Languages

Pages

Legal

www.cfraresearch.com

5G Paving the Way for Change Smart Connectivity – Beyond the Everyday Device

Angelo Zino, Keith Snyder, David Holt

August 21, 2018

Preparing for 5G – What Is It and What Lies Ahead?

Network Infrastructure – Growth and Challenges Ahead

Smart Applications – Mobile Devices and Connected Homes

Smart Applications – Connected Cars and Smart Cities

2

Agenda

Preparing for 5G – What Is It and What Lies Ahead?

3

Angelo Zino

What is 5G? Next generation of wireless networks

Will provide higher speeds, greater capacity, and lower latency

A network able to support billions of connected devices and things

Distributes intelligence throughout the network – the underlying infrastructure for AI (artificial intelligence)

4

Photo Credit: www.teligistics.com via www.CreativeCommons.org

Source: International Telecommunication Union (ITU)

Capability 5G 4GPeak Download Speed 20 Gbit/s 1 Gbit/sLatency 1 ms 30-50 msConnected Devices (per 0.38 sq. miles) 1 million 2,000

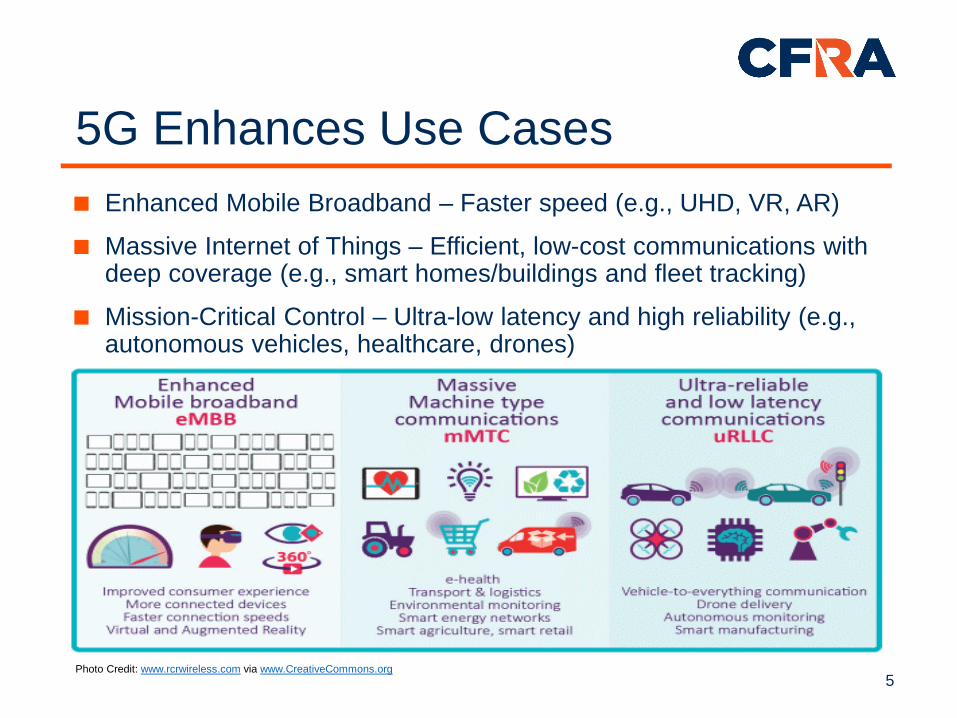

Enhanced Mobile Broadband – Faster speed (e.g., UHD, VR, AR)

Massive Internet of Things – Efficient, low-cost communications with deep coverage (e.g., smart homes/buildings and fleet tracking)

Mission-Critical Control – Ultra-low latency and high reliability (e.g., autonomous vehicles, healthcare, drones)

5 Photo Credit: www.rcrwireless.com via www.CreativeCommons.org

5G Enhances Use Cases

Wireless Carriers – Planning for 5G 5G hardware standards officially complete

Key to 5G – Millimeter wave spectrum and more antennas

Consumers will shift to wireless plans offering more data

6 Source: CFRA, Company press releases (AT&T, Sprint T-Mobile and Verizon)

Wireless Carrier 5G Plan Initial 5G Regions Anounced Comments

AT&T

*Commercial access in 12 cities by year-end (hotspot access only) *Phones in 2019

*Dallas, Waco, Atlanta, Charlotte, Raleigh and Oklahoma City

*5G Evolution (>140 markets) - 5G foundation *Selected to build first nationwide public safety broadband network

