Languages

Pages

Legal

FDI Determinants & Risks on Host Economies

1 | P a g e

A Review of the Literature on FDI Inflows

and Determinants and Risks on Host Economies

Abstract

This paper surveys the recent burgeoning literature that empirically examines the

Foreign direct investment (FDI) decisions of multinational companies (MNCs) and the resulting

Economic affect across the world. This paper is attempted to discuss the pro and con’s of current

debate on allowing foreign direct investment (FDI) in India’s retail trade which primarily focuses on

two issues – employment and consumer welfare. The supporters of the move have developed

consumer centric arguments while the opponents are more concerned with its adverse impact on

employment. In the process, some key areas of concern remain untouched Here, I have identified the

following few which deserve due attention of policy makers. A literature review, interviews and an

econometric analysis are carried out in order to examine FDI’s impact on the industry. The

contribution of the paper is to evaluate what we can say with relative confidence about FDI as a

profession, given the evidence, and what we cannot have much confidence in at this point.

FDI Determinants & Risks on Host Economies

2 | P a g e

Acronyms FDI Foreign Direct Investment OCED Organization for Economic Co-operation and Development IMF International Monetary Fund IBRD International Bank for Reconstruction and Development UNCTAD United Nations Conference on Trade and Development MNE Multi National Enterprise

INTRODUCTION A simple definition of FDI would be –“An investor based in one country acquires an

Asset in another country with the intent to manage that asset” (OECD, 2000).

FDI eludes definition owing to the presence of many authorities:OCED, IMF,IBRD and

UNCTAD. All these bodies attempt to illustrate the nature of FDI with certain measuring

methodologies.I observe that FDI refers to capital inflows from abroad that invest in the

production capacity of the host economy.I describe FDI as a source of economic development,

modernization, and employment generation, whereby the overall benefits (dependant on the

policies of the host government)

“Foreign Direct Investment (FDI) flows are usually preferred over other

Forms of external finance because they are non-debt creating, non-volatile and

Their returns depend on the performance of the projects financed by the

Investors. FDI also facilitates international trade and transfer of knowledge, Skills and technology.”1

Buckley & Casson 2 An MNE was defined as a firm that owns and controls activities in two or

more different countries.

I think FDI plays an extraordinary and growing role in global business. It can provide a MNE

with new markets and marketing channels, cheaper production facilities, access to new

technology, products, skills and financing. For a host country or the foreign firm (MNE) which

receives the investment, it can provide a source of new technologies, capital, processes, products,

organizational technologies and management skills, and as such can provide a strong impetus to

economic development. Foreign direct investment, in its classic definition, is defined as a

company from one country making a physical investment into building a factory in another

1 Planning Commission of India, 2002. Report of the Steering Group on Foreign Direct Investment:

Foreign

Investment India.[government report]. p 11. New Delhi: Planning Commission, Government of India. Accessed on June 10, 2005. Available at http://planningcommission.nic.in/aboutus/committee/strgrp/stgp_fdi.pdf. Internet.

2 Buckley & Casson The Future of the Multinational Enterprise (1976).

FDI Determinants & Risks on Host Economies

3 | P a g e

country. The direct investment in buildings, machinery and equipment is in contrast with

making a portfolio investment, which is considered an indirect investment.

Literature review In my view all FDI is ‘endurance seeking’ as MNE’s have to survive in current competitive

global scenario otherwise they will perish.

Vertical Foreign Direct Investment takes place when a MNE owns some shares of a foreign

enterprise, which supplies input for it or uses the output produced by the MNE.

Horizontal foreign direct investments happen when a MNE carries out a similar business

operation in different nations.

Also, I think that FDI is not horizontal or vertical but linear as firms attain synergies through

dual operations.

Types of Foreign Direct Investment: An Overview

FDIs can be broadly classified into two types as given below. This classification is based on the

types of restrictions imposed, and the various prerequisites required for these investments.

outward FDIs

inward FDIs

In this review we will be concentrating on Inward FDI’s and its impact on economic growth

and the problems associated with it.

Different economic factors encourage inward FDIs. Laura Altinger 3These include interest

loans, tax breaks, grants, subsidies, and the removal of restrictions and limitations. I also

believe that factors detrimental to the growth of FDIs include necessities of differential

performance and limitations related with ownership patterns. I am also of the opinion that

Consistent economic growth, de-regulation, liberal investment rules, and operational

flexibility are all the factors that help increase the inflow of Foreign Direct Investment or

FDI.

Why MNE’s engage in FDI? Hymer (1959)4 was the first one to explore this

Phenomenon in his doctoral dissertation and stated ‘FDI as a means of transferring

tangible and intangible assets to organize international production.’

