Languages

Pages

Legal

An Executive Overview, by Solidus, Inc.

Solidus | New England’s Branch Builder

White Papers

[Executive Overview] WHY A BRANCH REFRESH IS NOT ABOUT SUPERFICIAL DESIGN

Abstract: Branch banking today is highly competitive. Banks and credit unions must design

branches skillfully with customer experience and return on investment (ROI) foremost in mind.

Community engagement, brand loyalty, and the incorporation of technology are all indicators

of an institution’s relevance, and crucial for branch success. Simply put, the renovation of

financial branches is no longer a cosmetic affair. What was once a matter of choosing the right

carpets and wall color has now become a major undertaking requiring industry expertise and

the coordination of numerous disciplines. A modern branch upgrade is an exercise in efficiency

and cost-saving due to advances in cash handling equipment, interface redesigns, and banking

communications technology. For most, if not all, of today’s branches, these renovations are first

generation. All of the considerations discussed below must be properly mapped out to project

realistic hurdle rates and payback periods. For instance, a branch footprint can be

overestimated if mobile apps are promoted after a branch is designed. Up to 30% of

transactions may be transferred to apps, reducing the spatial requirements. This paper helps

guide those without the requisite knowledge to a fuller understanding of which branch

elements are of value to customers, and the ways in which these elements can be configured

for optimal return on investment. The focus is on community banks and credit unions in New

England.

1. INTRODUCTION

The proliferation of commercial material addressing changes in financial institutions states that

branches are shrinking, that technology is dominating the financial industry, and that branches

must now sport an ultra-modern look (which contradicts New England sensibilities). While

some of this is true, there is no single blueprint for the so-called “branch of the future”; every

case is different, not just from one institution to another, but from branch to branch within a

single institution. This paper will define the core requirements for a modern branch refresh

regardless of branch size or location, ignoring non-functional/non-value-added features. Five

definite required elements are:

Replacement of teller lines with dialogue towers and cash recyclers.

Branch staff being trained in the universal banker and customer-engagement role.

Value added offerings; PTM’s/ITM’s, financial advice/consultancy and the Omnichannel.

Retail communications, branding and merchandising.

Technology bars, café-lounges and learning spaces.

The dialogue pod: Changing the customer experience.