Sprint *5G commercially available 1H 2019*Los Angeles, Washington D.C., Atlanta, Chicago, Dallas and Houston

*Greatest availability of spectrum among the Big 4 *To utilize 800 MHz, 1.9 GHz, 2.5 GHz spectrum

T-Mobile *30+ cities 5G-ready by year-end *NYC, Los Angeles, Dallas and Las Vegas*Pending Sprint deal to support 5G investments *Primarily 600/700 MHZ and millimeter wave

Verizon

*Fixed 5G in 4 markets this year, intended to replace cable *Mobile in 2019 *Sacramento, Los Angeles and Houston

*Most exposure to high-bandwidth *We estimate > 1/3 share of millimeter wave spectrum

Note: FCC approved spectrum auction for high-bandwidth assets for November 2018 and second-half 2019

U.S. Mobile Subscribers (Millions)

7

Source: CFRA, IDC

2017 2018E 2019E 2020E 2021E 2022E0

100

200

300

400

500

600

2G/3G/4G Mobile Subscribers 5G Mobile Subscribers

U.S. 5G Subscribers (Millions)

8

Source: CFRA, IDC

2017 2018E 2019E 2020E 2021E 2022E0

20

40

60

80

100

5G Mobile Subscribers 5G Internet of Things (Non-Mobile) Connections

Network Infrastructure – Growth and Challenges Ahead

9

Keith Snyder

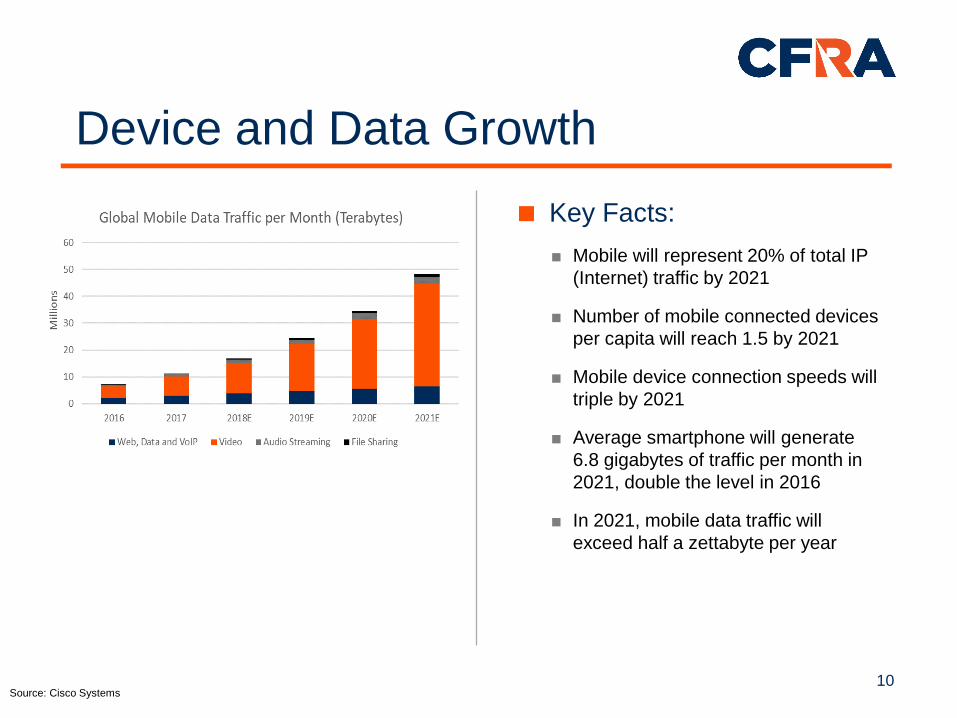

Device and Data Growth

10

Key Facts: Mobile will represent 20% of total IP

(Internet) traffic by 2021

Number of mobile connected devices per capita will reach 1.5 by 2021

Mobile device connection speeds will triple by 2021

Average smartphone will generate 6.8 gigabytes of traffic per month in 2021, double the level in 2016

In 2021, mobile data traffic will exceed half a zettabyte per year

Source: Cisco Systems

Basic Network Architecture

11

Data Aggregator

Network Core

Mobile devices communicate with antennas on cell tower/small cells.

Data from multiple cell sites is sent to an aggregation tool, which acts as the gateway into the operator’s network.

Data then moves into the operator’s network core, which provides the connection to Internet and other applications/services.