3 Laura Altinger 2010: FOREIGN DIRECT INVESTMENT, DOMESTIC INVESTMENT AND DEVELOPMENT:

ENHANCING PRODUCTIVE CAPACITIES P 14-15

4 Hymer, S. H. (1960): “The International Operations of National Firms: A Study of Direct Foreign

Investment”. PhD Dissertation. Published posthumously. The MIT Press, 1976. Cambridge, Mass.

FDI Determinants & Risks on Host Economies

4 | P a g e

Global FDI Inflows before the economic downturn

UNCTAD 2006 5 Trends of FDI Inflows across different economies

European Union Inflows: During the year 2006 the foreign direct investment made in the

economically developed countries has been $800 million. This has been an improvement of 48%.

The amount of foreign direct investment made in the United Kingdom has also been on the

higher side compared to the previous years. The 25 members of the European Union have

received 45% of the total foreign direct investment made in the year 2006.

The foreign direct investment in the members of the Organization for Economic Co-operation

and Development has been far from being impressive. The foreign direct investments made in

these countries have been on a downward slope since 2003. This situation has been brought

about by the relatively unimpressive economic performance of the significant members of this

association in the recent times.

Africa Inflows: In African continent the FDI inflow has touched new heights recently it is

estimated that more than $38 billion has been invested in the recent years and this is a record in

itself. The recent increase in the inflows has happened owing to the increase in the FDI that is

being made in countries that have high oil and other natural resources.

Caribbean & Latin American Inflows: In the Caribbean and the Latin American region the

rate of foreign direct investment has been on the wane. Mexico and Brazil are the leading

countries in this region as far as foreign direct investment is concerned. The inflows have

increased by 6% in Brazil and in Mexico the rate has been steady. Chile has experienced a 48%

increase in the foreign direct investment being made in their country. This has been owing to the

fact that the mining industry of Chile has had the lion's share of the reinvested earnings.

However, the foreign direct investments made in Argentina and Chile had gone down by 30%

and 52% respectively. In the countries like Bolivia, Venezuela and Ecuador the governmental

stance towards the extractive industries has changed. They are now pushing for increased

revenues, as well as governmental control. This is expected to have a negative effect on the

investors.

5 World Investment Report:UNCTAD 2006 FDI from Developing and Transition Economies:

Implications for Development (from internet) http://www.unctad.org/en/docs//wir2006_en.pdf

FDI Determinants & Risks on Host Economies

5 | P a g e

Asia and Oceania Inflows: In Asia and Oceania the FDI has been on the higher side. The figure

for 2006 was $230 billion and this was an improvement of 15% from 2005. China, Hong Kong

and Singapore have been the leading investment destinations in this area.

South Asian (India & China) Inflows: In the South Asian region, China and India have been

the leading investors. India has invested twice that what it did in 2005. India has also

experienced unprecedented levels of foreign direct investment in the country.

West Asian Inflows: In the West Asian region, countries like Turkey and others that have vast

oil reserves have also been receiving high foreign direct investment.

Developing countries are high beneficial of FDI when compared to developed countries.

I think MNE’s always look for developing economies.

“The most profound effect has been seen in developing countries, where yearly foreign direct

investment flows have increased from an average of less than $10 billion in the 1970’s to a

yearly average of less than $20 billion in the 1980’s, to explode in the 1990s from $26.7billion in

1990 to $179 billion in 1998 and $208 billion in 1999 and now comprise a large portion of global

FDI.. Driven by mergers and acquisitions and internationalization of production in a range of

industries, FDI into developed countries last year rose to $636 billion, from $481 billion in

1998” (Source: UNCTAD)

