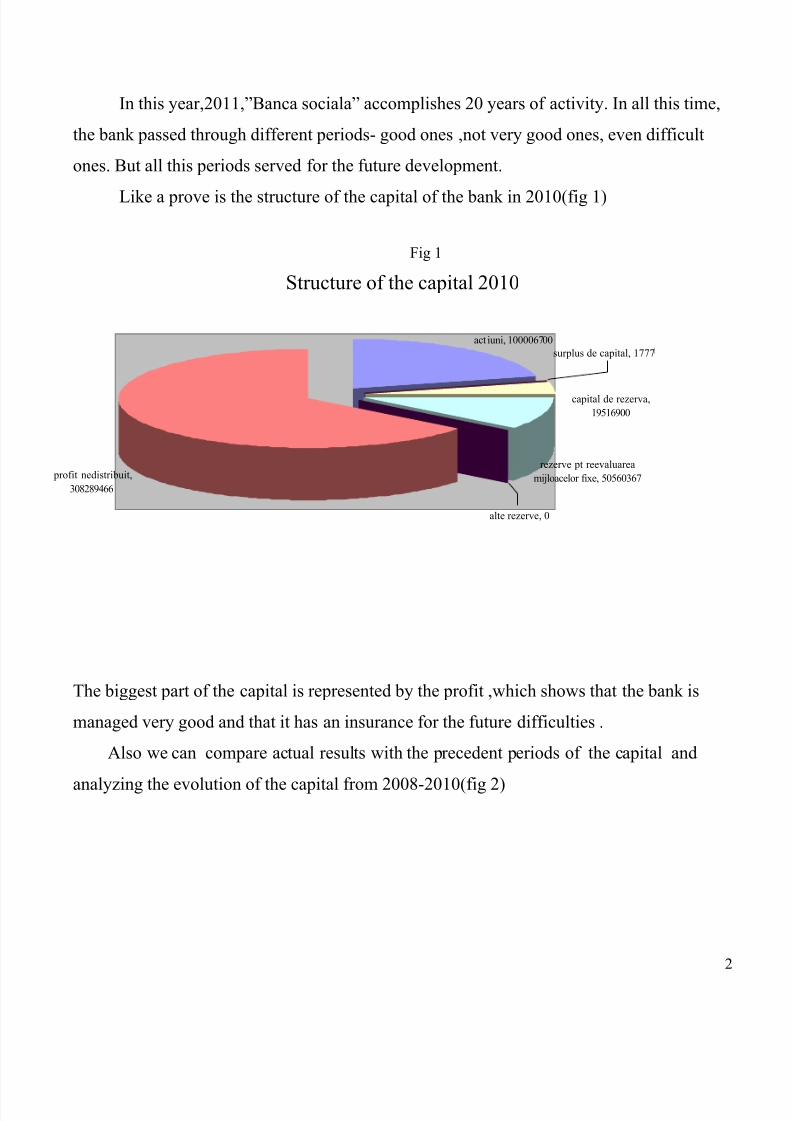

Like a prove is the structure of the capital of the bank in 2010(fig 1)

Fig 1

Structure of the capital 2010

profit nedistribuit,

308289466

act iuni, 100006700

rezerve pt reevaluarea

mijloacelor fixe, 50560367

alte rezerve, 0

surplus de capital, 1777

capital de rezerva,

19516900

The biggest part of the capital is represented by the profit ,which shows that the bank is

managed very good and that it has an insurance for the future difficulties .

Also we can compare actual results with the precedent periods of the capital and

analyzing the evolution of the capital from 2008-2010(fig 2)

