Languages

Pages

Legal

6-1

REPORTING AND ANALYZING INVENTORY

6

Determine the cost of goods sold and ending inventory

6-2

Classifying InventoryClassifying InventoryClassifying InventoryClassifying Inventory

One Classification:

Merchandise

Inventory

Three Classifications:

Raw Materials

Work in Process

Finished Goods

Merchandising Company

Manufacturing Company

Regardless of the classification, companies report all inventories under Current Assets on the balance sheet.

6-3

Physical Inventory is taken for two reasons:

In a Perpetual System

1. To compare the accuracy of inventory accounting records to

the actual inventory on hand.

2. To determine the amount of lost inventory from wasted raw

materials, customer shoplifting, or employee theft.

In a Periodic System

1. To determine ending inventory

2. To determine the cost of goods sold for the period.

3. The periodic inventory is not very accurate at identifying the

amount of inventory lost. The amount not counted in ending

inventory is simply assumed to have been sold or missing.

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

6-4

Taking a Physical Inventory: Involves counting (boxes), weighing (topsoil), or measuring (fabric, liquids) each kind of inventory on hand usually when the business is slow, closed or at the end of the accounting period. Note: when you count a box that’s supposed to have a TV in it, you must make sure there actually is a TV in it and it matches with the one listed in the accounting records!

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

Consigned Goods: Goods held for sale by one party even though ownership is still retained by another party. Someone else’s goods in on consignment at your store are not included as your inventory! Your goods out on consignment are still included in your inventory!

6-5

Unit costs can be applied to quantities on

hand using the following costing methods:

Specific Identification

First-in, first-out (FIFO)

Last-in, first-out (LIFO)

Average-cost

Inventory Inventory CostingCostingInventory Inventory CostingCosting

Cost Flow Assumptions

Management decides which inventory costing method is best to use!

6-6

Assume that Frank N. Furter TV Company purchases three

identical 50-inch TVs on different dates at costs of $700,

$750, and $800. During the year Furter sold two sets at

$1,200 each. These facts are summarized below.

Inventory CostingInventory CostingInventory CostingInventory Costing

6-7

Specific Identification

Inventory Costing – Specific IndentificationInventory Costing – Specific IndentificationInventory Costing – Specific IndentificationInventory Costing – Specific Indentification

If Furter sold 2 of the TVs it purchased on February 3 and May 22

for $2,400 ($1,200 each), then its cost of goods sold is $1,500

($700 + $800), and its ending inventory is $750.

6-8

A physical flow costing method: items in inventory each

have their own cost, they are added together to arrive at the

total cost of the ending inventory.

Use of this method is rare: used for unique items such as

precious gems, custom-made cars, antiques, one-of-a-kinds.

On the other hand, for similar type items, most companies

make assumptions called Cost Flow Assumptions about

which units were sold.

Inventory Costing – Specific IndentificationInventory Costing – Specific IndentificationInventory Costing – Specific IndentificationInventory Costing – Specific Indentification