FDI Determinants & Risks on Host Economies

6 | P a g e

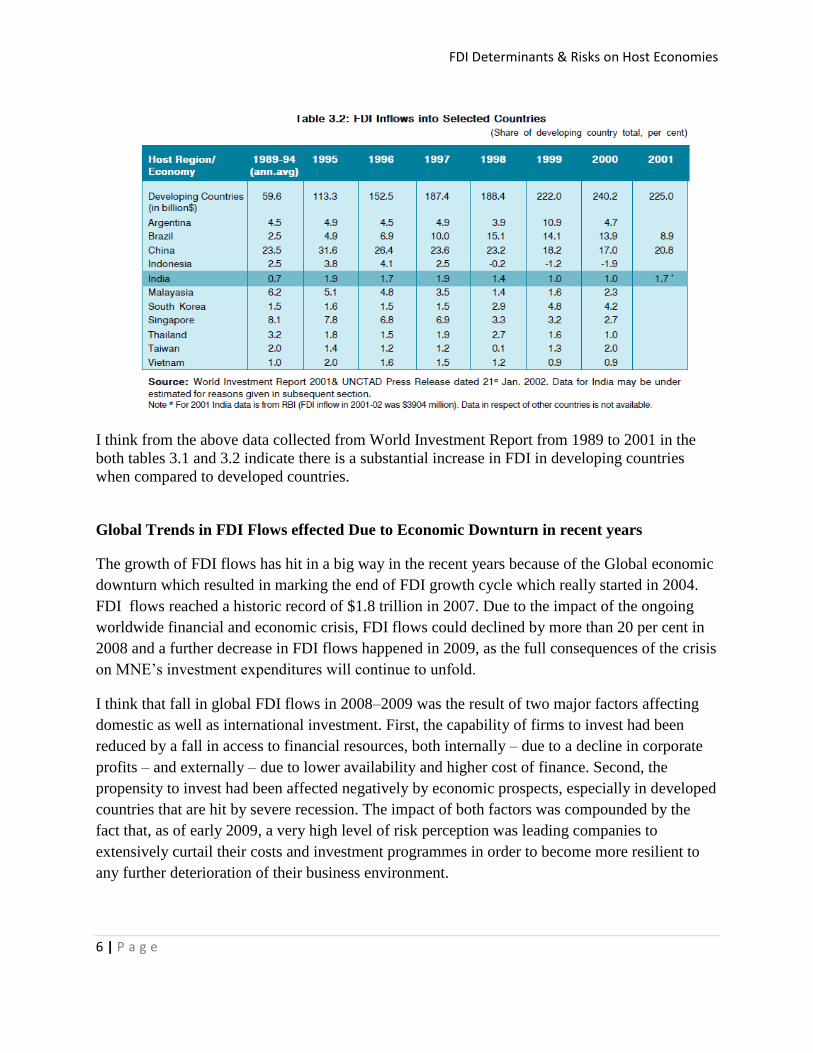

I think from the above data collected from World Investment Report from 1989 to 2001 in the

both tables 3.1 and 3.2 indicate there is a substantial increase in FDI in developing countries

when compared to developed countries.

Global Trends in FDI Flows effected Due to Economic Downturn in recent years

The growth of FDI flows has hit in a big way in the recent years because of the Global economic

downturn which resulted in marking the end of FDI growth cycle which really started in 2004.

FDI flows reached a historic record of $1.8 trillion in 2007. Due to the impact of the ongoing

worldwide financial and economic crisis, FDI flows could declined by more than 20 per cent in

2008 and a further decrease in FDI flows happened in 2009, as the full consequences of the crisis

on MNE’s investment expenditures will continue to unfold.

I think that fall in global FDI flows in 2008–2009 was the result of two major factors affecting

domestic as well as international investment. First, the capability of firms to invest had been

reduced by a fall in access to financial resources, both internally – due to a decline in corporate

profits – and externally – due to lower availability and higher cost of finance. Second, the

propensity to invest had been affected negatively by economic prospects, especially in developed

countries that are hit by severe recession. The impact of both factors was compounded by the

fact that, as of early 2009, a very high level of risk perception was leading companies to

extensively curtail their costs and investment programmes in order to become more resilient to

any further deterioration of their business environment.

FDI Determinants & Risks on Host Economies

7 | P a g e

UNCTAD 2009 Press release 6 confirms the instability in the financial sector and the global

economic slowdown. It also shows the uneven magnitude of the setback in international

investment among regions and industries. Developed countries were the most affected in 2008

whereas developing countries were affected badly in 1997 (such as the 1997 Asian crisis, see

UNCTAD, 1998) and had a significant negative influence on FDI inflows in a number of them

(such as Indonesia). The world economy is slowly regaining its momentum after universal

economic downturn and which in turn will help FDI inflows into different countries back to time

when it reached its peak in 2007.