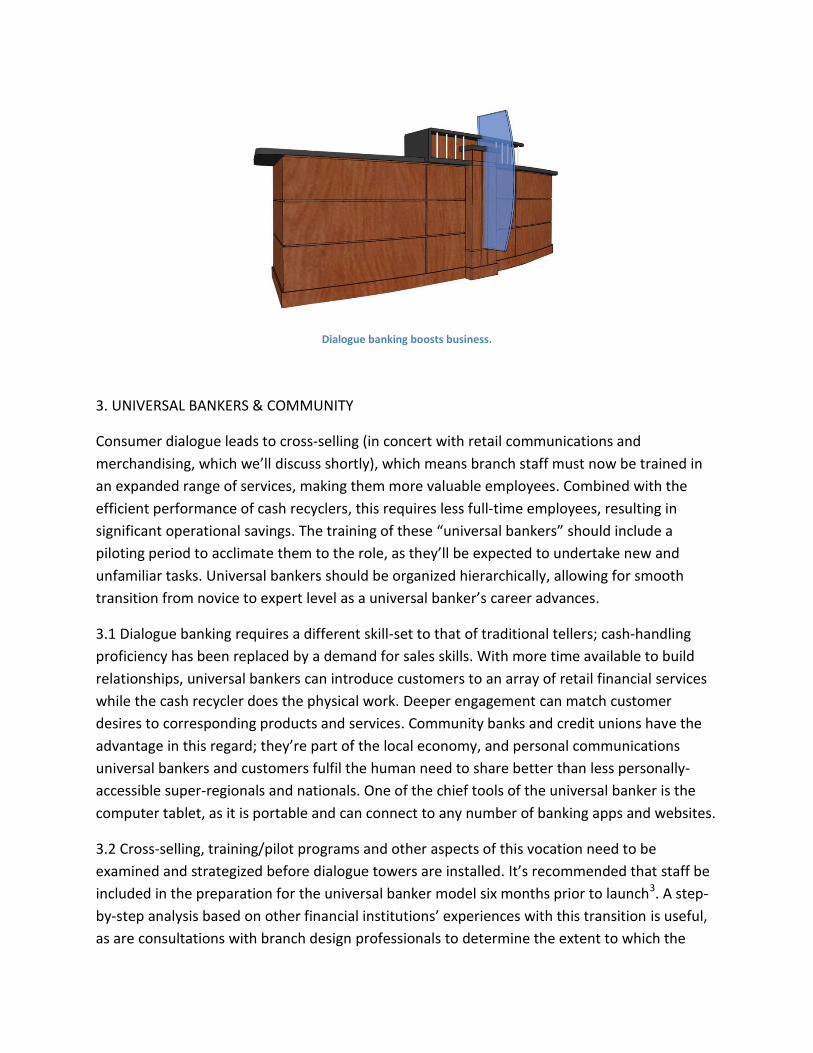

2. Dialogue Towers

Dialogue towers have opened up the role of branch staff to possibilities not dreamed of just 20

years ago. Where old style teller lines relied on their fortified appearance to reassure customers

that cash and valuables were safe, pods achieve the same effect via a new technology called

the cash recycler. From being housed like guards behind bulletproof glass or steel bars, branch

staff are now relationship managers, operating from open-plan workstations with no physical

barriers other than the counters necessary for supporting computers and transactional papers.

Pods can be designed for any aesthetic or regional sensibility. They can be purchased as a kit-of-

parts component or be custom-made for very specific locations in certain branches. Various

materials are used in their construction including wood, metal, plastic, glass and stone. They

also represent the most rational solution to the extra space created by removing teller lines

combined with smaller branch footprints.

A typical dialogue tower, showing privacy partition, multilevel counters, and computer monitor.

2.1 Dialogue towers may assume almost any form, but certain characteristics are usually

present. These include multilevel arrays of counter space, privacy partitions between stations,

computers with swivel-mounted monitors, storage drawers on the staff side, and branding

elements on the customer side. They are usually stand-alone “towers” with open access on all

sides, with the expectation that customers won’t venture into the business side unless invited.

Staff are fully expected to operate on both sides of the pod, especially if the computer monitors

aren’t mounted on swivel stands. The pod model is welcoming and makes a refreshing change

for consumers. But the single most revolutionary component of dialogue towers is the cash

recycler.

Cash recyclers represent a quantum leap in function and asset security.

2.2 Cash recyclers have brought an unprecedented level of secure cash handling to the banking

world. They’re inconspicuous and are designed for enhanced security; certified built-in safes

mean the cash can be stored inside overnight with no external vault required. Positioned in the

center of the pod between the dialogue bankers, recyclers can process 10 notes per second

(dispensed or deposited) in any combination of denominations. They can log serial numbers for

advanced error recovery. Their capacity can be as high as 17,100 notes, with continuous fast

processing of large banknote deposits uninterruptedly. They contain tamper-proof cassettes

that are fully secure and can be organized by denomination. Recyclers can count, organize,

bundle and strap cash at remarkable speed1. This frees up the dialogue banker, whose

attention can now be directed at the customer. Dialogue towers allow engagement banking at

its finest, where the branch employee, once chiefly preoccupied with counting cash, can now

participate in deeper interaction. The dialogue tower is therefore a key differentiator that

drives brand loyalty, enables cross- or up-selling, and attracts new business.

2.3 Dialogue towers need cash recyclers for security reasons and to function optimally.

Recyclers can be installed independent of a pod setup in other areas of the branch, most

notably at the drive-through window. Pods cannot be installed without recyclers; the recycler is

the “engine” of the pod, and without it all the benefits are completely absent and any cash

present is far too vulnerable to robbery2. This is due to the open nature of pods. They’re

designed to remove the traditional barriers of old and allow universal bankers to leave the

service side and physically greet customers as they approach.

2.4 Customer experience and return on investment (ROI) are the most important aspects of a

branch upgrade. When planning to migrate to pods, financial institutions must consult with

branch design professionals to ensure all vital elements are present. When the dialogue towers

are properly optimized for a dialogue banking experience, it opens up other retail possibilities

within the branch. It cannot be stressed enough that without a cash recycler, a dialogue tower

is merely a differently styled teller station, incapable of supporting dialogue banking in the true

sense of the term. In addition to the staff reductions allowed by the more fluid role of the so-

called universal banker, there are technological and other modifications that when combined

yield higher ROI. The following sections will detail these branch elements that improve long-

term efficiency and profits.

