Languages

Pages

Legal

Welcome, dear students !

Name:Muhammad Fahad Moaiz

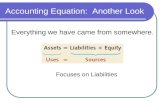

What is Accounting EquationAn Accounting Equation is a mathematical expression which shows that the assets andliabilities of a firm are equal.

An Accounting Equation is based on the dual aspect concept of accounting meaning, everytransaction has two aspects-debit and credit.

That further means in every business transaction for every debit there is a credit of equalamount and Vice Versa.

It means total claims (those of outsiders and of the proprietors) will always equal the totalassets of the firm.

The claims, also known as equities, are of two types:1. Owner's equity or capital and2. Liabilities or amounts due to outsiders (i.e., Outsiders Equity).

The relationship known as the Accounting Equation can be presented in equation form asgiven below in 4 ways:

And the Balance Sheet Equation can be presented in equation form as given as below:

Nature of Accounting Equation An Accounting Equation always holds true with every change that occurs due totransaction entered into. It is because of this reason that it is based on the dualaspect concept of accounting.

A transaction may affect either both sides of the equation by the same amount orone side of the equation only, by both increasing or decreasing it by equalamounts.

Transactions from the Accounting Equation viewpoint, can be divided into two,i.e.,1. Transactions Affecting Two Items and2. Transactions Affecting More Than Two Items.

Transactions Affecting Two items:As the title suggests, these are those transactions that affect two items of the accountingequation or Balance Sheet.

(a) Transactions affecting opposite sides are:

Increase in Asset, Increase in Liability.' Transaction such as credit purchases increase asset(stock) and also increase liability (creditor). Similarly, loans from bank increase asset (cash)and also increase liability (Loan).

Decrease in Liability, Decrease in Asset: Transaction of payment to a creditor decreasesLiability (creditor) and also reduces asset (cash or bank).

Increase in Asset, Increase in Owner's Equity: Introduction of capital by the proprietorincreases asset (cash or bank) and also liability (capital).

Decrease in owner's Capital, Decrease in Asset: Drawings by the proprietor decreasesliability (capital) and also asset (cash or bank).

(b) Transactions affecting same side butin opposite direction are:

Increase in one Asset, Decrease in Another Asset: Transactions such as cashpurchases or receipt from debtors increase one asset (goods and cash or bank,respectively) and decrease another asset (cash or bank and debtors).

Decrease in one Liability, Increase in Another Liability: Settlement of creditor by issueof Bill of Exchange decreases a liability (creditor) and increases another liability (BiII ofExchange).

Transactions Affecting More Than Two items:

Some transactions affect more than two items of the accounting equation or a BalanceSheet.

For example, when a sale is made in cash for Rs. 30,000, it is made at cost (Rs. 25,000)plus profit (Rs. 5,000).

• Cost of goods (Rs. 25,000) reduces asset (stock of goods);• Cash increases by Rs. 30,000; and• Owner's capital increases by the profit (Rs. 5,000).

It should be noted that profit increases the owner's capital and loss decreases it.

Procedure to prepare Accounting Equations

The procedure to workout an Accounting Equation is:

Analyze the transaction in terms of such variables as assets, liabilities, capital, revenuesand expenses.

Decide the effect of the transactions in terms of increase or decrease on variables assets,liabilities, capital, revenues and expenses.

Record the effect on the relevant side of the equation.

Illustrations

Let us take a few transactions to understand the accounting equation.

Transaction 1:Mr. Riaz commences his business with cash Rs.50,000.

This is an example of investment of asset in the business by the owner. The effect of this transaction on the accounting equation is that cash asset is increased by Rs.50,000 and the proprietorship (Riaz’s capital) is also increased by the same amount such as:

Assets = Liabilities + O.E/ Capital

Cash Riaz, Capital

+ 50,000 = —- + 50,000

Note that assets and equities increased by equal amounts

Transaction 2:Purchased furniture on cash Rs.10,000.

This transaction effected accounting equation as the increase in one new asset furniture and decreases in assets cash with the same amount. Thus

Assets = Liabilities + O.E / Capital

Cash Furniture Riaz, Capital

+ 50,000 = —- + 50,000

- 10,000 + 10,000

40,000 + 10,000 = 50,000

Note that this transaction has affected assets side only and no change is made in equities side of the equation.