2

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 3/15

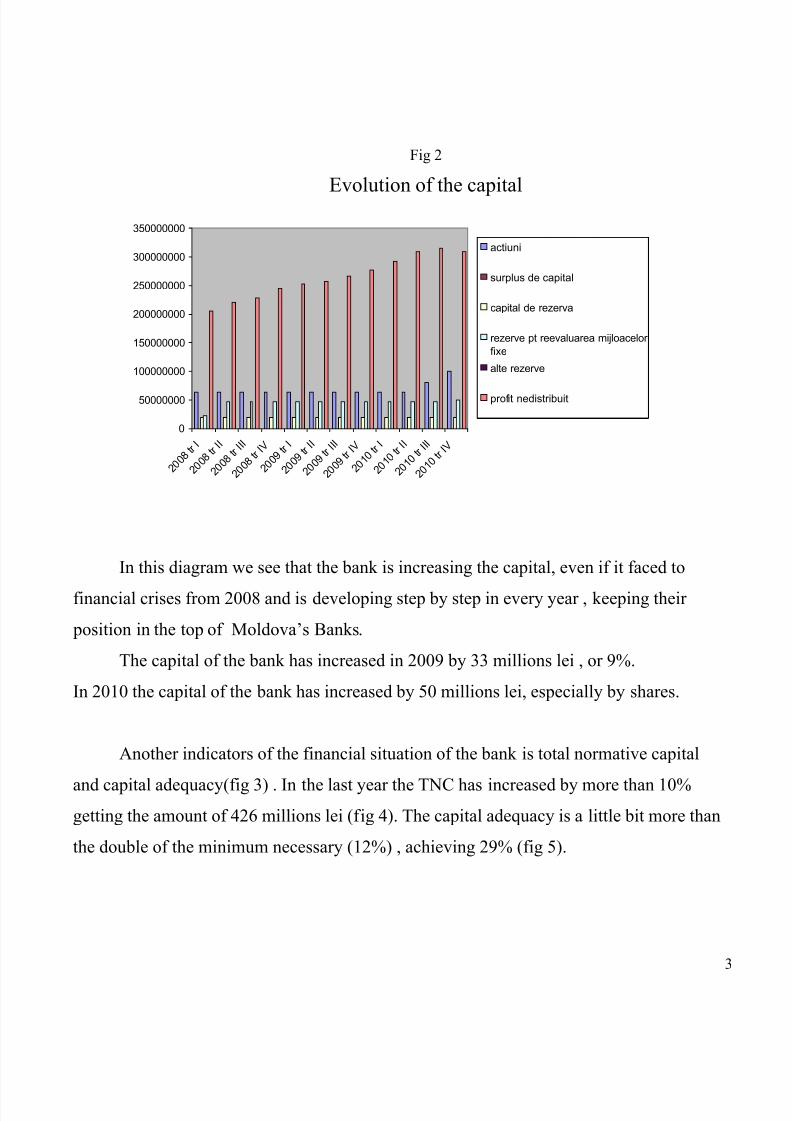

Fig 2

Evolution of the capital

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

2 0 0 8

t r I

2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 9

t r I

2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 1 0

t r I

2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

actiuni

surplus de capital

capital de rezerva

rezerve pt reevaluarea mijloacelor

fixe

alte rezerve

profit nedistribuit

In this diagram we see that the bank is increasing the capital, even if it faced to

financial crises from 2008 and is developing step by step in every year , keeping their

position in the top of Moldova’s Banks.

The capital of the bank has increased in 2009 by 33 millions lei , or 9%.

In 2010 the capital of the bank has increased by 50 millions lei, especially by shares.

Another indicators of the financial situation of the bank is total normative capital

and capital adequacy(fig 3) . In the last year the TNC has increased by more than 10%

getting the amount of 426 millions lei (fig 4). The capital adequacy is a little bit more than

the double of the minimum necessary (12%) , achieving 29% (fig 5).

3

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 4/15

Fig 3

Denumirea

indicatorilor

Normativ Perioada

2008 2009 2010Capital normative

total(mii lei)

X 331111 362439 426151

Capital de gradul I 100000 331111 362439 426151

Capital de gradul

II

X 0 0 0

Suficienta

capitalului ponderat

la risc(%)