Dialogue banking boosts business.

3. UNIVERSAL BANKERS & COMMUNITY

Consumer dialogue leads to cross-selling (in concert with retail communications and

merchandising, which we’ll discuss shortly), which means branch staff must now be trained in

an expanded range of services, making them more valuable employees. Combined with the

efficient performance of cash recyclers, this requires less full-time employees, resulting in

significant operational savings. The training of these “universal bankers” should include a

piloting period to acclimate them to the role, as they’ll be expected to undertake new and

unfamiliar tasks. Universal bankers should be organized hierarchically, allowing for smooth

transition from novice to expert level as a universal banker’s career advances.

3.1 Dialogue banking requires a different skill-set to that of traditional tellers; cash-handling

proficiency has been replaced by a demand for sales skills. With more time available to build

relationships, universal bankers can introduce customers to an array of retail financial services

while the cash recycler does the physical work. Deeper engagement can match customer

desires to corresponding products and services. Community banks and credit unions have the

advantage in this regard; they’re part of the local economy, and personal communications

universal bankers and customers fulfil the human need to share better than less personally-

accessible super-regionals and nationals. One of the chief tools of the universal banker is the

computer tablet, as it is portable and can connect to any number of banking apps and websites.

3.2 Cross-selling, training/pilot programs and other aspects of this vocation need to be

examined and strategized before dialogue towers are installed. It’s recommended that staff be

included in the preparation for the universal banker model six months prior to launch3. A step-

by-step analysis based on other financial institutions’ experiences with this transition is useful,

as are consultations with branch design professionals to determine the extent to which the

branch must be redesigned for fully holistic dialogue banking. Staff may be resistant to change,

necessitating an aggressive re-training program to determine those more able to make the

transition. Universal bankers are more valuable than traditional tellers, so the potential pay

raise will also be a great motivator.

3.3 Universal bankers’ strengths lie in versatility rather than physical territory, though universal

bankers are certainly not confined to the pod. The “roaming” model covers the entire retail

floor, where branch visitors can be intercepted and guided as they enter and explore the

business environment. The universal banker quickly determines visitors’ needs, and delivers

them either to a tech bar, advisor, loan officer, or attends to them personally. Concierges were

also tested more recently to provide a premium service feel to customers, but these have been

largely discontinued as their cost cannot be justified. Instead, universal bankers skilled in the art

and minutiae of selling products can now determine exactly which branch zone or staffer is

appropriate for a visitor’s needs. The concierge concept has been supplanted by that of the

universal banker at this point in time.

Universal bankers can leave the dialogue tower and roam the entire retail floor.

3.4 The strength of dialogue banking lies in its ability to encompass and endorse community

values and customs. When people interact on a more meaningful level, it’s an experience they

want to repeat. At one time, the drive-thru4 was heralded as the greatest thing to happen to

our consumption/mobility lifestyle, but digital banking has proved even more efficient.

Efficiency and convenience will always feature high as consumer priorities, with the latter

undergoing a shift in meaning over the next several decades; the value of “community” is

poised for resurgence, not just in banking but in all commercial and civic aspects of society.

Movements like Smart Growth America are championing “walkable neighborhoods”, mixed

land use, and direct stakeholder involvement in designed communities. The physical branch will

be of prime importance as these more sustainable communities are developed. New England is

well positioned to thrive under the so-called “complete streets” model, as many of our

communities were built during a time when high pedestrianism was the norm. This is worth

bearing in mind from a brand positioning as well as a branch refresh perspective. The Solidus

white paper, “Meaningful Community Participation for Banks and Credit Unions”, is

recommended for further reading.

Walkable neighborhoods: driving the emergence of “designed communities”

3.5 In conclusion, cross-selling and authentic community participation are the most effective

approaches to the changing branch role, but minus proper training the benefits won’t be

realized. There may be resistance to a transition from traditional tellers to universal bankers,

but the universal banker model is currently the one that best complements larger industry

changes. Ultimately, customer service skills and industry expertise can together build brand

trust, which leads to customers consolidating their financial accounts within a single financial

institution. With more financial “eggs in one basket”, consumers will be far less likely to leave a

brand, creating loyalty as well as higher value customers. Branch banking is at a tipping point;

without applying these changes in the next branch refresh, institutions will make themselves

more vulnerable to extinction.