Round trip travel time: 30 to 50 milliseconds (for a 4G network)

High Frequency Transmission Issues

12

Fiber Link

Small Cell

Small Cells

Cell Type Cell Radius

(km)

Users Location

Femtocell 0.010 to 0.1 1 to 30 Indoor

Pico Cell 0.1 to 0.2 30 to 100 Indoor/ Outdoor

Micro Cell 0.2 to 2.0 100 to 2000 Indoor/ Outdoor

Macro Cell 8 to 30 >2000 Outdoor

13

Benefits:

Low cost

Easy to deploy

Increases network density

Lower delay

Drawbacks:

Data backhaul

Increased network complexity

Regulatory hurdles

Source: QORVO

Small Cell Growth

14

Source: creativecommons.com

Source: IDC

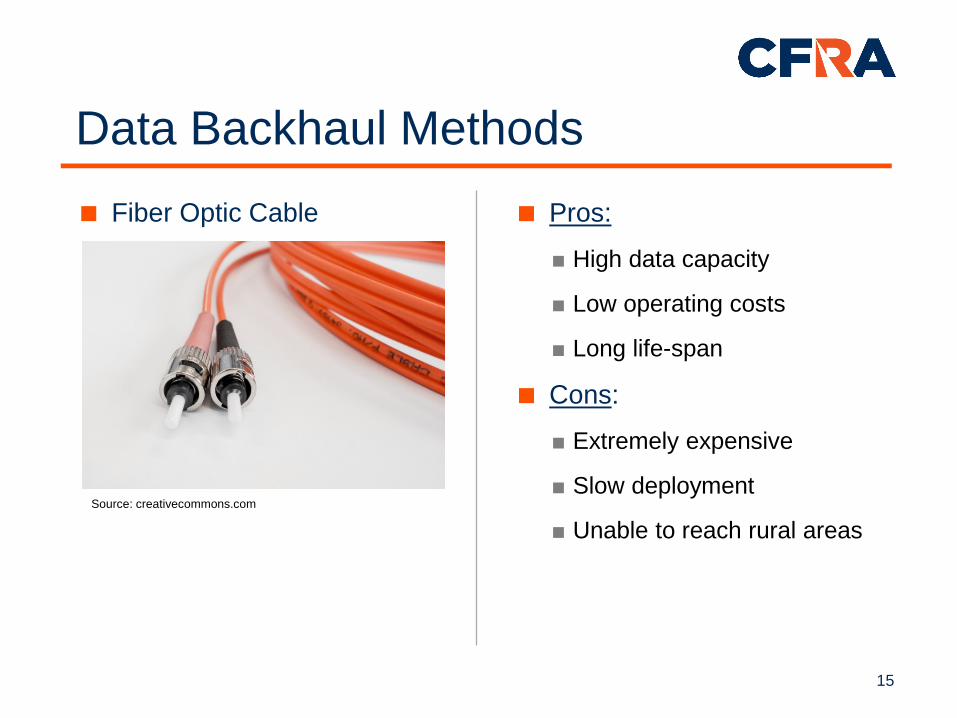

Data Backhaul Methods Fiber Optic Cable

15

Pros:

High data capacity

Low operating costs

Long life-span

Cons:

Extremely expensive

Slow deployment

Unable to reach rural areas

Source: creativecommons.com

Data Backhaul Methods Microwave Transmitter

16

Pros: Low upfront cost

Rapid deployment

Good for remote locations

Cons: Ties up spectrum

Limited data capacity

Require uninterrupted line-of-sight to function

Source: creativecommons.com

Edge Computing

17

MEC Server

Applications & Services

Network Core

Applications & Services

Devices connect to small cells.

Data is transported to main cell tower.

Mobile Edge Computing (MEC) servers at base of tower process data and deliver certain apps and services.

Data that can’t be processed by MEC server sent to network core.

