Languages

Pages

Legal

Association of Foreign Banks

13 May 2015, Stationer’s Hall, London

Adrian Ford – CEO, Aperio Intelligence Limited

Customer On-Boarding & AML Risk Issues

Agenda: Customer on-boarding & AML risk issues

Implications of the EU fourth anti-money laundering Directive

Current areas of UK regulatory focus and emerging issues

Transparency initiatives – corporate structures and Ultimate Beneficial Owners

Differing standards on identification of UBOs

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Progress of the EU fourth anti-money laundering Directive (MLD4)

Has now passed first reading at Council of European Union (April 2015)

Likely to pass second reading in current form shortly

Member states will have two years to implement the Directive

UK may seek to transpose into national law earlier

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Elements of the MLD4 relevant to customer on-boarding

Emphasises the risk-based approach (already well understood in UK)

Introduces changes relating to Simplified Due Diligence

Removes third country ‘equivalence’

Extends the definition of Politically Exposed Persons (PEPs)

Mandates tax evasion as a predicate offence (creating common EU standard)

Provides for the creation of central registers of beneficial owners in the EU

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Current UK regulatory focus

The FCA has undertaken two key AML reviews in recent years:

2011 AML thematic review: Bank’s management of high money-laundering risk situations

2014 update: How small banks manage money laundering and sanctions risk (focusing on high risk customers, PEPs and correspondent banking relationships)

Key findings from its 2014 update included:

Senior management engagement had improved

1/3rd of banks had inadequate resources

Staff often had a weak knowledge of money laundering risks

Some overseas banks struggled to reconcile group policies with higher UK standards

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Current UK regulatory focus (continued)

In addition, the FCA has found:

“Serious and persistent mishandling” of high risk accounts

Inadequate risk assessments

Inadequate governance of high risk customers

Questionable management judgments

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Steps proposed by the FCA to tackle shortcomings

The FCA has said it will:

Intervene earlier, e.g. restricting take-on of customers in high-risk locations

Increase the use of data to identify areas for intervention

Hold senior management to account (not just MLROs)

Increase the use of skilled persons and/or enforcement actions as required

Consider the need for formal attestation

Update its guidance, e.g. Financial Crime: a guide for firms

Additionally, the FCA is conducting shorter 2 – 4 day visits to assess levels of compliance at smaller firms

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Other areas of interest highlighted by the FCA

Firms’ strategies on customer de-risking

Virtual currencies and mobile payments systems

Adequate evidencing of information on source of wealth / source of funds

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Establishing Source of Wealth and Source of Funds

Source of Funds

Source of Wealth

Activity contributing to a business relationship or an occasional transaction

Information may have been collected as part of the Source of Wealth and Nature of Business enquiries

How the total wealth of the client is derived

Focus on the evolution of net worth, not just the activity contributing to the current relationship

Is wealth tainted by illegal activities?© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Substantiating Source of Wealth

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Practical issues that may arise:

Longstanding customer relationships

Unwillingness to deter potentially lucrative business

Reliance on verbal/undocumented assurances of RMs

Activities in opaque jurisdictions; cultures of secrecy or cultural sensitivities

Steps to address regulatory requirements:

Ask the customer, but seek independent confirmation

Document and review findings

Contemporaneous notes

Update as required

Recent case law – UK Privy Council

UK Privy Council decision in the case of Crédit Agricole Corporation and Investment Bank (Appellant) v Papadimitriou (Respondent) (Gibraltar)

Proprietary claim for proceeds of sale of valuable art-deco collection

Fraudulently sold by a family member via a Panamanian company, a Liechtenstein trust and a BVI company which held the bank account in Gibraltar

Use of a complex network of legal entities should have alerted the bank to the risk of money laundering

Bank should have made enquiries about the underlying legal purpose of the arrangement, not just the immediate source of funds

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Corporate transparency

“… dealing with tax evasion is not just about exchanging information. It is also about improving the quality and accuracy of that information. Put simply, that means we need to know who really owns and controls each and every company.”

David Cameron, 20 May 2013

“Ahead of the budget I set the treasury to work on providing further ways to pursue not just the tax evaders but those providing them with advice. Anyone involved in tax evasion, whatever your role, this government is coming after you. Unlike the last government, who simply turned a blind eye, this government is taking action now and will do so again at the budget.”

