Languages

Pages

Legal

Arvind Limited – Review Note Q4 & 2012-13

16th May 2013, Ahmedabad

Moderate revenue growth Strong profitability improvement

Highlights Q4 – 2012-13

1,406

1,278

1,100

1,200

1,300

1,400

1,500

Rev, Rs Cr

10%

FY2012-13 FY2011-12

203

131

0

100

200

300 54%

FY2012-13 FY2011-12

EBITDA, Rs Cr

7667

0

50

100

PAT, Rs Cr

14%

FY2012-13 FY2011-12

Revenue Growth of 10% achieved due to • 29% volume growth in shirting/khaki

textiles business • 17% topline growth in Brands & Retail

business • 15% price growth in Denim leading to 4%

topline growth despite 10% volume decline

EBIDTA Margin • EBIDTA margin improvement across all

textiles as well as brand & retail verticals One-time Depreciation charge Rs 7.6 Cr • As company decided to increase

depreciation from about 7% to 15% in Brands & Retail assets

Rs Cr

Q4FY13 Q4FY12 Change

Revenues 1,406 1,278 10%

Raw Materia l Consumed 610 594

Project Expenses 47 49

Employees ' Emoluments 149 116

Others 481 412

(Increase) / Decrease in Stock -83 -24

EBIDTA 203 131 54%

Margin 14.4% 10.3%

Other Income 20 41

Finance Cost 82 66

Cash Accruals 141 106 33%

Depreciation 64 41

Profi t Before Tax 76 65 17%

Net Profi t a fter Minori ty Interest 76 67 14%

Financial Performance Q4 – 2012-13

Key highlights

Moderate revenue growth Strong improvement in operating margins

Highlights FY 2012-13

5,293

4,925

3,000

4,000

5,000

6,000

Rev, Rs Cr

7.5%

FY2012-13 FY2011-12

687602

0

400

800+14.1%

FY2012-13 FY2011-12

EBITDA, Rs Cr

248245

0

100

200

300

PAT, Rs Cr +1.4%

FY2012-13 FY2011-12

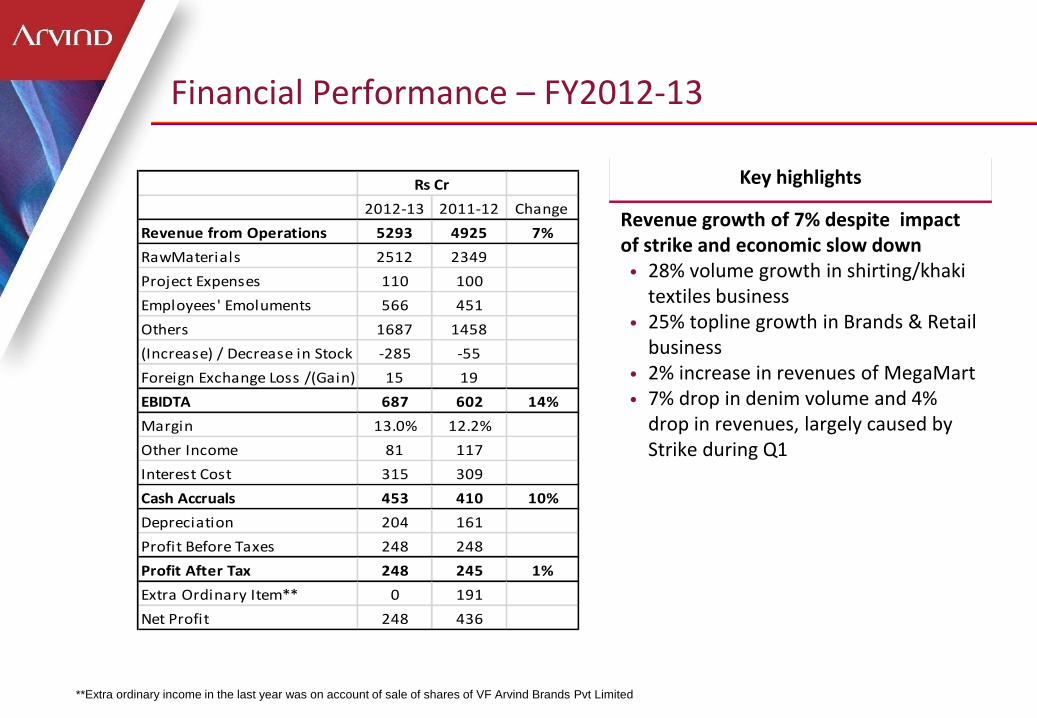

Revenue growth of 7% despite impact of strike and economic slow down • 28% volume growth in shirting/khaki