4. INCREASING ROI: COMBINING TECHNOLOGY WITH STAFFING STRATEGY

While superficial branch appearance can influence customer decisions and loyalties, it’s the

deeper functional aspects of a branch renovation (like cash recyclers) that truly affect ROI. In

selecting a reputable architect/design-builder, decision-makers should be clear about themes,

colors and other non-functional details. A branch upgrade is not a design contest; it’s an

opportunity for a financial institution to bring their business environment into line with the

most current industry standards or, if they’re fortunate, benefit from consultation with an

industry thought-leader who can implement “future-proof” modules that can be adapted in

real-time. These modules include dialogue towers, branding/merchandising kiosks and display

units, check desks and more. Staff roles, fixtures and millwork can therefore be designed

around each other. When staff are distilled down to their highest value-per-employee ratio, the

introduction of other value-added service features boosts ROI significantly. These include video

ATM’s, in-branch consultancies, and financial advisors.

Automated branches free up time and space for expanded financial services like advice and consultancy.

4.1 Basic teller transactions were automated to some extent by the introduction of ATM’s at

the turn of the 1970’s5. However, many customers needed more than a simple cash

withdrawal, and so traditional bank tellers prevailed. With the latest ATM technology,

customers are now connected to an audio-visual call center, where a remote banker

communicates with them via a speaker/phone and a TV screen on the cash machine. This new

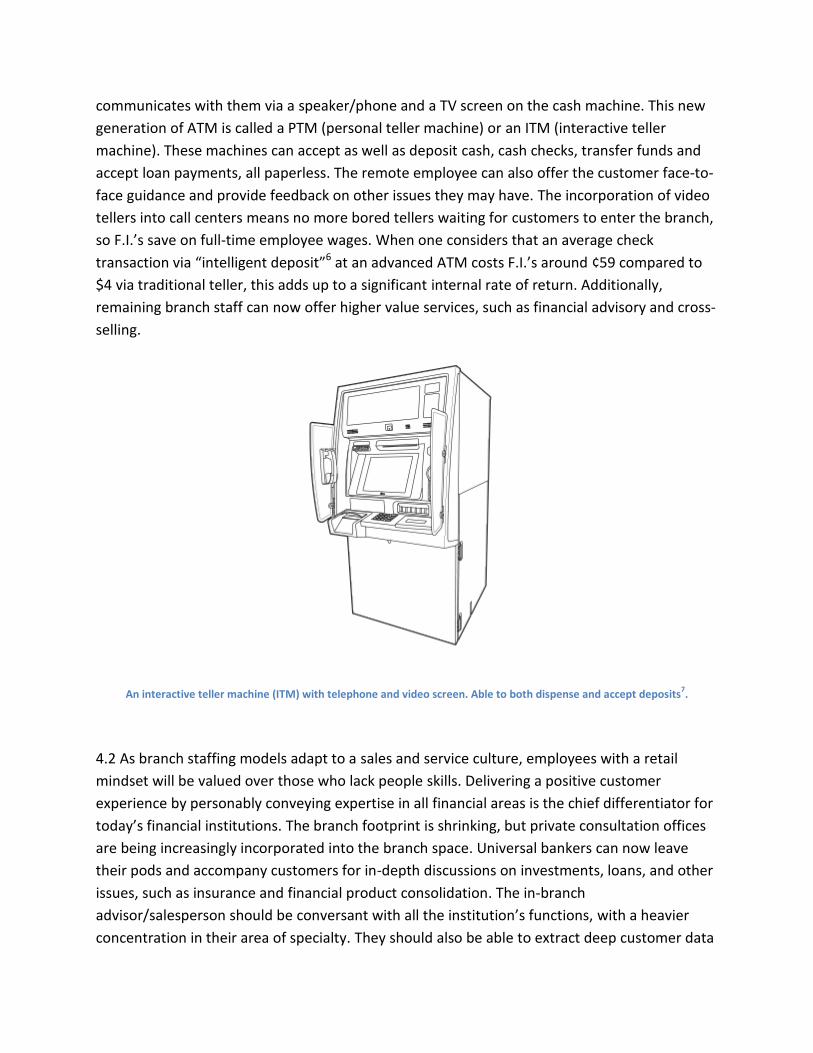

generation of ATM is called a PTM (personal teller machine) or an ITM (interactive teller

machine). These machines can accept as well as deposit cash, cash checks, transfer funds and

accept loan payments, all paperless. The remote employee can also offer the customer face-to-

face guidance and provide feedback on other issues they may have. The incorporation of video

tellers into call centers means no more bored tellers waiting for customers to enter the branch,

so F.I.’s save on full-time employee wages. When one considers that an average check

transaction via “intelligent deposit”6 at an advanced ATM costs F.I.’s around ¢59 compared to

$4 via traditional teller, this adds up to a significant internal rate of return. Additionally,

remaining branch staff can now offer higher value services, such as financial advisory and cross-

selling.