Round-trip travel time: 1 millisecond

Smart Applications – Mobile Devices and Connected Homes

18

Angelo Zino

5G Will Impact Mobile First Will help improve replacement cycles, but modestly

5G-enabled devices from Samsung and Huawei in 2019 (#1 and #3 market-share companies).

iPhones available starting 2020, according to CFRA projections

By 2022, over 1/3 of global smartphones sold will be 5G-enabled

Average 5G device price could cost as much as $100-$200 more, with wireless bills increasing as much as 25%-30%

Will help spur greater capabilities:

Ultra High Definition (UHD)

Augmented Reality (AR) / Virtual Reality (VR)

19

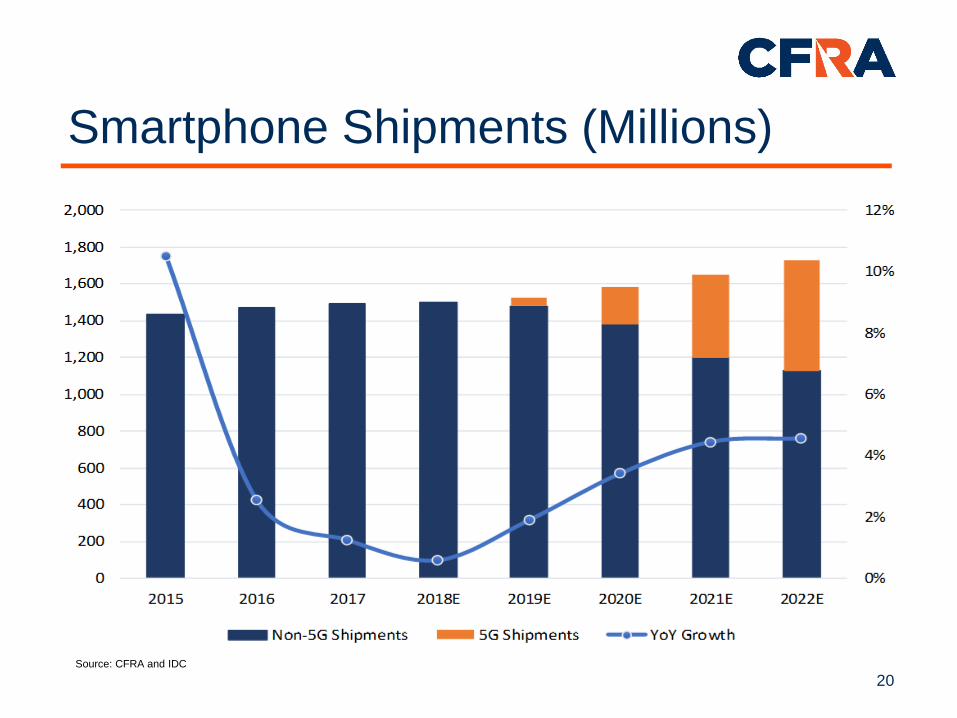

Smartphone Shipments (Millions)

20 Source: CFRA and IDC

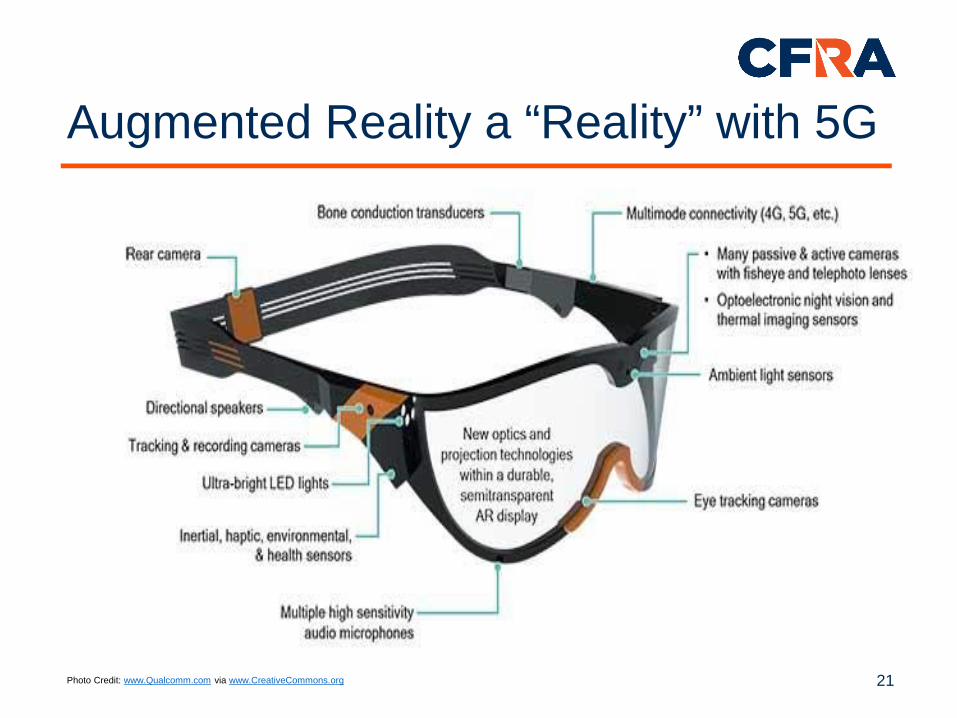

Augmented Reality a “Reality” with 5G

21

Photo Credit: www.maxpixel.net

Photo Credit: www.Qualcomm.com via www.CreativeCommons.org

The Smart Home Devices capable of communicating with each other

Why Connect? Convenience, cost savings, and energy efficiencies

Drivers? Greater access to high-speed Internet and smart assistants

Biggest Inhibitor? Privacy concerns.