textiles business • 25% topline growth in Brands & Retail

business • 2% increase in revenues of MegaMart • 7% drop in denim volume and 4%

drop in revenues, largely caused by Strike during Q1

Financial Performance – FY2012-13

Key highlights

**Extra ordinary income in the last year was on account of sale of shares of VF Arvind Brands Pvt Limited

2012-13 2011-12 Change

Revenue from Operations 5293 4925 7%

RawMaterials 2512 2349

Project Expenses 110 100

Employees' Emoluments 566 451

Others 1687 1458

(Increase) / Decrease in Stock -285 -55

Foreign Exchange Loss /(Gain) 15 19

EBIDTA 687 602 14%

Margin 13.0% 12.2%

Other Income 81 117

Interest Cost 315 309

Cash Accruals 453 410 10%

Depreciation 204 161

Profit Before Taxes 248 248

Profit After Tax 248 245 1%

Extra Ordinary Item** 0 191

Net Profit 248 436

Rs Cr

EB

IDTA

m

arg

in 15.6% 15.7%

14.7% 13.4%

15.6% 16.2%

17.3% 18.1%

6.6% 7.2% 7.7%

1.2% 1.1%

6.0% 6.6% 6.8%

13.6% 13.1% 12.0%

10.3% 11.2%

12.4% 13.6%

14.4%

Q1 11-12 Q2 11-12 Q3 11-12 Q4 11-12 Q1 12-13 Q2 12-13 Q3 12-13 Q4 12-13

Textiles B & R Total

Margins in B&R improving even after including losses from the newer acquired brands

Continued Q-o-Q improvement in margins for both Textiles as well as Brands & Retail Businesses