An interactive teller machine (ITM) with telephone and video screen. Able to both dispense and accept deposits7.

4.2 As branch staffing models adapt to a sales and service culture, employees with a retail

mindset will be valued over those who lack people skills. Delivering a positive customer

experience by personably conveying expertise in all financial areas is the chief differentiator for

today’s financial institutions. The branch footprint is shrinking, but private consultation offices

are being increasingly incorporated into the branch space. Universal bankers can now leave

their pods and accompany customers for in-depth discussions on investments, loans, and other

issues, such as insurance and financial product consolidation. The in-branch

advisor/salesperson should be conversant with all the institution’s functions, with a heavier

concentration in their area of specialty. They should also be able to extract deep customer data

during interactions. Branch consultant and advisor skill-sets should include the ability to

develop post-conversion (or post-customer communication) reports that help achieve higher

conversion rates across the entire branch team. In other words, their communications skills

should excel internally as well as customer-facing.

4.3 Financial advice and consultancy will function as gateways to the so-called Omnichannel

experience8. This is because these services apply closely to the on- and offline linkages the

Omnichannel opens up for consumers. For example, a bank may offer mortgages, and develop

a mobile app that shows available real estate within a certain radius. The app encourages

customer interaction from the outset, raising the probability that they’ll continue engaging with

the F.I. as their home buying experience progresses. The app can also feature advice portals,

and the ability to make appointments with an in-branch mortgage advisor. The visit to the

branch for advice, the mobile app, and the home buying experience, can all be managed within

a “leak-proof” continuous digital and real-life environment. The branch advisor can even

communicate with the home buyer via the app. The home buyer can transfer funds, track the

mortgage application process, and generally become more invested than ever in their financial

institution.

4.4 It is estimated that by 2017, America’s 50 million Gen X’ers will constitute the largest source

of new relationships for financial advisors, while 77 million Gen Y’ers will be the second-highest

source by 20239. This next generation of financial investor/advice seeker will be tech-savvier

and totally acclimated to the Omnichannel. The branch advisors themselves will be products of

the Information Age and, like universal bankers, will be qualified to provide financial guidance

across all aspects of their institution’s operations. Increasingly, advisors, consultants and

universal bankers are being empowered to waive fees on the fly if it means converting service

opportunities into sales events. Financial institutions enjoy a unique view into their customers’

most personal finances, and as the focus shifts from the Boomer investor to Gen X to the

Millennial, this data will be crucial in maintaining growth. Millennials will be the first generation

to have grown up with tellerless branches, PTM’s, and branches as “stores”. Smaller footprint

branches, featuring fully-automated services, with hoteling office space for financial

consultants, will be a familiar sight to them.

4.5 In conclusion, the advice/consultancy piece will replace lower-value teller cash transactions

by combining interactive technology, new staff roles and emphasis on private consultative

offices. Future generations of homebuyers, investors and account holders will be native to the

new branch model, as will be the consultant-advisors themselves. Financial institutions that

continue to employ the teller line model are at risk of becoming irrelevant and losing a large

fraction of their customer base.

A customer experience map showing the different retail zones in a financial branch.

5. RETAIL COMMUNICATIONS, BRANDING AND MERCHANDISING

Community banks and credit unions are morphing from the institutional to the store model.

Retail merchandising and commercial branding now play an essential role in communicating

offers, services and products to branch visitors. Similar to the more successful store brands,

financial institutions have become more sophisticated in the way they target prospects. The

branch is now analyzed in terms of discrete retail zones, each of which represents a different

stage of the customer journey, reflected by individual elements within each zone. Banks have

not traditionally provided particularly compelling environments; people actually speed up when

they walk past banks10. Today’s retail communications specialists therefore are faced with a

challenge in attracting new customers and engaging existing ones. However, by using data-

driven design, retail communications for banks and credit unions can be extremely effective.