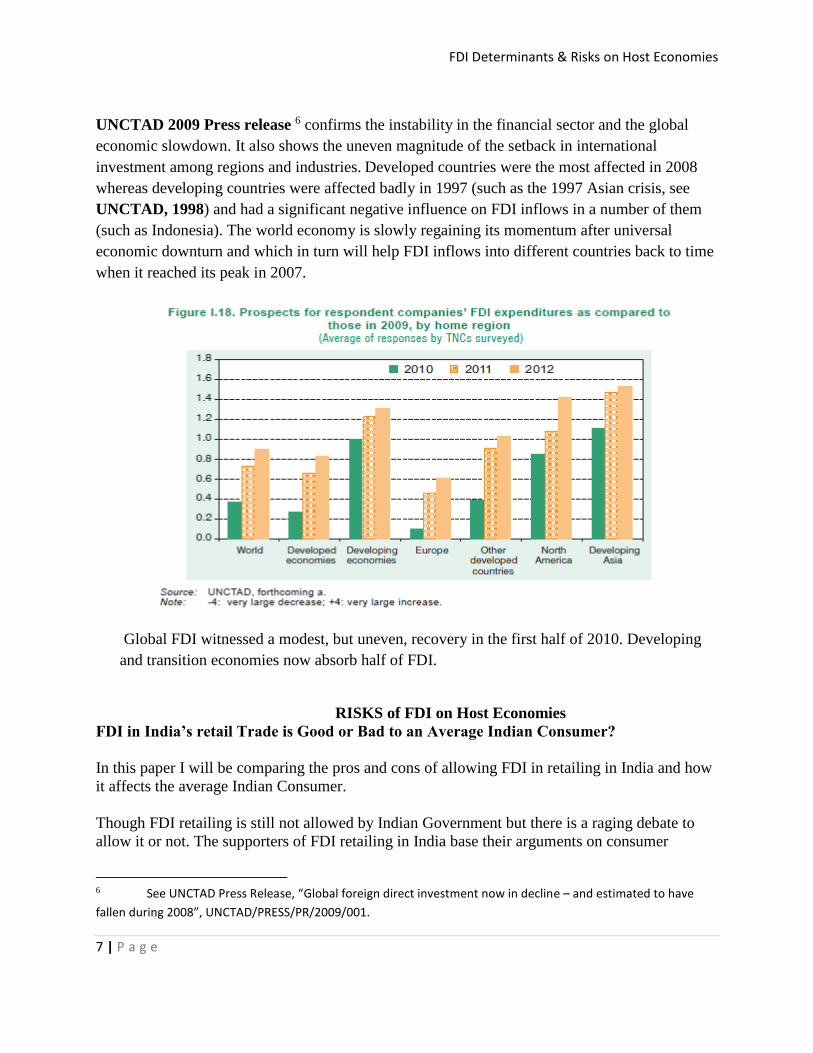

Global FDI witnessed a modest, but uneven, recovery in the first half of 2010. Developing

and transition economies now absorb half of FDI.

RISKS of FDI on Host Economies

FDI in India’s retail Trade is Good or Bad to an Average Indian Consumer?

In this paper I will be comparing the pros and cons of allowing FDI in retailing in India and how

it affects the average Indian Consumer.

Though FDI retailing is still not allowed by Indian Government but there is a raging debate to

allow it or not. The supporters of FDI retailing in India base their arguments on consumer

6 See UNCTAD Press Release, “Global foreign direct investment now in decline – and estimated to have

fallen during 2008”, UNCTAD/PRESS/PR/2009/001.

FDI Determinants & Risks on Host Economies

8 | P a g e

welfare whereas the opposing group of people is more concerned about the job losses if FDI is

allowed in retailing. This paper attempted to shed light on the issues which might help policy

makers to take a notice before making a final decision on whether to allow FDI retailing or not.

Guruswamy et al. (March, 2005)7 deliberated on this issue in detail and made an empirical

estimation of the future job losses, should the government allow entry of FDI in retail sector. The

estimated job loss ranged between 4,32.000 and 6,20,000.To analyze the effect of FDI on Indian

retail sector, I have made two different hypothesis of Indian economy in the next five years when

the level of FDI inflow is expected to increase and basing on the arguments of pro and con’s

allowing FDI retailing in India.

Hypothesis 1 – Assume if the economy grows at a faster rate, say like 10-12% or above and the benefits

of growth ‘travels/flows down’ the line (not “trickles down”) benefiting even the poorest of the poor.

Economic and social disparity reduces, which results in no difference between haves and have not’s

(‘poverty line’) becomes a topic of economic past, and purchasing power increases across different

economic classes and Human Development Index (HDI) improves substantially since people are

economically well off.

Hypothesis 2 – Assume if the economy grows at a faster rate, say like 10-12% or above but the benefits

of growth “trickles down” at a slower rate. Economic and social disparity widens, middle class and poorer

sections get marginalized resulting in big gap between have’s and have not’s, purchasing power of the

majority of the population does not improve, transition towards market economy becomes painful, and

there will be increase in “jobless growth”. The working class loses its bargaining strength and Human

Development Index (HDI) reduces substantially since majority of people are not economically well off

resulting in increase in crimes.