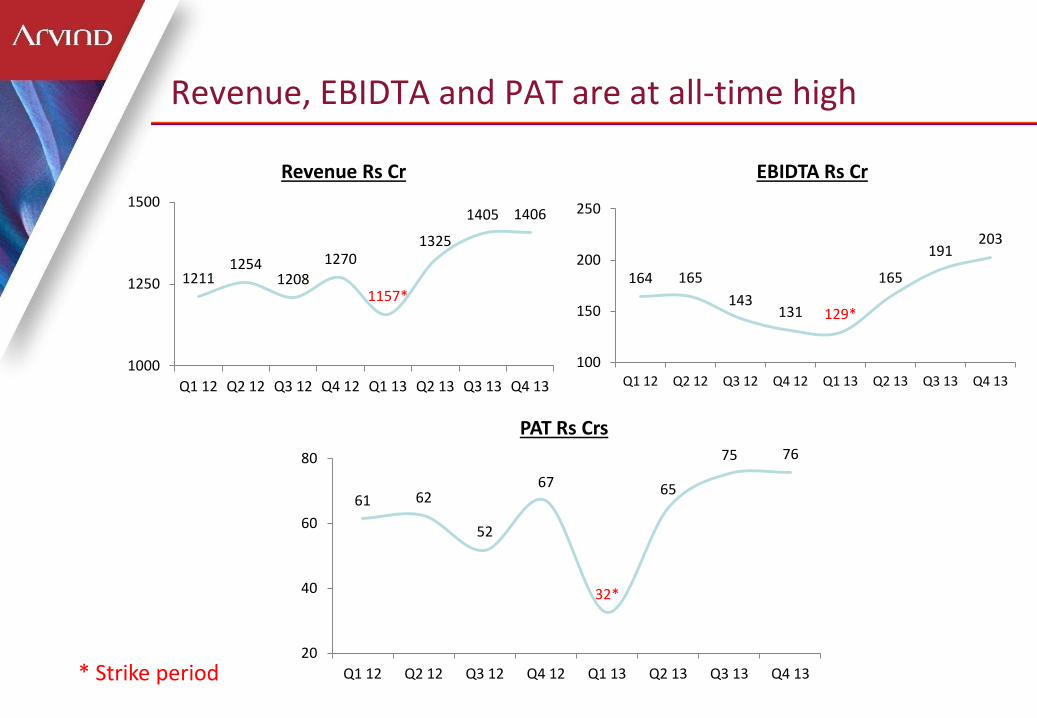

1211 1254

1208

1270

1157*

1325

1405 1406

1000

1250

1500

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13

Revenue Rs Cr

61 62

52

67

32*

65

75 76

20

40

60

80

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13

PAT Rs Crs

164 165

143 131 129*

165

191 203

100

150

200

250

Q1 12 Q2 12 Q3 12 Q4 12 Q1 13 Q2 13 Q3 13 Q4 13

EBIDTA Rs Cr

* Strike period

Revenue, EBIDTA and PAT are at all-time high

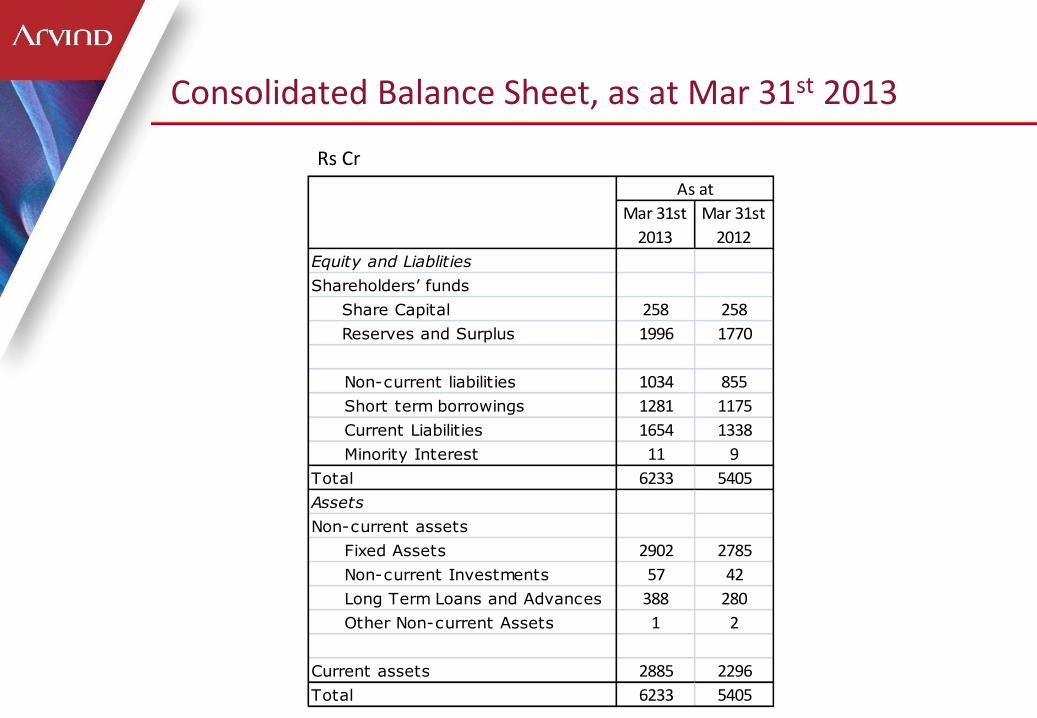

Mar 31st

2013

Mar 31st

2012

Equity and Liablities

Shareholders’ funds

Share Capital 258 258

Reserves and Surplus 1996 1770

Non-current liabilities 1034 855

Short term borrowings 1281 1175

Current Liabilities 1654 1338

Minority Interest 11 9

Total 6233 5405

Assets

Non-current assets

Fixed Assets 2902 2785

Non-current Investments 57 42

Long Term Loans and Advances 388 280

Other Non-current Assets 1 2

Current assets 2885 2296

Total 6233 5405

As at

Consolidated Balance Sheet, as at Mar 31st 2013

Rs Cr

ROCE and ROE lower due to:

1) Lost contribution on account of strike in Denim plant

2) Planned losses in newly acquired Brands & Retail businesses

Key Financial Ratios

2010-11 2011-12 2012-13

EPS 6.50 9.48 9.63

Debt / Equity 1.31 1.00 1.10

Debt / EBIDTA 3.7 2.8 3.2

ROCE 10.5% 13.1% 11.9%

ROE 8.4% 12.0% 11.3%

Revenue Growth 25% 20% 7%

Business Analysis All numbers in this section are consolidated unless specified otherwise

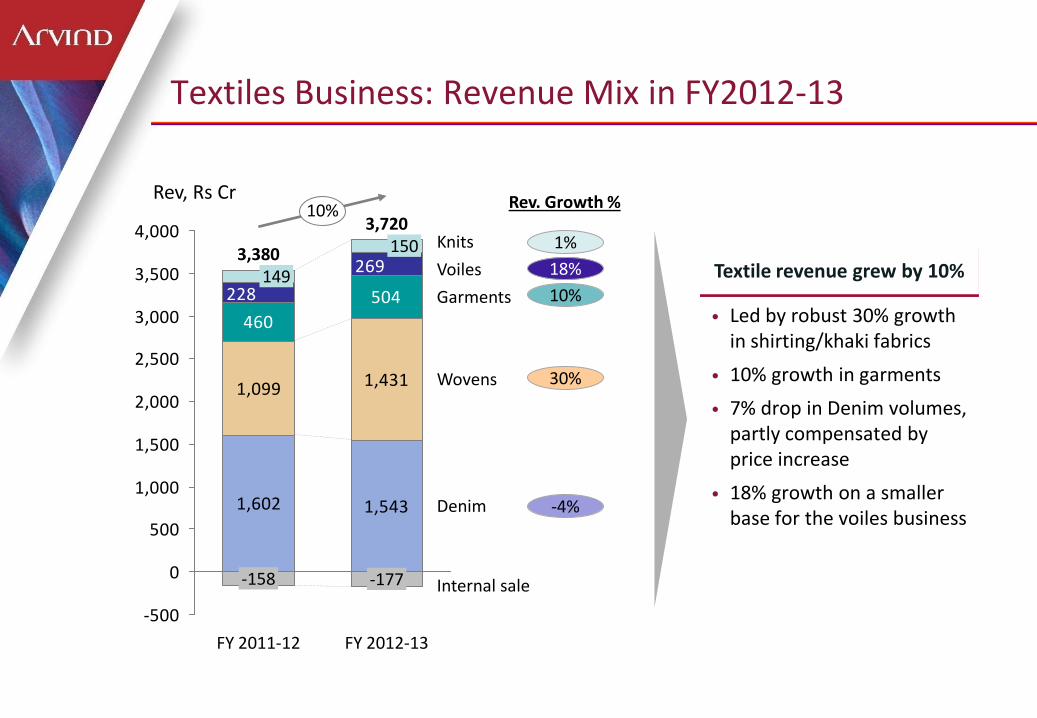

Textile revenue grew by 10%

Textiles Business: Revenue Mix in FY2012-13

1,602 1,543

1,099 1,431

460

504

269

228

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY 2012-13

150

Wovens

Knits

Denim

Rev, Rs Cr

Internal sale -177

3,720

Garments

Voiles

FY 2011-12

3,380

-158

149

10%

• Led by robust 30% growth in shirting/khaki fabrics

• 10% growth in garments

• 7% drop in Denim volumes, partly compensated by price increase

• 18% growth on a smaller base for the voiles business

1%

18%

10%

30%

-4%

Rev. Growth %

Denim Shirting & Khaki

Denim & Shirting/Khaki Volumes – FY2012-13

23.918.5

0

10

20

30