The “science of shopping” has arrived in the financial industry and F.I.’s are realizing the

advantages in its application.

5.1 Experience mapping is used to model discrete sub-contexts in a customer’s journey through

a retail environment. The map takes into account all activities branch visitors engage in and

pieces together the various touchpoints to construct a holistic picture. This can then be

translated into a diagram similar to the one above. The experience map is basically the financial

institute’s floor plan with all the touchpoints, branding and messaging transposed upon it. This

simple explanation doesn’t properly do justice to the complex process of researching data sets

based on large samples of customer behavior. The experience map provides a kind of cross-

channel panorama of where in the branch customers encounter the different service offerings

and where best to site messaging related to those offerings. The map can be used to

characterize the touchpoints both quantitatively and qualitatively, and is a useful tool in

designing bank and credit union interiors. Retail communications specialists are best qualified

for these types of analyses.

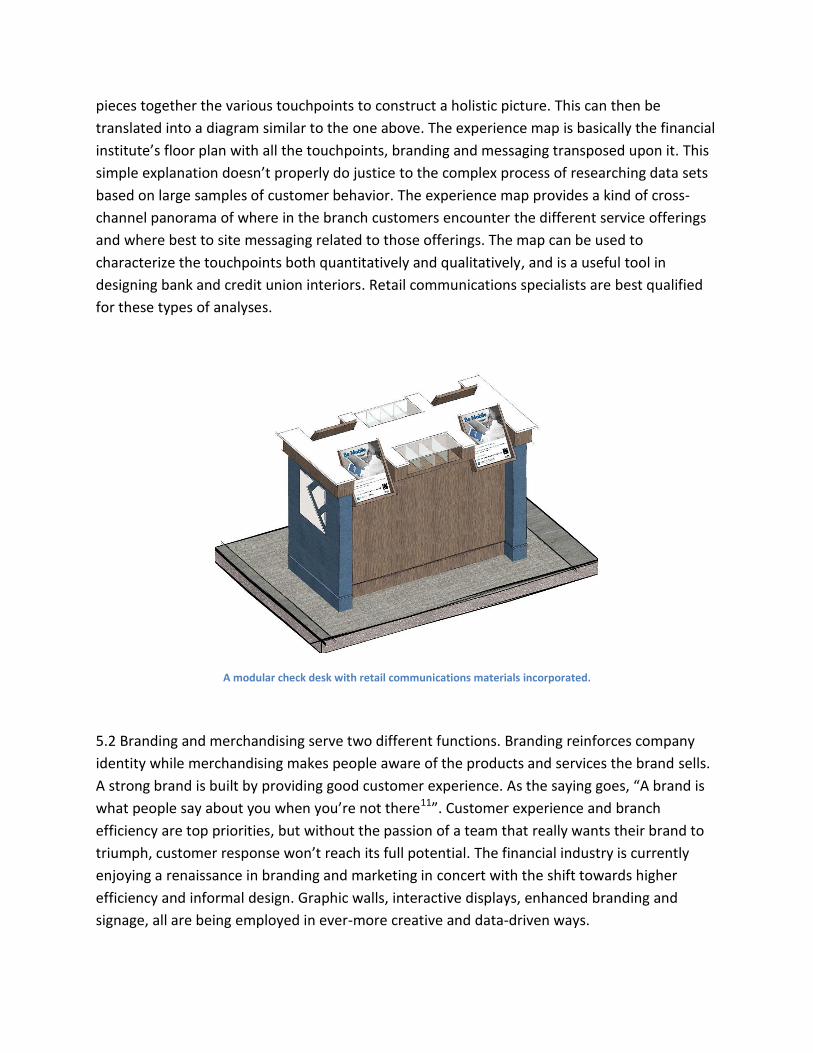

A modular check desk with retail communications materials incorporated.

5.2 Branding and merchandising serve two different functions. Branding reinforces company

identity while merchandising makes people aware of the products and services the brand sells.

A strong brand is built by providing good customer experience. As the saying goes, “A brand is

what people say about you when you’re not there11”. Customer experience and branch

efficiency are top priorities, but without the passion of a team that really wants their brand to

triumph, customer response won’t reach its full potential. The financial industry is currently

enjoying a renaissance in branding and marketing in concert with the shift towards higher

efficiency and informal design. Graphic walls, interactive displays, enhanced branding and

signage, all are being employed in ever-more creative and data-driven ways.