22 Photo Credit: www.pixabay.com via www.CreativeCommons.org

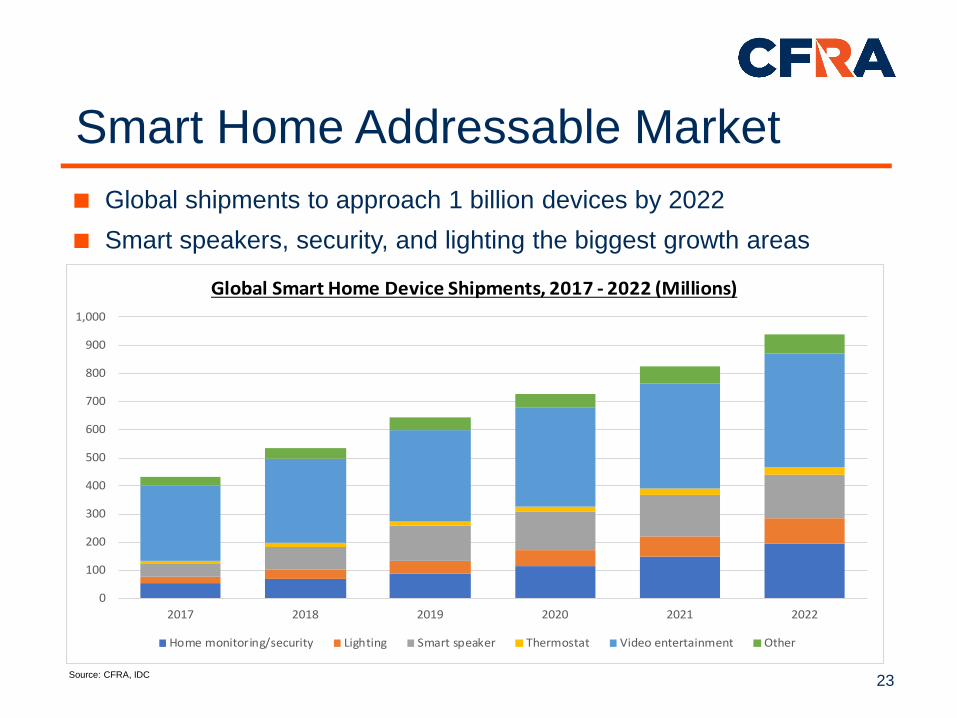

Smart Home Addressable Market Global shipments to approach 1 billion devices by 2022 Smart speakers, security, and lighting the biggest growth areas

23

0

100

200

300

400

500

600

700

800

900

1,000

2017 2018 2019 2020 2021 2022

Global Smart Home Device Shipments, 2017 - 2022 (Millions)

Home monitoring/security Lighting Smart speaker Thermostat Video entertainment Other

Source: CFRA, IDC

More Sensors Emerging in the Home

24

Alarm Siren

Appliances

Smart Switch Smart LED Bulb Smart Plug Smart Alarm Door/Window

Motion Sensors Water Leak Sensor Glass Sensor Smart Doorbell

Smoke Sensor

Humidity and Temperature Monitor

Smart Garage Door Sensor Smart Meters Smart Speakers

Analog Devices Broadcom Cypress Semiconductor Integrated Device Technology Maxim Integrated Products

MaxLinear Microchip QUALCOMM Silicon Laboratories Texas Instruments …And Others

Key Sensor Suppliers

Photo Credit for All Images: www.HomeDepot.com via www.CreativeCommons.org

Smart Applications – Connected Cars and Smart Cities

25

David Holt

Connected and Autonomous Cars Definition – Cars connecting with other cars, devices and cities

Why Connect? Traffic decongestion, accident prevention and pollution reduction

5G Catalysts – Quicker way to harvest data for safe and efficient driving experiences

Biggest Impediments – Data privacy and regulatory hurdles

Other Suppliers

Driving Systems Velodyne Robosense Valeo LeddarTech

Integrated Circuits Xilinx

Lattice Cypress Semiconductor

Teradyne

Others Flex

Amphenol National Instruments Trimble Navigation

Source: Company Logo Credit - www.creativecommons.org and Car Photo Credit - www.pixabay.com via www.CreativeCommons.org 26

Caution Construction ahead. Need to find a different route. Relayed to car behind it.