Specific Identification

6-9

Inventory CostingInventory CostingInventory CostingInventory Costing

The Cost Flow

Assumption

The recorded cost

does not need to

match the physical

movement of goods

From a survey of large corporations

6-10

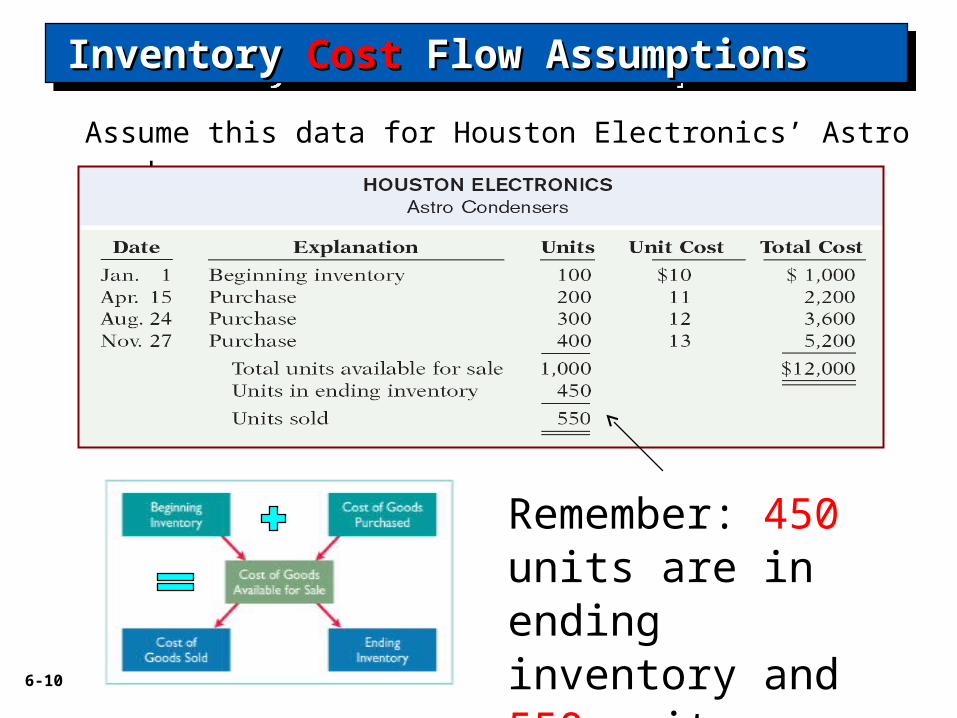

Assume this data for Houston Electronics’ Astro condensers.

Inventory Inventory CostCost Flow Assumptions Flow AssumptionsInventory Inventory CostCost Flow Assumptions Flow Assumptions

Remember: 450 units are in ending inventory and 550 units were sold!

6-11

Allocates cost of goods available for sale on the

basis of weighted-average unit cost incurred.

Assumes goods are similar in nature (gas, oil).

Applies weighted-average unit cost to the units

on hand to determine cost of the ending

inventory.

Average Cost Average Cost Inventory Cost Flow AssumptionsInventory Cost Flow AssumptionsAverage Cost Average Cost Inventory Cost Flow AssumptionsInventory Cost Flow Assumptions

Average-Cost

“What’s my

GPA?”

6-12

Average Cost Average Cost Inventory Cost Flow AssumptionsInventory Cost Flow AssumptionsAverage Cost Average Cost Inventory Cost Flow AssumptionsInventory Cost Flow Assumptions

Average-Cost: 550 Sold - 450 in Ending Inventory

450 units were in ending inventory and 550 units were sold.