Retail communications can bring “dead space” to life and raise branch conversion rates.

5.3 Community banks and credit unions need to explicitly demonstrate that they’re part of and

invested in their communities for authentic customer relationships and for proper dialogue

banking to proliferate. An important aspect of this is the installation of graphic walls that

combine branding with iconic features of local history or general interest. These graphic walls

can take various forms, including flat-screen TV displays, 3-D fixtures, large photographs and

even lifelike models. An interior designer will know exactly where in the branch this should be

sited for maximum impact, as with other elements of the retail experience.

A modular display kiosk with digital messaging and brochure dispensers.

5.4 As stated, a branch refresh (or a new build, for that matter) is about far more than cosmetic

appearance, but cosmetics are certainly important. The power of the new branch lies in its

efficient layout and technology, both of which can be designed or selected to complement any

desired color scheme, construction materials or architectural style. In addition to the graphic

community wall, there should be strategically sited kiosks, displays and dispensers, each placed

in optimal locations for their respective purposes. The universal banker’s station is an effective

focal point for promotional displays, as customers can ask for and receive more information

immediately. Retail communications professionals use experience maps to control customer

flow through the branch, exposing consumers to targeted messaging at specific touchpoints.

This enhances the brand experience and raises per-square-foot profitability.

5.5 Effective messaging with an emphasis on dialogue and communication educates branch

customers in financial decision-making and makes them savvier asset holders. This builds on the

relationship theme; engagement banking creates loyal customers who ideally will become

brand advocates. Financial branch interiors are no longer as intuitively navigable as they once

were, when the teller line was the first place people went to begin any financial process. For

this reason, proper retail communications have become a crucial factor in exploiting efficient

designs that may include remote video ATM’s, consulting offices, roaming floor staff, dialogue

towers and even coffee bars.

Modular beverage center designed for a bank or credit union.

6. TECHNOLOGY BARS, CAFÉ-LOUNGES AND LEARNING SPACES

This final bullet point is concerned with the user-friendly and recreational aspects of a branch

refresh; tech bars and café-lounge spaces. Technology bars offer branch visitors access to

multiple financial channels, as well as secure public Wi-Fi where they can read the news, use

email, and even communicate with people over Skype in some cases. The tech bar setup is

quite uniform across the industry: A waist-high counter, either against a wall or as an “island” in

the middle of the branch floor, with several mobile devices sitting on it. These devices are

laptops, tablets and smartphones. The devices are pre-loaded with the F.I.’s own banking apps,

and customers can simply log in and perform self-service tasks. If they need assistance, there

will be universal bankers on hand to provide it. The branch may also offer coffee and other

beverages, in an even less formal environment with easy chairs, couches and coffee-tables.

6.1 The so-called “coffee-shop branch” is a reality, with many of today’s institutions more

resembling café-bars than banks. It could be said that internet cafés paved the way for lounge

banking, with the ability to charge mobile devices and connect to the internet, as well as

browse hard-copy magazines and brochures. In these financial institutions customers can

receive training on mobile devices and even check in to an online queue where they can await

an appointment with a universal banker. The devices are also carried by universal bankers for

casual, barrier-free interaction with branch visitors. As ever-greater numbers of consumers use

tech bars in branches, financial institutions will accumulate more data than ever before on their

customers’ banking habits by tracking device activity. This bodes well for F.I.’s who have already

carried out, or are currently considering, a branch refresh or a new branch build.

6.2 The concept of in-branch mobile devices might initially sound counterintuitive, but tech

bars (as well as customers’ own mobile devices) add up to a vastly more productive financial

experience. By creating firewalled opt-in applications, financial institutions can share more

personal information with customers. They can also track customer activity to the point where

branch staff is alerted when top-tier customers merely enter the branch, so they can be greeted

and engaged with immediately. Currently, F.I.’s can be oblivious to the physical presence of

prime customers and fail to initiate processes that lead to conversions. Similar to non-financial

shopping apps, banks and credit unions can also now target customers with offers and

promotions when they’re known to be in the branch neighborhood. Financial institutions that

achieve Omnichannel interactions will enjoy access to a considerable range of user data that

can be used to message them responsively in real-time.

6.3 There are several terms such as “VIP lounge”, “anti-bank”, and “café bank” being used to

describe the phenomenon of banks and credit unions incorporating the coffee-shop element.