Hypothesis 1 gets approval from (ICRIER report 2005)8 recommends that FDI should be allowed

in retailing since it would speed up the growth of organized formats. The study found that

organized retailing has significant backward linkages by setting up of supply chains, investment

in food processing industry and manufacturing units, increased productivity of agriculture,

growth of interlinked sectors such as tourism and IT. Consumers have also gained from

organized retailing since it leads to lower prices, improves the quality of products and widens the

choice of products available to consumers.

ICRIER found in the report there would be only be mild effects on small shopkeepers found by

the ICRIER study is perhaps precisely the protectionist measures taken by Indian government

against foreign chains. I think that the local retail chains don’t have enough financial clout and

know how in order to drive a significant reduction in prices. Furthermore, I think it is reasonable

to think that the first wave of hypermarkets were open in rather well off areas, where lots of

customers are more sensible to choice then to price. I feel ICRIER has walked the rope rather

7 Mohan Guruswamy et al. 2005 : FDI in India’s Retail Sector More Bad than Good? February 12, The

Economic and Political Weekly, Mumbai.(internet find:

http://www.indiafdiwatch.org/fileadmin/India_site/CPAS_report.pdf)

8 ICRIER 2005 Survey report : Press release July 14,2005 can be obtained by the following link

FDI Determinants & Risks on Host Economies

9 | P a g e

cautiously, of course based on this report. It feels there will be a slump but five years hence. In

all practicality, there is going to be a slump for mom-n-pop shops. The demographic conditions

on India are such that it cannot live without these shops. Agreed the buying power of the Indian

consumer has increased but that has not produced a serious shopper in him. Even today going to

mall is equated as a family outing in the Indian mentality.

Wal-Mart is the world’s largest retailer regardless which matrix you use to measure the size of

the retailer and they ventured into India with a joint venture with Bharati and one thing they can

not do right now is front end retail. Wal-Mart India-Bharati are trying to lobby with the Indian

government and urging them to allow FDI in retail which will result in 2 million more jobs by

2013 and also result in bringing down food inflation by 20 to 30 basis points and it also pointed

out that INDIA requires at least 21 billion dollars in infrastructure development in retail which

mom and pops and Indian retailers will be unable to invest. The government is reluctant to allow

foreign companies to enter front-end retail fearing it will lead to large scale closure of mom and

pops stores which is a large vote bank of any government .Even though I do agree with some

valid points raised by walmart-bharthi because the mom & pop stores will not be able to raise the

capital for infrastructure. As per one survey done by dept of agriculture recently it was found that

a large of fresh produce gets wasted when it goes through unorganized retail these days if the

FDI is allowed and big retailers like Wal-Mart enters the fray the fresh produce will not be

wasted. I think it is the classic battle between producers/sellers and consumers. In India millions

of consumers lose the battle because of few thousand mom-and-pop sellers in some instances. In

a free democracy like India, market alone should be allowed to determine who survives and who

does not. Moreover there is a political pressure on Indian Congress government from opposition

parties like Bharatiya Janata Party (BJP) and Indian Communist and Marxist (CPI & CPM) are

very vocal against allowing FDI into retailing since most of the middle men and small time

retailers will be out of jobs and these parties wants to protect their vote bank are dead against the

FDI into retail.

So the Hypothesis 1 works only good when the If the social economic condition in the next five

years prevails in the same way as described in Hypothesis 1, issues like employment loss would

lose to attract much attention, as the expanding economy with better distributional equity would

be able to absorb such shocks. Moreover, with a general rise in purchasing power, consumer

would prefer more choices and better quality of products, which a modern retail chain would be

able to offer. In this context we must be concerned about the statement the Finance Minister,

Mr.P. Chidambaram, made while making the midyear review for 2004-05. “On retail, the review

notes that creating an effective supply chain from the producer to the consumer is critical for

development of many sectors, particularly processed and semi-processed agro-products. In this

FDI Determinants & Risks on Host Economies

10 | P a g e

context, it says, the role that could be played by organized retail chains, including international

ones merits careful attention.”9

When I observe the recent social economic trends, the projection as per Hypothesis 2 is more

likely. If FDI is allowed in retailing as per the request of MNE’s, we will have, on one hand,

smaller spreads between “disorganized” and “organized” prices. On the other hand, customers

that put a premium on their time. In that respect, the small, close to home shops could survive as

a handy alternative at the end of a working day. I don’t believe these conditions could be

replicated further, as the retail chains will expand to poor areas.