>=12% 25.02% 26.19% 29.10%

Fig 4

The evolution of the total normative capital

0

50000

100000

150000200000

250000

300000

350000

400000

450000

2008 2009 2010

capital

normativ total

4

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 5/15

Fig 5

Capital adequacy

0

5

10

15

20

25

30

35

4045

2008 2009 2010

suficientacapitalului

>12 %

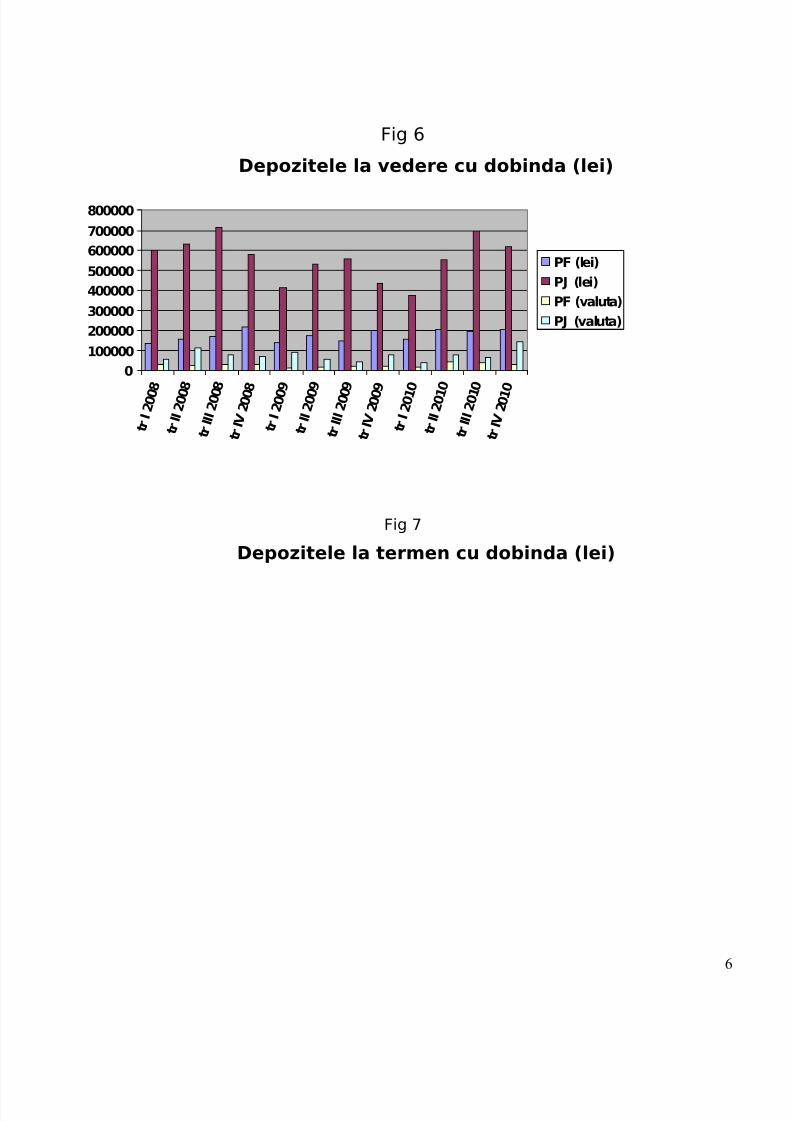

One of the premises of ensuring the long-term durable

development is attraction of the deposits. At this chapter the portfolio of

deposits is wade registering sight deposits, time deposits for individuals,

for legal entities .

First type are sight deposits with interest rate. Most of all are

interested of this type legal entities registering an increase by almost

100000 lei. Individuals have a rise of 50000 lei .(fig 6).

Also the bank is providing time deposits of which more interested

are individuals. In 2010 we have good results even if at the end of the

year the amount is decreasing in comparison with the start of the year

by 150000 lei (fig 7).

5

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 6/15

Fig 6

Depozitele la vedere cu dobinda (lei)

0

100000

200000

300000

400000

500000

600000

700000

800000

t r I 2 0 0 8

t r I I 2 0 0 8

t r I I I 2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I 2 0 0 9

t r I I I 2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I 2 0 1 0

t r I I I 2 0 1 0

t r I V

2 0 1 0

PF (lei)

PJ (lei)

PF (valuta)

PJ (valuta)

Fig 7

Depozitele la termen cu dobinda (lei)

6

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 7/15

0

50000

100000150000

200000

250000

300000

t r I 2 0 0 8

t r I I 2 0 0 8

t r I I I 2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I 2 0 0 9

t r I I I 2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I 2 0 1 0

t r I I I 2 0 1 0

t r I V

2 0 1 0

PF (lei)

PJ (lei)

PF (valuta)

PJ (valuta)