Source: CFRA and Car Image Credit - www.pixabay.com via www.creativecommons.org

Scenario 1 Scenario 2

Traffic Light Connected car can

automatically recognize and proceed accordingly.

Real-World Hypothetical Scenarios

27

Source: Yole Development, TE Connectivity

Total Addressable Market (TAM) – Over $130 billion currently

Connectivity is a linchpin for autonomous vehicles, solidifying the importance of 5G

ADAS – Advanced driver-assistance system

By 2045, more than 70% of all new vehicles sold expected to exhibit ADAS capabilities

28

Assisted Driving Addressable Market

Closer Look at Content Composition

29

Source: TE Connectivity, Yole Development, Car Image Credit - www.pixabay.com via www.creativecommons.org

Long-Range RadarASP/Unit - ~$140

Backup CameraASP/Unit - ~$30

GPS, Bluetooth, Wi-Fi AntennasASP/Unit - ~$5.50

LIDAR ASP/Unit - ~$350

Forward CameraASP/Unit - ~$40

Ultrasonic ASP/Unit - ~$6

In-Cabin/Driver Cam ASP/Unit - ~$30

Surround/Event CameraASP/Unit - ~$30

Short-Range RadarASP/Unit - ~$140

Content per Vehicle (CPV) Analysis

30

Source: Arrow Electronics, TE Connectivity, Yole Development

Sensors Quantity ASP/Unit ($) Quantity ASP/Unit ($) Quantity ASP/Unit ($) Quantity ASP/Unit ($) Quantity ASP/Unit ($)

Antennas 20 $5 20 $5 20 $5 20 $5 20 $5

Cameras (Front) 1 $40 3 $30 3 $27 3 $24 3 $20

Cameras (Rear) 1 $30 0 $0 0 $7,162 0 $0 0 $0

Cameras (In-Cabin Driver) 0 $0 0 $0 1 $20 1 $30 1 $25

Cameras (Surround) 0 $0 4 $25 4 $20 4 $15 4 $12

Radar Short Range 0 $0 0 $0 4 $43 4 $35 4 $31

Radar Long Range 1 $140 1 $135 1 $105 1 $70 1 $63

LIDAR 0 $0 0 $212 1 $1,500 2 $350 4 $200

Temperature Sensor 0 $0 0 $106 0 $0 1 $290 1 $190

Ultrasonic Sensor 6 $15 8 $15 8 $14 8 $13 8 $11

Other 0 $0 0 $0 0 $0 1 $350 1 $300

Total 29 $400 36 $545 42 $2,170 44 $1,916 1 $1,798

Level 4 Level 5Level 1 Level 2 Level 3

5G and new high-frequency bands require new “smart” technology

Emerging vehicle-to-everything (V2X) communication, real-time software updates crucial

In aggregate, there are 30-40 sensors (~$400 in content) in a car’s physical layer

Typical Level-3 ADAS equipped car will have another ~$2,170 in sensors

Doesn’t account for more advanced approaches (graphics processing units/GPUs)

Over 50% of world’s population now resides in urban areas

Rise in energy consumption, traffic congestion, and crime following increases

5G wireless networks will help enable smart-city solutions

End-result could be reduction in energy usage and improved public safety

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

1950 1975 2000 2025 2050

Total Population Urban Population

~68% Urban Population (United Nations Forecast)