Volume, Mn Mtrs

29%

Q4 2012-13 Q4 2011-12

86.967.7

0

50

100

150

Volume, Mn Mtrs

FY2011-12 FY2012-13

28%

22.925.3

0

10

20

30

Volume, Mn Mtrs -9%

Q4 2012-13 Q4 2011-12

89.295.9

0

50

100

150

Volume, Mn Mtrs

-7%

FY2012-13 FY2011-12

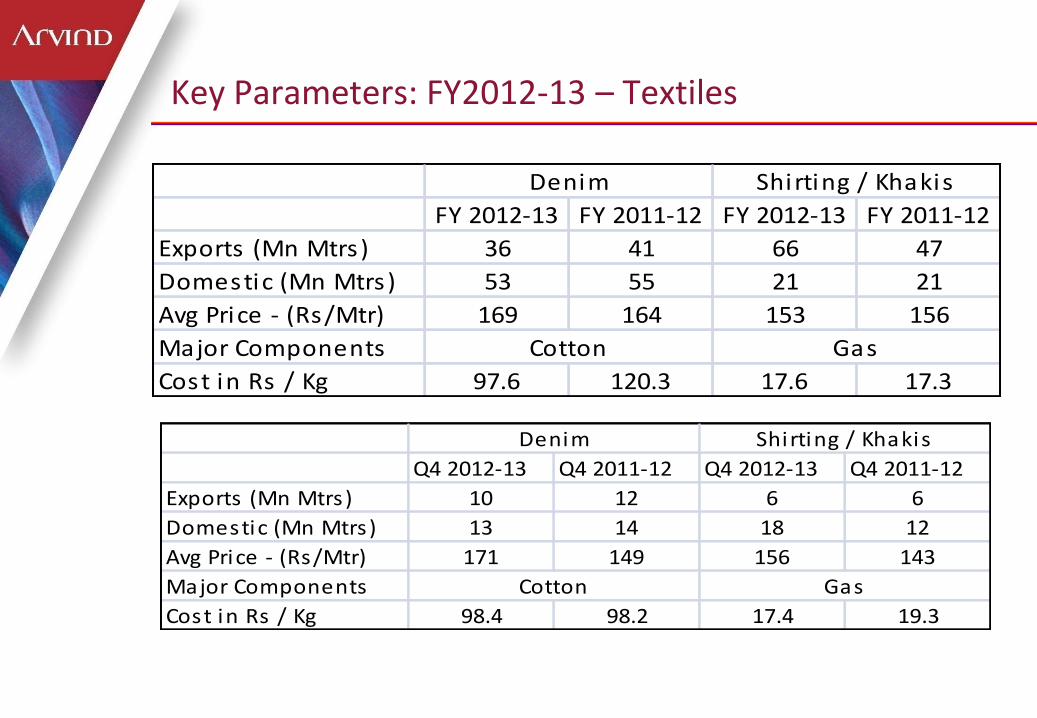

FY 2012-13 FY 2011-12 FY 2012-13 FY 2011-12

Exports (Mn Mtrs) 36 41 66 47

Domestic (Mn Mtrs) 53 55 21 21

Avg Price - (Rs/Mtr) 169 164 153 156

Major Components

Cost in Rs / Kg 97.6 120.3 17.6 17.3

Cotton Gas

Denim Shirting / Khakis

Q4 2012-13 Q4 2011-12 Q4 2012-13 Q4 2011-12

Exports (Mn Mtrs) 10 12 6 6

Domestic (Mn Mtrs) 13 14 18 12

Avg Price - (Rs/Mtr) 171 149 156 143

Major Components

Cost in Rs / Kg 98.4 98.2 17.4 19.3

Shirting / Khakis

Cotton Gas

Denim

Key Parameters: FY2012-13 – Textiles

Strong revenue growth Key highlights

Brands & Retail Business grew by 17% in Q4 2012-13

338

290

200

250

300

350

Rev, Rs Cr

17%

Q4 2012-13 Q4 2011-12

• Revenue growth of 17% achieved due to

– 37% revenue growth in Brands (29% growth excluding newly acquired brands)