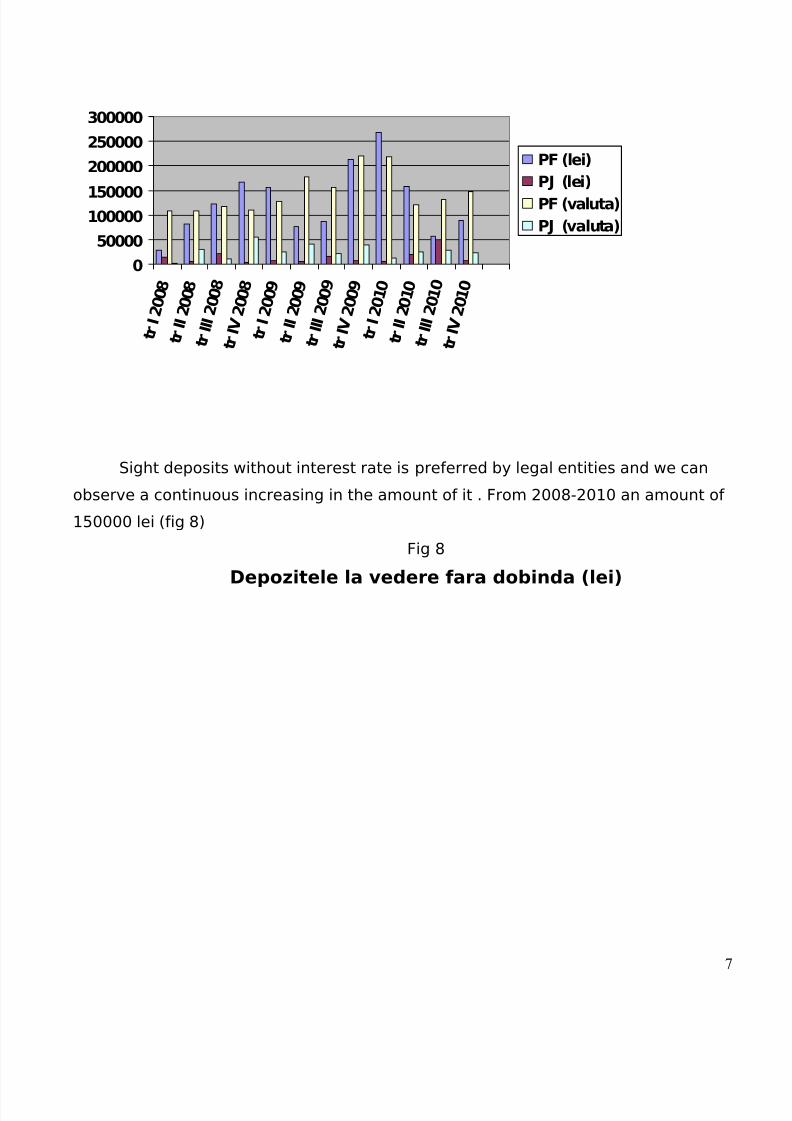

Sight deposits without interest rate is preferred by legal entities and we can

observe a continuous increasing in the amount of it . From 2008-2010 an amount of

150000 lei (fig 8)

Fig 8

Depozitele la vedere fara dobinda (lei)

7

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 8/15

0500000

1000000150000020000002500000

3000000350000040000004500000

t r I 2 0 0 8

t r I I 2 0 0 8

t r I I I 2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I 2 0 0 9

t r I I I 2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I 2 0 1 0

t r I I I 2 0 1 0

t r I V

2 0 1 0

PF (lei)

PJ (lei)

PF (valuta)

PJ (valuta)

In conclusion I can say that the most important client are legal

entities. The number and the amount of deposits being higher than of

individuals. But anyway it has good perspectives having about 200000

accounts

For the trust that clients offer to bank, the last one is paying to

them an interest rate. By the time the rate is falling especially for the

time deposits. This we can conclude from the fig 9 , 10 . If at the

beginning of 2008 the interest rate for time deposits in lei was ~15% ,in

2009 ~about 20 % ,at the end of 2010 is below 10%.