Transaction 3:Purchased merchandise for cash Rs.10,000.

This transaction will introduce a new element (merchandise) on the assets side and decrease the cash by Rs.10,000.

Assets = Liabilities + O.E / Capital

Cash Furniture Merchandise Riaz, Capital

+ 40,000 + 10,000 = —- + 50,000

-10,000 – + 10,000

30,000 10,000 + 10,000 = 50,000

Note that this transaction has affected assets side only and no change is made in equities side of the equation.

Transaction 4:Purchased merchandise on account (on credit) Rs.5,000.

Assets = Liabilities + O.E / Capital

Cash Furniture Merchandise Creditors Riaz, Capital

+ 30,000 + 10,000 + 10,000 = + 50,000

+ 5,000 + 5,000

30,000 +10,000 + 15,000 = + 5,000 + 50,000

Note that this transaction has affected assets side and liabilities. Both the sides of equation has increased with the same amount.

Transaction 5:Sold merchandise for cash Rs.2,000 cost of these merchandise were Rs.1,500

Assets = Liabilities + O.E / Capital

Cash Furniture Merchandise Creditors Riaz, Capital

+ 30,000 + 10,000 + 15,000 = + 5,000 + 50,000

+ 2,000 - 1,500 + 500 (Profit)

+ 32,000 +10,000 + 13,500 = + 5,000 + 50,500

Note that this transaction has affected assets side and also the proprietorship. Difference between sales price and cost price is treated as profit and has been added to capital.

Assets = Liabilities + O.E / Capital

Cash Furniture Merchandise Debtors Creditors Riaz, Capital

+ 32,000 + 10,000 + 13,500 = + 5,000 + 50,500

- 3,000 + 4,000 + 1,000

32,000 +10,000 + 10,500 + 4000 = + 5,000 + 51,500

Transaction 6:Sold merchandise on credit for Rs.4,000 costing Rs.3,000.

Note that this transaction has affected assets side and also the proprietorship. Anew element “debtors” has been introduced. Difference between sales price and cost price is treated as profit and has been added to capital.

Transaction 7:Paid Rs.1,000 to creditors for merchandise purchased.

Assets = Liabilities + O.E / Capital

Cash Furniture Merchandise Debtors Creditors Riaz, Capital

+ 32,000 + 10,000 + 10,500 + 4,000 = + 5,000 + 51,500

- 1,000 - 1,000

31,000 +10,000 + 10,500 + 4000 = + 4,000 + 51,500

Transaction 8:Received cash from a debtor Rs 1,000 whom a sale on credit was made earlier.

This is an example of collection from debtors. This transaction is an exchange of one asset for another. the effect is on one side of the equation, i.e., asset side. Thus:

Assets Liabilities + O.E / Capital

Cash Furniture Merchandise Debtors Creditors Riaz, Capital

+ 31,000 + 10,000 + 10,500 + 4,000 + 4,000 + 51,500

+ 1,000 - 1,000

32,000 +10,000 + 10,500 + 3000 = + 4,000 + 51,500

IllustrationFor Commerce

Bachelors

Prepare the Accounting Equation on the basis of following:

1. Mr. Shiraz Khan started business and introduce capital Rs. 1,00,000 in cash.

2. Purchased goods in cash Rs. 50,000.3. Purchased from Bismillah Furnitures Rs. 20,000.4. Sold goods costing Rs. 25,000 for Rs. 35,000.5. Paid Bismillah Furnitures in cash.

1 100000 = 0 + 100000

2 Add 50000

Less 50000

100000 = 0 + 100000

3 Add 20000 = 20000 + 0

120000 = 20000 + 100000

4 Less -25000

Add 35000 = 0 + 10000

130000 = 20000 + 110000

5 Less -20000 = -20000 + 0

110000 = 0 + 110000

No. TransactionAsset

Rs= +

Capital

Rs

Shiraz Khan started business with cash

Purchased goods in cash

Liabilities

Rs

New EquationPaid Bismillah Furnitures

New Equation

New EquationPurchased Goods from Bismillah Furnitures

New EquationSold goods costing Rs 25000

for Rs 35000 (Note)

Note: Profit should be added in Capital.

Special Thanks: Prof Shiraz Khan

Sir

Thank You and All the very best in your preparation

Top Related