I am not supporting protectionism. I simply doubt that further expanding the “organized” retail

will have so little effect on small shopkeepers and more over the small shop keepers have a very

good personal rapport with their consumers and most of the shopping is done by the Indian house

wife’s and most of them tend to go to mom and pop shops because they are easily accessible and

they get a good personal customer service. Moreover some of the Indian customers will have a

running debt with the regular mom and pops stores and they back whenever the consumer and

shopkeeper agreed upon this type of payment cannot be done with the regular big time retailers.

So Hypothesis 1 and ICRIER report 200510 confirm that FDI should be allowed in retailing and

this model works for the UK or Western Europe and may or may not work in India if FDI is

allowed in retailing because about 60% of India lives in the villages, to whom the supermarkets

are definitely not going to cater. The supermarkets are going to cater to the "middle class". But

what the "middle class" "and elite class” needs is not what India needs. Supermarkets are not a

pressing need; investment in infrastructure, compulsory primary education and basic universal

health care are what are required. But the fate of these corporations & their shareholders &

affiliates in India are not what should govern Indian policy. Indian policy should be focused on

the villages and the development of the village-dwellers.

As per (Kurten’s: When Corporations Rule the World)11 there is a no way Indian retailer will

ever be able to compete with the huge financial muscle of a Wall Mart or a Tesco. Thailand is a

country which went down the Tesco-Carrefour route & then realized what it had done to its mom

& pop stores. After all it is the welfare of these store-owners which should be the Indian

government's concern, not that of the shareholders of Wal-Mart, Tesco & Carrefour, which in all

likelihood are owned by Western mutual funds etc.

9 Review hints at FDI in retail, pp 1-15, Times of India, 14 Dec.2004

10 ICRIER 2005 Survey report : (Dr. Arpita Mukherjee, Ms. Nitisha Patel) Press release July 14,2005 can be

obtained by the following link (http://www.icrier.org/conference/2006/14july_05.html)

11 Korten's: When Corporations Rule the World & The Rise & Rise of Tesco 83

FDI Determinants & Risks on Host Economies

11 | P a g e

The small Mom & Pop stores that capitalist & elitist hates is what brings a quick personal touch

to shopping. Huge malls are more interested in bottom lines. Local shops and merchants offer

services like home delivery, quick product procurement, and higher-salary/profit employment,

local investment, etc. Huge malls strip away the wealth to feed to their CEOs multi-million

dollars, pollute the local environment a lot, and when strip-mined bare, they close and go.

In India millions benefit from small shops which are quick to access, provide Door services

(unlike Wal-Mart), and quick to heed only to consumer wishes. A large Wal-Mart decides what

the customer must buy. A diverse small shop locality knows the customer is the king.

In this context, the experience of Thailand, which opened up its retail sector for FDI in the

1980s, could be an eye opener for us. The Thai government liberalized their trading sector which

resulted in European retail giants Tesco, Carrefour had set up their operations in Thailand. As

expected, many of the traditional retailers had to down their shutters unable to compete with

global firms in an unequal fight. For example, traditional traders controlled 74% of the retail

market in 1997 but by 2002, their share came down to 60%. Faced with severe criticism from

local retailers, the government announced that they would put control on large retail

establishments by imposing the zoning policy regulation. In 2002, the ‘Retail Business Act' was

enacted to control the expansion of foreign retailers. However, the Thai government changed

their decision on zoning regulation allegedly under pressure from European Commission (EC)

who had requested Thailand to open up their retail sector for foreign retailers.

India is a larger economy than Thailand with a mature political system. In the changed global

trading environment, to protect the interest of its small producers and workers how government

of India will be able to bargain with opposition political parties and MNE’s and parties affected

(small retailers) by its decisions to allow FDI in retail trade is another important issue that should

be monitored carefully.

FDI - Exploitation of Labor

Exploiting workers in poor countries and initiating a "race to the bottom" in environmental and

labor standards. The experience comes from countries like Singapore, China, Chile and Ireland

which demonstrate how foreign direct investment (FDI) - with its transfer of technical and

organizational innovations and best practices stimulate rapid growth in incomes for all members

of society. When international flows of capital falter there's evidence that the poor in developing

countries suffer the most. In an interview, World Bank President James D. Wolfensohn12

predicted that between 20,000 and 40,000 more children may die worldwide and some 10 million

more people may be condemned to live below the poverty line of one dollar a day because of the

global economic aftershocks.