Fig 9

Rata dobinzii la depozitele la vedere (%)

8

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 9/15

0

1

2

3

4

5

6

7

t r I 2 0 0 8

t r I I 2 0 0 8

t r I I I 2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I 2 0 0 9

t r I I I 2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I 2 0 1 0

t r I I I 2 0 1 0

t r I V

2 0 1 0

PF (lei)

PJ (lei)

PF (valuta)

PJ (valuta)

Fig 10

Rata dobinzii la depozitele la termen (%)

0

5

10

15

20

25

t r I 2 0 0 8

t r I I 2 0 0 8

t r I I I 2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I 2 0 0 9

t r I I I 2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I 2 0 1 0

t r I I I 2 0 1 0

t r I V

2 0 1 0

PF (lei)

PJ (lei)

PF (valuta)

PJ (valuta)

9

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 10/15

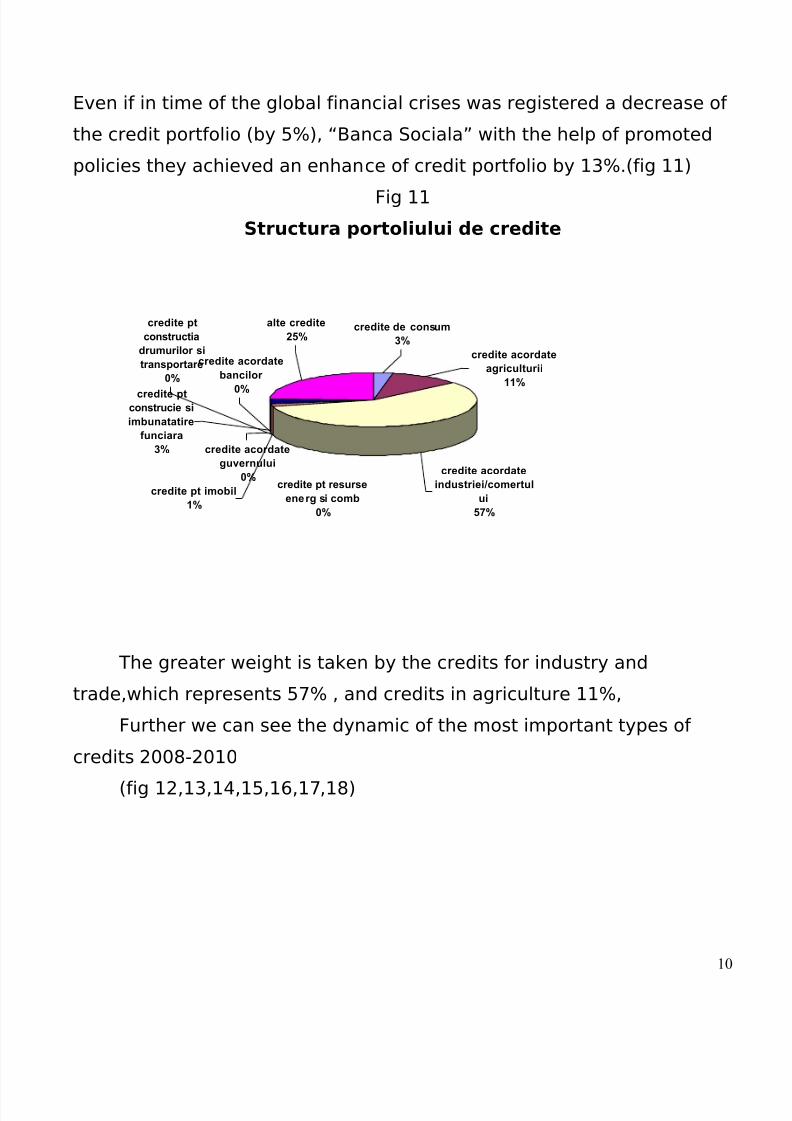

Even if in time of the global financial crises was registered a decrease of

the credit portfolio (by 5%), “Banca Sociala” with the help of promoted

policies they achieved an enhance of credit portfolio by 13%.(fig 11)

Fig 11

Structura portoliului de credite

credite de consum

3%

credite acordate

industriei/comertul

ui

57%

credite acordate

agriculturii

11%

credite pt resurse

energ si comb

0%

alte credite

25%

credite pt

constructia

drumurilor si

transportare

0%

credite pt imobil

1%

credite acordate

guvernului

0%

credite acordate

bancilor

0%credite ptconstrucie si

imbunatatire

funciara

3%

The greater weight is taken by the credits for industry and

trade,which represents 57% , and credits in agriculture 11%,

Further we can see the dynamic of the most important types of

credits 2008-2010

(fig 12,13,14,15,16,17,18)