550 units x $12

6-13

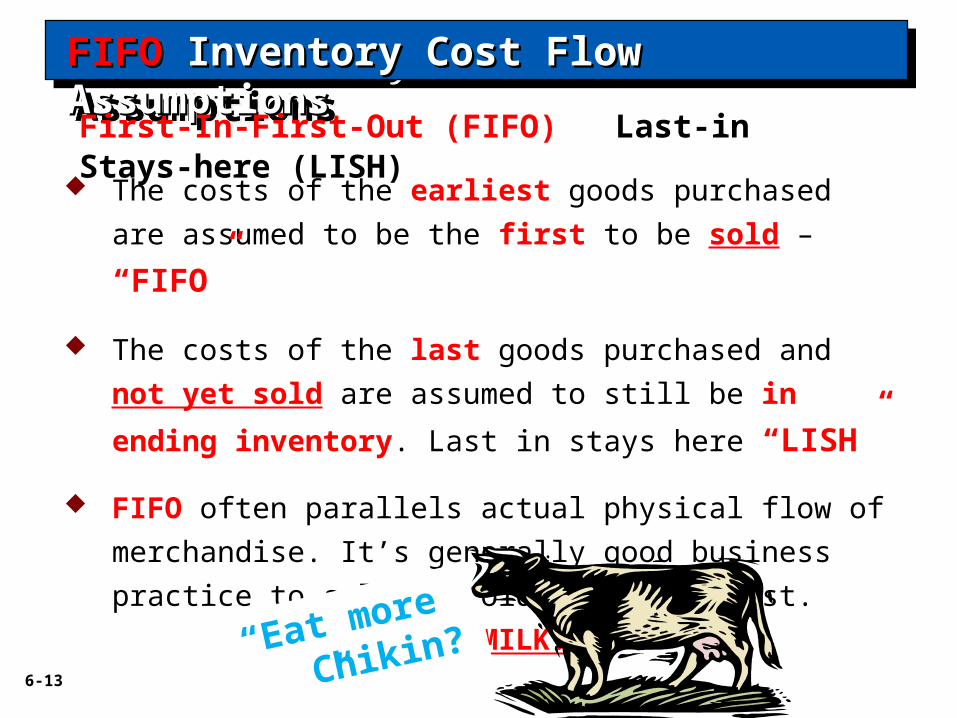

The costs of the earliest goods purchased are assumed to

be the first to be sold – “FIFO”

The costs of the last goods purchased and not yet sold are

assumed to still be in ending inventory. Last in stays here

“LISH”

FIFO often parallels actual physical flow of merchandise. It’s

generally good business practice to sell the oldest units first.

“GOT MILK?”

FIFOFIFO Inventory Cost Flow Assumptions Inventory Cost Flow AssumptionsFIFOFIFO Inventory Cost Flow Assumptions Inventory Cost Flow Assumptions

First-In-First-Out (FIFO) Last-in Stays-here (LISH)

“Eat more

Chikin?

”

6-14

FIFOFIFO Inventory Cost Flow Assumptions Inventory Cost Flow AssumptionsFIFOFIFO Inventory Cost Flow Assumptions Inventory Cost Flow Assumptions

Illustration 6-5

First-In-First-Out (550 Sold) Last In Stays Here (450 in End. Inv.)

Remember 450 units were counted as ending inventory! Another method would be to count the 550 units sold starting with the beginning inventory and working down.

(100 x $10) + (200 x $11) + (250 x $12)

6-15

The costs of the latest goods purchased are assumed to

be the first to be sold – “LIFO”

The costs of the first goods purchased and not yet sold

are assumed to still be in ending inventory. First in stays

here “FISH”

LIFO seldom coincides with actual physical flow of

merchandise. Exceptions include goods stored in piles

such as coal, mulch, hay, etc.

LIFOLIFO Inventory Cost Flow Assumptions Inventory Cost Flow AssumptionsLIFOLIFO Inventory Cost Flow Assumptions Inventory Cost Flow Assumptions

Last-In-First-Out (LIFO) First-In-Stays-Here (FISH)

“Sound

Fishy?”

6-16

LIFOLIFO Inventory Cost Flow Assumptions Inventory Cost Flow AssumptionsLIFOLIFO Inventory Cost Flow Assumptions Inventory Cost Flow Assumptions

Last-In-First-Out (550 Sold) First-In-Stays-Here (450 in End. Inv.)

Remember 450 units were counted as being in ending inventory! Another method would be to count the 550 units sold starting with the last purchase and working up.

(400 x $13) + (150 x $12)

6-17

FIFO* Sales $9,000 $9,000

$9,000

Cost of goods sold 6,200 6,6007,000

Gross profit 2,800 2,4002,000

* Operating expenses 330 330330

Income before taxes 2,470 2,0701,670

Income tax expense 140 120110

Net income $2,330 $1,950 $1,560

Ending Inventory $5,800 $5,400 $5,000

*Assume no differences in Sales or Operating Expenses

LIFOAverage

In Periods of Rising Prices FIFO Has The Highest Ending Inventory!

Financial Statement and Financial Statement and Tax EffectsTax EffectsFinancial Statement and Financial Statement and Tax EffectsTax Effects

6-18

Using Cost Flow Methods Consistently

Inventory CostingInventory CostingInventory CostingInventory Costing

Method should be used consistently because it

enhances comparability from one year to the next.

However, although consistency is preferred, a

company may change its inventory cost method.