12 Interview with president of world bank James D. Wolfensohn

http://discuss.worldbank.org/content/interview/detail/2058/

FDI Determinants & Risks on Host Economies

12 | P a g e

The extent to which foreign investment can help or harm the poor largely depend upon what

governments and firms choose to do. Many multinational companies voluntarily adopt

environmental, social, and governance practices designed precisely to guard against abuse of the

environment and the workforce when they invest in developing countries. But governments in

developing countries should facilitate and encourage the transfer of this social and environmental

practice and maximize the benefits from FDI. A Government keen to ensure FDI is truly pro-

poor should follow the following points.

Climate change I believe, now many people accept as real the phenomenon of climate change, And there is a

long overdue in building it in as a factor in structural specifications and in regulation .Any

industry involving substantial open air storage of residues in ponds and lagoons need to take

account of the fact that the structures which in the past were quite adequate to withstand the

worst weather conditions of the last fifty or hundred years , may not be adequate to withstand the

conditions which may prevail in the ten years ahead. Those responsible for structure design and

regulation need to take note.

Vedanta, a British Mining Company 13has been criticized by human rights and activist groups,

including Survival International and Amnesty International, due to their operations in Niyamgiri

Hills in Orissa, India that are said to threaten the lives14 of the Dongria Kondh that populate this

region. The Niyamgiri hills are also claimed to be an important wildlife habitat in Eastern Ghats

of India as per a report by the Wildlife Institute of India as well as independent reports/studies

carried out by civil society groups. In January 2009, thousands of locals formed a human chain

around the hill in protest at the plans to start bauxite mining in the area.

Determinants of Foreign Direct Investment

What are the determinants of FDI?

One of the most important determinants of foreign direct investment is the size as well as the

growth prospects of the economy of the country where the foreign direct investment is being

made. It is normally assumed that if the country has a big market, it can grow quickly from an

economic point of view and it is concluded that the investors would be able to make the most of

their investments in that country. In case of foreign direct investments that are based on export,

the dimensions of the host country are important as there are opportunities for bigger economies

of scale, as well as spill-over effects. The population of a country plays an important role in

attracting foreign direct investors to a country. In such cases the investors are lured by the

13 Vedanta British Mining company http://en.wikipedia.org/wiki/Vedanta_Resources

14 British mining company threatens sacred mountain

http://www.survivalinternational.org/tribes/dongria

FDI Determinants & Risks on Host Economies

13 | P a g e

prospects of a huge customer base. Now if the country has a high per capita income or if the

citizens have reasonably good spending capabilities then it would offer the foreign direct

investors with the scope of excellent performances. The status of the human resources in a

country is also instrumental in attracting direct investment from overseas. There are certain

countries like China that have taken an active interest in increasing the quality of their workers.

The Chinese government has made it compulsory for every Chinese citizen to receive at least

nine years of education. This has helped in enhancing the standards of the laborers in China. If a

particular country has plenty of natural resources it always finds investors willing to put their

money in them. A good example would be Saudi Arabia and other oil rich countries that have

had overseas companies investing in them in order to tap the unlimited oil resources at their

disposal. Inexpensive labor force is also an important determinant of attracting foreign direct

investment. The BPO revolution, as well as the boom of the Information Technology companies

in countries like India has been a proof of the fact that inexpensive labor force has played an

important part in attracting overseas direct investment. Infrastructural factors like the status of

telecommunications and railways play an important part in having the foreign direct investors

come into a particular country. I observed that if the infrastructural facilities are properly in place

in a country then that country receives a substantial amount of foreign direct investment. If a

country has extended its arms to overseas investors and is also able to get access to the

international markets then it stands a better chance of getting higher amounts of foreign direct

investment.

Literature review on FDI determinants suggests that market size (Lall

et al, 200315), market growth rates (Jenson16, 2003), political stability (Anantaram17, 2004),

Corruption (Wei18, 2003), exchange rate (Crowley and Lee, 200319), labor productivity

(Ramamurti20, 2004), economic freedom (Lee21, 2005), infrastructure (Chantasasawat, 15 Lall, Sanjaya, “Foreign Direct Investment in South Asia”, Asian Development Review,

11:1, 103-119, 1993

16 Jenson, Nathan M., “Democratic Governance and Multinational Corporations: Political

Regimes and inflows of Foreign Direct investment.” International Organization, 57, 587-

616, 2003

17 Anantaram, Rajeev, “The Empirical Determinants of State-wise Foreign Direct

Investment in India: Evidence From The Reform Years (1991-2002)”, Doctoral

Dissertation, 2004

18 Wei, Wenhui, “Foreign Direct Investment in China”, Doctoral Dissertation, 2004

19 Crowley, P., and Lee, J., “Exchange Rate Volatility and Foreign Investment:

International Evidence”, International Trade Journal, 13:1-26, 2003

20 Ramamurti, R., “Developing Countries and MNC’s: extending and enriching the

research

agenda”, Journal of International Business Studies, 35,277-283, 2004

FDI Determinants & Risks on Host Economies

14 | P a g e

2004), openness (Singh and Jun, 1995), human capital (Hsiao, 2001), and taxes affect

FDI flows to global markets.