The most common and practical version is a simple coffee and tea set-up based around a mid-

range brewing system. The branch provides cups, sugar, milk, etc, and possibly gives away

carry-mugs as a branding exercise. Furniture associated with this zone can be simple; a couple

of chairs and a coffee-table, with a tablet on it. This ensemble creates a mini-lounge, a

significantly less costly transition state than full-blown conversion to something more exotic.

There are F.I.’s that have taken the concept much further, however.

6.4 Return on investment is all-important, but some banks and credit unions have decided that

it’s worth it to go “all in” on a branch re-design and transform their image completely to that of

a café-style institution. These branches are also open to using their space for other community

activities, such as learning seminars, yoga practices, and even movie nights. These institutions

aren’t necessarily lavish (though some are), but instead embrace an urbane, edgier image.

Some are reminiscent of urban lofts, or premises converted from non-retail use, such as

warehouses and abattoirs. Others are more like hoteling or space-sharing outfits, with a fast

and fun attitude. There are branches that function as quasi-spas, where weary shoppers can

relax and enjoy a drink, while lounging and logging on to their financial apps. These types of

branches are most successful when located in neighborhoods with high foot traffic. The return

to the walkable neighborhood may well prove a boon to this model, as well as to community

banks and credit unions in general.

SUMMARY

Cosmetic branch makeovers do not improve ROI and discourage customer loyalty. To add value

to a branch and remain competitive, institutions must now look to processes that accelerate or

automate basic services and free up time to engage customers more deeply. These processes

include: Dialogue towers with cash recyclers installed; remote video machines; properly trained

universal bankers; retail communications, branding and merchandising designed by industry

professionals using experience maps; branch staff trained in the art of cross-selling and people

skills; technology bars where customers can log into mobile devices inside the branch; data

mining from banking apps, siting of private consultation booths or offices inside branches, and

community-oriented areas such as beverage centers, seminar spaces, and spa-lounges. Interior

design is still very much worthy of consideration, but decision-makers should transparently

convey their personal tastes in this regard to contractors and designers. The process of

selecting a company to perform a branch refresh or new build should not resemble a superficial

design contest. However, application of the above listed functional elements is crucial to the

success of modern financial institutions. Informed decisions on these types of upgrades have to

be carefully considered; realistic hurdle rates, payback periods and internal rates of return

cannot be calculated until branch offerings have been comprehensively assessed and marketing

of all capabilities optimized.

To learn more about branch renovations or new branch builds, make an appointment for a FREE

consultation with our financial industry professionals. Look out for our upcoming white papers,

“Meaningful Community Participation for Banks and Credit Unions” and “Creating the Omnichannel

Experience for Community Banks and Credit Unions”.

Mark Charette, CEO, Solidus.

860-838-3888

REFERENCES

[1] Specs for the RBG-100 Cash Recycler, Glory USA Inc.

[2] Source: New England Money Handling Systems, Inc.

[3] The American Bankers Association offers a Universal Bankers Certificate, which comprises 12 courses

spanning approximately 25 hours of study. The courses are available for one year from the date of

purchase.

[4] It’s interesting to note that the first drive-thru-incorporated business in the US was the City Center

Bank in Syracuse, NY in 1928, and not a restaurant as one might expect.

[5] There’s some debate about when the first ATM was invented and who invented it as several people,

beginning with Luther George Simjian in the late-1930’s, through the 1960’s and 1970’s with John

Shepherd-Barron, James Goodfellow, Don Wetzel, John D. White and Jairus Larson all claiming “firsts”.

In general, the popular version of the ATM was realized in various forms at the turn of the 1970’s.

[6] Image-enabled depository ATM’s that accept cash and check deposits via imaging, providing 24/7

transaction processing and credit upload within five minutes in most cases. Source: Sandy Dixon &

Associates, LLC.

[7] PTM image of SelfServ™ 32 Interactive Teller, NCR Corporation.

[8] For a more in-depth overview of what the Omnichannel means for financial institutions, please see

the Solidus white paper, “Creating the Omnichannel Experience for Community Banks and Credit

Unions”.

[9] The Boston Consulting Group, 2012.

[10] Why We Buy: The Science of Shopping, by Paco Underhill. Simon & Schuster (June 2, 2000)

[11] Jeff Bezos, CEO, Amazon.

Top Related