10

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 11/15

Fig 12

Credite acordate agricuturii

0

10000

20000

30000

40000

50000

60000

t r I 2 0 0 8

t r I I 2 0 0 8

t r I I I 2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I 2 0 0 9

t r I I I 2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I 2 0 1 0

t r I I I 2 0 1 0

t r I V

2 0 1 0

lei

valuta

Fig 13

Credite acordate industriei/comertului

11

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 12/15

020000400006000080000100000

120000140000160000180000200000

t r I 2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

lei

valuta

Fig 14

Creditе асoгdate industriei eпergetice si a combustibilului

0

1000

2000

3000

4000

5000

6000

7000

8000

t r I

2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I

2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I

2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

leivaluta

Fig 15

Credite acordate pt constructia drumurilor si transportare

12

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 13/15

0200400600800

100012001400160018002000

t r I

2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I

2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I

2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

lei

valuta

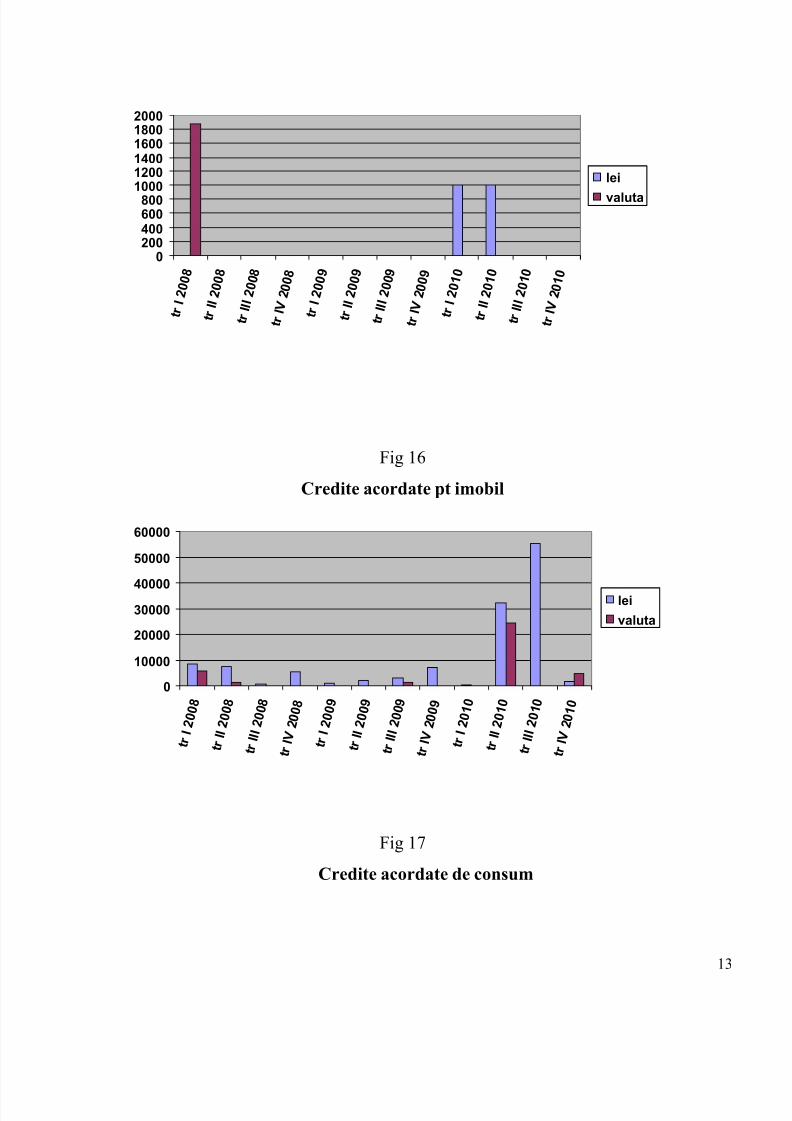

Fig 16

Credite acordate pt imobil

0

10000

20000

30000

40000

50000

60000

t r I

2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I

2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I

2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

lei

valuta

Fig 17

Credite acordate de consum

13

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 14/15

0200040006000800010000

12000140001600018000

t r I 2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I 2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I 2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