Gap expected to close as urbanization outpaces total

rise in population headcount

~30% Urban Population ~54% Urban Population

Gap w idened, as total population outpaced

urbanization

Source: Department of Economic and Social Affairs of United Nations

Smart Cities – Intelligent Urban Development

31

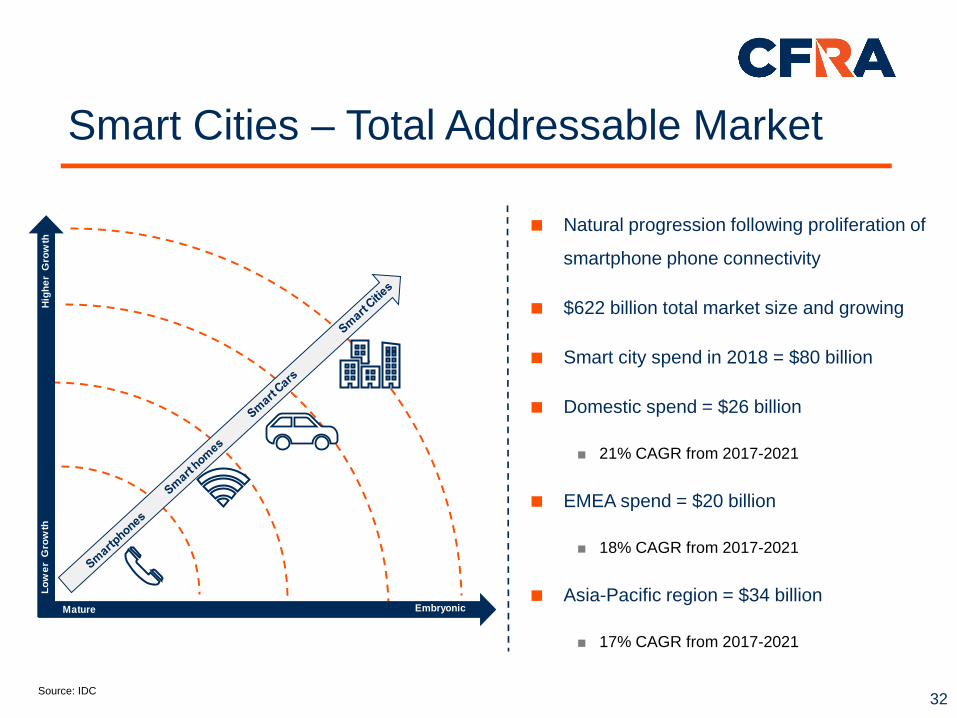

Smart Cities – Total Addressable Market

32

Low

er G

row

th

Mature Embryonic

Hig

her

Gro

wth

Natural progression following proliferation of

smartphone phone connectivity

$622 billion total market size and growing

Smart city spend in 2018 = $80 billion

Domestic spend = $26 billion

21% CAGR from 2017-2021

EMEA spend = $20 billion

18% CAGR from 2017-2021

Asia-Pacific region = $34 billion

17% CAGR from 2017-2021

Source: IDC

Public Transit Telematics Public transportation that

communicates with destination targets

Data Aggregation Lays the Foundation

Parking Capacity Smart meters that effectively monitor parking availability

V2X Connectivity Cars able to communicate with other cars and

structures to get from point A to B

Energy Management Consumption of each building is

tracked to rationalize where possible

Building Management Motion sensors and meters to have

greater insight into how buildings function

Traffic Monitoring Real-time ability to manage traffic congestion

Smart Street Lights Smart street lighting to optimize

power consumption

Source: Diagram Credit - Shutterstock 33

Law Enforcement and Safety Camera/sensor/meter surveillance for

quicker response to crime or fires

Combination of 5G and smart infrastructure creates economic benefits for municipalities of all sizes

Smart city pilots currently active – over 1,000

Implementation of sensors, meters and cameras help lend insight to how cities operate in real-time

Creates jobs and entire new industries

Focus areas for case study below – energy, public safety and transportation

Saratoga, CA Beaumont, TX Metro Chicago, IL TotalBenefits 29.9K Pop. 118K Pop. 90K Pop. Combined

Jobs Created 300 1,000 90000 500M

GDP Growth $50M $180M $14B $500B

Total Network Investment $20M $100M $8B $275B

Smart Grid +Transportation $10M $70M $5B NM

Smart City Case Study #1

Source: Accenture

34

Source: www.pixabay.com via www.creativecommons.org

Smart City Case Study #2

Source: Siemens and Smart Grid Image Credit - www.pixabay.com via www.creativecommons.org

Total Energy Benefits $1.9B

Smart Lighting Benefit $135M

Return on Invest. 4X

Payback Per. 7 Yrs.