George Osborne, 23 February 2015

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

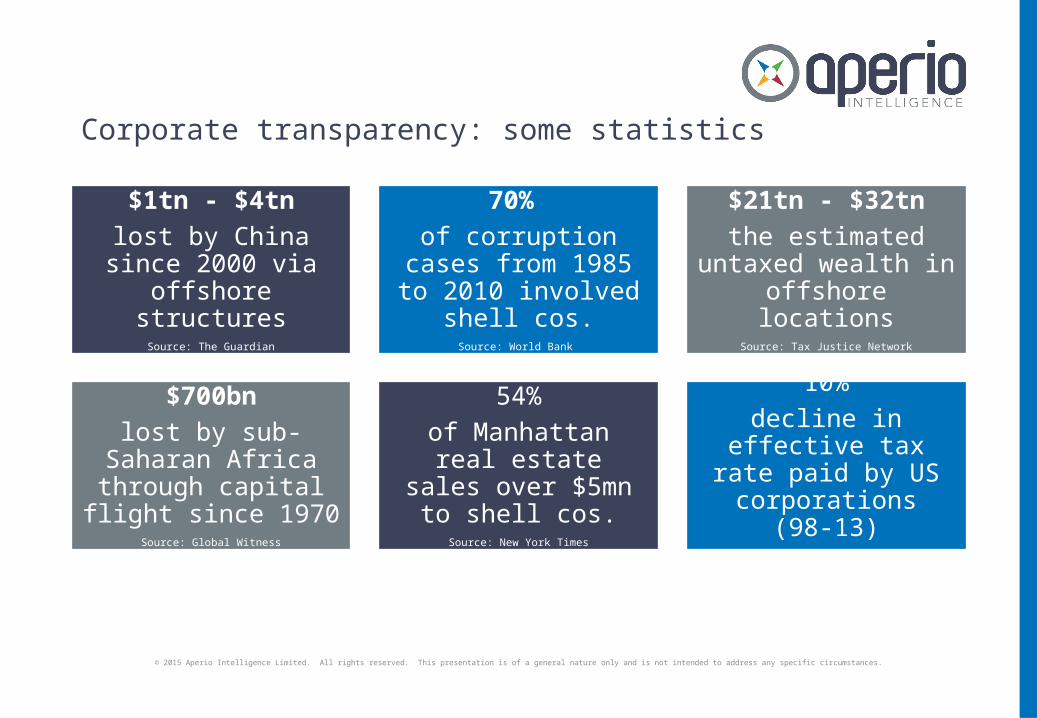

Corporate transparency: some statistics

$1tn - $4tnlost by China since 2000 via offshore

structuresSource: The Guardian

70% of corruption cases from 1985 to 2010 involved shell cos.

Source: World Bank

$21tn - $32tnthe estimated

untaxed wealth in offshore locations

Source: Tax Justice Network

$700bnlost by sub-Saharan

Africa through capital flight since

1970Source: Global Witness

54%of Manhattan real estate sales over $5mn to shell cos.

Source: New York Times

10%decline in effective tax rate paid by US corporations (98-

13)Source: Gabriel Zucman

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

UK and international initiatives to address corporate transparency issues

2013 - UK government consults on Transparency & Trust: Enhancing the transparency of UK company ownership and increasing trust in UK business

2014 – G20 issues statement on High-Level Principles on Beneficial Ownership Transparency

2014 – G8, under UK presidency, announces plans to create a register of beneficial owners

2014 – agreement on text of 4MLD, which contains provisions for creation of central registers of beneficial owners in the EU

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Beneficial ownership disclosure (UK)

Now covered by the Small Business, Enterprise and Employment Act 2015

Types of entities to which beneficial ownership disclosure will apply

Responsibility for updating beneficial ownership data

Repositories of information

Requirement and powers to investigate beneficial ownership

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Restrictions on bearer shares and corporate directors

Bearer share restrictions:

Issue of new bearer shares to be prohibited

Currently around 1,220 UK companies use bearer shares

Nine-month window to convert to registered shares, or cancel

Corporate director restrictions:

Heavy restrictions on use of corporate directors

Limiting “front” or “shadow” directors

Tightening director disqualification provisions

No register of nominee directors

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Determining beneficial ownership – varying requirements

Differing thresholds to determine beneficial ownership:

Most AML standards – 25%+ (including MLD4 and proposed FinCEN rules)

FATCA – 10%+ (where U.S. indicia)

U.S. Treasury OFAC – identifying holdings by Specially Designated Nationals of 50%+ in aggregate (where individual SDNs might own only 10%+)

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Summary

4MLD and the Risk-Based Approach

FCA’s recent findings and priorities

Source of wealth/funds considerations

Transparency initiatives

Variations in requirements to identify beneficial owners

© 2015 Aperio Intelligence Limited. All rights reserved. This presentation is of a general nature only and is not intended to address any specific circumstances.

Aperio Intelligence Limited125 Old Broad Street

London EC2N 1AR+44 (0)20 7073 0430

Registered Address: Carlton House, 101 New London Road, Chelmsford, Essex CM2 0PP.

Registered in England & Wales: 09164101 VAT: GB 195 2320 10

Top Related