Conclusions

The FDI debate has opened up many issues which deserve proper attention of the policy

makers before the retail sector is opened up to foreign investors. The findings and

deliberations in this paper reveal that unlike in other sectors, FDI in retail will have a

much wider impact on the economy. Essentially, organized global retail chains will break

the traditional symbiotic relationship that exists between small producers and small

retailers. Also, in the new retailing format, due to unequal terms of trade in a monopoly

like situation, small producers and suppliers are likely to suffer most.

21 Lee, Jim, “Cross Country Evidence On The Effectiveness Of Foreign Investment

Policies”, The International Trade Journal, Volume XIX, No.4, Winter 2005

FDI Determinants & Risks on Host Economies

15 | P a g e

REFERENCES

Peter J Buckley, M. C. (1976). The Future of the Multinational Enterprise , Journal of

International Business Studies (2009) 40, 1563–1580; doi:10.1057/jibs.2009.49.

Hymer, S. H. (1960): “The International Operations of National Firms: A Study of Direct

Foreign Investment”. PhD Dissertation. Published posthumously. The MIT Press, 1976.

Cambridge, Mass.

Guruswamy M, Sharma K, Mohanty JP, Korah T, 2005, FDI in India’s Retail Sector – More Bad

than Good, February 12, The Economic and Political Weekly,Mumbai. (Internet Link

http://www.indiafdiwatch.org/fileadmin/India_site/CPAS_report.pdf)

M.Casson (ed.), The Growth of International Business. Allen and Unwin, London.

Xing, Y.Q. (2004). Japanese FDI in China: Trend, Structure, and the Role of Exchange Rates.

International Development Program, International University of Japan, Yamato-machi, Niigata-

ken.<http://www.iuj.ac.jp/faculty/xing/papers/FDI_JC_xing.pdf> accessed on 7th Mar. 2004.

Planning Commission of India.2002. Report of the Steering Group on Foreign Direct Investment:

Foreign Investment India.[government report]. p 11. New Delhi: Planning Commission,

Government of India.Accessed on June 10, 2005. Available at

http://planningcommission.nic.in/aboutus/committee/strgrp/stgp_fdi.pdf. Internet.

Buckley & Casson The Future of the Multinational Enterprise (1976).

Yunshi, M and Jing, Y. (2005). Overseas investment trends change with times. China Daily, 11

October.

UNCTAD (2004). The Shift Towards Services. New York: United Nations.

UNCTC (1992). The Determinants of Foreign Direct Investment --- A Survey of the Evidence,

New York and

Geneva: United Nations.

UNCTAD (1995). World Investment Report, Transnational Corporations and Competitiveness,

New York and

Geneva: United Nations.

DETERMINANTS OF FDI IN CHINA

©Journal of Global Business and Technology, Volume 1, Number 2, Fall 2005 33

FDI Determinants & Risks on Host Economies

16 | P a g e

Vernon, R. (1979). The product cycle hypothesis in a new international environment. Oxford

Bulletin of

Economics and statistics, 41, pp255-267.

Wei, Y. and Liu, X. (2001), Foreign Direct Investment in China: Determinants and Impact,

Edward Elgar,

UK.

Lall, Sanjaya, “Foreign Direct Investment in South Asia”, Asian Development Review,

11:1, 103-119, 1993

Jenson, Nathan M., “Democratic Governance and Multinational Corporations: Political

Regimes and inflows of Foreign Direct investment.” International Organization, 57, 587-

616, 2003

Anantaram, Rajeev, “The Empirical Determinants of State-wise Foreign Direct

Investment in India: Evidence From The Reform Years (1991-2002)”, Doctoral

Dissertation, 2004

Wei, Wenhui, “Foreign Direct Investment in China”, Doctoral Dissertation, 2004

Crowley, P., and Lee, J., “Exchange Rate Volatility and Foreign Investment:

International Evidence”, International Trade Journal, 13:1-26, 2003

Ramamurti, R., “Developing Countries and MNC’s: extending and enriching the research

agenda”, Journal of International Business Studies, 35,277-283, 2004

Lee, Jim, “Cross Country Evidence On The Effectiveness Of Foreign Investment

Policies”, The International Trade Journal, Volume XIX, No.4, Winter 2005

Top Related