Energy Savings 20 GWh

City One Aberdeen

City Two Brussels

City Three East London

City Four Alba Iulia

City Five Kartal

35

Questions & Answers

36

Client Services: +1 212.981.1062 [email protected]

Disclosures S&P GLOBAL™ is used under license. The owner of this trademark is S&P Global Inc. or its affiliate, which are not affiliated with CFRA Research or the author of this content. The content of this Presentation and the opinions expressed herein are those of CFRA based upon publicly-available information that CFRA believes to be reliable but are subject to change without notice. This Presentation has not been submitted to, nor received approval from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this Presentation, CFRA AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, to the fullest extent permitted by law, regarding the accuracy, completeness, or usefulness of the information contained herein and assumes no liability with respect to the consequences of relying on this information for investment or other purposes. No content herein (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of CFRA. This Presentation shall not be used for any unlawful or unauthorized purposes. CFRA and its third-party providers, as well as its and their directors, officers, shareholders, employees or agents, do not guarantee the accuracy, completeness, timeliness or availability of this Presentation. CFRA's primary financial data provider is S&P Global Market Intelligence. THIS DOCUMENT CONTAINS COPYRIGHTED AND TRADE SECRET MATERIAL DISTRIBUTED UNDER LICENSE FROM S&P GLOBAL MARKET INTELLIGENCE. FOR RECIPIENT'S INTERNAL USE ONLY. Certain information in this presentation is provided by S&P Global, Inc. and/or its affiliates and subsidiaries (collectively “S&P Global”). Such information is subject to the following disclaimers and notices: “Copyright © 2018, S&P Global Market Intelligence (and its affiliates as applicable). All rights reserved. Nothing contained herein is investment advice and a reference to a particular investment or security, a credit rating or any observation concerning a security or investment provided by S&P Global is not a recommendation to buy, sell or hold such investment or security or make any other investment decisions. This may contain information obtained from third parties, including ratings from credit ratings agencies. Reproduction and distribution of S&P Global’s information and third party content in any form is prohibited except with the prior written permission of S&P Global or the related third party, as applicable. Neither S&P Global nor its third party providers guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such information or content. S&P GLOBAL AND ITS THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE AND ALL S&P INFORMATION IS PROVIDED ON AN AS-IS BASIS. S&P GLOBAL AND ITS THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR INFORMATION OR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.” CFRA, CFRA Accounting Lens, CFRA Legal Edge, CFRA Score, and all other CFRA product names are the trademarks, registered trademarks, or service marks of CFRA or its affiliates in the United States and other jurisdictions. CFRA Score may be protected by U.S. Patent No. 7,974,894 and/or other patents. Copyright © 2018 CFRA. All rights reserved. This Presentation is published and originally distributed by Accounting Research & Analytics, LLC d/b/a CFRA (“CFRA US”), with the following exceptions: In the UK/EU/EEA, it is published and originally distributed by CFRA UK Limited (company number 08456139 registered in England & Wales with its registered office address at PO Box 698, Titchfield House, 69-85 Tabernacle Street, London, EC2A 4RR, United Kingdom, which is regulated by the Financial Conduct Authority (No. 775151), and in Malaysia by CFRA MY Sdn Bhd (formerly known as Standard & Poor’s Malaysia Sdn Bhd) Company No. 683377-A and regulated by Securities Commission Malaysia, No. CMSL/A0181/2007 (“CFRA Malaysia”). CFRA Malaysia is a wholly-owned subsidiary of CFRA US. These parties and their subsidiaries maintain no responsibility for CFRA reports or materials redistributed by third parties such as brokers or financial advisors.

37

Disclosures, continued. Past performance is not necessarily indicative of future results. This Presentation may contain forward-looking statements or forecasts; such forecasts are not a reliable indicator of future performance. This Presentation is not intended to, and does not, constitute an offer or solicitation to buy and sell securities or engage in any investment activity. This Presentation is for informational purposes only. Recommendations in this Presentation are not made with respect to any particular investor or type of investor. Securities, financial instruments or strategies mentioned herein may not be suitable for all investors and this material is not intended for any specific investor and does not take into account any investor's particular investment objectives, financial situations or needs. Before acting on any recommendation in this material, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Additional information on a subject company may be available upon request. The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and S&P Global Market Intelligence. GICS is a service mark of MSCI and S&P Global Market Intelligence and has been licensed for use by CFRA. Any portions of the fund information contained in this Presentation supplied by Lipper, A Thomson Reuters Company, are subject to the following: “Copyright 2018 © Thomson Reuters. All rights reserved. Lipper shall not be liable for any errors or delays in the content, or for any actions taken in reliance thereon.” Copyright © 2018 CFRA. All rights reserved. CFRA and STARS are registered trademarks of CFRA.

38

Top Related