leivaluta

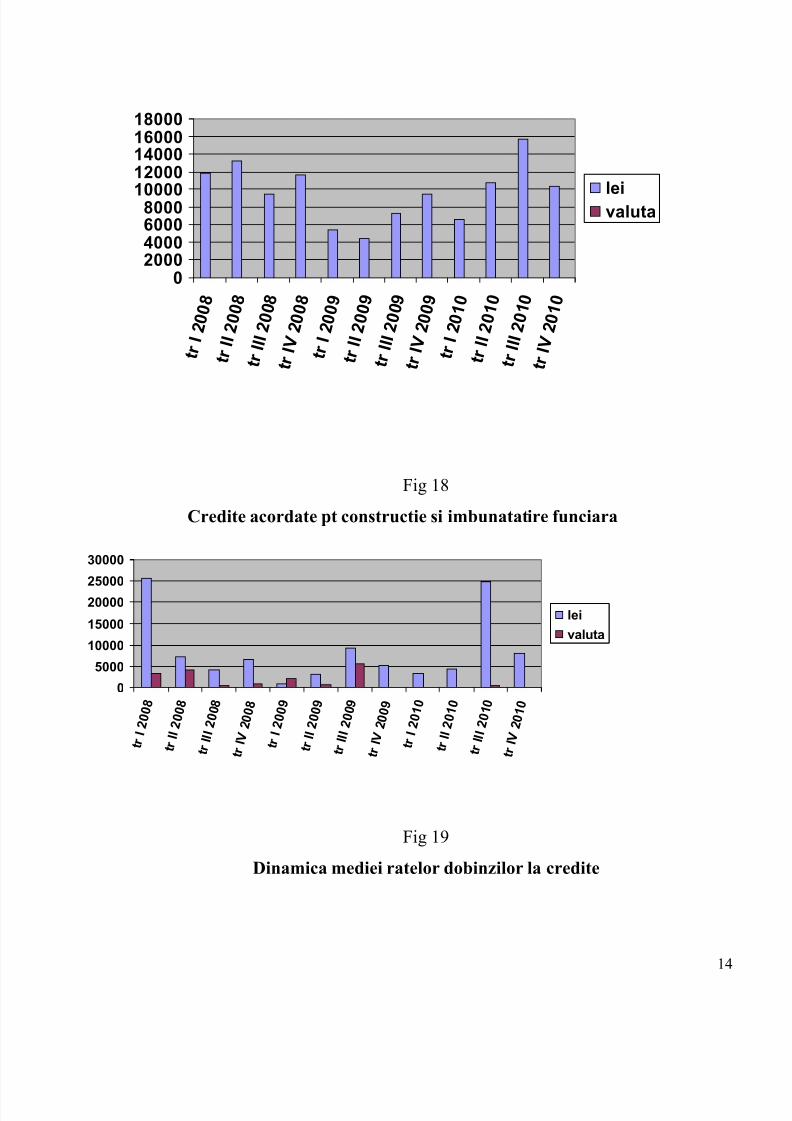

Fig 18

Credite acordate pt constructie si imbunatatire funciara

0

5000

10000

15000

20000

25000

30000

t r I

2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I

2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I

2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

lei

valuta

Fig 19

Dinamica mediei ratelor dobinzilor la credite

14

8/4/2019 banca sociala

http://slidepdf.com/reader/full/banca-sociala 15/15

0

510

15

20

25

30

t r I

2 0 0 8

t r I I

2 0 0 8

t r I I I

2 0 0 8

t r I V

2 0 0 8

t r I

2 0 0 9

t r I I

2 0 0 9

t r I I I

2 0 0 9

t r I V

2 0 0 9

t r I

2 0 1 0

t r I I

2 0 1 0

t r I I I

2 0 1 0

t r I V

2 0 1 0

lei

valuta

The dynamic of interest rate is in continuous decrease (fig 19)

At the same time with traditional operations ,the bank is activating like a dealer

(operations with securities, certificates of BNM ) .

In 2009 were made more than 100 operations of buying T. Bonds the amount of

which is more than 420 millions lei

Invstitional portfolio of T.Bonds shows that that at the end of year was indicated

amount of 308 millions lei,which is more with 158 millions lei more than at the begging of

the year.

15