6-19

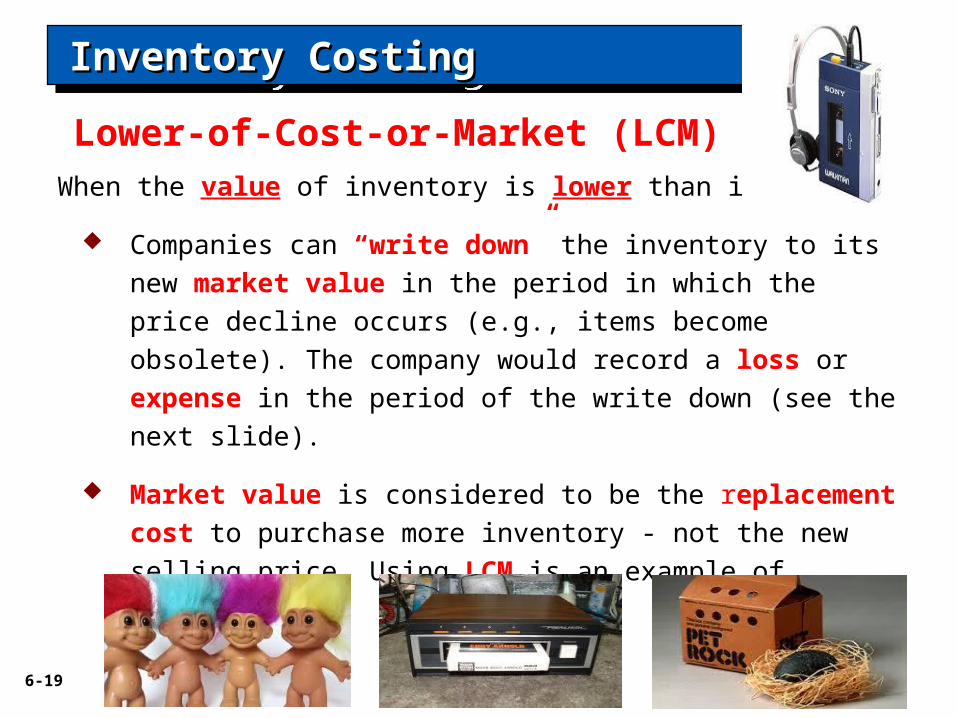

Lower-of-Cost-or-Market (LCM)

Inventory CostingInventory CostingInventory CostingInventory Costing

When the value of inventory is lower than its cost

Companies can “write down” the inventory to its new market

value in the period in which the price decline occurs (e.g., items

become obsolete). The company would record a loss or

expense in the period of the write down (see the next slide).

Market value is considered to be the replacement cost to

purchase more inventory - not the new selling price. Using LCM

is an example of conservatism.

6-20

Inventory CostingInventory CostingInventory CostingInventory Costing

Assume that Ken Tuckie TV has the following lines of

merchandise with costs and market values as indicated.

Lower-of-Cost-or-Market

The original total inventory cost was $168,000. After the adjustment we would write down the value of the inventory to $159,000 by crediting inventory for $9,000 and debiting a Loss on Reduction of Inventory or debiting the COGS as an expense

$168,000 $166,000

6-21

Ownership of the goods passes to the buyer when the

public carrier accepts the goods from the seller.

Ownership of the goods remains with the seller until the goods reach the buyer.

Shipping Terms Shipping Terms ReviewReview!!Shipping Terms Shipping Terms ReviewReview!!

Shipping Point Destination

Goods in transit should be included in the inventory of the company that has legal title to the goods. Legal title is determined by the terms of sale.

6-22

Goods in transit should be included in the inventory of

the buyer when the:

a. public carrier accepts the goods from the seller.

b. goods reach the buyer.

c. terms of sale are FOB destination.

d. terms of sale are FOB shipping point.

Review Question

Determining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory QuantitiesDetermining Inventory Quantities

6-23

The cost flow method that often parallels the actual

physical flow of merchandise is the:

a. FIFO method.

b. LIFO method.

c. average cost method.

d. gross profit method.

Review Question

Inventory Cost Flow AssumptionsInventory Cost Flow AssumptionsInventory Cost Flow AssumptionsInventory Cost Flow Assumptions

6-24

In a period of inflation (rising prices), the cost flow

method that results in the lowest income taxes is the:

a. FIFO method.

b. LIFO method.

c. average cost method.

d. gross profit method.

Inventory Cost Flow AssumptionsInventory Cost Flow AssumptionsInventory Cost Flow AssumptionsInventory Cost Flow Assumptions

Review Question

Top Related