– 9% revenue growth in MegaMart Retail, after de-growth in first 3 quarters

• Like to Like growth

– 0.2% LTL growth in Brands

– 5.4% LTL growth in MegaMart Retail , after registering negative LTL for first 3 quarters

Strong revenue growth Key highlights

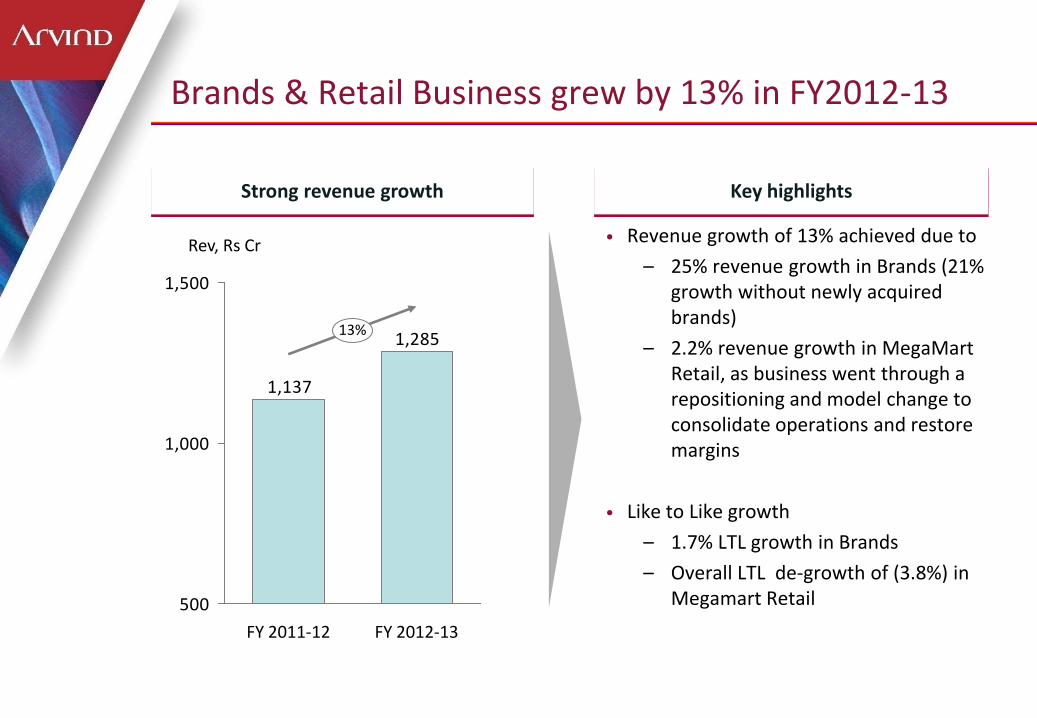

Brands & Retail Business grew by 13% in FY2012-13

1,285

1,137

500

1,000

1,500

Rev, Rs Cr

13%

FY 2012-13 FY 2011-12

• Revenue growth of 13% achieved due to

– 25% revenue growth in Brands (21% growth without newly acquired brands)

– 2.2% revenue growth in MegaMart Retail, as business went through a repositioning and model change to consolidate operations and restore margins

• Like to Like growth

– 1.7% LTL growth in Brands

– Overall LTL de-growth of (3.8%) in Megamart Retail

• Sales Increase in Key Account Counters: Growth of 32%

Particulars

FY11-12 FY12-13

# Stores Sq.ft # Stores Sq.ft

Brands 352 330,943 487 504,015

MM 216 691,770 197 710,133

Total 568 1,022,713 684 1,214,148

No of KA Exclusive Counters 327 376

Total KA Counters with Sub Brands

481 576

Brands & Retail Business – Distribution

Outlook for FY2013-14

• Revenue growth expected to be over 20% on account of volume growth in both Textiles and Brands & Retail

– Textiles: 12-15%

– Brands & Retail: 25%+

• International demand for textiles strong: Indian retail demand sluggish

• Company expects that margins for the coming year will be maintained – Margin for the Textiles businesses may improve marginally

– Margins for the Brands & Retail businesses may fall marginally due to higher investments in marketing and distribution for the newly acquired brands

Thank You

Top Related